Financial Analysis of a Restaurant: Costs, Funding, and Ratio Report

VerifiedAdded on 2020/07/23

|15

|4183

|33

Report

AI Summary

This report provides a detailed financial analysis of a restaurant business. It begins by discussing various sources of funding, including friends and family, angel investors, bank loans, and retained earnings. The report then explores different methods of income generation, such as offering complementary services, direct mailing, contests, and social media strategies. It outlines the elements of cost, gross profit, and selling prices, categorizing costs into material, labor, and overhead expenses, and distinguishing between fixed and variable costs. The report also examines methods for controlling stock and cash, including the just-in-time approach, economic order quantity (EOQ), balancing, securing cash, and routine reconciliation. Furthermore, the report includes the structure of a trial balance and the preparation of a balance sheet. It outlines the process and purpose of budgetary control, emphasizing its role in planning, cost control, and performance enhancement. The report computes key financial ratios and provides recommendations for improving the restaurant's performance. Finally, it categorizes various costs and presents a marginal costing statement, concluding with a discussion of the significance of break-even analysis. The report offers a comprehensive overview of financial management in the hospitality industry.

FINANCE IN

HOSPITALITY

HOSPITALITY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Discuss sources of funding to business............................................................................1

1.2 Discuss contribution of different methods of income generation....................................2

2.1 Outline elements of cost, gross profit and selling prices for products and services in the

restaurant................................................................................................................................3

2.2 Discuss methods of controlling stock and cash................................................................3

TASK 2 ...........................................................................................................................................4

3.1 Source and structure of trial balance................................................................................4

3.2 Preparation of balance sheet.............................................................................................5

3.3 Outline process and purpose of budgetary control in the businesses...............................6

3.4 Advice for enhancing performance of the business.........................................................7

TASK 3............................................................................................................................................8

4.1 Computation of financial ratios........................................................................................8

4.2 Recommendations to restaurant.......................................................................................9

TASK 4............................................................................................................................................9

5.1 Categorise various costs...................................................................................................9

5.2 Marginal costing statement...............................................................................................9

5.3 Significance of break even analysis...............................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Discuss sources of funding to business............................................................................1

1.2 Discuss contribution of different methods of income generation....................................2

2.1 Outline elements of cost, gross profit and selling prices for products and services in the

restaurant................................................................................................................................3

2.2 Discuss methods of controlling stock and cash................................................................3

TASK 2 ...........................................................................................................................................4

3.1 Source and structure of trial balance................................................................................4

3.2 Preparation of balance sheet.............................................................................................5

3.3 Outline process and purpose of budgetary control in the businesses...............................6

3.4 Advice for enhancing performance of the business.........................................................7

TASK 3............................................................................................................................................8

4.1 Computation of financial ratios........................................................................................8

4.2 Recommendations to restaurant.......................................................................................9

TASK 4............................................................................................................................................9

5.1 Categorise various costs...................................................................................................9

5.2 Marginal costing statement...............................................................................................9

5.3 Significance of break even analysis...............................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Finance is helpful for the business to meet daily needs which are utmost required by it.

The present report deals with hospitality and event planning business which raises source of

finance for the entity. The report also deals with budgetary control process and purpose of using

in the business. The financial ratios are also calculated for the organisation and as such, financial

health is highlighted in the best possible way. Moreover, income generation methods are also

discussed for the revenue generation of the business and various types of costs are also

discussed.

TASK 1

1.1 Discuss sources of funding to business

1. Friends and family -

The sources of finance are numerous and as such, friends and family is one of them. This

is one of the safest form of raising funds as family and friends can trust to the business. The

funds cane be raised from friends by the start up business with much ease. It is the safest form of

finance as they do not make pledge of goods and even may show interest in the business so that

good return may be generated (Jones and et.al, 2016).

2. Angel investors -

Another source of funding is through angel investors. This is another good source in

which the angel investors provide funds to business in return for ownership in it. This means that

certain part of ownership is being provided to business and as such, part of profits are also given

to them with reference to amount of loan provided by them. The part of profits are being shared

with angel investors.

3. Bank loans -

The loan from bank is also another source of raising funds for meeting day to day

requirements of the business so that operational activities are met with much ease. It is required

by the organisation that it should be able to take loans by seeking strength of it as loans are

repaid with interest amount along with the principal amount. As such, debt paying capacity is to

be analysed before taking loans from financial institution (Radojevic, Stanisic and Stanic, 2015).

4. Retained earnings -

1

Finance is helpful for the business to meet daily needs which are utmost required by it.

The present report deals with hospitality and event planning business which raises source of

finance for the entity. The report also deals with budgetary control process and purpose of using

in the business. The financial ratios are also calculated for the organisation and as such, financial

health is highlighted in the best possible way. Moreover, income generation methods are also

discussed for the revenue generation of the business and various types of costs are also

discussed.

TASK 1

1.1 Discuss sources of funding to business

1. Friends and family -

The sources of finance are numerous and as such, friends and family is one of them. This

is one of the safest form of raising funds as family and friends can trust to the business. The

funds cane be raised from friends by the start up business with much ease. It is the safest form of

finance as they do not make pledge of goods and even may show interest in the business so that

good return may be generated (Jones and et.al, 2016).

2. Angel investors -

Another source of funding is through angel investors. This is another good source in

which the angel investors provide funds to business in return for ownership in it. This means that

certain part of ownership is being provided to business and as such, part of profits are also given

to them with reference to amount of loan provided by them. The part of profits are being shared

with angel investors.

3. Bank loans -

The loan from bank is also another source of raising funds for meeting day to day

requirements of the business so that operational activities are met with much ease. It is required

by the organisation that it should be able to take loans by seeking strength of it as loans are

repaid with interest amount along with the principal amount. As such, debt paying capacity is to

be analysed before taking loans from financial institution (Radojevic, Stanisic and Stanic, 2015).

4. Retained earnings -

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is another source of raising funds with much ease. Retained earnings are ulitmate

source as business usually retain some part of profit which is then used for future activities. The

retained earnings are net income of the business which is usually deducted out of dividends paid

to shareholders. It is good source of finance as through this, it can pay out debt in the easiest way

(Lopes, 2016).

1.2 Discuss contribution of different methods of income generation

The business can be flourished with numerous ways which increases income of restaurant

in the best possible way. The restaurant can earn income by giving some part of it to another

person selling ice-cream which might raise income of himself and in turn can help restaurant to

earn that extra income as when customers' come for the purpose of eating ice cream, then they

might have food in the restaurant as well. This raises income and is an effective method for

generating profit.

Another method is through mailing prospective customers' regarding any new food or

offer is quoted by business. This is cost effective method as it involves low cost of direct mailing

to customers and generates huge income. In this way, technology has imparted new way of doing

business. This has great impact on the consumers' and as a result, income is produced by the

restaurant with much ease. Organising certain contests also inject sales and customers are lured

by such promotion technique (Liu and Pennington-Gray, 2015). It is done through by using radio

stations as this helps to build relationship with customers and they participate in such contests

and business is benefited by it.

Social media strategy is also huge source of income generation. As whole world is on the

social media networking websites, business attracts customers by offering certain discounts

related to food and impacts customers a lot, this helps business to generate income with much

ease. Several posts are being updated on the official page of the restaurant and as such, people

are attracted in the best possible way by posting advertisements related to new offers. This

injects sales and ultimately income is generated by implementing such strategy. The above said

methods are helpful for restaurant business as by implementing such strategies, income is

generated in the best possible way (Singal, 2014).

2

source as business usually retain some part of profit which is then used for future activities. The

retained earnings are net income of the business which is usually deducted out of dividends paid

to shareholders. It is good source of finance as through this, it can pay out debt in the easiest way

(Lopes, 2016).

1.2 Discuss contribution of different methods of income generation

The business can be flourished with numerous ways which increases income of restaurant

in the best possible way. The restaurant can earn income by giving some part of it to another

person selling ice-cream which might raise income of himself and in turn can help restaurant to

earn that extra income as when customers' come for the purpose of eating ice cream, then they

might have food in the restaurant as well. This raises income and is an effective method for

generating profit.

Another method is through mailing prospective customers' regarding any new food or

offer is quoted by business. This is cost effective method as it involves low cost of direct mailing

to customers and generates huge income. In this way, technology has imparted new way of doing

business. This has great impact on the consumers' and as a result, income is produced by the

restaurant with much ease. Organising certain contests also inject sales and customers are lured

by such promotion technique (Liu and Pennington-Gray, 2015). It is done through by using radio

stations as this helps to build relationship with customers and they participate in such contests

and business is benefited by it.

Social media strategy is also huge source of income generation. As whole world is on the

social media networking websites, business attracts customers by offering certain discounts

related to food and impacts customers a lot, this helps business to generate income with much

ease. Several posts are being updated on the official page of the restaurant and as such, people

are attracted in the best possible way by posting advertisements related to new offers. This

injects sales and ultimately income is generated by implementing such strategy. The above said

methods are helpful for restaurant business as by implementing such strategies, income is

generated in the best possible way (Singal, 2014).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.1 Outline elements of cost, gross profit and selling prices for products and services in the

restaurant

The elements of cost are divided into three categories such as material, labour and

overhead cost. In a restaurant business, these cost plays important role in determining gross

profit percentages and selling price of foods. The material cost means that cost which remains

part of product in the restaurant. Such as ingredients in flour for making bread is termed as

material cost. This is direct cost as it is identified with making of the product. The basic material

costs are food cost, beverage cost, tobacco cost and Sunday sales cost which is included in the

overall material cost (Fakharyan and et.al, 2014).

Apart from material costs, labour costs are also included to determine selling price of

foods. Wages, salaries and overtime labour expenses are also included. Cleaning supplies,

advertisements to customers' and depreciation are termed as indirect expenses. Moreover,

overheads expenses or costs include marketing costs, administrative costs, occupancy

expenditures, maintenance expenses as well. Therefore, Total cost = Material cost + Labour cost

+ Overhead cost. This is included in selling price of the product as well. Apart from this, fixed

and variable cost are also included in it. Fixed expenditures do not change as output varies as

restaurant has to incur whether it earns profit or not. On the other hand, variable cost completely

differs from fixed costs. Variable cost changes with slight change in outpuit and as a result, costs

are not constant (Wijesinghe, 2014).

The gross profit is calculated by having purchase price and total costs. For instance,

purchase price = 80, Kitchen percentage = 160, then gross profit is 160 - 80 = 80. Now in terms

of gross profit percentage is calculated by Gross profit * 100 / kitchen percentage. Therefore,

gross profit percentage = 80 * 100 / 160 = 50. Here, 50 is gross percentage. If cost is 80 and

gross percentage is 50, then selling price = 130.

2.2 Discuss methods of controlling stock and cash

The methods of controlling stock are as follows :

1. Just in time approach -

This approach is much useful for restaurant as through this, wastage and spoilage of

resources are minimised up to great extent (Stock control and inventory). The inventories are

3

restaurant

The elements of cost are divided into three categories such as material, labour and

overhead cost. In a restaurant business, these cost plays important role in determining gross

profit percentages and selling price of foods. The material cost means that cost which remains

part of product in the restaurant. Such as ingredients in flour for making bread is termed as

material cost. This is direct cost as it is identified with making of the product. The basic material

costs are food cost, beverage cost, tobacco cost and Sunday sales cost which is included in the

overall material cost (Fakharyan and et.al, 2014).

Apart from material costs, labour costs are also included to determine selling price of

foods. Wages, salaries and overtime labour expenses are also included. Cleaning supplies,

advertisements to customers' and depreciation are termed as indirect expenses. Moreover,

overheads expenses or costs include marketing costs, administrative costs, occupancy

expenditures, maintenance expenses as well. Therefore, Total cost = Material cost + Labour cost

+ Overhead cost. This is included in selling price of the product as well. Apart from this, fixed

and variable cost are also included in it. Fixed expenditures do not change as output varies as

restaurant has to incur whether it earns profit or not. On the other hand, variable cost completely

differs from fixed costs. Variable cost changes with slight change in outpuit and as a result, costs

are not constant (Wijesinghe, 2014).

The gross profit is calculated by having purchase price and total costs. For instance,

purchase price = 80, Kitchen percentage = 160, then gross profit is 160 - 80 = 80. Now in terms

of gross profit percentage is calculated by Gross profit * 100 / kitchen percentage. Therefore,

gross profit percentage = 80 * 100 / 160 = 50. Here, 50 is gross percentage. If cost is 80 and

gross percentage is 50, then selling price = 130.

2.2 Discuss methods of controlling stock and cash

The methods of controlling stock are as follows :

1. Just in time approach -

This approach is much useful for restaurant as through this, wastage and spoilage of

resources are minimised up to great extent (Stock control and inventory). The inventories are

3

required to be analysed by restaurant so that products can be made with much ease. This leads to

demand fulfilment of customers and does not lead to unnecessary wastage of valuable stock

(Claveria, Monte and Torra, 2015).

2. Economic Order Quantity (EOQ) -

The EOQ model is worth for any business and that too for restaurant as well. Through

this, holding costs and ordering costs are analysed and a perfect balance is arrived by ordering

not much quantity and not less quantity as well. This is a standard formula and is a cost effective

method as well for ordering quantities of stock. By arriving at EOQ, standard quantities are

ordered by the business and as such, wastage is not found.

The methods of controlling cash are listed below :

1. Balancing -

To control cash, balancing is required of every transaction occurred in the business.

When cash is received, cash receipts are required to be balanced in daily records of sales. Perfect

balancing of cash transaction in the cash register helps restaurant to take record of each and

every cash receipts and even cash withdrawal. This helps restaurant to control cash effectively.

2. Securing cash -

Another method is to keep security by installing cameras in the premises particularly at

the cash point. This helps to secure cash from theft and as such, cash is effectively controlled.

Assigning this job to one employee is required so that unauthorised access to money is not made

and as such, restaurant flourishes in the market quite effectively (Shkurkin and et.al, 2016).

3. Routine reconciliation -

Proper reconciliation helps restaurant to effectively control cash. This provides clarity to

restaurant and no discrepancies are occurred.

TASK 2

3.1 Source and structure of trial balance

The trial balance ensures that there are no arithmetical errors in the ledger posting and as

such, all debits and credits should meet and the process, trial balance meets accuracy is being

attained. The sources of trial balance are purchase ledger, sales and general ledgers. Purchase

4

demand fulfilment of customers and does not lead to unnecessary wastage of valuable stock

(Claveria, Monte and Torra, 2015).

2. Economic Order Quantity (EOQ) -

The EOQ model is worth for any business and that too for restaurant as well. Through

this, holding costs and ordering costs are analysed and a perfect balance is arrived by ordering

not much quantity and not less quantity as well. This is a standard formula and is a cost effective

method as well for ordering quantities of stock. By arriving at EOQ, standard quantities are

ordered by the business and as such, wastage is not found.

The methods of controlling cash are listed below :

1. Balancing -

To control cash, balancing is required of every transaction occurred in the business.

When cash is received, cash receipts are required to be balanced in daily records of sales. Perfect

balancing of cash transaction in the cash register helps restaurant to take record of each and

every cash receipts and even cash withdrawal. This helps restaurant to control cash effectively.

2. Securing cash -

Another method is to keep security by installing cameras in the premises particularly at

the cash point. This helps to secure cash from theft and as such, cash is effectively controlled.

Assigning this job to one employee is required so that unauthorised access to money is not made

and as such, restaurant flourishes in the market quite effectively (Shkurkin and et.al, 2016).

3. Routine reconciliation -

Proper reconciliation helps restaurant to effectively control cash. This provides clarity to

restaurant and no discrepancies are occurred.

TASK 2

3.1 Source and structure of trial balance

The trial balance ensures that there are no arithmetical errors in the ledger posting and as

such, all debits and credits should meet and the process, trial balance meets accuracy is being

attained. The sources of trial balance are purchase ledger, sales and general ledgers. Purchase

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

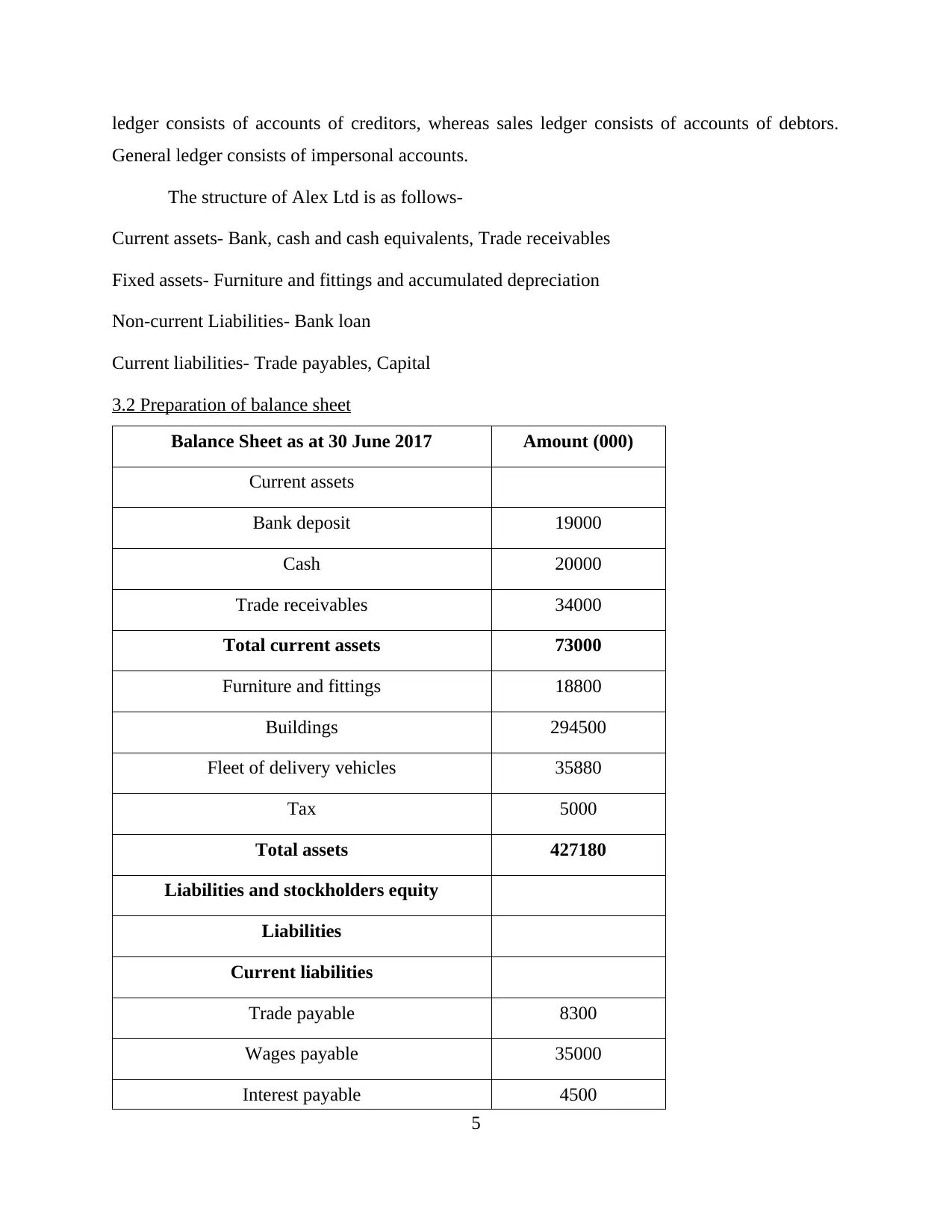

ledger consists of accounts of creditors, whereas sales ledger consists of accounts of debtors.

General ledger consists of impersonal accounts.

The structure of Alex Ltd is as follows-

Current assets- Bank, cash and cash equivalents, Trade receivables

Fixed assets- Furniture and fittings and accumulated depreciation

Non-current Liabilities- Bank loan

Current liabilities- Trade payables, Capital

3.2 Preparation of balance sheet

Balance Sheet as at 30 June 2017 Amount (000)

Current assets

Bank deposit 19000

Cash 20000

Trade receivables 34000

Total current assets 73000

Furniture and fittings 18800

Buildings 294500

Fleet of delivery vehicles 35880

Tax 5000

Total assets 427180

Liabilities and stockholders equity

Liabilities

Current liabilities

Trade payable 8300

Wages payable 35000

Interest payable 4500

5

General ledger consists of impersonal accounts.

The structure of Alex Ltd is as follows-

Current assets- Bank, cash and cash equivalents, Trade receivables

Fixed assets- Furniture and fittings and accumulated depreciation

Non-current Liabilities- Bank loan

Current liabilities- Trade payables, Capital

3.2 Preparation of balance sheet

Balance Sheet as at 30 June 2017 Amount (000)

Current assets

Bank deposit 19000

Cash 20000

Trade receivables 34000

Total current assets 73000

Furniture and fittings 18800

Buildings 294500

Fleet of delivery vehicles 35880

Tax 5000

Total assets 427180

Liabilities and stockholders equity

Liabilities

Current liabilities

Trade payable 8300

Wages payable 35000

Interest payable 4500

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

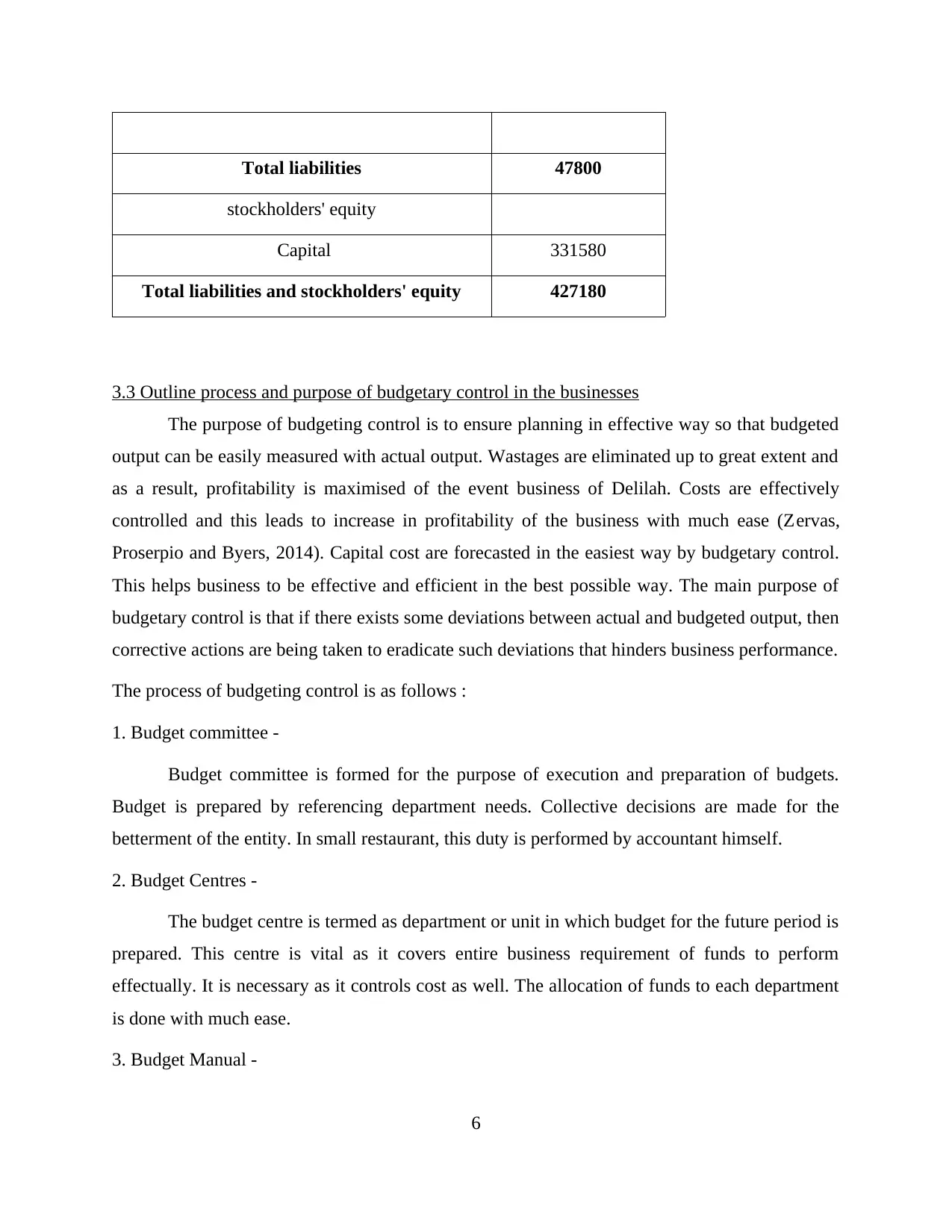

Total liabilities 47800

stockholders' equity

Capital 331580

Total liabilities and stockholders' equity 427180

3.3 Outline process and purpose of budgetary control in the businesses

The purpose of budgeting control is to ensure planning in effective way so that budgeted

output can be easily measured with actual output. Wastages are eliminated up to great extent and

as a result, profitability is maximised of the event business of Delilah. Costs are effectively

controlled and this leads to increase in profitability of the business with much ease (Zervas,

Proserpio and Byers, 2014). Capital cost are forecasted in the easiest way by budgetary control.

This helps business to be effective and efficient in the best possible way. The main purpose of

budgetary control is that if there exists some deviations between actual and budgeted output, then

corrective actions are being taken to eradicate such deviations that hinders business performance.

The process of budgeting control is as follows :

1. Budget committee -

Budget committee is formed for the purpose of execution and preparation of budgets.

Budget is prepared by referencing department needs. Collective decisions are made for the

betterment of the entity. In small restaurant, this duty is performed by accountant himself.

2. Budget Centres -

The budget centre is termed as department or unit in which budget for the future period is

prepared. This centre is vital as it covers entire business requirement of funds to perform

effectually. It is necessary as it controls cost as well. The allocation of funds to each department

is done with much ease.

3. Budget Manual -

6

stockholders' equity

Capital 331580

Total liabilities and stockholders' equity 427180

3.3 Outline process and purpose of budgetary control in the businesses

The purpose of budgeting control is to ensure planning in effective way so that budgeted

output can be easily measured with actual output. Wastages are eliminated up to great extent and

as a result, profitability is maximised of the event business of Delilah. Costs are effectively

controlled and this leads to increase in profitability of the business with much ease (Zervas,

Proserpio and Byers, 2014). Capital cost are forecasted in the easiest way by budgetary control.

This helps business to be effective and efficient in the best possible way. The main purpose of

budgetary control is that if there exists some deviations between actual and budgeted output, then

corrective actions are being taken to eradicate such deviations that hinders business performance.

The process of budgeting control is as follows :

1. Budget committee -

Budget committee is formed for the purpose of execution and preparation of budgets.

Budget is prepared by referencing department needs. Collective decisions are made for the

betterment of the entity. In small restaurant, this duty is performed by accountant himself.

2. Budget Centres -

The budget centre is termed as department or unit in which budget for the future period is

prepared. This centre is vital as it covers entire business requirement of funds to perform

effectually. It is necessary as it controls cost as well. The allocation of funds to each department

is done with much ease.

3. Budget Manual -

6

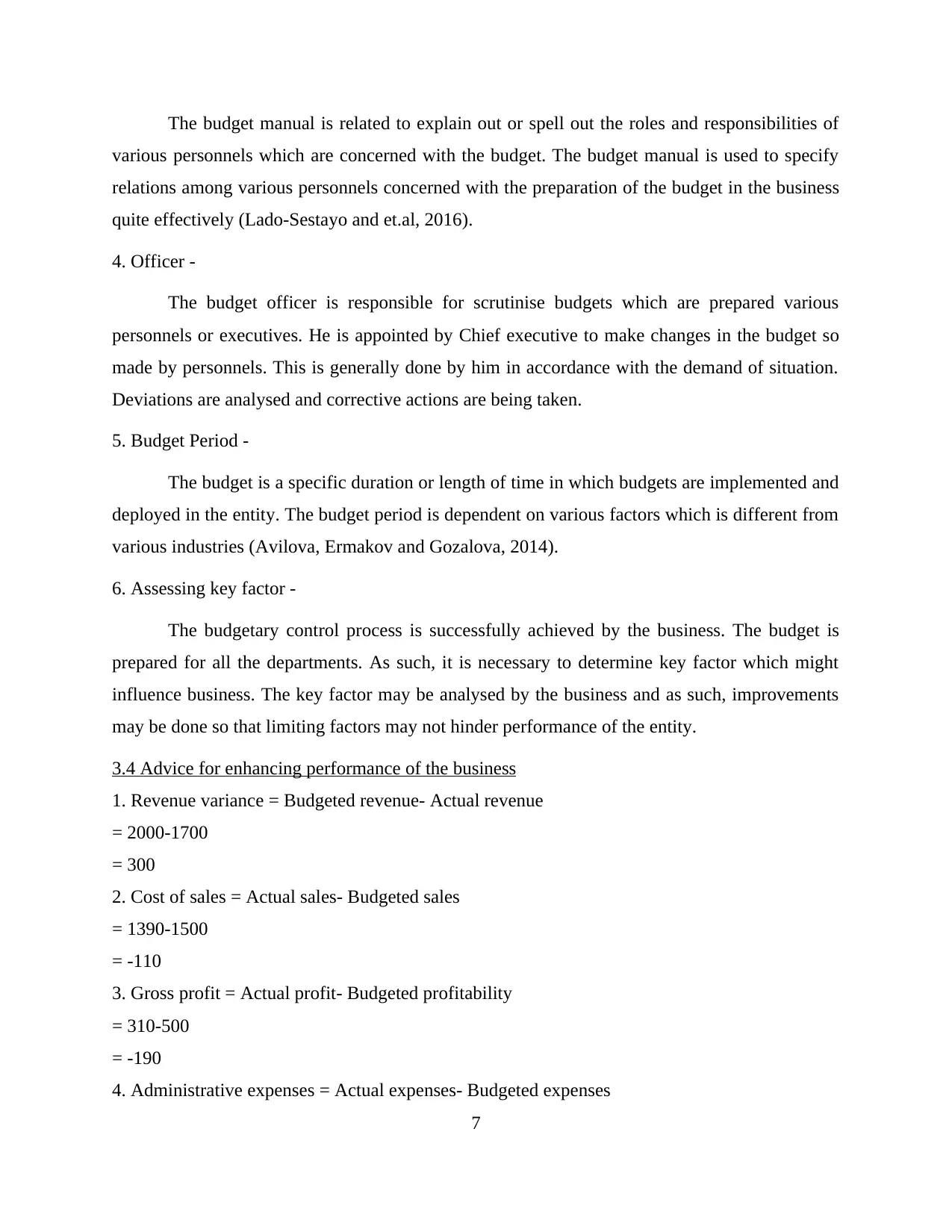

The budget manual is related to explain out or spell out the roles and responsibilities of

various personnels which are concerned with the budget. The budget manual is used to specify

relations among various personnels concerned with the preparation of the budget in the business

quite effectively (Lado-Sestayo and et.al, 2016).

4. Officer -

The budget officer is responsible for scrutinise budgets which are prepared various

personnels or executives. He is appointed by Chief executive to make changes in the budget so

made by personnels. This is generally done by him in accordance with the demand of situation.

Deviations are analysed and corrective actions are being taken.

5. Budget Period -

The budget is a specific duration or length of time in which budgets are implemented and

deployed in the entity. The budget period is dependent on various factors which is different from

various industries (Avilova, Ermakov and Gozalova, 2014).

6. Assessing key factor -

The budgetary control process is successfully achieved by the business. The budget is

prepared for all the departments. As such, it is necessary to determine key factor which might

influence business. The key factor may be analysed by the business and as such, improvements

may be done so that limiting factors may not hinder performance of the entity.

3.4 Advice for enhancing performance of the business

1. Revenue variance = Budgeted revenue- Actual revenue

= 2000-1700

= 300

2. Cost of sales = Actual sales- Budgeted sales

= 1390-1500

= -110

3. Gross profit = Actual profit- Budgeted profitability

= 310-500

= -190

4. Administrative expenses = Actual expenses- Budgeted expenses

7

various personnels which are concerned with the budget. The budget manual is used to specify

relations among various personnels concerned with the preparation of the budget in the business

quite effectively (Lado-Sestayo and et.al, 2016).

4. Officer -

The budget officer is responsible for scrutinise budgets which are prepared various

personnels or executives. He is appointed by Chief executive to make changes in the budget so

made by personnels. This is generally done by him in accordance with the demand of situation.

Deviations are analysed and corrective actions are being taken.

5. Budget Period -

The budget is a specific duration or length of time in which budgets are implemented and

deployed in the entity. The budget period is dependent on various factors which is different from

various industries (Avilova, Ermakov and Gozalova, 2014).

6. Assessing key factor -

The budgetary control process is successfully achieved by the business. The budget is

prepared for all the departments. As such, it is necessary to determine key factor which might

influence business. The key factor may be analysed by the business and as such, improvements

may be done so that limiting factors may not hinder performance of the entity.

3.4 Advice for enhancing performance of the business

1. Revenue variance = Budgeted revenue- Actual revenue

= 2000-1700

= 300

2. Cost of sales = Actual sales- Budgeted sales

= 1390-1500

= -110

3. Gross profit = Actual profit- Budgeted profitability

= 310-500

= -190

4. Administrative expenses = Actual expenses- Budgeted expenses

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 210-200

= 10

5. Distribution expenses = Actual expenses- Budgeted expenses

= 90-150

= -60

From the analysis of variances calculated above, it can be advised to management to take

strict action so that expenditures may be controlled as distribution expenses are in negative. As

such, revenue is also deteriorated as budgeted revenue is less than actual revenue by 300 which

is unfavourable. Management need to control cost to exceed revenue.

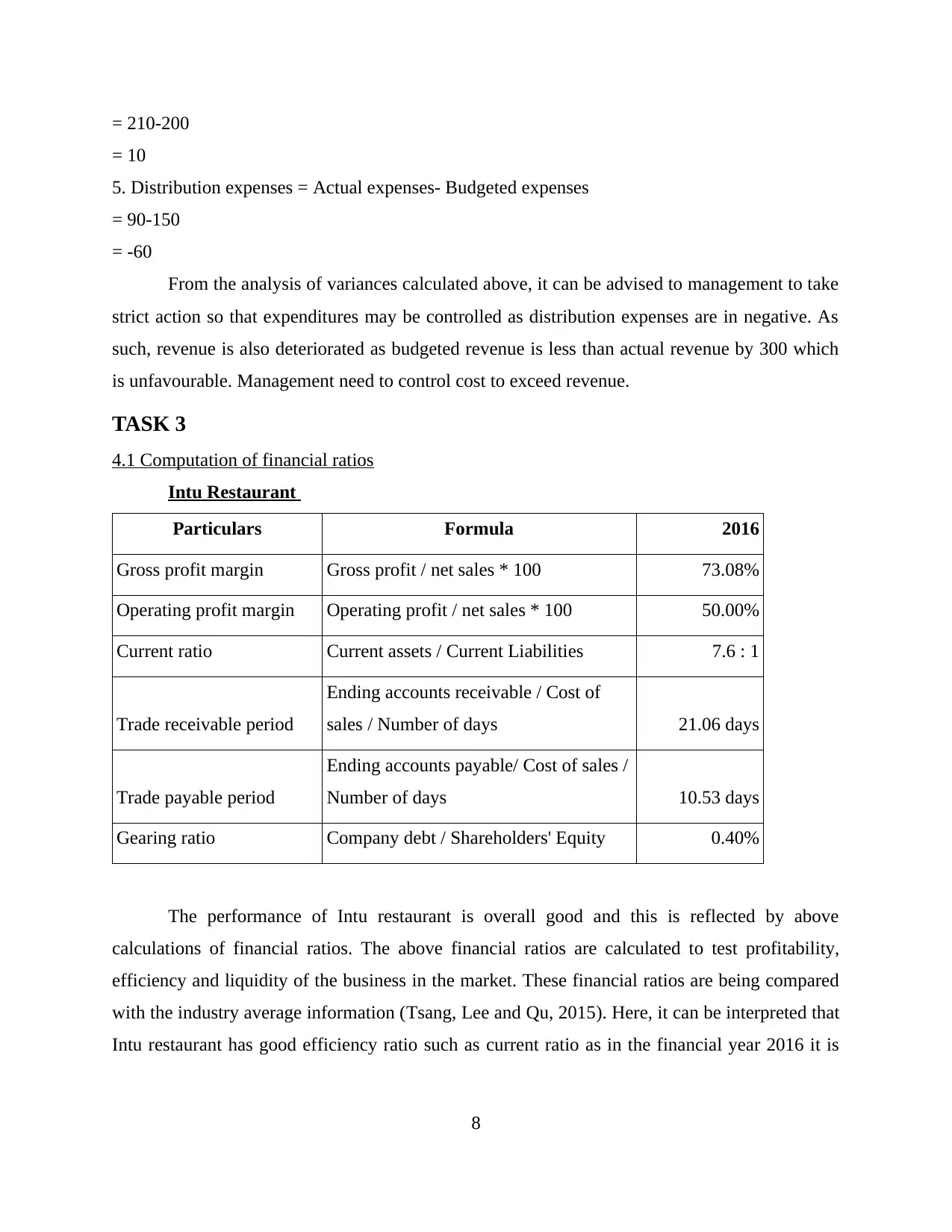

TASK 3

4.1 Computation of financial ratios

Intu Restaurant

Particulars Formula 2016

Gross profit margin Gross profit / net sales * 100 73.08%

Operating profit margin Operating profit / net sales * 100 50.00%

Current ratio Current assets / Current Liabilities 7.6 : 1

Trade receivable period

Ending accounts receivable / Cost of

sales / Number of days 21.06 days

Trade payable period

Ending accounts payable/ Cost of sales /

Number of days 10.53 days

Gearing ratio Company debt / Shareholders' Equity 0.40%

The performance of Intu restaurant is overall good and this is reflected by above

calculations of financial ratios. The above financial ratios are calculated to test profitability,

efficiency and liquidity of the business in the market. These financial ratios are being compared

with the industry average information (Tsang, Lee and Qu, 2015). Here, it can be interpreted that

Intu restaurant has good efficiency ratio such as current ratio as in the financial year 2016 it is

8

= 10

5. Distribution expenses = Actual expenses- Budgeted expenses

= 90-150

= -60

From the analysis of variances calculated above, it can be advised to management to take

strict action so that expenditures may be controlled as distribution expenses are in negative. As

such, revenue is also deteriorated as budgeted revenue is less than actual revenue by 300 which

is unfavourable. Management need to control cost to exceed revenue.

TASK 3

4.1 Computation of financial ratios

Intu Restaurant

Particulars Formula 2016

Gross profit margin Gross profit / net sales * 100 73.08%

Operating profit margin Operating profit / net sales * 100 50.00%

Current ratio Current assets / Current Liabilities 7.6 : 1

Trade receivable period

Ending accounts receivable / Cost of

sales / Number of days 21.06 days

Trade payable period

Ending accounts payable/ Cost of sales /

Number of days 10.53 days

Gearing ratio Company debt / Shareholders' Equity 0.40%

The performance of Intu restaurant is overall good and this is reflected by above

calculations of financial ratios. The above financial ratios are calculated to test profitability,

efficiency and liquidity of the business in the market. These financial ratios are being compared

with the industry average information (Tsang, Lee and Qu, 2015). Here, it can be interpreted that

Intu restaurant has good efficiency ratio such as current ratio as in the financial year 2016 it is

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7.6 which shows that it will be able to meet short-term liabilities of creditors with much ease. As

it much more than ideal ratio.

Furthermore, gross profit margin is 73. 08 % and operating profit margin is 50 % which

implies that it has strong profitability position as it is able to control the expenditures effectively.

This shows that it controls cost effectively which has led to increase in profits. Trade receivable

period is around 21.06 days which is not bad as it is able to receive cash from credit sales made

to customers. Trade payable period is less as it is 10.53 days which shows Intu restaurant is able

to meet payments of suppliers in the easiest way (Peters and Kallmuenzer, 2018). Gearing ratio

is not good as it is more as compared to average industry information. This means that restaurant

is using much debt than equity which resulted into more gearing ratio. Lower gearing ratio is

considered to be ideal.

4.2 Recommendations to restaurant

Hereby it can be recommended to the restaurant to improve upon gearing ratio as it is not

good in respect of the average information given of the restaurant industry. It is recommended

that Intu restaurant should use perfect blend or adequate mix of debt and equity so that lower

gearing ratio may be attained by it easily. As higher gearing ratio indicates that entity is using

more of debt than equity. It should not be used more than it raises debt obligations to restaurant

and profits may come down (Papaioannou and et.al, 2018).

Moreover, it should be able to control cost effectively and this will provide with more

profits in hand. By controlling expenditures, profitability position of the business may be

enhanced in a better way. It is recommended that it should also enhance efficiency ratios so that

short-term liabilities can be paid off with much ease. By implementing necessary strategies, it

may flourish in the market in the best possible way. To implement well-structured strategies such

as using social media strategy and necessary actions will provide restaurant with huge profits and

as such, it will be able to have strong financial position effectually (Kallmuenzer and Peters,

2018).

TASK 4

5.1 Categorise various costs

Fixed costs- These do not change with the output. It includes rent of the hall-45000.

9

it much more than ideal ratio.

Furthermore, gross profit margin is 73. 08 % and operating profit margin is 50 % which

implies that it has strong profitability position as it is able to control the expenditures effectively.

This shows that it controls cost effectively which has led to increase in profits. Trade receivable

period is around 21.06 days which is not bad as it is able to receive cash from credit sales made

to customers. Trade payable period is less as it is 10.53 days which shows Intu restaurant is able

to meet payments of suppliers in the easiest way (Peters and Kallmuenzer, 2018). Gearing ratio

is not good as it is more as compared to average industry information. This means that restaurant

is using much debt than equity which resulted into more gearing ratio. Lower gearing ratio is

considered to be ideal.

4.2 Recommendations to restaurant

Hereby it can be recommended to the restaurant to improve upon gearing ratio as it is not

good in respect of the average information given of the restaurant industry. It is recommended

that Intu restaurant should use perfect blend or adequate mix of debt and equity so that lower

gearing ratio may be attained by it easily. As higher gearing ratio indicates that entity is using

more of debt than equity. It should not be used more than it raises debt obligations to restaurant

and profits may come down (Papaioannou and et.al, 2018).

Moreover, it should be able to control cost effectively and this will provide with more

profits in hand. By controlling expenditures, profitability position of the business may be

enhanced in a better way. It is recommended that it should also enhance efficiency ratios so that

short-term liabilities can be paid off with much ease. By implementing necessary strategies, it

may flourish in the market in the best possible way. To implement well-structured strategies such

as using social media strategy and necessary actions will provide restaurant with huge profits and

as such, it will be able to have strong financial position effectually (Kallmuenzer and Peters,

2018).

TASK 4

5.1 Categorise various costs

Fixed costs- These do not change with the output. It includes rent of the hall-45000.

9

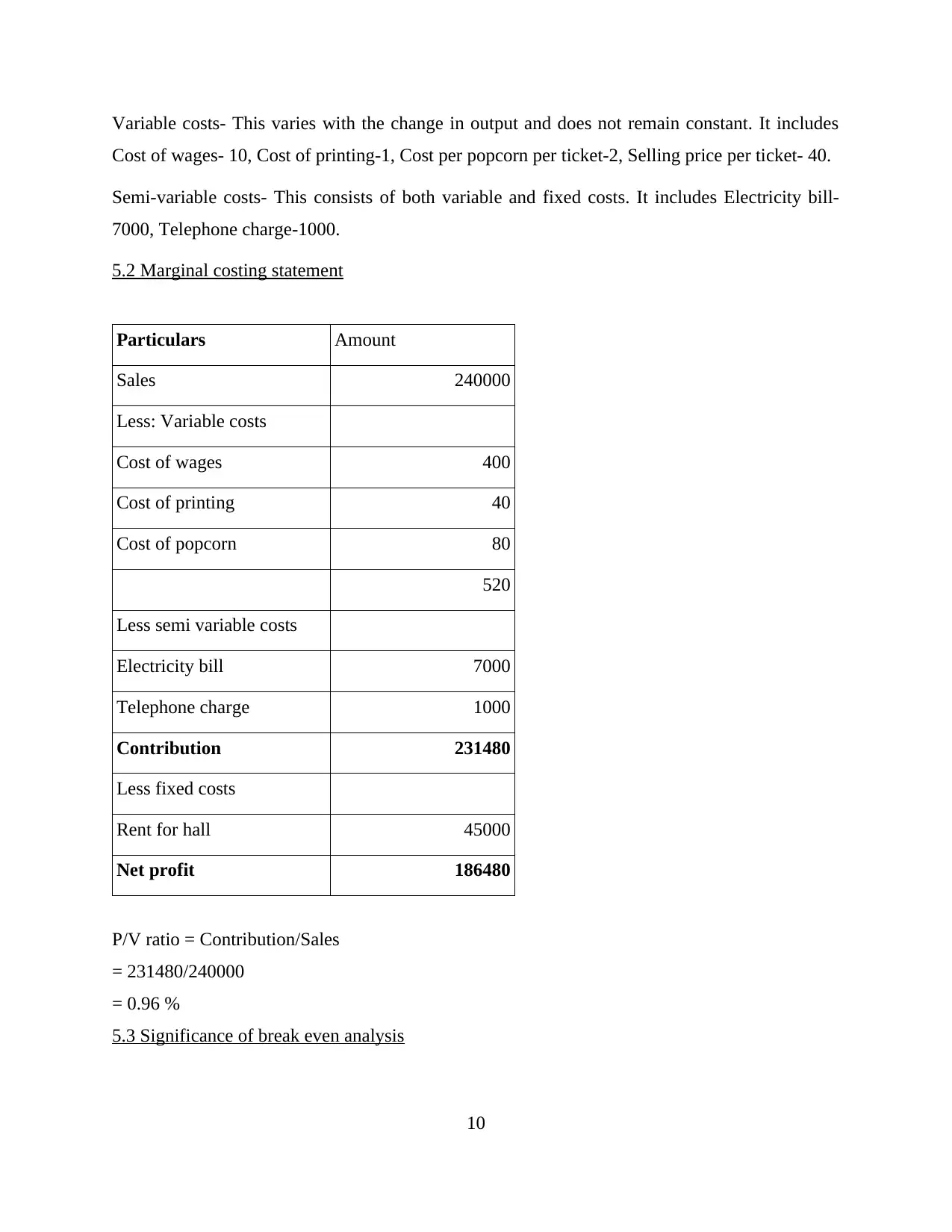

Variable costs- This varies with the change in output and does not remain constant. It includes

Cost of wages- 10, Cost of printing-1, Cost per popcorn per ticket-2, Selling price per ticket- 40.

Semi-variable costs- This consists of both variable and fixed costs. It includes Electricity bill-

7000, Telephone charge-1000.

5.2 Marginal costing statement

Particulars Amount

Sales 240000

Less: Variable costs

Cost of wages 400

Cost of printing 40

Cost of popcorn 80

520

Less semi variable costs

Electricity bill 7000

Telephone charge 1000

Contribution 231480

Less fixed costs

Rent for hall 45000

Net profit 186480

P/V ratio = Contribution/Sales

= 231480/240000

= 0.96 %

5.3 Significance of break even analysis

10

Cost of wages- 10, Cost of printing-1, Cost per popcorn per ticket-2, Selling price per ticket- 40.

Semi-variable costs- This consists of both variable and fixed costs. It includes Electricity bill-

7000, Telephone charge-1000.

5.2 Marginal costing statement

Particulars Amount

Sales 240000

Less: Variable costs

Cost of wages 400

Cost of printing 40

Cost of popcorn 80

520

Less semi variable costs

Electricity bill 7000

Telephone charge 1000

Contribution 231480

Less fixed costs

Rent for hall 45000

Net profit 186480

P/V ratio = Contribution/Sales

= 231480/240000

= 0.96 %

5.3 Significance of break even analysis

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.