Hospitality Accounting and Finance: Performance Evaluation Report

VerifiedAdded on 2022/08/31

|7

|1532

|17

Report

AI Summary

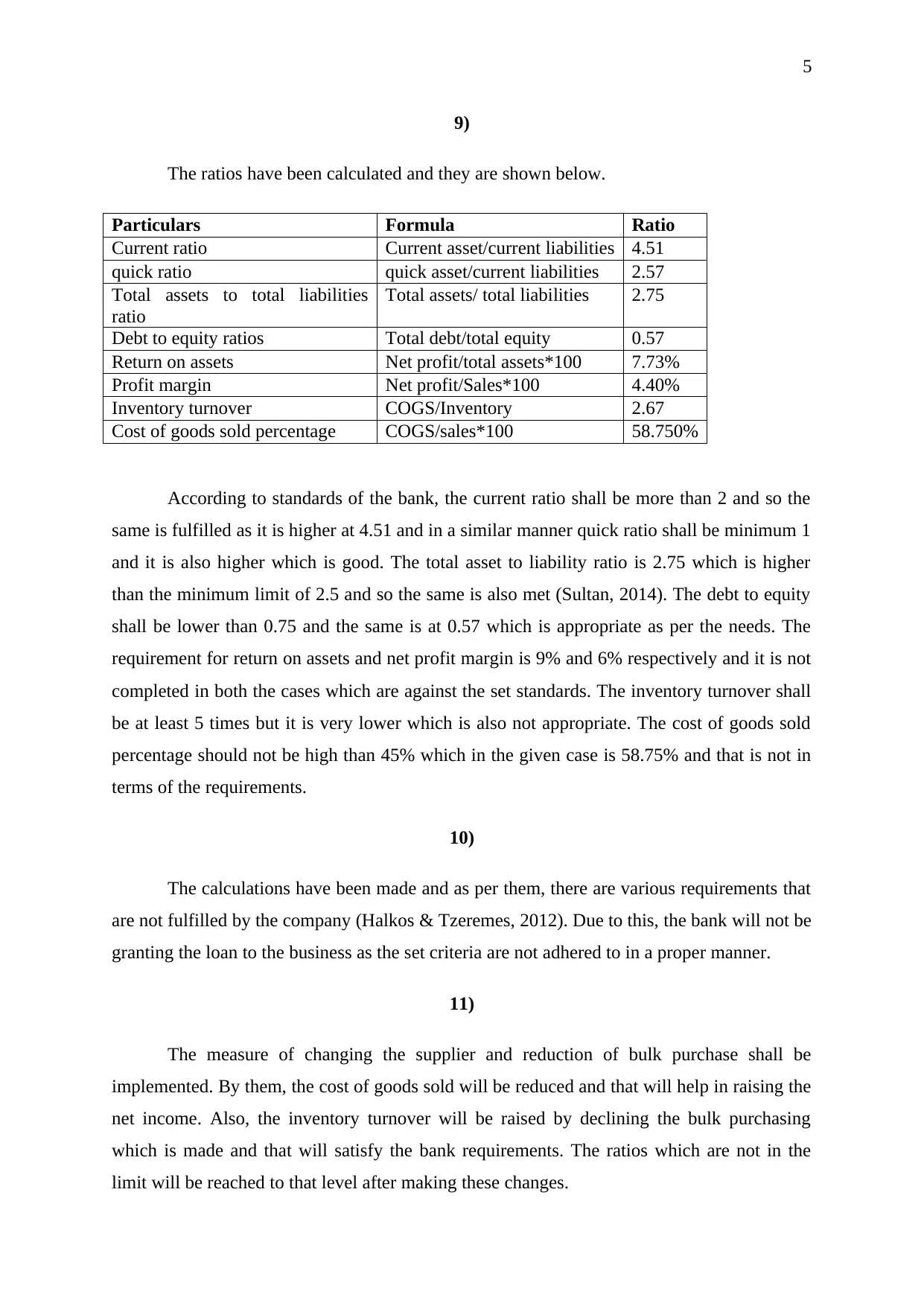

This report provides a financial analysis of a hospitality business, examining its income statement, balance sheet, and key financial ratios. It assesses the company's profitability, liquidity, and solvency, highlighting concerns about declining net income and cash position. The analysis includes ratio calculations and comparisons to industry standards, revealing areas where the company falls short. The report evaluates the impact of potential strategies, such as changing suppliers, modifying collection policies, and altering dividend policies, to improve financial performance. It also discusses the implications of a loan application and suggests improvements to meet bank requirements. The report emphasizes the importance of operational efficiency, customer satisfaction, and strategic financial planning for long-term success in the hospitality sector.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.