Financial Analysis and Management in the Hospitality Industry Report

VerifiedAdded on 2019/12/03

|17

|4732

|49

Report

AI Summary

This report provides a comprehensive analysis of financial management within the hospitality industry. It begins by examining the calculation of recipe costs, cost per portion, and the determination of selling prices to achieve an 85% gross profit margin. The report then delves into calculating the required quantities of ingredients for a specified number of portions and explores suitable methods for a restaurant to effectively control its stock levels, including supplier assistance, inventory control personnel, lead time management, and tracking systems. Furthermore, the report presents an adjusted profit and loss account and balance sheet for a hypothetical company, Morrison, followed by calculations related to a package deal, including total cost, cost per customer, and selling price based on a markup. The report also covers break-even analysis and profit calculations under different scenarios, along with a percentage breakdown of each category, variance analysis of profit, and suggestions for improving profit and reducing variance. The report concludes with a summary of the key findings and recommendations for effective financial management within the hospitality sector.

FINANCE IN HOSPITALITY

INDUSTRY

INDUSTRY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART 2 Assignment........................................................................................................................1

TASK A...........................................................................................................................................1

1. Calculation of recipe cost........................................................................................................1

2. Calculation of cost per portion.................................................................................................2

3. Calculation of selling price per portion to produce 85% gross profit......................................2

4. Calculation of quantity required for 70 portions.....................................................................2

5. Suitable ways for restaurant to control its stock......................................................................4

TASK B...........................................................................................................................................5

Adjusted profit and loss a/c and balance sheet of Morrison........................................................6

1. Total cost for this package deal and calculation of cost per customer..................................10

2. Selling price per seat if mark up is to be 35%.......................................................................11

3. Cost per customer if break even sales point is set 36 customers...........................................11

4. Profit for the package of 48 customers with breakeven point at 36 customers and profit

mark up is 35%..........................................................................................................................12

5. Percentage of each category..................................................................................................12

6.................................................................................................................................................12

A) Variance of profit..................................................................................................................12

B) Suggestions for the company to improve profit and reduce the variance.............................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

2

INTRODUCTION...........................................................................................................................1

PART 2 Assignment........................................................................................................................1

TASK A...........................................................................................................................................1

1. Calculation of recipe cost........................................................................................................1

2. Calculation of cost per portion.................................................................................................2

3. Calculation of selling price per portion to produce 85% gross profit......................................2

4. Calculation of quantity required for 70 portions.....................................................................2

5. Suitable ways for restaurant to control its stock......................................................................4

TASK B...........................................................................................................................................5

Adjusted profit and loss a/c and balance sheet of Morrison........................................................6

1. Total cost for this package deal and calculation of cost per customer..................................10

2. Selling price per seat if mark up is to be 35%.......................................................................11

3. Cost per customer if break even sales point is set 36 customers...........................................11

4. Profit for the package of 48 customers with breakeven point at 36 customers and profit

mark up is 35%..........................................................................................................................12

5. Percentage of each category..................................................................................................12

6.................................................................................................................................................12

A) Variance of profit..................................................................................................................12

B) Suggestions for the company to improve profit and reduce the variance.............................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

2

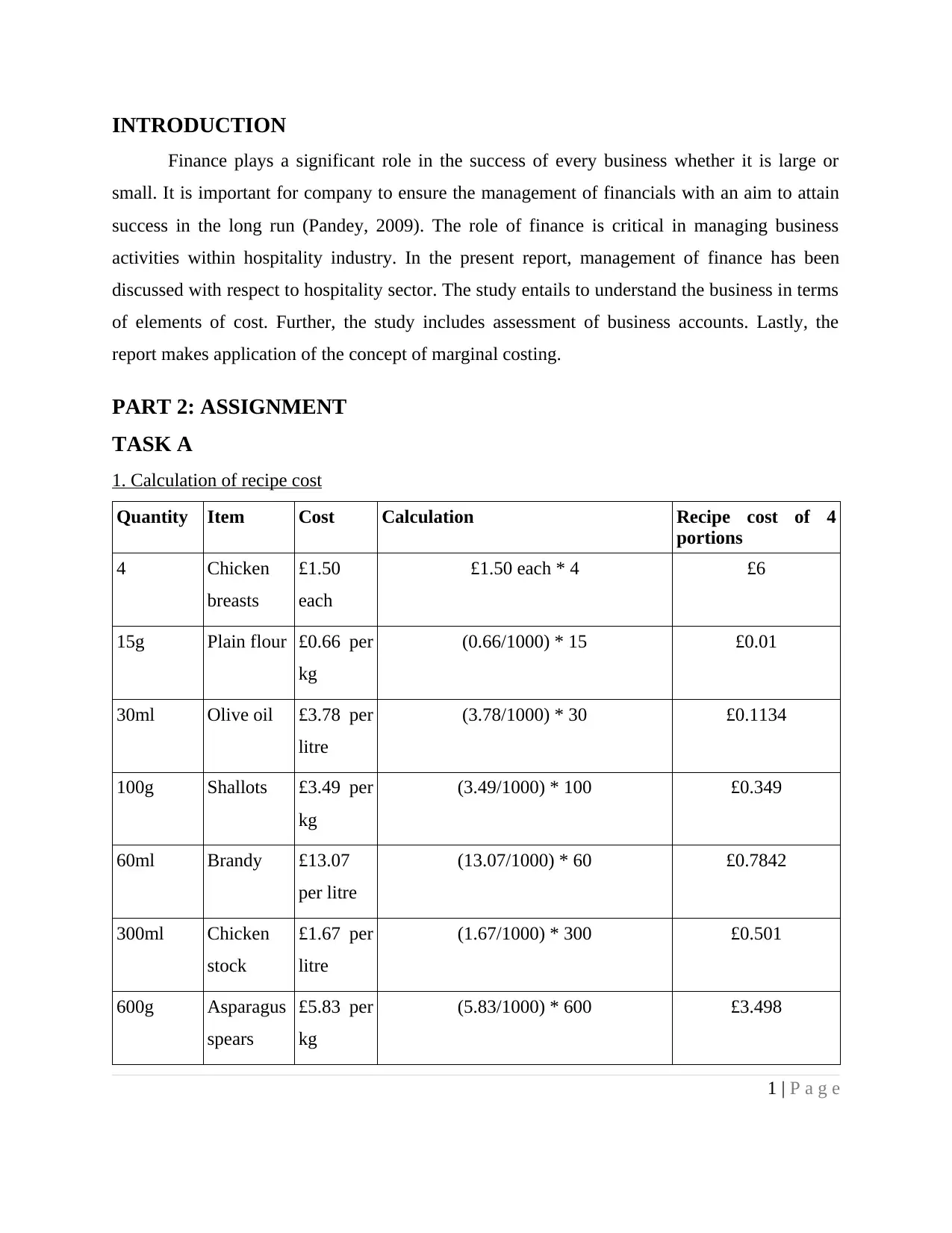

INTRODUCTION

Finance plays a significant role in the success of every business whether it is large or

small. It is important for company to ensure the management of financials with an aim to attain

success in the long run (Pandey, 2009). The role of finance is critical in managing business

activities within hospitality industry. In the present report, management of finance has been

discussed with respect to hospitality sector. The study entails to understand the business in terms

of elements of cost. Further, the study includes assessment of business accounts. Lastly, the

report makes application of the concept of marginal costing.

PART 2: ASSIGNMENT

TASK A

1. Calculation of recipe cost

Quantity Item Cost Calculation Recipe cost of 4

portions

4 Chicken

breasts

£1.50

each

£1.50 each * 4 £6

15g Plain flour £0.66 per

kg

(0.66/1000) * 15 £0.01

30ml Olive oil £3.78 per

litre

(3.78/1000) * 30 £0.1134

100g Shallots £3.49 per

kg

(3.49/1000) * 100 £0.349

60ml Brandy £13.07

per litre

(13.07/1000) * 60 £0.7842

300ml Chicken

stock

£1.67 per

litre

(1.67/1000) * 300 £0.501

600g Asparagus

spears

£5.83 per

kg

(5.83/1000) * 600 £3.498

1 | P a g e

Finance plays a significant role in the success of every business whether it is large or

small. It is important for company to ensure the management of financials with an aim to attain

success in the long run (Pandey, 2009). The role of finance is critical in managing business

activities within hospitality industry. In the present report, management of finance has been

discussed with respect to hospitality sector. The study entails to understand the business in terms

of elements of cost. Further, the study includes assessment of business accounts. Lastly, the

report makes application of the concept of marginal costing.

PART 2: ASSIGNMENT

TASK A

1. Calculation of recipe cost

Quantity Item Cost Calculation Recipe cost of 4

portions

4 Chicken

breasts

£1.50

each

£1.50 each * 4 £6

15g Plain flour £0.66 per

kg

(0.66/1000) * 15 £0.01

30ml Olive oil £3.78 per

litre

(3.78/1000) * 30 £0.1134

100g Shallots £3.49 per

kg

(3.49/1000) * 100 £0.349

60ml Brandy £13.07

per litre

(13.07/1000) * 60 £0.7842

300ml Chicken

stock

£1.67 per

litre

(1.67/1000) * 300 £0.501

600g Asparagus

spears

£5.83 per

kg

(5.83/1000) * 600 £3.498

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

50ml Crème

fraiche

£3.60 per

litre

(3.60/1000) * 50 £0.18

Total Recipe cost of

4 portion = £11.43

2. Calculation of cost per portion

The total recipe cost of 4 portions is £11.43.

Thus the cost per portion would be:

£11.43/ 4 = £2.85

3. Calculation of selling price per portion to produce 85% gross profit

Cost per portion = £2.85

In order to calculate selling price, the formula would be:

Selling price = Cost price+ (Cost Price* Profit %)

= £2.85+ (£2.85 * 85%)

=£2.85+ £2.42 = £5.27

4. Calculation of quantity required for 70 portions

Quantity Item Calculation

Quantity required

for 70 portions

4 Chicken breasts (4/4) * 70 70

15g Plain flour (15g/4) * 70 262.5g

30ml Olive oil (30ml/4)* 70 525ml

100g Shallots (100g/4)* 70 1750g

60ml Brandy (60ml/4)* 70 1050ml

300ml Chicken stock (300ml/4)* 70 5250ml

600g

Asparagus

spears (600g/4)* 70 10500g

50ml Crème fraiche (50ml/4)* 70 875ml

2

fraiche

£3.60 per

litre

(3.60/1000) * 50 £0.18

Total Recipe cost of

4 portion = £11.43

2. Calculation of cost per portion

The total recipe cost of 4 portions is £11.43.

Thus the cost per portion would be:

£11.43/ 4 = £2.85

3. Calculation of selling price per portion to produce 85% gross profit

Cost per portion = £2.85

In order to calculate selling price, the formula would be:

Selling price = Cost price+ (Cost Price* Profit %)

= £2.85+ (£2.85 * 85%)

=£2.85+ £2.42 = £5.27

4. Calculation of quantity required for 70 portions

Quantity Item Calculation

Quantity required

for 70 portions

4 Chicken breasts (4/4) * 70 70

15g Plain flour (15g/4) * 70 262.5g

30ml Olive oil (30ml/4)* 70 525ml

100g Shallots (100g/4)* 70 1750g

60ml Brandy (60ml/4)* 70 1050ml

300ml Chicken stock (300ml/4)* 70 5250ml

600g

Asparagus

spears (600g/4)* 70 10500g

50ml Crème fraiche (50ml/4)* 70 875ml

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

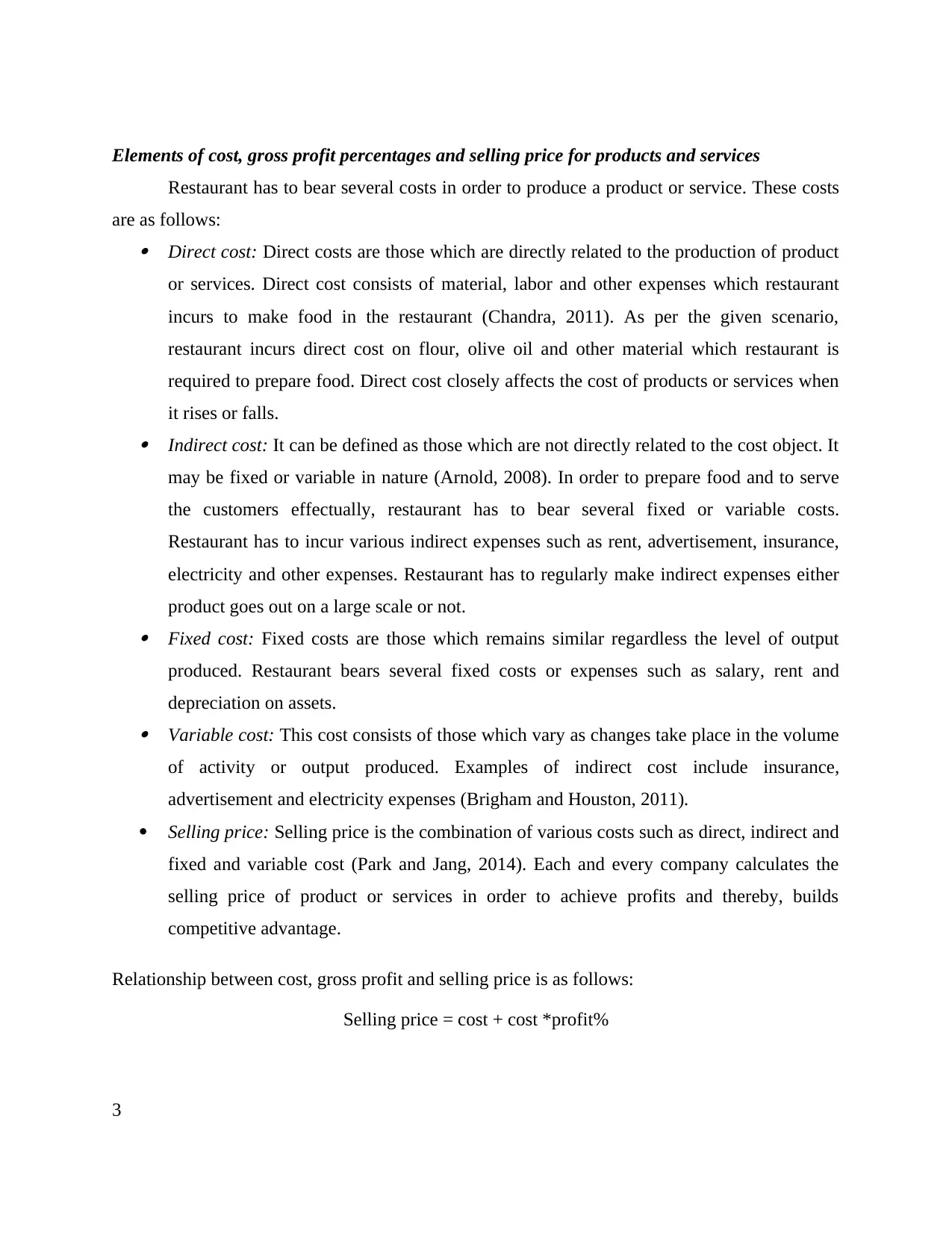

Elements of cost, gross profit percentages and selling price for products and services

Restaurant has to bear several costs in order to produce a product or service. These costs

are as follows: Direct cost: Direct costs are those which are directly related to the production of product

or services. Direct cost consists of material, labor and other expenses which restaurant

incurs to make food in the restaurant (Chandra, 2011). As per the given scenario,

restaurant incurs direct cost on flour, olive oil and other material which restaurant is

required to prepare food. Direct cost closely affects the cost of products or services when

it rises or falls. Indirect cost: It can be defined as those which are not directly related to the cost object. It

may be fixed or variable in nature (Arnold, 2008). In order to prepare food and to serve

the customers effectually, restaurant has to bear several fixed or variable costs.

Restaurant has to incur various indirect expenses such as rent, advertisement, insurance,

electricity and other expenses. Restaurant has to regularly make indirect expenses either

product goes out on a large scale or not. Fixed cost: Fixed costs are those which remains similar regardless the level of output

produced. Restaurant bears several fixed costs or expenses such as salary, rent and

depreciation on assets. Variable cost: This cost consists of those which vary as changes take place in the volume

of activity or output produced. Examples of indirect cost include insurance,

advertisement and electricity expenses (Brigham and Houston, 2011).

Selling price: Selling price is the combination of various costs such as direct, indirect and

fixed and variable cost (Park and Jang, 2014). Each and every company calculates the

selling price of product or services in order to achieve profits and thereby, builds

competitive advantage.

Relationship between cost, gross profit and selling price is as follows:

Selling price = cost + cost *profit%

3

Restaurant has to bear several costs in order to produce a product or service. These costs

are as follows: Direct cost: Direct costs are those which are directly related to the production of product

or services. Direct cost consists of material, labor and other expenses which restaurant

incurs to make food in the restaurant (Chandra, 2011). As per the given scenario,

restaurant incurs direct cost on flour, olive oil and other material which restaurant is

required to prepare food. Direct cost closely affects the cost of products or services when

it rises or falls. Indirect cost: It can be defined as those which are not directly related to the cost object. It

may be fixed or variable in nature (Arnold, 2008). In order to prepare food and to serve

the customers effectually, restaurant has to bear several fixed or variable costs.

Restaurant has to incur various indirect expenses such as rent, advertisement, insurance,

electricity and other expenses. Restaurant has to regularly make indirect expenses either

product goes out on a large scale or not. Fixed cost: Fixed costs are those which remains similar regardless the level of output

produced. Restaurant bears several fixed costs or expenses such as salary, rent and

depreciation on assets. Variable cost: This cost consists of those which vary as changes take place in the volume

of activity or output produced. Examples of indirect cost include insurance,

advertisement and electricity expenses (Brigham and Houston, 2011).

Selling price: Selling price is the combination of various costs such as direct, indirect and

fixed and variable cost (Park and Jang, 2014). Each and every company calculates the

selling price of product or services in order to achieve profits and thereby, builds

competitive advantage.

Relationship between cost, gross profit and selling price is as follows:

Selling price = cost + cost *profit%

3

As per the above calculation, it has been assessed that cost of per unit of product is £2.85

and to gain 85% profit margin, restaurant has to sell its product on £5.27.

5. Suitable ways for restaurant to control its stock

Inventory management is the system that is used for the purpose of overseeing flow of

products and services in and out of the business. The restaurant can decide on incorporating one

key inventory management technique or can make use of combination of several techniques so as

to fulfill the needs of firm (Muradoğlu and Sivaprasad, 2014). The role of stock control plays an

essential role within organization as it assists the firm in meeting customer’s demand within

specified duration of time in an effective manner. The ways in which restaurant can control stock

is enumerated in the manner below: Supplier's assistance: It is an effective manner that assists in managing the inventory. The

inventory managed by supplier provides vendor with an access to distributor's inventory

data. Based upon the need of distributors, the suppliers generate purchase orders. With

the assistance of supplier, restaurant can manage its inventory with effectiveness. Inventory control personnel: It is regarded as one of the most effective approaches of

inventory management as it includes hiring of inventory control specialists. With this, the

restaurant can manage all the merchandise items that are in the hands as well as in transit. Lead time: It is referred as the amount of time that is taken to reorder inventory. It is an

effective means through which stock can be managed (Rabiu and et.al., 2015). This is

because it essentially establishes lead time reports that assist in gaining insight to the

extent to which the inventory can be replenished. Thus, the restaurant can make use of

such technique in order to manage its inventory with effectiveness. Monitor inventory levels: By having high level of inventory, the expenses of company as

well as its overhead costs increase to a greater extent. Therefore, by undertaking effective

measures, organization can assess the needs of stock for the particular time period

(Gesimba, Alvar and Mante, 2014). It ensures smooth running of business operations or

activities and thereby, reduces high inventory cost. Customer delivery: It is an effectual way through which company can manage its

inventory level efficiently and cut down the storage cost. By using this technique,

4

and to gain 85% profit margin, restaurant has to sell its product on £5.27.

5. Suitable ways for restaurant to control its stock

Inventory management is the system that is used for the purpose of overseeing flow of

products and services in and out of the business. The restaurant can decide on incorporating one

key inventory management technique or can make use of combination of several techniques so as

to fulfill the needs of firm (Muradoğlu and Sivaprasad, 2014). The role of stock control plays an

essential role within organization as it assists the firm in meeting customer’s demand within

specified duration of time in an effective manner. The ways in which restaurant can control stock

is enumerated in the manner below: Supplier's assistance: It is an effective manner that assists in managing the inventory. The

inventory managed by supplier provides vendor with an access to distributor's inventory

data. Based upon the need of distributors, the suppliers generate purchase orders. With

the assistance of supplier, restaurant can manage its inventory with effectiveness. Inventory control personnel: It is regarded as one of the most effective approaches of

inventory management as it includes hiring of inventory control specialists. With this, the

restaurant can manage all the merchandise items that are in the hands as well as in transit. Lead time: It is referred as the amount of time that is taken to reorder inventory. It is an

effective means through which stock can be managed (Rabiu and et.al., 2015). This is

because it essentially establishes lead time reports that assist in gaining insight to the

extent to which the inventory can be replenished. Thus, the restaurant can make use of

such technique in order to manage its inventory with effectiveness. Monitor inventory levels: By having high level of inventory, the expenses of company as

well as its overhead costs increase to a greater extent. Therefore, by undertaking effective

measures, organization can assess the needs of stock for the particular time period

(Gesimba, Alvar and Mante, 2014). It ensures smooth running of business operations or

activities and thereby, reduces high inventory cost. Customer delivery: It is an effectual way through which company can manage its

inventory level efficiently and cut down the storage cost. By using this technique,

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

restaurant can assess the time which organization takes to sell and deliver the products

and services to the ultimate customer. It enables the corporation to manage its inventory

and to attain higher profits. Purchase software: Restaurant can design or use the purchasing software to manage its

inventory level to a great extent. It provides deeper insight regarding the availability of

stock within an organization (Isaac, Lawal and Okoli, 2015). Besides this, it also

indicates the level at which enterprise requires to make order for the stock. It is the most

suitable technique through which restaurant can manage its stock level. Tracking system: By developing tracking system, restaurant can manage its inventory

level and monitor the level of inventory after a regular interval. Stock tracking system

ranges from spreadsheet to computer program. It allows the business owner to make

effective control upon its stock level (Balogun, Mamidu and Owuze, 2015).

Work in progress: ThroughWIP Technique, company can track its inventory level when

they move from various operational stages. Firm needs to make use of cost effective

technique and need to make efforts to make optimum utlization raw materal to control

high storage cost (Top Ten Ways to Manage Inventory, 2015).

TASK B

Sources and structure of Trial balance

Trial balance represents the balance or summarizes ledger account which is prepared by

the finance manager at the end of accounting year. In order to prepare the financial statement,

finance manager needs to prepare trial balance of the firm (Balakrishnan, Labro and Soderstrom,

2014). It further helps in preparing balance sheet as well as P&L account of company.

Structure of trial balance

Particulars Debit (£) Credit (£)

Furniture xxx

Purchase xxx

Sales xxx

Bank loan xxx

Shares and debentures xxx

5

and services to the ultimate customer. It enables the corporation to manage its inventory

and to attain higher profits. Purchase software: Restaurant can design or use the purchasing software to manage its

inventory level to a great extent. It provides deeper insight regarding the availability of

stock within an organization (Isaac, Lawal and Okoli, 2015). Besides this, it also

indicates the level at which enterprise requires to make order for the stock. It is the most

suitable technique through which restaurant can manage its stock level. Tracking system: By developing tracking system, restaurant can manage its inventory

level and monitor the level of inventory after a regular interval. Stock tracking system

ranges from spreadsheet to computer program. It allows the business owner to make

effective control upon its stock level (Balogun, Mamidu and Owuze, 2015).

Work in progress: ThroughWIP Technique, company can track its inventory level when

they move from various operational stages. Firm needs to make use of cost effective

technique and need to make efforts to make optimum utlization raw materal to control

high storage cost (Top Ten Ways to Manage Inventory, 2015).

TASK B

Sources and structure of Trial balance

Trial balance represents the balance or summarizes ledger account which is prepared by

the finance manager at the end of accounting year. In order to prepare the financial statement,

finance manager needs to prepare trial balance of the firm (Balakrishnan, Labro and Soderstrom,

2014). It further helps in preparing balance sheet as well as P&L account of company.

Structure of trial balance

Particulars Debit (£) Credit (£)

Furniture xxx

Purchase xxx

Sales xxx

Bank loan xxx

Shares and debentures xxx

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

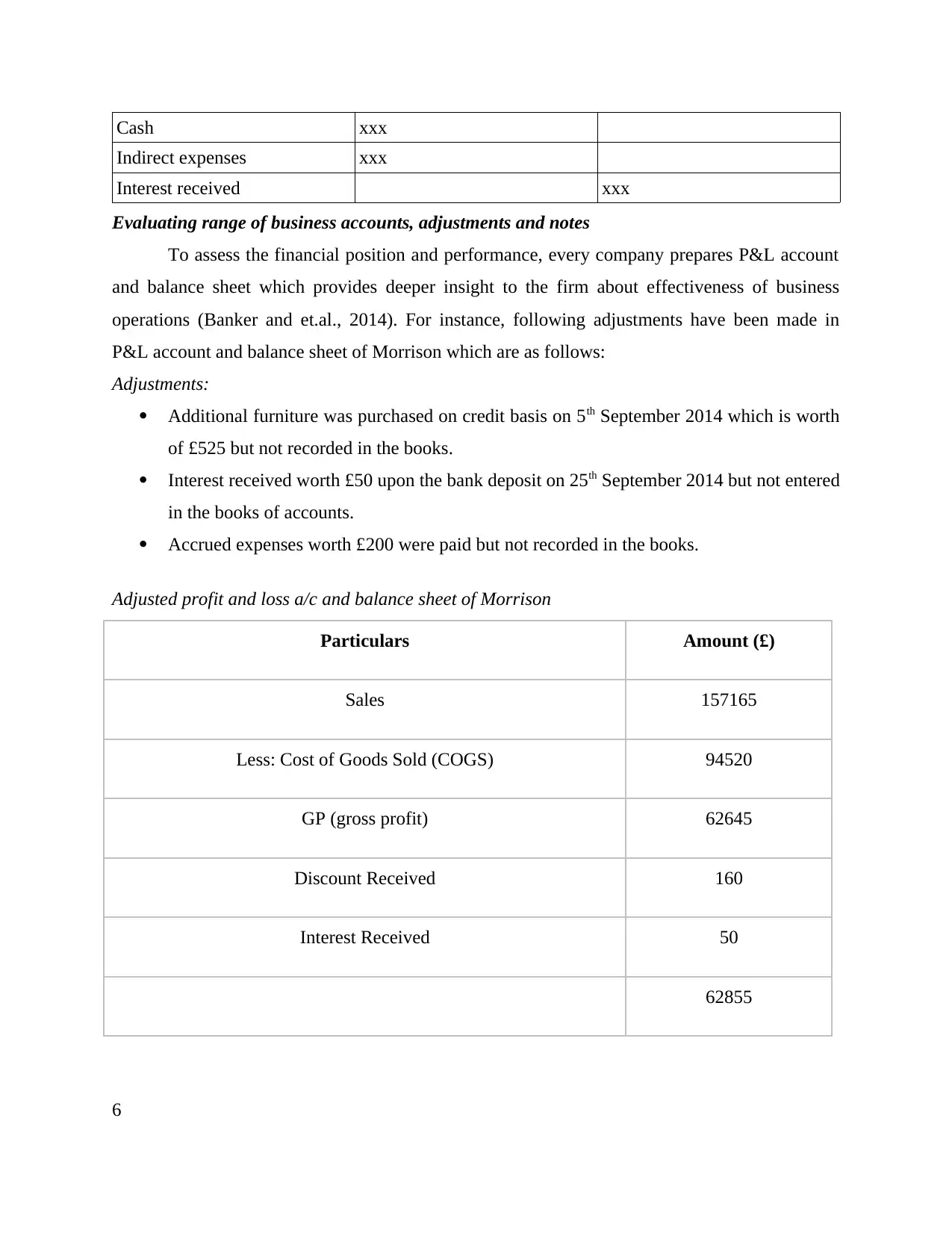

Cash xxx

Indirect expenses xxx

Interest received xxx

Evaluating range of business accounts, adjustments and notes

To assess the financial position and performance, every company prepares P&L account

and balance sheet which provides deeper insight to the firm about effectiveness of business

operations (Banker and et.al., 2014). For instance, following adjustments have been made in

P&L account and balance sheet of Morrison which are as follows:

Adjustments:

Additional furniture was purchased on credit basis on 5th September 2014 which is worth

of £525 but not recorded in the books.

Interest received worth £50 upon the bank deposit on 25th September 2014 but not entered

in the books of accounts.

Accrued expenses worth £200 were paid but not recorded in the books.

Adjusted profit and loss a/c and balance sheet of Morrison

Particulars Amount (£)

Sales 157165

Less: Cost of Goods Sold (COGS) 94520

GP (gross profit) 62645

Discount Received 160

Interest Received 50

62855

6

Indirect expenses xxx

Interest received xxx

Evaluating range of business accounts, adjustments and notes

To assess the financial position and performance, every company prepares P&L account

and balance sheet which provides deeper insight to the firm about effectiveness of business

operations (Banker and et.al., 2014). For instance, following adjustments have been made in

P&L account and balance sheet of Morrison which are as follows:

Adjustments:

Additional furniture was purchased on credit basis on 5th September 2014 which is worth

of £525 but not recorded in the books.

Interest received worth £50 upon the bank deposit on 25th September 2014 but not entered

in the books of accounts.

Accrued expenses worth £200 were paid but not recorded in the books.

Adjusted profit and loss a/c and balance sheet of Morrison

Particulars Amount (£)

Sales 157165

Less: Cost of Goods Sold (COGS) 94520

GP (gross profit) 62645

Discount Received 160

Interest Received 50

62855

6

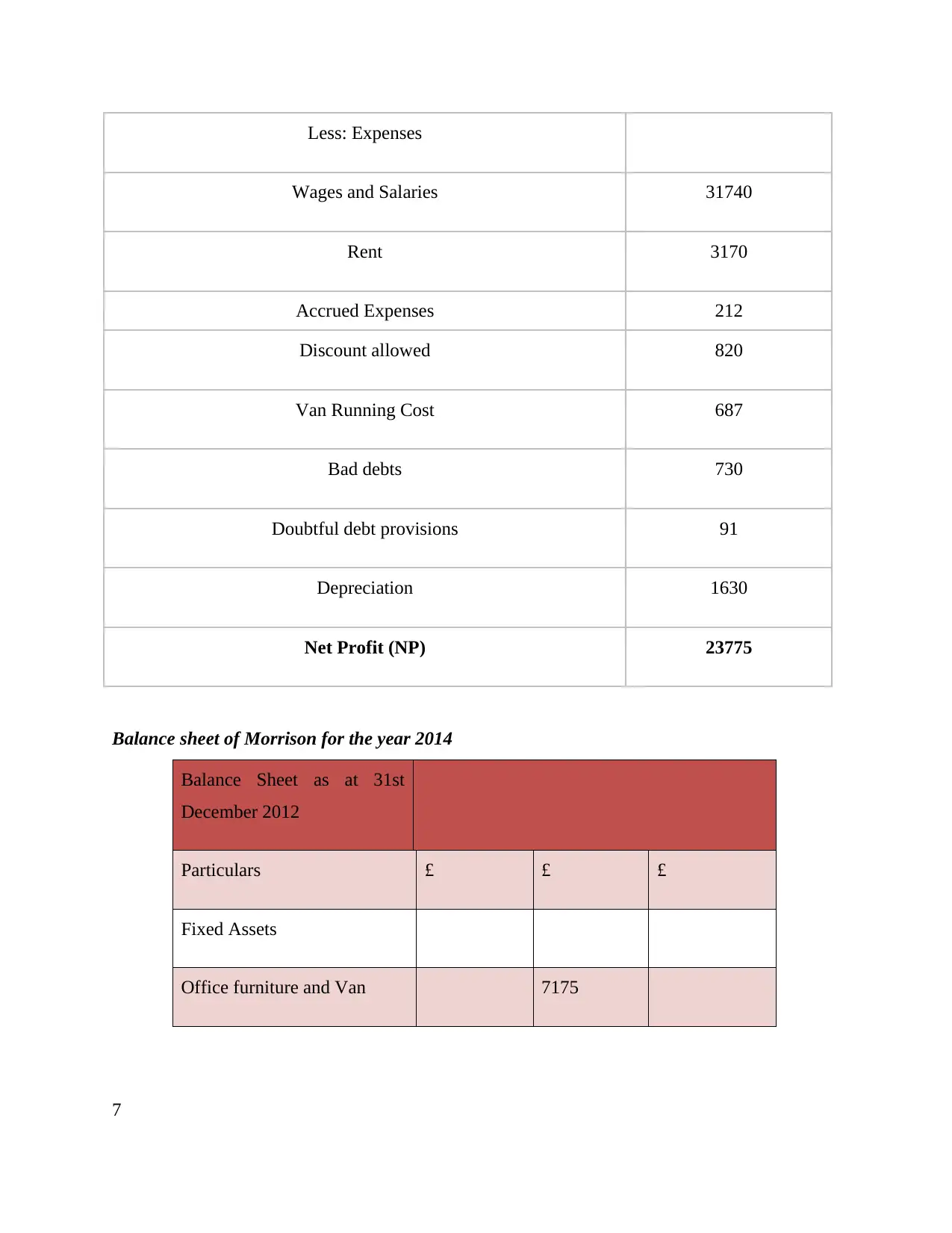

Less: Expenses

Wages and Salaries 31740

Rent 3170

Accrued Expenses 212

Discount allowed 820

Van Running Cost 687

Bad debts 730

Doubtful debt provisions 91

Depreciation 1630

Net Profit (NP) 23775

Balance sheet of Morrison for the year 2014

Balance Sheet as at 31st

December 2012

Particulars £ £ £

Fixed Assets

Office furniture and Van 7175

7

Wages and Salaries 31740

Rent 3170

Accrued Expenses 212

Discount allowed 820

Van Running Cost 687

Bad debts 730

Doubtful debt provisions 91

Depreciation 1630

Net Profit (NP) 23775

Balance sheet of Morrison for the year 2014

Balance Sheet as at 31st

December 2012

Particulars £ £ £

Fixed Assets

Office furniture and Van 7175

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

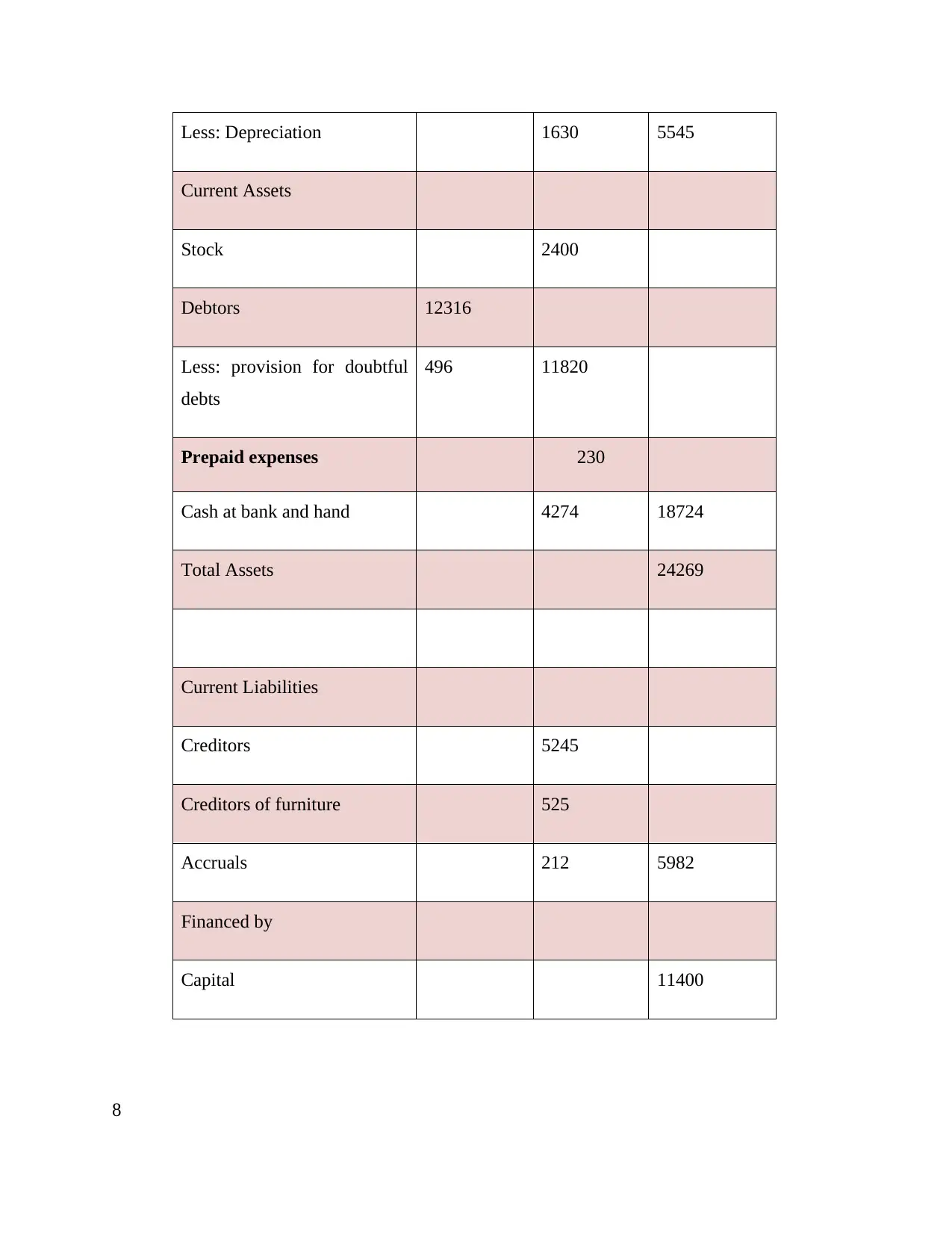

Less: Depreciation 1630 5545

Current Assets

Stock 2400

Debtors 12316

Less: provision for doubtful

debts

496 11820

Prepaid expenses 230

Cash at bank and hand 4274 18724

Total Assets 24269

Current Liabilities

Creditors 5245

Creditors of furniture 525

Accruals 212 5982

Financed by

Capital 11400

8

Current Assets

Stock 2400

Debtors 12316

Less: provision for doubtful

debts

496 11820

Prepaid expenses 230

Cash at bank and hand 4274 18724

Total Assets 24269

Current Liabilities

Creditors 5245

Creditors of furniture 525

Accruals 212 5982

Financed by

Capital 11400

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

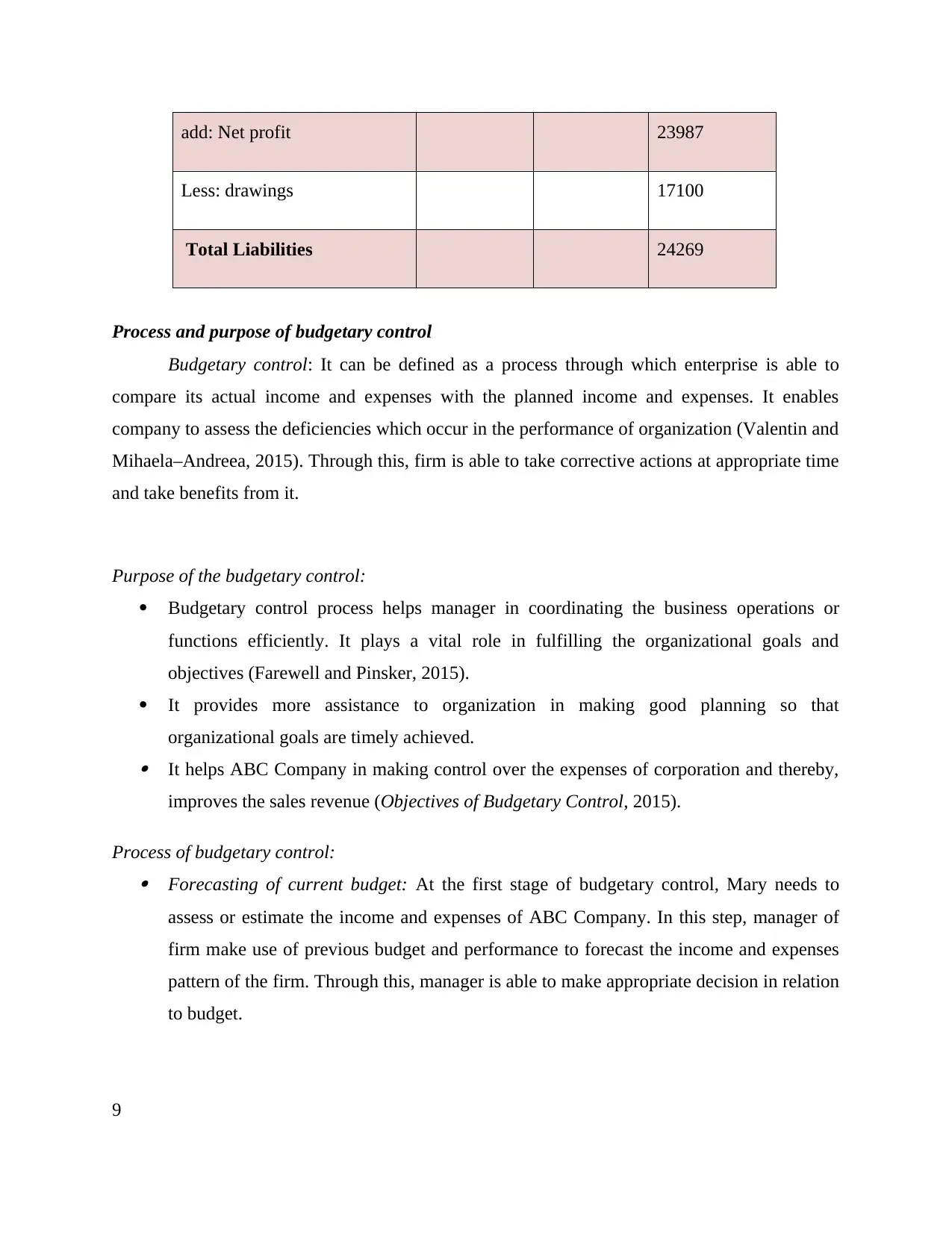

add: Net profit 23987

Less: drawings 17100

Total Liabilities 24269

Process and purpose of budgetary control

Budgetary control: It can be defined as a process through which enterprise is able to

compare its actual income and expenses with the planned income and expenses. It enables

company to assess the deficiencies which occur in the performance of organization (Valentin and

Mihaela–Andreea, 2015). Through this, firm is able to take corrective actions at appropriate time

and take benefits from it.

Purpose of the budgetary control:

Budgetary control process helps manager in coordinating the business operations or

functions efficiently. It plays a vital role in fulfilling the organizational goals and

objectives (Farewell and Pinsker, 2015).

It provides more assistance to organization in making good planning so that

organizational goals are timely achieved. It helps ABC Company in making control over the expenses of corporation and thereby,

improves the sales revenue (Objectives of Budgetary Control, 2015).

Process of budgetary control: Forecasting of current budget: At the first stage of budgetary control, Mary needs to

assess or estimate the income and expenses of ABC Company. In this step, manager of

firm make use of previous budget and performance to forecast the income and expenses

pattern of the firm. Through this, manager is able to make appropriate decision in relation

to budget.

9

Less: drawings 17100

Total Liabilities 24269

Process and purpose of budgetary control

Budgetary control: It can be defined as a process through which enterprise is able to

compare its actual income and expenses with the planned income and expenses. It enables

company to assess the deficiencies which occur in the performance of organization (Valentin and

Mihaela–Andreea, 2015). Through this, firm is able to take corrective actions at appropriate time

and take benefits from it.

Purpose of the budgetary control:

Budgetary control process helps manager in coordinating the business operations or

functions efficiently. It plays a vital role in fulfilling the organizational goals and

objectives (Farewell and Pinsker, 2015).

It provides more assistance to organization in making good planning so that

organizational goals are timely achieved. It helps ABC Company in making control over the expenses of corporation and thereby,

improves the sales revenue (Objectives of Budgetary Control, 2015).

Process of budgetary control: Forecasting of current budget: At the first stage of budgetary control, Mary needs to

assess or estimate the income and expenses of ABC Company. In this step, manager of

firm make use of previous budget and performance to forecast the income and expenses

pattern of the firm. Through this, manager is able to make appropriate decision in relation

to budget.

9

Preparation and approval of budget: Once income and expenses of ABC Company have

estimated then Mary prepares suitable budget for the financial year (Minnis and

Sutherland, 2014). In addition to this, Mary needs to take approval from high authority or

board of director before circulating it at all the levels of management. Comparison of actual performance with the budgeted performance: In this stage of

budgetary control process, manager of the firm compares actual performance with the

budgeted amount. Besides this, by comparing actual amount with the budgeted sum,

manager makes efforts to identity the deviations which occur in performance. Investigation of deviations: In this, manager investigates the reasons due to deficiencies

that occur in the performance. It is the most important stage upon which the success of

corrective action depends (Staples and et.al., 2014). Moreover, without knowing the

reason, manager of firm is unable to take corrective measures for making improvements

in the current or actual performance.

Taking corrective actions or measures: At the last stage of budgetary control process,

manager takes corrective actions or measures to improve the performance. It helps

company in achieving the aim and objectives.

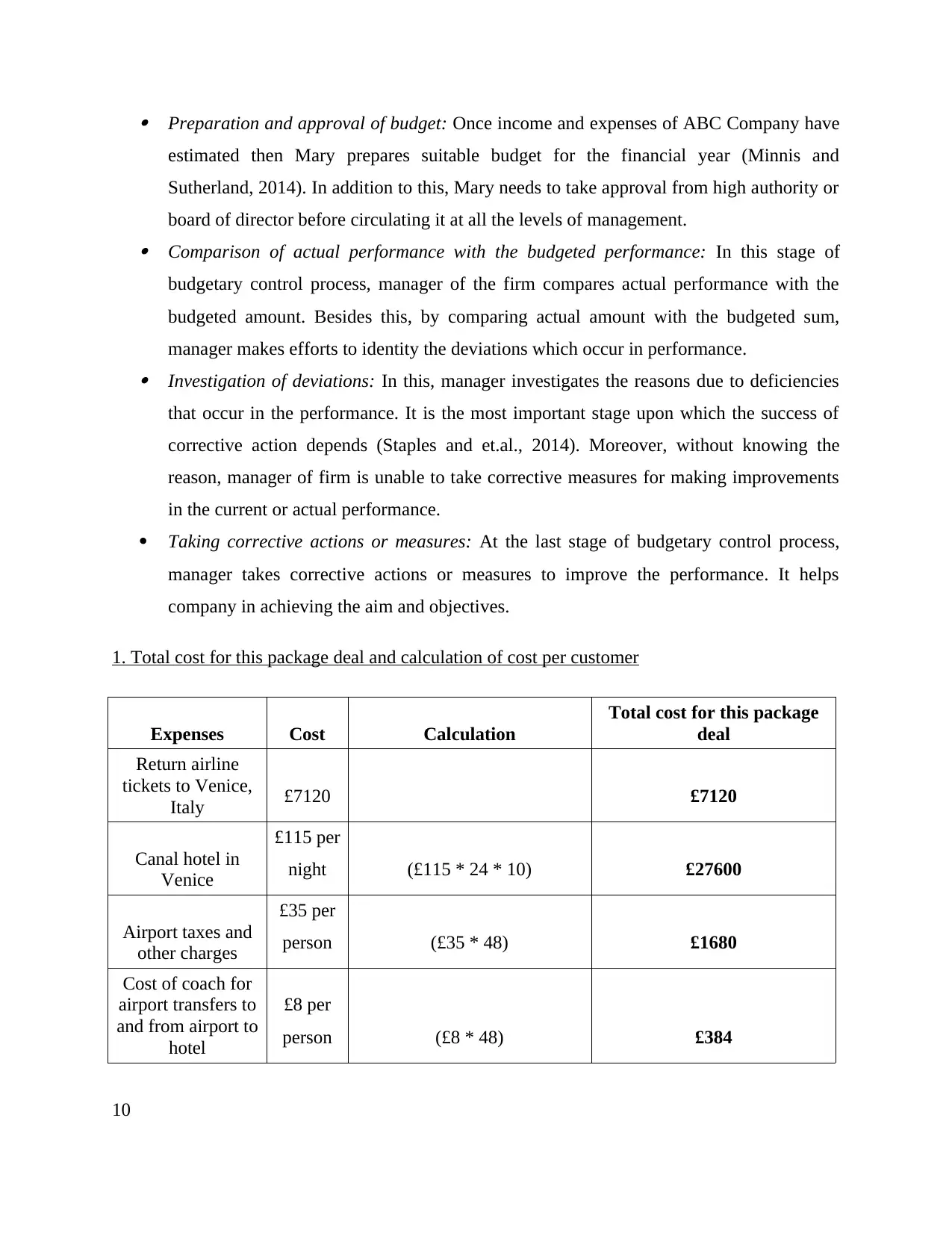

1. Total cost for this package deal and calculation of cost per customer

Expenses Cost Calculation

Total cost for this package

deal

Return airline

tickets to Venice,

Italy £7120 £7120

Canal hotel in

Venice

£115 per

night (£115 * 24 * 10) £27600

Airport taxes and

other charges

£35 per

person (£35 * 48) £1680

Cost of coach for

airport transfers to

and from airport to

hotel

£8 per

person (£8 * 48) £384

10

estimated then Mary prepares suitable budget for the financial year (Minnis and

Sutherland, 2014). In addition to this, Mary needs to take approval from high authority or

board of director before circulating it at all the levels of management. Comparison of actual performance with the budgeted performance: In this stage of

budgetary control process, manager of the firm compares actual performance with the

budgeted amount. Besides this, by comparing actual amount with the budgeted sum,

manager makes efforts to identity the deviations which occur in performance. Investigation of deviations: In this, manager investigates the reasons due to deficiencies

that occur in the performance. It is the most important stage upon which the success of

corrective action depends (Staples and et.al., 2014). Moreover, without knowing the

reason, manager of firm is unable to take corrective measures for making improvements

in the current or actual performance.

Taking corrective actions or measures: At the last stage of budgetary control process,

manager takes corrective actions or measures to improve the performance. It helps

company in achieving the aim and objectives.

1. Total cost for this package deal and calculation of cost per customer

Expenses Cost Calculation

Total cost for this package

deal

Return airline

tickets to Venice,

Italy £7120 £7120

Canal hotel in

Venice

£115 per

night (£115 * 24 * 10) £27600

Airport taxes and

other charges

£35 per

person (£35 * 48) £1680

Cost of coach for

airport transfers to

and from airport to

hotel

£8 per

person (£8 * 48) £384

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.