Finance in Hospitality: Transactions, Information, and Analysis

VerifiedAdded on 2023/03/31

|9

|2348

|115

Case Study

AI Summary

This assignment covers various aspects of finance in the hospitality industry, including defining assets, liabilities, equity, cost of sales, income, and expenses with relevant examples. It discusses financial reporting methods, fixed and variable costs, and key business performance indicators. The assignment also explores source documents, journal entries, transaction reports, and the importance of regular financial information review. It delves into double-entry bookkeeping rules and common accounting software like FRESHBOOKS. Furthermore, it includes a research project defining ledgers, subsidiary ledgers, receipts, disbursements, accounts payable, debtors, creditors, and cash flow, along with specific hospitality concepts like guest accounts, inventory, and revenue management, and GST reporting requirements. Finally, a case study analyzes the debt ratio, equity ratio, current ratio, gross profit margin, and net profit margin for Fat Freddie’s Fab Frogs, providing insights into the company's financial performance.

Answer to Part A – Written or Oral Questions

Answer 1:

a. Assets: An asset can be defined as any item of value or any resource that is valuable and

can be converted into cash or cash equivalent. Assets have value and are owned by

companies or individuals to reap their benefit over a longer period of time by generating

revenue or income from the use of the asset.

b. Liabilities: Liabilities can be defined as financial obligation that the company or

individual own in the course of operations. These are financial benefits that must be paid

by the company and thus create an obligation for them.

c. Equity: This is the share in the company owned by the shareholders. In a single word

equity is the stock of the company. It is issued by the company to the shareholders giving

them right in the share of the company.

d. Cost of Sales: Cost of sales is the direct cost incurred by the company to generate the

sales made by it. Also known as the Cost of Goods Sold, it is the cost of purchasing the

raw material for the goods to be manufactured by the company or the direct cost incurred

by the company to provide the offered services.

e. Income: Income is the receipt of money by the company for the sale of goods/services

that it provides. It is simply the money that the company or individual gets by selling the

goods or services to its customers.

f. Expense: Expenses can be defined as costs that must be incurred by the company to

generate sales and revenue. These are monetary payments that must be paid to convert

sales for the company.

Answer 2:

Examples of the above related to the hospitality industry is as below:

a. Assets: The hotel building, cash, inventory in terms of available rooms etc.

b. Liabilities: Providing rooms against advance booking

c. Equity: Stake in the hotel ownership or

d. Cost of sales: Room services cost

e. Income: Tariffs, Revenue from meals, laundry etc.

f. Expense: Staff Salary, Housekeeping, meals etc.

Answer 3:

The first date of the Australian financial year is 1st July and the last date is 30th June. There are

no other reporting periods and the hospitality businesses follow the same period.

1 | P a g e

Answer 1:

a. Assets: An asset can be defined as any item of value or any resource that is valuable and

can be converted into cash or cash equivalent. Assets have value and are owned by

companies or individuals to reap their benefit over a longer period of time by generating

revenue or income from the use of the asset.

b. Liabilities: Liabilities can be defined as financial obligation that the company or

individual own in the course of operations. These are financial benefits that must be paid

by the company and thus create an obligation for them.

c. Equity: This is the share in the company owned by the shareholders. In a single word

equity is the stock of the company. It is issued by the company to the shareholders giving

them right in the share of the company.

d. Cost of Sales: Cost of sales is the direct cost incurred by the company to generate the

sales made by it. Also known as the Cost of Goods Sold, it is the cost of purchasing the

raw material for the goods to be manufactured by the company or the direct cost incurred

by the company to provide the offered services.

e. Income: Income is the receipt of money by the company for the sale of goods/services

that it provides. It is simply the money that the company or individual gets by selling the

goods or services to its customers.

f. Expense: Expenses can be defined as costs that must be incurred by the company to

generate sales and revenue. These are monetary payments that must be paid to convert

sales for the company.

Answer 2:

Examples of the above related to the hospitality industry is as below:

a. Assets: The hotel building, cash, inventory in terms of available rooms etc.

b. Liabilities: Providing rooms against advance booking

c. Equity: Stake in the hotel ownership or

d. Cost of sales: Room services cost

e. Income: Tariffs, Revenue from meals, laundry etc.

f. Expense: Staff Salary, Housekeeping, meals etc.

Answer 3:

The first date of the Australian financial year is 1st July and the last date is 30th June. There are

no other reporting periods and the hospitality businesses follow the same period.

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Answer 4:

The two methods of Financial Reporting are:

1. Cash method of Accounting

2. Accrual method of accounting

Answer 5:

Cash method of Accounting: Under this method, income and expenses are recorded in the books

of accounts only when they are received and paid by the company. The company records the

income or revenue only when the cash is received by it and subsequently all expenses are

recorded only when the payment for the same has been made.

This is simple to use and applicable for small businesses having turnover of $25,000,000 or less

for the past three tax years and also applicable to individuals having business which is 95%

related to providing services.

Accrual method of Accounting: Under this method, companies recognise the revenue when they

are earned by them and not when they are realised. Further, expenses matching with the revenues

are also reported when the revenues are earned irrespective whether they have been paid or not.

This is used by companies having turnover of more than $25,000,000.

Answer 6:

Fixed costs are stagnant cost which does not change with the change in the activity level of the

hotel. They are constant and fixed irrespective of the operations of the hotel.

On the other hand, Variable costs are recurring expenses for the hotel which is based on the

actual activity level of the hotel. These are costs which are paid on the basis of change in some

variable on which the cost are dependent.

Answer 7:

Example of Fixed Cost: Staff Salary, license fees to the government etc.

Example of variable cost: Meal costs, laundry charges etc.

Answer 8:

The business performance indicators and benchmarks that could be used for decision making

purposes in the hospitality industry are:

Occupancy percentage

Rating of the hotel or unit

The Average Daily Rate or ADR

2 | P a g e

The two methods of Financial Reporting are:

1. Cash method of Accounting

2. Accrual method of accounting

Answer 5:

Cash method of Accounting: Under this method, income and expenses are recorded in the books

of accounts only when they are received and paid by the company. The company records the

income or revenue only when the cash is received by it and subsequently all expenses are

recorded only when the payment for the same has been made.

This is simple to use and applicable for small businesses having turnover of $25,000,000 or less

for the past three tax years and also applicable to individuals having business which is 95%

related to providing services.

Accrual method of Accounting: Under this method, companies recognise the revenue when they

are earned by them and not when they are realised. Further, expenses matching with the revenues

are also reported when the revenues are earned irrespective whether they have been paid or not.

This is used by companies having turnover of more than $25,000,000.

Answer 6:

Fixed costs are stagnant cost which does not change with the change in the activity level of the

hotel. They are constant and fixed irrespective of the operations of the hotel.

On the other hand, Variable costs are recurring expenses for the hotel which is based on the

actual activity level of the hotel. These are costs which are paid on the basis of change in some

variable on which the cost are dependent.

Answer 7:

Example of Fixed Cost: Staff Salary, license fees to the government etc.

Example of variable cost: Meal costs, laundry charges etc.

Answer 8:

The business performance indicators and benchmarks that could be used for decision making

purposes in the hospitality industry are:

Occupancy percentage

Rating of the hotel or unit

The Average Daily Rate or ADR

2 | P a g e

The Revenue per Available Room of the hotel

Customer Satisfaction

Return on Investment.

Answer 9:

Sl No. Document Sl No. Description

a Source documents v Details products and services provided to a

customer

b Journal entries vi A basic document that details the financial

transactions of a company

c Transaction reports iv Report detailing specific information, such as

EFTPOS and banking records

d Account summaries & balances ix These can be obtained from the bank, and

should maintain strict vigilance over

e Balance sheets ii Shows assets, liabilities and owner’s equity

f Profit & loss statements viii Shows the revenue and expenses of a

business over a period of time

g Invoices iii Original documents in paper form that prove

a transaction has taken place

h Budget reports vii Details budgeted figures compared to actual

figures

i Expenditure reports i Details budgeted spending vs actual spending

Answer 10:

It is important for hospitality business to review the above financial information regularly so as

to remain abreast with the health of the company and thus take remedial corrective action for any

adverse account immediately. Reviewing the financial information regularly gives the company

an edge on controlling and monitoring requirements. This enables them analyse the variances

from budgeted at an early stage thus giving better control.

Answer 11:

The basic rules under pinning the double entry bookkeeping are:

For every single debit entry in the books, there must be an equal and a corresponding

credit entry and vice versa

The rules of debit and credit for personal account

o Debit the receiver;

o Credit the giver.

The rules of debit and credit for Real Accounts

o Debit What Comes in;

3 | P a g e

Customer Satisfaction

Return on Investment.

Answer 9:

Sl No. Document Sl No. Description

a Source documents v Details products and services provided to a

customer

b Journal entries vi A basic document that details the financial

transactions of a company

c Transaction reports iv Report detailing specific information, such as

EFTPOS and banking records

d Account summaries & balances ix These can be obtained from the bank, and

should maintain strict vigilance over

e Balance sheets ii Shows assets, liabilities and owner’s equity

f Profit & loss statements viii Shows the revenue and expenses of a

business over a period of time

g Invoices iii Original documents in paper form that prove

a transaction has taken place

h Budget reports vii Details budgeted figures compared to actual

figures

i Expenditure reports i Details budgeted spending vs actual spending

Answer 10:

It is important for hospitality business to review the above financial information regularly so as

to remain abreast with the health of the company and thus take remedial corrective action for any

adverse account immediately. Reviewing the financial information regularly gives the company

an edge on controlling and monitoring requirements. This enables them analyse the variances

from budgeted at an early stage thus giving better control.

Answer 11:

The basic rules under pinning the double entry bookkeeping are:

For every single debit entry in the books, there must be an equal and a corresponding

credit entry and vice versa

The rules of debit and credit for personal account

o Debit the receiver;

o Credit the giver.

The rules of debit and credit for Real Accounts

o Debit What Comes in;

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

o Credit What Goes out.

The rules of debit and credit for Nominal Account

o Debit Expenses and Losses;

o Credit Incomes and Gains.

Answer 12:

One of the most common accounting software package used in the hospitality industry is

FRESHBOOKS. The general features of the same are as below:

Recording each transaction in form of journals

Creation of financial statements readily at all times for review

Summary of all the tax returns filed by the company.

Control on balance sheet items by providing graphical representation of the items.

Colour coded expenses details for better review.

Availability of various reports for control including expenses report, accounts payable

report, accounts receivable report, invoice details among many others.

4 | P a g e

The rules of debit and credit for Nominal Account

o Debit Expenses and Losses;

o Credit Incomes and Gains.

Answer 12:

One of the most common accounting software package used in the hospitality industry is

FRESHBOOKS. The general features of the same are as below:

Recording each transaction in form of journals

Creation of financial statements readily at all times for review

Summary of all the tax returns filed by the company.

Control on balance sheet items by providing graphical representation of the items.

Colour coded expenses details for better review.

Availability of various reports for control including expenses report, accounts payable

report, accounts receivable report, invoice details among many others.

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Answer to Part B: Research Project

Answer 1:

a. Ledgers: Ledgers are individual accounts opened by the company in which all the debits

and credits made to it during the year are posted from journal. Their balances reflect the

amount that we owe or they owe to us in the given period of time.

b. Subsidiary Ledger: This ledger is the dump house of the general ledger control account.

Once information has been recorded in a subsidiary ledger, it is summarized and posted

to a specific control account in the general ledger, based on which the financial

statements are prepared.

c. Receipt: This is the cash received by the company for providing the required goods

and/or services to the customers. Money that is paid by the customers to the company, or

interest received from the investment or cash received by the company by any means are

called receipts

d. Disbursement: This refers to distribution of available cash or resources to other,

Examples employers disburse the salary to the employees monthly indicating that cash is

distributed to them for their services for the company.

e. Accounts Payable: These are payments which must be paid by the company in a fixed

period of time. These are payments for services or resources that have already been used

by the company but not yet paid.

f. Debtors: Debtors can be defined as individual, company or country that owns money.

They are assets for the company and owe the company money for the services that they

have used.

g. Creditors: Creditors can be defined as individual, company or country that we owe

money to. They are liabilities for the company and we owe the company money for the

services that we have used.

h. Cash Flow: This can be defined as either the inflow of cash in form of income or

payment of cash for expenses. Cash flow refers to movement of cash in the firm both in

terms on inflow and outflow.

Answer 2:

Guest Account: The guest account is a temporary account is used to track all the transactions

made by a guest during his stay at the hotel. Once the guest checks out the balances are

transferred to normal revenue and expenses account and the guest account is closed.

Inventory: The inventory for the hospitality industry is the number and types of rooms available

for sale across the countries in which the company operates.

Revenue Management: This is the strategic distribution and pricing techniques used by the

companies to sell the inventory in forms of rooms and other perishable items so as to generate

the maximum revenue.

5 | P a g e

Answer 1:

a. Ledgers: Ledgers are individual accounts opened by the company in which all the debits

and credits made to it during the year are posted from journal. Their balances reflect the

amount that we owe or they owe to us in the given period of time.

b. Subsidiary Ledger: This ledger is the dump house of the general ledger control account.

Once information has been recorded in a subsidiary ledger, it is summarized and posted

to a specific control account in the general ledger, based on which the financial

statements are prepared.

c. Receipt: This is the cash received by the company for providing the required goods

and/or services to the customers. Money that is paid by the customers to the company, or

interest received from the investment or cash received by the company by any means are

called receipts

d. Disbursement: This refers to distribution of available cash or resources to other,

Examples employers disburse the salary to the employees monthly indicating that cash is

distributed to them for their services for the company.

e. Accounts Payable: These are payments which must be paid by the company in a fixed

period of time. These are payments for services or resources that have already been used

by the company but not yet paid.

f. Debtors: Debtors can be defined as individual, company or country that owns money.

They are assets for the company and owe the company money for the services that they

have used.

g. Creditors: Creditors can be defined as individual, company or country that we owe

money to. They are liabilities for the company and we owe the company money for the

services that we have used.

h. Cash Flow: This can be defined as either the inflow of cash in form of income or

payment of cash for expenses. Cash flow refers to movement of cash in the firm both in

terms on inflow and outflow.

Answer 2:

Guest Account: The guest account is a temporary account is used to track all the transactions

made by a guest during his stay at the hotel. Once the guest checks out the balances are

transferred to normal revenue and expenses account and the guest account is closed.

Inventory: The inventory for the hospitality industry is the number and types of rooms available

for sale across the countries in which the company operates.

Revenue Management: This is the strategic distribution and pricing techniques used by the

companies to sell the inventory in forms of rooms and other perishable items so as to generate

the maximum revenue.

5 | P a g e

Answer 3:

The GST reporting requirements for the hospitality business are:

Maintaining the proper receipt and expenses register

GST registration

Filling of GST return timely and regularly

Maintaining room tariff separately

Billing room tariff, laundry and meals separately.

6 | P a g e

The GST reporting requirements for the hospitality business are:

Maintaining the proper receipt and expenses register

GST registration

Filling of GST return timely and regularly

Maintaining room tariff separately

Billing room tariff, laundry and meals separately.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Answer to Part C – Case Study

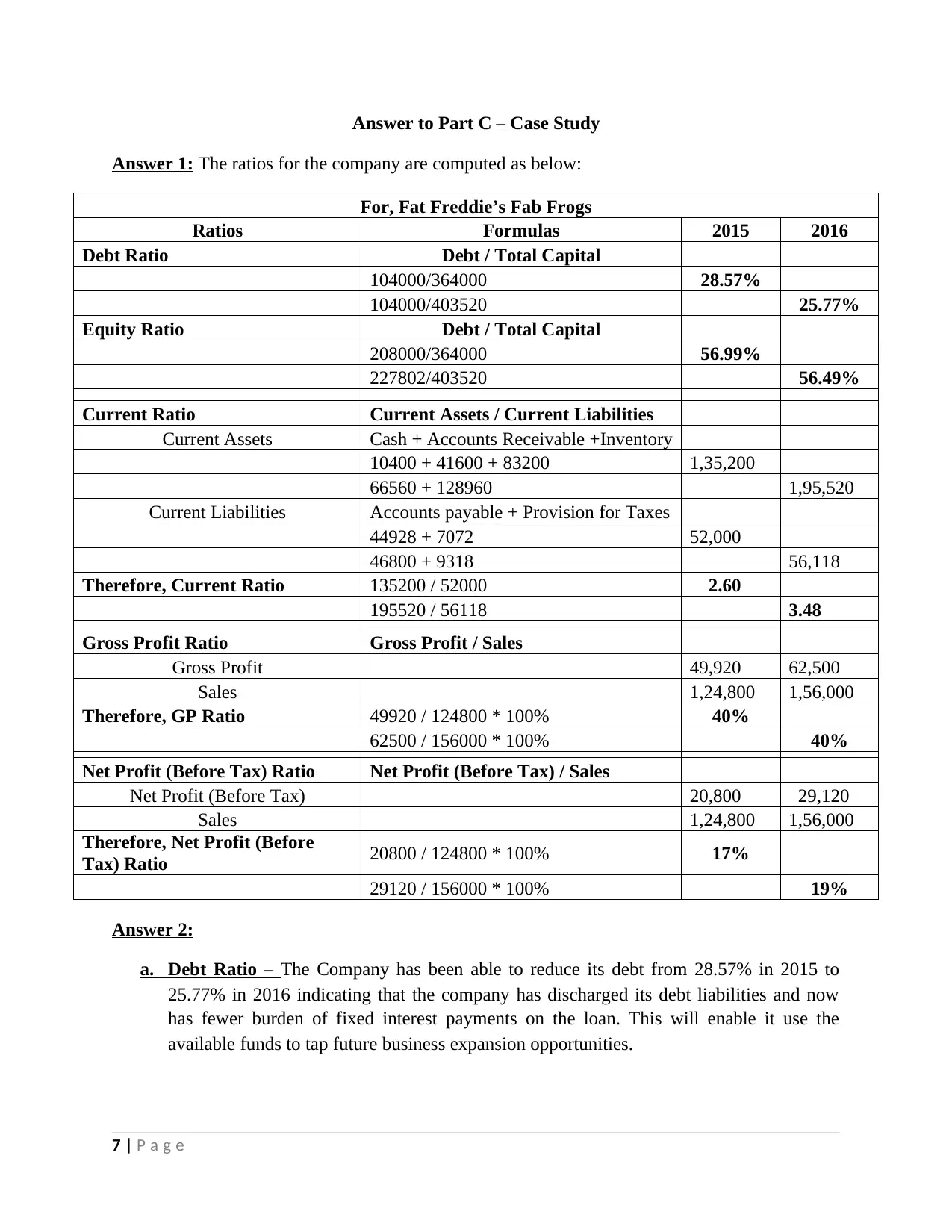

Answer 1: The ratios for the company are computed as below:

For, Fat Freddie’s Fab Frogs

Ratios Formulas 2015 2016

Debt Ratio Debt / Total Capital

104000/364000 28.57%

104000/403520 25.77%

Equity Ratio Debt / Total Capital

208000/364000 56.99%

227802/403520 56.49%

Current Ratio Current Assets / Current Liabilities

Current Assets Cash + Accounts Receivable +Inventory

10400 + 41600 + 83200 1,35,200

66560 + 128960 1,95,520

Current Liabilities Accounts payable + Provision for Taxes

44928 + 7072 52,000

46800 + 9318 56,118

Therefore, Current Ratio 135200 / 52000 2.60

195520 / 56118 3.48

Gross Profit Ratio Gross Profit / Sales

Gross Profit 49,920 62,500

Sales 1,24,800 1,56,000

Therefore, GP Ratio 49920 / 124800 * 100% 40%

62500 / 156000 * 100% 40%

Net Profit (Before Tax) Ratio Net Profit (Before Tax) / Sales

Net Profit (Before Tax) 20,800 29,120

Sales 1,24,800 1,56,000

Therefore, Net Profit (Before

Tax) Ratio 20800 / 124800 * 100% 17%

29120 / 156000 * 100% 19%

Answer 2:

a. Debt Ratio – The Company has been able to reduce its debt from 28.57% in 2015 to

25.77% in 2016 indicating that the company has discharged its debt liabilities and now

has fewer burden of fixed interest payments on the loan. This will enable it use the

available funds to tap future business expansion opportunities.

7 | P a g e

Answer 1: The ratios for the company are computed as below:

For, Fat Freddie’s Fab Frogs

Ratios Formulas 2015 2016

Debt Ratio Debt / Total Capital

104000/364000 28.57%

104000/403520 25.77%

Equity Ratio Debt / Total Capital

208000/364000 56.99%

227802/403520 56.49%

Current Ratio Current Assets / Current Liabilities

Current Assets Cash + Accounts Receivable +Inventory

10400 + 41600 + 83200 1,35,200

66560 + 128960 1,95,520

Current Liabilities Accounts payable + Provision for Taxes

44928 + 7072 52,000

46800 + 9318 56,118

Therefore, Current Ratio 135200 / 52000 2.60

195520 / 56118 3.48

Gross Profit Ratio Gross Profit / Sales

Gross Profit 49,920 62,500

Sales 1,24,800 1,56,000

Therefore, GP Ratio 49920 / 124800 * 100% 40%

62500 / 156000 * 100% 40%

Net Profit (Before Tax) Ratio Net Profit (Before Tax) / Sales

Net Profit (Before Tax) 20,800 29,120

Sales 1,24,800 1,56,000

Therefore, Net Profit (Before

Tax) Ratio 20800 / 124800 * 100% 17%

29120 / 156000 * 100% 19%

Answer 2:

a. Debt Ratio – The Company has been able to reduce its debt from 28.57% in 2015 to

25.77% in 2016 indicating that the company has discharged its debt liabilities and now

has fewer burden of fixed interest payments on the loan. This will enable it use the

available funds to tap future business expansion opportunities.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b. Equity Ratio: The company has increased equity ratio as because the lower debt burden

is now enabling the company to transfer higher net profit to retained earnings thus

increasing the owner’s equity proportion in the total capital structure.

c. Current ratio: The current ratio of the company has improved from 2.60 in 2015 to

3.48 in 2016. This indicates that the company has improved its current assets base as

compared to the increase in current liabilities for the firm. It is better equipped to meet

the debt obligation. However, greater current ratio also reflects loss of opportunity of

investing surplus assets for the benefit of the company.

d. Gross Profit Margin: The Company maintained a constant GP ratio of 40% for the years

2015 and 2016. This is a positive sign indicating that the cost of sales for the company is

constant with respect to the sales made by it during the years.

e. Net Profit Margin: The Company improved the NP ratio from 17% in 2015 to 19% in

2016. This is a positive sign as with the same GP increase in NP indicates that the

company has been able to effectively reduce its expenses, thus garnering better profit

margins.

Answer 3:

The balance sheet and income statement are two quintessential financial statements which reflect

the health of the company. In the hospitality sector, the areas where these would work are

understanding profitability, occupancy rate, and variable revenue per room, Asset and liabilities

position.

Answer 4:

Sharing appropriate financial information with the colleagues is important for the following

reasons:

In increases the accountability for the colleagues and make them more responsible

towards achieving the required numbers.

It empowers the employees and gives them a feeling of importance.

Improves job satisfaction.

8 | P a g e

is now enabling the company to transfer higher net profit to retained earnings thus

increasing the owner’s equity proportion in the total capital structure.

c. Current ratio: The current ratio of the company has improved from 2.60 in 2015 to

3.48 in 2016. This indicates that the company has improved its current assets base as

compared to the increase in current liabilities for the firm. It is better equipped to meet

the debt obligation. However, greater current ratio also reflects loss of opportunity of

investing surplus assets for the benefit of the company.

d. Gross Profit Margin: The Company maintained a constant GP ratio of 40% for the years

2015 and 2016. This is a positive sign indicating that the cost of sales for the company is

constant with respect to the sales made by it during the years.

e. Net Profit Margin: The Company improved the NP ratio from 17% in 2015 to 19% in

2016. This is a positive sign as with the same GP increase in NP indicates that the

company has been able to effectively reduce its expenses, thus garnering better profit

margins.

Answer 3:

The balance sheet and income statement are two quintessential financial statements which reflect

the health of the company. In the hospitality sector, the areas where these would work are

understanding profitability, occupancy rate, and variable revenue per room, Asset and liabilities

position.

Answer 4:

Sharing appropriate financial information with the colleagues is important for the following

reasons:

In increases the accountability for the colleagues and make them more responsible

towards achieving the required numbers.

It empowers the employees and gives them a feeling of importance.

Improves job satisfaction.

8 | P a g e

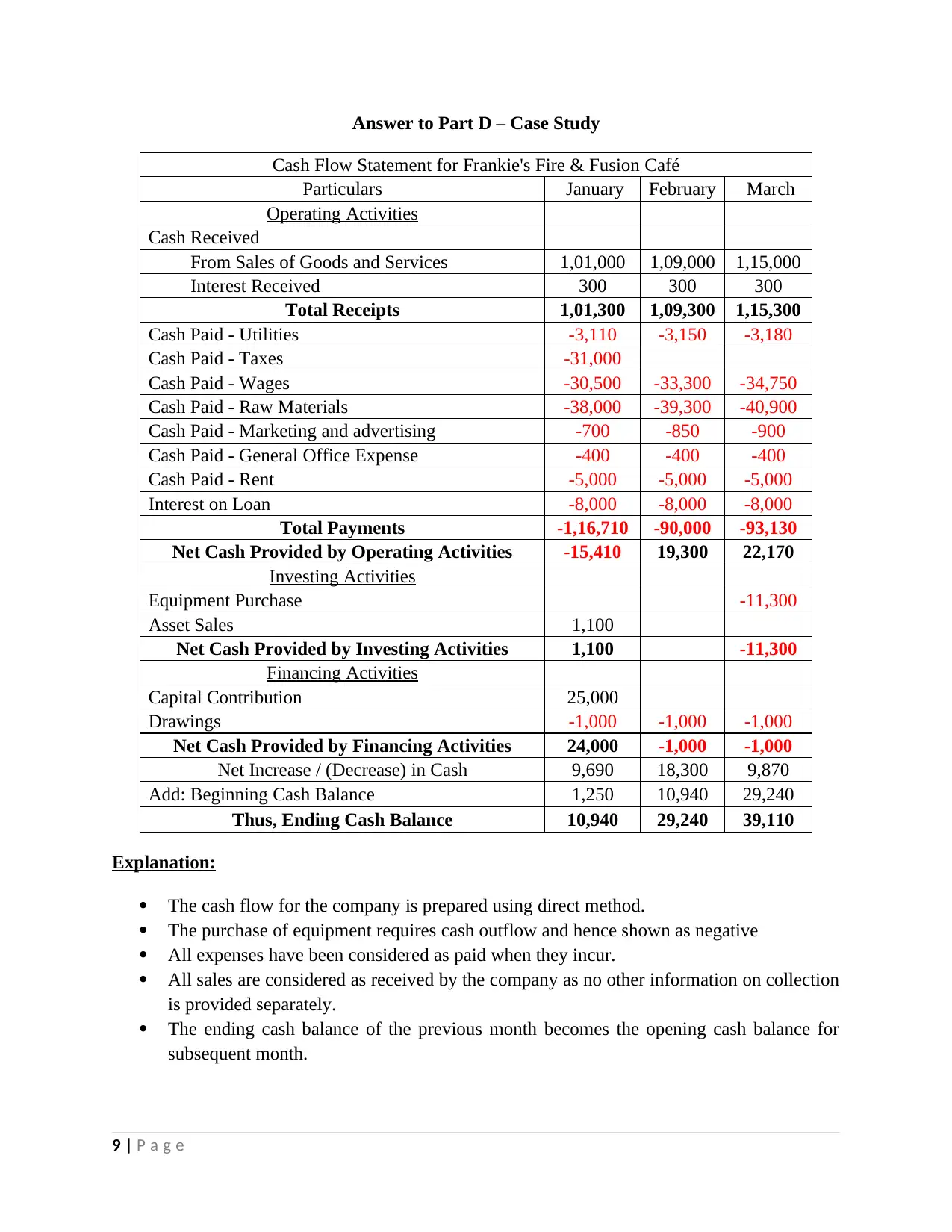

Answer to Part D – Case Study

Cash Flow Statement for Frankie's Fire & Fusion Café

Particulars January February March

Operating Activities

Cash Received

From Sales of Goods and Services 1,01,000 1,09,000 1,15,000

Interest Received 300 300 300

Total Receipts 1,01,300 1,09,300 1,15,300

Cash Paid - Utilities -3,110 -3,150 -3,180

Cash Paid - Taxes -31,000

Cash Paid - Wages -30,500 -33,300 -34,750

Cash Paid - Raw Materials -38,000 -39,300 -40,900

Cash Paid - Marketing and advertising -700 -850 -900

Cash Paid - General Office Expense -400 -400 -400

Cash Paid - Rent -5,000 -5,000 -5,000

Interest on Loan -8,000 -8,000 -8,000

Total Payments -1,16,710 -90,000 -93,130

Net Cash Provided by Operating Activities -15,410 19,300 22,170

Investing Activities

Equipment Purchase -11,300

Asset Sales 1,100

Net Cash Provided by Investing Activities 1,100 -11,300

Financing Activities

Capital Contribution 25,000

Drawings -1,000 -1,000 -1,000

Net Cash Provided by Financing Activities 24,000 -1,000 -1,000

Net Increase / (Decrease) in Cash 9,690 18,300 9,870

Add: Beginning Cash Balance 1,250 10,940 29,240

Thus, Ending Cash Balance 10,940 29,240 39,110

Explanation:

The cash flow for the company is prepared using direct method.

The purchase of equipment requires cash outflow and hence shown as negative

All expenses have been considered as paid when they incur.

All sales are considered as received by the company as no other information on collection

is provided separately.

The ending cash balance of the previous month becomes the opening cash balance for

subsequent month.

9 | P a g e

Cash Flow Statement for Frankie's Fire & Fusion Café

Particulars January February March

Operating Activities

Cash Received

From Sales of Goods and Services 1,01,000 1,09,000 1,15,000

Interest Received 300 300 300

Total Receipts 1,01,300 1,09,300 1,15,300

Cash Paid - Utilities -3,110 -3,150 -3,180

Cash Paid - Taxes -31,000

Cash Paid - Wages -30,500 -33,300 -34,750

Cash Paid - Raw Materials -38,000 -39,300 -40,900

Cash Paid - Marketing and advertising -700 -850 -900

Cash Paid - General Office Expense -400 -400 -400

Cash Paid - Rent -5,000 -5,000 -5,000

Interest on Loan -8,000 -8,000 -8,000

Total Payments -1,16,710 -90,000 -93,130

Net Cash Provided by Operating Activities -15,410 19,300 22,170

Investing Activities

Equipment Purchase -11,300

Asset Sales 1,100

Net Cash Provided by Investing Activities 1,100 -11,300

Financing Activities

Capital Contribution 25,000

Drawings -1,000 -1,000 -1,000

Net Cash Provided by Financing Activities 24,000 -1,000 -1,000

Net Increase / (Decrease) in Cash 9,690 18,300 9,870

Add: Beginning Cash Balance 1,250 10,940 29,240

Thus, Ending Cash Balance 10,940 29,240 39,110

Explanation:

The cash flow for the company is prepared using direct method.

The purchase of equipment requires cash outflow and hence shown as negative

All expenses have been considered as paid when they incur.

All sales are considered as received by the company as no other information on collection

is provided separately.

The ending cash balance of the previous month becomes the opening cash balance for

subsequent month.

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.