Analysis of Managing Financial Resources in Hospitality Industry

VerifiedAdded on 2023/06/17

|13

|3285

|351

Report

AI Summary

This report provides a comprehensive analysis of financial resource management within the hospitality industry. It begins by discussing Generally Accepted Accounting Principles (GAAP) and their importance in maintaining transparent and consistent financial reporting, outlining the ten core principles and their relevance to various stakeholders like owners, customers, suppliers, managers, lenders, and the government. The report then examines the significance of the income statement, balance sheet, and cash flow statement, detailing which statement is most useful for loan creditors and trade creditors, respectively. Furthermore, it identifies and explains the roles of auditor reports, notes to the financial statements, and management discussion and analysis (MD&A) in supplementing the financial position in annual reports. Finally, the report includes a calculation and interpretation of key financial ratios, such as net profit margin, return on assets, return on equity, current ratio, and quick ratio, using data from Smart Resort Ltd. to assess the company's financial performance and stability. Desklib offers a wide range of solved assignments and study resources for students.

Managing Financial Resources

in the Hospitality Industry

1

in the Hospitality Industry

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Main Body.......................................................................................................................................3

Question :1..................................................................................................................................3

Question 2...................................................................................................................................5

Question 3...................................................................................................................................6

Question 4...................................................................................................................................7

Question 5.................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERNCES:................................................................................................................................13

2

INTRODUCTION...........................................................................................................................3

Main Body.......................................................................................................................................3

Question :1..................................................................................................................................3

Question 2...................................................................................................................................5

Question 3...................................................................................................................................6

Question 4...................................................................................................................................7

Question 5.................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERNCES:................................................................................................................................13

2

INTRODUCTION

For a successful business it is very import to manger their financial resources. Financial

management plays a very important role for the organization to run effectively and efficiently. In

a hospitality industry the finance is directly link with their function. In each and every

department of the hotel a strong link exists between them. Financial management in the industry

includes preparing budgets, designing financial model of tracking, analysing audits and many

more. It is true in the case of hospitality industry that if they want to earn higher profits then they

need to mange their financial resources smoothly and in a productive way. A powerful financial

hospitality industry can take the business into a next stage. In short the financial resource and the

hospitality industry are the backbone of each other. This report is been prepared so that a proper

understanding could be gained that why financial management is important for proper

functioning of a hospitality industry.

Main Body

Question :1

Solution:

Generally Accepted Accounting Principle (GAAP)

GAAP is the collection of all the rules and standard that a company need to follow to maintain

their accounts. These are those principles which are used in making the financial report of any

organization((Kolomytseva, Medvedeva and Kolomiets, 2019). It was issued in the favour of

Financial Accounting Standard Board (FASB). The aim of the concept of GAAP is to provide a

clear, transparent, consistent sharing of financial information. There are total ten principles that

were adopted in GAAP.

1) Principle of Regularity 6) Principe of Periodicity

2) Principle of Sincerity 7) Principle of Non- Compensation

3) Principle of Consistency 8) Principle of utmost good faith

4) Principle of Prudence 9) Principle of Materiality

3

For a successful business it is very import to manger their financial resources. Financial

management plays a very important role for the organization to run effectively and efficiently. In

a hospitality industry the finance is directly link with their function. In each and every

department of the hotel a strong link exists between them. Financial management in the industry

includes preparing budgets, designing financial model of tracking, analysing audits and many

more. It is true in the case of hospitality industry that if they want to earn higher profits then they

need to mange their financial resources smoothly and in a productive way. A powerful financial

hospitality industry can take the business into a next stage. In short the financial resource and the

hospitality industry are the backbone of each other. This report is been prepared so that a proper

understanding could be gained that why financial management is important for proper

functioning of a hospitality industry.

Main Body

Question :1

Solution:

Generally Accepted Accounting Principle (GAAP)

GAAP is the collection of all the rules and standard that a company need to follow to maintain

their accounts. These are those principles which are used in making the financial report of any

organization((Kolomytseva, Medvedeva and Kolomiets, 2019). It was issued in the favour of

Financial Accounting Standard Board (FASB). The aim of the concept of GAAP is to provide a

clear, transparent, consistent sharing of financial information. There are total ten principles that

were adopted in GAAP.

1) Principle of Regularity 6) Principe of Periodicity

2) Principle of Sincerity 7) Principle of Non- Compensation

3) Principle of Consistency 8) Principle of utmost good faith

4) Principle of Prudence 9) Principle of Materiality

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5) Principle of Continuity 10) Principle of Permanence of methods

Various users of financial statements and the information needs by then to make decision:

Owners: They are those people of the organization who is actually incurred their capital in the

business. They are the title holder of the company. The information needed by them to make

decision is about the financial performance of the company (Sotiriadis, 2018). Information like

investment made in the company, what is the profit percentage and many more data is needed by

them to make the policies and plans according to the condition.

Customers:The person who buys the goods and services of the company for their own

consumption is called as customer. The information that they look with the help of financial

statement is that what is the company financial position i providing the product so hat there

needs and wants cab be fulfilled.

Suppliers:Suppliers are those party in the business who actually provide the raw material to the

company so that final goods and service can be manufactured. Information like the debt paying

capacity of the firm there sales margin so that they can make decision whether to supply the raw

material or not.

Managers : Managers are the people who act as an agent between the owner and the employee.

They are responsible for data to data functioning. The decision made by them is based upon the

operation(Merianos and Gotsis, 2018). They need information about the daily expenses

incurred, operational cost etc. This is required by them so that they can cut the unnecessary cost

and can attain the goal of the firm in efficient and effective manner.

Lenders:People who provide financial support to the organization is known as lender. They help

the business by granting loans. Information that they need from financial statement is debt

capacity, assets that they have to make them liquid etc.

Government :Judicial authority of the country is known as government. They need information

like shares of the company, earning before tax paid and many more so that they can charge fair

tax from the organization.

4

Various users of financial statements and the information needs by then to make decision:

Owners: They are those people of the organization who is actually incurred their capital in the

business. They are the title holder of the company. The information needed by them to make

decision is about the financial performance of the company (Sotiriadis, 2018). Information like

investment made in the company, what is the profit percentage and many more data is needed by

them to make the policies and plans according to the condition.

Customers:The person who buys the goods and services of the company for their own

consumption is called as customer. The information that they look with the help of financial

statement is that what is the company financial position i providing the product so hat there

needs and wants cab be fulfilled.

Suppliers:Suppliers are those party in the business who actually provide the raw material to the

company so that final goods and service can be manufactured. Information like the debt paying

capacity of the firm there sales margin so that they can make decision whether to supply the raw

material or not.

Managers : Managers are the people who act as an agent between the owner and the employee.

They are responsible for data to data functioning. The decision made by them is based upon the

operation(Merianos and Gotsis, 2018). They need information about the daily expenses

incurred, operational cost etc. This is required by them so that they can cut the unnecessary cost

and can attain the goal of the firm in efficient and effective manner.

Lenders:People who provide financial support to the organization is known as lender. They help

the business by granting loans. Information that they need from financial statement is debt

capacity, assets that they have to make them liquid etc.

Government :Judicial authority of the country is known as government. They need information

like shares of the company, earning before tax paid and many more so that they can charge fair

tax from the organization.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are many more users of the financial statement made by the organization rest of the users

are Competitor, Investors, Unions , Financial analyst and General public

Question 2

Solution:

Income statement is that part of the overall financial statement of the company which

shows the organization revenue and expense of a particular financial year.

Financial position helps the organization by showing the leftover assts, liabilities and equity of

the company in a specific year(Lee, 2020 )

Cash flow statement is that part of financial statement which deal with the cash and cash

equivalent. It is used to show the inflow and outflow of the cash and cash equivalent.

Out of the three which one is good for:

a) A loan creditor:

A loan creditor is that person who provides financial support to the company by granting

loans. They help the organization by providing monetary support. Out of the three

financial statements the loan creditor is much more concerned in seeing the balance

sheet of the company. It is because it provides the overall performance of the company’s

assets, liability and the equity. Financial position of the company is actually seeing by

looking in it(Clikeman, 2019). It shows a detailed summary in terms of short term and

long term resources that company had. It is used by the loaner so that a proper analysis is

made that if they should grant loan or not. And if they are granting the loan then what

will be the time period in which there amount can be recovered. Before providing the

loan by the creditor they see that which asset they can use as a mortgage to recover their

amount. It also shoe that what companies hold within the organization and what are the

liabilities that they are need to pay. It also provides a insights to the equity side. The

shares the organization has, there market rate and many more.

b) A trade creditor:

Trade creditors are the account payable of the organization. They are those people to whom

the company needs to pay the amount for the purchase that they made. The financial

statement in which they are more interested is the income statement. The account payable

5

are Competitor, Investors, Unions , Financial analyst and General public

Question 2

Solution:

Income statement is that part of the overall financial statement of the company which

shows the organization revenue and expense of a particular financial year.

Financial position helps the organization by showing the leftover assts, liabilities and equity of

the company in a specific year(Lee, 2020 )

Cash flow statement is that part of financial statement which deal with the cash and cash

equivalent. It is used to show the inflow and outflow of the cash and cash equivalent.

Out of the three which one is good for:

a) A loan creditor:

A loan creditor is that person who provides financial support to the company by granting

loans. They help the organization by providing monetary support. Out of the three

financial statements the loan creditor is much more concerned in seeing the balance

sheet of the company. It is because it provides the overall performance of the company’s

assets, liability and the equity. Financial position of the company is actually seeing by

looking in it(Clikeman, 2019). It shows a detailed summary in terms of short term and

long term resources that company had. It is used by the loaner so that a proper analysis is

made that if they should grant loan or not. And if they are granting the loan then what

will be the time period in which there amount can be recovered. Before providing the

loan by the creditor they see that which asset they can use as a mortgage to recover their

amount. It also shoe that what companies hold within the organization and what are the

liabilities that they are need to pay. It also provides a insights to the equity side. The

shares the organization has, there market rate and many more.

b) A trade creditor:

Trade creditors are the account payable of the organization. They are those people to whom

the company needs to pay the amount for the purchase that they made. The financial

statement in which they are more interested is the income statement. The account payable

5

is more found to see this because through this they can found the debt paying capacity of

the firm. Inn income statement company income and expenses are recorded and the traders

are more interested in seeing the revenue the company earns in a single financial

year(Aifuwa and Saidu, 2020 ). This is useful because by seeing this they can make the

prediction that whether they should supply raw material to the company or not. This is

done so that they can be sure that amount can be recovered within the year. Trade creditor

analysis the income statement very deeply so that they can be sure that the company hold

enough income to pay their purchase amount. One of the most important usefulness of this

is that it help them to know the past paying capacity of the business.

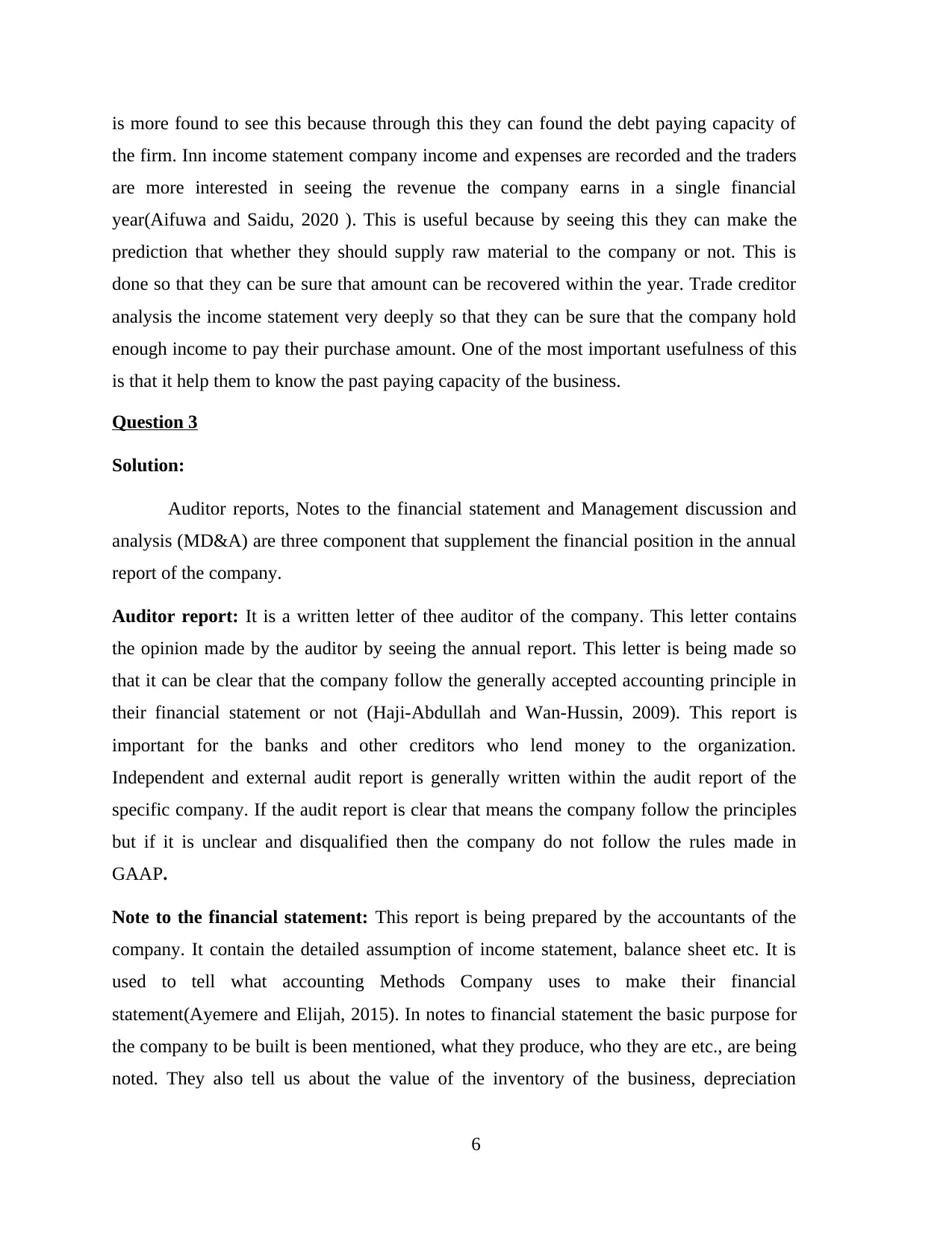

Question 3

Solution:

Auditor reports, Notes to the financial statement and Management discussion and

analysis (MD&A) are three component that supplement the financial position in the annual

report of the company.

Auditor report: It is a written letter of thee auditor of the company. This letter contains

the opinion made by the auditor by seeing the annual report. This letter is being made so

that it can be clear that the company follow the generally accepted accounting principle in

their financial statement or not (Haji-Abdullah and Wan-Hussin, 2009). This report is

important for the banks and other creditors who lend money to the organization.

Independent and external audit report is generally written within the audit report of the

specific company. If the audit report is clear that means the company follow the principles

but if it is unclear and disqualified then the company do not follow the rules made in

GAAP.

Note to the financial statement: This report is being prepared by the accountants of the

company. It contain the detailed assumption of income statement, balance sheet etc. It is

used to tell what accounting Methods Company uses to make their financial

statement(Ayemere and Elijah, 2015). In notes to financial statement the basic purpose for

the company to be built is been mentioned, what they produce, who they are etc., are being

noted. They also tell us about the value of the inventory of the business, depreciation

6

the firm. Inn income statement company income and expenses are recorded and the traders

are more interested in seeing the revenue the company earns in a single financial

year(Aifuwa and Saidu, 2020 ). This is useful because by seeing this they can make the

prediction that whether they should supply raw material to the company or not. This is

done so that they can be sure that amount can be recovered within the year. Trade creditor

analysis the income statement very deeply so that they can be sure that the company hold

enough income to pay their purchase amount. One of the most important usefulness of this

is that it help them to know the past paying capacity of the business.

Question 3

Solution:

Auditor reports, Notes to the financial statement and Management discussion and

analysis (MD&A) are three component that supplement the financial position in the annual

report of the company.

Auditor report: It is a written letter of thee auditor of the company. This letter contains

the opinion made by the auditor by seeing the annual report. This letter is being made so

that it can be clear that the company follow the generally accepted accounting principle in

their financial statement or not (Haji-Abdullah and Wan-Hussin, 2009). This report is

important for the banks and other creditors who lend money to the organization.

Independent and external audit report is generally written within the audit report of the

specific company. If the audit report is clear that means the company follow the principles

but if it is unclear and disqualified then the company do not follow the rules made in

GAAP.

Note to the financial statement: This report is being prepared by the accountants of the

company. It contain the detailed assumption of income statement, balance sheet etc. It is

used to tell what accounting Methods Company uses to make their financial

statement(Ayemere and Elijah, 2015). In notes to financial statement the basic purpose for

the company to be built is been mentioned, what they produce, who they are etc., are being

noted. They also tell us about the value of the inventory of the business, depreciation

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

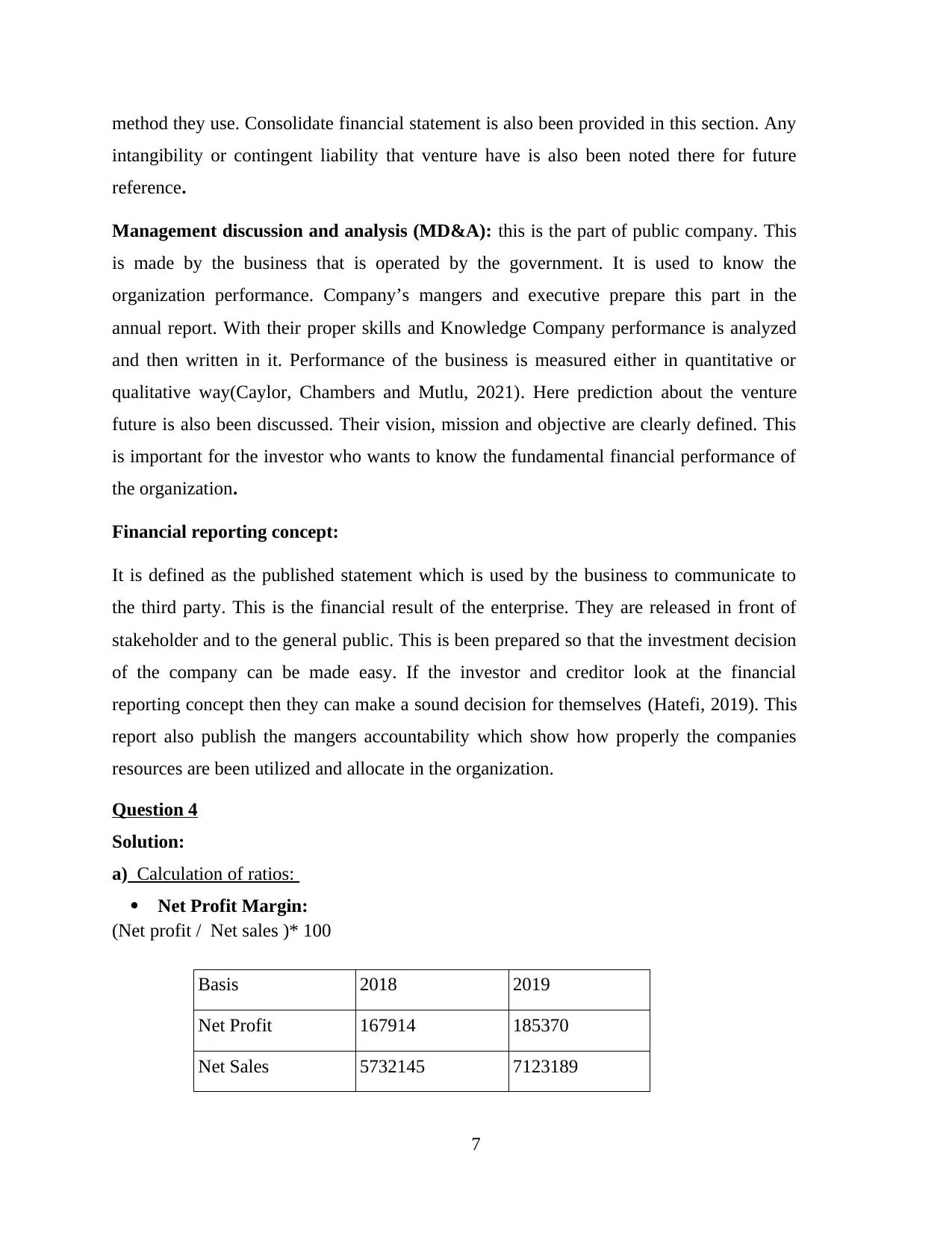

method they use. Consolidate financial statement is also been provided in this section. Any

intangibility or contingent liability that venture have is also been noted there for future

reference.

Management discussion and analysis (MD&A): this is the part of public company. This

is made by the business that is operated by the government. It is used to know the

organization performance. Company’s mangers and executive prepare this part in the

annual report. With their proper skills and Knowledge Company performance is analyzed

and then written in it. Performance of the business is measured either in quantitative or

qualitative way(Caylor, Chambers and Mutlu, 2021). Here prediction about the venture

future is also been discussed. Their vision, mission and objective are clearly defined. This

is important for the investor who wants to know the fundamental financial performance of

the organization.

Financial reporting concept:

It is defined as the published statement which is used by the business to communicate to

the third party. This is the financial result of the enterprise. They are released in front of

stakeholder and to the general public. This is been prepared so that the investment decision

of the company can be made easy. If the investor and creditor look at the financial

reporting concept then they can make a sound decision for themselves (Hatefi, 2019). This

report also publish the mangers accountability which show how properly the companies

resources are been utilized and allocate in the organization.

Question 4

Solution:

a) Calculation of ratios:

Net Profit Margin:

(Net profit / Net sales )* 100

Basis 2018 2019

Net Profit 167914 185370

Net Sales 5732145 7123189

7

intangibility or contingent liability that venture have is also been noted there for future

reference.

Management discussion and analysis (MD&A): this is the part of public company. This

is made by the business that is operated by the government. It is used to know the

organization performance. Company’s mangers and executive prepare this part in the

annual report. With their proper skills and Knowledge Company performance is analyzed

and then written in it. Performance of the business is measured either in quantitative or

qualitative way(Caylor, Chambers and Mutlu, 2021). Here prediction about the venture

future is also been discussed. Their vision, mission and objective are clearly defined. This

is important for the investor who wants to know the fundamental financial performance of

the organization.

Financial reporting concept:

It is defined as the published statement which is used by the business to communicate to

the third party. This is the financial result of the enterprise. They are released in front of

stakeholder and to the general public. This is been prepared so that the investment decision

of the company can be made easy. If the investor and creditor look at the financial

reporting concept then they can make a sound decision for themselves (Hatefi, 2019). This

report also publish the mangers accountability which show how properly the companies

resources are been utilized and allocate in the organization.

Question 4

Solution:

a) Calculation of ratios:

Net Profit Margin:

(Net profit / Net sales )* 100

Basis 2018 2019

Net Profit 167914 185370

Net Sales 5732145 7123189

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

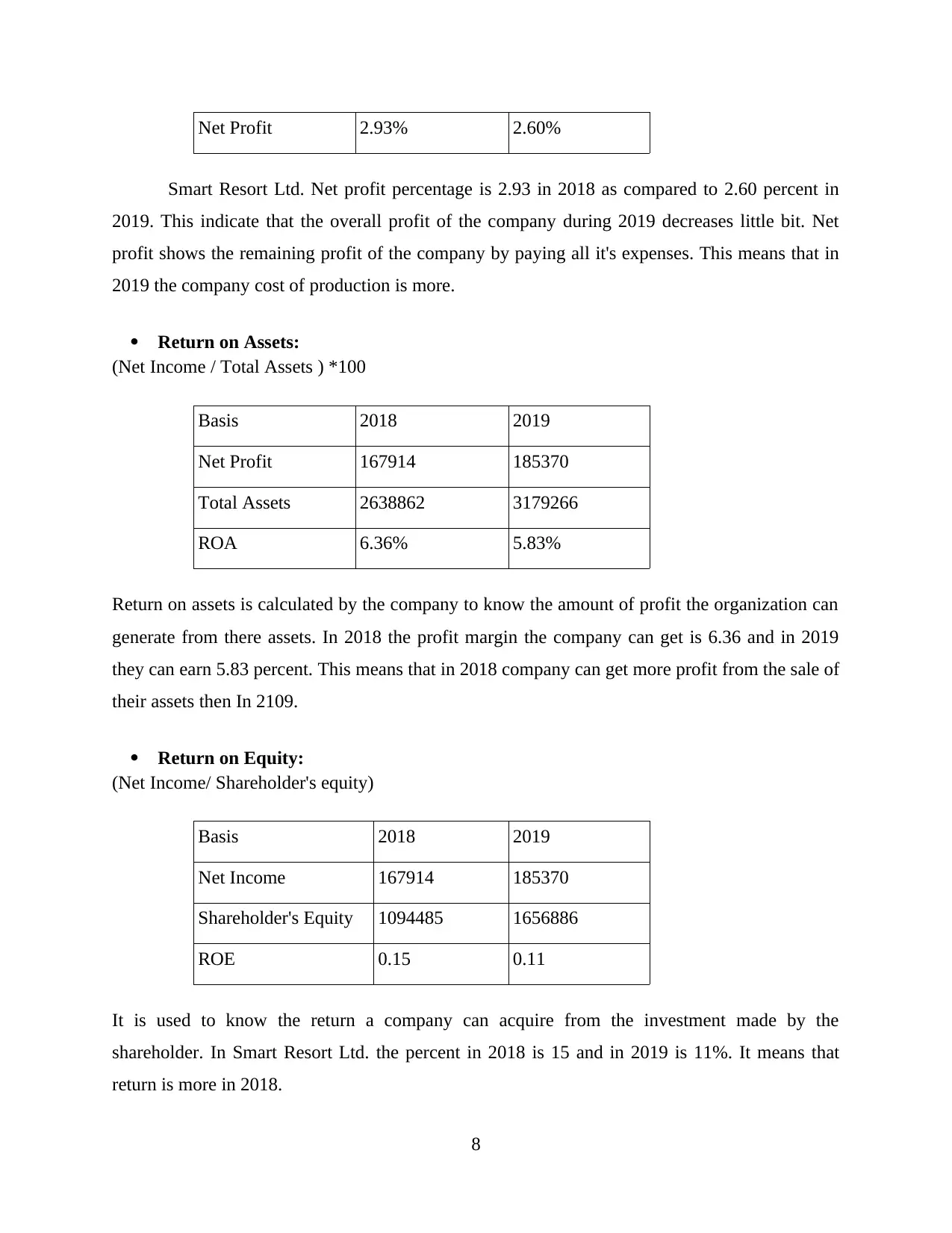

Net Profit 2.93% 2.60%

Smart Resort Ltd. Net profit percentage is 2.93 in 2018 as compared to 2.60 percent in

2019. This indicate that the overall profit of the company during 2019 decreases little bit. Net

profit shows the remaining profit of the company by paying all it's expenses. This means that in

2019 the company cost of production is more.

Return on Assets:

(Net Income / Total Assets ) *100

Basis 2018 2019

Net Profit 167914 185370

Total Assets 2638862 3179266

ROA 6.36% 5.83%

Return on assets is calculated by the company to know the amount of profit the organization can

generate from there assets. In 2018 the profit margin the company can get is 6.36 and in 2019

they can earn 5.83 percent. This means that in 2018 company can get more profit from the sale of

their assets then In 2109.

Return on Equity:

(Net Income/ Shareholder's equity)

Basis 2018 2019

Net Income 167914 185370

Shareholder's Equity 1094485 1656886

ROE 0.15 0.11

It is used to know the return a company can acquire from the investment made by the

shareholder. In Smart Resort Ltd. the percent in 2018 is 15 and in 2019 is 11%. It means that

return is more in 2018.

8

Smart Resort Ltd. Net profit percentage is 2.93 in 2018 as compared to 2.60 percent in

2019. This indicate that the overall profit of the company during 2019 decreases little bit. Net

profit shows the remaining profit of the company by paying all it's expenses. This means that in

2019 the company cost of production is more.

Return on Assets:

(Net Income / Total Assets ) *100

Basis 2018 2019

Net Profit 167914 185370

Total Assets 2638862 3179266

ROA 6.36% 5.83%

Return on assets is calculated by the company to know the amount of profit the organization can

generate from there assets. In 2018 the profit margin the company can get is 6.36 and in 2019

they can earn 5.83 percent. This means that in 2018 company can get more profit from the sale of

their assets then In 2109.

Return on Equity:

(Net Income/ Shareholder's equity)

Basis 2018 2019

Net Income 167914 185370

Shareholder's Equity 1094485 1656886

ROE 0.15 0.11

It is used to know the return a company can acquire from the investment made by the

shareholder. In Smart Resort Ltd. the percent in 2018 is 15 and in 2019 is 11%. It means that

return is more in 2018.

8

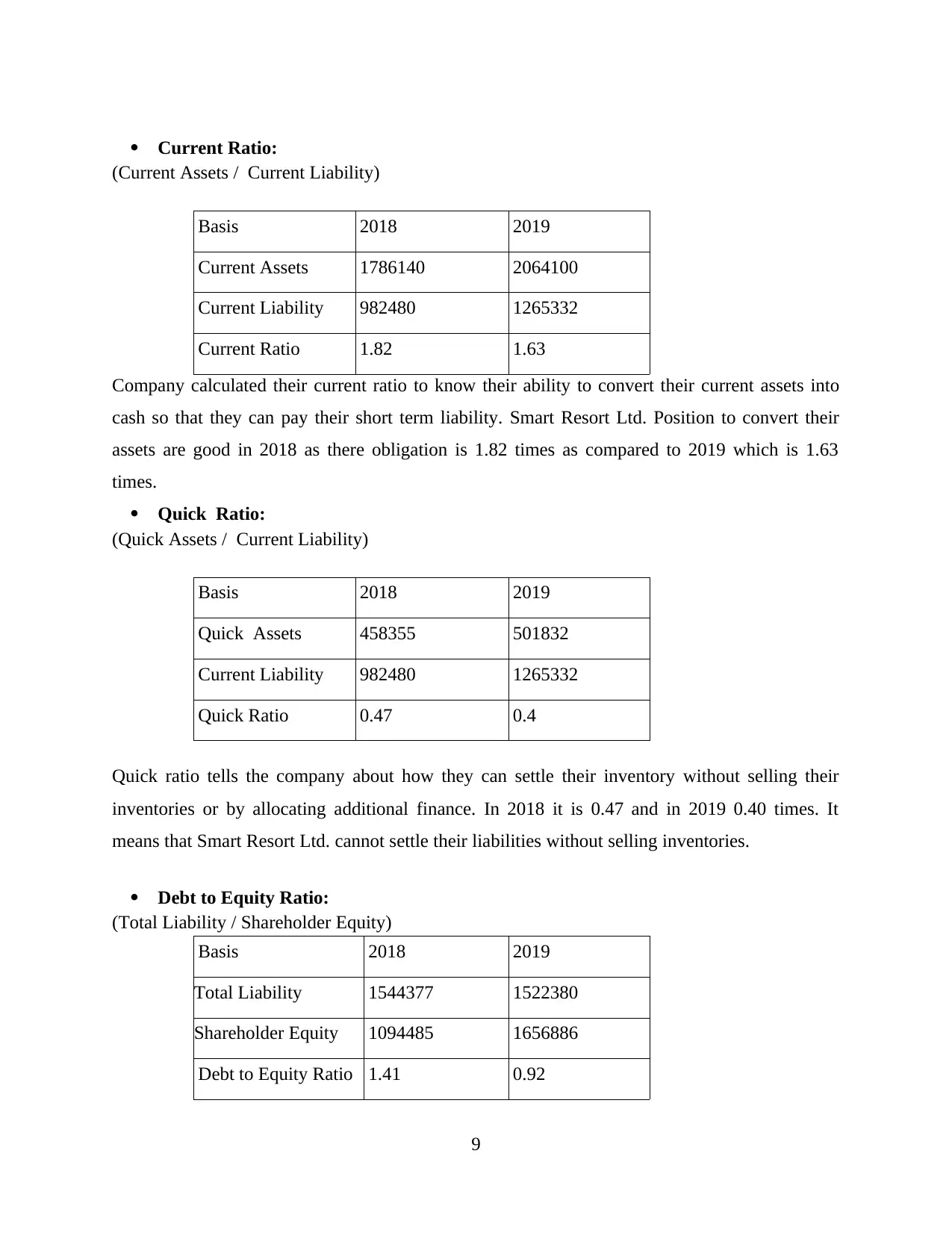

Current Ratio:

(Current Assets / Current Liability)

Basis 2018 2019

Current Assets 1786140 2064100

Current Liability 982480 1265332

Current Ratio 1.82 1.63

Company calculated their current ratio to know their ability to convert their current assets into

cash so that they can pay their short term liability. Smart Resort Ltd. Position to convert their

assets are good in 2018 as there obligation is 1.82 times as compared to 2019 which is 1.63

times.

Quick Ratio:

(Quick Assets / Current Liability)

Basis 2018 2019

Quick Assets 458355 501832

Current Liability 982480 1265332

Quick Ratio 0.47 0.4

Quick ratio tells the company about how they can settle their inventory without selling their

inventories or by allocating additional finance. In 2018 it is 0.47 and in 2019 0.40 times. It

means that Smart Resort Ltd. cannot settle their liabilities without selling inventories.

Debt to Equity Ratio:

(Total Liability / Shareholder Equity)

Basis 2018 2019

Total Liability 1544377 1522380

Shareholder Equity 1094485 1656886

Debt to Equity Ratio 1.41 0.92

9

(Current Assets / Current Liability)

Basis 2018 2019

Current Assets 1786140 2064100

Current Liability 982480 1265332

Current Ratio 1.82 1.63

Company calculated their current ratio to know their ability to convert their current assets into

cash so that they can pay their short term liability. Smart Resort Ltd. Position to convert their

assets are good in 2018 as there obligation is 1.82 times as compared to 2019 which is 1.63

times.

Quick Ratio:

(Quick Assets / Current Liability)

Basis 2018 2019

Quick Assets 458355 501832

Current Liability 982480 1265332

Quick Ratio 0.47 0.4

Quick ratio tells the company about how they can settle their inventory without selling their

inventories or by allocating additional finance. In 2018 it is 0.47 and in 2019 0.40 times. It

means that Smart Resort Ltd. cannot settle their liabilities without selling inventories.

Debt to Equity Ratio:

(Total Liability / Shareholder Equity)

Basis 2018 2019

Total Liability 1544377 1522380

Shareholder Equity 1094485 1656886

Debt to Equity Ratio 1.41 0.92

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

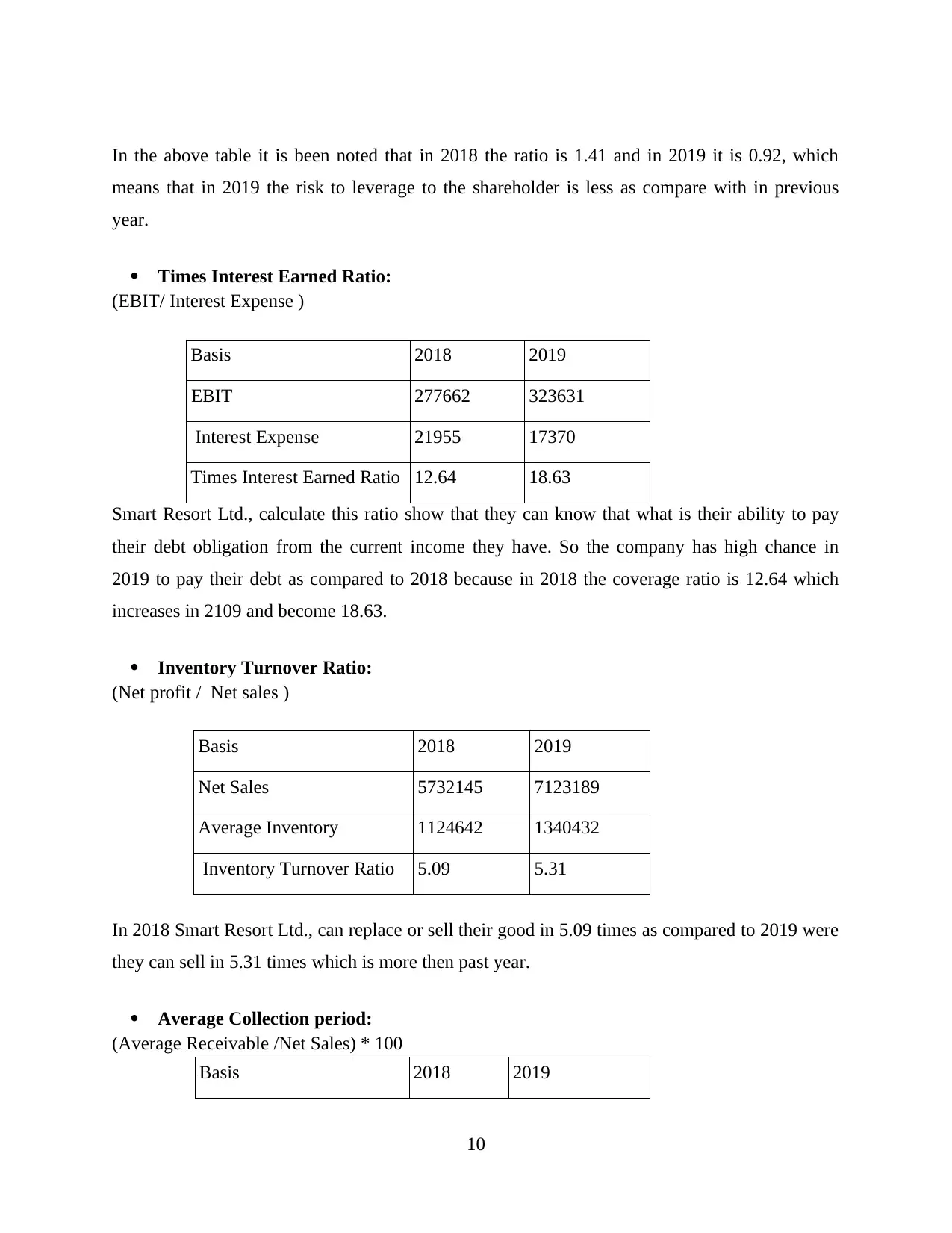

In the above table it is been noted that in 2018 the ratio is 1.41 and in 2019 it is 0.92, which

means that in 2019 the risk to leverage to the shareholder is less as compare with in previous

year.

Times Interest Earned Ratio:

(EBIT/ Interest Expense )

Basis 2018 2019

EBIT 277662 323631

Interest Expense 21955 17370

Times Interest Earned Ratio 12.64 18.63

Smart Resort Ltd., calculate this ratio show that they can know that what is their ability to pay

their debt obligation from the current income they have. So the company has high chance in

2019 to pay their debt as compared to 2018 because in 2018 the coverage ratio is 12.64 which

increases in 2109 and become 18.63.

Inventory Turnover Ratio:

(Net profit / Net sales )

Basis 2018 2019

Net Sales 5732145 7123189

Average Inventory 1124642 1340432

Inventory Turnover Ratio 5.09 5.31

In 2018 Smart Resort Ltd., can replace or sell their good in 5.09 times as compared to 2019 were

they can sell in 5.31 times which is more then past year.

Average Collection period:

(Average Receivable /Net Sales) * 100

Basis 2018 2019

10

means that in 2019 the risk to leverage to the shareholder is less as compare with in previous

year.

Times Interest Earned Ratio:

(EBIT/ Interest Expense )

Basis 2018 2019

EBIT 277662 323631

Interest Expense 21955 17370

Times Interest Earned Ratio 12.64 18.63

Smart Resort Ltd., calculate this ratio show that they can know that what is their ability to pay

their debt obligation from the current income they have. So the company has high chance in

2019 to pay their debt as compared to 2018 because in 2018 the coverage ratio is 12.64 which

increases in 2109 and become 18.63.

Inventory Turnover Ratio:

(Net profit / Net sales )

Basis 2018 2019

Net Sales 5732145 7123189

Average Inventory 1124642 1340432

Inventory Turnover Ratio 5.09 5.31

In 2018 Smart Resort Ltd., can replace or sell their good in 5.09 times as compared to 2019 were

they can sell in 5.31 times which is more then past year.

Average Collection period:

(Average Receivable /Net Sales) * 100

Basis 2018 2019

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

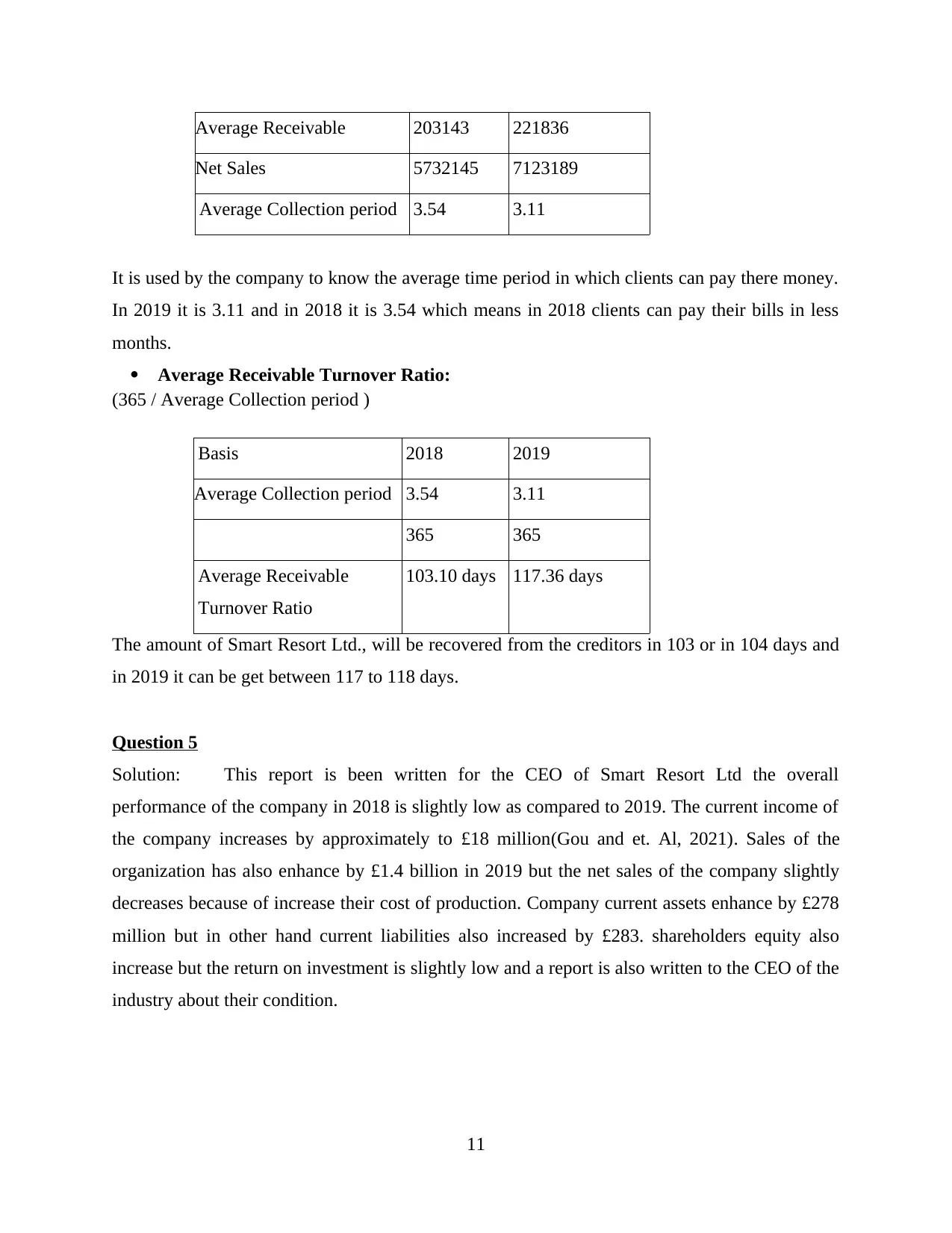

Average Receivable 203143 221836

Net Sales 5732145 7123189

Average Collection period 3.54 3.11

It is used by the company to know the average time period in which clients can pay there money.

In 2019 it is 3.11 and in 2018 it is 3.54 which means in 2018 clients can pay their bills in less

months.

Average Receivable Turnover Ratio:

(365 / Average Collection period )

Basis 2018 2019

Average Collection period 3.54 3.11

365 365

Average Receivable

Turnover Ratio

103.10 days 117.36 days

The amount of Smart Resort Ltd., will be recovered from the creditors in 103 or in 104 days and

in 2019 it can be get between 117 to 118 days.

Question 5

Solution: This report is been written for the CEO of Smart Resort Ltd the overall

performance of the company in 2018 is slightly low as compared to 2019. The current income of

the company increases by approximately to £18 million(Gou and et. Al, 2021). Sales of the

organization has also enhance by £1.4 billion in 2019 but the net sales of the company slightly

decreases because of increase their cost of production. Company current assets enhance by £278

million but in other hand current liabilities also increased by £283. shareholders equity also

increase but the return on investment is slightly low and a report is also written to the CEO of the

industry about their condition.

11

Net Sales 5732145 7123189

Average Collection period 3.54 3.11

It is used by the company to know the average time period in which clients can pay there money.

In 2019 it is 3.11 and in 2018 it is 3.54 which means in 2018 clients can pay their bills in less

months.

Average Receivable Turnover Ratio:

(365 / Average Collection period )

Basis 2018 2019

Average Collection period 3.54 3.11

365 365

Average Receivable

Turnover Ratio

103.10 days 117.36 days

The amount of Smart Resort Ltd., will be recovered from the creditors in 103 or in 104 days and

in 2019 it can be get between 117 to 118 days.

Question 5

Solution: This report is been written for the CEO of Smart Resort Ltd the overall

performance of the company in 2018 is slightly low as compared to 2019. The current income of

the company increases by approximately to £18 million(Gou and et. Al, 2021). Sales of the

organization has also enhance by £1.4 billion in 2019 but the net sales of the company slightly

decreases because of increase their cost of production. Company current assets enhance by £278

million but in other hand current liabilities also increased by £283. shareholders equity also

increase but the return on investment is slightly low and a report is also written to the CEO of the

industry about their condition.

11

CONCLUSION

From the above report it is been concluded that financial resources plays important role in

hospitality industry. The company need to proper analyse and make their accounts clear with

using all the rules and principles that are being adopted by GAPP. The various decision maker

like government, employee, owner and many more are interested in knowing financial statement.

In this report the different ratio of Sara resort Ltd is also being identify so that company can

know what current assets current liabilities and equity they hold in 2019 as compared to 2018.

12

From the above report it is been concluded that financial resources plays important role in

hospitality industry. The company need to proper analyse and make their accounts clear with

using all the rules and principles that are being adopted by GAPP. The various decision maker

like government, employee, owner and many more are interested in knowing financial statement.

In this report the different ratio of Sara resort Ltd is also being identify so that company can

know what current assets current liabilities and equity they hold in 2019 as compared to 2018.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.