Finance in Hospitality: Funding, Cost Control, Budgeting, and Analysis

VerifiedAdded on 2020/07/23

|17

|4908

|27

Report

AI Summary

This report comprehensively examines financial management within the hospitality sector, focusing on key areas such as sources of funding for new and existing businesses, including personal investment, venture capital, and bank loans. It analyzes various methods of generating income like sales promotion and sub-letting. The report delves into cost elements, including material, labor, and overhead, along with methods for controlling stock and cash. Budgeting techniques, trial balance structures, and evaluation of budget variances are also discussed. Furthermore, it includes the calculation of financial ratios for Belgravia Hotels, providing recommendations for future management strategies and determining issues associated with performance through break-even analysis. The report also provides an overview of the contribution per unit and justification of short term management decisions. The report covers the importance of financial management, the various methods of managing finances, and the importance of maintaining books of accounts for efficient business management.

Finance in Hospitality

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1Sources of funding to new and existing business...................................................................1

1.2 Contribution of different methods for the purpose of generating income............................3

M1: Effective approaches to determine sources of finance........................................................3

D1: Range of various methods of generating income.................................................................3

TASK 2............................................................................................................................................4

2.1 Cost.......................................................................................................................................4

2.2 Methods of controlling stock and cash..................................................................................5

M2: Relevant theories and techniques of setting prices..............................................................5

D2: Critical evaluation to have planned, manage and organise a number of activities..............5

TASK 3............................................................................................................................................6

3.1 Source and Structure of Trial Balance..................................................................................6

3.2: Evaluation of budget account ..............................................................................................6

3.3 Process and Purpose of Budgetary Control...........................................................................8

3.4: Evaluating budget variances................................................................................................9

M3: Structure and approaches to assess the trail balance.........................................................10

TASK 4..........................................................................................................................................11

4.1: Calculation of different ratios of Belgravia Hotels............................................................11

4.2: Recommendation about future management strategies.....................................................12

TASK 5..........................................................................................................................................12

5.1: Classification of various types of costs..............................................................................12

5.2: Contribution per unit..........................................................................................................13

5.3: Justification of short term management decision...............................................................13

D3: Determining issues associated with performance by BEP analysis...................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1Sources of funding to new and existing business...................................................................1

1.2 Contribution of different methods for the purpose of generating income............................3

M1: Effective approaches to determine sources of finance........................................................3

D1: Range of various methods of generating income.................................................................3

TASK 2............................................................................................................................................4

2.1 Cost.......................................................................................................................................4

2.2 Methods of controlling stock and cash..................................................................................5

M2: Relevant theories and techniques of setting prices..............................................................5

D2: Critical evaluation to have planned, manage and organise a number of activities..............5

TASK 3............................................................................................................................................6

3.1 Source and Structure of Trial Balance..................................................................................6

3.2: Evaluation of budget account ..............................................................................................6

3.3 Process and Purpose of Budgetary Control...........................................................................8

3.4: Evaluating budget variances................................................................................................9

M3: Structure and approaches to assess the trail balance.........................................................10

TASK 4..........................................................................................................................................11

4.1: Calculation of different ratios of Belgravia Hotels............................................................11

4.2: Recommendation about future management strategies.....................................................12

TASK 5..........................................................................................................................................12

5.1: Classification of various types of costs..............................................................................12

5.2: Contribution per unit..........................................................................................................13

5.3: Justification of short term management decision...............................................................13

D3: Determining issues associated with performance by BEP analysis...................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Every business requires proper maintenance of accounts as well finance of the company

there are various methods that are being used by the company for the purpose of managing

finance. Hospitality sector is one of the fastest growing sectors and the need of managing finance

in this sector is growing quite rapidly (Jones, Hillier and Comfort, 2016). Some of the methods

of managing finances would include budgetary control, cash control, etc. Proper maintenance of

books of accounts is also important for making sure that business is managed efficiently.

Belgravia Hotels is well known company in the in Hospitality industry and is growing rapidly

due to demand from tourists and customers in this regard. It is necessary for the company to

manage its books of accounts efficiently so that business can be taken ahead to reach to its full

potential.

TASK 1

1.1Sources of funding to new and existing business

There are large numbers of sources through which a firm can raise funds for the purpose

of raising its business, these are described as follows:

New business

Personal investment: it is basically investment, which are being made by the owner himself in

the company the risk involved in this kind of capital is very low.

Advantages

It is a good sign if owner puts his own capital in the business, it gives a good message to

bankers and venture capital list that the owner himself are ready to put his money at risk

and believe in his idea.

The owner will put his best possible efforts for growing it’s business as his own capital is at risk

(Martínez, Pérez and Rodríguez del Bosque, 2013).

Disadvantages One of the disadvantage can be that there might be a lack of professional advice for

investment.

Venture Capital: It is the kind of private which is provided to small businessIn order to earn

huge profit but at the same time involves a lot of risk. Usually a venture capital list would invest

1

Every business requires proper maintenance of accounts as well finance of the company

there are various methods that are being used by the company for the purpose of managing

finance. Hospitality sector is one of the fastest growing sectors and the need of managing finance

in this sector is growing quite rapidly (Jones, Hillier and Comfort, 2016). Some of the methods

of managing finances would include budgetary control, cash control, etc. Proper maintenance of

books of accounts is also important for making sure that business is managed efficiently.

Belgravia Hotels is well known company in the in Hospitality industry and is growing rapidly

due to demand from tourists and customers in this regard. It is necessary for the company to

manage its books of accounts efficiently so that business can be taken ahead to reach to its full

potential.

TASK 1

1.1Sources of funding to new and existing business

There are large numbers of sources through which a firm can raise funds for the purpose

of raising its business, these are described as follows:

New business

Personal investment: it is basically investment, which are being made by the owner himself in

the company the risk involved in this kind of capital is very low.

Advantages

It is a good sign if owner puts his own capital in the business, it gives a good message to

bankers and venture capital list that the owner himself are ready to put his money at risk

and believe in his idea.

The owner will put his best possible efforts for growing it’s business as his own capital is at risk

(Martínez, Pérez and Rodríguez del Bosque, 2013).

Disadvantages One of the disadvantage can be that there might be a lack of professional advice for

investment.

Venture Capital: It is the kind of private which is provided to small businessIn order to earn

huge profit but at the same time involves a lot of risk. Usually a venture capital list would invest

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in small and medium business and will hold necessary percentage of share in the firm but the

ultimate owner remains the entrepreneur (McManus, 2013).

Advantages

Guess the entrepreneur and initially start to take his business forward and build it in a

strong manner. Necessary resources can be arranged with the capital which is infused by

the venture capital list. It comes with no cost of capital as there is no interest that has to be paid on this capital

Disadvantage.

The control over company is lost by the entrepreneur as most of the stake would belong to

Venture capitalist (Campo, Díaz and Yagüe, 2014).

Already Established Business

Bank Loan: It is one of the most important and easy way of raising funds for small and

medium size business. They just have to apply to any commercial bank for raising funds in the

bank will give loans on the basis of eligibility of the consent business.

Advantages

It is an easy way of raising funds and there is minimum paperwork involved. The company do not have to share profits with those for provided funds and just have to

pay a fixed amount of interest.

Disadvantages

The business might have to pay interest which will be a liability for the company and

will reduce profits.

Debenture: It is issued by the company to general public to raise funds. It is the liability of the

company and the company will have to pay a particular date of interest to the debenture holders,

irrespective of the fact whether company is generating profits or not (Singh., 2016 ).

Advantages

The company will not have to share profits with dementia holders. Will give necessary

funds for expansion of Management. Control is not delegate to people for giving funds.

Retained Earnings: It is basically accumulated profits that are earned by company over

period of time. It does not involve any cost and it is your profits that earned by company through

its operations.

2

ultimate owner remains the entrepreneur (McManus, 2013).

Advantages

Guess the entrepreneur and initially start to take his business forward and build it in a

strong manner. Necessary resources can be arranged with the capital which is infused by

the venture capital list. It comes with no cost of capital as there is no interest that has to be paid on this capital

Disadvantage.

The control over company is lost by the entrepreneur as most of the stake would belong to

Venture capitalist (Campo, Díaz and Yagüe, 2014).

Already Established Business

Bank Loan: It is one of the most important and easy way of raising funds for small and

medium size business. They just have to apply to any commercial bank for raising funds in the

bank will give loans on the basis of eligibility of the consent business.

Advantages

It is an easy way of raising funds and there is minimum paperwork involved. The company do not have to share profits with those for provided funds and just have to

pay a fixed amount of interest.

Disadvantages

The business might have to pay interest which will be a liability for the company and

will reduce profits.

Debenture: It is issued by the company to general public to raise funds. It is the liability of the

company and the company will have to pay a particular date of interest to the debenture holders,

irrespective of the fact whether company is generating profits or not (Singh., 2016 ).

Advantages

The company will not have to share profits with dementia holders. Will give necessary

funds for expansion of Management. Control is not delegate to people for giving funds.

Retained Earnings: It is basically accumulated profits that are earned by company over

period of time. It does not involve any cost and it is your profits that earned by company through

its operations.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages It can help in providing stability to business.

Disadvantages

One of the biggest disadvantage is that it may lead to improper utilisation of funds.

1.2 Contribution of different methods for the purpose of generating income

There are radius methods which could help a business to earn profits and generating

income from its operations in an affective way, some of these methods are discussed

below:

Sales Promotion: under this, the company try to promote its products through various

measures of sales like door-to-door selling, television and newspaper advertising etc.

Sub Letting: it is yet another method of generating income, under this the company will

give its property or assets to another user for the purpose of using it and in return the company

would be getting a rent. This can complement the income sources of company and may help it in

generating more profits.

Sponsorship: Under this, company or a business will provide support to any activity that

would be taking place within the area or in the city and by doing this it will be able to market the

name of company or its products. The support can be monetary or non-monetary.

M1: Effective approaches to determine sources of finance

From all the above mentioned various sources of finance available to hospitality sectors

are discussed. Out of which there are some of them are more effective or beneficial for them in

near future. Retain earning can assist them to make expansion for increasing size of the business.

Loan is another great option of raising funds and can available to business in much easily. They

are beneficial for them to plan their operations in effective manner.

D1: Range of various methods of generating income

It has been seen that there are wide range of modes from which income can be generated

for conducting an effective business plan for an organisation. Commission is said to be crucial

aspects which would be retain from outside parties or suppliers to manage and operate internal

and external department of an organisation. With the help of government grant company can

easily be able to manage and regulate their operations in more effective ways in near future time.

3

Disadvantages

One of the biggest disadvantage is that it may lead to improper utilisation of funds.

1.2 Contribution of different methods for the purpose of generating income

There are radius methods which could help a business to earn profits and generating

income from its operations in an affective way, some of these methods are discussed

below:

Sales Promotion: under this, the company try to promote its products through various

measures of sales like door-to-door selling, television and newspaper advertising etc.

Sub Letting: it is yet another method of generating income, under this the company will

give its property or assets to another user for the purpose of using it and in return the company

would be getting a rent. This can complement the income sources of company and may help it in

generating more profits.

Sponsorship: Under this, company or a business will provide support to any activity that

would be taking place within the area or in the city and by doing this it will be able to market the

name of company or its products. The support can be monetary or non-monetary.

M1: Effective approaches to determine sources of finance

From all the above mentioned various sources of finance available to hospitality sectors

are discussed. Out of which there are some of them are more effective or beneficial for them in

near future. Retain earning can assist them to make expansion for increasing size of the business.

Loan is another great option of raising funds and can available to business in much easily. They

are beneficial for them to plan their operations in effective manner.

D1: Range of various methods of generating income

It has been seen that there are wide range of modes from which income can be generated

for conducting an effective business plan for an organisation. Commission is said to be crucial

aspects which would be retain from outside parties or suppliers to manage and operate internal

and external department of an organisation. With the help of government grant company can

easily be able to manage and regulate their operations in more effective ways in near future time.

3

TASK 2

2.1 Cost

(a)Elements of Cost

Cost: It is an amount which is spent by the company in the process of producing goods and

services. This can take form of raw material, labour, overheads etc.

Some of the main elements of cost discussed as follows:

Material: it refers to the material, which are being used for the purpose of producing goods. It

can be of two types direct material and indirect material. Direct material are those which can be

ascertained by looking at the product itself and indirect material are those which are ancillary in

production of a product cannot be ascertained by looking at product (Ndoda, 2013). Labour: these are the manpower of the company it involves employees.workers,

management etc. they are the one who are responsible for taking the Company forward.

The amount paid to labours by the company are recorded as wages in the books.

Overhead: it refers to any extra expenditure that might have acquired by the company on

production of a product or service except raw material and labour cost. It can be further

sub-classified into various cost like:

-Production Expenses

-Selling and overheads expenses

-Administrative Expenses

-Distribution Expenses

(b) Gross profit percentage as well as selling Price

Gross Profit percentages: It is the ratio which describes the relationship of a company’s

gross profit as percentage of sales. A gross profit tells about company’s profit from operations. It

helps company in making comparison of profits of two organisations (Guerrier, 2013).

Gross Profit Percentage = Gross Profit/ Total sales*100

Selling price+COGS+MARKUP

In order to arrive at net profit which are being earned by the company, it will have to deduct all

its operational expenses from gross profit. The net profit is the ultimate profit that goes to the

reserve of company.

4

2.1 Cost

(a)Elements of Cost

Cost: It is an amount which is spent by the company in the process of producing goods and

services. This can take form of raw material, labour, overheads etc.

Some of the main elements of cost discussed as follows:

Material: it refers to the material, which are being used for the purpose of producing goods. It

can be of two types direct material and indirect material. Direct material are those which can be

ascertained by looking at the product itself and indirect material are those which are ancillary in

production of a product cannot be ascertained by looking at product (Ndoda, 2013). Labour: these are the manpower of the company it involves employees.workers,

management etc. they are the one who are responsible for taking the Company forward.

The amount paid to labours by the company are recorded as wages in the books.

Overhead: it refers to any extra expenditure that might have acquired by the company on

production of a product or service except raw material and labour cost. It can be further

sub-classified into various cost like:

-Production Expenses

-Selling and overheads expenses

-Administrative Expenses

-Distribution Expenses

(b) Gross profit percentage as well as selling Price

Gross Profit percentages: It is the ratio which describes the relationship of a company’s

gross profit as percentage of sales. A gross profit tells about company’s profit from operations. It

helps company in making comparison of profits of two organisations (Guerrier, 2013).

Gross Profit Percentage = Gross Profit/ Total sales*100

Selling price+COGS+MARKUP

In order to arrive at net profit which are being earned by the company, it will have to deduct all

its operational expenses from gross profit. The net profit is the ultimate profit that goes to the

reserve of company.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.2 Methods of controlling stock and cash

Cash Control Method Implementation of efficient cash handling strategies: Under this, a organisation would

frame necessary policies and strategies which would help in maintenance of adequate

cash level within the organisation. Accountability Form: It means preparation of cash accounting forms which will further

improves companies profits and will enable it to overcome from looses. Setting up of Cash Flow Target: It involves forecasting the various requirements of cash

in an organisation for effective control in future. Strategies are framed keeping in mind

the cash requirement of the company.

Stock Controlling Methods Just in Time: It is a method to manage inventory, under this the order for replenishment

of stock is made just before its use and hence it results in saving of various costs to

company. Inventory Budget: It basically means preparation of budget in advance about various

elements of cost like materials, operational costs, other expenses, logistics etc.

Perpetual Inventory System: It assist company in keeping an eye on quantity as well as

value of Stock.

M2: Relevant theories and techniques of setting prices

A business can uses a wide range of methods of pricing whcih are used by an

organisation during selling of products and services. It is done to maximise profitability of each

transactions done by an organisation. Conventinal pricing techniques that emphasised that setting

separate equal contribution margines to various earning segments serve by hotel industries.

D2: Critical evaluation to have planned, manage and organise a number of activities

As per the mentioned various activities that are related with stock controlling is consider

as primary mode of reliable functioning of daily transactions and working capital management in

an organisation. It is done to avoid unnecessary inventory purchases that are done by “Belgravia

Hotels”.

5

Cash Control Method Implementation of efficient cash handling strategies: Under this, a organisation would

frame necessary policies and strategies which would help in maintenance of adequate

cash level within the organisation. Accountability Form: It means preparation of cash accounting forms which will further

improves companies profits and will enable it to overcome from looses. Setting up of Cash Flow Target: It involves forecasting the various requirements of cash

in an organisation for effective control in future. Strategies are framed keeping in mind

the cash requirement of the company.

Stock Controlling Methods Just in Time: It is a method to manage inventory, under this the order for replenishment

of stock is made just before its use and hence it results in saving of various costs to

company. Inventory Budget: It basically means preparation of budget in advance about various

elements of cost like materials, operational costs, other expenses, logistics etc.

Perpetual Inventory System: It assist company in keeping an eye on quantity as well as

value of Stock.

M2: Relevant theories and techniques of setting prices

A business can uses a wide range of methods of pricing whcih are used by an

organisation during selling of products and services. It is done to maximise profitability of each

transactions done by an organisation. Conventinal pricing techniques that emphasised that setting

separate equal contribution margines to various earning segments serve by hotel industries.

D2: Critical evaluation to have planned, manage and organise a number of activities

As per the mentioned various activities that are related with stock controlling is consider

as primary mode of reliable functioning of daily transactions and working capital management in

an organisation. It is done to avoid unnecessary inventory purchases that are done by “Belgravia

Hotels”.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

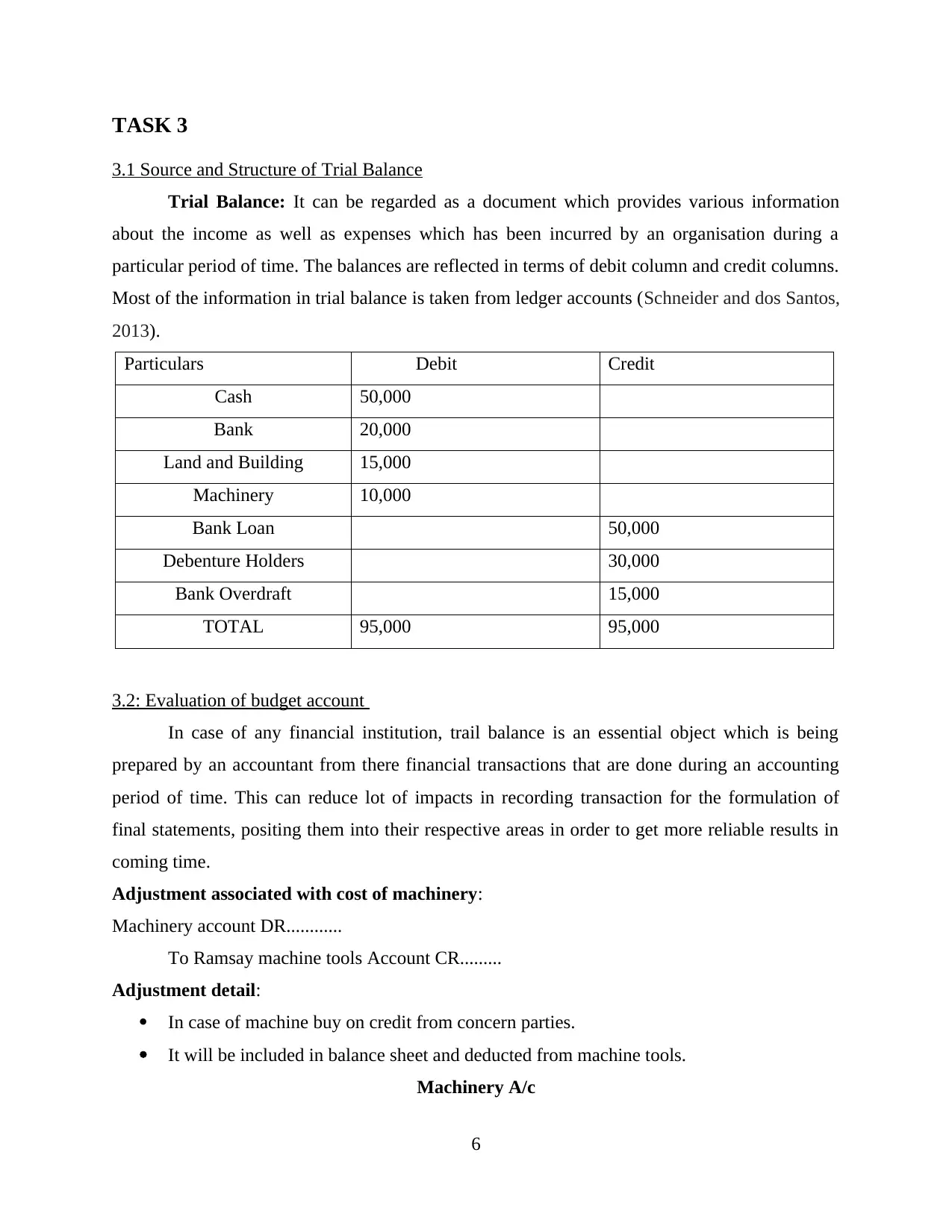

3.1 Source and Structure of Trial Balance

Trial Balance: It can be regarded as a document which provides various information

about the income as well as expenses which has been incurred by an organisation during a

particular period of time. The balances are reflected in terms of debit column and credit columns.

Most of the information in trial balance is taken from ledger accounts (Schneider and dos Santos,

2013).

Particulars Debit Credit

Cash 50,000

Bank 20,000

Land and Building 15,000

Machinery 10,000

Bank Loan 50,000

Debenture Holders 30,000

Bank Overdraft 15,000

TOTAL 95,000 95,000

3.2: Evaluation of budget account

In case of any financial institution, trail balance is an essential object which is being

prepared by an accountant from there financial transactions that are done during an accounting

period of time. This can reduce lot of impacts in recording transaction for the formulation of

final statements, positing them into their respective areas in order to get more reliable results in

coming time.

Adjustment associated with cost of machinery:

Machinery account DR............

To Ramsay machine tools Account CR.........

Adjustment detail:

In case of machine buy on credit from concern parties.

It will be included in balance sheet and deducted from machine tools.

Machinery A/c

6

3.1 Source and Structure of Trial Balance

Trial Balance: It can be regarded as a document which provides various information

about the income as well as expenses which has been incurred by an organisation during a

particular period of time. The balances are reflected in terms of debit column and credit columns.

Most of the information in trial balance is taken from ledger accounts (Schneider and dos Santos,

2013).

Particulars Debit Credit

Cash 50,000

Bank 20,000

Land and Building 15,000

Machinery 10,000

Bank Loan 50,000

Debenture Holders 30,000

Bank Overdraft 15,000

TOTAL 95,000 95,000

3.2: Evaluation of budget account

In case of any financial institution, trail balance is an essential object which is being

prepared by an accountant from there financial transactions that are done during an accounting

period of time. This can reduce lot of impacts in recording transaction for the formulation of

final statements, positing them into their respective areas in order to get more reliable results in

coming time.

Adjustment associated with cost of machinery:

Machinery account DR............

To Ramsay machine tools Account CR.........

Adjustment detail:

In case of machine buy on credit from concern parties.

It will be included in balance sheet and deducted from machine tools.

Machinery A/c

6

Particular Amount DR Particular Amount Cr

To Balance B/d 58000 By Balance C/d 78000

To XYZ machine tool 20000

78000 78000

XYZ machine tool A/c

Particular Amount Particular Amount

To Balance C/d 20000 By Machinery C/d 20000

20000 20000

In case of wage account:

The amount must be recorded on teh debit balance. Because of this, there total value goes

on increasing (Altinay, Paraskevas and Jang, 2015). There effects are seen over some

transactions. Such as:

Negative balance from salary accounting is being indicating on debt side of profit and

loss statements.

Positive value related to wages is being indicating on debit side of trading accounting.

7

To Balance B/d 58000 By Balance C/d 78000

To XYZ machine tool 20000

78000 78000

XYZ machine tool A/c

Particular Amount Particular Amount

To Balance C/d 20000 By Machinery C/d 20000

20000 20000

In case of wage account:

The amount must be recorded on teh debit balance. Because of this, there total value goes

on increasing (Altinay, Paraskevas and Jang, 2015). There effects are seen over some

transactions. Such as:

Negative balance from salary accounting is being indicating on debt side of profit and

loss statements.

Positive value related to wages is being indicating on debit side of trading accounting.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Posting into journals

Salary A/c

Particular Amount Particular Amount

To Balance D/d 15300 By wages 43000

By Balance c/d 11000

Total 15300 Total 15300

Wages A/c

Particular Amount Particular Amount

To Balance B/d 18000 By Balance C/d 51000

To salary a/c 33000

Total 51000 Total 51000

Salary account: It has been obsered that debit account balance which has be credited

with total amount of 33000. Its toal balance should be reduce to 33000. The entries will be

posted in profit and loss account in appropriate manner. Thus, total balance of salary is being

used to record in incomes statements of the company.

3.3 Process and Purpose of Budgetary Control

A control method whereby genuine outcomes are contrasted and spending plans. Any

distinctions (changes) are made the obligation of key people who can either practice control

activity or modify the first spending plans. Budgetary control and duty focuses; these empower

directors to screen hierarchical capacities. A good budgetary control would help in preparing

efficient budget as well maintain higher level of profits through achieving good productivity. It

can help in various department of the company like purchase, sales, marketing, administration

etc.

8

Salary A/c

Particular Amount Particular Amount

To Balance D/d 15300 By wages 43000

By Balance c/d 11000

Total 15300 Total 15300

Wages A/c

Particular Amount Particular Amount

To Balance B/d 18000 By Balance C/d 51000

To salary a/c 33000

Total 51000 Total 51000

Salary account: It has been obsered that debit account balance which has be credited

with total amount of 33000. Its toal balance should be reduce to 33000. The entries will be

posted in profit and loss account in appropriate manner. Thus, total balance of salary is being

used to record in incomes statements of the company.

3.3 Process and Purpose of Budgetary Control

A control method whereby genuine outcomes are contrasted and spending plans. Any

distinctions (changes) are made the obligation of key people who can either practice control

activity or modify the first spending plans. Budgetary control and duty focuses; these empower

directors to screen hierarchical capacities. A good budgetary control would help in preparing

efficient budget as well maintain higher level of profits through achieving good productivity. It

can help in various department of the company like purchase, sales, marketing, administration

etc.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 1Process of Budgetary Control

3.4: Evaluating budget variances

In every business organisation, it has been found that the primary objective which is

being helpful for the purpose of formulating final statements of Belgravia Hotels. It is necessary

for the company to make analysis of all material and labour variances that are present in an

organization (Hoque, 2013). The budget cost use to allows managers to set prices and total

estimation of profits. In accordance to wide reason, cost and total income that can be categories

in higher or medium-sized at the time of calculation. Budget is an estimation of future costs and

expenses a company is going to invest. This can assist an organization to make control of their

resources in effective manner. Variance analysis is an essential part for the company to make

comparison of outcomes collected from past and present time results. The data would be taken

into consider for increase overall aims and objectives for the company. This will be taken as to

analyse adverse and favourable result collated from total cost of production.

Budget variance

Particular Standards Actual Variances

Unit sold 50000 20000 30000

9

3.4: Evaluating budget variances

In every business organisation, it has been found that the primary objective which is

being helpful for the purpose of formulating final statements of Belgravia Hotels. It is necessary

for the company to make analysis of all material and labour variances that are present in an

organization (Hoque, 2013). The budget cost use to allows managers to set prices and total

estimation of profits. In accordance to wide reason, cost and total income that can be categories

in higher or medium-sized at the time of calculation. Budget is an estimation of future costs and

expenses a company is going to invest. This can assist an organization to make control of their

resources in effective manner. Variance analysis is an essential part for the company to make

comparison of outcomes collected from past and present time results. The data would be taken

into consider for increase overall aims and objectives for the company. This will be taken as to

analyse adverse and favourable result collated from total cost of production.

Budget variance

Particular Standards Actual Variances

Unit sold 50000 20000 30000

9

Material 17,000 20500 -3500

Direct labour 21500 22375 -875

Particular Material(£) Labour (£)

Price / Variance Efficiency -5500 3750

Variance -3000 -5425

Total Variance 2500 -1675

From the above inforamtion which is made on assumption basis. The collected data is

being analyse on the basis of total 50000 standard units. The total variance is being determine by

using direct material and labour variances that are being dicussed in the above table. The resulst

are showing adverse impacts on the material and labour costs. There are various types of

adjustment entries that are needed to be taken into account in accordance with the preparation of

trail balance.

M3: Structure and approaches to assess the trail balance

Sources of preparation trail balances is related with major three categories such as

general ledger, sales and purchase ledger book. Structure of trail balances is concern with all

specific categories that are consists of current assets and contra assets and current liability as

well as long term liability. Such as:

Trail balance as on 31st April, 2018

Particular Debit Credit

Cash at bank 60150

Account receivable 2500

Building 199400

Office supplies 450

Common stock 250000

Rent expenses 12500

10

Direct labour 21500 22375 -875

Particular Material(£) Labour (£)

Price / Variance Efficiency -5500 3750

Variance -3000 -5425

Total Variance 2500 -1675

From the above inforamtion which is made on assumption basis. The collected data is

being analyse on the basis of total 50000 standard units. The total variance is being determine by

using direct material and labour variances that are being dicussed in the above table. The resulst

are showing adverse impacts on the material and labour costs. There are various types of

adjustment entries that are needed to be taken into account in accordance with the preparation of

trail balance.

M3: Structure and approaches to assess the trail balance

Sources of preparation trail balances is related with major three categories such as

general ledger, sales and purchase ledger book. Structure of trail balances is concern with all

specific categories that are consists of current assets and contra assets and current liability as

well as long term liability. Such as:

Trail balance as on 31st April, 2018

Particular Debit Credit

Cash at bank 60150

Account receivable 2500

Building 199400

Office supplies 450

Common stock 250000

Rent expenses 12500

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.