Hospitality Business Toolkit Report: HR and Legal Aspects

VerifiedAdded on 2022/12/28

|22

|4137

|1

Report

AI Summary

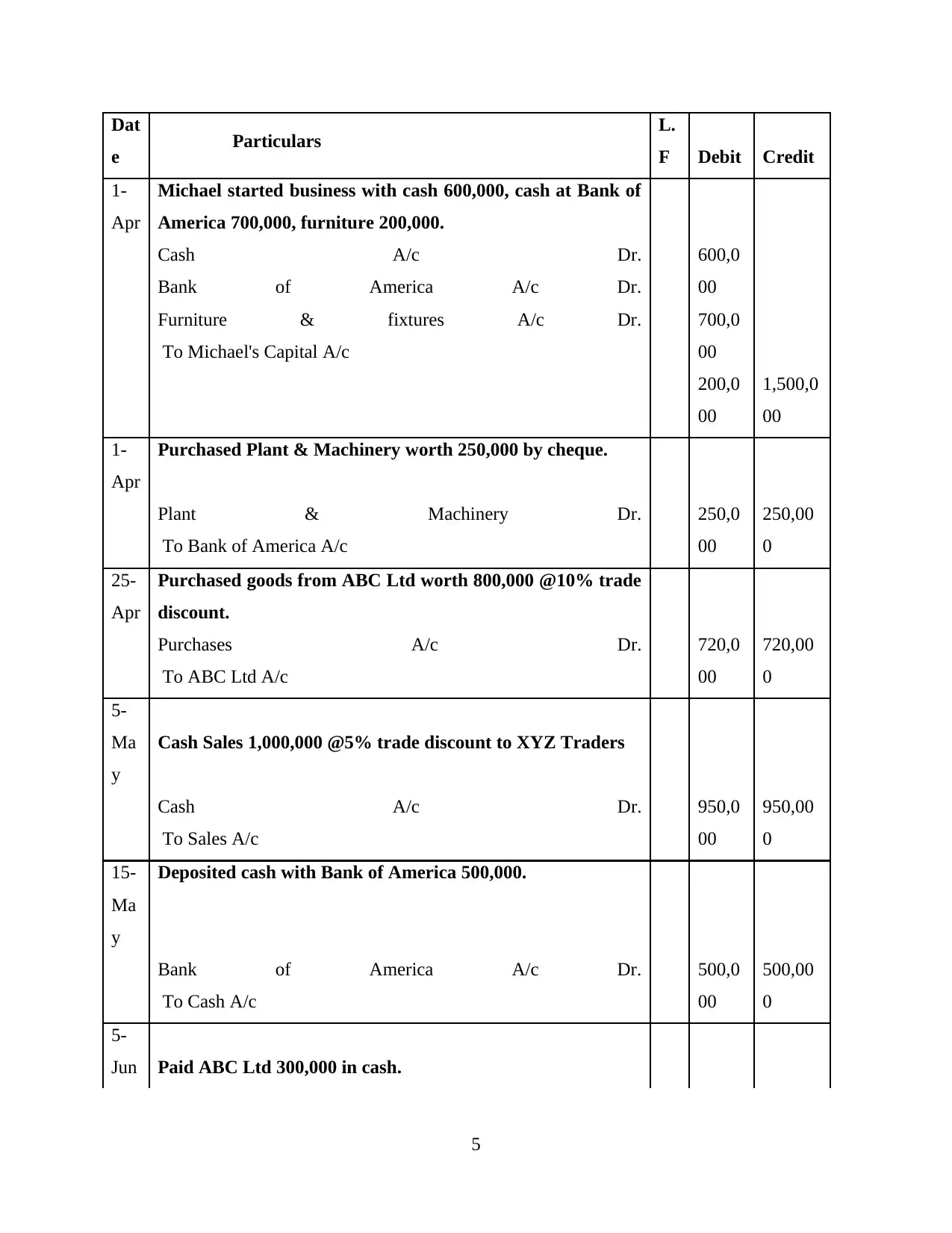

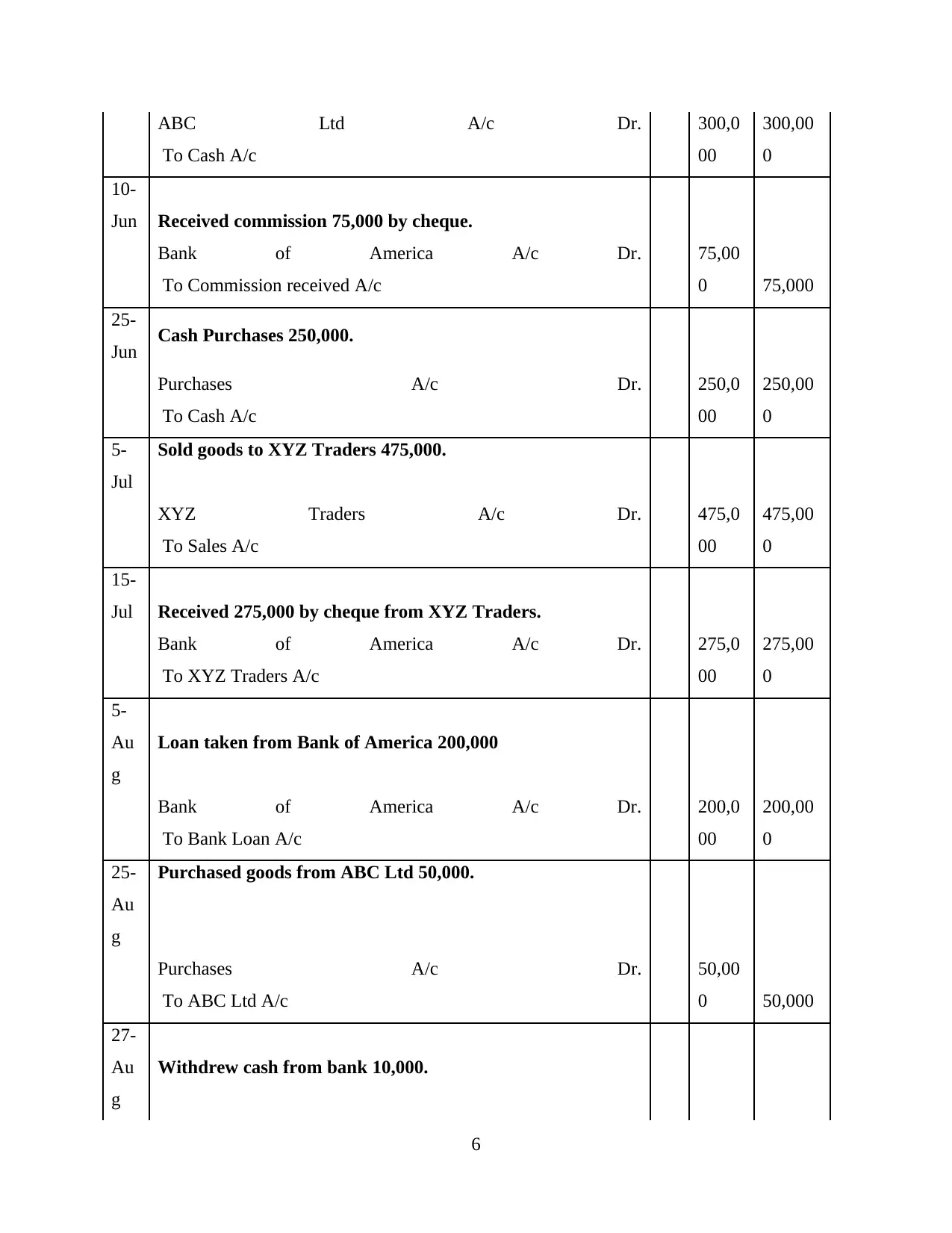

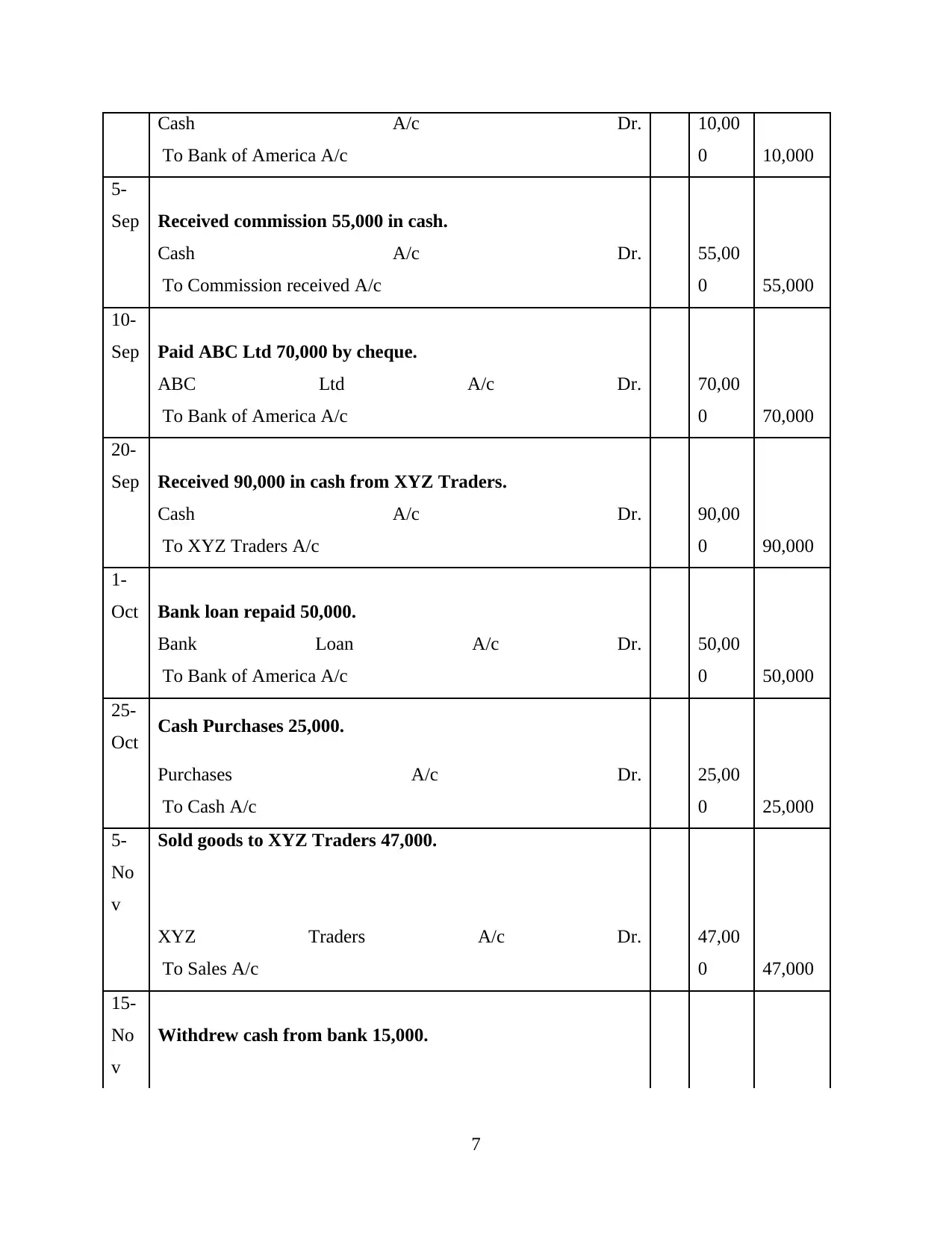

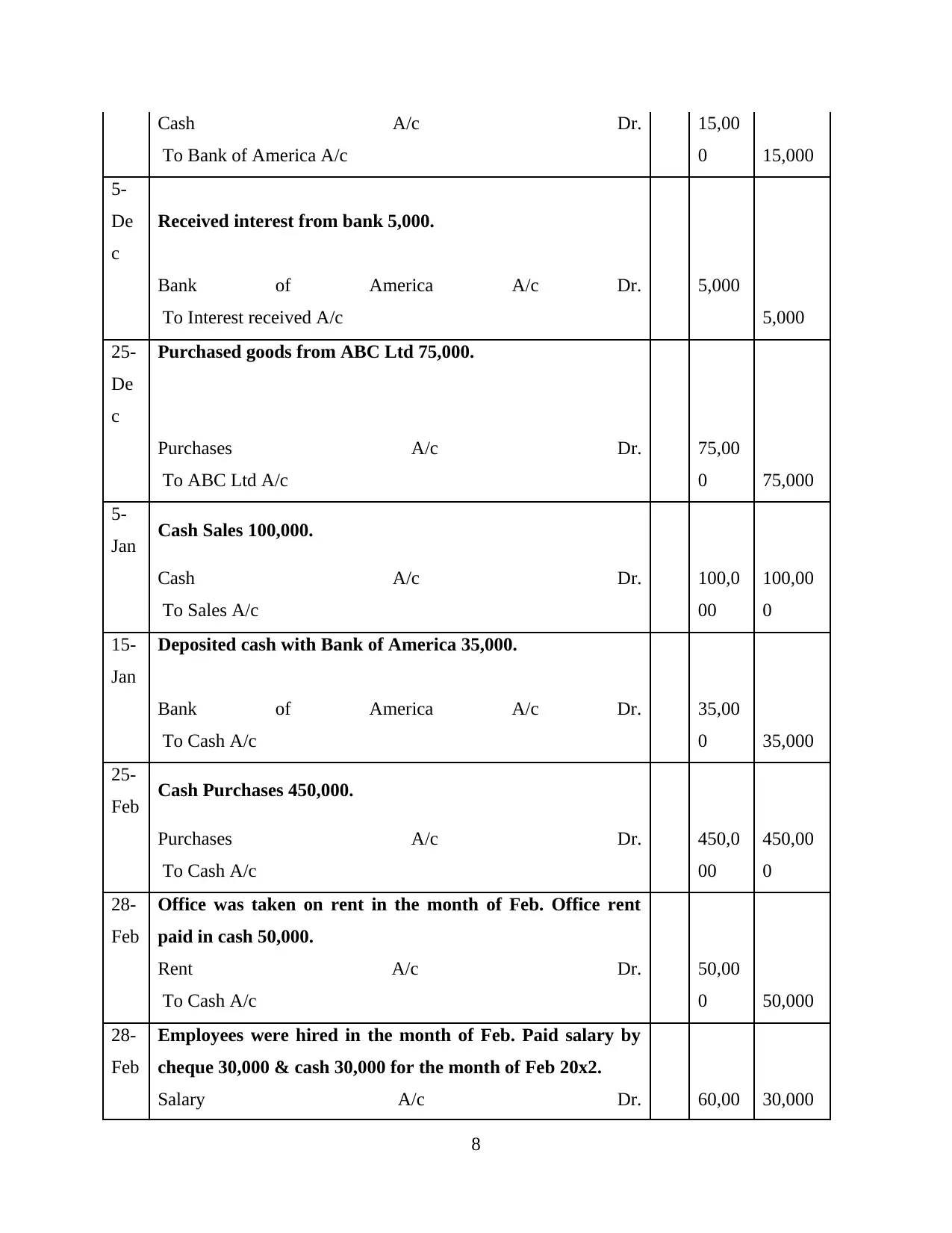

This report analyzes the hospitality business toolkit, using the Bicester Hotel as a case study. It begins by investigating the principles of managing and monitoring financial performance, including financial statements, stock records, and overhead costs. The report then applies the double-entry bookkeeping system, providing journal entries and a trial balance. Task 2 delves into the HR life cycle, focusing on recruitment, onboarding, career development, and retention, with a focus on performance management plans to address negative behaviors and staff retention issues. Task 3 examines legal compliance, identifying relevant legislation and illustrating its impact on business decision-making. Finally, the report explores the interrelation of functional roles and methods of communication within the hospitality sector to strengthen the value chain, followed by a conclusion and references.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.