Hospitality Industry: Managing Financial Resources and Reporting

VerifiedAdded on 2023/06/16

|12

|3096

|72

Report

AI Summary

This report provides a detailed analysis of financial resource management within the hospitality sector. It begins by explaining Generally Accepted Accounting Principles (GAAP) and their importance in standardizing accounting practices across industries, highlighting key principles such as regularity, consistency, sincerity, and prudence. The report identifies various users of financial statements, including company management, customers, competitors, employees, governments, and unions, and discusses their specific information needs. It then examines the significance of income statements, balance sheets, and cash flow statements for loan creditors and trade creditors, emphasizing the importance of ratios derived from these statements. Furthermore, the report describes the components that supplement financial statements in an annual report, such as assets, liabilities, equities, and revenues, and discusses financial reporting concepts. The report concludes with an interpretation of financial statements using financial ratios to compare two years of performance. Desklib is the perfect platform for students seeking similar solved assignments and study resources.

Managing Financial

Resources in Hospitality

Industry

1

Resources in Hospitality

Industry

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of content

Table of Contents

Introduction......................................................................................................................................3

Main Body.......................................................................................................................................3

Explain the meaning of generally accepted accounting principles. Also explain the users of

financial statements in order to assess the information needs of different decision makers. .....3

The annual financial statements of organisation are used by various parties in order to serve a

wide variety of purpose. Discuss which three statements of income, financial position and

cash flows can be of most interest for a loan creditor and a trade creditor. ...............................5

Describe the components that tend to supplement the financial statements in an annual report.

Also discuss the various financial reporting concepts. ..............................................................5

Interpret financial statement while using the appropriate financial ratios and compare the two

years of performance...................................................................................................................7

Conclusion ......................................................................................................................................9

References......................................................................................................................................10

2

Table of Contents

Introduction......................................................................................................................................3

Main Body.......................................................................................................................................3

Explain the meaning of generally accepted accounting principles. Also explain the users of

financial statements in order to assess the information needs of different decision makers. .....3

The annual financial statements of organisation are used by various parties in order to serve a

wide variety of purpose. Discuss which three statements of income, financial position and

cash flows can be of most interest for a loan creditor and a trade creditor. ...............................5

Describe the components that tend to supplement the financial statements in an annual report.

Also discuss the various financial reporting concepts. ..............................................................5

Interpret financial statement while using the appropriate financial ratios and compare the two

years of performance...................................................................................................................7

Conclusion ......................................................................................................................................9

References......................................................................................................................................10

2

Introduction

Managing Financial resources is a concept that tends to address the complicated issues in

context of planning and control in terms of finance. Managing financial resources is a concept

that includes measurement of performance, cost analysis, methods of improving the profitability

as well as the analysis of the cost. The report focuses upon the management of financial

resources in the hospitality sector. As, it is very important for the organisations to have a clear

business plan in order to manage the financial resources (Flink. and Molina Jr, 2021).

Main Body

Explain the meaning of generally accepted accounting principles. Also explain the users of

financial statements in order to assess the information needs of different decision makers.

Generally Accepted Accounting Principles is a concept that helps in governing the

accounting in accordance with the general rules as well as guidelines. The purpose of the

Generally Accepted Accounting Principles is to standardise as well as regulate the definitions,

assumptions as well as methods that are to be used in the accounting process across various

industries. The Generally Accepted Accounting Principles is to cover various topics like

recognition of revenue, classification of the balance sheets as well as the concept of materiality.

The main purpose that is fulfilled through Generally Accepted Accounting principles is to make

sure that the financial statements are fulfilled, consistent as well as comparable. The various

principles in accordance with the GAAP are-

Principles of Regularity- The principle of regularity states that accountant is required to

adhere with the Generally Accepted Accounting Principles are basically rules and

regulations that act as a standard (Kembauw and et.al., 2020).

Principle of Consistency- The principle of Consistency is wherein the accountants tend

to commit to the application of several consistent standards through out a reporting

process from one period to the next period. Consistency is important in order to

facilitate the financial comparability between different accounting periods of the

organisation.

Principle of sincerity- Principle of sincerity tends to strive in order to provide impartial

and accurate depiction of financial situation of the organisation.

3

Managing Financial resources is a concept that tends to address the complicated issues in

context of planning and control in terms of finance. Managing financial resources is a concept

that includes measurement of performance, cost analysis, methods of improving the profitability

as well as the analysis of the cost. The report focuses upon the management of financial

resources in the hospitality sector. As, it is very important for the organisations to have a clear

business plan in order to manage the financial resources (Flink. and Molina Jr, 2021).

Main Body

Explain the meaning of generally accepted accounting principles. Also explain the users of

financial statements in order to assess the information needs of different decision makers.

Generally Accepted Accounting Principles is a concept that helps in governing the

accounting in accordance with the general rules as well as guidelines. The purpose of the

Generally Accepted Accounting Principles is to standardise as well as regulate the definitions,

assumptions as well as methods that are to be used in the accounting process across various

industries. The Generally Accepted Accounting Principles is to cover various topics like

recognition of revenue, classification of the balance sheets as well as the concept of materiality.

The main purpose that is fulfilled through Generally Accepted Accounting principles is to make

sure that the financial statements are fulfilled, consistent as well as comparable. The various

principles in accordance with the GAAP are-

Principles of Regularity- The principle of regularity states that accountant is required to

adhere with the Generally Accepted Accounting Principles are basically rules and

regulations that act as a standard (Kembauw and et.al., 2020).

Principle of Consistency- The principle of Consistency is wherein the accountants tend

to commit to the application of several consistent standards through out a reporting

process from one period to the next period. Consistency is important in order to

facilitate the financial comparability between different accounting periods of the

organisation.

Principle of sincerity- Principle of sincerity tends to strive in order to provide impartial

and accurate depiction of financial situation of the organisation.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principle of Prudence- The principle of Prudence emphasises upon the fact based

representation of the financial data that can not be clouded by speculation.

Principle of Non Compensation- The principle of non-compensation states that both the

negatives as well as positives need to be reported with full transparency and without the

expectations of compensation of debt (Levitskaya, 2021).

Principle of Periodicity- The principle of permanence of methods is required to be

consistent that allows comparison between the financial information of the organisation.

Principle of Continuity- Principles of continuity is referred to the valuation of assets that

focus upon assumptions that the business will operate in the long run.

Principle of Materiality- The principle of materiality focuses upon the fact that

accountants are required to disclose all the essential details regarding the financial data

and accounting in terms of financial reports. Principle of Utmost Good faith- The principle of utmost good faith tends to focus upon

the suppression of positive values. It states tat the parties must be honest in regards of

the transactions.

Users of financial statements

Company management- The management team of an organisation is required to

understand the profitability, cash flow as well as liquidity along with the cash flows so

that efficient operational and financial decisions can be taken.

Customers- The customers are also considered as the users of the financial statements as

the customers tend to consider the various suppliers for a major contract. The customers

tend to evaluate and judge the financial ability of a supplier. This helps in analysing If the

supplier will survive in the market for long and will be able to supply and fulfil the needs

of the organisation (Li, F., 2020).

Competitors- Competitors are basically the entities that work against the business

organisation. The competitors are users of the financial statements as they attempt to gain

the access of the competitive strategy.

Employees- Employees are also considered as the users of the financial statements of the

organisation. The employees tend to have a detailed explanation in order to increase the

employee involvement and understand the business.

4

representation of the financial data that can not be clouded by speculation.

Principle of Non Compensation- The principle of non-compensation states that both the

negatives as well as positives need to be reported with full transparency and without the

expectations of compensation of debt (Levitskaya, 2021).

Principle of Periodicity- The principle of permanence of methods is required to be

consistent that allows comparison between the financial information of the organisation.

Principle of Continuity- Principles of continuity is referred to the valuation of assets that

focus upon assumptions that the business will operate in the long run.

Principle of Materiality- The principle of materiality focuses upon the fact that

accountants are required to disclose all the essential details regarding the financial data

and accounting in terms of financial reports. Principle of Utmost Good faith- The principle of utmost good faith tends to focus upon

the suppression of positive values. It states tat the parties must be honest in regards of

the transactions.

Users of financial statements

Company management- The management team of an organisation is required to

understand the profitability, cash flow as well as liquidity along with the cash flows so

that efficient operational and financial decisions can be taken.

Customers- The customers are also considered as the users of the financial statements as

the customers tend to consider the various suppliers for a major contract. The customers

tend to evaluate and judge the financial ability of a supplier. This helps in analysing If the

supplier will survive in the market for long and will be able to supply and fulfil the needs

of the organisation (Li, F., 2020).

Competitors- Competitors are basically the entities that work against the business

organisation. The competitors are users of the financial statements as they attempt to gain

the access of the competitive strategy.

Employees- Employees are also considered as the users of the financial statements of the

organisation. The employees tend to have a detailed explanation in order to increase the

employee involvement and understand the business.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Governments- The government is also considered as the user of financial statements as

the government in which the jurisdiction of the organisation is established in order to

determine if the business has paid the appropriate amount of taxes.

Unions- The unions are also considered as the users of the financial statements of the

organisation as it tends to evaluate the ability of the business of paying compensation and

further it helps in determining if the benefits are being paid to the various union members

as well (Mosteanu, N.R., 2020).

The annual financial statements of organisation are used by various parties in order to serve a

wide variety of purpose. Discuss which three statements of income, financial position and

cash flows can be of most interest for a loan creditor and a trade creditor.

The various kind of financial statements have been discussed below.

a. INCOME STATEMENTS: From this statement, an organisation knows what amount of

revenue it is earning and what are its expenses. Also, they get to know whether they are incurring

loss or profit.

b. BALANCE SHEET: From this organisation gets to know that what are their assets and

liabilities. If assets are more than it is good sign for them as they can cover their liabilities from

it.

c. CASH FLOW STATEMENTS: From this statement, organisation gets to know the inflow and

outflow of the cash. This inflow and outflow is of three types i.e. from operating activities, from

investing activities and from financing activities.

The statements that can be of most interest to a loan creditor is balance sheet since it contains

assets and liabilities. From it they can know, what amount of assets an organisation has and if in

future a situation arises can business repay the loan by selling off its assets. Also, they can find

out various ratios from balance sheet like quick ratio, debt to equity ratio and debt service

coverage ratio. From these ratios, they can know the exact position of the business. Quick ratio is

important because from it they can know if they can pay the loan which is of less than one year.

From debt service coverage ratio they can know that their current debt can be paid off by

comparing it with net income with its total debt. From debt to equity ratio they can analyse if

company takes an additional debt will it be able to pay that or not (Moşteanu, Faccia and

Cavaliere, 2020).

5

the government in which the jurisdiction of the organisation is established in order to

determine if the business has paid the appropriate amount of taxes.

Unions- The unions are also considered as the users of the financial statements of the

organisation as it tends to evaluate the ability of the business of paying compensation and

further it helps in determining if the benefits are being paid to the various union members

as well (Mosteanu, N.R., 2020).

The annual financial statements of organisation are used by various parties in order to serve a

wide variety of purpose. Discuss which three statements of income, financial position and

cash flows can be of most interest for a loan creditor and a trade creditor.

The various kind of financial statements have been discussed below.

a. INCOME STATEMENTS: From this statement, an organisation knows what amount of

revenue it is earning and what are its expenses. Also, they get to know whether they are incurring

loss or profit.

b. BALANCE SHEET: From this organisation gets to know that what are their assets and

liabilities. If assets are more than it is good sign for them as they can cover their liabilities from

it.

c. CASH FLOW STATEMENTS: From this statement, organisation gets to know the inflow and

outflow of the cash. This inflow and outflow is of three types i.e. from operating activities, from

investing activities and from financing activities.

The statements that can be of most interest to a loan creditor is balance sheet since it contains

assets and liabilities. From it they can know, what amount of assets an organisation has and if in

future a situation arises can business repay the loan by selling off its assets. Also, they can find

out various ratios from balance sheet like quick ratio, debt to equity ratio and debt service

coverage ratio. From these ratios, they can know the exact position of the business. Quick ratio is

important because from it they can know if they can pay the loan which is of less than one year.

From debt service coverage ratio they can know that their current debt can be paid off by

comparing it with net income with its total debt. From debt to equity ratio they can analyse if

company takes an additional debt will it be able to pay that or not (Moşteanu, Faccia and

Cavaliere, 2020).

5

The statements that can be of most interest to trade creditor is income statement since it contains

the profit and losses of the business. From it they can know, that the asset that the company has

purchased from them can be paid by the company or not. Since trade creditors can charge

interest or not depending upon the credit period. Also, this statement tells that revenue that has

been earned by the company is enough to meet its expenses or not. Trade creditors ask for

income statement of last two to three years to know the worthiness of the business (Naumkin,

2020).

Describe the components that tend to supplement the financial statements in an annual report.

Also discuss the various financial reporting concepts.

Financial statements are considered as the important reports of the organisation that tends

to provide financial information to the entity regarding a specific period of time that can be used

by various stakeholders which include employees, management, investors, shareholders,

suppliers, customers, bankers as well as stakeholders. The statements of the organisation are

prepared in order to cope with the requirements of the various stakeholders. There are basically

five financial statements and these comprise of five elements as a whole. The five statements

include statement of financial position or balance sheet, statement of financial performance

which is also known as income statement, statement of change in equity, statement of cash flow

as well as noted to financial statements.

The five elements of the financial statements comprises of five main elements of the

financial information. The five elements of the financial statements have been discussed below.

Assets- The assets are considered as the resources control by the entity as a result of

various events that have occurred in the past. The assets tend to provide economic

benefits that are expected to flow in an entity. The assets are basically the sum of all the

liabilities as well as the equity of an organisation. There are basically two kinds of assets

that are held by the organisation, namely current assets and non current assets. The

current assets is referred to the assets that are short term assets. The current assets have

high liquidity in terms of assets and also these kind of assets can not be depreciated. The

movement of the current assets are charged directly in the income statement. The useful

life of current assets is generally less than 12 months. Non current assets are basically the

long term assets that have a useful life of more than an year. Further, the non current

6

the profit and losses of the business. From it they can know, that the asset that the company has

purchased from them can be paid by the company or not. Since trade creditors can charge

interest or not depending upon the credit period. Also, this statement tells that revenue that has

been earned by the company is enough to meet its expenses or not. Trade creditors ask for

income statement of last two to three years to know the worthiness of the business (Naumkin,

2020).

Describe the components that tend to supplement the financial statements in an annual report.

Also discuss the various financial reporting concepts.

Financial statements are considered as the important reports of the organisation that tends

to provide financial information to the entity regarding a specific period of time that can be used

by various stakeholders which include employees, management, investors, shareholders,

suppliers, customers, bankers as well as stakeholders. The statements of the organisation are

prepared in order to cope with the requirements of the various stakeholders. There are basically

five financial statements and these comprise of five elements as a whole. The five statements

include statement of financial position or balance sheet, statement of financial performance

which is also known as income statement, statement of change in equity, statement of cash flow

as well as noted to financial statements.

The five elements of the financial statements comprises of five main elements of the

financial information. The five elements of the financial statements have been discussed below.

Assets- The assets are considered as the resources control by the entity as a result of

various events that have occurred in the past. The assets tend to provide economic

benefits that are expected to flow in an entity. The assets are basically the sum of all the

liabilities as well as the equity of an organisation. There are basically two kinds of assets

that are held by the organisation, namely current assets and non current assets. The

current assets is referred to the assets that are short term assets. The current assets have

high liquidity in terms of assets and also these kind of assets can not be depreciated. The

movement of the current assets are charged directly in the income statement. The useful

life of current assets is generally less than 12 months. Non current assets are basically the

long term assets that have a useful life of more than an year. Further, the non current

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

assets are termed as fixed assets which do not have a high liquidity. The value of fixed

assets tend to decrease from time to time due to the depreciation.

Liabilities- Liabilities are also a component of the financial statements. Liabilities are

basically the obligations that arise from the past events. The settlements of the liabilities

is expected to have an impact upon the outflow from the various resources that tend to

embody the economic benefit. Again, the liabilities are segregated in form of current

liabilities as well as non current liabilities. The current liabilities are the liabilities that

tend to have a repayment period of less than 12 months. The non current liabilities are

basically the long term liabilities that need to be repaid after 12 months of duration. The

liabilities are basically the elimination of total equities from the total assets. Also, the

sum of non current liabilities and current liabilities is also summed up as the total amount

of liabilities.

Equities- Equity is referred as the residual interest of the organisation in the assets of the

organisation after the deduction of the liabilities. Equities can be ascertained after

deducting the value of liabilities from the assets. The equity can also be referred as the

ordinary share capital as well as retained earnings. The value of equity has a tendency to

increase and decrease in accordance with the movement of assets as well as liabilities. If

the assets are rising and the liabilities are stable then the equities are likely to increase

and in case, the assets are constant and the liabilities increase then the equity tend to

decrease.

Revenues- Revenues is considered as the increase in the economic benefits of the

organisation during the accounting period. The revenues can increase through the mode

of inflows as well as enhancements of assets or reduction in the liabilities. These tend to

have a direct impact over the rise in equity. The sales revenues in several cases is

considered as the income in the income statement. In order to record the revenue, there

are two approaches basically which are cash basis and the other one is accrual basis. Expenses- Expenses can be referred as the decrease in the economic benefits of an

organisation during an accounting period. The expenses can occur in form of outflows as

well as depreciation of assets or increase in the liabilities that results in decrease in equity

as well. There are various kind of expenses that are incurred by the business which are

7

assets tend to decrease from time to time due to the depreciation.

Liabilities- Liabilities are also a component of the financial statements. Liabilities are

basically the obligations that arise from the past events. The settlements of the liabilities

is expected to have an impact upon the outflow from the various resources that tend to

embody the economic benefit. Again, the liabilities are segregated in form of current

liabilities as well as non current liabilities. The current liabilities are the liabilities that

tend to have a repayment period of less than 12 months. The non current liabilities are

basically the long term liabilities that need to be repaid after 12 months of duration. The

liabilities are basically the elimination of total equities from the total assets. Also, the

sum of non current liabilities and current liabilities is also summed up as the total amount

of liabilities.

Equities- Equity is referred as the residual interest of the organisation in the assets of the

organisation after the deduction of the liabilities. Equities can be ascertained after

deducting the value of liabilities from the assets. The equity can also be referred as the

ordinary share capital as well as retained earnings. The value of equity has a tendency to

increase and decrease in accordance with the movement of assets as well as liabilities. If

the assets are rising and the liabilities are stable then the equities are likely to increase

and in case, the assets are constant and the liabilities increase then the equity tend to

decrease.

Revenues- Revenues is considered as the increase in the economic benefits of the

organisation during the accounting period. The revenues can increase through the mode

of inflows as well as enhancements of assets or reduction in the liabilities. These tend to

have a direct impact over the rise in equity. The sales revenues in several cases is

considered as the income in the income statement. In order to record the revenue, there

are two approaches basically which are cash basis and the other one is accrual basis. Expenses- Expenses can be referred as the decrease in the economic benefits of an

organisation during an accounting period. The expenses can occur in form of outflows as

well as depreciation of assets or increase in the liabilities that results in decrease in equity

as well. There are various kind of expenses that are incurred by the business which are

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

namely operating expenses, administrative expenses, etc. which include expenses like

cost of goods sold. Depreciation and several more (Эшов, 2020).

Financial reporting concepts

Financial reporting can be referred as the concept of defining communication of various

published financial statements and information in context of a business organisation. The

information is required to be shared with the third parties which include the creditors,

shareholders, creditors, public, etc. It is basically a total communication system that involves

company as a user wherein the investors and creditors are considered as primary users. The

primary objectives of the financial reporting is investment decision making as well as

Management accountability

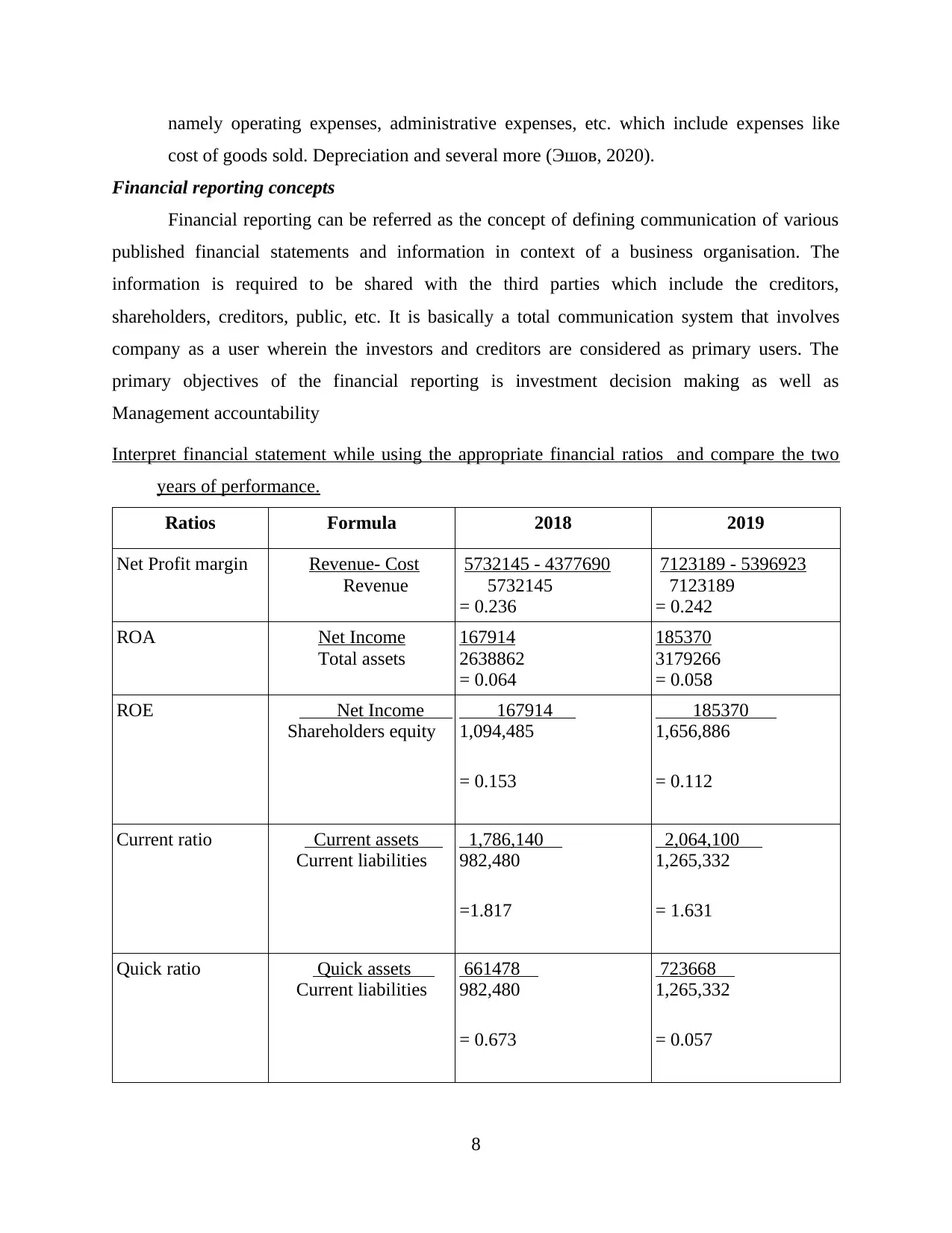

Interpret financial statement while using the appropriate financial ratios and compare the two

years of performance.

Ratios Formula 2018 2019

Net Profit margin Revenue- Cost

Revenue

5732145 - 4377690

5732145

= 0.236

7123189 - 5396923

7123189

= 0.242

ROA Net Income

Total assets

167914

2638862

= 0.064

185370

3179266

= 0.058

ROE Net Income

Shareholders equity

167914

1,094,485

= 0.153

185370

1,656,886

= 0.112

Current ratio Current assets

Current liabilities

1,786,140

982,480

=1.817

2,064,100

1,265,332

= 1.631

Quick ratio Quick assets

Current liabilities

661478

982,480

= 0.673

723668

1,265,332

= 0.057

8

cost of goods sold. Depreciation and several more (Эшов, 2020).

Financial reporting concepts

Financial reporting can be referred as the concept of defining communication of various

published financial statements and information in context of a business organisation. The

information is required to be shared with the third parties which include the creditors,

shareholders, creditors, public, etc. It is basically a total communication system that involves

company as a user wherein the investors and creditors are considered as primary users. The

primary objectives of the financial reporting is investment decision making as well as

Management accountability

Interpret financial statement while using the appropriate financial ratios and compare the two

years of performance.

Ratios Formula 2018 2019

Net Profit margin Revenue- Cost

Revenue

5732145 - 4377690

5732145

= 0.236

7123189 - 5396923

7123189

= 0.242

ROA Net Income

Total assets

167914

2638862

= 0.064

185370

3179266

= 0.058

ROE Net Income

Shareholders equity

167914

1,094,485

= 0.153

185370

1,656,886

= 0.112

Current ratio Current assets

Current liabilities

1,786,140

982,480

=1.817

2,064,100

1,265,332

= 1.631

Quick ratio Quick assets

Current liabilities

661478

982,480

= 0.673

723668

1,265,332

= 0.057

8

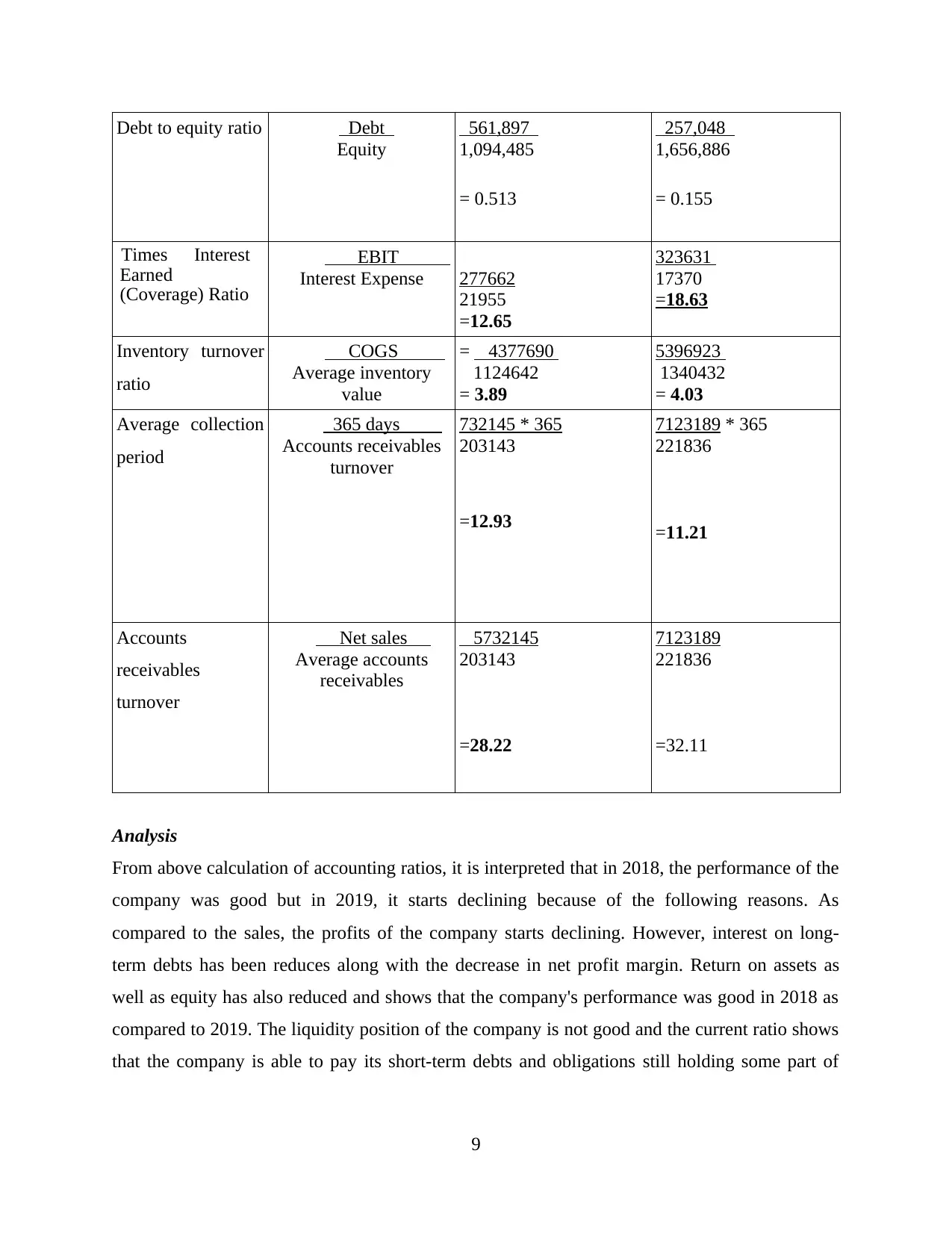

Debt to equity ratio Debt

Equity

561,897

1,094,485

= 0.513

257,048

1,656,886

= 0.155

Times Interest

Earned

(Coverage) Ratio

EBIT

Interest Expense 277662

21955

=12.65

323631

17370

=18.63

Inventory turnover

ratio

COGS

Average inventory

value

= 4377690

1124642

= 3.89

5396923

1340432

= 4.03

Average collection

period

365 days

Accounts receivables

turnover

732145 * 365

203143

=12.93

7123189 * 365

221836

=11.21

Accounts

receivables

turnover

Net sales

Average accounts

receivables

5732145

203143

=28.22

7123189

221836

=32.11

Analysis

From above calculation of accounting ratios, it is interpreted that in 2018, the performance of the

company was good but in 2019, it starts declining because of the following reasons. As

compared to the sales, the profits of the company starts declining. However, interest on long-

term debts has been reduces along with the decrease in net profit margin. Return on assets as

well as equity has also reduced and shows that the company's performance was good in 2018 as

compared to 2019. The liquidity position of the company is not good and the current ratio shows

that the company is able to pay its short-term debts and obligations still holding some part of

9

Equity

561,897

1,094,485

= 0.513

257,048

1,656,886

= 0.155

Times Interest

Earned

(Coverage) Ratio

EBIT

Interest Expense 277662

21955

=12.65

323631

17370

=18.63

Inventory turnover

ratio

COGS

Average inventory

value

= 4377690

1124642

= 3.89

5396923

1340432

= 4.03

Average collection

period

365 days

Accounts receivables

turnover

732145 * 365

203143

=12.93

7123189 * 365

221836

=11.21

Accounts

receivables

turnover

Net sales

Average accounts

receivables

5732145

203143

=28.22

7123189

221836

=32.11

Analysis

From above calculation of accounting ratios, it is interpreted that in 2018, the performance of the

company was good but in 2019, it starts declining because of the following reasons. As

compared to the sales, the profits of the company starts declining. However, interest on long-

term debts has been reduces along with the decrease in net profit margin. Return on assets as

well as equity has also reduced and shows that the company's performance was good in 2018 as

compared to 2019. The liquidity position of the company is not good and the current ratio shows

that the company is able to pay its short-term debts and obligations still holding some part of

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

assets. Overall, the performance of organisation is not bad and the firm has to pay attention on

some aspects to attain the level of profitability.

Conclusion

It can be concluded from the report that it is important for the organisations to manage its

financial resources in order to survive in the market. Managing Financial resources is a concept

that tends to address the complicated issues in context of planning and control in terms of

finance. The report has highlighted the concepts of generally accepted accounting principles

along with the various users as well as the stakeholders of the organisation. Also, ratio analysis

has been performed for the organisation in order to analyse the financial performance of the

business.

10

some aspects to attain the level of profitability.

Conclusion

It can be concluded from the report that it is important for the organisations to manage its

financial resources in order to survive in the market. Managing Financial resources is a concept

that tends to address the complicated issues in context of planning and control in terms of

finance. The report has highlighted the concepts of generally accepted accounting principles

along with the various users as well as the stakeholders of the organisation. Also, ratio analysis

has been performed for the organisation in order to analyse the financial performance of the

business.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Flink, C. and Molina Jr, A.L., 2021. Improving the performance of public organizations:

Financial resources and the conditioning effect of clientele context. Public

Administration, 99(2), pp.387-404.

Kembauw, E. and et.al., 2020. Strategies of Financial Management Quality Control in

Business. TEST Engineering & Management, 82, pp.16256-16266.

Levitskaya, N.L., 2021, March. Financial Resources as a Factor of Economic Security of a

Municipality. In IOP Conference Series: Earth and Environmental Science (Vol. 666,

No. 6, p. 062113). IOP Publishing.

Li, F., 2020. Leading digital transformation: three emerging approaches for managing the

transition. International Journal of Operations & Production Management.

Mosteanu, N.R., 2020. Socio-Financial Disruption–Key Tips To Manage And Ensure The

Business Continuity. Global Journal of Social Sciences Studies, 6(2), pp.87-95.

Moşteanu, N.R., Faccia, A. and Cavaliere, L.P.L., 2020, August. Disaster Management,

Digitalization and Financial Resources: key factors to keep the organization ongoing.

In Proceedings of the 2020 4th International Conference on Cloud and Big Data

Computing (pp. 118-122).

Naumkin, V.A., 2020. Financial resources of small businesses: internal and external factors

influencing the sources of their formation. Bulletin of National Academy of sciences of

the Republic of Kazakhstan, 2(384), pp.106-110.

Эшов, М., 2020. Impact of Financial Sustainability on Enterprise Value Expansion. Архив

научных исследований, (18).

11

Flink, C. and Molina Jr, A.L., 2021. Improving the performance of public organizations:

Financial resources and the conditioning effect of clientele context. Public

Administration, 99(2), pp.387-404.

Kembauw, E. and et.al., 2020. Strategies of Financial Management Quality Control in

Business. TEST Engineering & Management, 82, pp.16256-16266.

Levitskaya, N.L., 2021, March. Financial Resources as a Factor of Economic Security of a

Municipality. In IOP Conference Series: Earth and Environmental Science (Vol. 666,

No. 6, p. 062113). IOP Publishing.

Li, F., 2020. Leading digital transformation: three emerging approaches for managing the

transition. International Journal of Operations & Production Management.

Mosteanu, N.R., 2020. Socio-Financial Disruption–Key Tips To Manage And Ensure The

Business Continuity. Global Journal of Social Sciences Studies, 6(2), pp.87-95.

Moşteanu, N.R., Faccia, A. and Cavaliere, L.P.L., 2020, August. Disaster Management,

Digitalization and Financial Resources: key factors to keep the organization ongoing.

In Proceedings of the 2020 4th International Conference on Cloud and Big Data

Computing (pp. 118-122).

Naumkin, V.A., 2020. Financial resources of small businesses: internal and external factors

influencing the sources of their formation. Bulletin of National Academy of sciences of

the Republic of Kazakhstan, 2(384), pp.106-110.

Эшов, М., 2020. Impact of Financial Sustainability on Enterprise Value Expansion. Архив

научных исследований, (18).

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.