Hospitality Simulation Management Assignment: Revenue and Cash Flow

VerifiedAdded on 2022/08/12

|9

|974

|17

Homework Assignment

AI Summary

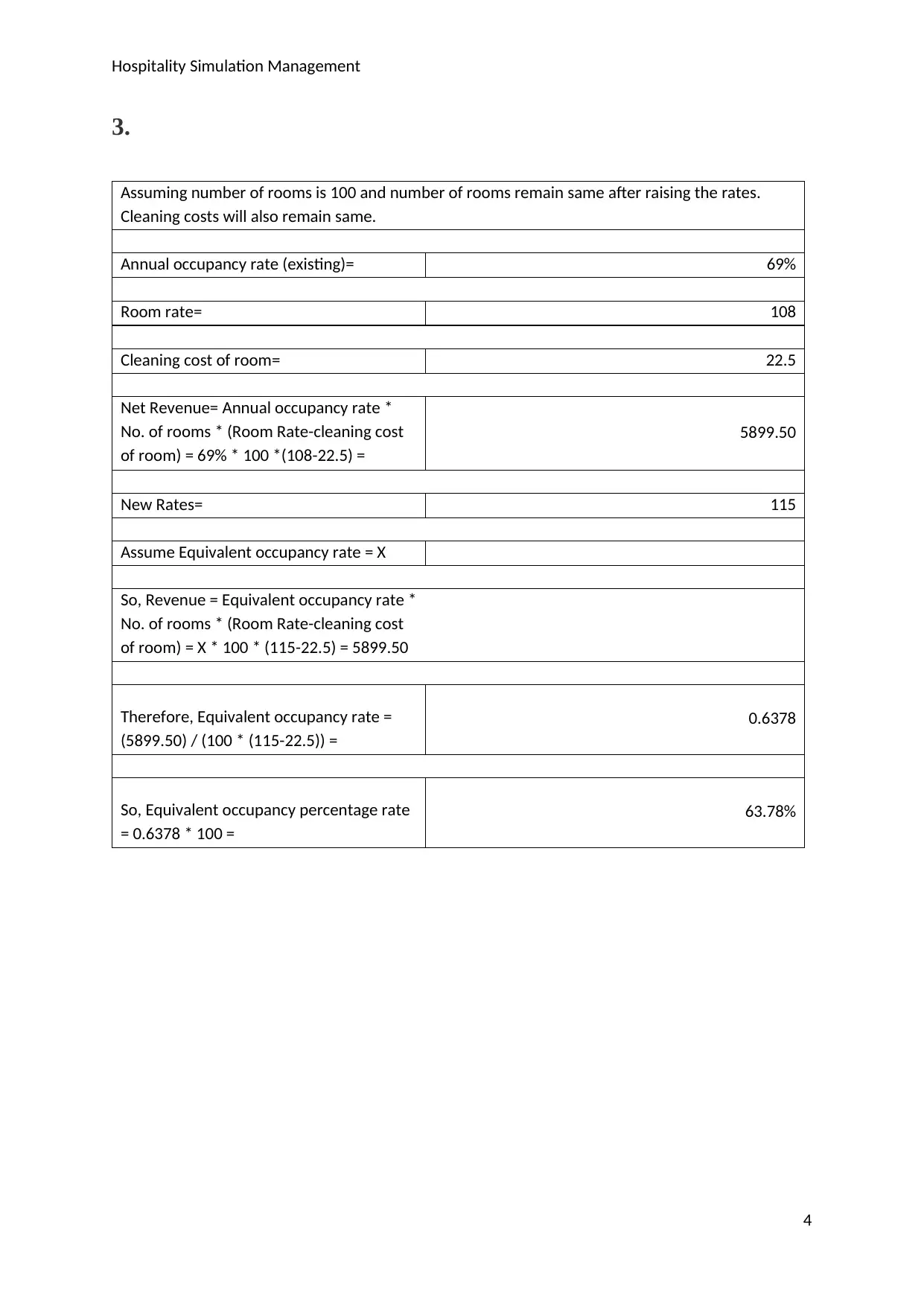

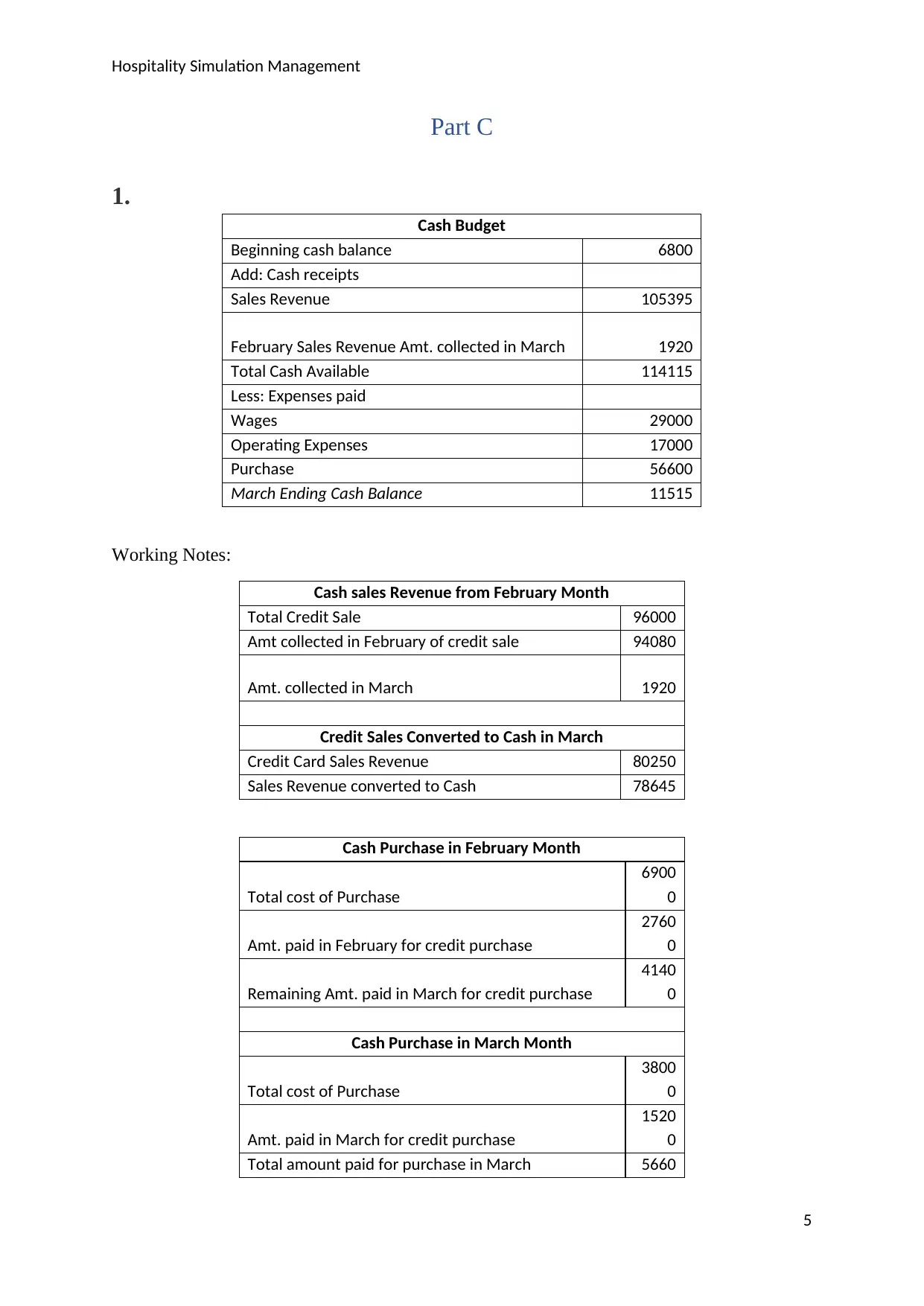

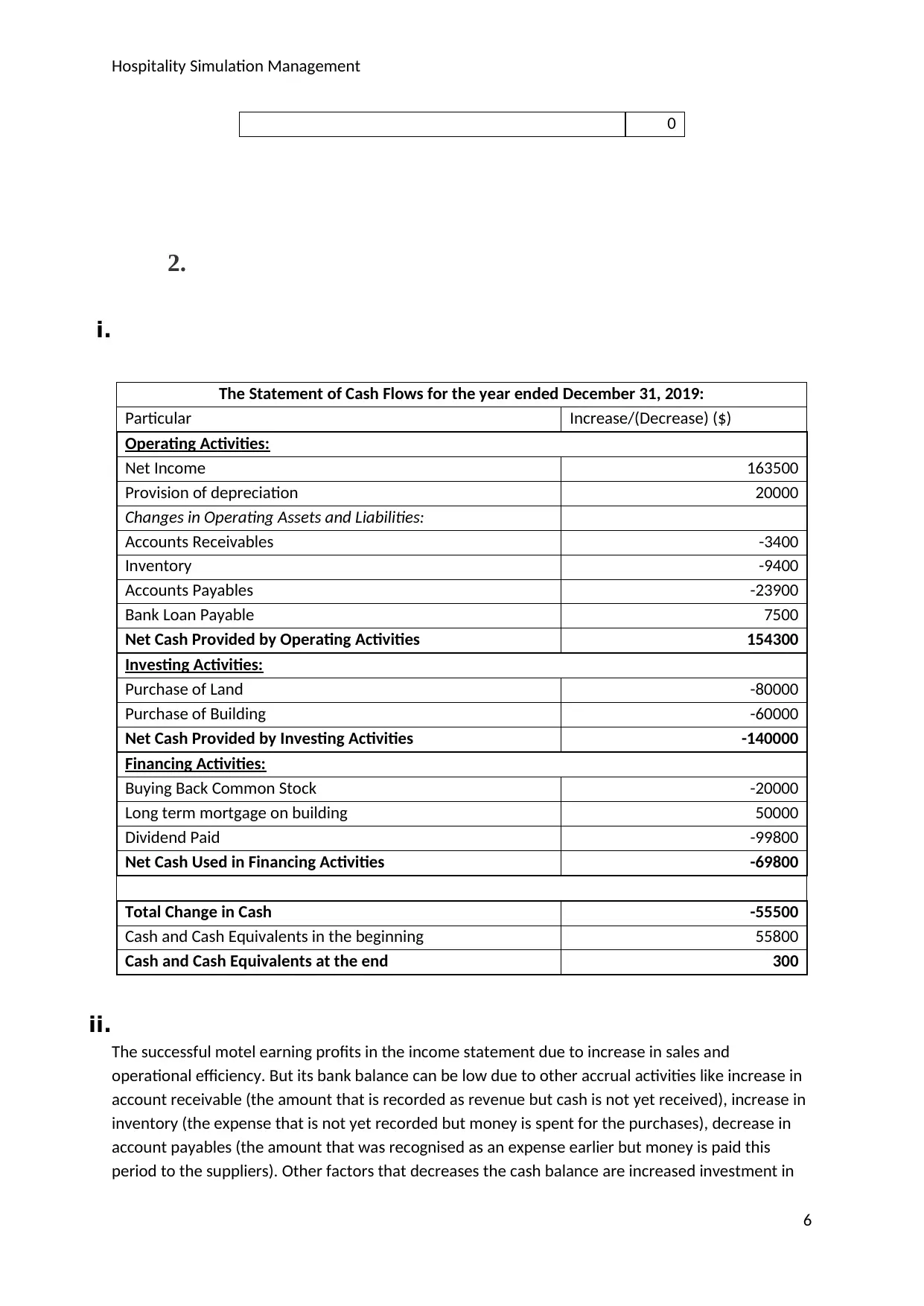

This assignment solution addresses a Hospitality Simulation Management scenario, encompassing financial analysis, revenue management, and cash flow projections. Part A focuses on understanding cash flow statements and depreciation. Part B explores revenue management strategies, including pricing adjustments, service offerings, and occupancy rate optimization. Part C presents a cash budget and a statement of cash flows, analyzing the motel's financial performance and identifying factors impacting its cash balance, such as accounts receivable, inventory, and investment decisions. The solution highlights the importance of balancing profitability with cash management, offering insights into how operational efficiency and strategic financial planning contribute to a business's financial health.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.