Hotel Grand Central Limited Financial Statement Presentation 2016

VerifiedAdded on 2023/06/16

|22

|3611

|282

Report

AI Summary

This report provides a comprehensive analysis of the financial statements of Hotel Grand Central Limited, a hotel business operating in multiple countries and listed on the Singapore stock exchange. The report covers the presentation of the balance sheet and trading, profit and loss account for the year ending 31st December 2016, adhering to the financial reporting framework and aiming to provide stakeholders with reliable information for making informed economic decisions. It also discusses the objectives of financial statements in meeting the information needs of various stakeholders, including investors, creditors, employees, and government entities. The report further explains two key methods of calculating depreciation on long-term operating assets: the straight-line method and the reducing balance method, detailing their applications and suitability for different types of assets. The financial statements are presented in Singapore dollars and include detailed workings for various income and expense items, along with earnings per share calculations. The report also recommends ways to improve financial reporting transparency and provide a true and fair view of the company's financial position.

Running Head: Presentation of Financial Statements

Hotel Grand Central Limited

Hotel Grand Central Limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Presentation of Financial Statements 1

Executive summary

This report covers the preparation of financial statements of Hotel Grand Central Limited.

The report also discusses the two key methods of calculating depreciation on the long term

operating assets of the entity. All the financial information relating to the company have been

presented in the Singapore currency as the company is headquartered in Singapore. Along

with the presentation of financial statements i.e. the balance sheet and trading Profit and Loss

Account, the report also covers the recommended manner of financial reporting to promote

the true and fair view of financial statements and to enhance the transparency in reporting

about the entity’s state of affairs.

Executive summary

This report covers the preparation of financial statements of Hotel Grand Central Limited.

The report also discusses the two key methods of calculating depreciation on the long term

operating assets of the entity. All the financial information relating to the company have been

presented in the Singapore currency as the company is headquartered in Singapore. Along

with the presentation of financial statements i.e. the balance sheet and trading Profit and Loss

Account, the report also covers the recommended manner of financial reporting to promote

the true and fair view of financial statements and to enhance the transparency in reporting

about the entity’s state of affairs.

Presentation of Financial Statements 2

Introduction

Hotel grand central Limited is engaged in the hotel business. It was incorporated in 1968

however it got listed on the Singapore stock exchange in 1978. It owns and manages the

hotels through its 5 segments located in 5 different countries. These countries are Singapore,

Malaysia, New Zealand, Australia and China. The hotel is also holding equity interests in

more than 10 hotels across Malaysia through its subsidiaries that are wholly owned by it. In

the entire Malaysian country, more than six hotel grand continental as well as hotel grand

crystal properties provides the range of facilities to the travellers. The hotel is also operating

under the group brand of grand hotel international in the entire Australia. The Australian

properties of the hotel are situated in many countries such as Melbourne, Adelaide, Hobart,

Brisbane and Launceston. The hotels of grand central limited in New Zealand are situated in

the business districts of Auckland as well as Wellington. The hotels offers additional facilities

like arranging conferences and other events of the corporate bodies along with restaurant

facilities. It has more than 5 venues catering for around 400 delegates (Reuters, 2017).

Introduction

Hotel grand central Limited is engaged in the hotel business. It was incorporated in 1968

however it got listed on the Singapore stock exchange in 1978. It owns and manages the

hotels through its 5 segments located in 5 different countries. These countries are Singapore,

Malaysia, New Zealand, Australia and China. The hotel is also holding equity interests in

more than 10 hotels across Malaysia through its subsidiaries that are wholly owned by it. In

the entire Malaysian country, more than six hotel grand continental as well as hotel grand

crystal properties provides the range of facilities to the travellers. The hotel is also operating

under the group brand of grand hotel international in the entire Australia. The Australian

properties of the hotel are situated in many countries such as Melbourne, Adelaide, Hobart,

Brisbane and Launceston. The hotels of grand central limited in New Zealand are situated in

the business districts of Auckland as well as Wellington. The hotels offers additional facilities

like arranging conferences and other events of the corporate bodies along with restaurant

facilities. It has more than 5 venues catering for around 400 delegates (Reuters, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Presentation of Financial Statements 3

Objectives of financial statements

Financial statements are prepared and presented with the intention of meeting the information

needs of intended users. Intended users are the stakeholders of the company who directly or

indirectly maintains the business relationships with the company. As the company is indulged

in the hotel operations business it may have a range of stakeholders such as the employees,

managers, clients or customers, investors or shareholders, providers of finance such as banks

and other financial institutions, government etc. Financial statements are prepared and

presented as per the regulatory requirements applicable to the reporting entity.

In the present report financial statements i.e. the balance sheet and the trading, profit and loss

account of Hotel Grand Central Limited are presented in the prescribed format that is

applicable to the listed companies of Singapore. The financial statements for the year ending

31st December, 2016 are presented with the intention of adhering to the financial reporting

framework. The main objective of such financial statements is to provide necessary and

reliable information to the stakeholders of the business. The presentation of financial

statements of Hotel Grand Central Limited is intended to achieve the true and fair view of the

financial position of the company. The financial information that is shared with the

stakeholders through the means of financial reports is contained the financial statements such

as trading, profit and loss account and balance sheet (Fraser, Ormiston & Fraser, 2010).

The presentation of financial statements is done in such a way that it can help the intended

users in making sound economic decisions. These financial statements covers the summary of

all the necessary transactions that the company has entered into and also the impact of other

significant events that has occurred during the financial year ending on 31st December, 2016

(Annual report, 2016). The preparation and presentation of financial statement is aimed to

Objectives of financial statements

Financial statements are prepared and presented with the intention of meeting the information

needs of intended users. Intended users are the stakeholders of the company who directly or

indirectly maintains the business relationships with the company. As the company is indulged

in the hotel operations business it may have a range of stakeholders such as the employees,

managers, clients or customers, investors or shareholders, providers of finance such as banks

and other financial institutions, government etc. Financial statements are prepared and

presented as per the regulatory requirements applicable to the reporting entity.

In the present report financial statements i.e. the balance sheet and the trading, profit and loss

account of Hotel Grand Central Limited are presented in the prescribed format that is

applicable to the listed companies of Singapore. The financial statements for the year ending

31st December, 2016 are presented with the intention of adhering to the financial reporting

framework. The main objective of such financial statements is to provide necessary and

reliable information to the stakeholders of the business. The presentation of financial

statements of Hotel Grand Central Limited is intended to achieve the true and fair view of the

financial position of the company. The financial information that is shared with the

stakeholders through the means of financial reports is contained the financial statements such

as trading, profit and loss account and balance sheet (Fraser, Ormiston & Fraser, 2010).

The presentation of financial statements is done in such a way that it can help the intended

users in making sound economic decisions. These financial statements covers the summary of

all the necessary transactions that the company has entered into and also the impact of other

significant events that has occurred during the financial year ending on 31st December, 2016

(Annual report, 2016). The preparation and presentation of financial statement is aimed to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Presentation of Financial Statements 4

influence the reader’s decision by providing complete and true picture of company’s state of

affairs.

The preparation and presentation of financial statements is undertaken by keeping in mind the

interest various stakeholders such as providers of finance in the company. As the company

has borrowed significant amount of funds from various banks and other financial institutions,

they seek to inquire about the solvency position of the company. These financial statements

are intended to provide relevant information to those providers of finance so that they can

assess company’s credit worthiness (Costello, 2011).

Moreover, the potential investors of the company seeks the financial information of the

company to understand the financial position of the company so that they can invest their

funds in the company. The presentation of financial statements is intended to deliver to them

all the necessary and relevant information about the company such as its profitability,

solvency and liquidity position (Healy & Palepu, 2012).

The employees and managers are also taken into consideration while presenting the financial

statements of the company so that they can have the proper knowledge of company’s

financial performance which will enable them to function accordingly in future. Such reports

will help them in formulating the necessary strategies and policies to achieve the company’s

goals and objectives (Freeman, 2010).

The presentation of financial statements of the company is also undertaken with the motive of

satisfying the governmental rules and regulations so that any legal consequences of non-

compliances can be prevented.

The financial statements are also intended to provide the information of company’s clients

and customers so that they can review the situation and performance of the company’s

influence the reader’s decision by providing complete and true picture of company’s state of

affairs.

The preparation and presentation of financial statements is undertaken by keeping in mind the

interest various stakeholders such as providers of finance in the company. As the company

has borrowed significant amount of funds from various banks and other financial institutions,

they seek to inquire about the solvency position of the company. These financial statements

are intended to provide relevant information to those providers of finance so that they can

assess company’s credit worthiness (Costello, 2011).

Moreover, the potential investors of the company seeks the financial information of the

company to understand the financial position of the company so that they can invest their

funds in the company. The presentation of financial statements is intended to deliver to them

all the necessary and relevant information about the company such as its profitability,

solvency and liquidity position (Healy & Palepu, 2012).

The employees and managers are also taken into consideration while presenting the financial

statements of the company so that they can have the proper knowledge of company’s

financial performance which will enable them to function accordingly in future. Such reports

will help them in formulating the necessary strategies and policies to achieve the company’s

goals and objectives (Freeman, 2010).

The presentation of financial statements of the company is also undertaken with the motive of

satisfying the governmental rules and regulations so that any legal consequences of non-

compliances can be prevented.

The financial statements are also intended to provide the information of company’s clients

and customers so that they can review the situation and performance of the company’s

Presentation of Financial Statements 5

business before getting associated with the company in any kind of business

deals(Armstrong, Guay, Weber, 2010).

Depreciation is an accounting system that is used to allocate the historical cost of any fixed

asset over the useful time span of that asset. Historical cost is the cost at which the asset is

acquired. Such cost is systematically reduced till the time value of assets become negligible.

Fixed assets like furniture, buildings, plant and machineries, motor vehicles etc. are

depreciated over their useful lives using various methods of depreciation. The depreciation is

charged to the asset because of the factors like efflux of time and their wear and tear nature.

Moreover, these assets are subject to obsolescence. Depreciation is charged to the assets in

order to determine the true and clear picture of business and to carry the depreciable assets at

the appropriate values in the financial statements. The two most common methods used to

calculate the depreciation on any tangible fixed asset are: Straight Line Method and Reducing

Balance Method. These methods are discussed below:

Straight line method:

Under this method the cost of the tangible fixed asset is distributed uniformly over the entire

useful life of the asset. The cost of asset covers all the expenses that are incurred to bring the

asset in the workable position such as freight charges, carriage expenses and the cost of

installation. While calculating the depreciation on these assets, if there is an estimate of

residual value at the end of life of asset then such residual value is reduced from the cost of

asset and then the remaining amount is distributed to the overall estimated life span of the

asset. Straight line method of depreciation is suitable for those tangible fixed assets that can

generate constant benefits. This method is more realistic in nature and is quite simple to be

applied. It is mostly preferred due to the uniformity of depreciation charges throughout the

life of asset. However, it is sometimes criticised because it does not take into account the

business before getting associated with the company in any kind of business

deals(Armstrong, Guay, Weber, 2010).

Depreciation is an accounting system that is used to allocate the historical cost of any fixed

asset over the useful time span of that asset. Historical cost is the cost at which the asset is

acquired. Such cost is systematically reduced till the time value of assets become negligible.

Fixed assets like furniture, buildings, plant and machineries, motor vehicles etc. are

depreciated over their useful lives using various methods of depreciation. The depreciation is

charged to the asset because of the factors like efflux of time and their wear and tear nature.

Moreover, these assets are subject to obsolescence. Depreciation is charged to the assets in

order to determine the true and clear picture of business and to carry the depreciable assets at

the appropriate values in the financial statements. The two most common methods used to

calculate the depreciation on any tangible fixed asset are: Straight Line Method and Reducing

Balance Method. These methods are discussed below:

Straight line method:

Under this method the cost of the tangible fixed asset is distributed uniformly over the entire

useful life of the asset. The cost of asset covers all the expenses that are incurred to bring the

asset in the workable position such as freight charges, carriage expenses and the cost of

installation. While calculating the depreciation on these assets, if there is an estimate of

residual value at the end of life of asset then such residual value is reduced from the cost of

asset and then the remaining amount is distributed to the overall estimated life span of the

asset. Straight line method of depreciation is suitable for those tangible fixed assets that can

generate constant benefits. This method is more realistic in nature and is quite simple to be

applied. It is mostly preferred due to the uniformity of depreciation charges throughout the

life of asset. However, it is sometimes criticised because it does not take into account the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Presentation of Financial Statements 6

actual usage factor of the asset. Also straight line method does not match the costs and

revenues of different types of long term assets. This method is not appropriate for those fixed

assets that involves rapidly developing technologies such as computers (Radu & Marius,

2011).

Reducing balance method:

This method is also known as diminishing balance method. To calculate depreciation under

this method the assets are depreciated at the historic cost in the 1st year at a particular rate of

depreciation and then from the 2nd year onwards the depreciation in calculated by applying

the rate of depreciation to the net book value of the asset. The rate at which depreciation is

calculated remains same through-out the life of asset. However, if there is any change in the

estimates regarding the rate or life of asset, then such changes are incorporated under this

method. Net book value is the value on which asset is carried in the statement of financial

position. The net book value or the carrying amount is calculated by reducing the

depreciation of the previous years from the historic cost of the asset (Sachs, Russell, Rogers

& Nadel, 2012). This method results in declining depreciation charges with each successive

year. It is mostly preferred due to the higher tax benefits that are available in the initial years.

Moreover, this method is mainly used for the assets that loses their values more quickly like

computers and vehicles. These assets have more efficiency in the earlier years. For such

assets diminishing balance method matches the depreciation charges in better ways with

actual decline in the fair market value of asset (Lawrence & Okechukwu, 2013).

actual usage factor of the asset. Also straight line method does not match the costs and

revenues of different types of long term assets. This method is not appropriate for those fixed

assets that involves rapidly developing technologies such as computers (Radu & Marius,

2011).

Reducing balance method:

This method is also known as diminishing balance method. To calculate depreciation under

this method the assets are depreciated at the historic cost in the 1st year at a particular rate of

depreciation and then from the 2nd year onwards the depreciation in calculated by applying

the rate of depreciation to the net book value of the asset. The rate at which depreciation is

calculated remains same through-out the life of asset. However, if there is any change in the

estimates regarding the rate or life of asset, then such changes are incorporated under this

method. Net book value is the value on which asset is carried in the statement of financial

position. The net book value or the carrying amount is calculated by reducing the

depreciation of the previous years from the historic cost of the asset (Sachs, Russell, Rogers

& Nadel, 2012). This method results in declining depreciation charges with each successive

year. It is mostly preferred due to the higher tax benefits that are available in the initial years.

Moreover, this method is mainly used for the assets that loses their values more quickly like

computers and vehicles. These assets have more efficiency in the earlier years. For such

assets diminishing balance method matches the depreciation charges in better ways with

actual decline in the fair market value of asset (Lawrence & Okechukwu, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Presentation of Financial Statements 7

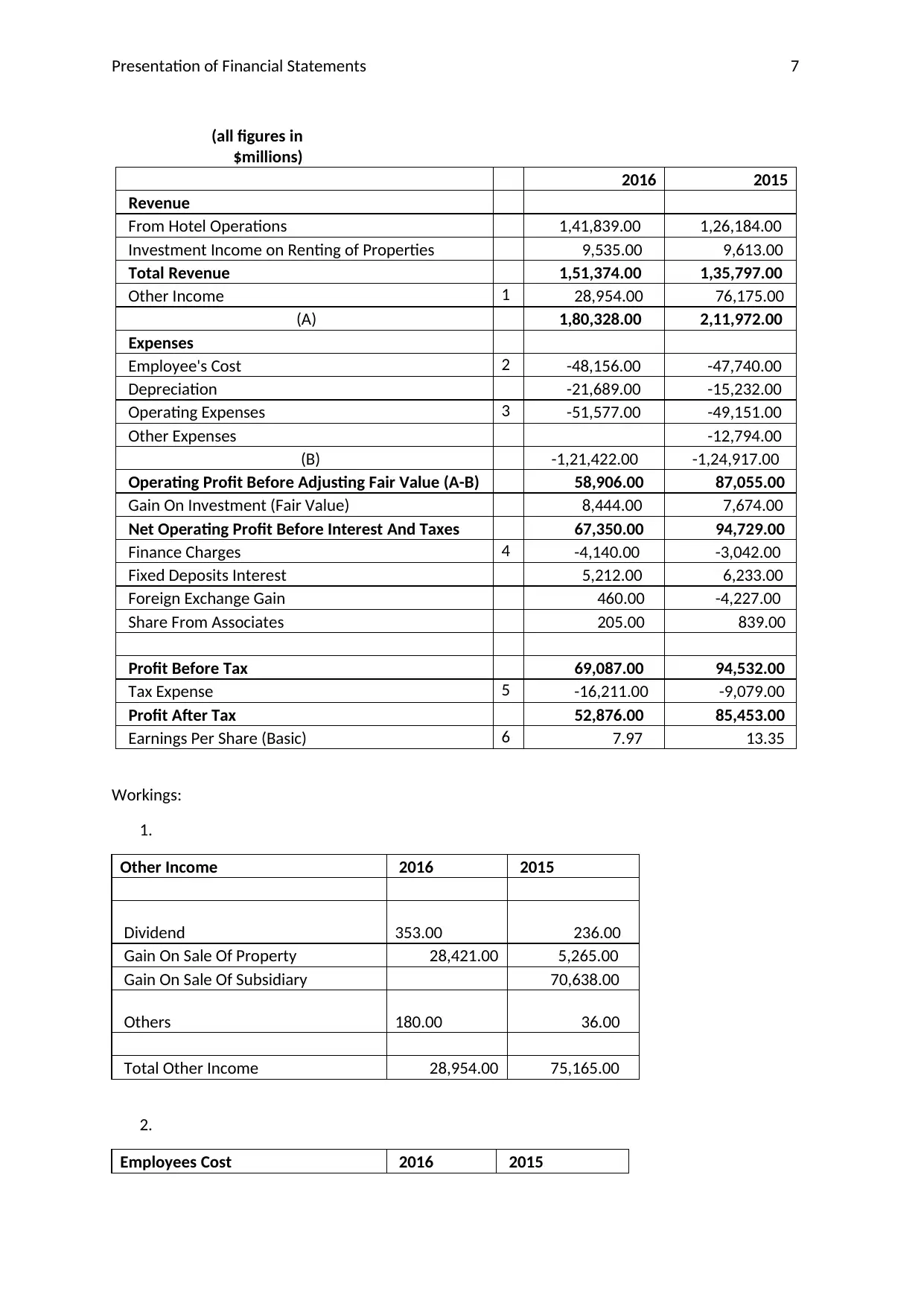

(all figures in

$millions)

2016 2015

Revenue

From Hotel Operations 1,41,839.00 1,26,184.00

Investment Income on Renting of Properties 9,535.00 9,613.00

Total Revenue 1,51,374.00 1,35,797.00

Other Income 1 28,954.00 76,175.00

(A) 1,80,328.00 2,11,972.00

Expenses

Employee's Cost 2 -48,156.00 -47,740.00

Depreciation -21,689.00 -15,232.00

Operating Expenses 3 -51,577.00 -49,151.00

Other Expenses -12,794.00

(B) -1,21,422.00 -1,24,917.00

Operating Profit Before Adjusting Fair Value (A-B) 58,906.00 87,055.00

Gain On Investment (Fair Value) 8,444.00 7,674.00

Net Operating Profit Before Interest And Taxes 67,350.00 94,729.00

Finance Charges 4 -4,140.00 -3,042.00

Fixed Deposits Interest 5,212.00 6,233.00

Foreign Exchange Gain 460.00 -4,227.00

Share From Associates 205.00 839.00

Profit Before Tax 69,087.00 94,532.00

Tax Expense 5 -16,211.00 -9,079.00

Profit After Tax 52,876.00 85,453.00

Earnings Per Share (Basic) 6 7.97 13.35

Workings:

1.

Other Income 2016 2015

Dividend 353.00 236.00

Gain On Sale Of Property 28,421.00 5,265.00

Gain On Sale Of Subsidiary 70,638.00

Others 180.00 36.00

Total Other Income 28,954.00 75,165.00

2.

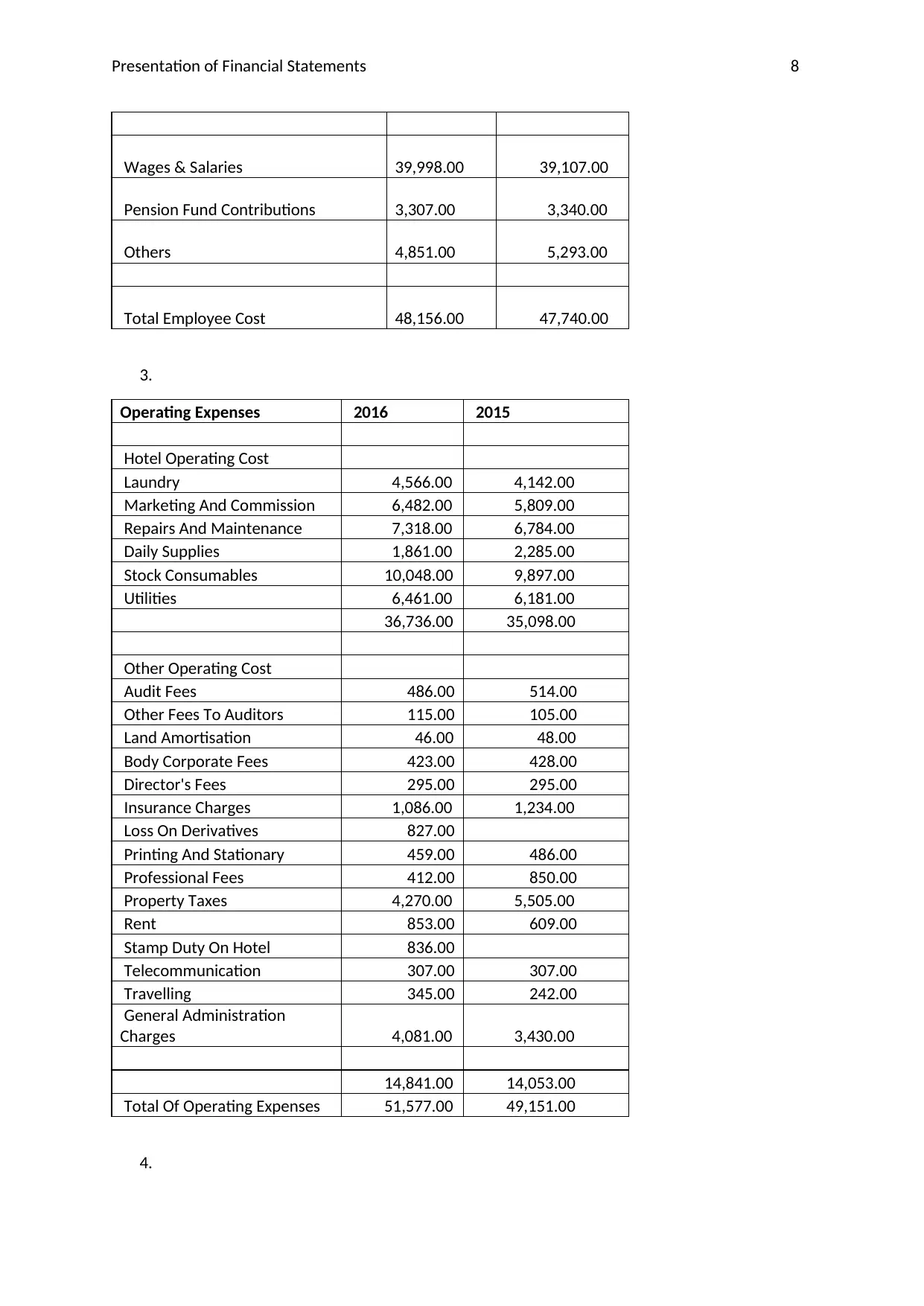

Employees Cost 2016 2015

(all figures in

$millions)

2016 2015

Revenue

From Hotel Operations 1,41,839.00 1,26,184.00

Investment Income on Renting of Properties 9,535.00 9,613.00

Total Revenue 1,51,374.00 1,35,797.00

Other Income 1 28,954.00 76,175.00

(A) 1,80,328.00 2,11,972.00

Expenses

Employee's Cost 2 -48,156.00 -47,740.00

Depreciation -21,689.00 -15,232.00

Operating Expenses 3 -51,577.00 -49,151.00

Other Expenses -12,794.00

(B) -1,21,422.00 -1,24,917.00

Operating Profit Before Adjusting Fair Value (A-B) 58,906.00 87,055.00

Gain On Investment (Fair Value) 8,444.00 7,674.00

Net Operating Profit Before Interest And Taxes 67,350.00 94,729.00

Finance Charges 4 -4,140.00 -3,042.00

Fixed Deposits Interest 5,212.00 6,233.00

Foreign Exchange Gain 460.00 -4,227.00

Share From Associates 205.00 839.00

Profit Before Tax 69,087.00 94,532.00

Tax Expense 5 -16,211.00 -9,079.00

Profit After Tax 52,876.00 85,453.00

Earnings Per Share (Basic) 6 7.97 13.35

Workings:

1.

Other Income 2016 2015

Dividend 353.00 236.00

Gain On Sale Of Property 28,421.00 5,265.00

Gain On Sale Of Subsidiary 70,638.00

Others 180.00 36.00

Total Other Income 28,954.00 75,165.00

2.

Employees Cost 2016 2015

Presentation of Financial Statements 8

Wages & Salaries 39,998.00 39,107.00

Pension Fund Contributions 3,307.00 3,340.00

Others 4,851.00 5,293.00

Total Employee Cost 48,156.00 47,740.00

3.

Operating Expenses 2016 2015

Hotel Operating Cost

Laundry 4,566.00 4,142.00

Marketing And Commission 6,482.00 5,809.00

Repairs And Maintenance 7,318.00 6,784.00

Daily Supplies 1,861.00 2,285.00

Stock Consumables 10,048.00 9,897.00

Utilities 6,461.00 6,181.00

36,736.00 35,098.00

Other Operating Cost

Audit Fees 486.00 514.00

Other Fees To Auditors 115.00 105.00

Land Amortisation 46.00 48.00

Body Corporate Fees 423.00 428.00

Director's Fees 295.00 295.00

Insurance Charges 1,086.00 1,234.00

Loss On Derivatives 827.00

Printing And Stationary 459.00 486.00

Professional Fees 412.00 850.00

Property Taxes 4,270.00 5,505.00

Rent 853.00 609.00

Stamp Duty On Hotel 836.00

Telecommunication 307.00 307.00

Travelling 345.00 242.00

General Administration

Charges 4,081.00 3,430.00

14,841.00 14,053.00

Total Of Operating Expenses 51,577.00 49,151.00

4.

Wages & Salaries 39,998.00 39,107.00

Pension Fund Contributions 3,307.00 3,340.00

Others 4,851.00 5,293.00

Total Employee Cost 48,156.00 47,740.00

3.

Operating Expenses 2016 2015

Hotel Operating Cost

Laundry 4,566.00 4,142.00

Marketing And Commission 6,482.00 5,809.00

Repairs And Maintenance 7,318.00 6,784.00

Daily Supplies 1,861.00 2,285.00

Stock Consumables 10,048.00 9,897.00

Utilities 6,461.00 6,181.00

36,736.00 35,098.00

Other Operating Cost

Audit Fees 486.00 514.00

Other Fees To Auditors 115.00 105.00

Land Amortisation 46.00 48.00

Body Corporate Fees 423.00 428.00

Director's Fees 295.00 295.00

Insurance Charges 1,086.00 1,234.00

Loss On Derivatives 827.00

Printing And Stationary 459.00 486.00

Professional Fees 412.00 850.00

Property Taxes 4,270.00 5,505.00

Rent 853.00 609.00

Stamp Duty On Hotel 836.00

Telecommunication 307.00 307.00

Travelling 345.00 242.00

General Administration

Charges 4,081.00 3,430.00

14,841.00 14,053.00

Total Of Operating Expenses 51,577.00 49,151.00

4.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Presentation of Financial Statements 9

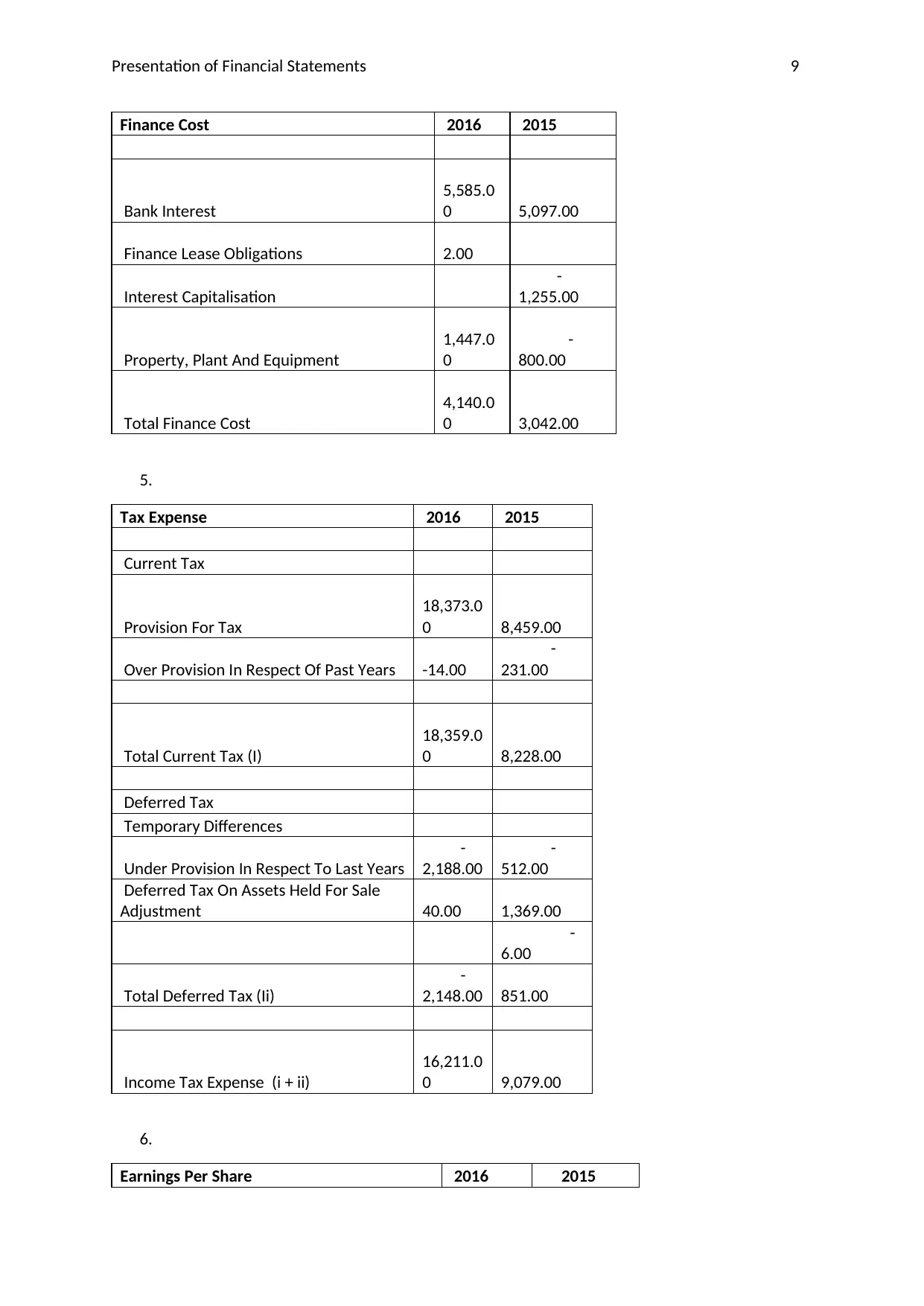

Finance Cost 2016 2015

Bank Interest

5,585.0

0 5,097.00

Finance Lease Obligations 2.00

Interest Capitalisation

-

1,255.00

Property, Plant And Equipment

1,447.0

0

-

800.00

Total Finance Cost

4,140.0

0 3,042.00

5.

Tax Expense 2016 2015

Current Tax

Provision For Tax

18,373.0

0 8,459.00

Over Provision In Respect Of Past Years -14.00

-

231.00

Total Current Tax (I)

18,359.0

0 8,228.00

Deferred Tax

Temporary Differences

Under Provision In Respect To Last Years

-

2,188.00

-

512.00

Deferred Tax On Assets Held For Sale

Adjustment 40.00 1,369.00

-

6.00

Total Deferred Tax (Ii)

-

2,148.00 851.00

Income Tax Expense (i + ii)

16,211.0

0 9,079.00

6.

Earnings Per Share 2016 2015

Finance Cost 2016 2015

Bank Interest

5,585.0

0 5,097.00

Finance Lease Obligations 2.00

Interest Capitalisation

-

1,255.00

Property, Plant And Equipment

1,447.0

0

-

800.00

Total Finance Cost

4,140.0

0 3,042.00

5.

Tax Expense 2016 2015

Current Tax

Provision For Tax

18,373.0

0 8,459.00

Over Provision In Respect Of Past Years -14.00

-

231.00

Total Current Tax (I)

18,359.0

0 8,228.00

Deferred Tax

Temporary Differences

Under Provision In Respect To Last Years

-

2,188.00

-

512.00

Deferred Tax On Assets Held For Sale

Adjustment 40.00 1,369.00

-

6.00

Total Deferred Tax (Ii)

-

2,148.00 851.00

Income Tax Expense (i + ii)

16,211.0

0 9,079.00

6.

Earnings Per Share 2016 2015

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Presentation of Financial Statements 10

Profit Available To Shareholders 52,876.00 85,453.00

Weighted Average Number of Shares

663033.0

0 640169.00

EPS (cents per share) 7.97 13.35

Profit Available To Shareholders 52,876.00 85,453.00

Weighted Average Number of Shares

663033.0

0 640169.00

EPS (cents per share) 7.97 13.35

Presentation of Financial Statements 11

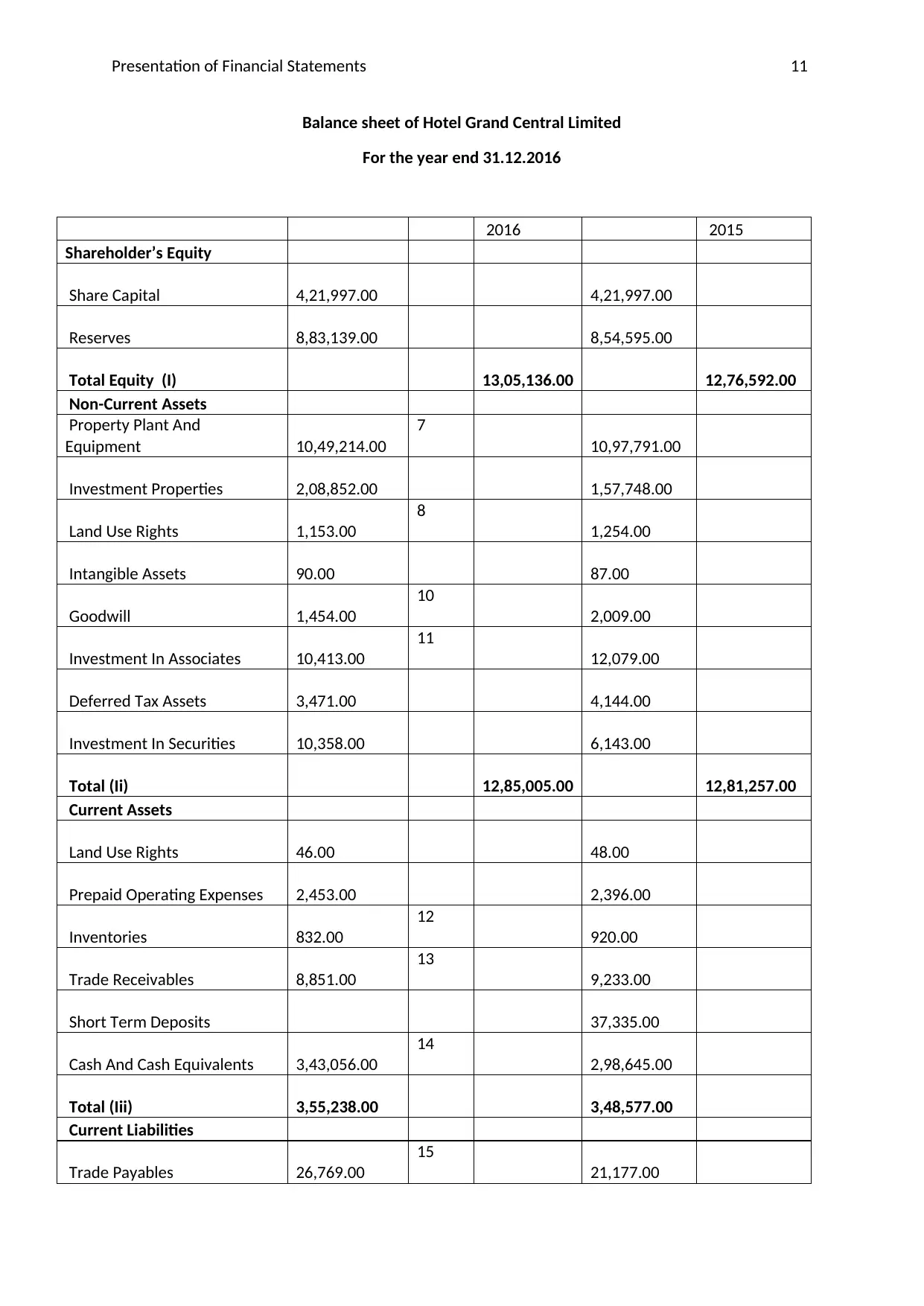

Balance sheet of Hotel Grand Central Limited

For the year end 31.12.2016

2016 2015

Shareholder’s Equity

Share Capital 4,21,997.00 4,21,997.00

Reserves 8,83,139.00 8,54,595.00

Total Equity (I) 13,05,136.00 12,76,592.00

Non-Current Assets

Property Plant And

Equipment 10,49,214.00

7

10,97,791.00

Investment Properties 2,08,852.00 1,57,748.00

Land Use Rights 1,153.00

8

1,254.00

Intangible Assets 90.00 87.00

Goodwill 1,454.00

10

2,009.00

Investment In Associates 10,413.00

11

12,079.00

Deferred Tax Assets 3,471.00 4,144.00

Investment In Securities 10,358.00 6,143.00

Total (Ii) 12,85,005.00 12,81,257.00

Current Assets

Land Use Rights 46.00 48.00

Prepaid Operating Expenses 2,453.00 2,396.00

Inventories 832.00

12

920.00

Trade Receivables 8,851.00

13

9,233.00

Short Term Deposits 37,335.00

Cash And Cash Equivalents 3,43,056.00

14

2,98,645.00

Total (Iii) 3,55,238.00 3,48,577.00

Current Liabilities

Trade Payables 26,769.00

15

21,177.00

Balance sheet of Hotel Grand Central Limited

For the year end 31.12.2016

2016 2015

Shareholder’s Equity

Share Capital 4,21,997.00 4,21,997.00

Reserves 8,83,139.00 8,54,595.00

Total Equity (I) 13,05,136.00 12,76,592.00

Non-Current Assets

Property Plant And

Equipment 10,49,214.00

7

10,97,791.00

Investment Properties 2,08,852.00 1,57,748.00

Land Use Rights 1,153.00

8

1,254.00

Intangible Assets 90.00 87.00

Goodwill 1,454.00

10

2,009.00

Investment In Associates 10,413.00

11

12,079.00

Deferred Tax Assets 3,471.00 4,144.00

Investment In Securities 10,358.00 6,143.00

Total (Ii) 12,85,005.00 12,81,257.00

Current Assets

Land Use Rights 46.00 48.00

Prepaid Operating Expenses 2,453.00 2,396.00

Inventories 832.00

12

920.00

Trade Receivables 8,851.00

13

9,233.00

Short Term Deposits 37,335.00

Cash And Cash Equivalents 3,43,056.00

14

2,98,645.00

Total (Iii) 3,55,238.00 3,48,577.00

Current Liabilities

Trade Payables 26,769.00

15

21,177.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.