Cost and Performance Management: A Case Study of Hotel Elephant

VerifiedAdded on 2023/03/31

|11

|2325

|421

Report

AI Summary

This report provides a comprehensive analysis of cost and performance management at The Hotel Elephant, focusing on the implications of the budget and the hotel's financial standing. It examines cost control measures, performance analysis, and cost-revenue dynamics, identifying key areas of concern such as advertising expenses, labor costs, and repair & maintenance expenditures. Recommendations include cross-training staff, exploring biodegradable energy sources, and leveraging digital marketing strategies to reduce costs and enhance revenue. The report concludes that Hotel Elephant can improve its financial performance by carefully managing expenses, focusing on delivering quality services, and proactively addressing non-operating costs to increase profitability. Desklib provides access to similar solved assignments and study tools for students.

Cost and Performance Management

6/7/2019

6/7/2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost and performance management 1

Executive summary

Budgeting is one of the most important tools that are used by the company to analyse

where the company is and where it wants to reach in future. In this report, The Hotel

Elephant has been considered to understand the implications of the budget and whether the

situation is favourable or not for the hotel. The report also talks about the control of the cost

and the overall recommendations to enhance the performance of the Hotel Elephant.

Executive summary

Budgeting is one of the most important tools that are used by the company to analyse

where the company is and where it wants to reach in future. In this report, The Hotel

Elephant has been considered to understand the implications of the budget and whether the

situation is favourable or not for the hotel. The report also talks about the control of the cost

and the overall recommendations to enhance the performance of the Hotel Elephant.

Cost and performance management 2

Table of Contents

Introduction...........................................................................................................................................3

Part 1.....................................................................................................................................................3

Cost control...........................................................................................................................................3

Part 2.....................................................................................................................................................4

Performance Analysis............................................................................................................................4

Part 3.....................................................................................................................................................5

Cost and Revenue Analysis...................................................................................................................5

Make a plan...........................................................................................................................................6

Recommendations.................................................................................................................................6

Conclusion.............................................................................................................................................7

References.............................................................................................................................................8

Appendix...............................................................................................................................................9

Table of Contents

Introduction...........................................................................................................................................3

Part 1.....................................................................................................................................................3

Cost control...........................................................................................................................................3

Part 2.....................................................................................................................................................4

Performance Analysis............................................................................................................................4

Part 3.....................................................................................................................................................5

Cost and Revenue Analysis...................................................................................................................5

Make a plan...........................................................................................................................................6

Recommendations.................................................................................................................................6

Conclusion.............................................................................................................................................7

References.............................................................................................................................................8

Appendix...............................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost and performance management 3

Introduction

Budgeting in the tourism sector is the one of the most crucial factor in growing the

industry of the tourism and hospitality. It acts as a planning pillar that can create a way for

the management to move ahead and secure greater market share in the industry. It not covers

a specific time frame at the same time with the help of the financial plans the company has

the clarity what the actual destination is. In order to find out the income statement is prepared

and it is compared against the budgeted results. If there are any variance it can be found out

and the necessary initiatives can be taken to overcome the situation. The budgets are

necessary for the strategic decision making and the internal development of the organization

(Vukovic, 2016).

Planning and cost control incorporates the nutty gritty estimation of costs, the setting of

concurred spending plans, and control of expenses against that financial limit. Planning of the

budget incorporates the three major stages which are, arranging, control of the costs and

auditing (Turner, 2017). It will probably include the following scenarios as well.

Decide the salary and consumption profiles for the work;

Create spending plans and line up with subsidizing;

Actualize frameworks to oversee salary and consumption

Part 1

Cost control

There are different types of the cost associated with the Hotel Elephant, which can be

bifurcated into the fixed and the variable expenses. The fixed expenses are of static nature

and they are bound to be incurred irrespective of the years. The variable expense on the other

hand is those which are of irregular nature and might fluctuate. As per the income statement

of the Hotel Elephant the following are the fixed and the variable expenses and the

recommendations on how to control them (Ivanova, Ivano & Magnini, 2016).

Advertising expenses are the one that have been higher than the budgeted amount.

The advertising costs have been increased from $3937 to $4953. These costs can be

controlled by understanding the fact that at times the marketing is not understood by a

large mass and just throwing money on the advertising would only increase the cost of

Introduction

Budgeting in the tourism sector is the one of the most crucial factor in growing the

industry of the tourism and hospitality. It acts as a planning pillar that can create a way for

the management to move ahead and secure greater market share in the industry. It not covers

a specific time frame at the same time with the help of the financial plans the company has

the clarity what the actual destination is. In order to find out the income statement is prepared

and it is compared against the budgeted results. If there are any variance it can be found out

and the necessary initiatives can be taken to overcome the situation. The budgets are

necessary for the strategic decision making and the internal development of the organization

(Vukovic, 2016).

Planning and cost control incorporates the nutty gritty estimation of costs, the setting of

concurred spending plans, and control of expenses against that financial limit. Planning of the

budget incorporates the three major stages which are, arranging, control of the costs and

auditing (Turner, 2017). It will probably include the following scenarios as well.

Decide the salary and consumption profiles for the work;

Create spending plans and line up with subsidizing;

Actualize frameworks to oversee salary and consumption

Part 1

Cost control

There are different types of the cost associated with the Hotel Elephant, which can be

bifurcated into the fixed and the variable expenses. The fixed expenses are of static nature

and they are bound to be incurred irrespective of the years. The variable expense on the other

hand is those which are of irregular nature and might fluctuate. As per the income statement

of the Hotel Elephant the following are the fixed and the variable expenses and the

recommendations on how to control them (Ivanova, Ivano & Magnini, 2016).

Advertising expenses are the one that have been higher than the budgeted amount.

The advertising costs have been increased from $3937 to $4953. These costs can be

controlled by understanding the fact that at times the marketing is not understood by a

large mass and just throwing money on the advertising would only increase the cost of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost and performance management 4

the hotel. The quality services will act as the word of mouth for the hotel (Taylor,

2018).

Labour consumes nearly 50% of the hotel expenses and in order to curtail the expense

the hotel must cross train the staff for hotels like Hotel Elephant.

Casual employee wages cannot be controlled as such, however if the existing

employees are made aware with the necessary skills the future cost can be retained.

The hiring costs can also be reduced if the management hires the inexperienced

people and are willing to spend on the enhancement of the skills rather than paying

more than what the training would cost.

The electricity charges can be controlled by shifting to the biodegradable energy or by

using the solar systems.

The water charges can be controlled by recycling of the water and by applying the

automatic tabs.

The better management of the cost would lie where the Hotel tries to circulate the

money in house only to cover most of the costs (Turner & Coote, 2018).

Credit card commission can be discussed with the bank for making the single long-

term payment rather than doing it as a pay as you go as this will control the cost.

Part 2

Performance Analysis

A performance analysis plan is a spending that mirrors the contribution of assets and

the yield of administrations for every unit of an association. This kind of spending plan is

usually utilized by government bodies to demonstrate the connection between citizen reserves

and the result of administrations given by bureaucratic, state, or neighbourhood governments

(Phillips, Barnes, Zigan & Schegg, 2017).

In order to manage the tourism and the hospitality sector it seems to be more

troublesome than ever. Expanded requests set by buyers, rivalry and contracting supervisory

groups have brought about more enthusiasm for quality administration rehearses. The client’s

decision is built on the basis of the competition prevailing in the market, administration

desires, and at last the estimation of the dollar spent. As the hotel industry business moves

toward becoming increasingly focused, experts in the field are searching for approaches to

pick up an upper hand, draw in, and hold visitors. The nature of administration has been

the hotel. The quality services will act as the word of mouth for the hotel (Taylor,

2018).

Labour consumes nearly 50% of the hotel expenses and in order to curtail the expense

the hotel must cross train the staff for hotels like Hotel Elephant.

Casual employee wages cannot be controlled as such, however if the existing

employees are made aware with the necessary skills the future cost can be retained.

The hiring costs can also be reduced if the management hires the inexperienced

people and are willing to spend on the enhancement of the skills rather than paying

more than what the training would cost.

The electricity charges can be controlled by shifting to the biodegradable energy or by

using the solar systems.

The water charges can be controlled by recycling of the water and by applying the

automatic tabs.

The better management of the cost would lie where the Hotel tries to circulate the

money in house only to cover most of the costs (Turner & Coote, 2018).

Credit card commission can be discussed with the bank for making the single long-

term payment rather than doing it as a pay as you go as this will control the cost.

Part 2

Performance Analysis

A performance analysis plan is a spending that mirrors the contribution of assets and

the yield of administrations for every unit of an association. This kind of spending plan is

usually utilized by government bodies to demonstrate the connection between citizen reserves

and the result of administrations given by bureaucratic, state, or neighbourhood governments

(Phillips, Barnes, Zigan & Schegg, 2017).

In order to manage the tourism and the hospitality sector it seems to be more

troublesome than ever. Expanded requests set by buyers, rivalry and contracting supervisory

groups have brought about more enthusiasm for quality administration rehearses. The client’s

decision is built on the basis of the competition prevailing in the market, administration

desires, and at last the estimation of the dollar spent. As the hotel industry business moves

toward becoming increasingly focused, experts in the field are searching for approaches to

pick up an upper hand, draw in, and hold visitors. The nature of administration has been

Cost and performance management 5

observed to be the manner in which hotel’s associations separate themselves (Phillips, Zigan

Silva & Schegg, 2015).

From the performance analysis of the Elephant hotel it can be stated that the company

has performed altogether good and smoothly in comparison to the budgeted figures however

there are some areas such as the advertising, credit card commission, hiring of the kitchen

utensils, cost of the repair and the maintenance and the overall net profit has turned into more

achievable profit. This situation mainly because of the negligence towards the areas

determined above. The repair and maintenance increased from $9375 to $12531 and increase

by 25%, which is a huge expense surge. This needs to be controlled by the management as

this would increase with faster growth as compared to the previous year. The amount of the

credit card on the other hand have increased from $13590 to $16192, this could have been

dealt with care by dealing in the cash transactions. The electricity expense has not increased

much; hence the hotel can improve the existing performance well (Duan, Yu, Cao & Levy,

2016).

Part 3

Cost and Revenue Analysis

Cost analysis supports the company to identify the expected costs and benefits of specific

asset, new product, or plan of the action. The in-depth analysis related to the cost can reveal

the hidden costs that are embedded within the company. Further, the revenue analysis shows

the amount that has been generated from the sales of their product and services. In order to

generate more, the company can enhance the prices of the present goods and services along

with this they can offer the additional services. Collectively, the analysis of cost and revenue

shows that they keep the cost at the minimum so that they can attain maximum revenue. After

the overall analysis, it can be concluded that the BOB and BIB can make sure to follow

certain steps that could necessarily reduce the costs and they would not have to worry about

the business. The proactive decisions shall also be taken with regards to where to spend the

money and how much to spent to (Akbar & Tracogna, 2018). The major cost drivers that

have been pointed out are the non-operating expenses because of which the hotel is suffering

from the low profits. The sales could be increased my diversifying in the areas or by

providing the discount and the schemes. The Hotel can also offer the package deals to attract

the large number of the tourists and the local customer as well. The daily activities can be

organized for the entertainment purpose. The facility of the pool can be made access by the

customers to have more incomings of the people. All these strategies can surely increase the

sales and reduce the costs and can make a balance between the revenue as well as the costs

(Arbelo, Pérez-Gómez & Arbelo-Pérez, 2017).

observed to be the manner in which hotel’s associations separate themselves (Phillips, Zigan

Silva & Schegg, 2015).

From the performance analysis of the Elephant hotel it can be stated that the company

has performed altogether good and smoothly in comparison to the budgeted figures however

there are some areas such as the advertising, credit card commission, hiring of the kitchen

utensils, cost of the repair and the maintenance and the overall net profit has turned into more

achievable profit. This situation mainly because of the negligence towards the areas

determined above. The repair and maintenance increased from $9375 to $12531 and increase

by 25%, which is a huge expense surge. This needs to be controlled by the management as

this would increase with faster growth as compared to the previous year. The amount of the

credit card on the other hand have increased from $13590 to $16192, this could have been

dealt with care by dealing in the cash transactions. The electricity expense has not increased

much; hence the hotel can improve the existing performance well (Duan, Yu, Cao & Levy,

2016).

Part 3

Cost and Revenue Analysis

Cost analysis supports the company to identify the expected costs and benefits of specific

asset, new product, or plan of the action. The in-depth analysis related to the cost can reveal

the hidden costs that are embedded within the company. Further, the revenue analysis shows

the amount that has been generated from the sales of their product and services. In order to

generate more, the company can enhance the prices of the present goods and services along

with this they can offer the additional services. Collectively, the analysis of cost and revenue

shows that they keep the cost at the minimum so that they can attain maximum revenue. After

the overall analysis, it can be concluded that the BOB and BIB can make sure to follow

certain steps that could necessarily reduce the costs and they would not have to worry about

the business. The proactive decisions shall also be taken with regards to where to spend the

money and how much to spent to (Akbar & Tracogna, 2018). The major cost drivers that

have been pointed out are the non-operating expenses because of which the hotel is suffering

from the low profits. The sales could be increased my diversifying in the areas or by

providing the discount and the schemes. The Hotel can also offer the package deals to attract

the large number of the tourists and the local customer as well. The daily activities can be

organized for the entertainment purpose. The facility of the pool can be made access by the

customers to have more incomings of the people. All these strategies can surely increase the

sales and reduce the costs and can make a balance between the revenue as well as the costs

(Arbelo, Pérez-Gómez & Arbelo-Pérez, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost and performance management 6

Make a plan

Identification of cost

The cost that has been identified in the income and expense statement are advertising, bank

charges, casual employee wages, food delivery vehicle service costs, property insurance,

repairs and maintenance, waste removal, website hosting charges, and Netflix subscription

etc. While making an appropriate plan, it is realised that earlier all the cost are assumed as

variable. In order to adjust the plan and make it more realistic, the company will consider

casual employee wages and electricity are fixed.

Considering variable cost and fixed cost

Fixed cost are those expenses that remain same even when the number of units sales or the

level changes. To have an effective income and expense sheet, it is seen that electricity and

casual employee wage are considered as fixed.

Variable cost is a cost that differs from the level of production and sales.

Variances

While viewing the excel sheet, it is seen that when casual employee wages and electricity is

assumed as fixed. According to actual income expenses, electricity and gases are $37,125 and

budgeted is assumed as $37000, so the unfavourable factor of negative $125 will be

eliminated. Casual employees’ wages is seen as $180625 according to actual income

expenses whereas, budgeted is estimated as $ 187500 which is favourable but it will be fixed

as per actual.

Recommendations

It is important to make a proper decision in regards to the classification of variable and fixed

cost. The basis on which this classification should rely upon should consider the demand of

the customers because the increase in expenses can be controlled by the company only when

the cost is variable. It is mandatory for a business to apply correct costing method so that the

company can identify correct profits. As per the recent criteria, the company should apply

ABC costing. Different allocation to different costs is important as cost per unit based on

activity will be more accurate and it will be reflected as per the actual efforts related to the

production. The companies have begun to use ABC costing information so that it could

practise management based on activity.

Make a plan

Identification of cost

The cost that has been identified in the income and expense statement are advertising, bank

charges, casual employee wages, food delivery vehicle service costs, property insurance,

repairs and maintenance, waste removal, website hosting charges, and Netflix subscription

etc. While making an appropriate plan, it is realised that earlier all the cost are assumed as

variable. In order to adjust the plan and make it more realistic, the company will consider

casual employee wages and electricity are fixed.

Considering variable cost and fixed cost

Fixed cost are those expenses that remain same even when the number of units sales or the

level changes. To have an effective income and expense sheet, it is seen that electricity and

casual employee wage are considered as fixed.

Variable cost is a cost that differs from the level of production and sales.

Variances

While viewing the excel sheet, it is seen that when casual employee wages and electricity is

assumed as fixed. According to actual income expenses, electricity and gases are $37,125 and

budgeted is assumed as $37000, so the unfavourable factor of negative $125 will be

eliminated. Casual employees’ wages is seen as $180625 according to actual income

expenses whereas, budgeted is estimated as $ 187500 which is favourable but it will be fixed

as per actual.

Recommendations

It is important to make a proper decision in regards to the classification of variable and fixed

cost. The basis on which this classification should rely upon should consider the demand of

the customers because the increase in expenses can be controlled by the company only when

the cost is variable. It is mandatory for a business to apply correct costing method so that the

company can identify correct profits. As per the recent criteria, the company should apply

ABC costing. Different allocation to different costs is important as cost per unit based on

activity will be more accurate and it will be reflected as per the actual efforts related to the

production. The companies have begun to use ABC costing information so that it could

practise management based on activity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost and performance management 7

Further, it is recommended to the company to conduct the advertisement through digital and

social media, as this will reduce the cost. The social media tools that can be used by the

company include Facebook, twitter, and many others. On the other hand, digital media

include the e-mail and other online modes. This effectively contributes in reducing the cost

and generating the maximum awareness.

Conclusion

From the above analysis it can be concluded that the Hotel Elephant has performed

much better in comparison to the budgeted figures. All the hotel needs to do is, to curb the

extra costs that can be minimised easily and the net loss of the company can be turned into

profits. Moreover the hotel must make expense wisely and focus on delivering the quality

services. The brand of the hotel will eventually grow and the demand will rise.

Further, it is recommended to the company to conduct the advertisement through digital and

social media, as this will reduce the cost. The social media tools that can be used by the

company include Facebook, twitter, and many others. On the other hand, digital media

include the e-mail and other online modes. This effectively contributes in reducing the cost

and generating the maximum awareness.

Conclusion

From the above analysis it can be concluded that the Hotel Elephant has performed

much better in comparison to the budgeted figures. All the hotel needs to do is, to curb the

extra costs that can be minimised easily and the net loss of the company can be turned into

profits. Moreover the hotel must make expense wisely and focus on delivering the quality

services. The brand of the hotel will eventually grow and the demand will rise.

Cost and performance management 8

References

Akbar, Y. H., & Tracogna, A. (2018). The sharing economy and the future of the hotel

industry: Transaction cost theory and platform economics. International Journal of

Hospitality Management, 71, 91-101.

Arbelo, A., Pérez-Gómez, P., & Arbelo-Pérez, M. (2017). Cost efficiency and its

determinants in the hotel industry. Tourism Economics, 23(5), 1056-1068.

Duan, W., Yu, Y., Cao, Q., & Levy, S. (2016). Exploring the impact of social media on hotel

service performance: a sentimental analysis approach. Cornell Hospitality

Quarterly, 57(3), 282-296.

Ivanova, M., Ivanov, S., & Magnini, V. P. (2016). Handbook of hotel chain management.

Phillips, P., Barnes, S., Zigan, K., & Schegg, R. (2017). Understanding the impact of online

reviews on hotel performance: an empirical analysis. Journal of Travel

Research, 56(2), 235-249.

Phillips, P., Zigan, K., Silva, M. M. S., & Schegg, R. (2015). The interactive effects of online

reviews on the determinants of Swiss hotel performance: A neural network

analysis. Tourism Management, 50, 130-141.

Taylor, D. (2018). 7 Straightforward Ways to Cut Back on Hotel Costs. Retrieved from

https://blog.capterra.com/7-straightforward-ways-to-cut-back-on-hotel-costs/

Turner, M. J. (2017). Precursors to the financial and strategic orientation of hotel property

capital budgeting. Journal of Hospitality and Tourism Management, 33, 31-42.

Turner, M. J., & Coote, L. V. (2018). Incentives and monitoring: impact on the financial and

non-financial orientation of capital budgeting. Meditari Accountancy Research, 26(1),

122-144.

Vukovic, D. (2016). BUDGETING P ROCESS IN TOURISM COMPANIES FOR THE

PURPOSE OF IMPROVING THE QUALITY OF TOURISM PRODUCTS. Retrieved

from file:///C:/Users/Manita/Downloads/181-186.pdf

References

Akbar, Y. H., & Tracogna, A. (2018). The sharing economy and the future of the hotel

industry: Transaction cost theory and platform economics. International Journal of

Hospitality Management, 71, 91-101.

Arbelo, A., Pérez-Gómez, P., & Arbelo-Pérez, M. (2017). Cost efficiency and its

determinants in the hotel industry. Tourism Economics, 23(5), 1056-1068.

Duan, W., Yu, Y., Cao, Q., & Levy, S. (2016). Exploring the impact of social media on hotel

service performance: a sentimental analysis approach. Cornell Hospitality

Quarterly, 57(3), 282-296.

Ivanova, M., Ivanov, S., & Magnini, V. P. (2016). Handbook of hotel chain management.

Phillips, P., Barnes, S., Zigan, K., & Schegg, R. (2017). Understanding the impact of online

reviews on hotel performance: an empirical analysis. Journal of Travel

Research, 56(2), 235-249.

Phillips, P., Zigan, K., Silva, M. M. S., & Schegg, R. (2015). The interactive effects of online

reviews on the determinants of Swiss hotel performance: A neural network

analysis. Tourism Management, 50, 130-141.

Taylor, D. (2018). 7 Straightforward Ways to Cut Back on Hotel Costs. Retrieved from

https://blog.capterra.com/7-straightforward-ways-to-cut-back-on-hotel-costs/

Turner, M. J. (2017). Precursors to the financial and strategic orientation of hotel property

capital budgeting. Journal of Hospitality and Tourism Management, 33, 31-42.

Turner, M. J., & Coote, L. V. (2018). Incentives and monitoring: impact on the financial and

non-financial orientation of capital budgeting. Meditari Accountancy Research, 26(1),

122-144.

Vukovic, D. (2016). BUDGETING P ROCESS IN TOURISM COMPANIES FOR THE

PURPOSE OF IMPROVING THE QUALITY OF TOURISM PRODUCTS. Retrieved

from file:///C:/Users/Manita/Downloads/181-186.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost and performance management 9

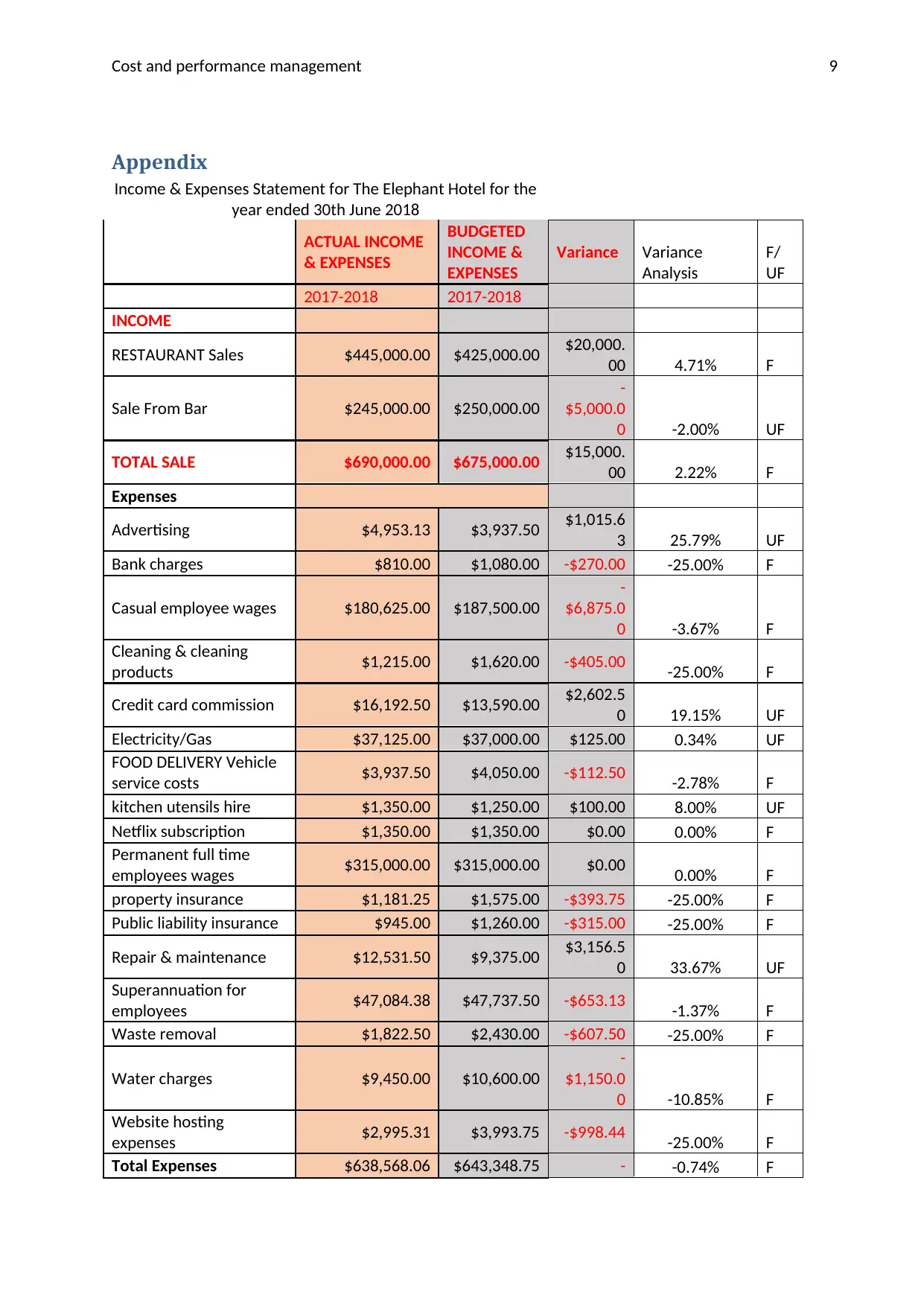

Appendix

Income & Expenses Statement for The Elephant Hotel for the

year ended 30th June 2018

ACTUAL INCOME

& EXPENSES

BUDGETED

INCOME &

EXPENSES

Variance Variance

Analysis

F/

UF

2017-2018 2017-2018

INCOME

RESTAURANT Sales $445,000.00 $425,000.00 $20,000.

00 4.71% F

Sale From Bar $245,000.00 $250,000.00

-

$5,000.0

0 -2.00% UF

TOTAL SALE $690,000.00 $675,000.00 $15,000.

00 2.22% F

Expenses

Advertising $4,953.13 $3,937.50 $1,015.6

3 25.79% UF

Bank charges $810.00 $1,080.00 -$270.00 -25.00% F

Casual employee wages $180,625.00 $187,500.00

-

$6,875.0

0 -3.67% F

Cleaning & cleaning

products $1,215.00 $1,620.00 -$405.00 -25.00% F

Credit card commission $16,192.50 $13,590.00 $2,602.5

0 19.15% UF

Electricity/Gas $37,125.00 $37,000.00 $125.00 0.34% UF

FOOD DELIVERY Vehicle

service costs $3,937.50 $4,050.00 -$112.50 -2.78% F

kitchen utensils hire $1,350.00 $1,250.00 $100.00 8.00% UF

Netflix subscription $1,350.00 $1,350.00 $0.00 0.00% F

Permanent full time

employees wages $315,000.00 $315,000.00 $0.00 0.00% F

property insurance $1,181.25 $1,575.00 -$393.75 -25.00% F

Public liability insurance $945.00 $1,260.00 -$315.00 -25.00% F

Repair & maintenance $12,531.50 $9,375.00 $3,156.5

0 33.67% UF

Superannuation for

employees $47,084.38 $47,737.50 -$653.13 -1.37% F

Waste removal $1,822.50 $2,430.00 -$607.50 -25.00% F

Water charges $9,450.00 $10,600.00

-

$1,150.0

0 -10.85% F

Website hosting

expenses $2,995.31 $3,993.75 -$998.44 -25.00% F

Total Expenses $638,568.06 $643,348.75 - -0.74% F

Appendix

Income & Expenses Statement for The Elephant Hotel for the

year ended 30th June 2018

ACTUAL INCOME

& EXPENSES

BUDGETED

INCOME &

EXPENSES

Variance Variance

Analysis

F/

UF

2017-2018 2017-2018

INCOME

RESTAURANT Sales $445,000.00 $425,000.00 $20,000.

00 4.71% F

Sale From Bar $245,000.00 $250,000.00

-

$5,000.0

0 -2.00% UF

TOTAL SALE $690,000.00 $675,000.00 $15,000.

00 2.22% F

Expenses

Advertising $4,953.13 $3,937.50 $1,015.6

3 25.79% UF

Bank charges $810.00 $1,080.00 -$270.00 -25.00% F

Casual employee wages $180,625.00 $187,500.00

-

$6,875.0

0 -3.67% F

Cleaning & cleaning

products $1,215.00 $1,620.00 -$405.00 -25.00% F

Credit card commission $16,192.50 $13,590.00 $2,602.5

0 19.15% UF

Electricity/Gas $37,125.00 $37,000.00 $125.00 0.34% UF

FOOD DELIVERY Vehicle

service costs $3,937.50 $4,050.00 -$112.50 -2.78% F

kitchen utensils hire $1,350.00 $1,250.00 $100.00 8.00% UF

Netflix subscription $1,350.00 $1,350.00 $0.00 0.00% F

Permanent full time

employees wages $315,000.00 $315,000.00 $0.00 0.00% F

property insurance $1,181.25 $1,575.00 -$393.75 -25.00% F

Public liability insurance $945.00 $1,260.00 -$315.00 -25.00% F

Repair & maintenance $12,531.50 $9,375.00 $3,156.5

0 33.67% UF

Superannuation for

employees $47,084.38 $47,737.50 -$653.13 -1.37% F

Waste removal $1,822.50 $2,430.00 -$607.50 -25.00% F

Water charges $9,450.00 $10,600.00

-

$1,150.0

0 -10.85% F

Website hosting

expenses $2,995.31 $3,993.75 -$998.44 -25.00% F

Total Expenses $638,568.06 $643,348.75 - -0.74% F

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost and performance management 10

$4,780.6

9

Month Net Profit /

(Loss) $51,431.94 $31,651.25 $19,780.

69 62.50% UF

$4,780.6

9

Month Net Profit /

(Loss) $51,431.94 $31,651.25 $19,780.

69 62.50% UF

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.