WACC, DCF Valuation for Hotel Shilla Co Limited: Financial Analysis

VerifiedAdded on 2021/06/17

|10

|1362

|128

Project

AI Summary

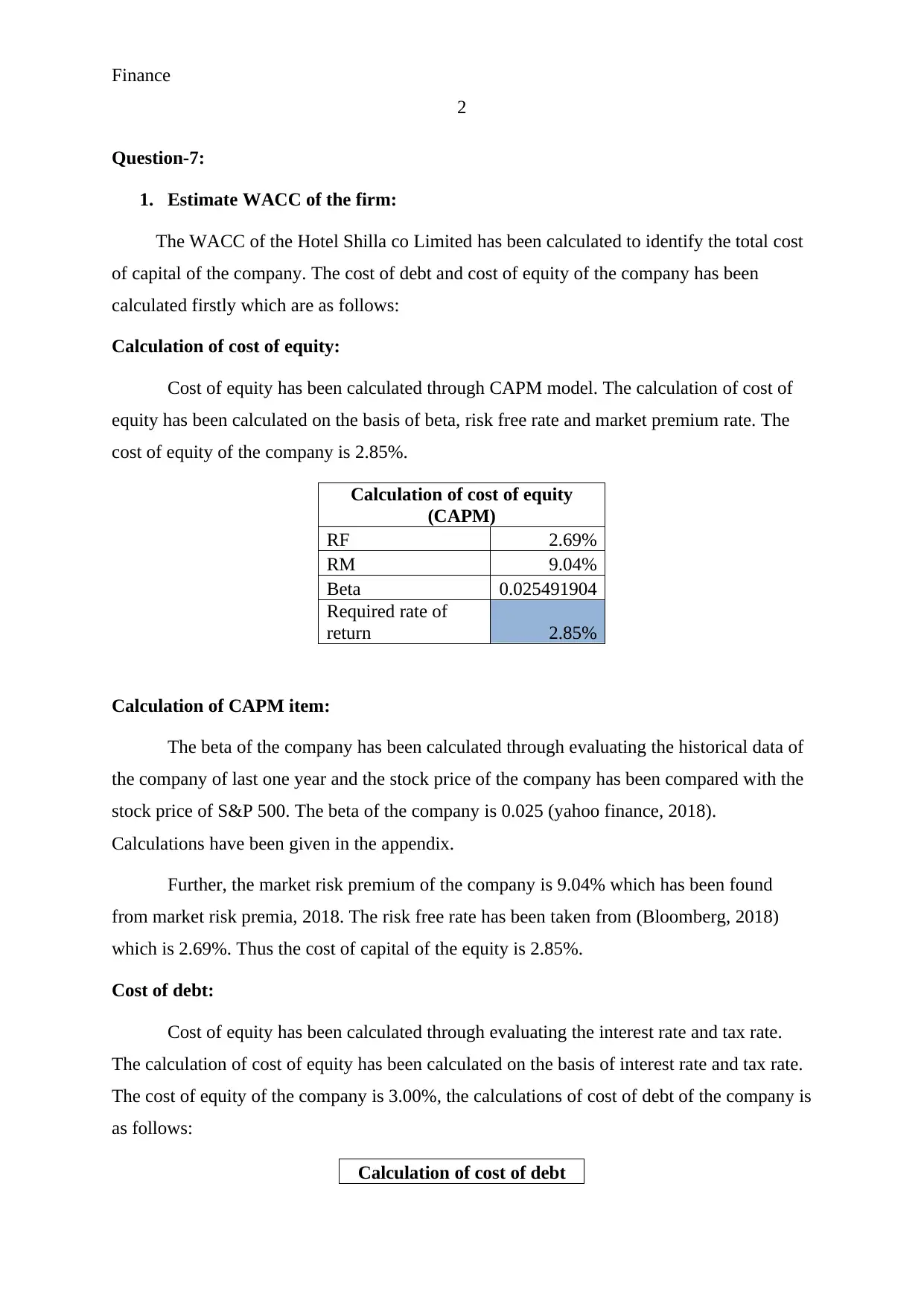

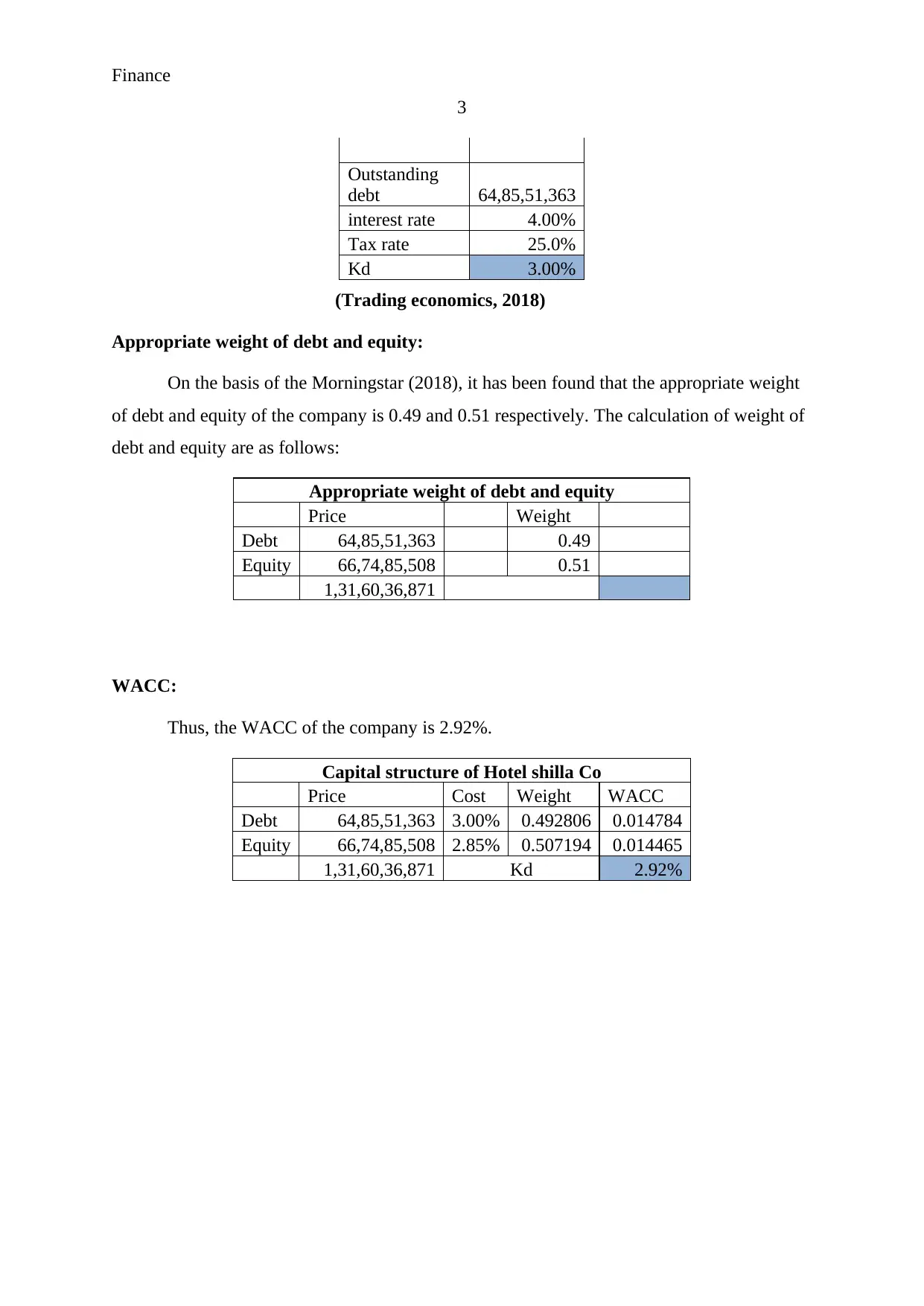

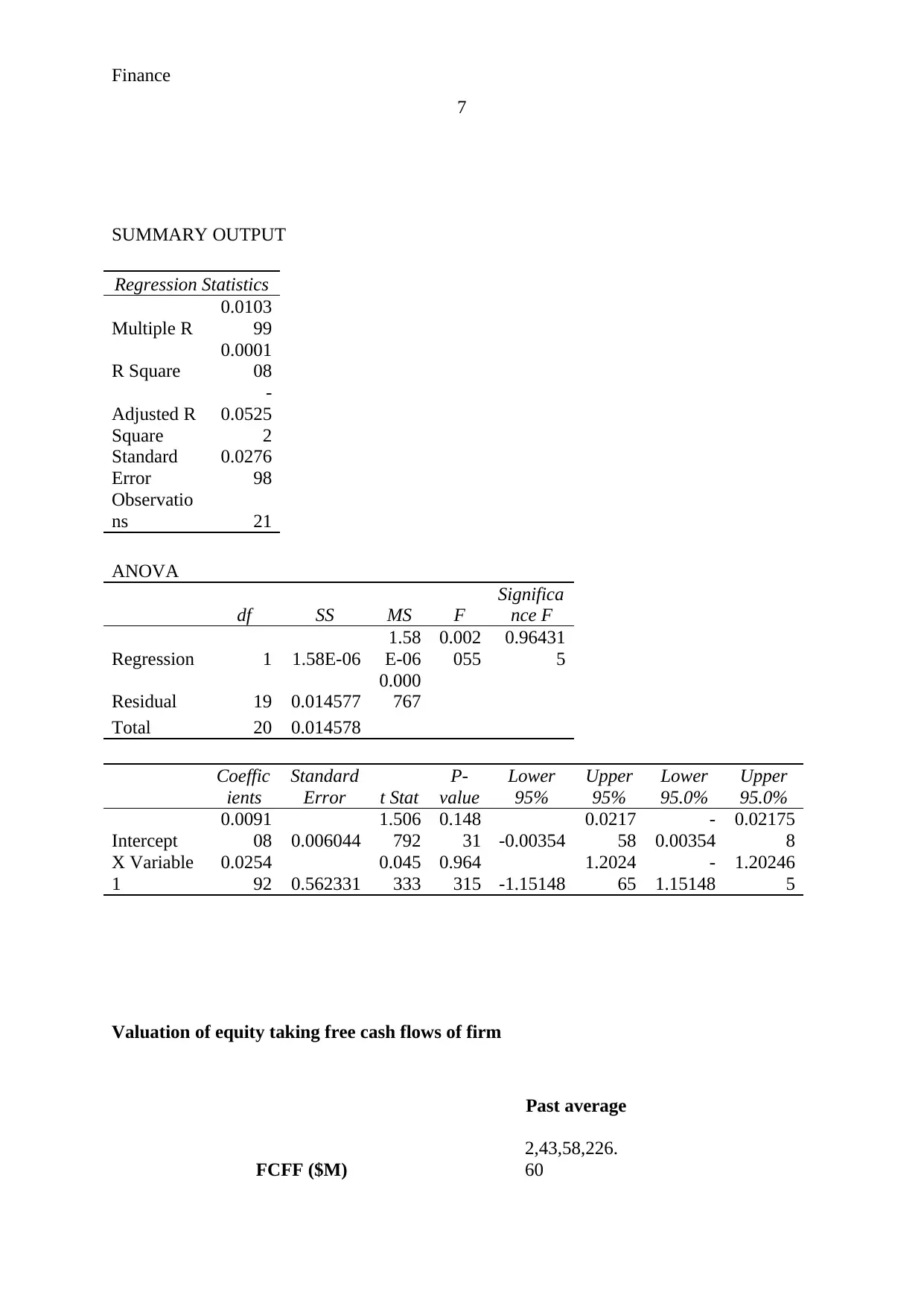

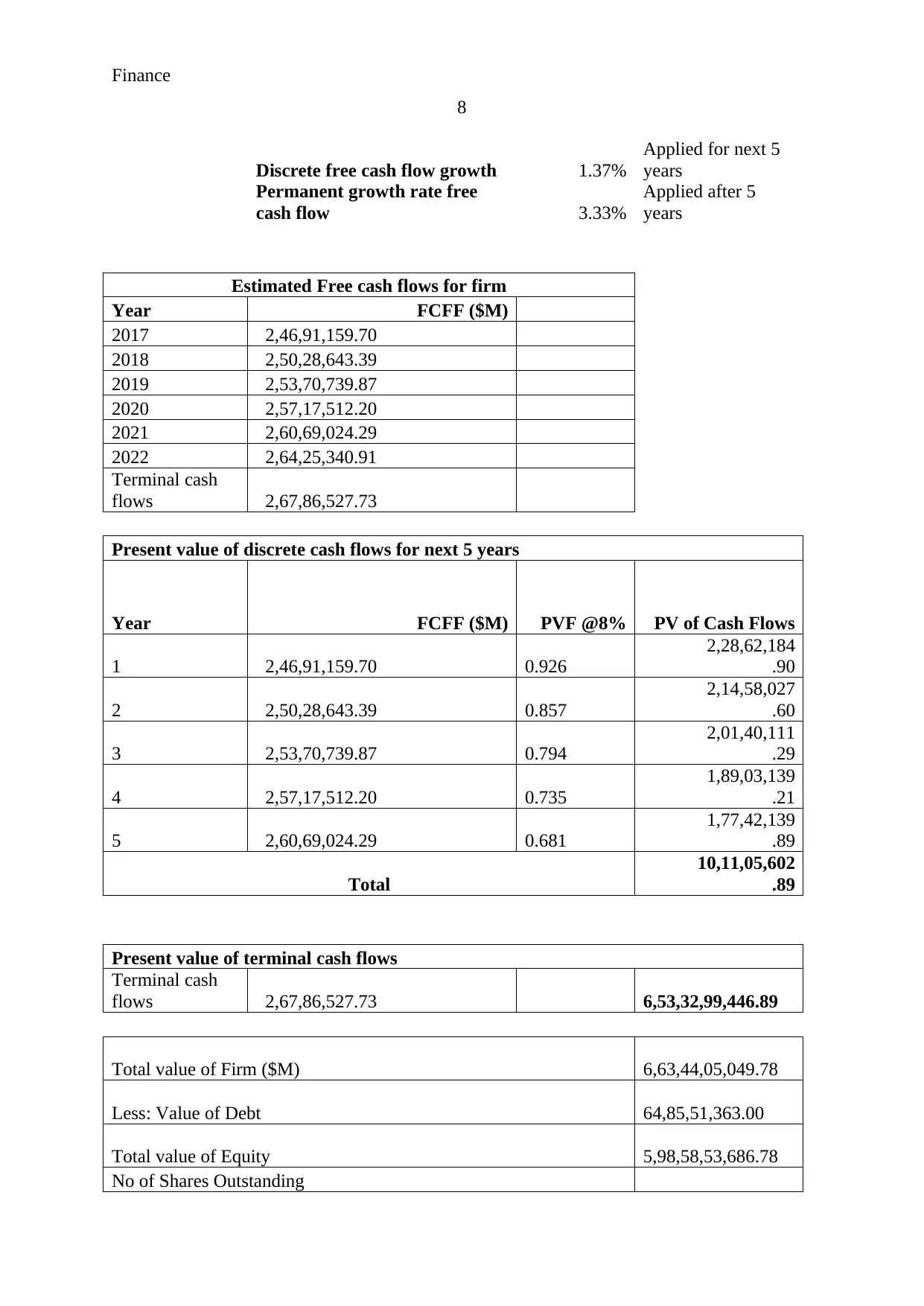

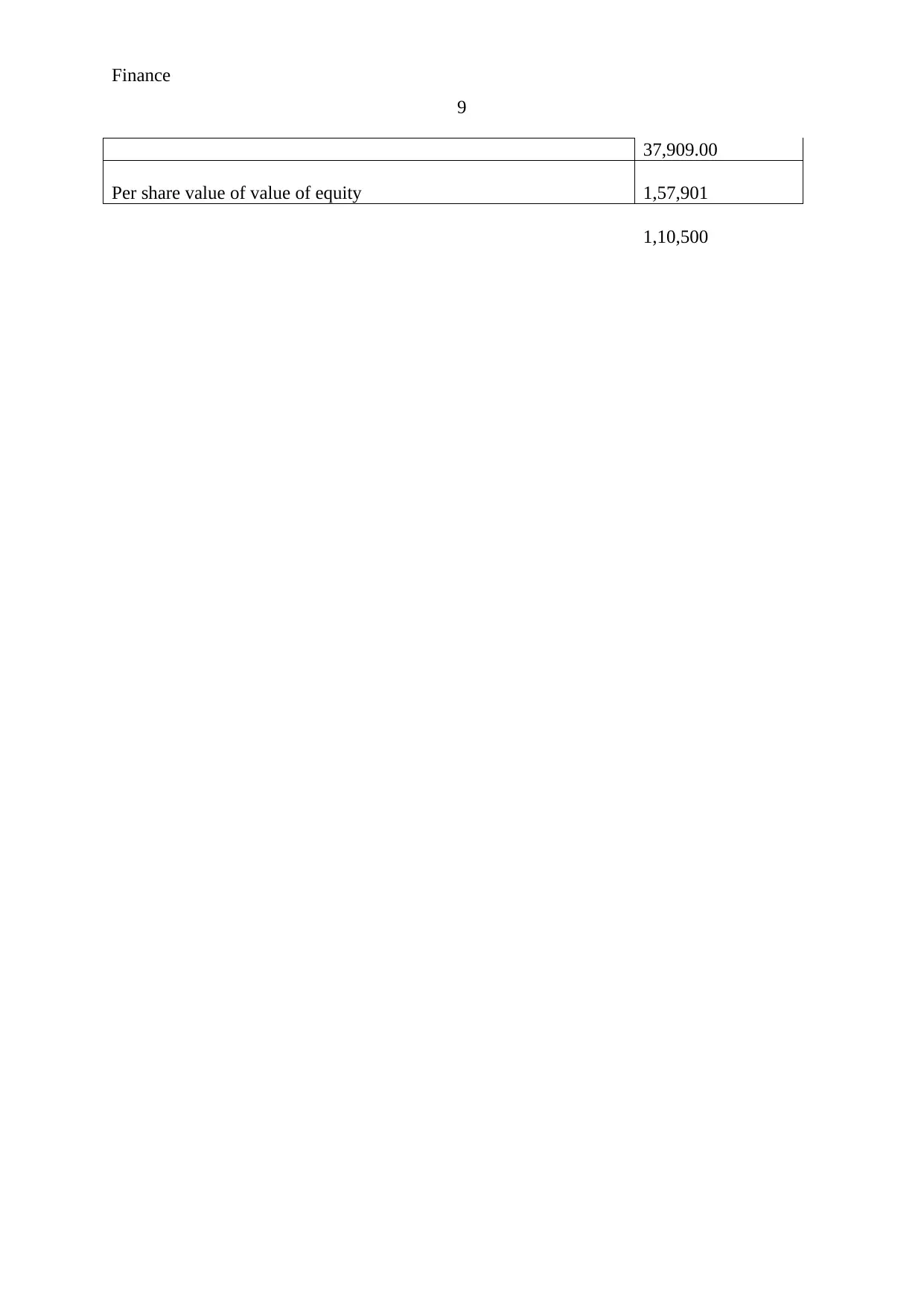

This project undertakes a financial analysis of Hotel Shilla Co Limited, focusing on the calculation of its Weighted Average Cost of Capital (WACC) and the application of Discounted Cash Flow (DCF) analysis to determine the firm's equity value. The WACC calculation incorporates the cost of equity, derived using the Capital Asset Pricing Model (CAPM) considering beta, risk-free rate, and market risk premium, and the cost of debt, based on the interest rate and tax rate. The appropriate weights of debt and equity are determined using Morningstar data. The DCF analysis estimates the company's equity value, projecting free cash flows for the firm and calculating the present value of these cash flows, including a terminal value. The project concludes with a valuation of the company's stock price, comparing it to the market price to assess whether the stock is undervalued or overvalued. The analysis uses financial data from various sources, including Yahoo Finance, Bloomberg, and Trading Economics, to support the calculations and conclusions.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.