Planning and Forecasting House Prices: UK Economics & Finance H5

VerifiedAdded on 2023/06/10

|24

|3871

|185

Report

AI Summary

This report analyzes the planning and forecasting of house prices in the UK, focusing on the impact of government subsidies, credit scores, and mortgage rates. It examines the economics of house prices, considering housing as both a consumer good and an investment. The study uses OLS regression and log-linear regression models to estimate the relationship between house prices and factors like gross household income, mortgage rates, and government schemes. The results indicate a significant positive correlation between house prices and gross household income, while the impact of mortgage rates varies depending on the presence of government schemes. The report discusses the limitations of the OLS model, including autocorrelation and multicollinearity, and addresses these issues through log-linear transformation. The log-linear model reveals that a 1% change in average gross income leads to a 1.08% increase in house prices, while a 1% increase in mortgage rates results in a 0.65% decrease.

1

MODULE TITLE: Planning and Forecasting (CRN 14302)

TITLE OF ASSESSMENT: Planning and Forecasting of House Prices

LEVEL: H5

COURSE:

MODULE TITLE: Planning and Forecasting (CRN 14302)

TITLE OF ASSESSMENT: Planning and Forecasting of House Prices

LEVEL: H5

COURSE:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

Introduction.................................................................................................................................................2

Economics of house prices..........................................................................................................................4

Estimation Procedure...................................................................................................................................6

Results of the econometric analysis.............................................................................................................7

Discussion.................................................................................................................................................12

Conclusion.................................................................................................................................................12

Appendix A: OLS Regression...................................................................................................................13

Appendix B: Log linear OLS regression....................................................................................................18

Table of Contents

Introduction.................................................................................................................................................2

Economics of house prices..........................................................................................................................4

Estimation Procedure...................................................................................................................................6

Results of the econometric analysis.............................................................................................................7

Discussion.................................................................................................................................................12

Conclusion.................................................................................................................................................12

Appendix A: OLS Regression...................................................................................................................13

Appendix B: Log linear OLS regression....................................................................................................18

3

Introduction

The impact of government subsidy and credit score of an individual on real estate

prices are two major impact factors. In particular, the link between housing costs and

the credit structure of house buying people is important. The cost of homes in the

United Kingdom has expanded impressively since the mid-1990s, and the vast majority

of these costs have expanded in the cost of existing homes as opposed to in new

homes. Over the most recent 30 years, it has likewise turned out to be less demanding

for mortgage holders to acquire against the security estimation of their home. The

housing fund framework in the United Kingdom was all the while recuperating from the

credit emergency and the 2007-2008 money related emergency, due to volatility in US

markets. A few highlights of the framework have made it especially defenseless against

this emergency, including the degree to which loan specialists have depended on

currency markets and securitization to loan them and the liberality of credit conditions,

particularly after 2005. The highlights helped the framework conquer the emergency,

including the moderately low exchange rate and the predominance of variable rate and

following home loans, which implies that a considerable lot of the present borrowers

have seen their advantage installments fizzle (Dell'Ariccia, Igan & Laeven, 2008. ).

In this article, basic in the gross and disposable income of the buyers have been

highlighted, the impact of the government scheme and mortgage rates on house prices

were scrutinized. The central area shows a framework of the determinants of the

income and financing of the financial agencies. The second area talks about rights and

facts about the assistance provided by the government of the country (Elbourne, 2008).

Introduction

The impact of government subsidy and credit score of an individual on real estate

prices are two major impact factors. In particular, the link between housing costs and

the credit structure of house buying people is important. The cost of homes in the

United Kingdom has expanded impressively since the mid-1990s, and the vast majority

of these costs have expanded in the cost of existing homes as opposed to in new

homes. Over the most recent 30 years, it has likewise turned out to be less demanding

for mortgage holders to acquire against the security estimation of their home. The

housing fund framework in the United Kingdom was all the while recuperating from the

credit emergency and the 2007-2008 money related emergency, due to volatility in US

markets. A few highlights of the framework have made it especially defenseless against

this emergency, including the degree to which loan specialists have depended on

currency markets and securitization to loan them and the liberality of credit conditions,

particularly after 2005. The highlights helped the framework conquer the emergency,

including the moderately low exchange rate and the predominance of variable rate and

following home loans, which implies that a considerable lot of the present borrowers

have seen their advantage installments fizzle (Dell'Ariccia, Igan & Laeven, 2008. ).

In this article, basic in the gross and disposable income of the buyers have been

highlighted, the impact of the government scheme and mortgage rates on house prices

were scrutinized. The central area shows a framework of the determinants of the

income and financing of the financial agencies. The second area talks about rights and

facts about the assistance provided by the government of the country (Elbourne, 2008).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Economics of house prices

The housing market is generally considered as a business opportunity for the

construction of a house when in reality there are two special activities. The owners who

live in the apartment have administration services with residence. Second, by owning

the house, people are looking for speculation. The ownership of a property owned by a

company has important economic benefits to avoid paying the rent. Two cost schemes

represent these commercial sectors. Rental costs are governed by the free market

operation of the administration, while the costs of housing regulate free market activity

as housing company (Gallin, 2008). These commercial sectors are distinguished from

each other. It is quite conceivable that it is in the market for one and not for one.

Leasing allows one to live in an apartment without a house or to renovate the property,

but people do not live there (Mayer, Pence & Sherlund, 2009).

Housing is a multidimensional element, which can be considered as a durable

consumer good that offers a series of services as a refuge and as an asset for the

investments through which leased income or capital gains are obtained. Therefore, the

demand for housing can also be classified in demand and investment demand. Income

can only explain part of housing prices and there is a crisis related to housing when

income growth does not coincide with housing prices. The literature on housing has

suggested that housing prices and income should have a long-term equilibrium (Mayer,

Pence & Sherlund, 2009).

Economics of house prices

The housing market is generally considered as a business opportunity for the

construction of a house when in reality there are two special activities. The owners who

live in the apartment have administration services with residence. Second, by owning

the house, people are looking for speculation. The ownership of a property owned by a

company has important economic benefits to avoid paying the rent. Two cost schemes

represent these commercial sectors. Rental costs are governed by the free market

operation of the administration, while the costs of housing regulate free market activity

as housing company (Gallin, 2008). These commercial sectors are distinguished from

each other. It is quite conceivable that it is in the market for one and not for one.

Leasing allows one to live in an apartment without a house or to renovate the property,

but people do not live there (Mayer, Pence & Sherlund, 2009).

Housing is a multidimensional element, which can be considered as a durable

consumer good that offers a series of services as a refuge and as an asset for the

investments through which leased income or capital gains are obtained. Therefore, the

demand for housing can also be classified in demand and investment demand. Income

can only explain part of housing prices and there is a crisis related to housing when

income growth does not coincide with housing prices. The literature on housing has

suggested that housing prices and income should have a long-term equilibrium (Mayer,

Pence & Sherlund, 2009).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

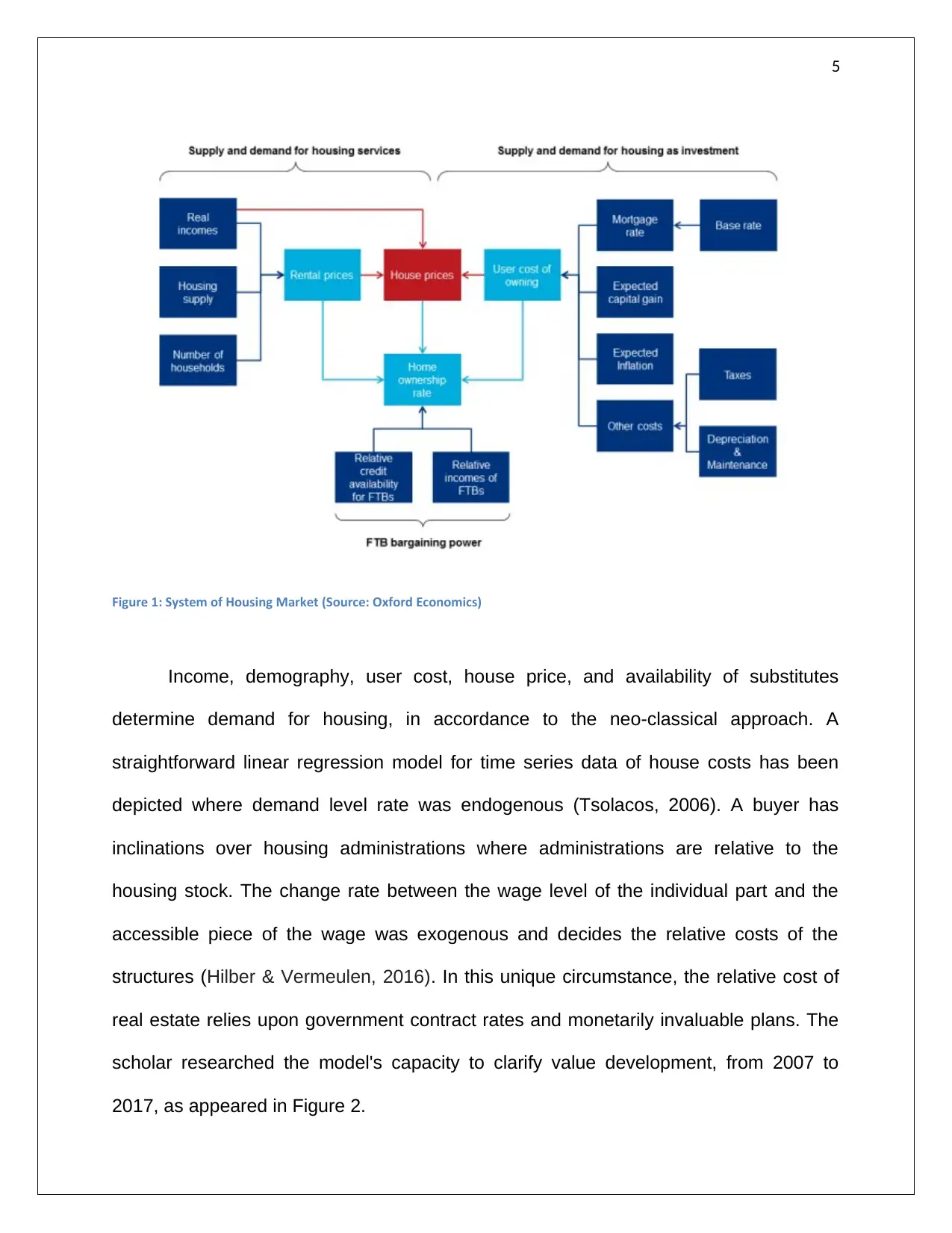

Figure 1: System of Housing Market (Source: Oxford Economics)

Income, demography, user cost, house price, and availability of substitutes

determine demand for housing, in accordance to the neo-classical approach. A

straightforward linear regression model for time series data of house costs has been

depicted where demand level rate was endogenous (Tsolacos, 2006). A buyer has

inclinations over housing administrations where administrations are relative to the

housing stock. The change rate between the wage level of the individual part and the

accessible piece of the wage was exogenous and decides the relative costs of the

structures (Hilber & Vermeulen, 2016). In this unique circumstance, the relative cost of

real estate relies upon government contract rates and monetarily invaluable plans. The

scholar researched the model's capacity to clarify value development, from 2007 to

2017, as appeared in Figure 2.

Figure 1: System of Housing Market (Source: Oxford Economics)

Income, demography, user cost, house price, and availability of substitutes

determine demand for housing, in accordance to the neo-classical approach. A

straightforward linear regression model for time series data of house costs has been

depicted where demand level rate was endogenous (Tsolacos, 2006). A buyer has

inclinations over housing administrations where administrations are relative to the

housing stock. The change rate between the wage level of the individual part and the

accessible piece of the wage was exogenous and decides the relative costs of the

structures (Hilber & Vermeulen, 2016). In this unique circumstance, the relative cost of

real estate relies upon government contract rates and monetarily invaluable plans. The

scholar researched the model's capacity to clarify value development, from 2007 to

2017, as appeared in Figure 2.

6

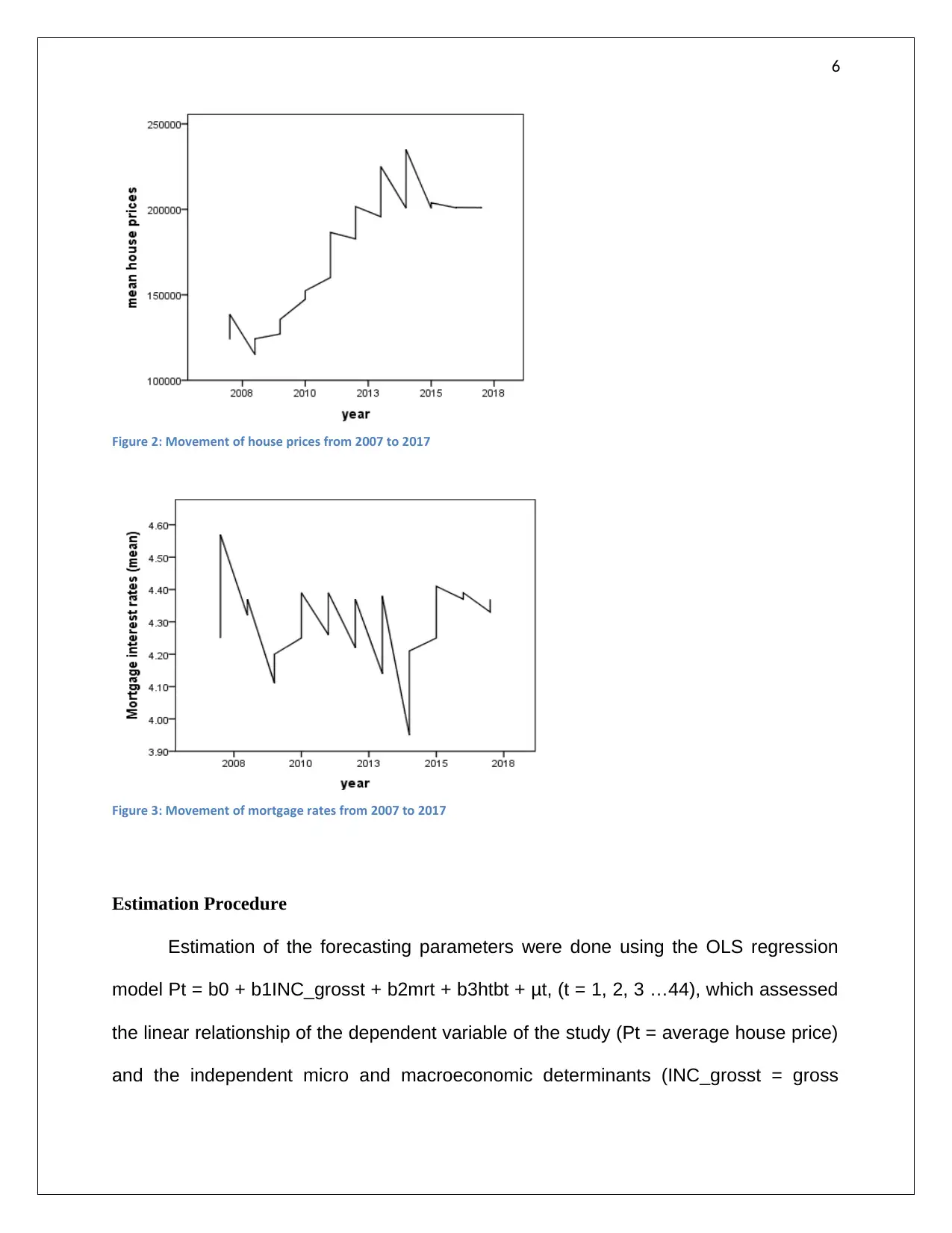

Figure 2: Movement of house prices from 2007 to 2017

Figure 3: Movement of mortgage rates from 2007 to 2017

Estimation Procedure

Estimation of the forecasting parameters were done using the OLS regression

model Pt = b0 + b1INC_grosst + b2mrt + b3htbt + μt, (t = 1, 2, 3 …44), which assessed

the linear relationship of the dependent variable of the study (Pt = average house price)

and the independent micro and macroeconomic determinants (INC_grosst = gross

Figure 2: Movement of house prices from 2007 to 2017

Figure 3: Movement of mortgage rates from 2007 to 2017

Estimation Procedure

Estimation of the forecasting parameters were done using the OLS regression

model Pt = b0 + b1INC_grosst + b2mrt + b3htbt + μt, (t = 1, 2, 3 …44), which assessed

the linear relationship of the dependent variable of the study (Pt = average house price)

and the independent micro and macroeconomic determinants (INC_grosst = gross

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

household income, mrt = mortgage rate, htbt = government scheme) of the study (Chen

and Patel, 2002). It was hypothesized that the independent factors have insignificant

impact on house prices in UK. The model was utilized to estimate the coefficients of

forecasting of the house prices. The sensibility of this econometric representation for the

three bedroom model was in line with hedonic model of economics (Selim, 2009).

The analysis was reassessed with log linear regression model lnPt = b0 +

b1lnINC_grosst + b2lnmrt + b3htbt + μt, (t = 1, 2, 3 …44), where the coefficients of the

independent factors represented the elasticity of the variance of the independent

factors(Drake, 1993). The percentage alteration of the house prices was explained from

this model (Zietz, Zietz & Sirmans, 2008).

Results of the econometric analysis

The average house prices between 2007 and 2017 was calculated as 175168.18

(SD = 35424.59), mean gross household income was 37813.64 (SD = 3842.03),

standard mortgage interest rates as 4.31% (SD = 0.10%). The correlation between the

house price and the gross household income revealed highly significant correlation (r =

0.92, p < 0.05), whereas mortgage interest rate had statistically insignificant negative

correlation (r = -0.1, p =0.27) with house prices of UK. Hence, the coefficient estimates

on INC_gross and mr was expected to be positive and negative correspondingly, in the

regression equation.

The dummy variable htb was used for sub grouping the results for status of the

government schemes. The impact of the scheme on the model was positive in nature

(Table 2). Hence, before 2011 the linear model was able to explain 58.5% variance of

household income, mrt = mortgage rate, htbt = government scheme) of the study (Chen

and Patel, 2002). It was hypothesized that the independent factors have insignificant

impact on house prices in UK. The model was utilized to estimate the coefficients of

forecasting of the house prices. The sensibility of this econometric representation for the

three bedroom model was in line with hedonic model of economics (Selim, 2009).

The analysis was reassessed with log linear regression model lnPt = b0 +

b1lnINC_grosst + b2lnmrt + b3htbt + μt, (t = 1, 2, 3 …44), where the coefficients of the

independent factors represented the elasticity of the variance of the independent

factors(Drake, 1993). The percentage alteration of the house prices was explained from

this model (Zietz, Zietz & Sirmans, 2008).

Results of the econometric analysis

The average house prices between 2007 and 2017 was calculated as 175168.18

(SD = 35424.59), mean gross household income was 37813.64 (SD = 3842.03),

standard mortgage interest rates as 4.31% (SD = 0.10%). The correlation between the

house price and the gross household income revealed highly significant correlation (r =

0.92, p < 0.05), whereas mortgage interest rate had statistically insignificant negative

correlation (r = -0.1, p =0.27) with house prices of UK. Hence, the coefficient estimates

on INC_gross and mr was expected to be positive and negative correspondingly, in the

regression equation.

The dummy variable htb was used for sub grouping the results for status of the

government schemes. The impact of the scheme on the model was positive in nature

(Table 2). Hence, before 2011 the linear model was able to explain 58.5% variance of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

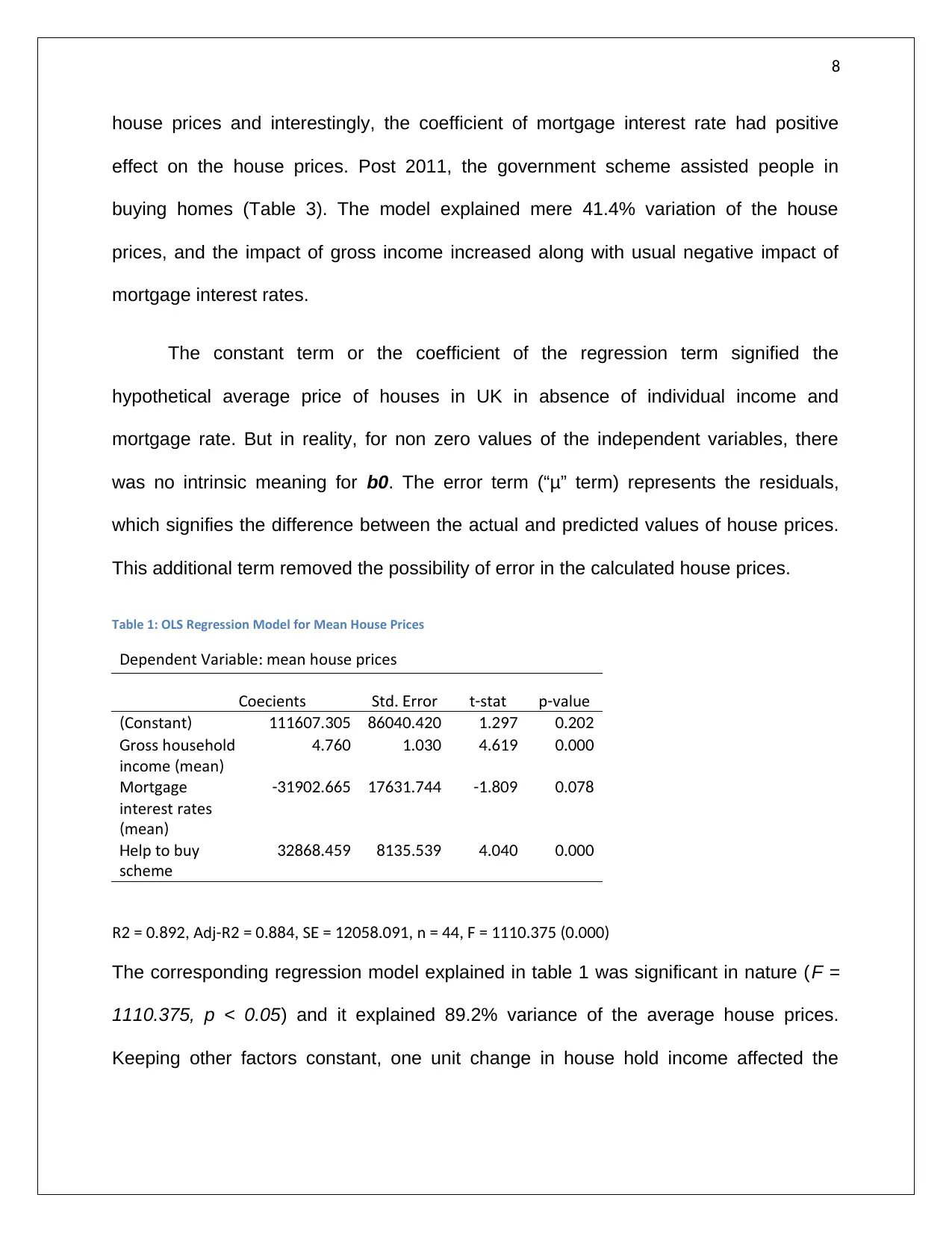

house prices and interestingly, the coefficient of mortgage interest rate had positive

effect on the house prices. Post 2011, the government scheme assisted people in

buying homes (Table 3). The model explained mere 41.4% variation of the house

prices, and the impact of gross income increased along with usual negative impact of

mortgage interest rates.

The constant term or the coefficient of the regression term signified the

hypothetical average price of houses in UK in absence of individual income and

mortgage rate. But in reality, for non zero values of the independent variables, there

was no intrinsic meaning for b0. The error term (“μ” term) represents the residuals,

which signifies the difference between the actual and predicted values of house prices.

This additional term removed the possibility of error in the calculated house prices.

Table 1: OLS Regression Model for Mean House Prices

Dependent Variable mean house prices:

Coefficients Std rror. E t stat- p value-

Constant( ) 111607.305 86040.420 1.297 0.202

ross householdG

income mean( )

4.760 1.030 4.619 0.000

Mortgage

interest rates

mean( )

-31902.665 17631.744 -1.809 0.078

elp to buyH

scheme

32868.459 8135.539 4.040 0.000

R Adj R S n2 = 0.892, - 2 = 0.884, E = 12058.091, = 44, F = 1110.375 (0.000)

The corresponding regression model explained in table 1 was significant in nature (F =

1110.375, p < 0.05) and it explained 89.2% variance of the average house prices.

Keeping other factors constant, one unit change in house hold income affected the

house prices and interestingly, the coefficient of mortgage interest rate had positive

effect on the house prices. Post 2011, the government scheme assisted people in

buying homes (Table 3). The model explained mere 41.4% variation of the house

prices, and the impact of gross income increased along with usual negative impact of

mortgage interest rates.

The constant term or the coefficient of the regression term signified the

hypothetical average price of houses in UK in absence of individual income and

mortgage rate. But in reality, for non zero values of the independent variables, there

was no intrinsic meaning for b0. The error term (“μ” term) represents the residuals,

which signifies the difference between the actual and predicted values of house prices.

This additional term removed the possibility of error in the calculated house prices.

Table 1: OLS Regression Model for Mean House Prices

Dependent Variable mean house prices:

Coefficients Std rror. E t stat- p value-

Constant( ) 111607.305 86040.420 1.297 0.202

ross householdG

income mean( )

4.760 1.030 4.619 0.000

Mortgage

interest rates

mean( )

-31902.665 17631.744 -1.809 0.078

elp to buyH

scheme

32868.459 8135.539 4.040 0.000

R Adj R S n2 = 0.892, - 2 = 0.884, E = 12058.091, = 44, F = 1110.375 (0.000)

The corresponding regression model explained in table 1 was significant in nature (F =

1110.375, p < 0.05) and it explained 89.2% variance of the average house prices.

Keeping other factors constant, one unit change in house hold income affected the

9

house price by 4.76 times. For one percent change in mortgage rate the average house

price was appeared to be negatively affected.

Table 2: Regression Model for Mean House Prices (Scheme Not Present)

Dependent Variable mean house prices Scheme not present: ( )

Coefficients Std rror. E t stat- p value-

Constant( ) -63433.13 102941.35 -0.616 0.548

ross householdG

income mean( )

4.74 1.128 4.205 0.001

Mortgage

interest rates

mean( )

8896.948 19844.54 0.448 0.661

R Adj R S n2 = 0.585, - 2 = 0.522, E = 8096.26, = 44, F = 9.177 (0.000)

Table 3: Regression Model for Mean House Prices (Scheme Active)

Dependent Variable mean house prices Scheme Active: ( )

Coefficients Std rror. E t stat- p value-

Constant( ) 234890.259 119881.601 1.959 0.061

rossG

household

income mean( )

5.314 1.477 3.598 0.001

Mortgage

interest rates

mean( )

-58086.490 24817.290 -2.341 0.028

R Adj R S n2 = 0.414, - 2 = 0.367, E = 13330.997, = 44, F = 8.829 (0.001)

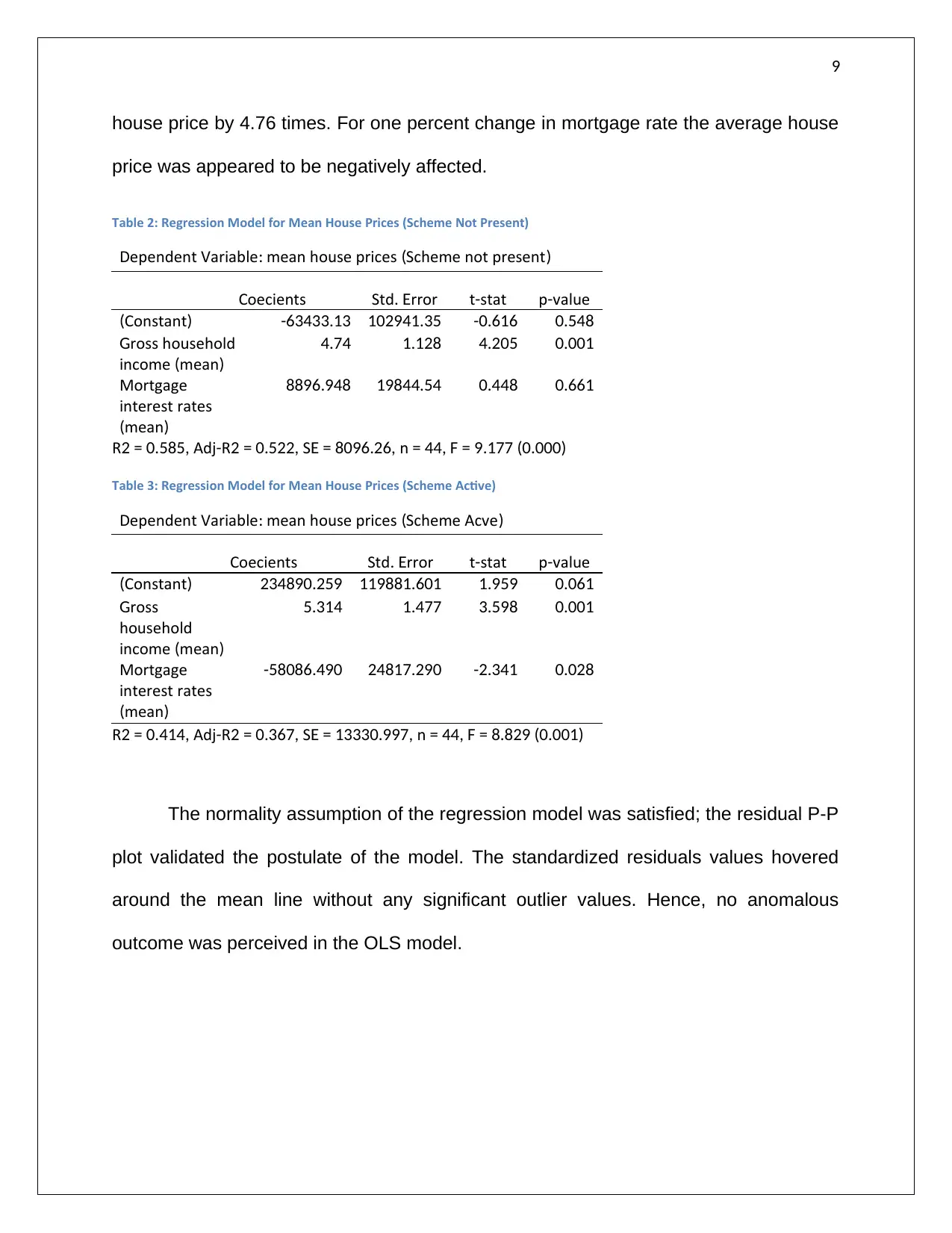

The normality assumption of the regression model was satisfied; the residual P-P

plot validated the postulate of the model. The standardized residuals values hovered

around the mean line without any significant outlier values. Hence, no anomalous

outcome was perceived in the OLS model.

house price by 4.76 times. For one percent change in mortgage rate the average house

price was appeared to be negatively affected.

Table 2: Regression Model for Mean House Prices (Scheme Not Present)

Dependent Variable mean house prices Scheme not present: ( )

Coefficients Std rror. E t stat- p value-

Constant( ) -63433.13 102941.35 -0.616 0.548

ross householdG

income mean( )

4.74 1.128 4.205 0.001

Mortgage

interest rates

mean( )

8896.948 19844.54 0.448 0.661

R Adj R S n2 = 0.585, - 2 = 0.522, E = 8096.26, = 44, F = 9.177 (0.000)

Table 3: Regression Model for Mean House Prices (Scheme Active)

Dependent Variable mean house prices Scheme Active: ( )

Coefficients Std rror. E t stat- p value-

Constant( ) 234890.259 119881.601 1.959 0.061

rossG

household

income mean( )

5.314 1.477 3.598 0.001

Mortgage

interest rates

mean( )

-58086.490 24817.290 -2.341 0.028

R Adj R S n2 = 0.414, - 2 = 0.367, E = 13330.997, = 44, F = 8.829 (0.001)

The normality assumption of the regression model was satisfied; the residual P-P

plot validated the postulate of the model. The standardized residuals values hovered

around the mean line without any significant outlier values. Hence, no anomalous

outcome was perceived in the OLS model.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Figure 4: Normality of residuals of OLS Regression model

The Durbin-Watson value was 0.84 (p < 0.05), which suggested that the time

series data had positive autocorrelation. As the value of the statistics was less than 1, it

was a matter of concern for the OLS regression model (Field, 2009). The probable

solution was to assess the dependent variable as Pt −ρPt−1 in the regression equation,

where ρwas the measure of autocorrelation (Hill et al., 2008).

The OLS model also has multicollinearity problem, as the VIF value for the

average gross household income (VIF = 4.64) with tolerance of 0.216. The value of VIF

was greater than 3, and hence the high correlation between gross household income

and government scheme was considered as the primary reason for multicollinearity.

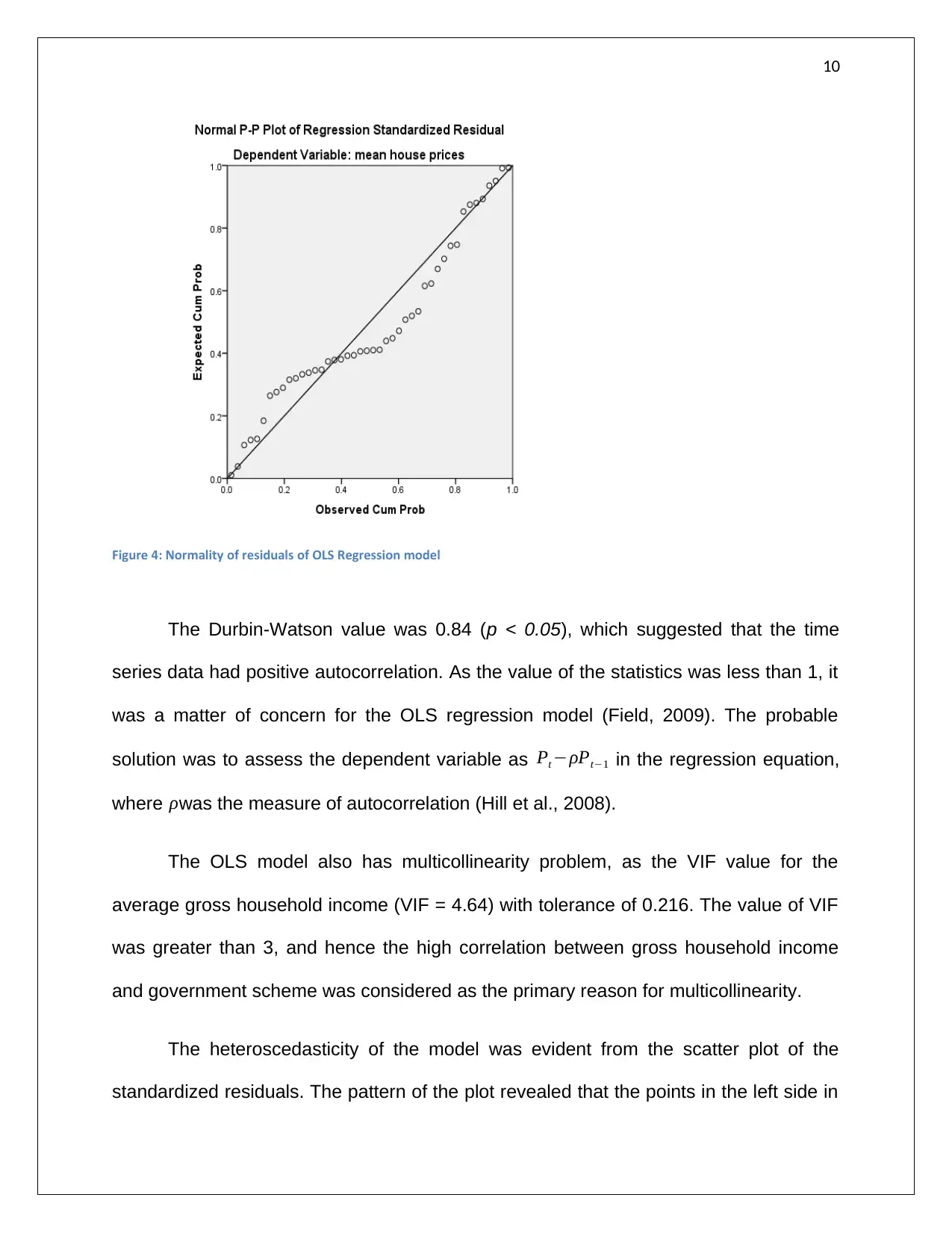

The heteroscedasticity of the model was evident from the scatter plot of the

standardized residuals. The pattern of the plot revealed that the points in the left side in

Figure 4: Normality of residuals of OLS Regression model

The Durbin-Watson value was 0.84 (p < 0.05), which suggested that the time

series data had positive autocorrelation. As the value of the statistics was less than 1, it

was a matter of concern for the OLS regression model (Field, 2009). The probable

solution was to assess the dependent variable as Pt −ρPt−1 in the regression equation,

where ρwas the measure of autocorrelation (Hill et al., 2008).

The OLS model also has multicollinearity problem, as the VIF value for the

average gross household income (VIF = 4.64) with tolerance of 0.216. The value of VIF

was greater than 3, and hence the high correlation between gross household income

and government scheme was considered as the primary reason for multicollinearity.

The heteroscedasticity of the model was evident from the scatter plot of the

standardized residuals. The pattern of the plot revealed that the points in the left side in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

the graph were closely plotted, whereas the points plotted in the right were spaced

vertically. Hence, the plot indicated heteroscedasticity, which was a violation of the

assumption of the model and the output of the house prices was not predicted properly.

Figure 5: Scatter plot of Residuals

The OLS regression model was transformed using natural logarithms as, lnPt =

b0 + b1lnINC_grosst + b2lnmrt + b3htbt + μt. this transformation was done to assess

the percentage change effect of the house prices. The probable non linear relation

between the factors or parameters was removed by this method, and required linearity

in factors was established.

Table 4: Regression Model for Log linear Mean House Prices

Dependent Variable ln: P

Coefficients

Std.

rrorE t stat- p value-

Constant( ) 1.529 2.332 0.656 0.516

ln C grossIN _ 1.077 0.210 5.130 0.000

lnmr -0.650 0.415 -1.567 0.125

elp to buyH

scheme

0.198 0.045 4.375 0.000

R Adj R S n2 = 0.910, - 2 = 0.903, E = 0.066, = 44, F = 134.461 (0.000)

The corresponding regression model explained in table 4 was significant in

nature (F = 134.461, p < 0.05) and it explained 91.0% variance of the average house

the graph were closely plotted, whereas the points plotted in the right were spaced

vertically. Hence, the plot indicated heteroscedasticity, which was a violation of the

assumption of the model and the output of the house prices was not predicted properly.

Figure 5: Scatter plot of Residuals

The OLS regression model was transformed using natural logarithms as, lnPt =

b0 + b1lnINC_grosst + b2lnmrt + b3htbt + μt. this transformation was done to assess

the percentage change effect of the house prices. The probable non linear relation

between the factors or parameters was removed by this method, and required linearity

in factors was established.

Table 4: Regression Model for Log linear Mean House Prices

Dependent Variable ln: P

Coefficients

Std.

rrorE t stat- p value-

Constant( ) 1.529 2.332 0.656 0.516

ln C grossIN _ 1.077 0.210 5.130 0.000

lnmr -0.650 0.415 -1.567 0.125

elp to buyH

scheme

0.198 0.045 4.375 0.000

R Adj R S n2 = 0.910, - 2 = 0.903, E = 0.066, = 44, F = 134.461 (0.000)

The corresponding regression model explained in table 4 was significant in

nature (F = 134.461, p < 0.05) and it explained 91.0% variance of the average house

12

prices. The adjusted R-square was 0.90 and was almost equal to the coefficient of

determination.

The coefficients of the log-log regression represent elasticity of variables of the

model. This indicated that, for 1% change in average gross income, the price of the

house will increase by 1.08% (Keeping other factors constant). Similarly, for 1%

increase in mortgage rate, the average house price will come down by 0.65%.

The bivariate correlation between “natural log of disposable household income”

and the “natural log of gross household income” was insignificant in nature ( r = -0.03, p

= 0.416). The uncorrelated nature implied that the variables were not linearly related,

and hence independent in nature. Due to the uncorrelated nature, there was no share of

variance with each other and hence combined effect on house prices was not possible.

Therefore, regression model with any one of the variables was as good as the

combined model.

Discussion

The initial hypothesis of uncorrelated house price and independent factors was

rejected based on the evidences from the regression model. The linear model was less

than a viable predictor because of multicollinearity and observed heteroscedasticity.

Auto correlation in the OLS model was on the predicted line, as the model was built on

a time series data. Non linear relation between the predictors was removed by the log-

log regression model.

prices. The adjusted R-square was 0.90 and was almost equal to the coefficient of

determination.

The coefficients of the log-log regression represent elasticity of variables of the

model. This indicated that, for 1% change in average gross income, the price of the

house will increase by 1.08% (Keeping other factors constant). Similarly, for 1%

increase in mortgage rate, the average house price will come down by 0.65%.

The bivariate correlation between “natural log of disposable household income”

and the “natural log of gross household income” was insignificant in nature ( r = -0.03, p

= 0.416). The uncorrelated nature implied that the variables were not linearly related,

and hence independent in nature. Due to the uncorrelated nature, there was no share of

variance with each other and hence combined effect on house prices was not possible.

Therefore, regression model with any one of the variables was as good as the

combined model.

Discussion

The initial hypothesis of uncorrelated house price and independent factors was

rejected based on the evidences from the regression model. The linear model was less

than a viable predictor because of multicollinearity and observed heteroscedasticity.

Auto correlation in the OLS model was on the predicted line, as the model was built on

a time series data. Non linear relation between the predictors was removed by the log-

log regression model.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.