TAX 2020: Housing Choices Australia Social Housing Feasibility Study

VerifiedAdded on 2022/10/17

|22

|2553

|301

Report

AI Summary

This report provides a detailed feasibility study for a social housing project in Central Melbourne undertaken by Housing Choices Australia. The study examines the financial viability of the project, considering various factors such as construction costs, government subsidies, and affordable rent levels. It includes a comprehensive financial analysis, sensitivity analysis to assess the impact of rent fluctuations, and a life cycle costing analysis over a 25-year period. The report also explores the allocation of housing units to different demographics, including people with disabilities, mental health conditions, and families. The analysis reveals that while the project may incur financial losses when charging affordable rents, it aligns with the organization's mission to provide housing to those in need. Group journals and recommendations are also included.

Running head: TAX

Cost Engineering

Name of the Student:

Name of the University:

Authors Note:

Cost Engineering

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAX

Executive summary:

A detailed feasibility study on the project of developing social housing in Central Melbourne has

been conducted in this document to assess the expected outcome of the project in the future.

Housing Choices Australia is in the process of undertaking a project to develop social housing in

the region. Feasibility study shall help the organization to assess the impact of the project on

various stakeholders to help the organization to decide whether to proceed with the project or

not. The objective of conducting a feasibility study is to estimate the expected outcomes from a

project. Considering the noble objective of the project of building and developing social housing

in Central Melbourne with special emphasis to allocate the houses to people with disabilities the

feasibility study shall give importance to different aspects of the project and not only focus on

profitability of the project.

TAX

Executive summary:

A detailed feasibility study on the project of developing social housing in Central Melbourne has

been conducted in this document to assess the expected outcome of the project in the future.

Housing Choices Australia is in the process of undertaking a project to develop social housing in

the region. Feasibility study shall help the organization to assess the impact of the project on

various stakeholders to help the organization to decide whether to proceed with the project or

not. The objective of conducting a feasibility study is to estimate the expected outcomes from a

project. Considering the noble objective of the project of building and developing social housing

in Central Melbourne with special emphasis to allocate the houses to people with disabilities the

feasibility study shall give importance to different aspects of the project and not only focus on

profitability of the project.

2

TAX

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Assumptions:...................................................................................................................................3

Discussions:.....................................................................................................................................4

Financial analysis:...........................................................................................................................5

Sensitivity analysis:.......................................................................................................................11

Life cycle costing analysis:............................................................................................................16

Group journals by each team member for meetings:.....................................................................18

Recommendations:........................................................................................................................19

References:....................................................................................................................................20

TAX

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Assumptions:...................................................................................................................................3

Discussions:.....................................................................................................................................4

Financial analysis:...........................................................................................................................5

Sensitivity analysis:.......................................................................................................................11

Life cycle costing analysis:............................................................................................................16

Group journals by each team member for meetings:.....................................................................18

Recommendations:........................................................................................................................19

References:....................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAX

Introduction:

Housing Choices Australia (Housing Choices) has experience of 20 years in developing and

building social housing and in providing homes to people with disabilities. At present the

company owns 1300 properties. The company also manages 2400 tenancies in all across

Victoria, Tasmania and the Northern Territory. The organization has experienced that there is

need for flexible housing models for the benefits of the residents (Davidson Frame, 2018). Thus,

with special emphasis to provide at least 25% of all stock to the people with varying degree of

disabilities, the company is currently considering building a social housing in Central Melbourne

in near future. Taking into consideration the facts and assumptions provided about the housing

society to be developed in Central Melbourne a feasibility report is provided below.

Assumptions:

Cost of housing project:

As per the estimates it is expected that the housing project in Central Melbourne would

approximately cost around $7.4 million. 25% of the total project cost must be incurred by the

Housing Choices (Bryde, 2018).

Borrowings for the project:

It has been assumed that Housing Choices will borrow the funds required for completion of the

project, i.e. 25% of total project cost from private debt and is expected to repay the debt over the

next 25 years.

Affordable rents:

TAX

Introduction:

Housing Choices Australia (Housing Choices) has experience of 20 years in developing and

building social housing and in providing homes to people with disabilities. At present the

company owns 1300 properties. The company also manages 2400 tenancies in all across

Victoria, Tasmania and the Northern Territory. The organization has experienced that there is

need for flexible housing models for the benefits of the residents (Davidson Frame, 2018). Thus,

with special emphasis to provide at least 25% of all stock to the people with varying degree of

disabilities, the company is currently considering building a social housing in Central Melbourne

in near future. Taking into consideration the facts and assumptions provided about the housing

society to be developed in Central Melbourne a feasibility report is provided below.

Assumptions:

Cost of housing project:

As per the estimates it is expected that the housing project in Central Melbourne would

approximately cost around $7.4 million. 25% of the total project cost must be incurred by the

Housing Choices (Bryde, 2018).

Borrowings for the project:

It has been assumed that Housing Choices will borrow the funds required for completion of the

project, i.e. 25% of total project cost from private debt and is expected to repay the debt over the

next 25 years.

Affordable rents:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAX

As per the existing market conditions the affordable rents are set at 25% of aggregate income of

individuals in the region.

Housing choices:

As per the information over 50% of the 2,400 tenants are people requiring help and support to

live independently. Thus, the housing choices in the future society in Central Melbourne shall

also follow the trend by giving preferential treatments to the residents requiring support to live

independently (E Rawlings, 2018).

Number of bedrooms:

It is assumed that there is significant demand for houses with three bedrooms. Though there is

expected to be high demand for one and two bedroom houses but there will be houses with three

bedrooms to in the new housing society.

Support requirements:

Assistance and support are mainly required by the single people and families to live

independently.

Safe and suitable housing:

The housing project must keep in mind the requirements of safe and suitable housing for people

with disabilities. Thus, the housing project will have homes with the features required for the

people with disabilities to live independently (Lee & Om, 2017).

Discussions:

Federal Government has awarded Housing Choices $5.57 million as the project in Central

Melbourne is for a social cause to support the people with disabilities by providing them with

TAX

As per the existing market conditions the affordable rents are set at 25% of aggregate income of

individuals in the region.

Housing choices:

As per the information over 50% of the 2,400 tenants are people requiring help and support to

live independently. Thus, the housing choices in the future society in Central Melbourne shall

also follow the trend by giving preferential treatments to the residents requiring support to live

independently (E Rawlings, 2018).

Number of bedrooms:

It is assumed that there is significant demand for houses with three bedrooms. Though there is

expected to be high demand for one and two bedroom houses but there will be houses with three

bedrooms to in the new housing society.

Support requirements:

Assistance and support are mainly required by the single people and families to live

independently.

Safe and suitable housing:

The housing project must keep in mind the requirements of safe and suitable housing for people

with disabilities. Thus, the housing project will have homes with the features required for the

people with disabilities to live independently (Lee & Om, 2017).

Discussions:

Federal Government has awarded Housing Choices $5.57 million as the project in Central

Melbourne is for a social cause to support the people with disabilities by providing them with

5

TAX

affordable housing with special features. The subsidy given by the Federal Government was to

support the organization to successfully deliver the social housing project in Arden-McCauley

area in Melbourne. The company has also received $360,000 from philanthropic contributions

from a charitable organization (Mikkelsen, 2015).

It is expected that 30 social housing units shall be built in the housing project to provide for the

benefits of people with disabilities and others. People with mental health conditions and without

homes shall be allocated 5 out of the 30 residential units. 5 modified units shall be allocated to

tenants with other disabilities. Elderly people without homes shall be allocated 10 units in the

new housing project and the remaining 10 units shall be kept for families.

The housing project must comply with disability codes AS 1428.1 and 1428.2 is must for the

new project to be developed in Central Melbourne (Ruben, 2018).

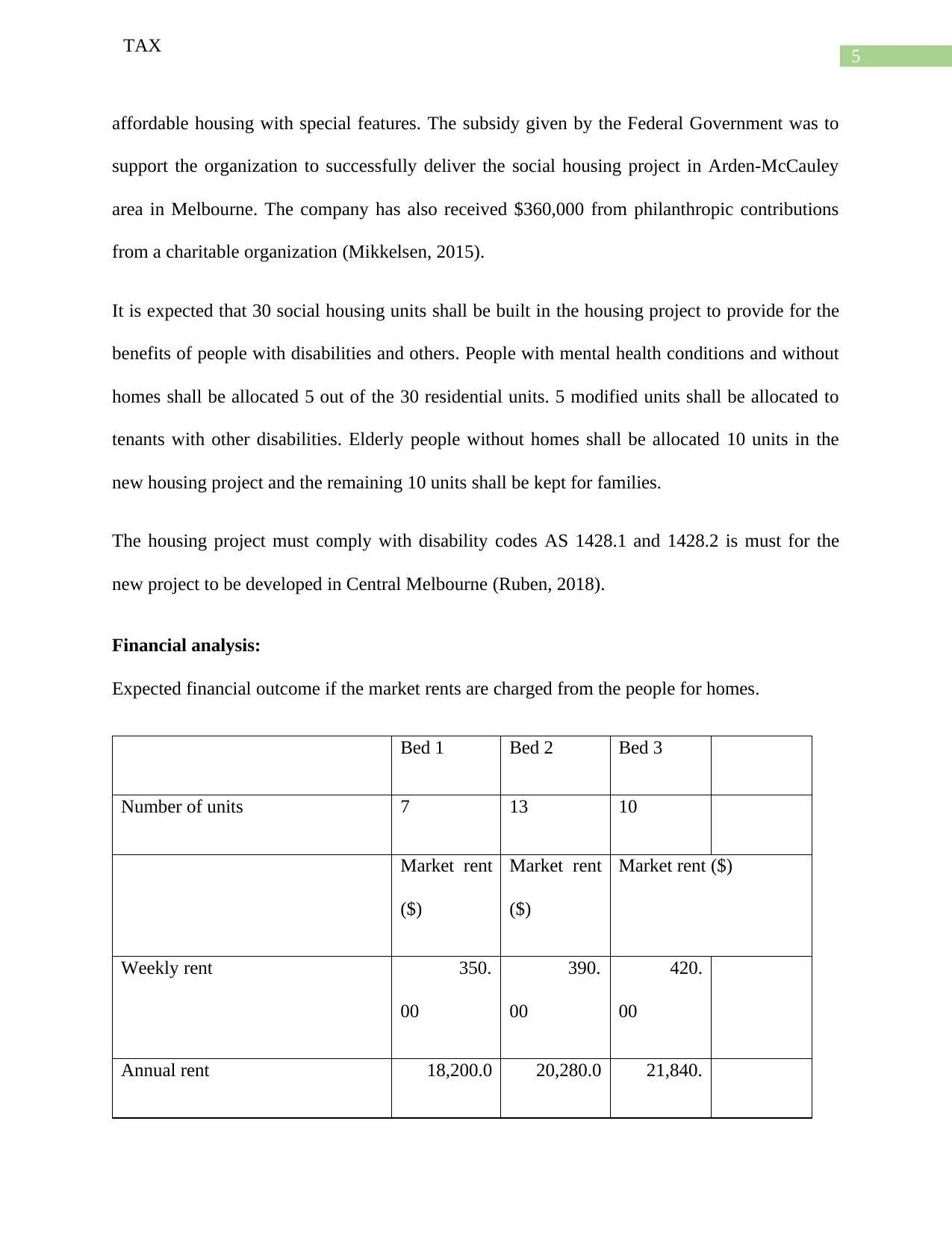

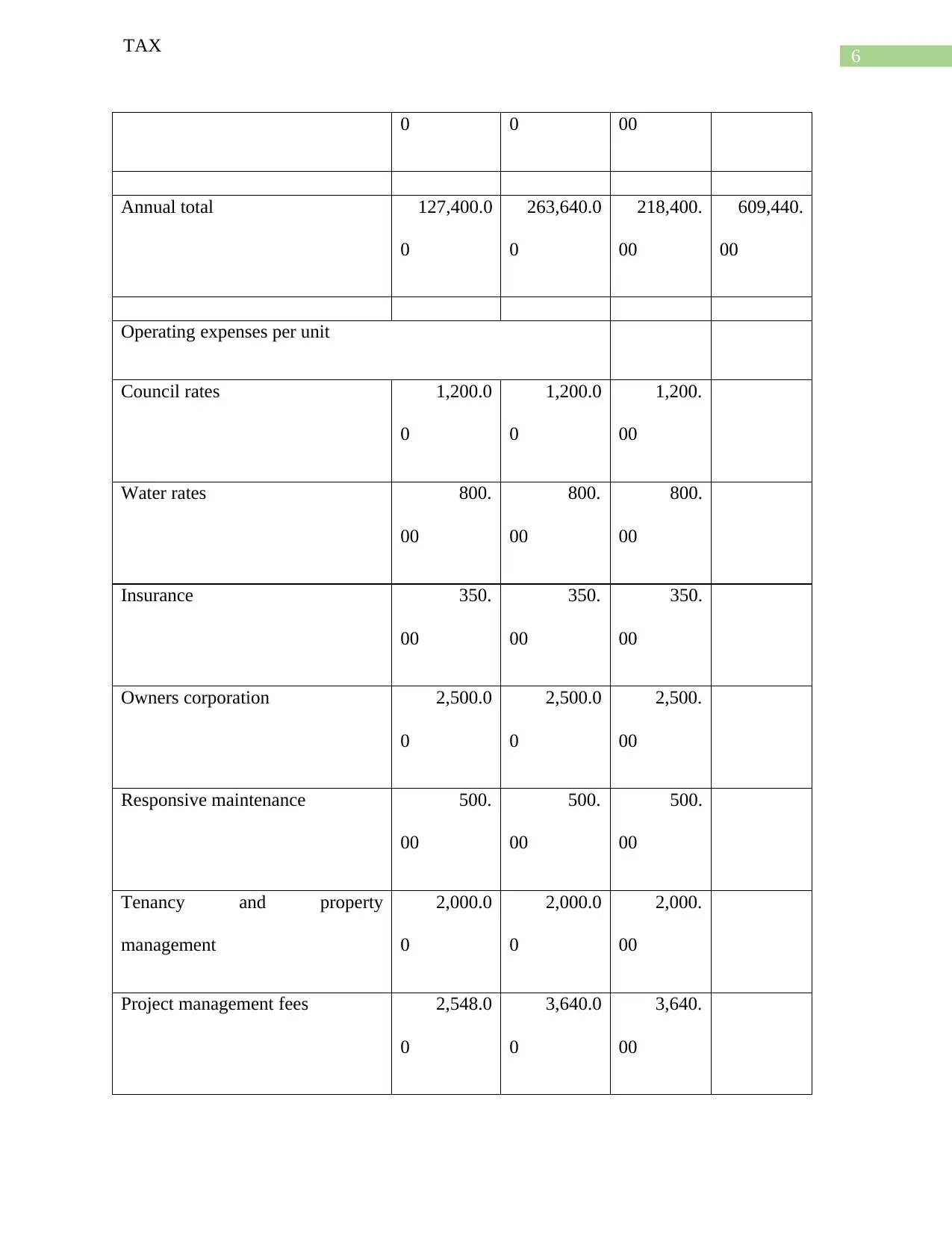

Financial analysis:

Expected financial outcome if the market rents are charged from the people for homes.

Bed 1 Bed 2 Bed 3

Number of units 7 13 10

Market rent

($)

Market rent

($)

Market rent ($)

Weekly rent 350.

00

390.

00

420.

00

Annual rent 18,200.0 20,280.0 21,840.

TAX

affordable housing with special features. The subsidy given by the Federal Government was to

support the organization to successfully deliver the social housing project in Arden-McCauley

area in Melbourne. The company has also received $360,000 from philanthropic contributions

from a charitable organization (Mikkelsen, 2015).

It is expected that 30 social housing units shall be built in the housing project to provide for the

benefits of people with disabilities and others. People with mental health conditions and without

homes shall be allocated 5 out of the 30 residential units. 5 modified units shall be allocated to

tenants with other disabilities. Elderly people without homes shall be allocated 10 units in the

new housing project and the remaining 10 units shall be kept for families.

The housing project must comply with disability codes AS 1428.1 and 1428.2 is must for the

new project to be developed in Central Melbourne (Ruben, 2018).

Financial analysis:

Expected financial outcome if the market rents are charged from the people for homes.

Bed 1 Bed 2 Bed 3

Number of units 7 13 10

Market rent

($)

Market rent

($)

Market rent ($)

Weekly rent 350.

00

390.

00

420.

00

Annual rent 18,200.0 20,280.0 21,840.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAX

0 0 00

Annual total 127,400.0

0

263,640.0

0

218,400.

00

609,440.

00

Operating expenses per unit

Council rates 1,200.0

0

1,200.0

0

1,200.

00

Water rates 800.

00

800.

00

800.

00

Insurance 350.

00

350.

00

350.

00

Owners corporation 2,500.0

0

2,500.0

0

2,500.

00

Responsive maintenance 500.

00

500.

00

500.

00

Tenancy and property

management

2,000.0

0

2,000.0

0

2,000.

00

Project management fees 2,548.0

0

3,640.0

0

3,640.

00

TAX

0 0 00

Annual total 127,400.0

0

263,640.0

0

218,400.

00

609,440.

00

Operating expenses per unit

Council rates 1,200.0

0

1,200.0

0

1,200.

00

Water rates 800.

00

800.

00

800.

00

Insurance 350.

00

350.

00

350.

00

Owners corporation 2,500.0

0

2,500.0

0

2,500.

00

Responsive maintenance 500.

00

500.

00

500.

00

Tenancy and property

management

2,000.0

0

2,000.0

0

2,000.

00

Project management fees 2,548.0

0

3,640.0

0

3,640.

00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAX

Development management fees 2,548.0

0

3,640.0

0

3,640.

00

Operating cost of each unit 12,446.0

0

14,630.0

0

14,630.

00

Total operating cost for respective

units

87,122.0

0

190,190.0

0

146,300.

00

423,612.

00

Earning before payment of interest 185,828.

00

Less: interest on debt 149,145.

00

Profit / (loss) 36,683.

00

Working notes:

Amount of loan to be taken and the interest to be paid on the debt are calculated below.

Particulars Amount ($)

Total cost of the project 7,400,000.

00

Less: Grant from Federal Govt. 5,570,000.

TAX

Development management fees 2,548.0

0

3,640.0

0

3,640.

00

Operating cost of each unit 12,446.0

0

14,630.0

0

14,630.

00

Total operating cost for respective

units

87,122.0

0

190,190.0

0

146,300.

00

423,612.

00

Earning before payment of interest 185,828.

00

Less: interest on debt 149,145.

00

Profit / (loss) 36,683.

00

Working notes:

Amount of loan to be taken and the interest to be paid on the debt are calculated below.

Particulars Amount ($)

Total cost of the project 7,400,000.

00

Less: Grant from Federal Govt. 5,570,000.

8

TAX

00

Amount to be borrowed 1,830,000.

00

Rate of interest 8.15%

Interest on borrowed fund 149,145.

00

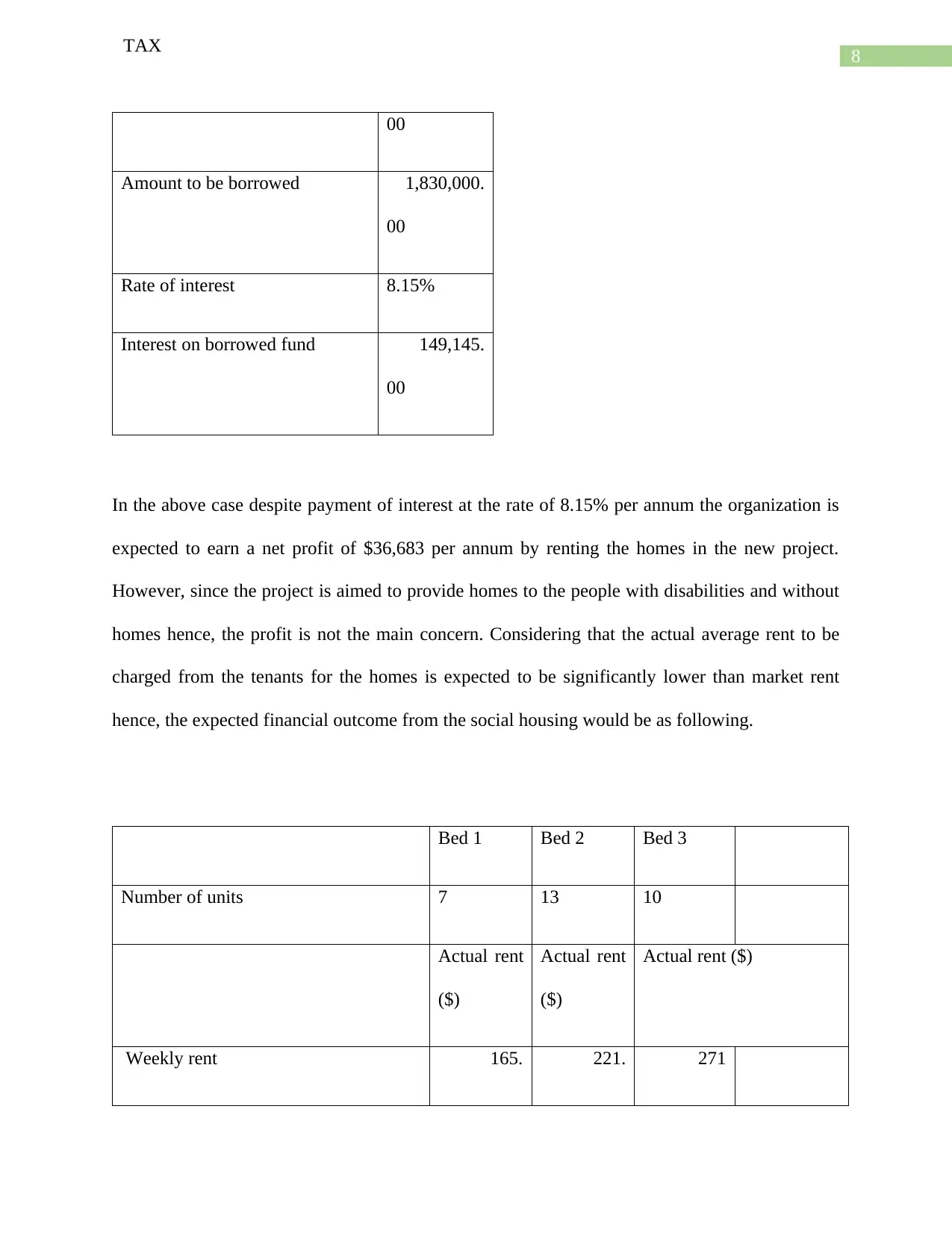

In the above case despite payment of interest at the rate of 8.15% per annum the organization is

expected to earn a net profit of $36,683 per annum by renting the homes in the new project.

However, since the project is aimed to provide homes to the people with disabilities and without

homes hence, the profit is not the main concern. Considering that the actual average rent to be

charged from the tenants for the homes is expected to be significantly lower than market rent

hence, the expected financial outcome from the social housing would be as following.

Bed 1 Bed 2 Bed 3

Number of units 7 13 10

Actual rent

($)

Actual rent

($)

Actual rent ($)

Weekly rent 165. 221. 271

TAX

00

Amount to be borrowed 1,830,000.

00

Rate of interest 8.15%

Interest on borrowed fund 149,145.

00

In the above case despite payment of interest at the rate of 8.15% per annum the organization is

expected to earn a net profit of $36,683 per annum by renting the homes in the new project.

However, since the project is aimed to provide homes to the people with disabilities and without

homes hence, the profit is not the main concern. Considering that the actual average rent to be

charged from the tenants for the homes is expected to be significantly lower than market rent

hence, the expected financial outcome from the social housing would be as following.

Bed 1 Bed 2 Bed 3

Number of units 7 13 10

Actual rent

($)

Actual rent

($)

Actual rent ($)

Weekly rent 165. 221. 271

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

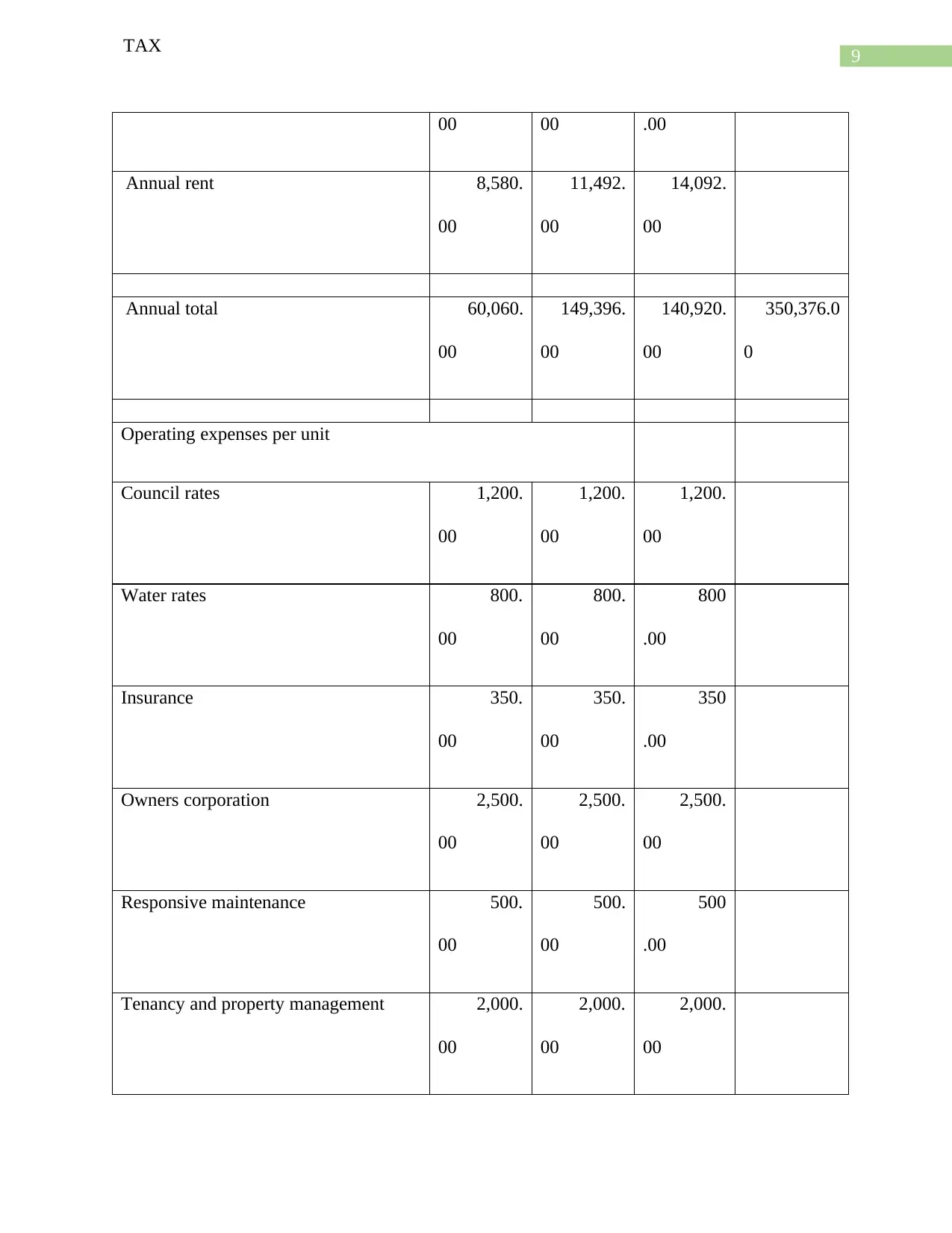

TAX

00 00 .00

Annual rent 8,580.

00

11,492.

00

14,092.

00

Annual total 60,060.

00

149,396.

00

140,920.

00

350,376.0

0

Operating expenses per unit

Council rates 1,200.

00

1,200.

00

1,200.

00

Water rates 800.

00

800.

00

800

.00

Insurance 350.

00

350.

00

350

.00

Owners corporation 2,500.

00

2,500.

00

2,500.

00

Responsive maintenance 500.

00

500.

00

500

.00

Tenancy and property management 2,000.

00

2,000.

00

2,000.

00

TAX

00 00 .00

Annual rent 8,580.

00

11,492.

00

14,092.

00

Annual total 60,060.

00

149,396.

00

140,920.

00

350,376.0

0

Operating expenses per unit

Council rates 1,200.

00

1,200.

00

1,200.

00

Water rates 800.

00

800.

00

800

.00

Insurance 350.

00

350.

00

350

.00

Owners corporation 2,500.

00

2,500.

00

2,500.

00

Responsive maintenance 500.

00

500.

00

500

.00

Tenancy and property management 2,000.

00

2,000.

00

2,000.

00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

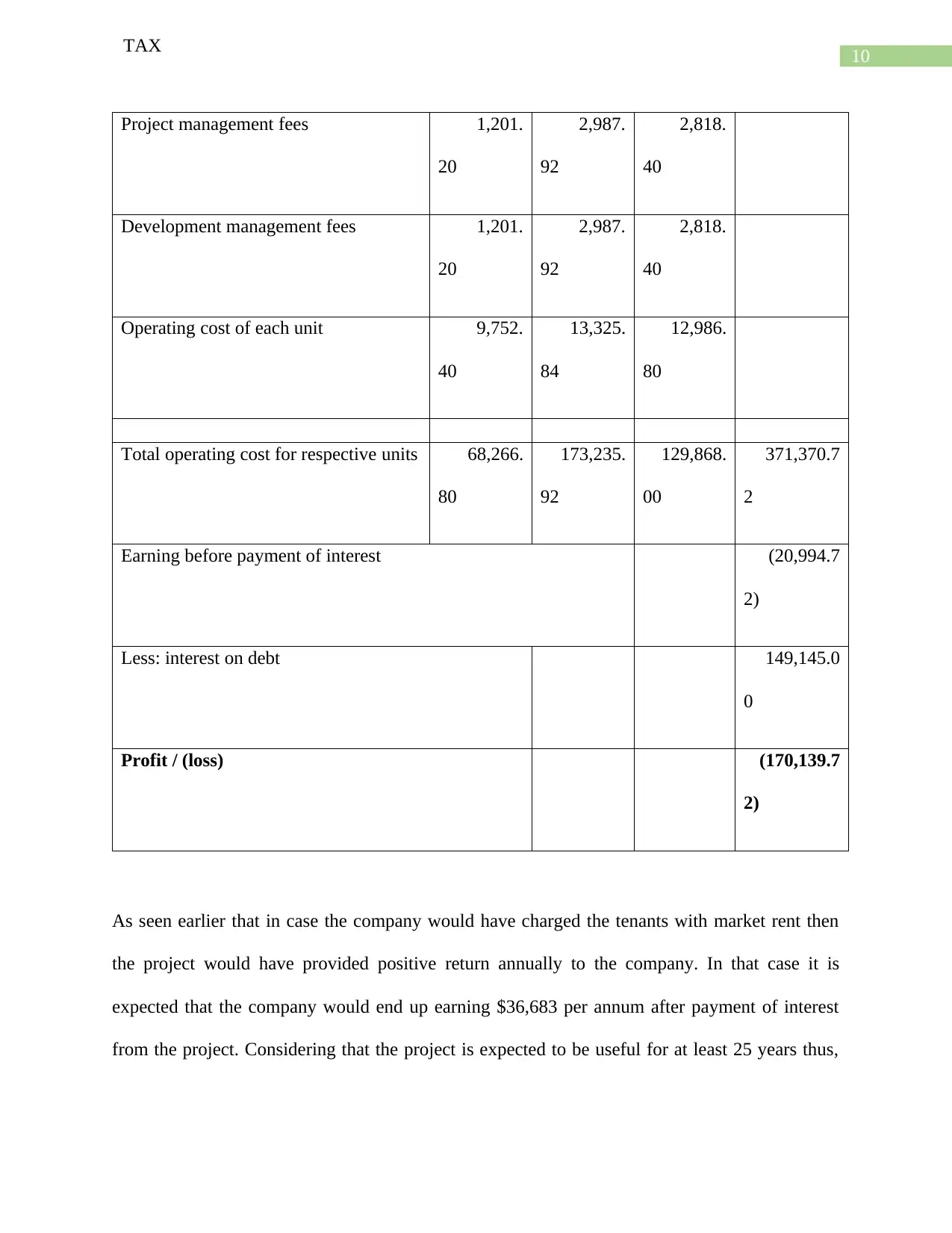

TAX

Project management fees 1,201.

20

2,987.

92

2,818.

40

Development management fees 1,201.

20

2,987.

92

2,818.

40

Operating cost of each unit 9,752.

40

13,325.

84

12,986.

80

Total operating cost for respective units 68,266.

80

173,235.

92

129,868.

00

371,370.7

2

Earning before payment of interest (20,994.7

2)

Less: interest on debt 149,145.0

0

Profit / (loss) (170,139.7

2)

As seen earlier that in case the company would have charged the tenants with market rent then

the project would have provided positive return annually to the company. In that case it is

expected that the company would end up earning $36,683 per annum after payment of interest

from the project. Considering that the project is expected to be useful for at least 25 years thus,

TAX

Project management fees 1,201.

20

2,987.

92

2,818.

40

Development management fees 1,201.

20

2,987.

92

2,818.

40

Operating cost of each unit 9,752.

40

13,325.

84

12,986.

80

Total operating cost for respective units 68,266.

80

173,235.

92

129,868.

00

371,370.7

2

Earning before payment of interest (20,994.7

2)

Less: interest on debt 149,145.0

0

Profit / (loss) (170,139.7

2)

As seen earlier that in case the company would have charged the tenants with market rent then

the project would have provided positive return annually to the company. In that case it is

expected that the company would end up earning $36,683 per annum after payment of interest

from the project. Considering that the project is expected to be useful for at least 25 years thus,

11

TAX

the total cost of the project will be recovered if the company charges market rent from the

tenants (Shtub, 2016).

Since, the average expected rent to be charged from tenants is significantly lower than market

rent hence, it would be important to assess the financial outcome of the project by using the

actual expected rent to be charged from the tenants instead of market rent. The financial outcome

with actual rent is analyzed below.

The company is expected to incur an annual loss of $170,139.72 in case the houses are rented

below the market rent, i.e. at expected annual average rent. Thus, the company will end up

incurring significant loss each year if it provides the homes at lower rent as per the above

forecast. However, as mentioned earlier the project is to be assessed on number of different

criterions and profitability is not the main consideration in determining the feasibility of the

project.

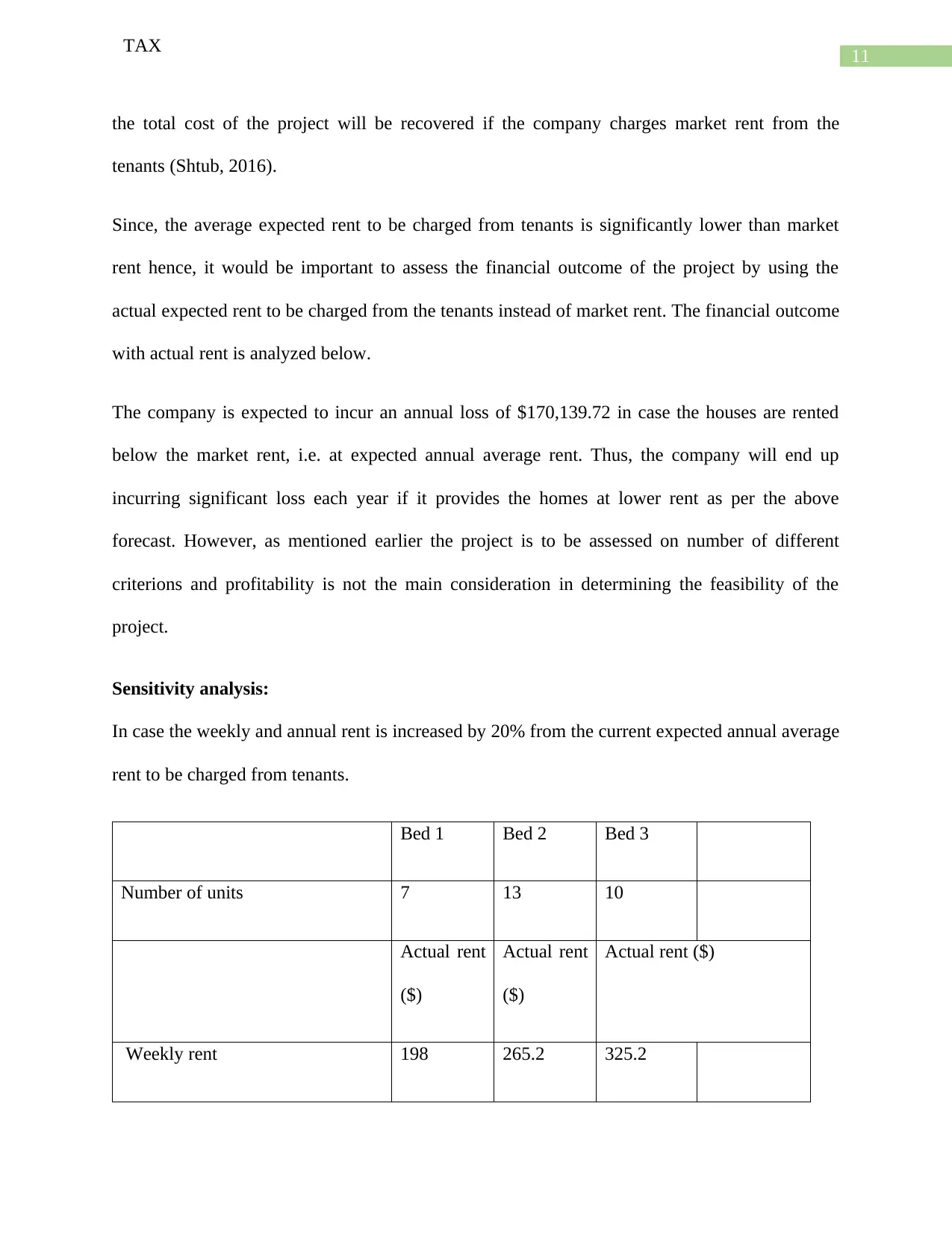

Sensitivity analysis:

In case the weekly and annual rent is increased by 20% from the current expected annual average

rent to be charged from tenants.

Bed 1 Bed 2 Bed 3

Number of units 7 13 10

Actual rent

($)

Actual rent

($)

Actual rent ($)

Weekly rent 198 265.2 325.2

TAX

the total cost of the project will be recovered if the company charges market rent from the

tenants (Shtub, 2016).

Since, the average expected rent to be charged from tenants is significantly lower than market

rent hence, it would be important to assess the financial outcome of the project by using the

actual expected rent to be charged from the tenants instead of market rent. The financial outcome

with actual rent is analyzed below.

The company is expected to incur an annual loss of $170,139.72 in case the houses are rented

below the market rent, i.e. at expected annual average rent. Thus, the company will end up

incurring significant loss each year if it provides the homes at lower rent as per the above

forecast. However, as mentioned earlier the project is to be assessed on number of different

criterions and profitability is not the main consideration in determining the feasibility of the

project.

Sensitivity analysis:

In case the weekly and annual rent is increased by 20% from the current expected annual average

rent to be charged from tenants.

Bed 1 Bed 2 Bed 3

Number of units 7 13 10

Actual rent

($)

Actual rent

($)

Actual rent ($)

Weekly rent 198 265.2 325.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.