University of Suffolk BABS Assignment: UK Housing Market Analysis

VerifiedAdded on 2023/01/10

|11

|3794

|45

Report

AI Summary

This report provides a comprehensive analysis of the UK housing market, examining its performance from 2010 to 2019 and the subsequent impact of the COVID-19 pandemic. It begins by charting the changes in average housing prices over the decades, highlighting the market's growth until 2020, and then detailing the decline due to the pandemic. The report delves into the economic determinants influencing the housing market, including disposable income, unemployment rates, interest rates, mortgage availability, and consumer confidence. It further explores the impact of government actions, such as taxes, subsidies, and price controls, on housing prices. The analysis concludes by assessing the specific effects of the COVID-19 pandemic on the UK housing market, providing a holistic view of the sector's dynamics.

evaluating internal and

external business

environment

external business

environment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.................................................................................................................................3

MAINBODY.........................................................................................................................................3

1. Changes in average prices of housing property changed in decades..........................................3

2. Economic determinants of the change in the Housing Market.......................................................4

3.Impact of government actions over housing prices in UK..............................................................7

4. Impact of COVID-19 on UK housing market................................................................................8

CONCLUSION.....................................................................................................................................9

REFERENCES....................................................................................................................................11

INTRODUCTION.................................................................................................................................3

MAINBODY.........................................................................................................................................3

1. Changes in average prices of housing property changed in decades..........................................3

2. Economic determinants of the change in the Housing Market.......................................................4

3.Impact of government actions over housing prices in UK..............................................................7

4. Impact of COVID-19 on UK housing market................................................................................8

CONCLUSION.....................................................................................................................................9

REFERENCES....................................................................................................................................11

INTRODUCTION

Business environment is a sum of internal and external factors that put an impact over

the business outcomes of organisation. This report is based on the case study on housing

prices in UK. Over the last one decade how the housing prices in UK has changed.

Comparative analysis over the average housing prices in UK will be done in this project.

Economic determinant will also analyse in this report to assess the impact over the housing

prices in UK. What are the impacts government actions has put over the housing prices in UK

will also further analyse in this report. Furthermore report will also assess the effects of

COVID 19 over the housing prices in UK.

MAINBODY

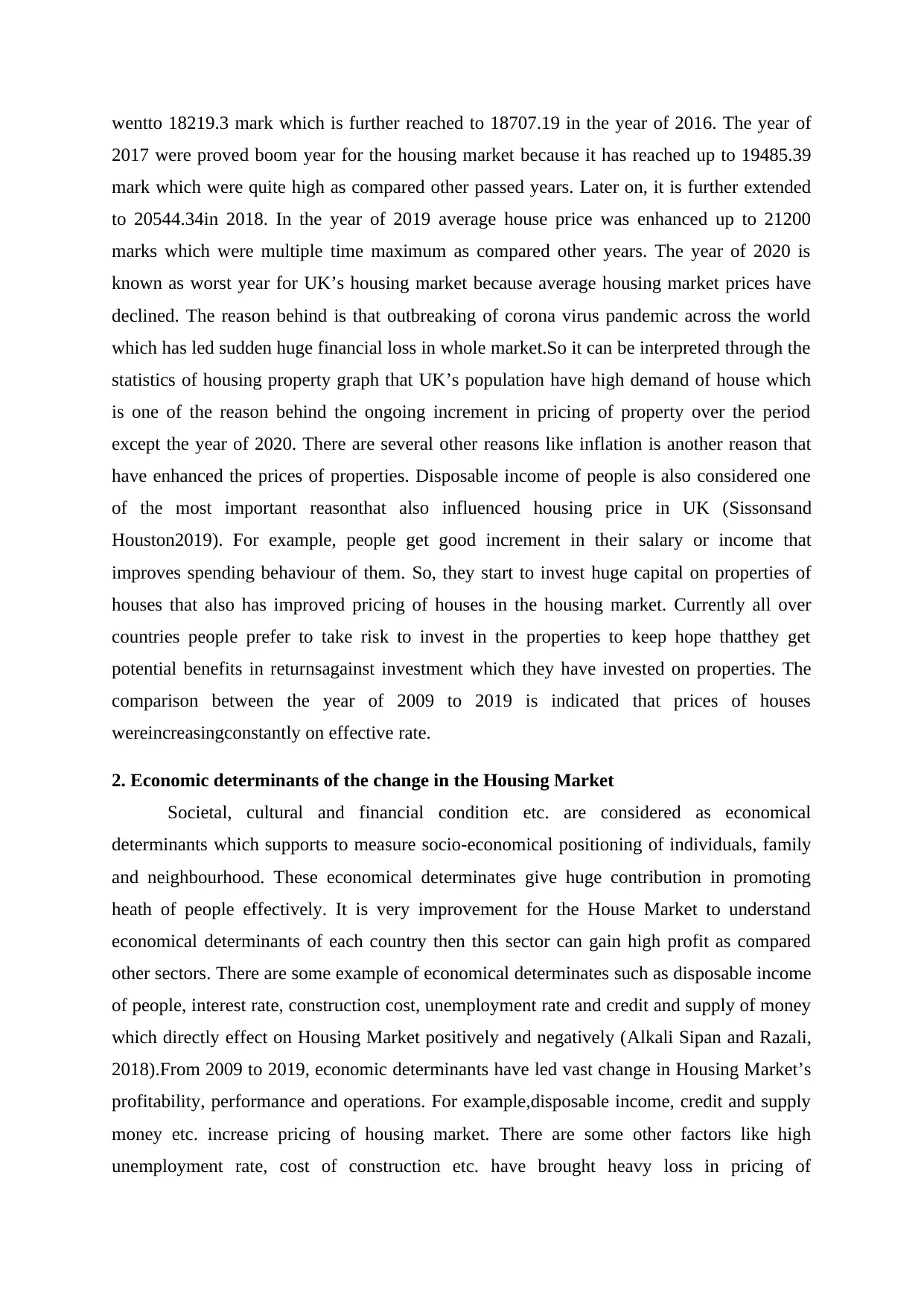

1. Changes in average prices of housing property changed in decades

(Tanand et.al., 2018)

From the above graph can be analysed that how prices of housing market in UK have

improved from the year of 2010 to 2019. The average housing prices of UK have increased

21200 marks in 2019 as compared in the year of 2010 around 14992.05 marks. While in the

year of 2011 house price is went around 15542.58 marks that was further externed upto

16197.91 marks. With this comparison project can be estimated that average housing price of

market has been grown rapidly over the period in UK. For example,the year of 2013 average

price of housing has increased up to 16784.85 marks which is extended around 17521.75 in

2014 (Agnello, Castroand Sousa, 2018). As same in the year of 2015 whereas average house

Business environment is a sum of internal and external factors that put an impact over

the business outcomes of organisation. This report is based on the case study on housing

prices in UK. Over the last one decade how the housing prices in UK has changed.

Comparative analysis over the average housing prices in UK will be done in this project.

Economic determinant will also analyse in this report to assess the impact over the housing

prices in UK. What are the impacts government actions has put over the housing prices in UK

will also further analyse in this report. Furthermore report will also assess the effects of

COVID 19 over the housing prices in UK.

MAINBODY

1. Changes in average prices of housing property changed in decades

(Tanand et.al., 2018)

From the above graph can be analysed that how prices of housing market in UK have

improved from the year of 2010 to 2019. The average housing prices of UK have increased

21200 marks in 2019 as compared in the year of 2010 around 14992.05 marks. While in the

year of 2011 house price is went around 15542.58 marks that was further externed upto

16197.91 marks. With this comparison project can be estimated that average housing price of

market has been grown rapidly over the period in UK. For example,the year of 2013 average

price of housing has increased up to 16784.85 marks which is extended around 17521.75 in

2014 (Agnello, Castroand Sousa, 2018). As same in the year of 2015 whereas average house

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

wentto 18219.3 mark which is further reached to 18707.19 in the year of 2016. The year of

2017 were proved boom year for the housing market because it has reached up to 19485.39

mark which were quite high as compared other passed years. Later on, it is further extended

to 20544.34in 2018. In the year of 2019 average house price was enhanced up to 21200

marks which were multiple time maximum as compared other years. The year of 2020 is

known as worst year for UK’s housing market because average housing market prices have

declined. The reason behind is that outbreaking of corona virus pandemic across the world

which has led sudden huge financial loss in whole market.So it can be interpreted through the

statistics of housing property graph that UK’s population have high demand of house which

is one of the reason behind the ongoing increment in pricing of property over the period

except the year of 2020. There are several other reasons like inflation is another reason that

have enhanced the prices of properties. Disposable income of people is also considered one

of the most important reasonthat also influenced housing price in UK (Sissonsand

Houston2019). For example, people get good increment in their salary or income that

improves spending behaviour of them. So, they start to invest huge capital on properties of

houses that also has improved pricing of houses in the housing market. Currently all over

countries people prefer to take risk to invest in the properties to keep hope thatthey get

potential benefits in returnsagainst investment which they have invested on properties. The

comparison between the year of 2009 to 2019 is indicated that prices of houses

wereincreasingconstantly on effective rate.

2. Economic determinants of the change in the Housing Market

Societal, cultural and financial condition etc. are considered as economical

determinants which supports to measure socio-economical positioning of individuals, family

and neighbourhood. These economical determinates give huge contribution in promoting

heath of people effectively. It is very improvement for the House Market to understand

economical determinants of each country then this sector can gain high profit as compared

other sectors. There are some example of economical determinates such as disposable income

of people, interest rate, construction cost, unemployment rate and credit and supply of money

which directly effect on Housing Market positively and negatively (Alkali Sipan and Razali,

2018).From 2009 to 2019, economic determinants have led vast change in Housing Market’s

profitability, performance and operations. For example,disposable income, credit and supply

money etc. increase pricing of housing market. There are some other factors like high

unemployment rate, cost of construction etc. have brought heavy loss in pricing of

2017 were proved boom year for the housing market because it has reached up to 19485.39

mark which were quite high as compared other passed years. Later on, it is further extended

to 20544.34in 2018. In the year of 2019 average house price was enhanced up to 21200

marks which were multiple time maximum as compared other years. The year of 2020 is

known as worst year for UK’s housing market because average housing market prices have

declined. The reason behind is that outbreaking of corona virus pandemic across the world

which has led sudden huge financial loss in whole market.So it can be interpreted through the

statistics of housing property graph that UK’s population have high demand of house which

is one of the reason behind the ongoing increment in pricing of property over the period

except the year of 2020. There are several other reasons like inflation is another reason that

have enhanced the prices of properties. Disposable income of people is also considered one

of the most important reasonthat also influenced housing price in UK (Sissonsand

Houston2019). For example, people get good increment in their salary or income that

improves spending behaviour of them. So, they start to invest huge capital on properties of

houses that also has improved pricing of houses in the housing market. Currently all over

countries people prefer to take risk to invest in the properties to keep hope thatthey get

potential benefits in returnsagainst investment which they have invested on properties. The

comparison between the year of 2009 to 2019 is indicated that prices of houses

wereincreasingconstantly on effective rate.

2. Economic determinants of the change in the Housing Market

Societal, cultural and financial condition etc. are considered as economical

determinants which supports to measure socio-economical positioning of individuals, family

and neighbourhood. These economical determinates give huge contribution in promoting

heath of people effectively. It is very improvement for the House Market to understand

economical determinants of each country then this sector can gain high profit as compared

other sectors. There are some example of economical determinates such as disposable income

of people, interest rate, construction cost, unemployment rate and credit and supply of money

which directly effect on Housing Market positively and negatively (Alkali Sipan and Razali,

2018).From 2009 to 2019, economic determinants have led vast change in Housing Market’s

profitability, performance and operations. For example,disposable income, credit and supply

money etc. increase pricing of housing market. There are some other factors like high

unemployment rate, cost of construction etc. have brought heavy loss in pricing of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UK’shousing market. Generally, price of the Housing Market improves when disposable

income of people is high and lowerinterest rate of financial institutions. Impact of economical

determinateon the price of Housing Market are mentioned below:

Economic growth: It is considered one of the main economic determinantsamong

others which directly impact on pricing of housing market. For example,when disposable

income of population is strong that automatically improves demands of housing in housing

market because people are highly capable to invest their more funds on houses. With this fact

it can be understood that when demand of house become high that directly declines

bargaining power of customers for the hike price of house. However,demands of house is

properly based on income elasticity i.e. improving disposable income. When people have

good disposable income that improves spending behaviour on the house. As same hypothesis

is applied in recession time such as when people’s disposable income decreases or loss job or

may possible to fail paying mortgage payments that directly impact on their purchasing

behaviour because they do not have such income which can invest on buying of luxury

houses.

Unemployment rate: It is another economicaldeterminantthat also affect housing

market in the UK. Country’s economic growth is properly dependent of employment ratio

(Ansell and Adler, 2019). For example, in 2009 employment ratiowas too less due to less

availability of job opportunity which caused most of the people wereunable to afford

housesand others who were potential had fear of job loss or unemployment that demotivated

them to invest in housing market. So, economic growth of UK was too weak in 2009. This

issue became major issues for the UK’s government so they gave response on this situation

by releasing large number of job vacancies for the people so that unemployment issue

resolve. Due to high presence of job opportunities have increased interest of individuals to

grab job opportunity and improves their lifestyle. By and by employment ratio was increasing

which improves demands of housing market in them.Currently UK become financially strong

country among other developed countries. Thus,housing market has become one of the most

emerging market among other top markets till 2019. So, it can be examined that

unemployment ratio in country is also an effective economic determinant.

Interest rate: This determinant impacts on the price of monthly mortgage effectively

such as when interest rate of mortgage is high then people avoids to take loanthat

automatically impact on demands of housing market. However, high interest rate increases

income of people is high and lowerinterest rate of financial institutions. Impact of economical

determinateon the price of Housing Market are mentioned below:

Economic growth: It is considered one of the main economic determinantsamong

others which directly impact on pricing of housing market. For example,when disposable

income of population is strong that automatically improves demands of housing in housing

market because people are highly capable to invest their more funds on houses. With this fact

it can be understood that when demand of house become high that directly declines

bargaining power of customers for the hike price of house. However,demands of house is

properly based on income elasticity i.e. improving disposable income. When people have

good disposable income that improves spending behaviour on the house. As same hypothesis

is applied in recession time such as when people’s disposable income decreases or loss job or

may possible to fail paying mortgage payments that directly impact on their purchasing

behaviour because they do not have such income which can invest on buying of luxury

houses.

Unemployment rate: It is another economicaldeterminantthat also affect housing

market in the UK. Country’s economic growth is properly dependent of employment ratio

(Ansell and Adler, 2019). For example, in 2009 employment ratiowas too less due to less

availability of job opportunity which caused most of the people wereunable to afford

housesand others who were potential had fear of job loss or unemployment that demotivated

them to invest in housing market. So, economic growth of UK was too weak in 2009. This

issue became major issues for the UK’s government so they gave response on this situation

by releasing large number of job vacancies for the people so that unemployment issue

resolve. Due to high presence of job opportunities have increased interest of individuals to

grab job opportunity and improves their lifestyle. By and by employment ratio was increasing

which improves demands of housing market in them.Currently UK become financially strong

country among other developed countries. Thus,housing market has become one of the most

emerging market among other top markets till 2019. So, it can be examined that

unemployment ratio in country is also an effective economic determinant.

Interest rate: This determinant impacts on the price of monthly mortgage effectively

such as when interest rate of mortgage is high then people avoids to take loanthat

automatically impact on demands of housing market. However, high interest rate increases

prices of rented houses that makes it attractive instead of buying.Meanwhile 2011 to 2012,

there were various property dealing organization in the Housing Market which faced financial

loss due to sudden how increment in interest rate because most of the small-scale

propertydealers were failed to pay mortgage payments with high interest rates. That’s why

UK’s government declared to reduce interest rate of mortgage payments in 2013

(Augustyniak and et.al., 2018). This announcement again improved buying behaviour of

homeowners whch directly enhanced prices of UK’s housing market.

Mortgage availability: Mortgage availability in UK’s market is another considerable

economic determinant because they play improvement role in improving spending behaviour

of homeowners.The years of 2009 to 2014 are considered flourishingyears for the UK’s

Housing market. the reason behind is that there were number of bankswhich were keening to

offerloansto the people as much as they require. So, lots of banksinfluences UK’s population

to lend large capital in multiple times from their actual income through advertisements. Apart

from this Mortgagesoffers loan on low deposit means hundred percent loans which inspires

homeowners to lend large capitals four to five times. Thus, extensive availability of

mortgages has increased demands of houses in the housing market while property dealers got

opportunity to generate high profit margin on each house in 2013 (Milesand Monro, 2019).

There were other banks that provided credit crunch services which raised funds to lend on the

money markets. The credit crunch services has tightenedlending criteria and needs huge

deposit to buy houses. Such process reduced availability of Mortgages in it’s busines market

that directly led fall in demanding of house among homeowners. In this situation UK’s

government took initiatives to improve mortgages availability such as they decreased 0.5%

interest rate which decreased mortgage payments. While the years of 2016 to 2019, there

were various banks which creates different platforms of financial services so that customers

can lend money accordingly their requirements without worrying about interest rates.

Consumer Confidence: Consumer confidence is also included in economic

determinants. The reason behind is that it is important to determine that people attitude such

as they like to take risk of buying houses on loan payments or avoid to buy house on lend

payments (Hamnettand Reades, 2019). So, expectation is more crucial in the housing market

because when people are filled with more expectation then they prefer to take risk by buying

large number of houses to keep hope that they will get high financial benefit. In other case,

when people have nature to avoid risk then they do not like to buy with this fear like house

prices can be fall out. So, confidence is considered major determinants of housing market

there were various property dealing organization in the Housing Market which faced financial

loss due to sudden how increment in interest rate because most of the small-scale

propertydealers were failed to pay mortgage payments with high interest rates. That’s why

UK’s government declared to reduce interest rate of mortgage payments in 2013

(Augustyniak and et.al., 2018). This announcement again improved buying behaviour of

homeowners whch directly enhanced prices of UK’s housing market.

Mortgage availability: Mortgage availability in UK’s market is another considerable

economic determinant because they play improvement role in improving spending behaviour

of homeowners.The years of 2009 to 2014 are considered flourishingyears for the UK’s

Housing market. the reason behind is that there were number of bankswhich were keening to

offerloansto the people as much as they require. So, lots of banksinfluences UK’s population

to lend large capital in multiple times from their actual income through advertisements. Apart

from this Mortgagesoffers loan on low deposit means hundred percent loans which inspires

homeowners to lend large capitals four to five times. Thus, extensive availability of

mortgages has increased demands of houses in the housing market while property dealers got

opportunity to generate high profit margin on each house in 2013 (Milesand Monro, 2019).

There were other banks that provided credit crunch services which raised funds to lend on the

money markets. The credit crunch services has tightenedlending criteria and needs huge

deposit to buy houses. Such process reduced availability of Mortgages in it’s busines market

that directly led fall in demanding of house among homeowners. In this situation UK’s

government took initiatives to improve mortgages availability such as they decreased 0.5%

interest rate which decreased mortgage payments. While the years of 2016 to 2019, there

were various banks which creates different platforms of financial services so that customers

can lend money accordingly their requirements without worrying about interest rates.

Consumer Confidence: Consumer confidence is also included in economic

determinants. The reason behind is that it is important to determine that people attitude such

as they like to take risk of buying houses on loan payments or avoid to buy house on lend

payments (Hamnettand Reades, 2019). So, expectation is more crucial in the housing market

because when people are filled with more expectation then they prefer to take risk by buying

large number of houses to keep hope that they will get high financial benefit. In other case,

when people have nature to avoid risk then they do not like to buy with this fear like house

prices can be fall out. So, confidence is considered major determinants of housing market

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which influence people to buy large number of houses on risk. UK’s population are quite

confident and hopeful as compared other countries population, so they like to take risk in the

form of buying large number of houses without fearing about financial crisis.

3.Impact of government actions over housing prices in UK

Government in United Kingdom has always been concerned towards controlling the

housing prices in United Kingdom. It is important to control the prices based on the per

capita income of UK so that proper shelters to all peoples based in UK can be served.

Different steps government has also taken to control these prices in UK. All the steps can be

summarises in following points.

Taxes and subsidiaries: Government in United Kingdom followed the tax deduction policy

to control the housing prices of UK. This policy of government created positive impacts over

controlling the housing prices. This step taken by government has motivated to all peoples in

UK to buy properties in UK. With the implication of section 24 the tax benefits granted to all

buyer willing to purchase in United Kingdom (Reeves, Levin and Ueda, 2016). This step of

government has increased the demands of housing properties in UK. Tax deduction always

creates positive impact over the mindset of peoples in order to buy assets. Government also

serves subsidies to all the individual plans to purchase property in UK. Tax and subsidiary

benefits impacts over the decision making of all investors looking for investment in UK and

it also influence the decision making of all business persons looking for opening up new

ventures or expand the business in UK. All these factors have increased the property prices

due to increase in demands of property in UK. This step of government has also controlled

the prices at some extent but it has significantly increased the property prices also due to

increase in demand.

Maximum and minimum prices: Government in United Kingdom follow practice to set the

maximum and minimum prices for housing property. Minimum rate denote the minimum

purchase price buyer needs to pay and all sellers or property dealers has specific right to offer

property at this price. Maximum price denoted the figure which can be maximum chargeable

in any case irrespective to any demand of a particular property (Chekh and Vinnyk, 2017).

On the basis of different factors like location, demand, average property price in such

location, per capita income of peoples in UK and many other factors that has influenced the

property prices. The maximum and minimum prices will differ based on the location of

property. Every location in United Kingdom carries the minimum as well as maximum price

confident and hopeful as compared other countries population, so they like to take risk in the

form of buying large number of houses without fearing about financial crisis.

3.Impact of government actions over housing prices in UK

Government in United Kingdom has always been concerned towards controlling the

housing prices in United Kingdom. It is important to control the prices based on the per

capita income of UK so that proper shelters to all peoples based in UK can be served.

Different steps government has also taken to control these prices in UK. All the steps can be

summarises in following points.

Taxes and subsidiaries: Government in United Kingdom followed the tax deduction policy

to control the housing prices of UK. This policy of government created positive impacts over

controlling the housing prices. This step taken by government has motivated to all peoples in

UK to buy properties in UK. With the implication of section 24 the tax benefits granted to all

buyer willing to purchase in United Kingdom (Reeves, Levin and Ueda, 2016). This step of

government has increased the demands of housing properties in UK. Tax deduction always

creates positive impact over the mindset of peoples in order to buy assets. Government also

serves subsidies to all the individual plans to purchase property in UK. Tax and subsidiary

benefits impacts over the decision making of all investors looking for investment in UK and

it also influence the decision making of all business persons looking for opening up new

ventures or expand the business in UK. All these factors have increased the property prices

due to increase in demands of property in UK. This step of government has also controlled

the prices at some extent but it has significantly increased the property prices also due to

increase in demand.

Maximum and minimum prices: Government in United Kingdom follow practice to set the

maximum and minimum prices for housing property. Minimum rate denote the minimum

purchase price buyer needs to pay and all sellers or property dealers has specific right to offer

property at this price. Maximum price denoted the figure which can be maximum chargeable

in any case irrespective to any demand of a particular property (Chekh and Vinnyk, 2017).

On the basis of different factors like location, demand, average property price in such

location, per capita income of peoples in UK and many other factors that has influenced the

property prices. The maximum and minimum prices will differ based on the location of

property. Every location in United Kingdom carries the minimum as well as maximum price

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that can be charged by the owner of the property. Both these prices have increased over the

year irrespective of any control of government over the property prices in UK. Apart from the

increasing trend in property prices due to these steps and actions of government at some level

government have been capable to control the prices of property in UK.

Regulating the market: Government in United Kingdom has also regulated the property

market on a regular basis. Regulations are also modified time to time based on the demands

of the market. Necessary modification in property prices has allowed government to control

the property trade in UK at larger extent. Regulatory compliances allows government to keep

they eye over every property trade. This drives government to check that weather the

property trade is conducting based on the rules and regulation or not (Beynon-Davies, 2020).

These regulations have created positive impacts over the property prices hike in United

Kingdom. Regulations are aimed to control the property market of United Kingdom.

Regulation of government like tax deduction and subsidiaries has significantly impacted the

property trade in UK.

State ownership: In UK every property comes under the state ownership. The property

located in whichever state will be the owner of such property. In UK even the state carries

specific right to make any regulation due to ownership. State has its own regulation which

also needs to get fulfilled in order to conduct the property trade in UK (Köhler, 2020). This

step of government by giving the ownership to states has also controlled the prices at some

extent apart from increasing demands of property in UK. This supported government to

implement minimum and maximum prices of property.

All the above points have denoted different actions and steps taken by government to

control the property prices in UK. This is becomes mandatory for government to have a

control over the prices so that irrespective to any income group all peoples in UK can afford a

shelter for the family. Maximum and minimum price regulation opposed by government is

among the major steps behind controlling the property prices in UK.

4. Impact of COVID-19 on UK housing market

COCID 19 Pandemic has significantly impacted the entire business environment

across the globe. Due to these pandemic prices has decreased in UK of all the properties due

to less demand of property. The incident has badly heat the income base of people all across

the globe. Many industries have already shut its operations. The individuals who have already

purchased the property just before the COVID 19 are not been able to pay the interest or

year irrespective of any control of government over the property prices in UK. Apart from the

increasing trend in property prices due to these steps and actions of government at some level

government have been capable to control the prices of property in UK.

Regulating the market: Government in United Kingdom has also regulated the property

market on a regular basis. Regulations are also modified time to time based on the demands

of the market. Necessary modification in property prices has allowed government to control

the property trade in UK at larger extent. Regulatory compliances allows government to keep

they eye over every property trade. This drives government to check that weather the

property trade is conducting based on the rules and regulation or not (Beynon-Davies, 2020).

These regulations have created positive impacts over the property prices hike in United

Kingdom. Regulations are aimed to control the property market of United Kingdom.

Regulation of government like tax deduction and subsidiaries has significantly impacted the

property trade in UK.

State ownership: In UK every property comes under the state ownership. The property

located in whichever state will be the owner of such property. In UK even the state carries

specific right to make any regulation due to ownership. State has its own regulation which

also needs to get fulfilled in order to conduct the property trade in UK (Köhler, 2020). This

step of government by giving the ownership to states has also controlled the prices at some

extent apart from increasing demands of property in UK. This supported government to

implement minimum and maximum prices of property.

All the above points have denoted different actions and steps taken by government to

control the property prices in UK. This is becomes mandatory for government to have a

control over the prices so that irrespective to any income group all peoples in UK can afford a

shelter for the family. Maximum and minimum price regulation opposed by government is

among the major steps behind controlling the property prices in UK.

4. Impact of COVID-19 on UK housing market

COCID 19 Pandemic has significantly impacted the entire business environment

across the globe. Due to these pandemic prices has decreased in UK of all the properties due

to less demand of property. The incident has badly heat the income base of people all across

the globe. Many industries have already shut its operations. The individuals who have already

purchased the property just before the COVID 19 are not been able to pay the interest or

repay the housing loans. The whole situation of COVID 19 has immensely suffered to middle

class and lower middle class backgrounds of peoples all across the globe (Mani, 2020). The

income of such people has blocked due to unemployment. The pandemic has increased the

level of poverty in UK. All the industries along with real estate are suffering from the low

demands in market. Peoples become more restricted to do any serious investment. The

market has witnessed the complete instability due to the casualties in UK. It can be projected

that there is a possibility that the situation might get some time to get back to normal as the

normal situation will take time to come UK.

After the incident of COVID 19 demands have significantly touched to its lowest rate in UK.

The property prices in both industrial segment and residential segment have lost its earlier

values. No investment is getting registered after the COVID 19 in UK. Major investments are

postponed by industries and entrepreneurs to expand the business in UK. The biggest

influence COVID 19 has created due to unemployment. Peoples have loosed the jobs market

has completely diminished and many industries have loosed the growth rate. All these

situations are raised due to lockdown in the country. The growth rate registered earlier could

go down completely. Companies do not even able to meet up its expenses after the situation.

This is predicted that it might take another one or two year for the market to get into its

normal pace. In UK income background of peoples are very good which have supported them

to survive in this pandemic crisis somehow (Nam, Lee and Lee, 2019). This made them

realise to think before doing any expense. All these aspects have reduced the property

demands in UK after COVID 19. The situation of COVID 19 has also raised opportunity for

high income background peoples or for upper economic class to invest in property market.

This is a good time to invest as the property prices are low. This factor of COVID 19 has

created some impacts in UK and many upper economic class peoples have looked up for

investments in properties. This has keeps the property prices at certain level. The market

could also fluctuate due to this aspect of COVID 19. Apart from this it can be projected that

the pandemic has negative affected the property market UK. Investments are getting lower in

the crisis.

CONCLUSION

This report has projected the analysis of the property prices in UK. It can be projected

that many steps of government like minimum and maximum price fixation, tax benefits and

subsidiaries and other steps have created a positive impacts over controlling the property

class and lower middle class backgrounds of peoples all across the globe (Mani, 2020). The

income of such people has blocked due to unemployment. The pandemic has increased the

level of poverty in UK. All the industries along with real estate are suffering from the low

demands in market. Peoples become more restricted to do any serious investment. The

market has witnessed the complete instability due to the casualties in UK. It can be projected

that there is a possibility that the situation might get some time to get back to normal as the

normal situation will take time to come UK.

After the incident of COVID 19 demands have significantly touched to its lowest rate in UK.

The property prices in both industrial segment and residential segment have lost its earlier

values. No investment is getting registered after the COVID 19 in UK. Major investments are

postponed by industries and entrepreneurs to expand the business in UK. The biggest

influence COVID 19 has created due to unemployment. Peoples have loosed the jobs market

has completely diminished and many industries have loosed the growth rate. All these

situations are raised due to lockdown in the country. The growth rate registered earlier could

go down completely. Companies do not even able to meet up its expenses after the situation.

This is predicted that it might take another one or two year for the market to get into its

normal pace. In UK income background of peoples are very good which have supported them

to survive in this pandemic crisis somehow (Nam, Lee and Lee, 2019). This made them

realise to think before doing any expense. All these aspects have reduced the property

demands in UK after COVID 19. The situation of COVID 19 has also raised opportunity for

high income background peoples or for upper economic class to invest in property market.

This is a good time to invest as the property prices are low. This factor of COVID 19 has

created some impacts in UK and many upper economic class peoples have looked up for

investments in properties. This has keeps the property prices at certain level. The market

could also fluctuate due to this aspect of COVID 19. Apart from this it can be projected that

the pandemic has negative affected the property market UK. Investments are getting lower in

the crisis.

CONCLUSION

This report has projected the analysis of the property prices in UK. It can be projected

that many steps of government like minimum and maximum price fixation, tax benefits and

subsidiaries and other steps have created a positive impacts over controlling the property

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

prices in UK. Over the last one decade the prices of property has increased immensely due to

increasing trends of property demands in UK. The pandemic of COVID 19 has changed the

position of market immensely. It has reduced the demands of all the sector involve in

business environment. The property prices after the COVID crisis has reduced which has

given opportunity to upper economic background peoples to invest in residential properties to

gain the advantages of this crisis. This can be predicted that it will take some time to back the

market at a normal pace.

increasing trends of property demands in UK. The pandemic of COVID 19 has changed the

position of market immensely. It has reduced the demands of all the sector involve in

business environment. The property prices after the COVID crisis has reduced which has

given opportunity to upper economic background peoples to invest in residential properties to

gain the advantages of this crisis. This can be predicted that it will take some time to back the

market at a normal pace.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Agnello, L., Castro, V. and Sousa, R.M., 2018. Economic activity, credit market conditions,

and the housing market. Macroeconomic Dynamics, 22(7), pp.1769-1789.

Alkali, M.A., Sipan, I. and Razali, M.N., 2018. An Overview of Macro-Economic

Determinants of Real Estate Price in . International Journal of Engineering &

Technology, 7(3.30), pp.484-488.

Ansell, B. and Adler, D., 2019. Brexit and the Politics of Housing in Britain. The Political

Quarterly, 90, pp.105-116.

Augustyniak, H and et.al., 2018. Empirical analysis of the determinants of the housing cycle

in the primary housing market and its forecast. Recent tRends, p.103.

Beynon-Davies, P., 2020. Business information systems. Red Globe Press.

Chekh, N. and Vinnyk, I., 2017. Regulatory environment of business activities in

Ukraine. Innovative Technologies and Scientific Solutions for Industries, (1 (1).

pp.124-129.

Hamnett, C. and Reades, J., 2019. Mind the gap: implications of overseas investment for

regional house price divergence in Britain. Housing Studies, 34(3), pp.388-406.

Köhler, I., 2020. EU-Vietnam Free Trade Agreement-A study of EVFTA’s impact on

authoritative control in Vietnam’s business environment.

Mani, M. I. E., 2020. Future of Business Education in India. Tathapi with ISSN 2320-0693 is

an UGC CARE Journal. 19(46). pp.1-4.

Miles, D. and Monro, V., 2019. UK house prices and three decades of decline in the risk-free

real interest rate.

Nam, D., Lee, J. and Lee, H., 2019. Business analytics use in CRM: A nomological net from

IT competence to CRM performance. International Journal of Information

Management. 45. pp.233-245.

Reeves, M., Levin, S. and Ueda, D., 2016. The biology of corporate survival: Natural

ecosystems hold surprising lessons for business. Harvard Business Review. 94(1-2).

pp.46-56.

Sissons, P. and Houston, D., 2019. Changes in transitions from private renting to

homeownership in the context of rapidly rising house prices. Housing Studies, 34(1),

pp.49-65.

Tan, C. T. and et.al., 2018. A Nonlinear ARDL Analysis on the Relation between Housing

Price and Interest Rate: The case of Malaysia. Journal of Islamic, Social, Economics

and Development. 3(14). pp.109-121.

Books and Journals

Agnello, L., Castro, V. and Sousa, R.M., 2018. Economic activity, credit market conditions,

and the housing market. Macroeconomic Dynamics, 22(7), pp.1769-1789.

Alkali, M.A., Sipan, I. and Razali, M.N., 2018. An Overview of Macro-Economic

Determinants of Real Estate Price in . International Journal of Engineering &

Technology, 7(3.30), pp.484-488.

Ansell, B. and Adler, D., 2019. Brexit and the Politics of Housing in Britain. The Political

Quarterly, 90, pp.105-116.

Augustyniak, H and et.al., 2018. Empirical analysis of the determinants of the housing cycle

in the primary housing market and its forecast. Recent tRends, p.103.

Beynon-Davies, P., 2020. Business information systems. Red Globe Press.

Chekh, N. and Vinnyk, I., 2017. Regulatory environment of business activities in

Ukraine. Innovative Technologies and Scientific Solutions for Industries, (1 (1).

pp.124-129.

Hamnett, C. and Reades, J., 2019. Mind the gap: implications of overseas investment for

regional house price divergence in Britain. Housing Studies, 34(3), pp.388-406.

Köhler, I., 2020. EU-Vietnam Free Trade Agreement-A study of EVFTA’s impact on

authoritative control in Vietnam’s business environment.

Mani, M. I. E., 2020. Future of Business Education in India. Tathapi with ISSN 2320-0693 is

an UGC CARE Journal. 19(46). pp.1-4.

Miles, D. and Monro, V., 2019. UK house prices and three decades of decline in the risk-free

real interest rate.

Nam, D., Lee, J. and Lee, H., 2019. Business analytics use in CRM: A nomological net from

IT competence to CRM performance. International Journal of Information

Management. 45. pp.233-245.

Reeves, M., Levin, S. and Ueda, D., 2016. The biology of corporate survival: Natural

ecosystems hold surprising lessons for business. Harvard Business Review. 94(1-2).

pp.46-56.

Sissons, P. and Houston, D., 2019. Changes in transitions from private renting to

homeownership in the context of rapidly rising house prices. Housing Studies, 34(1),

pp.49-65.

Tan, C. T. and et.al., 2018. A Nonlinear ARDL Analysis on the Relation between Housing

Price and Interest Rate: The case of Malaysia. Journal of Islamic, Social, Economics

and Development. 3(14). pp.109-121.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.