Detailed Finance Report: Assessment 1 and 2 for Houzit Pty Ltd

VerifiedAdded on 2023/06/09

|16

|3519

|483

Report

AI Summary

This report provides a comprehensive analysis of financial data for Houzit Pty Ltd, encompassing two assessments. Assessment 1 focuses on sales and profit budgets, cash flow analysis, and aged debtor schedules, providing detailed breakdowns of sales percentages, GST calculations, and debtor aging. It also addresses key financial concepts such as income tax, corporate regulations, accounting software, and the matching principle, offering insights into probity, risk management, and potential improvements to enhance financial performance. Assessment 2 delves into budget variances, comparing actual results to the budget across various financial metrics, including sales, cost of goods sold, and various expense categories, providing a detailed variance analysis and highlighting areas of over and underperformance. This report includes tables and analysis to provide a clear understanding of the company's financial position and performance.

Running head: MANAGE FINANCE

Manage Finance

Name of the Student:

Name of the University:

Authors Note:

Manage Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGE FINANCE

Table of Contents

Assessment 1...................................................................................................................................2

Sales and Profit Budget...................................................................................................................2

Answer to Question 1:.....................................................................................................................6

Answer to Question 2:.....................................................................................................................6

Answer to Question 3:.....................................................................................................................7

Answer to Question 4:.....................................................................................................................7

Answer to Question 5:.....................................................................................................................8

Answer to Question 6:.....................................................................................................................8

Answer to Question 7:.....................................................................................................................9

Answer to Question 8:.....................................................................................................................9

Assessment 2.................................................................................................................................10

Budget Variance............................................................................................................................10

Debtors ageing ratio.......................................................................................................................12

Reference.......................................................................................................................................13

Table of Contents

Assessment 1...................................................................................................................................2

Sales and Profit Budget...................................................................................................................2

Answer to Question 1:.....................................................................................................................6

Answer to Question 2:.....................................................................................................................6

Answer to Question 3:.....................................................................................................................7

Answer to Question 4:.....................................................................................................................7

Answer to Question 5:.....................................................................................................................8

Answer to Question 6:.....................................................................................................................8

Answer to Question 7:.....................................................................................................................9

Answer to Question 8:.....................................................................................................................9

Assessment 2.................................................................................................................................10

Budget Variance............................................................................................................................10

Debtors ageing ratio.......................................................................................................................12

Reference.......................................................................................................................................13

2MANAGE FINANCE

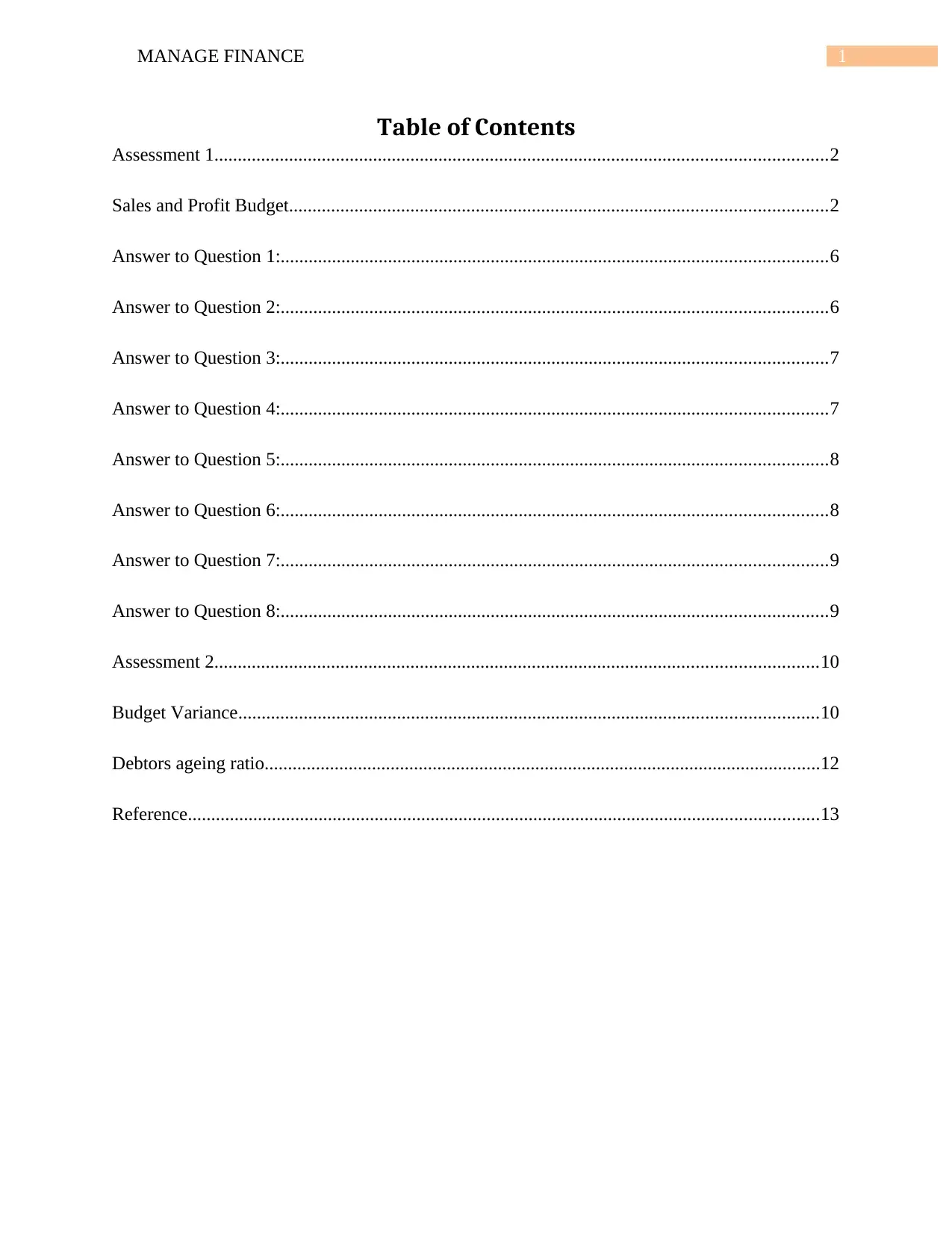

Assessment 1

Sales and Profit Budget

SALES and

PROFIT

BUDGET

2011/12 Qtr 1 Qtr 2 Qtr 3 Qtr 4

Revenue 100% 20% 24% 26% 30%

Sales $16,971,236 $3,394,248 $4,073,097 $4,412,521 $5,091,370

– Cost of Goods

Sold

$9,673,604 $1,934,721 $2,321,665 $2,515,137 $2,902,081

Gross Profit $7,297,632 $1,459,527 $1,751,432 $1,897,384 $2,189,289

Gross Profit % 43% 43% 43% 43% 43%

Expenses

– Accounting Fees $10,000 $2,500 $2,500 $2,500 $2,500

– Interest Expense $84,508 $21,127 $21,127 $21,127 $21,127

– Bank Charges $1,600 $400 $400 $400 $400

– Depreciation $170,000 $42,500 $42,500 $42,500 $42,500

– Insurance $13,390 $3,348 $3,348 $3,348 $3,348

– Store Supplies $3,749 $937 $937 $937 $937

– Advertising $350,000 $200,000 $50,000 $50,000 $50,000

Assessment 1

Sales and Profit Budget

SALES and

PROFIT

BUDGET

2011/12 Qtr 1 Qtr 2 Qtr 3 Qtr 4

Revenue 100% 20% 24% 26% 30%

Sales $16,971,236 $3,394,248 $4,073,097 $4,412,521 $5,091,370

– Cost of Goods

Sold

$9,673,604 $1,934,721 $2,321,665 $2,515,137 $2,902,081

Gross Profit $7,297,632 $1,459,527 $1,751,432 $1,897,384 $2,189,289

Gross Profit % 43% 43% 43% 43% 43%

Expenses

– Accounting Fees $10,000 $2,500 $2,500 $2,500 $2,500

– Interest Expense $84,508 $21,127 $21,127 $21,127 $21,127

– Bank Charges $1,600 $400 $400 $400 $400

– Depreciation $170,000 $42,500 $42,500 $42,500 $42,500

– Insurance $13,390 $3,348 $3,348 $3,348 $3,348

– Store Supplies $3,749 $937 $937 $937 $937

– Advertising $350,000 $200,000 $50,000 $50,000 $50,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGE FINANCE

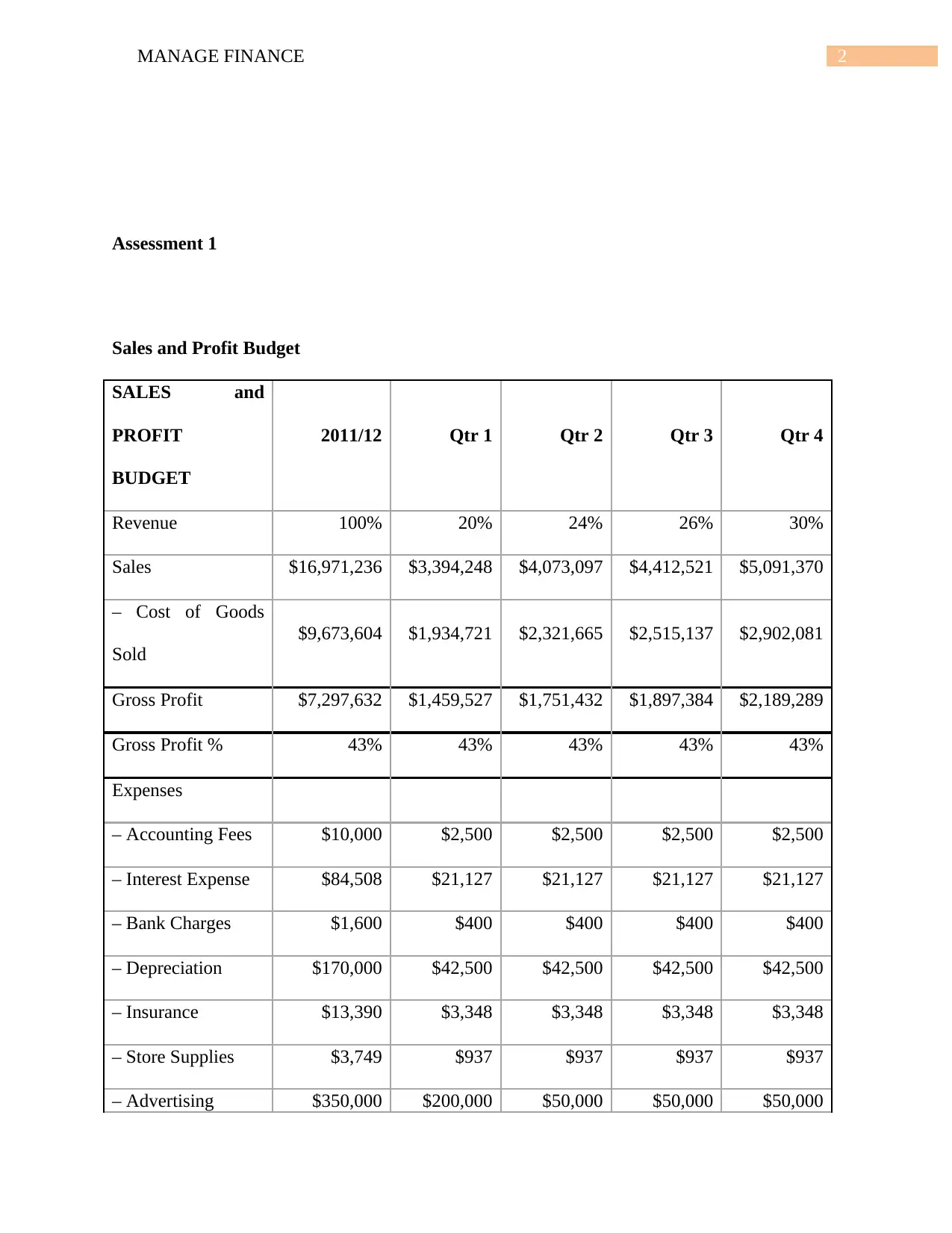

– Cleaning $16,282 $3,256 $3,908 $4,233 $4,885

– Repairs &

Maintenance

$64,272 $16,068 $16,068 $16,068 $16,068

– Rent $2,640,508 $660,127 $660,127 $660,127 $660,127

– Telephone $14,997 $2,999 $3,599 $3,899 $4,499

– Electricity

Expense

$26,780 $5,356 $6,427 $6,963 $8,034

– Luxury Car Tax $12,000 $12,000 $0 $0 $0

– Fringe Benefits

Tax

$28,000 $7,000 $7,000 $7,000 $7,000

– Superannuation $187,020 $37,404 $44,885 $48,625 $56,106

– Wages & Salaries $2,078,000 $415,600 $498,720 $540,280 $623,400

– Payroll Tax $98,705 $19,741 $23,689 $25,663 $29,611

– Workers’

Compensation

$41,560 $8,312 $9,974 $10,806 $12,468

Total Expenses $5,841,371 $1,458,676 $1,395,209 $1,444,476 $1,543,010

Net Profit (Before

Tax)

$1,456,261 $851 $356,222 $452,908 $646,280

Income Tax $436,878 $255 $106,867 $135,872 $193,884

Net Profit $1,019,383 $596 $249,356 $317,036 $452,396

– Cleaning $16,282 $3,256 $3,908 $4,233 $4,885

– Repairs &

Maintenance

$64,272 $16,068 $16,068 $16,068 $16,068

– Rent $2,640,508 $660,127 $660,127 $660,127 $660,127

– Telephone $14,997 $2,999 $3,599 $3,899 $4,499

– Electricity

Expense

$26,780 $5,356 $6,427 $6,963 $8,034

– Luxury Car Tax $12,000 $12,000 $0 $0 $0

– Fringe Benefits

Tax

$28,000 $7,000 $7,000 $7,000 $7,000

– Superannuation $187,020 $37,404 $44,885 $48,625 $56,106

– Wages & Salaries $2,078,000 $415,600 $498,720 $540,280 $623,400

– Payroll Tax $98,705 $19,741 $23,689 $25,663 $29,611

– Workers’

Compensation

$41,560 $8,312 $9,974 $10,806 $12,468

Total Expenses $5,841,371 $1,458,676 $1,395,209 $1,444,476 $1,543,010

Net Profit (Before

Tax)

$1,456,261 $851 $356,222 $452,908 $646,280

Income Tax $436,878 $255 $106,867 $135,872 $193,884

Net Profit $1,019,383 $596 $249,356 $317,036 $452,396

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGE FINANCE

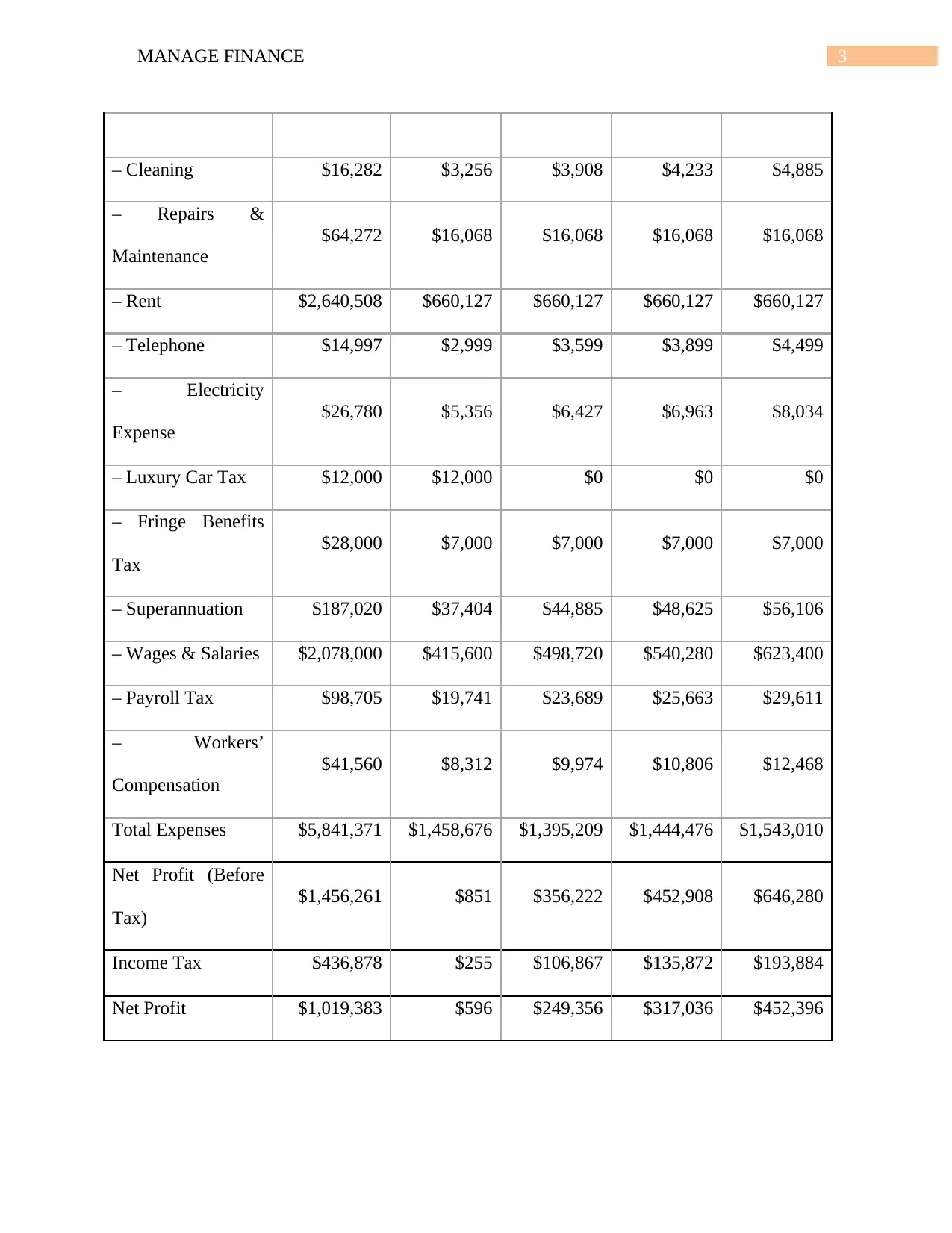

Table 1: Sales and Profit Budget

(Source: Created by Author)

CASH FLOW

ANALYSIS – GST

2015/16 Qtr 1 Qtr 2 Qtr 3 Qtr 4

GST Collected $1,697,124 $339,425 $407,310 $441,252 $509,137

Less GST Paid $1,281,358 $283,046 $306,881 $326,298 $365,133

GST Payable $415,765 $56,378 $100,429 $114,954 $144,004

Table 2: Cash Flow Analysis

(Source: Created by Author)

AGED

DEBTORS

BUDGET

TOTAL Qtr 1 Qtr 2 Qtr 3 Qtr 4

Sales 16971236 3394247.63 4073096.73 4412521.274 5091370.368

% Debtors

Sales

20% 20% 20% 20%

Total Debtors 100% $678,849 $814,619 $882,504 $1,018,274

Current 84.00% $570,233 $684,280 $741,303 $855,350

30 Days 10% $67,885 $81,462 $88,250 $101,827

60 Days 5% $33,942 $40,731 $44,125 $50,914

90 Days 1% $6,788 $8,146 $8,825 $10,183

Table 1: Sales and Profit Budget

(Source: Created by Author)

CASH FLOW

ANALYSIS – GST

2015/16 Qtr 1 Qtr 2 Qtr 3 Qtr 4

GST Collected $1,697,124 $339,425 $407,310 $441,252 $509,137

Less GST Paid $1,281,358 $283,046 $306,881 $326,298 $365,133

GST Payable $415,765 $56,378 $100,429 $114,954 $144,004

Table 2: Cash Flow Analysis

(Source: Created by Author)

AGED

DEBTORS

BUDGET

TOTAL Qtr 1 Qtr 2 Qtr 3 Qtr 4

Sales 16971236 3394247.63 4073096.73 4412521.274 5091370.368

% Debtors

Sales

20% 20% 20% 20%

Total Debtors 100% $678,849 $814,619 $882,504 $1,018,274

Current 84.00% $570,233 $684,280 $741,303 $855,350

30 Days 10% $67,885 $81,462 $88,250 $101,827

60 Days 5% $33,942 $40,731 $44,125 $50,914

90 Days 1% $6,788 $8,146 $8,825 $10,183

5MANAGE FINANCE

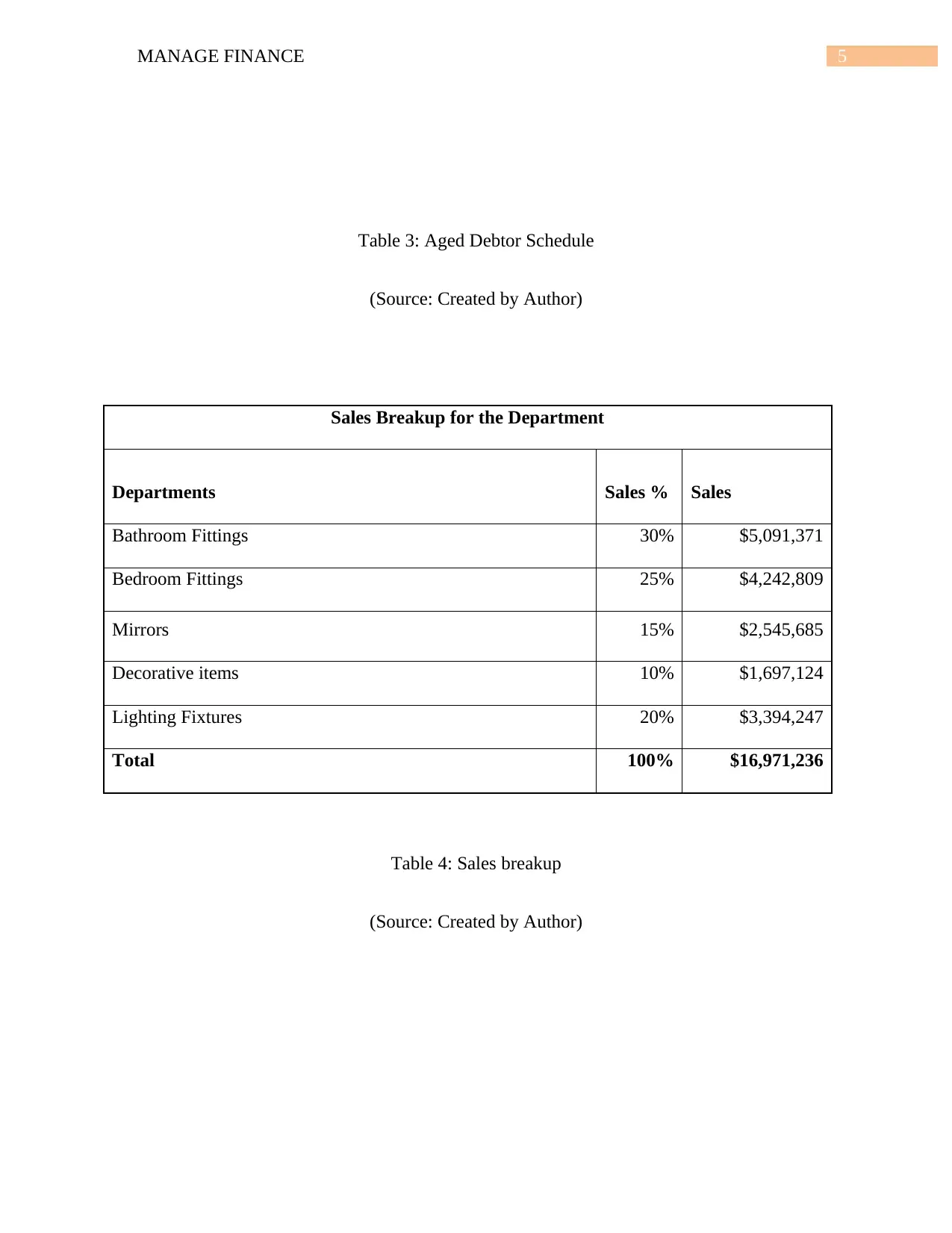

Table 3: Aged Debtor Schedule

(Source: Created by Author)

Sales Breakup for the Department

Departments Sales % Sales

Bathroom Fittings 30% $5,091,371

Bedroom Fittings 25% $4,242,809

Mirrors 15% $2,545,685

Decorative items 10% $1,697,124

Lighting Fixtures 20% $3,394,247

Total 100% $16,971,236

Table 4: Sales breakup

(Source: Created by Author)

Table 3: Aged Debtor Schedule

(Source: Created by Author)

Sales Breakup for the Department

Departments Sales % Sales

Bathroom Fittings 30% $5,091,371

Bedroom Fittings 25% $4,242,809

Mirrors 15% $2,545,685

Decorative items 10% $1,697,124

Lighting Fixtures 20% $3,394,247

Total 100% $16,971,236

Table 4: Sales breakup

(Source: Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGE FINANCE

Answer to Question 1:

According to the Income Tax Assessment Act 1997, a company has to pay taxes for their

taxable income allocated to them by the Act. In the case of Houzit Pty Ltd, the amount of tax

allocated to them is quite big in figures. After preparing the financial budget of the company, it

has to pay the income or capital gain tax to the income tax department. The tax that is allocated

to the company is 30% of their profit. In such scenario, the company also has to imply some

provisions along with the GST Act, as it is mandatory. GST is mandatory to claim input tax

credit for the payment of the suppliers (Cucchiella et al., 2015). In addition to this, another

important and mandatory requirement for tax compliance is to file Income Tax return to identify

income and deduction. Some other reports that the company has to prepare are business activity

statement, GST annual return, PAYG withholding annual reports and tax payments and returns.

Answer to Question 2:

As par the Corporation Act, 2001, companies which are registered under this act, has to

fulfil various requirements stated in that act in order to continue business (DiMuro et al., 2014).

It is mandatory to follow the regulations issued by the government in order to perform the tasks

of the company. Some of those regulations are:-

One resident of Australia should be in the directorial bodies of the company.

Registered office and a permanent postal address are mandatory for the company.

Financial statement of the company should be recorded.

In case of substituting any board member of the company, it should notify the Australian

society about the affair.

Answer to Question 1:

According to the Income Tax Assessment Act 1997, a company has to pay taxes for their

taxable income allocated to them by the Act. In the case of Houzit Pty Ltd, the amount of tax

allocated to them is quite big in figures. After preparing the financial budget of the company, it

has to pay the income or capital gain tax to the income tax department. The tax that is allocated

to the company is 30% of their profit. In such scenario, the company also has to imply some

provisions along with the GST Act, as it is mandatory. GST is mandatory to claim input tax

credit for the payment of the suppliers (Cucchiella et al., 2015). In addition to this, another

important and mandatory requirement for tax compliance is to file Income Tax return to identify

income and deduction. Some other reports that the company has to prepare are business activity

statement, GST annual return, PAYG withholding annual reports and tax payments and returns.

Answer to Question 2:

As par the Corporation Act, 2001, companies which are registered under this act, has to

fulfil various requirements stated in that act in order to continue business (DiMuro et al., 2014).

It is mandatory to follow the regulations issued by the government in order to perform the tasks

of the company. Some of those regulations are:-

One resident of Australia should be in the directorial bodies of the company.

Registered office and a permanent postal address are mandatory for the company.

Financial statement of the company should be recorded.

In case of substituting any board member of the company, it should notify the Australian

society about the affair.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGE FINANCE

Answer to Question 3:

Nowadays, as the electronics technology is progressing in a rapid speed, it is very

common to get an electronic assistance to make a task easier. As for accounting, there are several

good accounting software to help in the task of accounting. However, as far as usability and

affordability is concerned, two most popular accounting software available in Australia are

MYOB and Quick Book. MYOB is likely to be popular for its low price, presenting, and

preparing the required task for financial management (Nesticò & Pipolo, 2015). The security

level of MYOB regarding the encryption of data is also up to dated. However, Quick Book can

provide more analyzed data based on the financial statement of the company regarding the

management tasks. It also works well both in online and offline format. It also makes the

company up to date by providing regular updates regarding the development taxes. Thus, the

software suits the best according to the needs of the company.

Answer to Question 4:

The term matching principle means to keep tracks of all the expenses and revenues at the

same time in order to match them within the specific period of time. It is a major point to be

observed responsibly in order to monitor the financial condition of the business. It is required to

record all the expenses made in order to track the overall condition. The data can be used while

making the financial statement of the company and thus, the upcoming planning for the business

can be decided easily with a chance of less error (Rai & Evans, 2015). Thus, some problems

regarding the funding can easily be solved by implementing this method. It is also helpful to

keep the lucidity of the company.

Account group means a group of accounting items recorded as a whole. This makes

accounting easier to identify certain areas of the business by analysing those groups instead of

Answer to Question 3:

Nowadays, as the electronics technology is progressing in a rapid speed, it is very

common to get an electronic assistance to make a task easier. As for accounting, there are several

good accounting software to help in the task of accounting. However, as far as usability and

affordability is concerned, two most popular accounting software available in Australia are

MYOB and Quick Book. MYOB is likely to be popular for its low price, presenting, and

preparing the required task for financial management (Nesticò & Pipolo, 2015). The security

level of MYOB regarding the encryption of data is also up to dated. However, Quick Book can

provide more analyzed data based on the financial statement of the company regarding the

management tasks. It also works well both in online and offline format. It also makes the

company up to date by providing regular updates regarding the development taxes. Thus, the

software suits the best according to the needs of the company.

Answer to Question 4:

The term matching principle means to keep tracks of all the expenses and revenues at the

same time in order to match them within the specific period of time. It is a major point to be

observed responsibly in order to monitor the financial condition of the business. It is required to

record all the expenses made in order to track the overall condition. The data can be used while

making the financial statement of the company and thus, the upcoming planning for the business

can be decided easily with a chance of less error (Rai & Evans, 2015). Thus, some problems

regarding the funding can easily be solved by implementing this method. It is also helpful to

keep the lucidity of the company.

Account group means a group of accounting items recorded as a whole. This makes

accounting easier to identify certain areas of the business by analysing those groups instead of

8MANAGE FINANCE

going through the entire financial statement. This is more time saving and effective in order to

make better analysis of a business.

Time of preparing a budget is very essential as it determines the effectiveness of the

budget. Budget can be made in two time periods, one is short term budget and the other is short

term budget. While long-term budget is made for stating the financial changes the company has

made, short-term budget is used for framing the long-term budget and analysis the error and

mistakes so that it can be compensated in the near future (Shouman et al., 2016). The short-term

budget can be the basis of the long-term budget as it is more reliable than the long term budget.

Answer to Question 5:

Probity is a term to describe the act of doing a job with sincerity, honesty and

willingness. It is mandatory to maintain probity while preparing the financial statement and

budget. To maintain the lucidity and truthfulness of the budget, it is highly recommended to

maintain the same amount of probity from start to end. These decrease the chances of any error

and mistakes while preparing the budget (Słyś & Kordana, 2014). To maintain the probity while

preparing the budget, proper analysis, honest and thoughtful examination should be done.

Answer to Question 6:

Regarding the past affairs in the statement of Houzit Pty Ltd, it seems necessary to make

some improvements in certain sector of the company in order to generate resources in the next

financial cycle. There can be three possible steps to make the business more successful. Which

are:-

Reducing the rate of gross profit by 0.9% will help the company to keep up with the

steady growth in sales.

going through the entire financial statement. This is more time saving and effective in order to

make better analysis of a business.

Time of preparing a budget is very essential as it determines the effectiveness of the

budget. Budget can be made in two time periods, one is short term budget and the other is short

term budget. While long-term budget is made for stating the financial changes the company has

made, short-term budget is used for framing the long-term budget and analysis the error and

mistakes so that it can be compensated in the near future (Shouman et al., 2016). The short-term

budget can be the basis of the long-term budget as it is more reliable than the long term budget.

Answer to Question 5:

Probity is a term to describe the act of doing a job with sincerity, honesty and

willingness. It is mandatory to maintain probity while preparing the financial statement and

budget. To maintain the lucidity and truthfulness of the budget, it is highly recommended to

maintain the same amount of probity from start to end. These decrease the chances of any error

and mistakes while preparing the budget (Słyś & Kordana, 2014). To maintain the probity while

preparing the budget, proper analysis, honest and thoughtful examination should be done.

Answer to Question 6:

Regarding the past affairs in the statement of Houzit Pty Ltd, it seems necessary to make

some improvements in certain sector of the company in order to generate resources in the next

financial cycle. There can be three possible steps to make the business more successful. Which

are:-

Reducing the rate of gross profit by 0.9% will help the company to keep up with the

steady growth in sales.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGE FINANCE

To generate the demand in market more effectively, the company may increase the

advertisement budget.

Some extension to the salaries and wages budget will surely motivate the employees of

the company to earn more commissions in sales, which will surely help to reach the

company its sales target.

Answer to Question 7:

Apart from the items, which has been shown in the budget of Houzit Pty Ltd, there are,

some other items which be included and proved beneficial to the company. These are:-

The loans should be paid in time to get rid of the expenditure of paying additional

interest.

The discount given by the company can be reduced to a certain percentage in order to rise

the net profit.

The payroll system can be improved in order to keep exact account of the salary and

wages budget. This can reduce additional costs regarding the expenses.

Answer to Question 8:

Risk management is a very important task to do for a management team of the company in order

to secure the purpose of it. Thus, some additional modification is required to manage the risks in

a more efficient manner (Vogel, 2014). As for Houzit Pty Ltd, following suggestions can be

granted in order to manage the risks from various aspects.

The customers’ base should be secured in a more dignified manner in order to measure

the demands in the market more effectively.

To generate the demand in market more effectively, the company may increase the

advertisement budget.

Some extension to the salaries and wages budget will surely motivate the employees of

the company to earn more commissions in sales, which will surely help to reach the

company its sales target.

Answer to Question 7:

Apart from the items, which has been shown in the budget of Houzit Pty Ltd, there are,

some other items which be included and proved beneficial to the company. These are:-

The loans should be paid in time to get rid of the expenditure of paying additional

interest.

The discount given by the company can be reduced to a certain percentage in order to rise

the net profit.

The payroll system can be improved in order to keep exact account of the salary and

wages budget. This can reduce additional costs regarding the expenses.

Answer to Question 8:

Risk management is a very important task to do for a management team of the company in order

to secure the purpose of it. Thus, some additional modification is required to manage the risks in

a more efficient manner (Vogel, 2014). As for Houzit Pty Ltd, following suggestions can be

granted in order to manage the risks from various aspects.

The customers’ base should be secured in a more dignified manner in order to measure

the demands in the market more effectively.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGE FINANCE

The discounts given should be reflected in the invoices given to its clients estimate it

properly in the later budget.

The cash balance should be verified after every specific period of time to get rid of the

treachery.

It should be ensured that the workers are being paid after completing the work given to

them. It is the duty of the service manager to keep monitoring about the workers and the

work done by them.

The assets should be identified with the unique code to keep track to them.

Debtors balance should be settled within a specific period of time.

It must be accounted about the newly employed workers and the quitters in order to

maintain the clarity in the payroll system. Sometimes, the supervisors are responsible for

making error in the payroll for their own benefits (Vittorini & Cipollone, 2016).

An individual person should do the reconciliation of cash balance so that the lucidity in

accounting can be maintained well.

Assessment 2

Budget Variance

Houzit Pty Ltd

Variance to Budget

1 Quarter ended September-2015

Actual Results Budget-Qx Actual-Qx $ %

Variance F or U

Variance

Sales $3,394,247.63 $3,371,200.00 -$23,047.63 -1% U

The discounts given should be reflected in the invoices given to its clients estimate it

properly in the later budget.

The cash balance should be verified after every specific period of time to get rid of the

treachery.

It should be ensured that the workers are being paid after completing the work given to

them. It is the duty of the service manager to keep monitoring about the workers and the

work done by them.

The assets should be identified with the unique code to keep track to them.

Debtors balance should be settled within a specific period of time.

It must be accounted about the newly employed workers and the quitters in order to

maintain the clarity in the payroll system. Sometimes, the supervisors are responsible for

making error in the payroll for their own benefits (Vittorini & Cipollone, 2016).

An individual person should do the reconciliation of cash balance so that the lucidity in

accounting can be maintained well.

Assessment 2

Budget Variance

Houzit Pty Ltd

Variance to Budget

1 Quarter ended September-2015

Actual Results Budget-Qx Actual-Qx $ %

Variance F or U

Variance

Sales $3,394,247.63 $3,371,200.00 -$23,047.63 -1% U

11MANAGE FINANCE

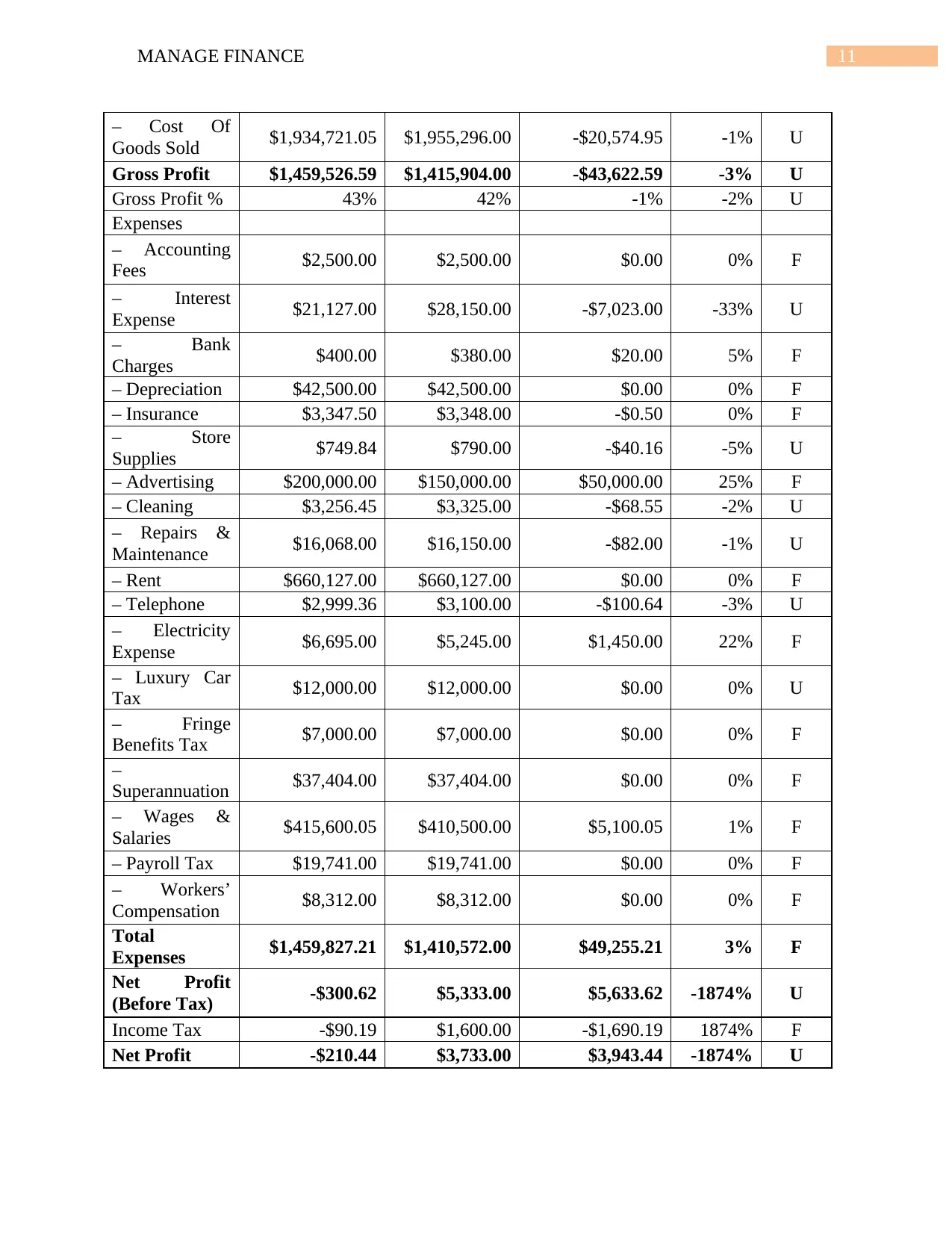

– Cost Of

Goods Sold $1,934,721.05 $1,955,296.00 -$20,574.95 -1% U

Gross Profit $1,459,526.59 $1,415,904.00 -$43,622.59 -3% U

Gross Profit % 43% 42% -1% -2% U

Expenses

– Accounting

Fees $2,500.00 $2,500.00 $0.00 0% F

– Interest

Expense $21,127.00 $28,150.00 -$7,023.00 -33% U

– Bank

Charges $400.00 $380.00 $20.00 5% F

– Depreciation $42,500.00 $42,500.00 $0.00 0% F

– Insurance $3,347.50 $3,348.00 -$0.50 0% F

– Store

Supplies $749.84 $790.00 -$40.16 -5% U

– Advertising $200,000.00 $150,000.00 $50,000.00 25% F

– Cleaning $3,256.45 $3,325.00 -$68.55 -2% U

– Repairs &

Maintenance $16,068.00 $16,150.00 -$82.00 -1% U

– Rent $660,127.00 $660,127.00 $0.00 0% F

– Telephone $2,999.36 $3,100.00 -$100.64 -3% U

– Electricity

Expense $6,695.00 $5,245.00 $1,450.00 22% F

– Luxury Car

Tax $12,000.00 $12,000.00 $0.00 0% U

– Fringe

Benefits Tax $7,000.00 $7,000.00 $0.00 0% F

–

Superannuation $37,404.00 $37,404.00 $0.00 0% F

– Wages &

Salaries $415,600.05 $410,500.00 $5,100.05 1% F

– Payroll Tax $19,741.00 $19,741.00 $0.00 0% F

– Workers’

Compensation $8,312.00 $8,312.00 $0.00 0% F

Total

Expenses $1,459,827.21 $1,410,572.00 $49,255.21 3% F

Net Profit

(Before Tax) -$300.62 $5,333.00 $5,633.62 -1874% U

Income Tax -$90.19 $1,600.00 -$1,690.19 1874% F

Net Profit -$210.44 $3,733.00 $3,943.44 -1874% U

– Cost Of

Goods Sold $1,934,721.05 $1,955,296.00 -$20,574.95 -1% U

Gross Profit $1,459,526.59 $1,415,904.00 -$43,622.59 -3% U

Gross Profit % 43% 42% -1% -2% U

Expenses

– Accounting

Fees $2,500.00 $2,500.00 $0.00 0% F

– Interest

Expense $21,127.00 $28,150.00 -$7,023.00 -33% U

– Bank

Charges $400.00 $380.00 $20.00 5% F

– Depreciation $42,500.00 $42,500.00 $0.00 0% F

– Insurance $3,347.50 $3,348.00 -$0.50 0% F

– Store

Supplies $749.84 $790.00 -$40.16 -5% U

– Advertising $200,000.00 $150,000.00 $50,000.00 25% F

– Cleaning $3,256.45 $3,325.00 -$68.55 -2% U

– Repairs &

Maintenance $16,068.00 $16,150.00 -$82.00 -1% U

– Rent $660,127.00 $660,127.00 $0.00 0% F

– Telephone $2,999.36 $3,100.00 -$100.64 -3% U

– Electricity

Expense $6,695.00 $5,245.00 $1,450.00 22% F

– Luxury Car

Tax $12,000.00 $12,000.00 $0.00 0% U

– Fringe

Benefits Tax $7,000.00 $7,000.00 $0.00 0% F

–

Superannuation $37,404.00 $37,404.00 $0.00 0% F

– Wages &

Salaries $415,600.05 $410,500.00 $5,100.05 1% F

– Payroll Tax $19,741.00 $19,741.00 $0.00 0% F

– Workers’

Compensation $8,312.00 $8,312.00 $0.00 0% F

Total

Expenses $1,459,827.21 $1,410,572.00 $49,255.21 3% F

Net Profit

(Before Tax) -$300.62 $5,333.00 $5,633.62 -1874% U

Income Tax -$90.19 $1,600.00 -$1,690.19 1874% F

Net Profit -$210.44 $3,733.00 $3,943.44 -1874% U

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.