FIN2138M: Analysis of HSBC Bank's Financial Performance Report

VerifiedAdded on 2022/09/21

|13

|2363

|20

Report

AI Summary

This report provides a comprehensive analysis of HSBC's financial performance, focusing on its capital and liquidity management. It examines key financial ratios such as Net Interest Margin, Return on Assets, Capital Adequacy Ratio, Liquidity Ratio, Return on Equity, and CET1 Ratio, comparing HSBC's performance with competitors like Royal Bank of Scotland and Barclays Bank. The report also explores the importance of capital and liquidity management in modern banking, particularly in light of the 2008 Global Financial Crisis, and discusses changes in HSBC's practices, including Basel III and CRD IV. Furthermore, it identifies current challenges in the banking sector, such as the impact of digitalization, and offers recommendations for how these can be addressed through diversification, improved digital services, enhanced security measures, and organizational restructuring. The report concludes by emphasizing the critical role of liquidity and capital management in ensuring the stability and long-term success of banking institutions.

Running head: FIN138M-1920

FIN2138M - 1920

Name of the Student

Name of the University

FIN2138M - 1920

Name of the Student

Name of the University

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FIN2138M-1920

Executive Summary

This report contains an analysis of the business model of HSBC and its financial performance in

comparison to Royal Bank of Scotland and Barclays Bank in recent years. The focus is also laid

on the importance of liquidity and capital management of the modern day banks. The changes in

the liquidity and capital management procedures of HSBC after the 2008 Global Financial Crisis

is also discussed. The report concludes by identifying the challenges occurring in the modern day

banks and the manner in which they can be overcome by the businesses.

FIN2138M-1920

Executive Summary

This report contains an analysis of the business model of HSBC and its financial performance in

comparison to Royal Bank of Scotland and Barclays Bank in recent years. The focus is also laid

on the importance of liquidity and capital management of the modern day banks. The changes in

the liquidity and capital management procedures of HSBC after the 2008 Global Financial Crisis

is also discussed. The report concludes by identifying the challenges occurring in the modern day

banks and the manner in which they can be overcome by the businesses.

2

FIN2138M-1920

Author Note

FIN2138M-1920

Author Note

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FIN2138M-1920

Table of Contents

Introduction..................................................................................................................................2

Evaluation of Financial Performance...........................................................................................2

Importance of capital and liquidity management.........................................................................6

Conclusion and Recommendations..............................................................................................8

Bibliography.................................................................................................................................9

FIN2138M-1920

Table of Contents

Introduction..................................................................................................................................2

Evaluation of Financial Performance...........................................................................................2

Importance of capital and liquidity management.........................................................................6

Conclusion and Recommendations..............................................................................................8

Bibliography.................................................................................................................................9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FIN2138M-1920

Introduction

The Hong Kong and Shanghai Business Corporation (HSBC) is one of the largest

multinational investment banking and financial services holding company in the world. As of

2018, it was one of the largest banks in the world with its total assets valued around $2.5 trillion.

The company first opened in 1865 and was incorporated in the year 1866. The business model of

HSBC is based on an international network which connects faster growing and newly developing

markets with each other. The banks tend to take deposits from customers and use these funds in

conducting business activities like providing loans, mortgages, overdrafts and loan facilities to

entities. Apart from these, other services provided by the business include asset management,

broking, financial advisory, corporate finance and alternative investments. The key aspects of the

revenue generated by the entity include the net interest income, net fee income and the net

trading income of the business. The key revenue generators of the business of the entity include

the interest charged on loans, discount earned from bills discounted, commission earned by

providing guarantee and other payments received from the customers for providing the services.

The costs Some of the key costs incurred as a part of the business of the entity include the cost of

funds, fund distribution and infrastructure costs, staffing, marketing and Risk Management and

Compliance Costs.

Evaluation of Financial Performance

In order to evaluate the financial performance of the entity, a ratio analysis of the bank

was conducted. The main aspects which were analysed with the help of these ratios are the

liquidity, profitability and the capital adequacy of the business. In order to obtain a better

understanding of the adequacy of the performance of the bank, analysis was also conducted in

FIN2138M-1920

Introduction

The Hong Kong and Shanghai Business Corporation (HSBC) is one of the largest

multinational investment banking and financial services holding company in the world. As of

2018, it was one of the largest banks in the world with its total assets valued around $2.5 trillion.

The company first opened in 1865 and was incorporated in the year 1866. The business model of

HSBC is based on an international network which connects faster growing and newly developing

markets with each other. The banks tend to take deposits from customers and use these funds in

conducting business activities like providing loans, mortgages, overdrafts and loan facilities to

entities. Apart from these, other services provided by the business include asset management,

broking, financial advisory, corporate finance and alternative investments. The key aspects of the

revenue generated by the entity include the net interest income, net fee income and the net

trading income of the business. The key revenue generators of the business of the entity include

the interest charged on loans, discount earned from bills discounted, commission earned by

providing guarantee and other payments received from the customers for providing the services.

The costs Some of the key costs incurred as a part of the business of the entity include the cost of

funds, fund distribution and infrastructure costs, staffing, marketing and Risk Management and

Compliance Costs.

Evaluation of Financial Performance

In order to evaluate the financial performance of the entity, a ratio analysis of the bank

was conducted. The main aspects which were analysed with the help of these ratios are the

liquidity, profitability and the capital adequacy of the business. In order to obtain a better

understanding of the adequacy of the performance of the bank, analysis was also conducted in

5

FIN2138M-1920

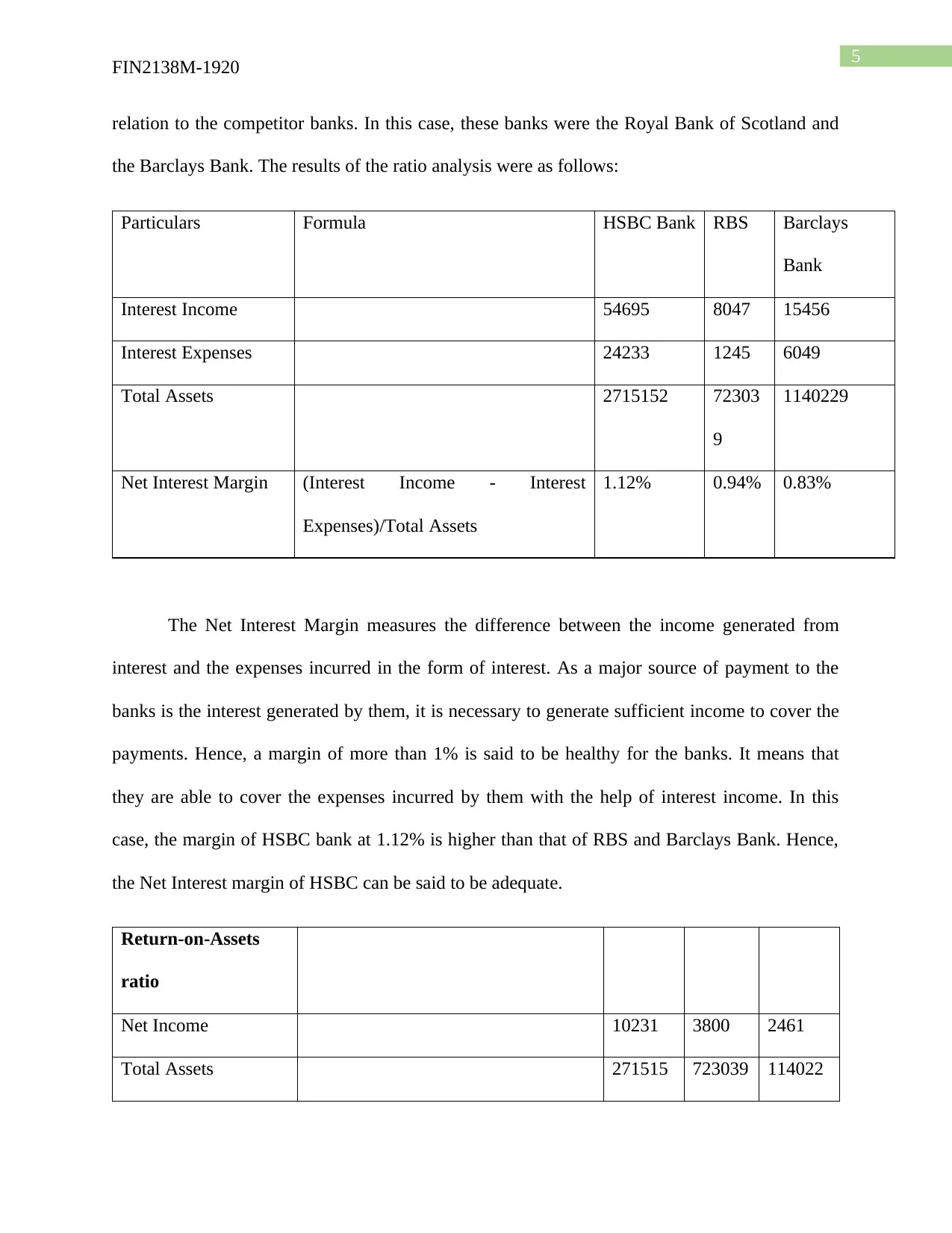

relation to the competitor banks. In this case, these banks were the Royal Bank of Scotland and

the Barclays Bank. The results of the ratio analysis were as follows:

Particulars Formula HSBC Bank RBS Barclays

Bank

Interest Income 54695 8047 15456

Interest Expenses 24233 1245 6049

Total Assets 2715152 72303

9

1140229

Net Interest Margin (Interest Income - Interest

Expenses)/Total Assets

1.12% 0.94% 0.83%

The Net Interest Margin measures the difference between the income generated from

interest and the expenses incurred in the form of interest. As a major source of payment to the

banks is the interest generated by them, it is necessary to generate sufficient income to cover the

payments. Hence, a margin of more than 1% is said to be healthy for the banks. It means that

they are able to cover the expenses incurred by them with the help of interest income. In this

case, the margin of HSBC bank at 1.12% is higher than that of RBS and Barclays Bank. Hence,

the Net Interest margin of HSBC can be said to be adequate.

Return-on-Assets

ratio

Net Income 10231 3800 2461

Total Assets 271515 723039 114022

FIN2138M-1920

relation to the competitor banks. In this case, these banks were the Royal Bank of Scotland and

the Barclays Bank. The results of the ratio analysis were as follows:

Particulars Formula HSBC Bank RBS Barclays

Bank

Interest Income 54695 8047 15456

Interest Expenses 24233 1245 6049

Total Assets 2715152 72303

9

1140229

Net Interest Margin (Interest Income - Interest

Expenses)/Total Assets

1.12% 0.94% 0.83%

The Net Interest Margin measures the difference between the income generated from

interest and the expenses incurred in the form of interest. As a major source of payment to the

banks is the interest generated by them, it is necessary to generate sufficient income to cover the

payments. Hence, a margin of more than 1% is said to be healthy for the banks. It means that

they are able to cover the expenses incurred by them with the help of interest income. In this

case, the margin of HSBC bank at 1.12% is higher than that of RBS and Barclays Bank. Hence,

the Net Interest margin of HSBC can be said to be adequate.

Return-on-Assets

ratio

Net Income 10231 3800 2461

Total Assets 271515 723039 114022

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FIN2138M-1920

2 9

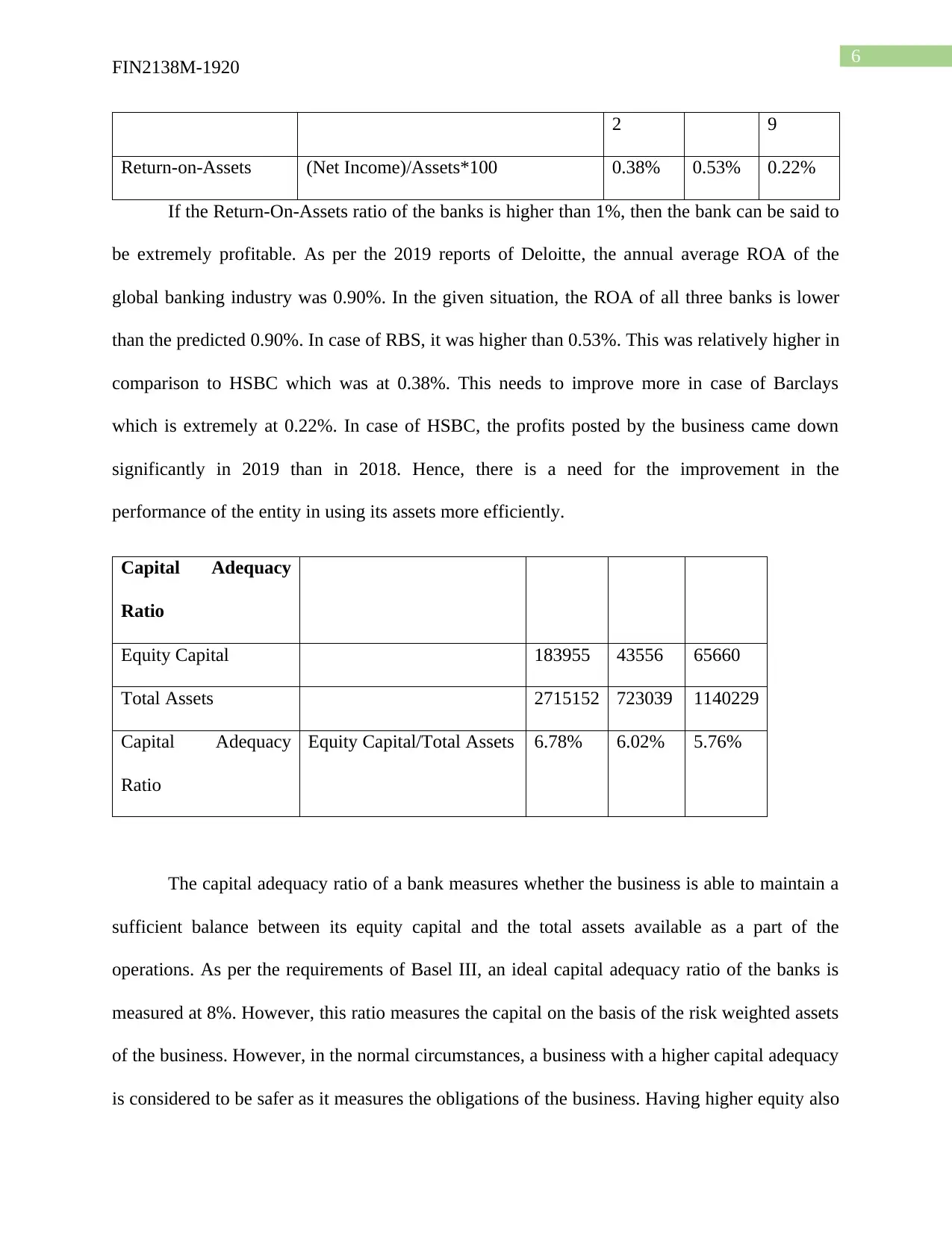

Return-on-Assets (Net Income)/Assets*100 0.38% 0.53% 0.22%

If the Return-On-Assets ratio of the banks is higher than 1%, then the bank can be said to

be extremely profitable. As per the 2019 reports of Deloitte, the annual average ROA of the

global banking industry was 0.90%. In the given situation, the ROA of all three banks is lower

than the predicted 0.90%. In case of RBS, it was higher than 0.53%. This was relatively higher in

comparison to HSBC which was at 0.38%. This needs to improve more in case of Barclays

which is extremely at 0.22%. In case of HSBC, the profits posted by the business came down

significantly in 2019 than in 2018. Hence, there is a need for the improvement in the

performance of the entity in using its assets more efficiently.

Capital Adequacy

Ratio

Equity Capital 183955 43556 65660

Total Assets 2715152 723039 1140229

Capital Adequacy

Ratio

Equity Capital/Total Assets 6.78% 6.02% 5.76%

The capital adequacy ratio of a bank measures whether the business is able to maintain a

sufficient balance between its equity capital and the total assets available as a part of the

operations. As per the requirements of Basel III, an ideal capital adequacy ratio of the banks is

measured at 8%. However, this ratio measures the capital on the basis of the risk weighted assets

of the business. However, in the normal circumstances, a business with a higher capital adequacy

is considered to be safer as it measures the obligations of the business. Having higher equity also

FIN2138M-1920

2 9

Return-on-Assets (Net Income)/Assets*100 0.38% 0.53% 0.22%

If the Return-On-Assets ratio of the banks is higher than 1%, then the bank can be said to

be extremely profitable. As per the 2019 reports of Deloitte, the annual average ROA of the

global banking industry was 0.90%. In the given situation, the ROA of all three banks is lower

than the predicted 0.90%. In case of RBS, it was higher than 0.53%. This was relatively higher in

comparison to HSBC which was at 0.38%. This needs to improve more in case of Barclays

which is extremely at 0.22%. In case of HSBC, the profits posted by the business came down

significantly in 2019 than in 2018. Hence, there is a need for the improvement in the

performance of the entity in using its assets more efficiently.

Capital Adequacy

Ratio

Equity Capital 183955 43556 65660

Total Assets 2715152 723039 1140229

Capital Adequacy

Ratio

Equity Capital/Total Assets 6.78% 6.02% 5.76%

The capital adequacy ratio of a bank measures whether the business is able to maintain a

sufficient balance between its equity capital and the total assets available as a part of the

operations. As per the requirements of Basel III, an ideal capital adequacy ratio of the banks is

measured at 8%. However, this ratio measures the capital on the basis of the risk weighted assets

of the business. However, in the normal circumstances, a business with a higher capital adequacy

is considered to be safer as it measures the obligations of the business. Having higher equity also

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FIN2138M-1920

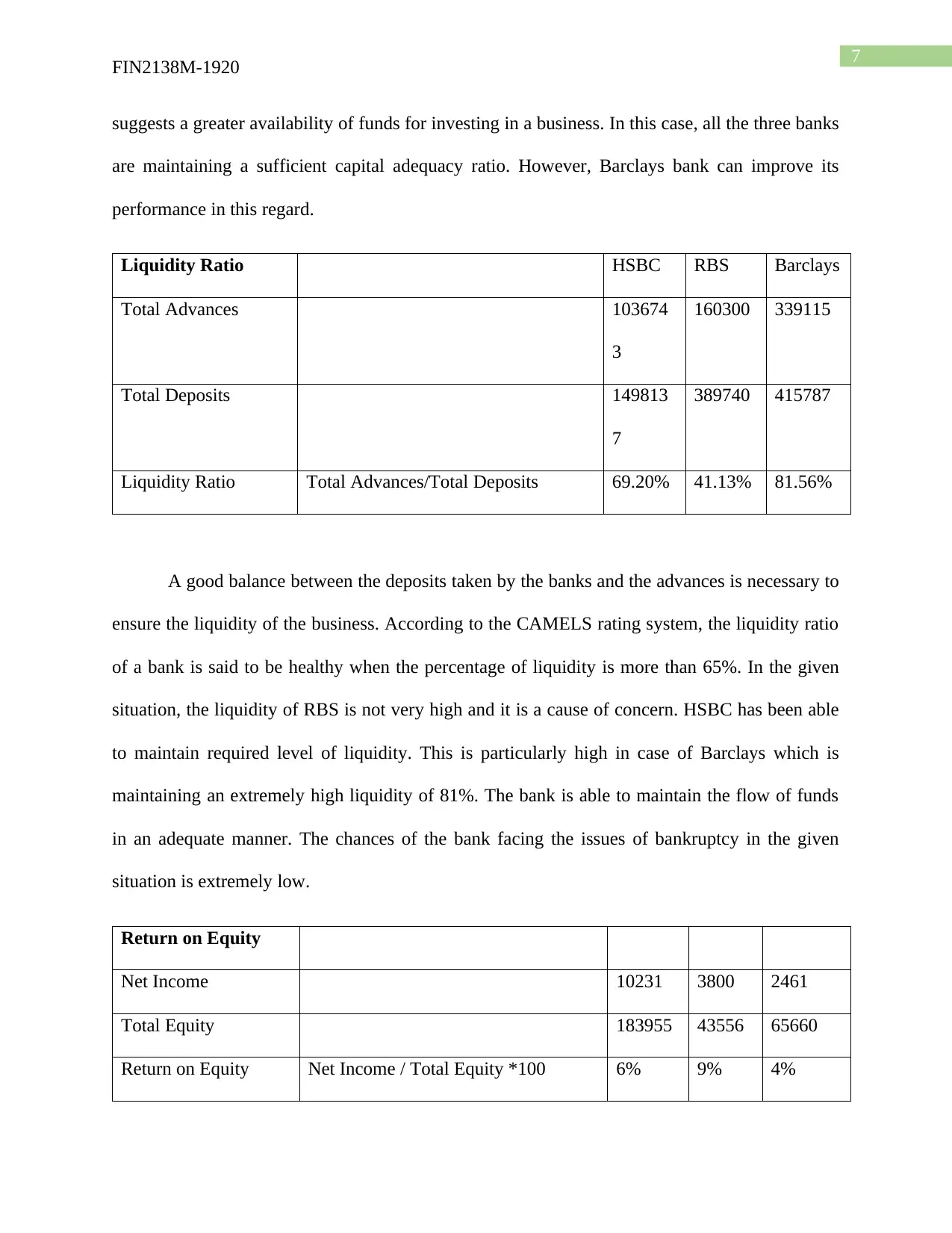

suggests a greater availability of funds for investing in a business. In this case, all the three banks

are maintaining a sufficient capital adequacy ratio. However, Barclays bank can improve its

performance in this regard.

Liquidity Ratio HSBC RBS Barclays

Total Advances 103674

3

160300 339115

Total Deposits 149813

7

389740 415787

Liquidity Ratio Total Advances/Total Deposits 69.20% 41.13% 81.56%

A good balance between the deposits taken by the banks and the advances is necessary to

ensure the liquidity of the business. According to the CAMELS rating system, the liquidity ratio

of a bank is said to be healthy when the percentage of liquidity is more than 65%. In the given

situation, the liquidity of RBS is not very high and it is a cause of concern. HSBC has been able

to maintain required level of liquidity. This is particularly high in case of Barclays which is

maintaining an extremely high liquidity of 81%. The bank is able to maintain the flow of funds

in an adequate manner. The chances of the bank facing the issues of bankruptcy in the given

situation is extremely low.

Return on Equity

Net Income 10231 3800 2461

Total Equity 183955 43556 65660

Return on Equity Net Income / Total Equity *100 6% 9% 4%

FIN2138M-1920

suggests a greater availability of funds for investing in a business. In this case, all the three banks

are maintaining a sufficient capital adequacy ratio. However, Barclays bank can improve its

performance in this regard.

Liquidity Ratio HSBC RBS Barclays

Total Advances 103674

3

160300 339115

Total Deposits 149813

7

389740 415787

Liquidity Ratio Total Advances/Total Deposits 69.20% 41.13% 81.56%

A good balance between the deposits taken by the banks and the advances is necessary to

ensure the liquidity of the business. According to the CAMELS rating system, the liquidity ratio

of a bank is said to be healthy when the percentage of liquidity is more than 65%. In the given

situation, the liquidity of RBS is not very high and it is a cause of concern. HSBC has been able

to maintain required level of liquidity. This is particularly high in case of Barclays which is

maintaining an extremely high liquidity of 81%. The bank is able to maintain the flow of funds

in an adequate manner. The chances of the bank facing the issues of bankruptcy in the given

situation is extremely low.

Return on Equity

Net Income 10231 3800 2461

Total Equity 183955 43556 65660

Return on Equity Net Income / Total Equity *100 6% 9% 4%

8

FIN2138M-1920

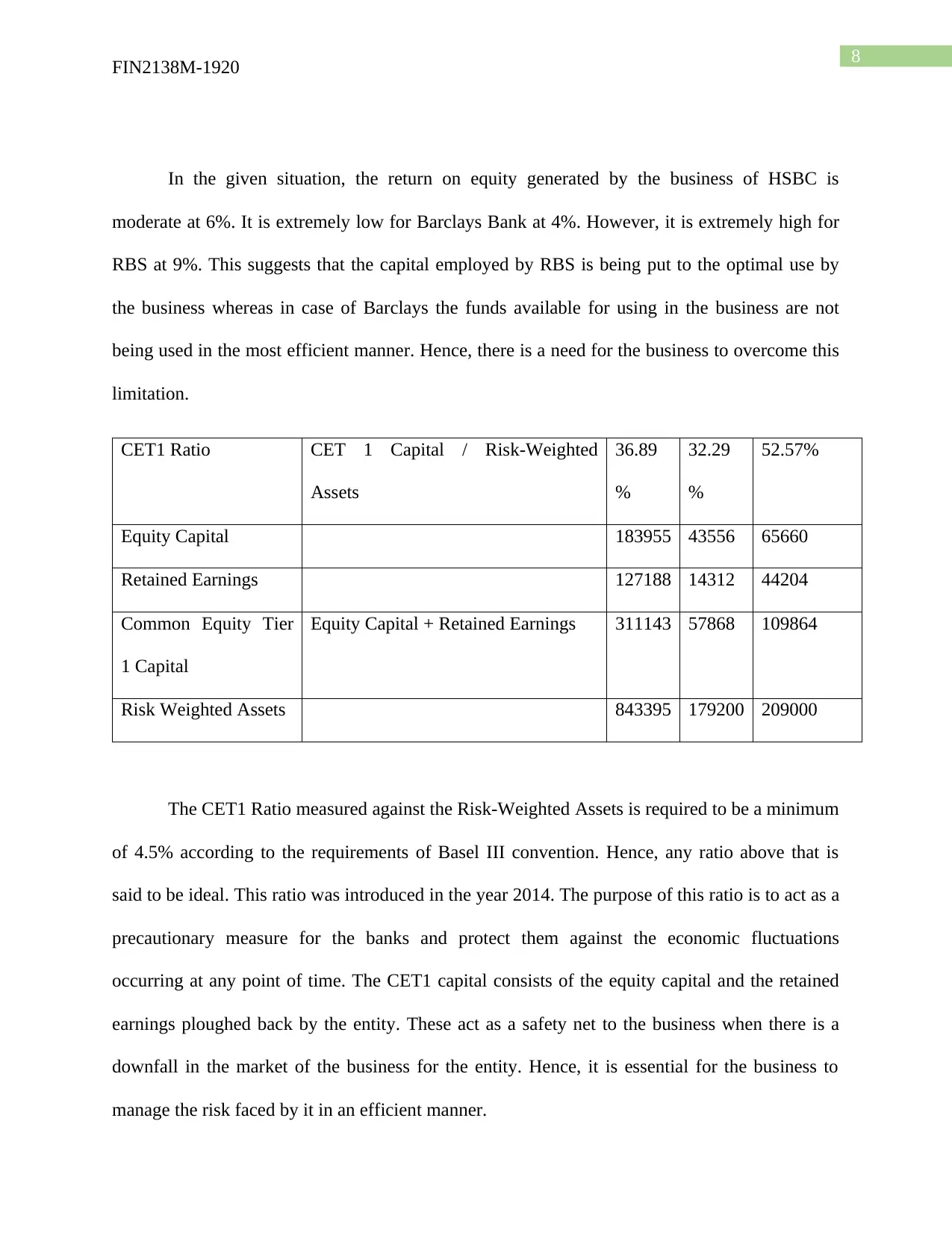

In the given situation, the return on equity generated by the business of HSBC is

moderate at 6%. It is extremely low for Barclays Bank at 4%. However, it is extremely high for

RBS at 9%. This suggests that the capital employed by RBS is being put to the optimal use by

the business whereas in case of Barclays the funds available for using in the business are not

being used in the most efficient manner. Hence, there is a need for the business to overcome this

limitation.

CET1 Ratio CET 1 Capital / Risk-Weighted

Assets

36.89

%

32.29

%

52.57%

Equity Capital 183955 43556 65660

Retained Earnings 127188 14312 44204

Common Equity Tier

1 Capital

Equity Capital + Retained Earnings 311143 57868 109864

Risk Weighted Assets 843395 179200 209000

The CET1 Ratio measured against the Risk-Weighted Assets is required to be a minimum

of 4.5% according to the requirements of Basel III convention. Hence, any ratio above that is

said to be ideal. This ratio was introduced in the year 2014. The purpose of this ratio is to act as a

precautionary measure for the banks and protect them against the economic fluctuations

occurring at any point of time. The CET1 capital consists of the equity capital and the retained

earnings ploughed back by the entity. These act as a safety net to the business when there is a

downfall in the market of the business for the entity. Hence, it is essential for the business to

manage the risk faced by it in an efficient manner.

FIN2138M-1920

In the given situation, the return on equity generated by the business of HSBC is

moderate at 6%. It is extremely low for Barclays Bank at 4%. However, it is extremely high for

RBS at 9%. This suggests that the capital employed by RBS is being put to the optimal use by

the business whereas in case of Barclays the funds available for using in the business are not

being used in the most efficient manner. Hence, there is a need for the business to overcome this

limitation.

CET1 Ratio CET 1 Capital / Risk-Weighted

Assets

36.89

%

32.29

%

52.57%

Equity Capital 183955 43556 65660

Retained Earnings 127188 14312 44204

Common Equity Tier

1 Capital

Equity Capital + Retained Earnings 311143 57868 109864

Risk Weighted Assets 843395 179200 209000

The CET1 Ratio measured against the Risk-Weighted Assets is required to be a minimum

of 4.5% according to the requirements of Basel III convention. Hence, any ratio above that is

said to be ideal. This ratio was introduced in the year 2014. The purpose of this ratio is to act as a

precautionary measure for the banks and protect them against the economic fluctuations

occurring at any point of time. The CET1 capital consists of the equity capital and the retained

earnings ploughed back by the entity. These act as a safety net to the business when there is a

downfall in the market of the business for the entity. Hence, it is essential for the business to

manage the risk faced by it in an efficient manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FIN2138M-1920

Importance of capital and liquidity management

In case of a bank, there is a tangible difference between the liquidity and the capital

available to the business. While liquidity measures the cash and other short term assets available

with a bank to quickly pay off the short term bills, capital measures the resources that a bank has

to absorb the losses incurred by it. Researchers suggest that the quick ratio and capital adequacy

ratio have a positive impact on the performance of a bank. This is based on their positive impact

on the determinants of profitability such as the earnings per share and return on assets. Cash ratio

and current ratio have been found to have a negative impact on the return on assets. Interest

coverage ratio is positively associated with the return on equity whereas earnings per share also

has a negative impact on the return on equity. Hence, on an overall basis, it can be suggested that

the liquidity management by an entity plays an important role in positively impacting the

profitability of a bank. These findings suggest that banks should look to maintain sufficient

amount of liquidity. This not only meets the short term requirements of the business but also

helps in exploiting the short term investment opportunities available to the banks. Lack of

adequate liquidity management makes it difficult for the banks to fulfil their short term

obligations and lose out on the profit making ventures.

The major changes which have occurred in the Banking Industry after the 2008 Global

Financial Crisis are the increase in the reforms and their implementation. Many governments

across the world pushed for increased transparency to provide more transparency and reduce the

risk in the financial systems. Some of the steps which are followed by HSBC in the liquidity

management and the capital management processes are the Basel III reforms and the CRD IV.

The BASEL III is designed to increase the resilience of the bank and reduce the impact of the

financial crisis. These include the management of a minimum amount of Tier I capital against the

FIN2138M-1920

Importance of capital and liquidity management

In case of a bank, there is a tangible difference between the liquidity and the capital

available to the business. While liquidity measures the cash and other short term assets available

with a bank to quickly pay off the short term bills, capital measures the resources that a bank has

to absorb the losses incurred by it. Researchers suggest that the quick ratio and capital adequacy

ratio have a positive impact on the performance of a bank. This is based on their positive impact

on the determinants of profitability such as the earnings per share and return on assets. Cash ratio

and current ratio have been found to have a negative impact on the return on assets. Interest

coverage ratio is positively associated with the return on equity whereas earnings per share also

has a negative impact on the return on equity. Hence, on an overall basis, it can be suggested that

the liquidity management by an entity plays an important role in positively impacting the

profitability of a bank. These findings suggest that banks should look to maintain sufficient

amount of liquidity. This not only meets the short term requirements of the business but also

helps in exploiting the short term investment opportunities available to the banks. Lack of

adequate liquidity management makes it difficult for the banks to fulfil their short term

obligations and lose out on the profit making ventures.

The major changes which have occurred in the Banking Industry after the 2008 Global

Financial Crisis are the increase in the reforms and their implementation. Many governments

across the world pushed for increased transparency to provide more transparency and reduce the

risk in the financial systems. Some of the steps which are followed by HSBC in the liquidity

management and the capital management processes are the Basel III reforms and the CRD IV.

The BASEL III is designed to increase the resilience of the bank and reduce the impact of the

financial crisis. These include the management of a minimum amount of Tier I capital against the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FIN2138M-1920

risk-weighted assets of the business. There should also be an increase in the disclosure of the

decisions made by the business. The need for transparency in the business has increased

significantly.

With respect to capital management, the Capital Requirement Directives (CRD) suggest

that the business holds sufficient resources to cover the well-known risks of the business. These

guidelines tend to focus on strengthening of the prudential framework guiding the individual

institutions. The guidelines of the Directive are mostly as a response to the issues arising from

the Financial Crisis. The main aspects to which the CRD IV offers an enhancement on the

previous known legislations include the enhanced governance and enhanced transparency on the

part of the banks.

Conclusion and Recommendations

On the basis of the above discussion, it can be suggested that the two most important

aspects related to a banking business include the liquidity and the capital management. These are

not only necessary in measuring the performance but also required to ensure its stability in the

long run. Some of the more recent trends occurring in the Banking Industry include greater

stability, more regulations and the increased speed of digitalisation of the business. The business

should opt for diversification strategies and focus more on improving their capabilities in

providing these digitalised services. The power of the available data and technologies should be

harnessed together to drive a more competitive growth in the industry. The issues arising with

the digitalisation include the security and privacy issues. Sufficient security measures should be

undertaken to maximise the security procedures of the organisation. The restructuring of the

organisation should take place more quickly to ensure that the businesses are able to meet the

new challenges occurring due to digitalisation. Similarly, the reach of investment banking should

FIN2138M-1920

risk-weighted assets of the business. There should also be an increase in the disclosure of the

decisions made by the business. The need for transparency in the business has increased

significantly.

With respect to capital management, the Capital Requirement Directives (CRD) suggest

that the business holds sufficient resources to cover the well-known risks of the business. These

guidelines tend to focus on strengthening of the prudential framework guiding the individual

institutions. The guidelines of the Directive are mostly as a response to the issues arising from

the Financial Crisis. The main aspects to which the CRD IV offers an enhancement on the

previous known legislations include the enhanced governance and enhanced transparency on the

part of the banks.

Conclusion and Recommendations

On the basis of the above discussion, it can be suggested that the two most important

aspects related to a banking business include the liquidity and the capital management. These are

not only necessary in measuring the performance but also required to ensure its stability in the

long run. Some of the more recent trends occurring in the Banking Industry include greater

stability, more regulations and the increased speed of digitalisation of the business. The business

should opt for diversification strategies and focus more on improving their capabilities in

providing these digitalised services. The power of the available data and technologies should be

harnessed together to drive a more competitive growth in the industry. The issues arising with

the digitalisation include the security and privacy issues. Sufficient security measures should be

undertaken to maximise the security procedures of the organisation. The restructuring of the

organisation should take place more quickly to ensure that the businesses are able to meet the

new challenges occurring due to digitalisation. Similarly, the reach of investment banking should

11

FIN2138M-1920

be increased by implementing new client interaction models and orchestration of a better and

more conductive business environment.

FIN2138M-1920

be increased by implementing new client interaction models and orchestration of a better and

more conductive business environment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.