Report: Financial Resource Management in Health and Social Care

VerifiedAdded on 2020/01/28

|16

|4735

|230

Report

AI Summary

This report delves into the critical role of financial resources in the health and social care (HSC) sector, emphasizing their importance for effective operations centered on people-focused services. It examines the application of costing principles, business control systems, and the information necessary for managing resources within institutions like St. Patrick’s Nursing Home. The report analyzes diverse income sources, factors affecting finance availability, and different types of budget expenditure, including a detailed cash flow forecast. It also explores regulatory requirements, such as the Health and Social Care Act 2012 and the role of bodies like Monitor and the Care Quality Commission. Finally, the report evaluates expenditure decisions, budget monitoring arrangements, and suggests measures for improvement, providing a comprehensive overview of financial management in the HSC context.

FINANCIAL RESOURCES

IN HSC

IN HSC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Principles of costing and business control systems...............................................................1

1.2 Information needed to manage the resources........................................................................2

1.3 Regulatory requirements for managing resources.................................................................4

TASK 2............................................................................................................................................5

2.1 Diverse sources of income.....................................................................................................5

2.2 Factors influencing the availability of finance......................................................................6

2.3 Different types of budget expenditure...................................................................................7

TASK 3............................................................................................................................................9

TASK 4............................................................................................................................................9

1.4 Systems for managing financial resources............................................................................9

2.4 Evaluate the decisions about expenditure..............................................................................9

3.3 Budget monitoring arrangements........................................................................................10

4.1 Information needed for making financial decisions............................................................10

4.2 Analyse the relationship......................................................................................................11

4.3 Factors affecting the individual...........................................................................................11

4.4 Measures for improvement..................................................................................................12

CONCLUSION..............................................................................................................................12

References......................................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Principles of costing and business control systems...............................................................1

1.2 Information needed to manage the resources........................................................................2

1.3 Regulatory requirements for managing resources.................................................................4

TASK 2............................................................................................................................................5

2.1 Diverse sources of income.....................................................................................................5

2.2 Factors influencing the availability of finance......................................................................6

2.3 Different types of budget expenditure...................................................................................7

TASK 3............................................................................................................................................9

TASK 4............................................................................................................................................9

1.4 Systems for managing financial resources............................................................................9

2.4 Evaluate the decisions about expenditure..............................................................................9

3.3 Budget monitoring arrangements........................................................................................10

4.1 Information needed for making financial decisions............................................................10

4.2 Analyse the relationship......................................................................................................11

4.3 Factors affecting the individual...........................................................................................11

4.4 Measures for improvement..................................................................................................12

CONCLUSION..............................................................................................................................12

References......................................................................................................................................13

INTRODUCTION

Financial resources play an important role in functioning of the business within health

and social care. Within this industry the services are centred on the people. However, for an

effective functioning of the operations it is essential that financial resources are to be managed in

best manner. The purpose of this report is to understand how systems are used to manage the

monetary resources in health and social care centres. It will describe the role of planning in the

management of budgets. It will also state how the budgets are monitored. At last, the report will

end in suggesting measures for bringing improvements in these organizations.

TASK 1

1.1 Principles of costing and business control systems

St Patrick’s Nursing Home is a rehabilitation centre and health care institution for the

patients. The principles of costing and business control systems under the organization can be

described in the following manner:

Costs - There are different types of costs used in the nursing home.

Variable costs changes in direct proportion along with the change in output. For example

direct material costs (Brandon and Welch, 2009)

Fixed costs remains the same always as it does not change when output increases or

decreases. For example rent, rates etc.

Semi-variable costs – It includes element of both variables as well as fixed costs. For

example telephone expenses.

Cost benefit Analysis–It includes identifying the benefits associated with a course of

action and then cost related with the action is compared. The results of the technique are

displayed in form of payback period ( Cortes, 2009). This period is regarded as the time, the

method takes for benefits to repay the costs. St Patrick’s Nursing Home can use it different

conditions i.e. in hiring new employees, analysing an investment proposal etc.

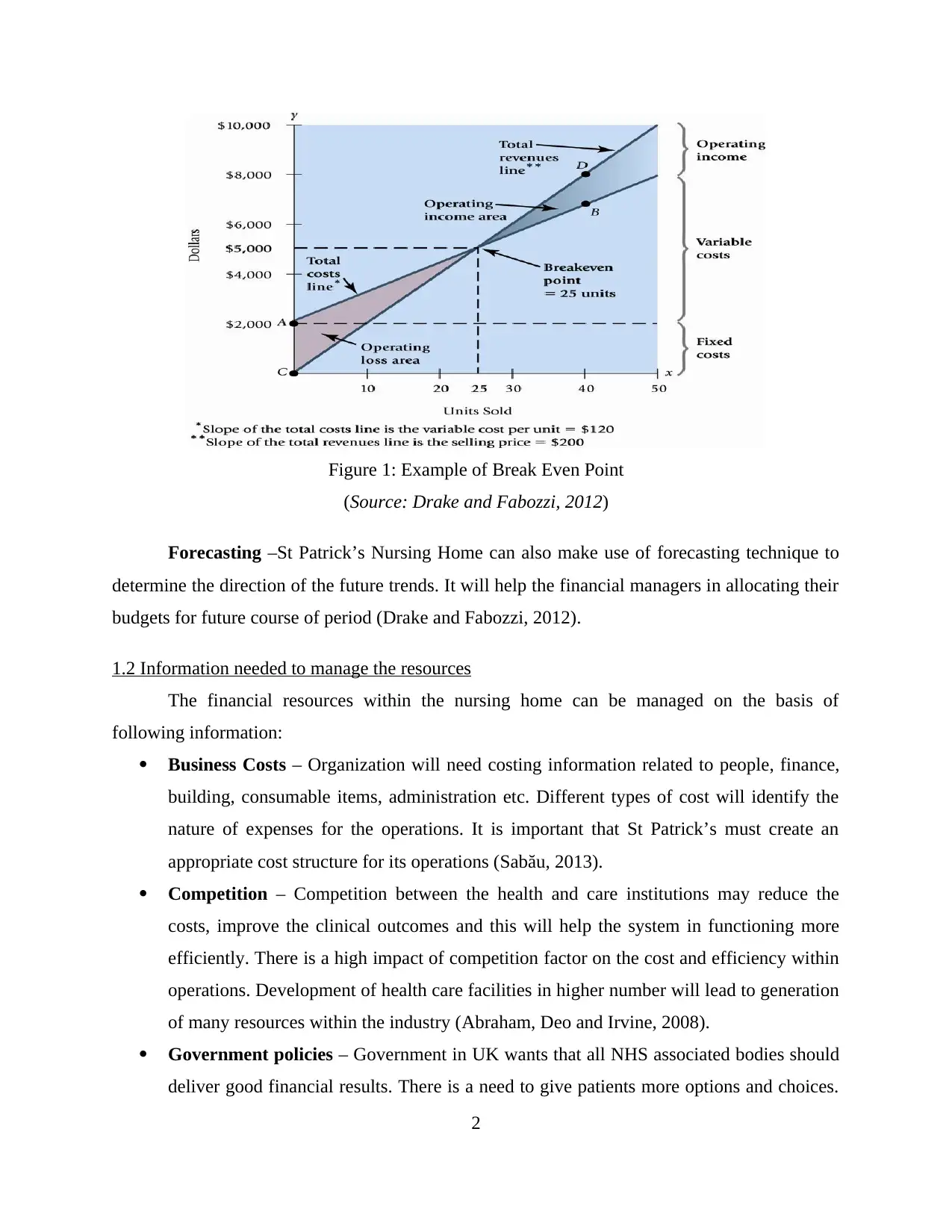

Breakeven point - At this point within the business, company has no profit or no loss at

the given sales level.

1

Financial resources play an important role in functioning of the business within health

and social care. Within this industry the services are centred on the people. However, for an

effective functioning of the operations it is essential that financial resources are to be managed in

best manner. The purpose of this report is to understand how systems are used to manage the

monetary resources in health and social care centres. It will describe the role of planning in the

management of budgets. It will also state how the budgets are monitored. At last, the report will

end in suggesting measures for bringing improvements in these organizations.

TASK 1

1.1 Principles of costing and business control systems

St Patrick’s Nursing Home is a rehabilitation centre and health care institution for the

patients. The principles of costing and business control systems under the organization can be

described in the following manner:

Costs - There are different types of costs used in the nursing home.

Variable costs changes in direct proportion along with the change in output. For example

direct material costs (Brandon and Welch, 2009)

Fixed costs remains the same always as it does not change when output increases or

decreases. For example rent, rates etc.

Semi-variable costs – It includes element of both variables as well as fixed costs. For

example telephone expenses.

Cost benefit Analysis–It includes identifying the benefits associated with a course of

action and then cost related with the action is compared. The results of the technique are

displayed in form of payback period ( Cortes, 2009). This period is regarded as the time, the

method takes for benefits to repay the costs. St Patrick’s Nursing Home can use it different

conditions i.e. in hiring new employees, analysing an investment proposal etc.

Breakeven point - At this point within the business, company has no profit or no loss at

the given sales level.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 1: Example of Break Even Point

(Source: Drake and Fabozzi, 2012)

Forecasting –St Patrick’s Nursing Home can also make use of forecasting technique to

determine the direction of the future trends. It will help the financial managers in allocating their

budgets for future course of period (Drake and Fabozzi, 2012).

1.2 Information needed to manage the resources

The financial resources within the nursing home can be managed on the basis of

following information:

Business Costs – Organization will need costing information related to people, finance,

building, consumable items, administration etc. Different types of cost will identify the

nature of expenses for the operations. It is important that St Patrick’s must create an

appropriate cost structure for its operations (Sabău, 2013).

Competition – Competition between the health and care institutions may reduce the

costs, improve the clinical outcomes and this will help the system in functioning more

efficiently. There is a high impact of competition factor on the cost and efficiency within

operations. Development of health care facilities in higher number will lead to generation

of many resources within the industry (Abraham, Deo and Irvine, 2008).

Government policies – Government in UK wants that all NHS associated bodies should

deliver good financial results. There is a need to give patients more options and choices.

2

(Source: Drake and Fabozzi, 2012)

Forecasting –St Patrick’s Nursing Home can also make use of forecasting technique to

determine the direction of the future trends. It will help the financial managers in allocating their

budgets for future course of period (Drake and Fabozzi, 2012).

1.2 Information needed to manage the resources

The financial resources within the nursing home can be managed on the basis of

following information:

Business Costs – Organization will need costing information related to people, finance,

building, consumable items, administration etc. Different types of cost will identify the

nature of expenses for the operations. It is important that St Patrick’s must create an

appropriate cost structure for its operations (Sabău, 2013).

Competition – Competition between the health and care institutions may reduce the

costs, improve the clinical outcomes and this will help the system in functioning more

efficiently. There is a high impact of competition factor on the cost and efficiency within

operations. Development of health care facilities in higher number will lead to generation

of many resources within the industry (Abraham, Deo and Irvine, 2008).

Government policies – Government in UK wants that all NHS associated bodies should

deliver good financial results. There is a need to give patients more options and choices.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Doctors and nurses are developed in good numbers to meet the requirements of the

patients. However the nursing homes are required to abide by the policies that are set by

the authorities (Ball, Jayaraman and Shivakumar, 2012). It will facilitate better

management of resources.

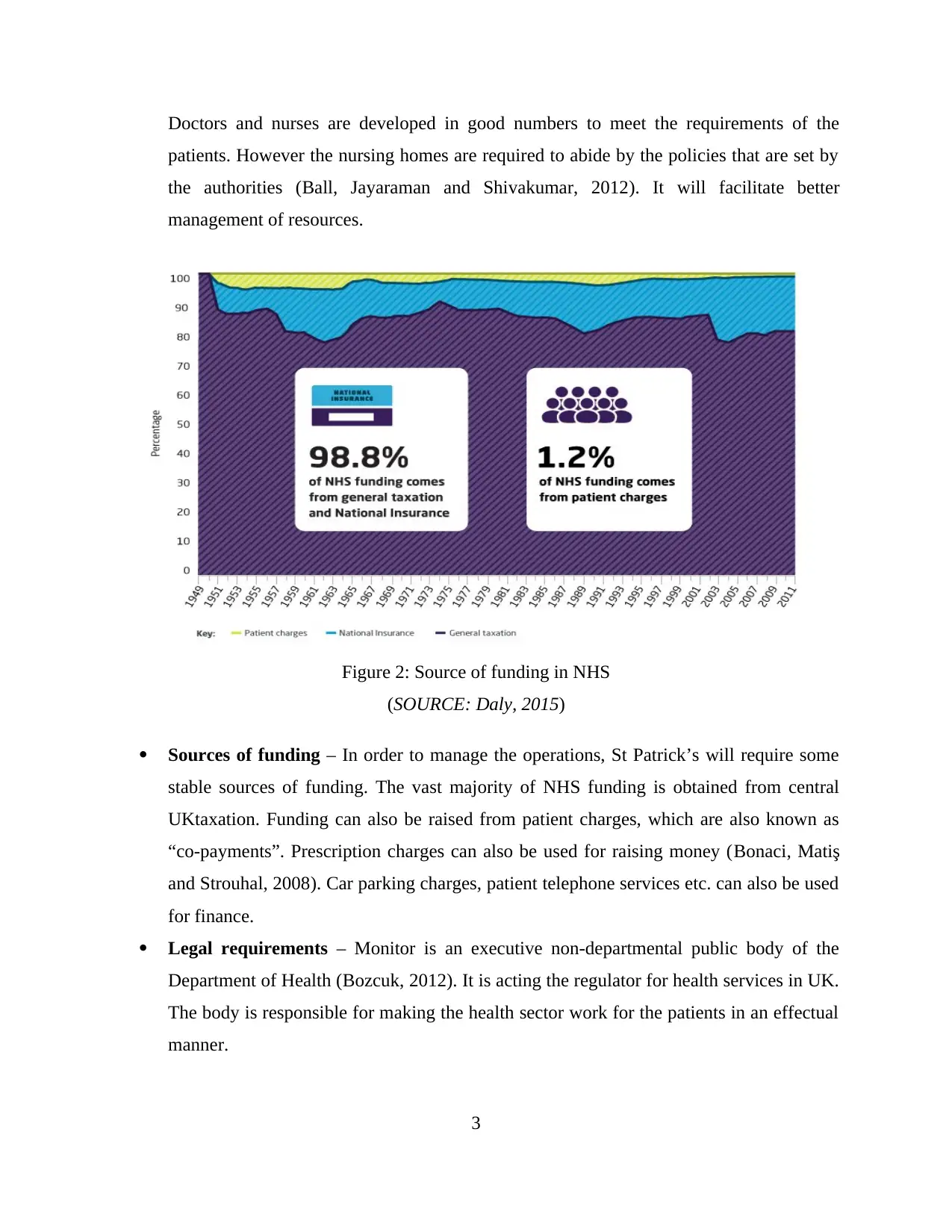

Figure 2: Source of funding in NHS

(SOURCE: Daly, 2015)

Sources of funding – In order to manage the operations, St Patrick’s will require some

stable sources of funding. The vast majority of NHS funding is obtained from central

UKtaxation. Funding can also be raised from patient charges, which are also known as

“co-payments”. Prescription charges can also be used for raising money (Bonaci, Matiş

and Strouhal, 2008). Car parking charges, patient telephone services etc. can also be used

for finance.

Legal requirements – Monitor is an executive non-departmental public body of the

Department of Health (Bozcuk, 2012). It is acting the regulator for health services in UK.

The body is responsible for making the health sector work for the patients in an effectual

manner.

3

patients. However the nursing homes are required to abide by the policies that are set by

the authorities (Ball, Jayaraman and Shivakumar, 2012). It will facilitate better

management of resources.

Figure 2: Source of funding in NHS

(SOURCE: Daly, 2015)

Sources of funding – In order to manage the operations, St Patrick’s will require some

stable sources of funding. The vast majority of NHS funding is obtained from central

UKtaxation. Funding can also be raised from patient charges, which are also known as

“co-payments”. Prescription charges can also be used for raising money (Bonaci, Matiş

and Strouhal, 2008). Car parking charges, patient telephone services etc. can also be used

for finance.

Legal requirements – Monitor is an executive non-departmental public body of the

Department of Health (Bozcuk, 2012). It is acting the regulator for health services in UK.

The body is responsible for making the health sector work for the patients in an effectual

manner.

3

1.3 Regulatory requirements for managing resources

St Patrick’s nursing body can face different types of regulatory requirements in the

management of resources. These can be described as follows:

The Health and Social Care Act, 2012 – This Act makes significant changes to the

whole system of the NHS. It is responsible for strengthening the role of Monitor as the

sector regulator. Under this act, a new organization named Health watch England has

been developed which is working for the welfare of the patients (Gibson, 2012). It also

makes provision about a National Health Service Commissioning Board and Clinical

Commissioning groups.

Monitor -This body is acting as the sector regulatory for the health services within

England. It holds the responsibility for authorising, monitoring and regulating the

foundation trust of NHS. These trusts are regulated so that they can provide quality care

on sustainable basis (Maynard, 2013). Monitor also facilitate safety to patient choice and

provides protection to the patients with respect to anti-competitive behaviour which is

against their interests. For example in the year 2010, the body de-authorize the working

of Mid Staffordshire NHS Foundation Trust.

Care Quality Commission – It is an independent regulating authority for health and

social care in UK. The commission is responsible for making sure that health care firms

are imparting safe, effective, compassionate and high quality care to the patients. Efforts

are also made to improve the services. For the purpose of control, CQC has developed

fundamental standards of quality and safety (Nobes, 2014). Performance rating is also

used by the commission so that users can select their own service providers.

The Care Act, 2014 – The act is established to decide the statutory roles of the Chief

Inspector of Hospitals, The Chief Inspector of General Practice and The Chief Inspector

of Adult Social Care (Bhowmik and Saha, 2013). The health and adult social care

services providers are subjected to criminal sanctions if they supply or publish any false

or misleading information.

TASK 2

(A)

4

St Patrick’s nursing body can face different types of regulatory requirements in the

management of resources. These can be described as follows:

The Health and Social Care Act, 2012 – This Act makes significant changes to the

whole system of the NHS. It is responsible for strengthening the role of Monitor as the

sector regulator. Under this act, a new organization named Health watch England has

been developed which is working for the welfare of the patients (Gibson, 2012). It also

makes provision about a National Health Service Commissioning Board and Clinical

Commissioning groups.

Monitor -This body is acting as the sector regulatory for the health services within

England. It holds the responsibility for authorising, monitoring and regulating the

foundation trust of NHS. These trusts are regulated so that they can provide quality care

on sustainable basis (Maynard, 2013). Monitor also facilitate safety to patient choice and

provides protection to the patients with respect to anti-competitive behaviour which is

against their interests. For example in the year 2010, the body de-authorize the working

of Mid Staffordshire NHS Foundation Trust.

Care Quality Commission – It is an independent regulating authority for health and

social care in UK. The commission is responsible for making sure that health care firms

are imparting safe, effective, compassionate and high quality care to the patients. Efforts

are also made to improve the services. For the purpose of control, CQC has developed

fundamental standards of quality and safety (Nobes, 2014). Performance rating is also

used by the commission so that users can select their own service providers.

The Care Act, 2014 – The act is established to decide the statutory roles of the Chief

Inspector of Hospitals, The Chief Inspector of General Practice and The Chief Inspector

of Adult Social Care (Bhowmik and Saha, 2013). The health and adult social care

services providers are subjected to criminal sanctions if they supply or publish any false

or misleading information.

TASK 2

(A)

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

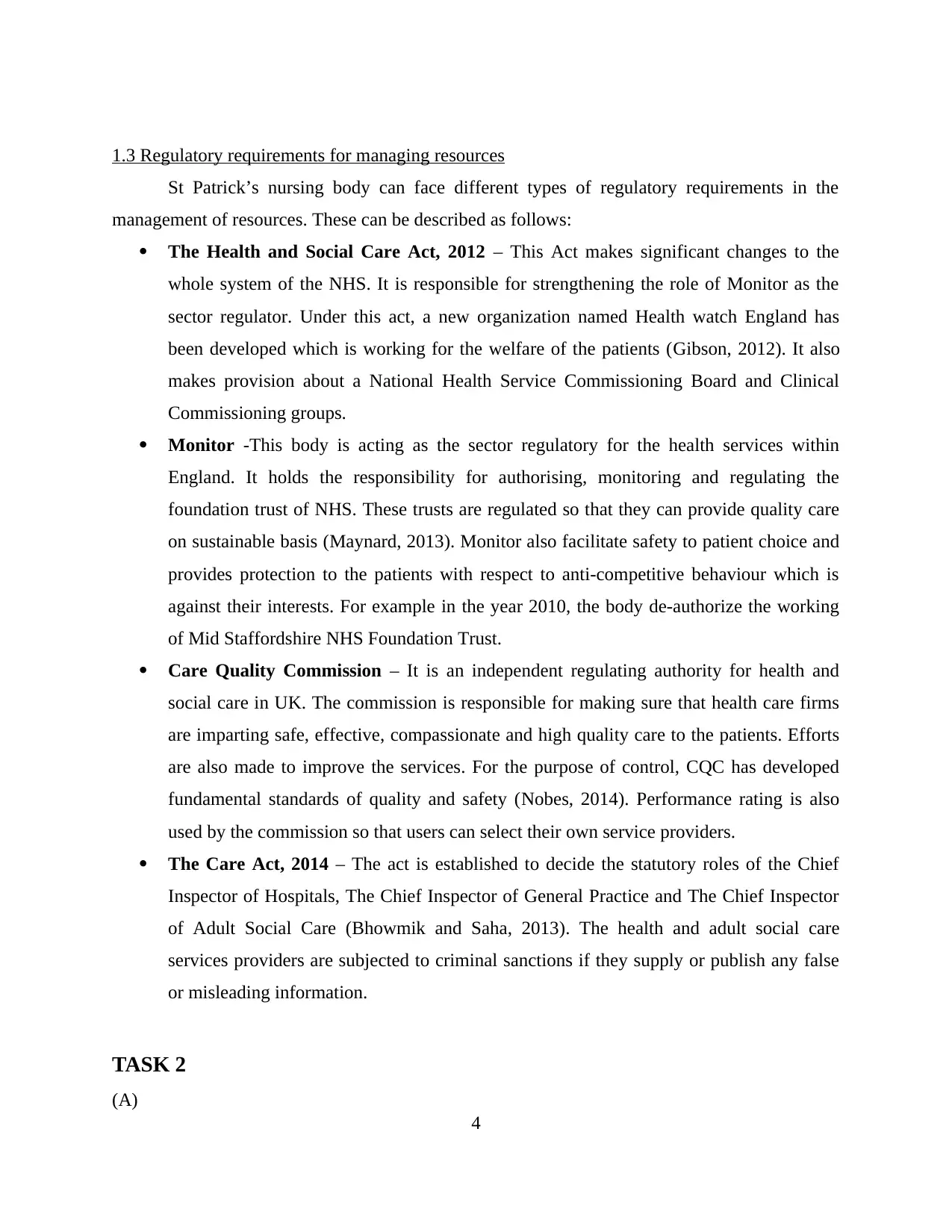

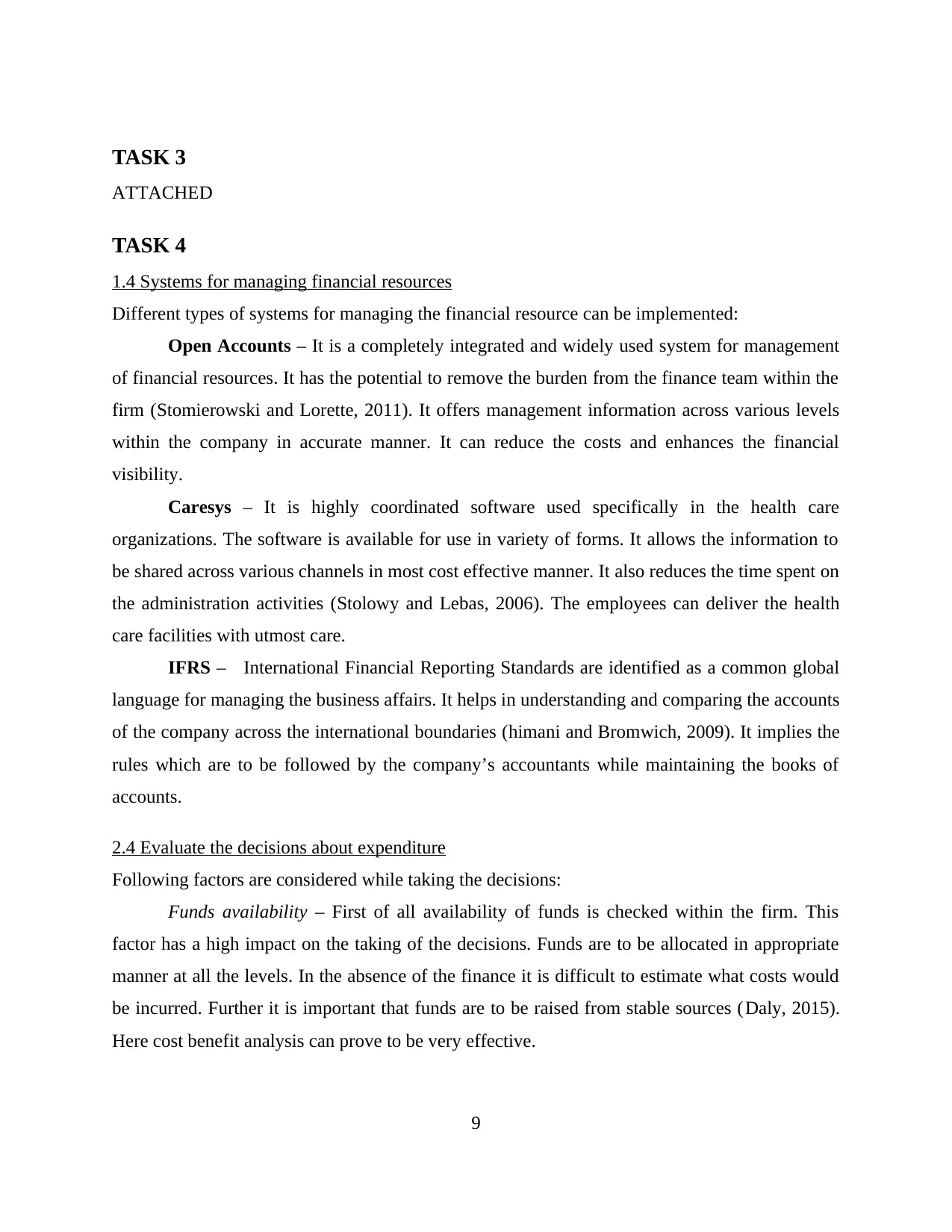

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Brought

Forward

40,000

Sales 200,00

0

300,00

0

300,00

0

300,00

0

250,00

0

260,00

0

300,00

0

260,00

0

300,00

0

325,00

0

265,00

0

265,00

0

Total Income 240,00

0

300,00

0

300,00

0

300,00

0

250,00

0

260,00

0

300,00

0

260,00

0

300,00

0

325,00

0

265,00

0

265,00

0

Purchases 150,00

0

140,00

0

135,00

0

135,00

0

140,00

0

130,00

0

135,00

0

145,00

0

140,00

0

140,00

0

145,00

0

145,00

0

Wages 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000

Rent &

Rates

56,000 56,000 56,000 56,000

Light &

Heat

55,000 55,000 55,000 55,000

Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000

Insurances 55,000 52,000

Equipment 50,000 10,000 10,000 10,000

Vehicles 20,000

Directors'

Salaries

22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000

Motor

Expenses

11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000

Sundry

Expenses

11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000

Total

Expenditure

432,00

0

251,00

0

291,00

0

302,00

0

293,00

0

296,00

0

292,00

0

246,00

0

296,00

0

297,00

0

246,00

0

301,00

0

Monthly

Deficit /

Surplus

-

192,00

0

49,000 9,000 -2,000 -

43,000

-

36,000

8,000 14,000 4,000 28,000 19,000 -

36,000

Accumulativ

e Deficit /

Surplus

-

192,00

0

-

143,00

0

-

134,00

0

-

136,00

0

-

179,00

0

-

215,00

0

-

207,00

0

-

193,00

0

-

189,00

0

-

161,00

0

-

142,00

0

-

178,00

0

(B)

2.1 Diverse sources of income

St Patrick’s nursing home can obtain finance from varied financial sources. These can be

described as follows:

Central Taxation UK – It is the source from which majority of income is derived for the

health and social care firms. The taxes paid by the residents of the country are utilized in form of

financial resources for these firms. The paid money is used for development and for improving

the health services in UK (Brigham and Ehrhardt, 2011). It is a stable source because taxes are to

be paid by people in regular manner.

5

Brought

Forward

40,000

Sales 200,00

0

300,00

0

300,00

0

300,00

0

250,00

0

260,00

0

300,00

0

260,00

0

300,00

0

325,00

0

265,00

0

265,00

0

Total Income 240,00

0

300,00

0

300,00

0

300,00

0

250,00

0

260,00

0

300,00

0

260,00

0

300,00

0

325,00

0

265,00

0

265,00

0

Purchases 150,00

0

140,00

0

135,00

0

135,00

0

140,00

0

130,00

0

135,00

0

145,00

0

140,00

0

140,00

0

145,00

0

145,00

0

Wages 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000

Rent &

Rates

56,000 56,000 56,000 56,000

Light &

Heat

55,000 55,000 55,000 55,000

Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000

Insurances 55,000 52,000

Equipment 50,000 10,000 10,000 10,000

Vehicles 20,000

Directors'

Salaries

22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000

Motor

Expenses

11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000

Sundry

Expenses

11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000

Total

Expenditure

432,00

0

251,00

0

291,00

0

302,00

0

293,00

0

296,00

0

292,00

0

246,00

0

296,00

0

297,00

0

246,00

0

301,00

0

Monthly

Deficit /

Surplus

-

192,00

0

49,000 9,000 -2,000 -

43,000

-

36,000

8,000 14,000 4,000 28,000 19,000 -

36,000

Accumulativ

e Deficit /

Surplus

-

192,00

0

-

143,00

0

-

134,00

0

-

136,00

0

-

179,00

0

-

215,00

0

-

207,00

0

-

193,00

0

-

189,00

0

-

161,00

0

-

142,00

0

-

178,00

0

(B)

2.1 Diverse sources of income

St Patrick’s nursing home can obtain finance from varied financial sources. These can be

described as follows:

Central Taxation UK – It is the source from which majority of income is derived for the

health and social care firms. The taxes paid by the residents of the country are utilized in form of

financial resources for these firms. The paid money is used for development and for improving

the health services in UK (Brigham and Ehrhardt, 2011). It is a stable source because taxes are to

be paid by people in regular manner.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget from government – Government also makes a budget for the NHS in England

every year. A specific amount is decided for use. At present the confined budget for the sector is

£116.4 billion. Every country in the European Union is free to decide how much to spend on the

NHS. It is the most trusted source of finance as it comes from the side of legal authorities.

Prescription charges – Another source of income is prescription charging. It is the most

widely used source for generating money (Broadbent and Cullen, 2012). In England, eligible

patients pay a prescription charge of £8.20 on meeting with a doctor. The charge is taken on the

drugs and medicines which are prescribed to the patients.

Other sources – Apart from the regular options, there are many other methods through

which finance can be arranged. Firm can establish charges for seeing overseas patients. Further

income can also be arranged through car parking fees and through telephonic services with the

patients.

2.2 Factors influencing the availability of finance

There can be many factors which can affect the financing for St Patricks. These can be

described as follows:

Government policies - The current long term economic plan reflects the values. It is the

responsibility of the government to pass on unaffordable levels of debt to the next generation.

There is a need to remove the deficit by using more sensible and balanced approaches. It will aid

in increasing the spending for the health and social care services (Ittelson, 2009). Hence all the

government policies are to be designed in a manner that they can give benefits to both service

providers as well as the users.

Agency objectives and policies – The Department of Health in UK enables the health care

firms to provide services according to the priorities. These departments are required to work in

coordination with the government. The Secretary of State for Health holds the major

responsibility for assuring that the entire industry work together to fulfil the needs of the patients.

Efforts are to be made to give them the best health care facilities (Siano, Kitchen and Confetto,

2010)

6

every year. A specific amount is decided for use. At present the confined budget for the sector is

£116.4 billion. Every country in the European Union is free to decide how much to spend on the

NHS. It is the most trusted source of finance as it comes from the side of legal authorities.

Prescription charges – Another source of income is prescription charging. It is the most

widely used source for generating money (Broadbent and Cullen, 2012). In England, eligible

patients pay a prescription charge of £8.20 on meeting with a doctor. The charge is taken on the

drugs and medicines which are prescribed to the patients.

Other sources – Apart from the regular options, there are many other methods through

which finance can be arranged. Firm can establish charges for seeing overseas patients. Further

income can also be arranged through car parking fees and through telephonic services with the

patients.

2.2 Factors influencing the availability of finance

There can be many factors which can affect the financing for St Patricks. These can be

described as follows:

Government policies - The current long term economic plan reflects the values. It is the

responsibility of the government to pass on unaffordable levels of debt to the next generation.

There is a need to remove the deficit by using more sensible and balanced approaches. It will aid

in increasing the spending for the health and social care services (Ittelson, 2009). Hence all the

government policies are to be designed in a manner that they can give benefits to both service

providers as well as the users.

Agency objectives and policies – The Department of Health in UK enables the health care

firms to provide services according to the priorities. These departments are required to work in

coordination with the government. The Secretary of State for Health holds the major

responsibility for assuring that the entire industry work together to fulfil the needs of the patients.

Efforts are to be made to give them the best health care facilities (Siano, Kitchen and Confetto,

2010)

6

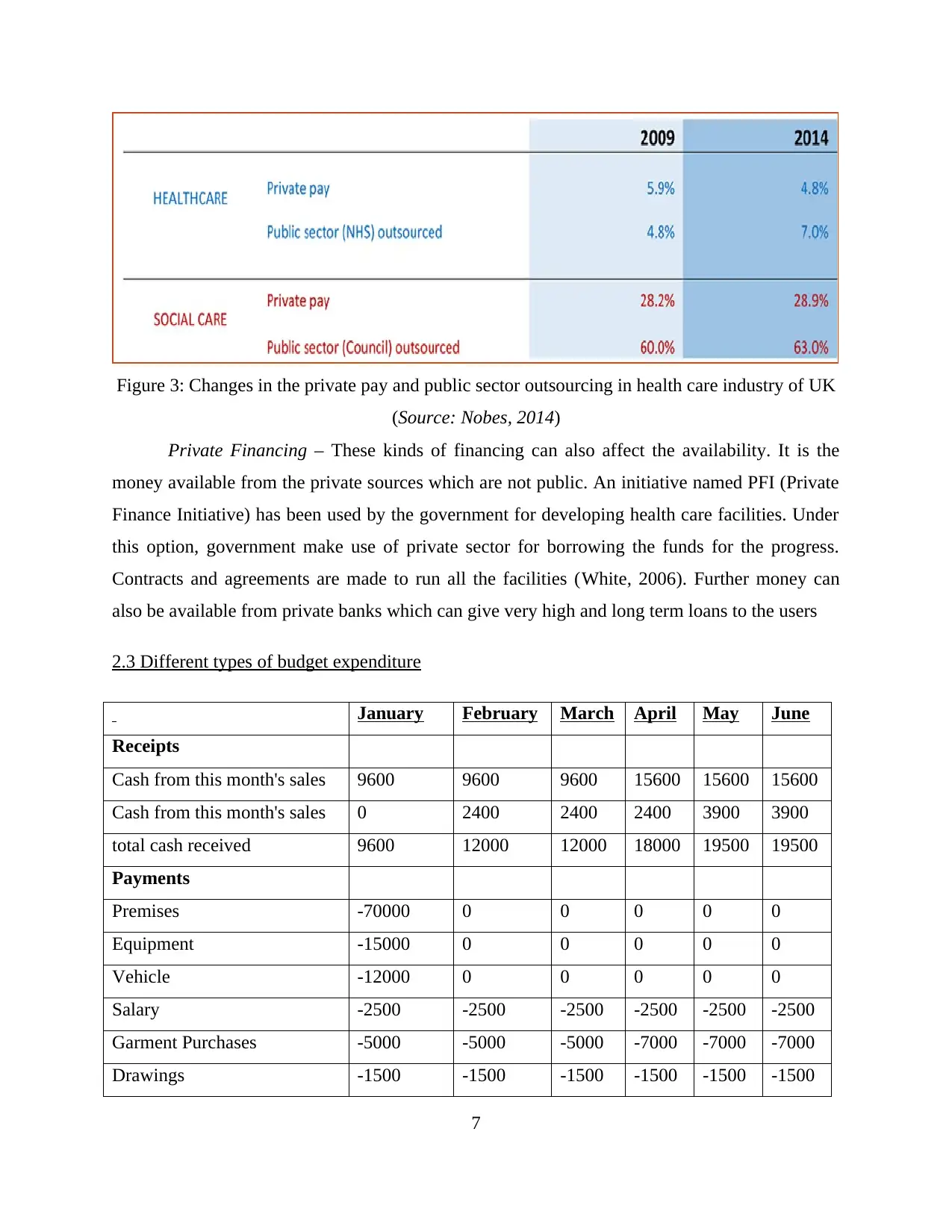

Figure 3: Changes in the private pay and public sector outsourcing in health care industry of UK

(Source: Nobes, 2014)

Private Financing – These kinds of financing can also affect the availability. It is the

money available from the private sources which are not public. An initiative named PFI (Private

Finance Initiative) has been used by the government for developing health care facilities. Under

this option, government make use of private sector for borrowing the funds for the progress.

Contracts and agreements are made to run all the facilities (White, 2006). Further money can

also be available from private banks which can give very high and long term loans to the users

2.3 Different types of budget expenditure

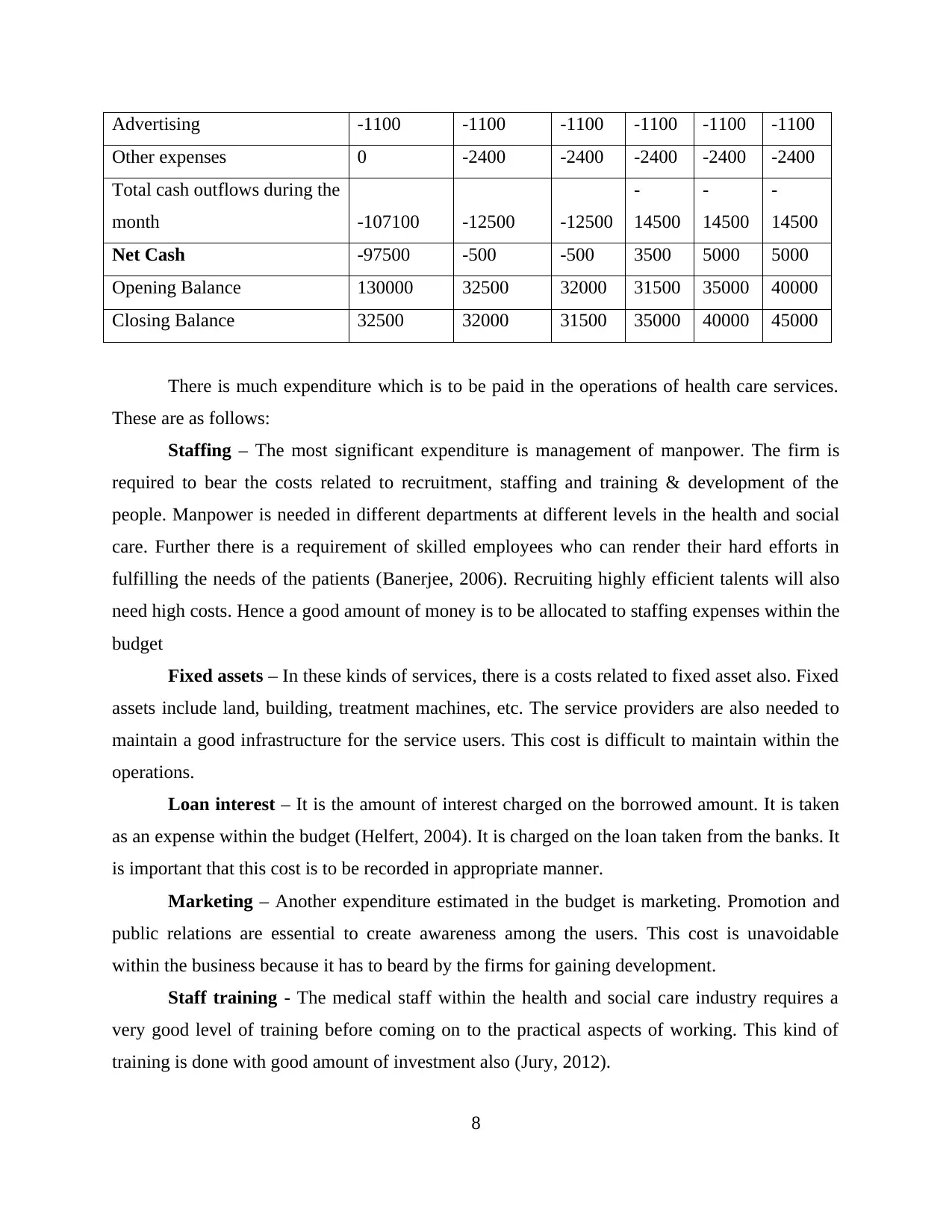

January February March April May June

Receipts

Cash from this month's sales 9600 9600 9600 15600 15600 15600

Cash from this month's sales 0 2400 2400 2400 3900 3900

total cash received 9600 12000 12000 18000 19500 19500

Payments

Premises -70000 0 0 0 0 0

Equipment -15000 0 0 0 0 0

Vehicle -12000 0 0 0 0 0

Salary -2500 -2500 -2500 -2500 -2500 -2500

Garment Purchases -5000 -5000 -5000 -7000 -7000 -7000

Drawings -1500 -1500 -1500 -1500 -1500 -1500

7

(Source: Nobes, 2014)

Private Financing – These kinds of financing can also affect the availability. It is the

money available from the private sources which are not public. An initiative named PFI (Private

Finance Initiative) has been used by the government for developing health care facilities. Under

this option, government make use of private sector for borrowing the funds for the progress.

Contracts and agreements are made to run all the facilities (White, 2006). Further money can

also be available from private banks which can give very high and long term loans to the users

2.3 Different types of budget expenditure

January February March April May June

Receipts

Cash from this month's sales 9600 9600 9600 15600 15600 15600

Cash from this month's sales 0 2400 2400 2400 3900 3900

total cash received 9600 12000 12000 18000 19500 19500

Payments

Premises -70000 0 0 0 0 0

Equipment -15000 0 0 0 0 0

Vehicle -12000 0 0 0 0 0

Salary -2500 -2500 -2500 -2500 -2500 -2500

Garment Purchases -5000 -5000 -5000 -7000 -7000 -7000

Drawings -1500 -1500 -1500 -1500 -1500 -1500

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advertising -1100 -1100 -1100 -1100 -1100 -1100

Other expenses 0 -2400 -2400 -2400 -2400 -2400

Total cash outflows during the

month -107100 -12500 -12500

-

14500

-

14500

-

14500

Net Cash -97500 -500 -500 3500 5000 5000

Opening Balance 130000 32500 32000 31500 35000 40000

Closing Balance 32500 32000 31500 35000 40000 45000

There is much expenditure which is to be paid in the operations of health care services.

These are as follows:

Staffing – The most significant expenditure is management of manpower. The firm is

required to bear the costs related to recruitment, staffing and training & development of the

people. Manpower is needed in different departments at different levels in the health and social

care. Further there is a requirement of skilled employees who can render their hard efforts in

fulfilling the needs of the patients (Banerjee, 2006). Recruiting highly efficient talents will also

need high costs. Hence a good amount of money is to be allocated to staffing expenses within the

budget

Fixed assets – In these kinds of services, there is a costs related to fixed asset also. Fixed

assets include land, building, treatment machines, etc. The service providers are also needed to

maintain a good infrastructure for the service users. This cost is difficult to maintain within the

operations.

Loan interest – It is the amount of interest charged on the borrowed amount. It is taken

as an expense within the budget (Helfert, 2004). It is charged on the loan taken from the banks. It

is important that this cost is to be recorded in appropriate manner.

Marketing – Another expenditure estimated in the budget is marketing. Promotion and

public relations are essential to create awareness among the users. This cost is unavoidable

within the business because it has to beard by the firms for gaining development.

Staff training - The medical staff within the health and social care industry requires a

very good level of training before coming on to the practical aspects of working. This kind of

training is done with good amount of investment also (Jury, 2012).

8

Other expenses 0 -2400 -2400 -2400 -2400 -2400

Total cash outflows during the

month -107100 -12500 -12500

-

14500

-

14500

-

14500

Net Cash -97500 -500 -500 3500 5000 5000

Opening Balance 130000 32500 32000 31500 35000 40000

Closing Balance 32500 32000 31500 35000 40000 45000

There is much expenditure which is to be paid in the operations of health care services.

These are as follows:

Staffing – The most significant expenditure is management of manpower. The firm is

required to bear the costs related to recruitment, staffing and training & development of the

people. Manpower is needed in different departments at different levels in the health and social

care. Further there is a requirement of skilled employees who can render their hard efforts in

fulfilling the needs of the patients (Banerjee, 2006). Recruiting highly efficient talents will also

need high costs. Hence a good amount of money is to be allocated to staffing expenses within the

budget

Fixed assets – In these kinds of services, there is a costs related to fixed asset also. Fixed

assets include land, building, treatment machines, etc. The service providers are also needed to

maintain a good infrastructure for the service users. This cost is difficult to maintain within the

operations.

Loan interest – It is the amount of interest charged on the borrowed amount. It is taken

as an expense within the budget (Helfert, 2004). It is charged on the loan taken from the banks. It

is important that this cost is to be recorded in appropriate manner.

Marketing – Another expenditure estimated in the budget is marketing. Promotion and

public relations are essential to create awareness among the users. This cost is unavoidable

within the business because it has to beard by the firms for gaining development.

Staff training - The medical staff within the health and social care industry requires a

very good level of training before coming on to the practical aspects of working. This kind of

training is done with good amount of investment also (Jury, 2012).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

ATTACHED

TASK 4

1.4 Systems for managing financial resources

Different types of systems for managing the financial resource can be implemented:

Open Accounts – It is a completely integrated and widely used system for management

of financial resources. It has the potential to remove the burden from the finance team within the

firm (Stomierowski and Lorette, 2011). It offers management information across various levels

within the company in accurate manner. It can reduce the costs and enhances the financial

visibility.

Caresys – It is highly coordinated software used specifically in the health care

organizations. The software is available for use in variety of forms. It allows the information to

be shared across various channels in most cost effective manner. It also reduces the time spent on

the administration activities (Stolowy and Lebas, 2006). The employees can deliver the health

care facilities with utmost care.

IFRS – International Financial Reporting Standards are identified as a common global

language for managing the business affairs. It helps in understanding and comparing the accounts

of the company across the international boundaries (himani and Bromwich, 2009). It implies the

rules which are to be followed by the company’s accountants while maintaining the books of

accounts.

2.4 Evaluate the decisions about expenditure

Following factors are considered while taking the decisions:

Funds availability – First of all availability of funds is checked within the firm. This

factor has a high impact on the taking of the decisions. Funds are to be allocated in appropriate

manner at all the levels. In the absence of the finance it is difficult to estimate what costs would

be incurred. Further it is important that funds are to be raised from stable sources (Daly, 2015).

Here cost benefit analysis can prove to be very effective.

9

ATTACHED

TASK 4

1.4 Systems for managing financial resources

Different types of systems for managing the financial resource can be implemented:

Open Accounts – It is a completely integrated and widely used system for management

of financial resources. It has the potential to remove the burden from the finance team within the

firm (Stomierowski and Lorette, 2011). It offers management information across various levels

within the company in accurate manner. It can reduce the costs and enhances the financial

visibility.

Caresys – It is highly coordinated software used specifically in the health care

organizations. The software is available for use in variety of forms. It allows the information to

be shared across various channels in most cost effective manner. It also reduces the time spent on

the administration activities (Stolowy and Lebas, 2006). The employees can deliver the health

care facilities with utmost care.

IFRS – International Financial Reporting Standards are identified as a common global

language for managing the business affairs. It helps in understanding and comparing the accounts

of the company across the international boundaries (himani and Bromwich, 2009). It implies the

rules which are to be followed by the company’s accountants while maintaining the books of

accounts.

2.4 Evaluate the decisions about expenditure

Following factors are considered while taking the decisions:

Funds availability – First of all availability of funds is checked within the firm. This

factor has a high impact on the taking of the decisions. Funds are to be allocated in appropriate

manner at all the levels. In the absence of the finance it is difficult to estimate what costs would

be incurred. Further it is important that funds are to be raised from stable sources (Daly, 2015).

Here cost benefit analysis can prove to be very effective.

9

Location – Another factor which is important in taking of decision is the location. The

place does matter in the rendering of the health and social care services. Location is to be eco-

friendly and free from environmental disturbances. Patients would prefer to come at the place

which is good from the point of view of environment (Prieto and Revilla, 2006).

Legal framework – As discussed earlier bodies such as Monitor, Care Quality

Commission and acts such as The Care Act, 2014 The Health and Social Care Act, 2012 etc

influence the activities of health and social care firms. The decisions are influenced from these

legal aspects.

Government policies - Government should focus on increasing the spending for the health

and social care services (Stansbury, 2012). In this regard, government policies are to be designed

in a manner that they can give benefits to both service providers as well as the users.

3.3 Budget monitoring arrangements

Following budget monitoring arrangements can be used for the control. These are as follows:

Internal Audit- Internal auditing is performed to scan the internal working condition of

an organization. It can be regarded as an independent, objective assurance and consulting action

which is taken to bring improvements and add value in the company’s operations. The control is

implemented by adopting a systematic and disciplined approach (Brandon and Welch, 2009). All

the risks related to budget implementation can be accessed through performing internal audit. It

has a very wide scope and can bring integrity in the accountancy procedures. Unethical practices

such as fraud and misrepresentation can be scanned very effectively through internal auditing.

External audit – This type of auditing is done in accordance with the specific laws and

rules. For example publication of the financial statements of a public limited company in front of

the general public at constant intervals is a kind of external audit. The information derived from

this audit is very useful for external stakeholders of the business. It includes government,

investors, general public etc ( Cortes, 2009). External audit is a reflector of company’s true and

fair financial position. It is mainly concerned with implementing internal controls in place in

order to manage the risks. Different types of stakeholders can take their respective financial

decisions on the basis of external audit.

10

place does matter in the rendering of the health and social care services. Location is to be eco-

friendly and free from environmental disturbances. Patients would prefer to come at the place

which is good from the point of view of environment (Prieto and Revilla, 2006).

Legal framework – As discussed earlier bodies such as Monitor, Care Quality

Commission and acts such as The Care Act, 2014 The Health and Social Care Act, 2012 etc

influence the activities of health and social care firms. The decisions are influenced from these

legal aspects.

Government policies - Government should focus on increasing the spending for the health

and social care services (Stansbury, 2012). In this regard, government policies are to be designed

in a manner that they can give benefits to both service providers as well as the users.

3.3 Budget monitoring arrangements

Following budget monitoring arrangements can be used for the control. These are as follows:

Internal Audit- Internal auditing is performed to scan the internal working condition of

an organization. It can be regarded as an independent, objective assurance and consulting action

which is taken to bring improvements and add value in the company’s operations. The control is

implemented by adopting a systematic and disciplined approach (Brandon and Welch, 2009). All

the risks related to budget implementation can be accessed through performing internal audit. It

has a very wide scope and can bring integrity in the accountancy procedures. Unethical practices

such as fraud and misrepresentation can be scanned very effectively through internal auditing.

External audit – This type of auditing is done in accordance with the specific laws and

rules. For example publication of the financial statements of a public limited company in front of

the general public at constant intervals is a kind of external audit. The information derived from

this audit is very useful for external stakeholders of the business. It includes government,

investors, general public etc ( Cortes, 2009). External audit is a reflector of company’s true and

fair financial position. It is mainly concerned with implementing internal controls in place in

order to manage the risks. Different types of stakeholders can take their respective financial

decisions on the basis of external audit.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.