HSHM521 Financial Management in Healthcare: Melbourne Hospital Report

VerifiedAdded on 2023/06/03

|8

|1356

|265

Report

AI Summary

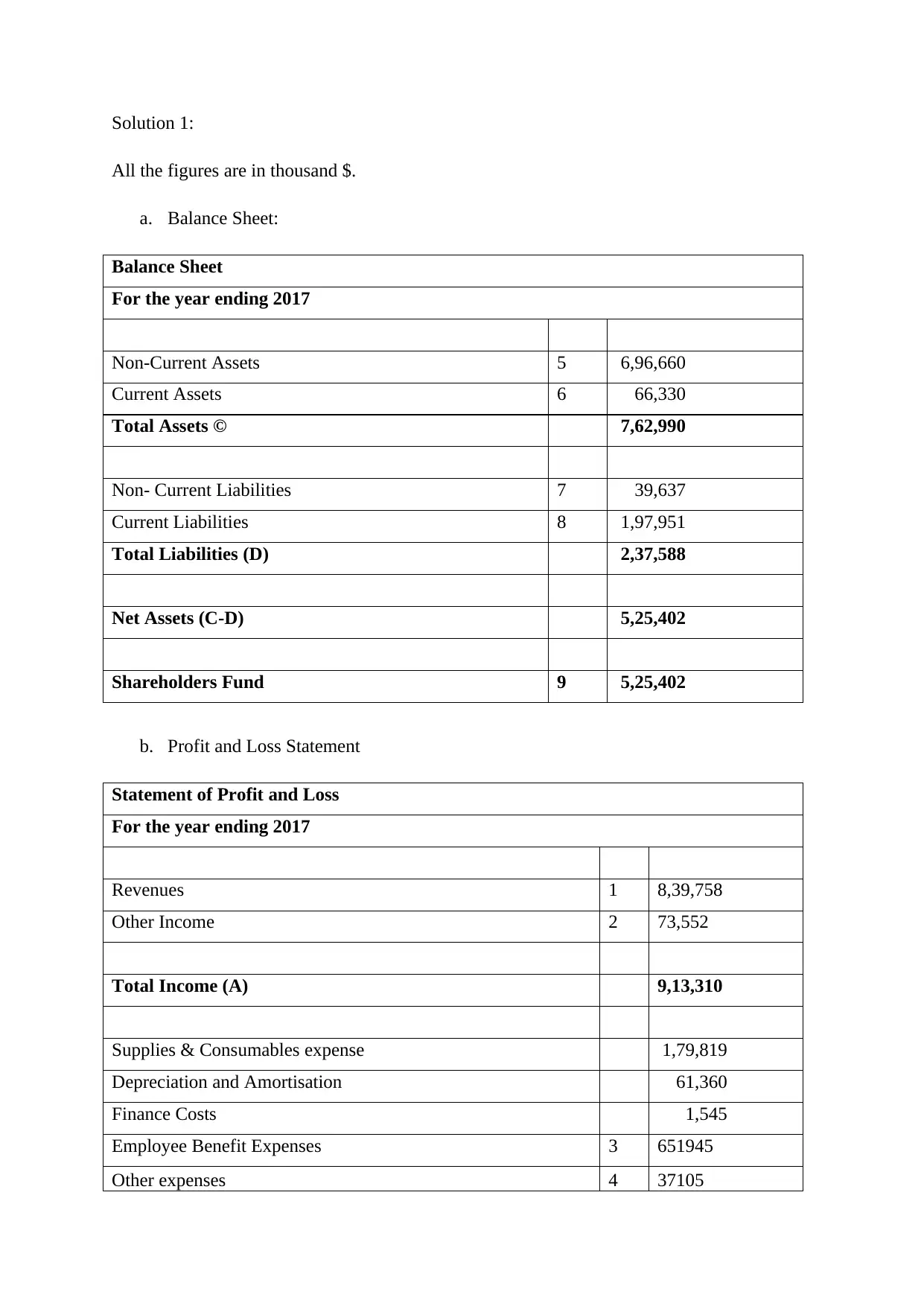

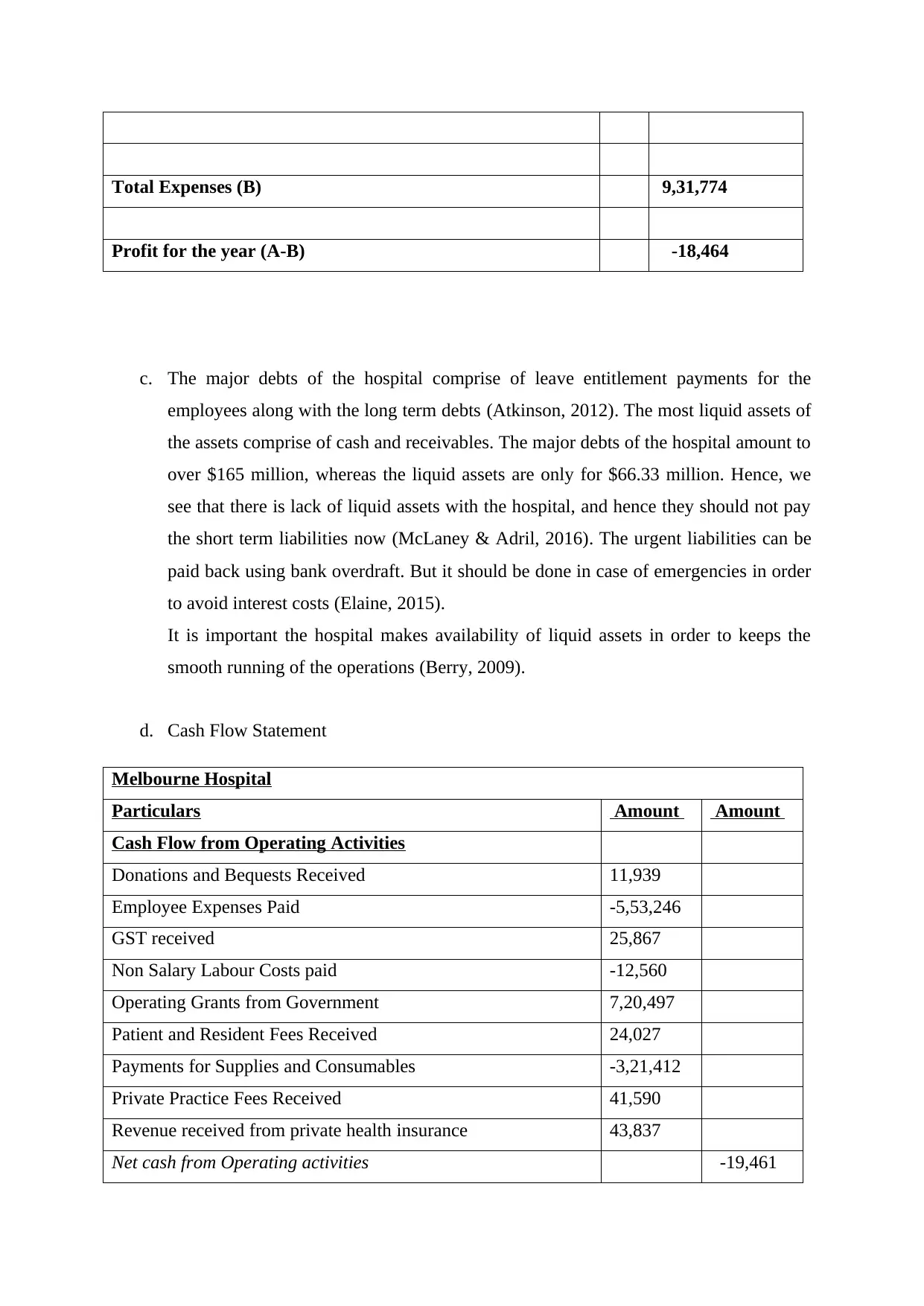

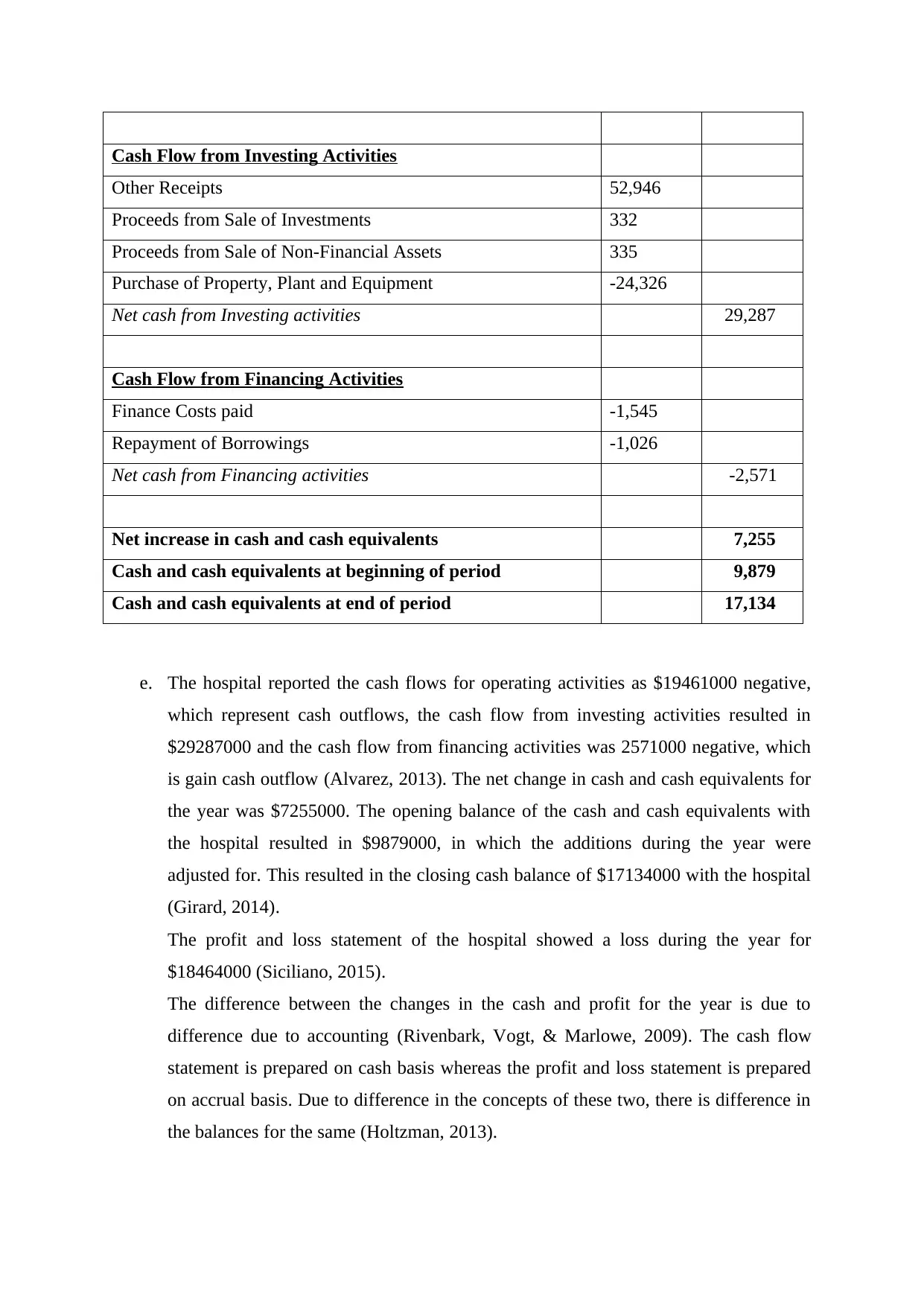

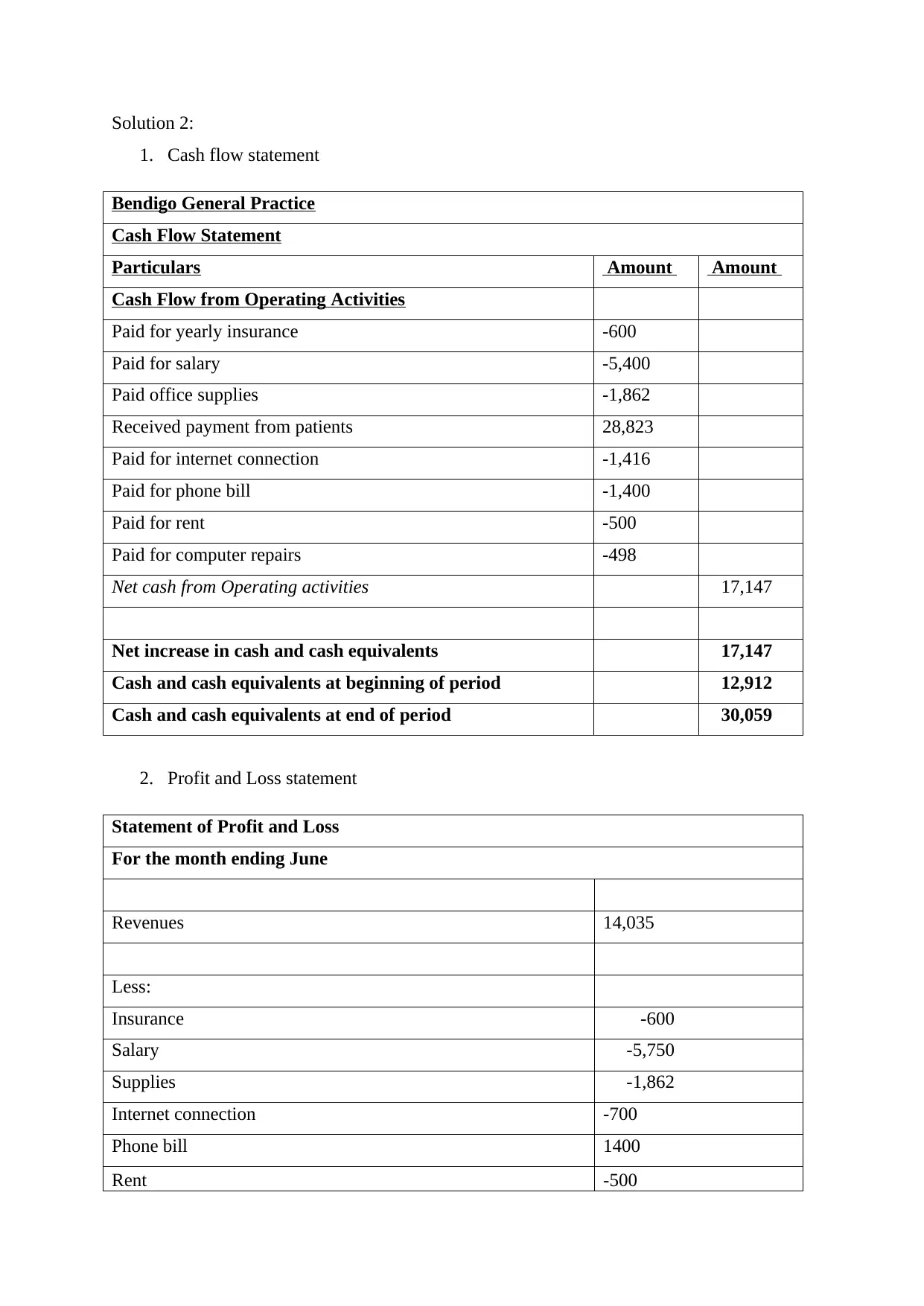

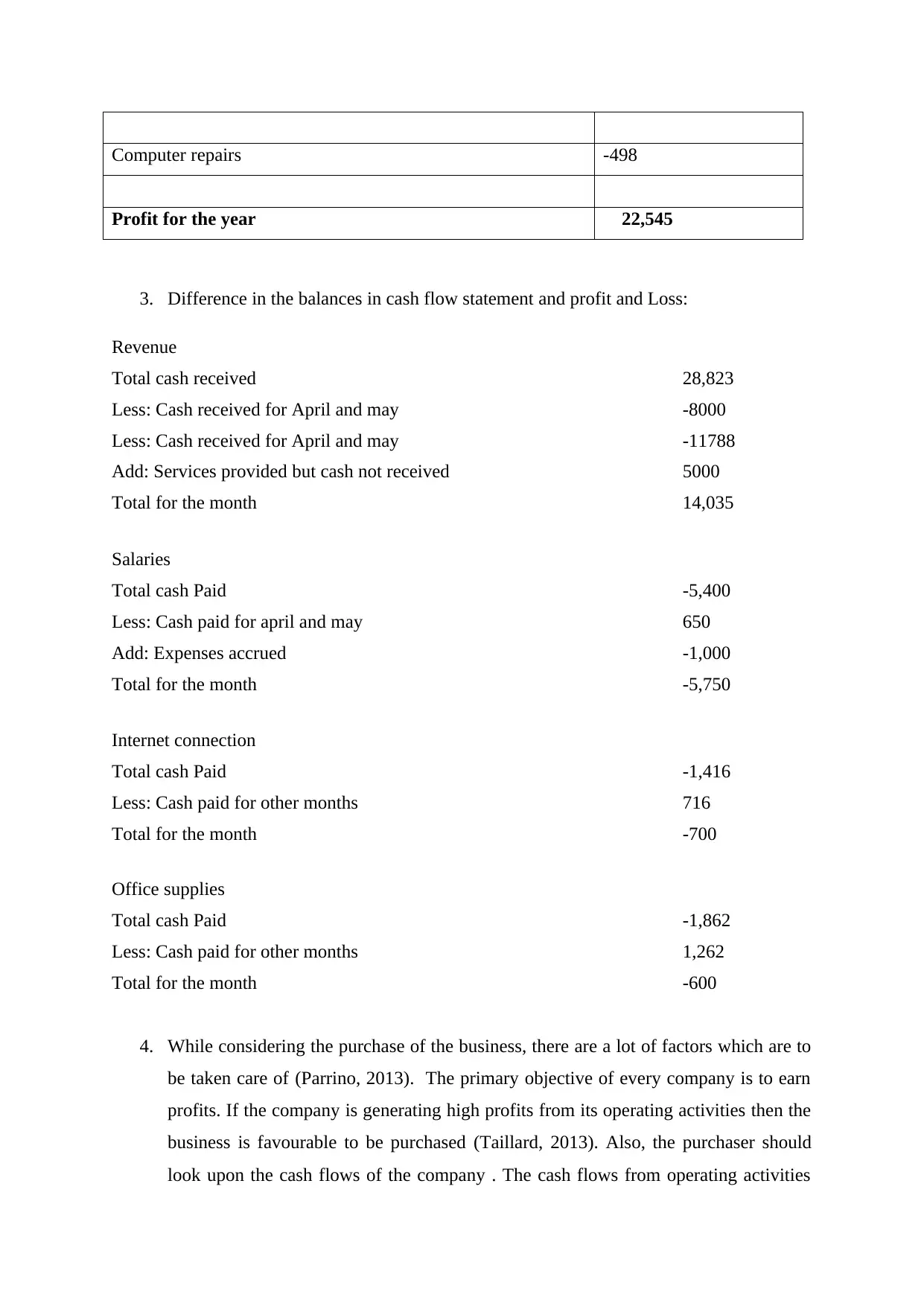

This report provides a comprehensive financial analysis of Melbourne Hospital, including the creation of a balance sheet, profit and loss statement, and cash flow statement for the year 2017. It analyzes the hospital's major debts and liquid assets, highlighting a potential lack of liquidity. The report also examines the cash flows from operating, investing, and financing activities, noting a negative cash flow from operations and a loss reported in the profit and loss statement, with a discussion on the differences arising from accrual versus cash basis accounting. Furthermore, the report includes a cash flow and profit and loss statement for Bendigo General Practice, discussing the differences in balances and key factors to consider when purchasing the business, such as profitability, cash flows, and financial ratios. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.