Hult EMBA Accounting: Deferred Expenses, Revenue, and Accounting Cycle

VerifiedAdded on 2021/04/21

|31

|5043

|43

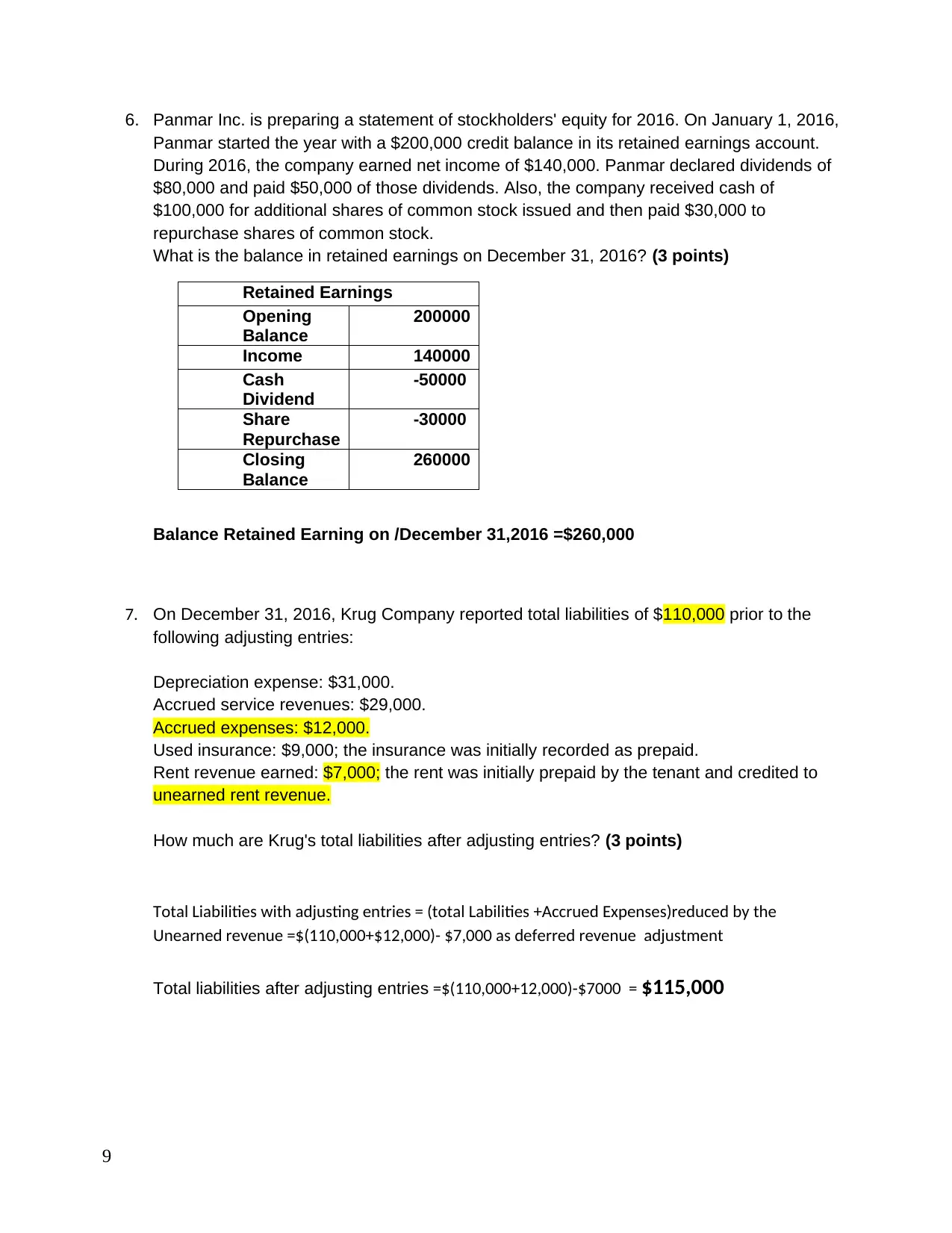

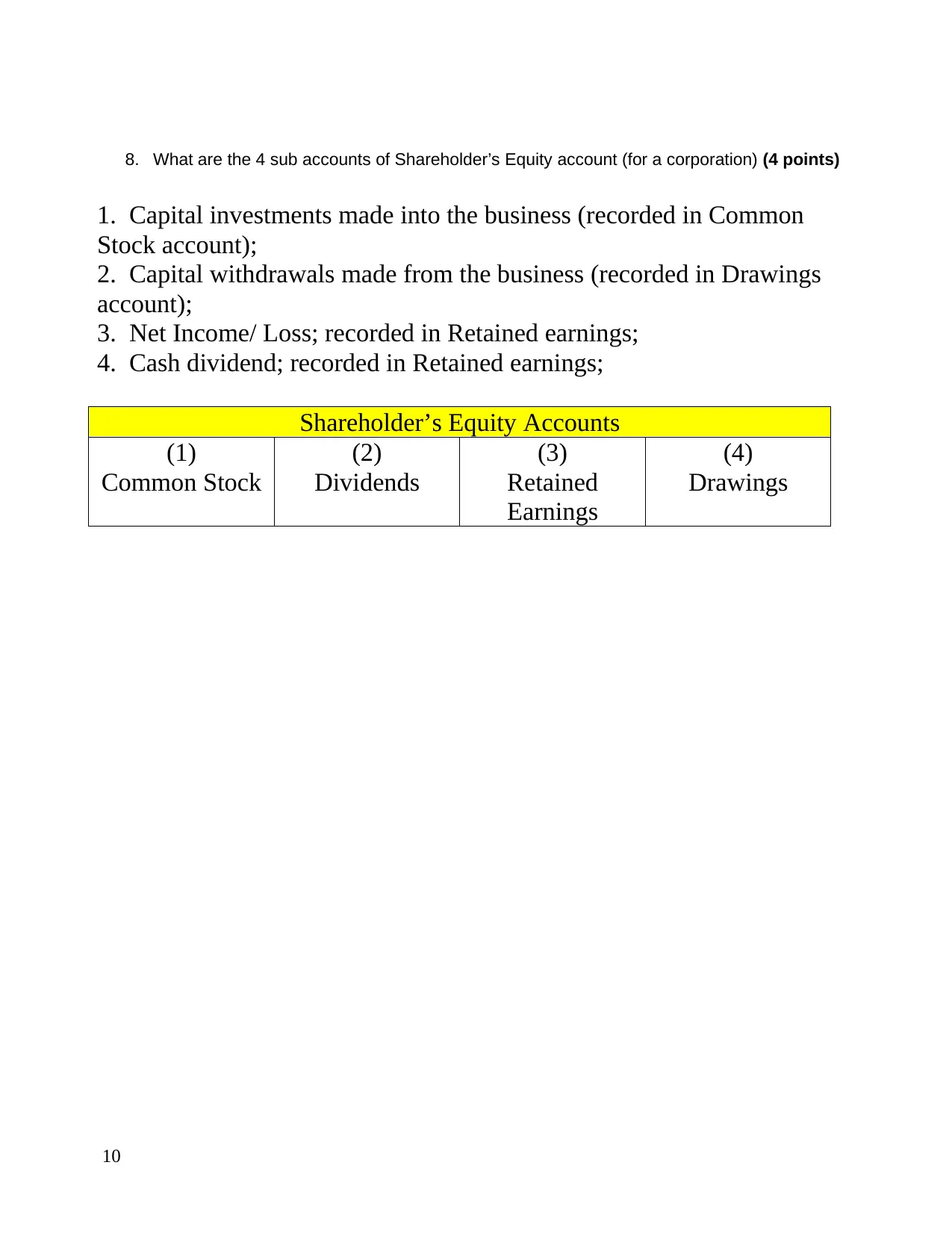

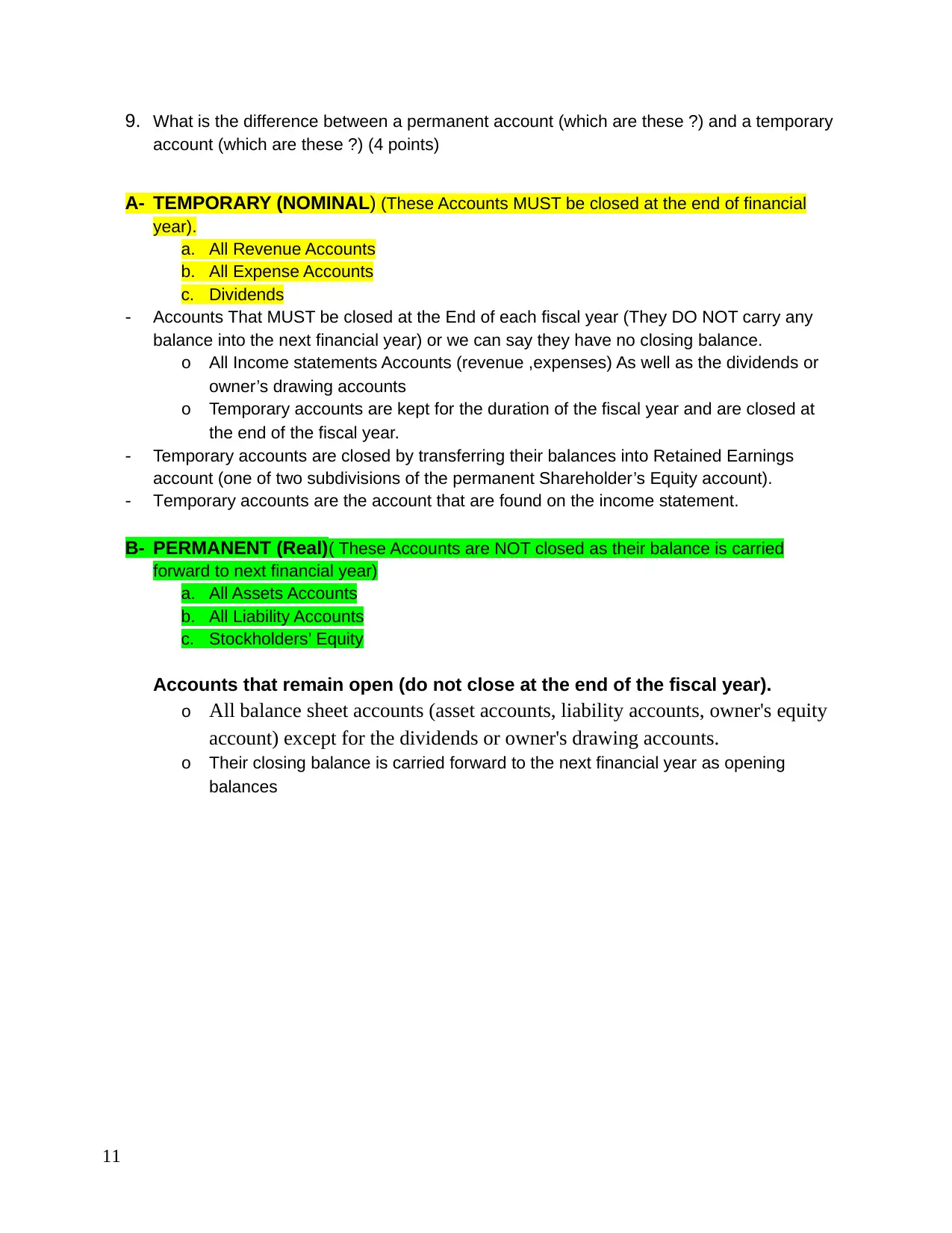

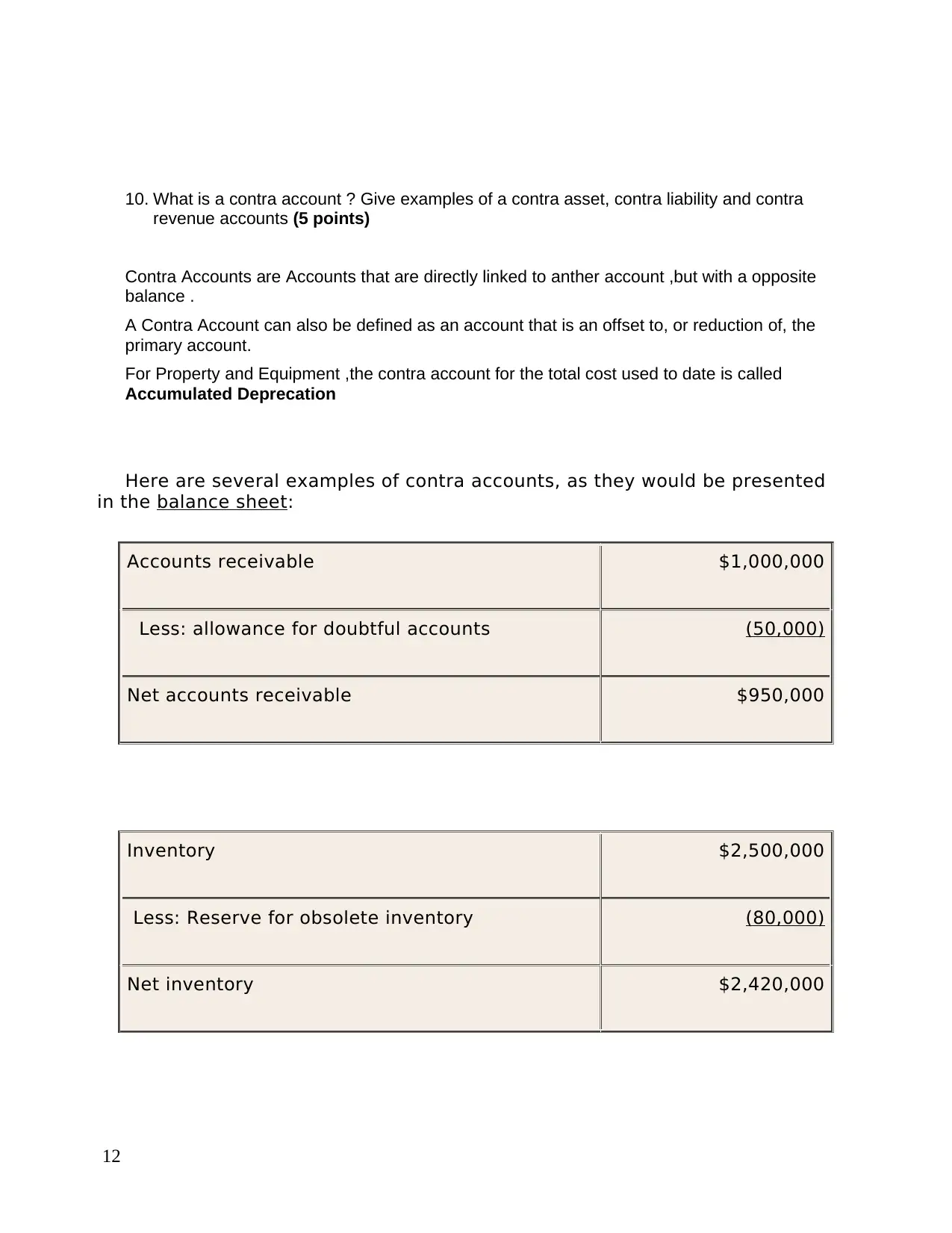

Homework Assignment

AI Summary

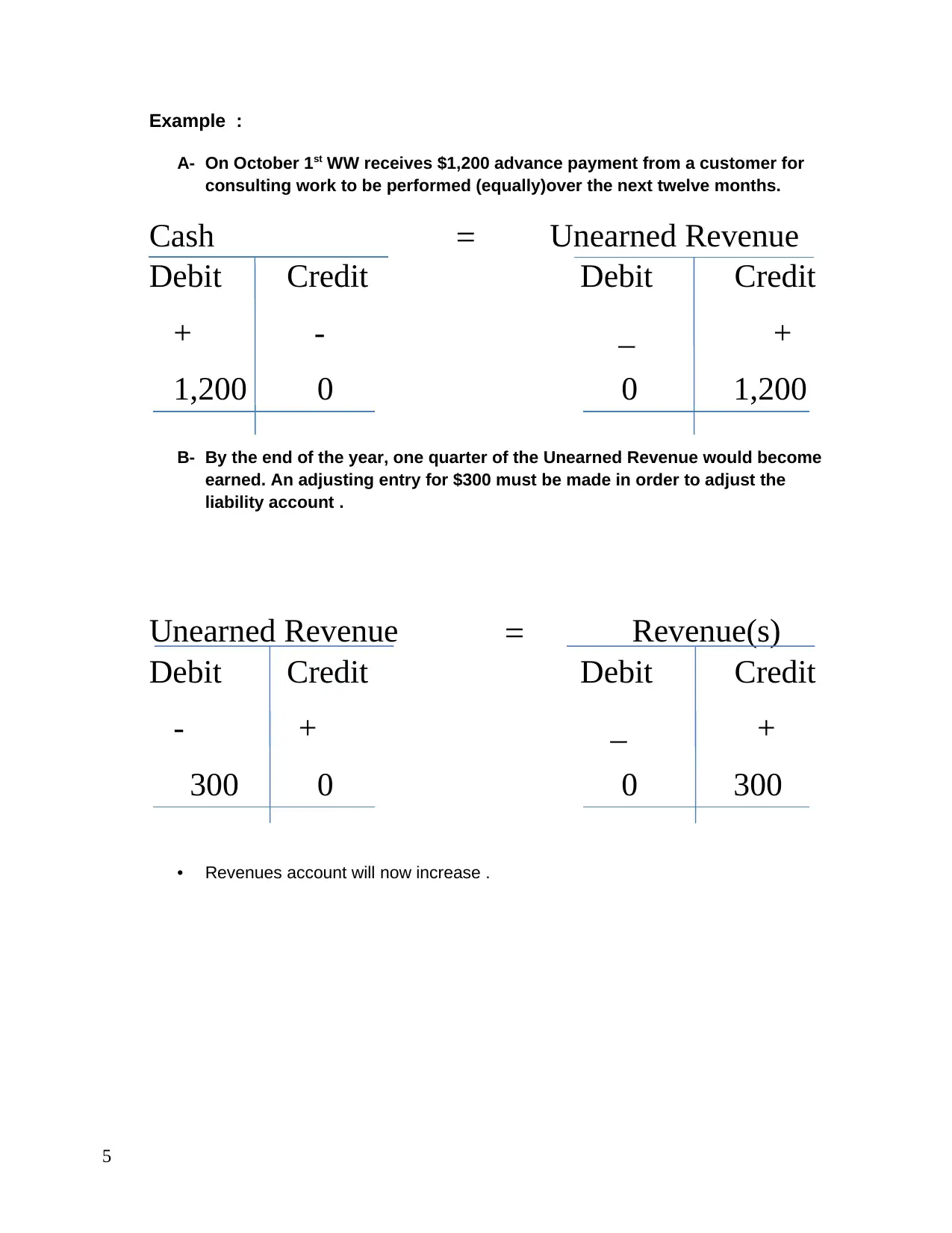

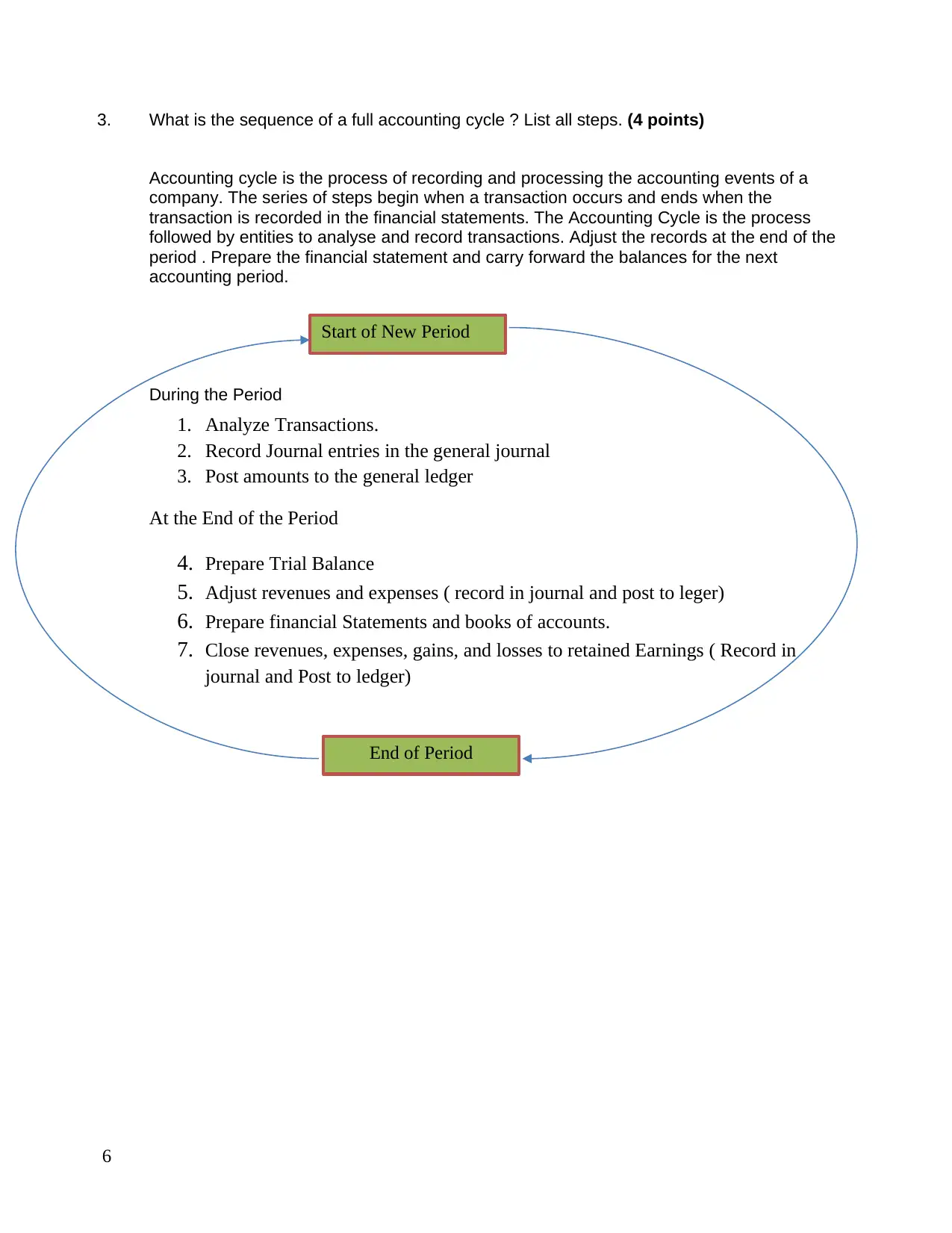

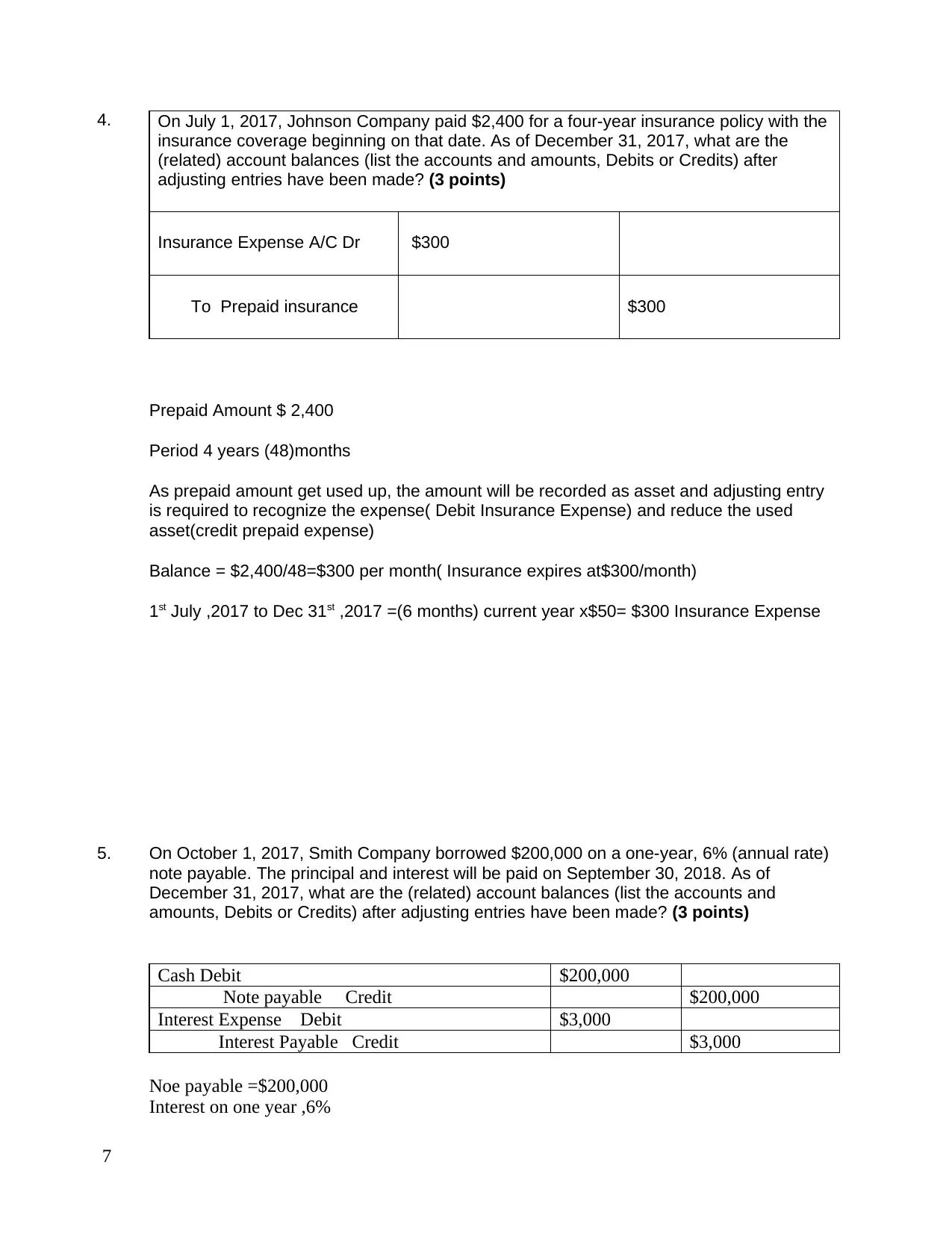

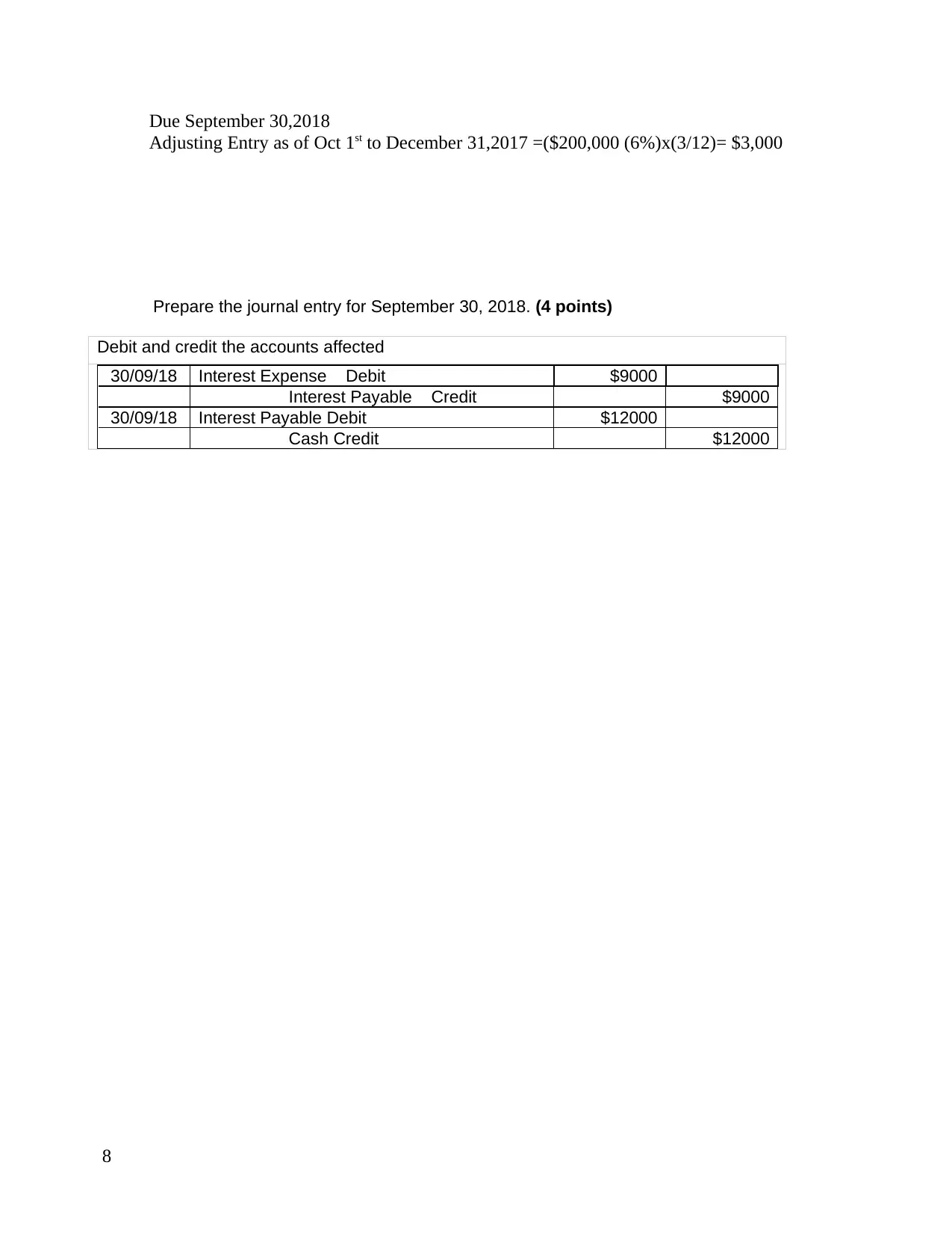

This document presents a comprehensive solution to an accounting assignment from Hult International Business School's EMBA program. The assignment covers fundamental accounting concepts, including deferred expenses and unearned revenue, providing definitions, examples, and journal entries. It explores the sequence of the full accounting cycle, requiring students to list all steps involved. The solution also addresses specific scenarios involving adjusting entries, such as insurance and interest calculations. Furthermore, it delves into shareholder's equity, differentiating between permanent and temporary accounts and explaining contra accounts. A key component is the construction of a standard cash flow statement, detailing the segmentation of cash flows. Finally, the assignment addresses the distinctions between perpetual and periodic inventory accounting systems and touches upon the concept of goodwill. The solutions provide detailed explanations and calculations, making it a valuable resource for students studying accounting principles.

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.