Detailed Corporate Accounting Analysis of Insurance Australia Group

VerifiedAdded on 2021/05/31

|13

|3037

|20

Report

AI Summary

This report provides a comprehensive analysis of the corporate accounting practices of Insurance Australia Group Limited (IAG), an Australian multinational insurance company listed on the ASX. The analysis begins with an examination of the cash flow statement, detailing changes in operating, investing, and financing activities, including reasons for these changes. The report then provides a comparative analysis of these three cash flow categories. It also explores the items included in the other comprehensive income statement, explaining each item and why they are not reported in the income statement. The report further describes IAG's income tax expense, verifying the calculation of tax expense and the treatment of deferred tax. Additionally, it examines the relationship between income tax expense and income tax paid, and highlights unique characteristics of IAG's financial statements, offering new insights and information. The analysis is supported by references and an appendix, providing a complete overview of IAG's financial performance and accounting practices.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student

Name of the University

Author Note

Corporate Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Table of Contents

Changes in each item of cash flows statement for the firm over the past year along with the

reasons for the change................................................................................................................2

Comparative analysis of the company’s three broad categories of cash flows that is operating

activities, investing activities and financing activities:..............................................................3

Items of Other Comprehensive Income Statement....................................................................4

Insightful explanation of each item of Other Comprehensive Income Statement.....................4

Reasons for the items have not been reported in Income Statement/Profit and Loss Statement

....................................................................................................................................................5

Clear description of your firm’s income tax expense................................................................5

Verification of the figure of tax being same as the company tax rate times the firm’s

accounting income.....................................................................................................................5

Deferred tax that is reported in the balance sheet along with the reasons for the record...........5

Current tax assets or income tax payable recorded by the company.........................................6

Verification of the income tax expense shown in the income statement same as the income

tax paid shown in the cash flow statement.................................................................................6

Unique characteristics in the financial statements, new insights, and other information..........6

References..................................................................................................................................8

Appendix....................................................................................................................................8

CORPORATE ACCOUNTING

Table of Contents

Changes in each item of cash flows statement for the firm over the past year along with the

reasons for the change................................................................................................................2

Comparative analysis of the company’s three broad categories of cash flows that is operating

activities, investing activities and financing activities:..............................................................3

Items of Other Comprehensive Income Statement....................................................................4

Insightful explanation of each item of Other Comprehensive Income Statement.....................4

Reasons for the items have not been reported in Income Statement/Profit and Loss Statement

....................................................................................................................................................5

Clear description of your firm’s income tax expense................................................................5

Verification of the figure of tax being same as the company tax rate times the firm’s

accounting income.....................................................................................................................5

Deferred tax that is reported in the balance sheet along with the reasons for the record...........5

Current tax assets or income tax payable recorded by the company.........................................6

Verification of the income tax expense shown in the income statement same as the income

tax paid shown in the cash flow statement.................................................................................6

Unique characteristics in the financial statements, new insights, and other information..........6

References..................................................................................................................................8

Appendix....................................................................................................................................8

2

CORPORATE ACCOUNTING

In order to analyze the annual report the chosen company listed on the Australian

Stock exchange (ASX) is Insurance Australia Group Limited which is a multinational

insurance company in Sydney, Australia. IAG is listed on the Australian Securities

Exchange and is a constituent of the S&P/ASX 50 index. The principal continuing activity of

the Group is the underwriting of general insurance and related corporate services and

investing activities.

Changes in each item of cash flows statement for the firm over the past year along with

the reasons for the change

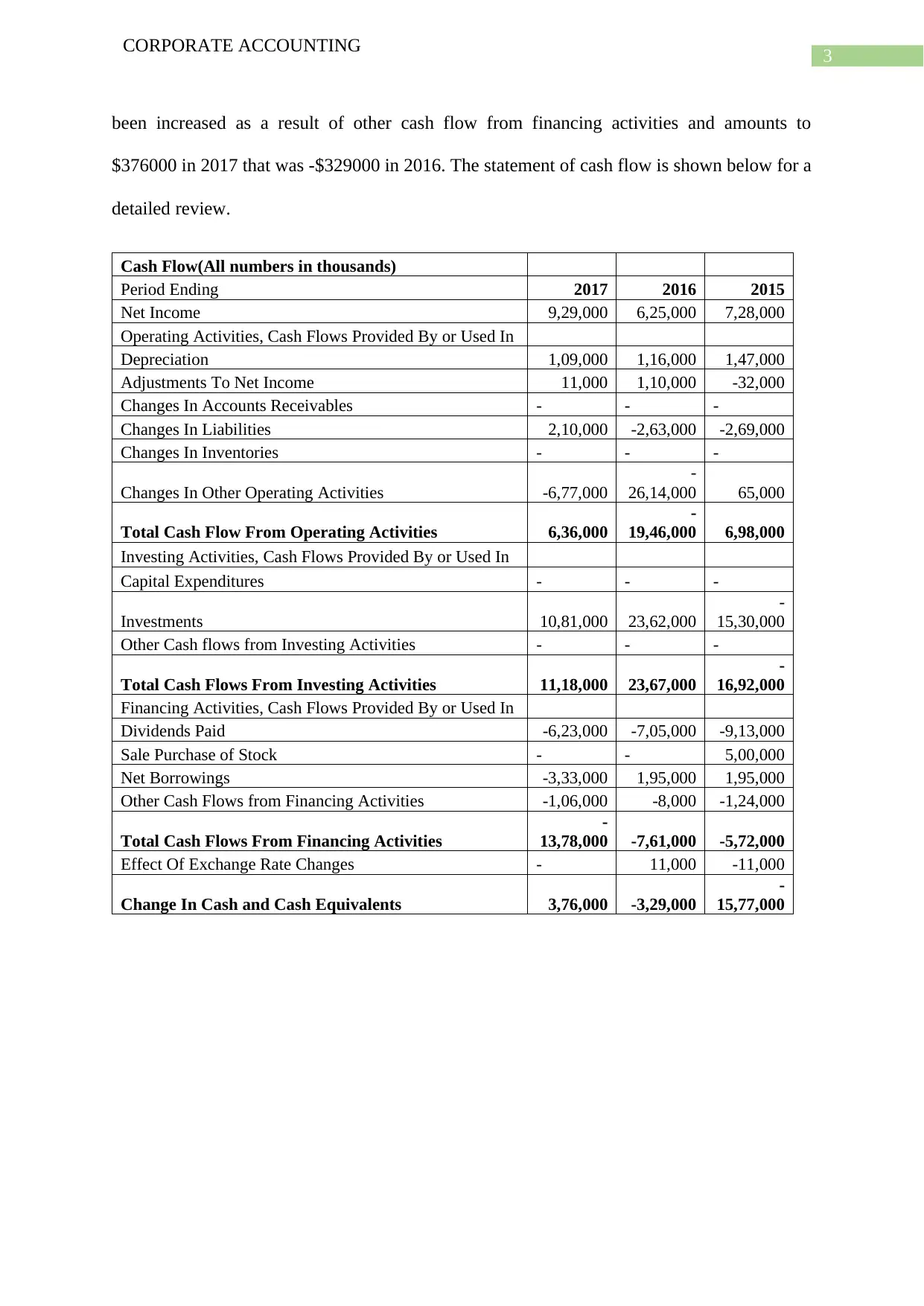

The cash flow statement of the chosen company of Insurance Australia Group Limited

consist of the usual three segments that includes cash flow from operating activities, investing

activities, Financing activities and the net cash and cash equivalents of the company. In the

operating activities there are items like the depreciation, income adjustments, and changes in

the accounts receivables, inventories and liability changes (Duff, 2016). It can be said from

the above items that the cash flow of each of the item has been decreased. This is due to more

income generation that is cash inflow.

Then comes the investing activities that deals with the capital expenditures,

investments and other cash expenses. The net cash outflow from investing activities have

been increased from 2016 to 2017 this is due to the increase in the capital expenditures in the

present year (Schaltegger & Burritt, 2017).

In the cash flow statement of Insurance Australia Group Limited the financing

activities consists of the dividends that are paid, sale and purchase of stock and net

borrowings(Goodwin, AtilganSimsir & Ahmed, 2017). There has been a drastic increase in

the financing cash inflow due to the amount of other cash flow from financing activities -

$106000 which was -$ 8000 in the last year of 2016.The cash and cash equivalents have also

CORPORATE ACCOUNTING

In order to analyze the annual report the chosen company listed on the Australian

Stock exchange (ASX) is Insurance Australia Group Limited which is a multinational

insurance company in Sydney, Australia. IAG is listed on the Australian Securities

Exchange and is a constituent of the S&P/ASX 50 index. The principal continuing activity of

the Group is the underwriting of general insurance and related corporate services and

investing activities.

Changes in each item of cash flows statement for the firm over the past year along with

the reasons for the change

The cash flow statement of the chosen company of Insurance Australia Group Limited

consist of the usual three segments that includes cash flow from operating activities, investing

activities, Financing activities and the net cash and cash equivalents of the company. In the

operating activities there are items like the depreciation, income adjustments, and changes in

the accounts receivables, inventories and liability changes (Duff, 2016). It can be said from

the above items that the cash flow of each of the item has been decreased. This is due to more

income generation that is cash inflow.

Then comes the investing activities that deals with the capital expenditures,

investments and other cash expenses. The net cash outflow from investing activities have

been increased from 2016 to 2017 this is due to the increase in the capital expenditures in the

present year (Schaltegger & Burritt, 2017).

In the cash flow statement of Insurance Australia Group Limited the financing

activities consists of the dividends that are paid, sale and purchase of stock and net

borrowings(Goodwin, AtilganSimsir & Ahmed, 2017). There has been a drastic increase in

the financing cash inflow due to the amount of other cash flow from financing activities -

$106000 which was -$ 8000 in the last year of 2016.The cash and cash equivalents have also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

been increased as a result of other cash flow from financing activities and amounts to

$376000 in 2017 that was -$329000 in 2016. The statement of cash flow is shown below for a

detailed review.

Cash Flow(All numbers in thousands)

Period Ending 2017 2016 2015

Net Income 9,29,000 6,25,000 7,28,000

Operating Activities, Cash Flows Provided By or Used In

Depreciation 1,09,000 1,16,000 1,47,000

Adjustments To Net Income 11,000 1,10,000 -32,000

Changes In Accounts Receivables - - -

Changes In Liabilities 2,10,000 -2,63,000 -2,69,000

Changes In Inventories - - -

Changes In Other Operating Activities -6,77,000

-

26,14,000 65,000

Total Cash Flow From Operating Activities 6,36,000

-

19,46,000 6,98,000

Investing Activities, Cash Flows Provided By or Used In

Capital Expenditures - - -

Investments 10,81,000 23,62,000

-

15,30,000

Other Cash flows from Investing Activities - - -

Total Cash Flows From Investing Activities 11,18,000 23,67,000

-

16,92,000

Financing Activities, Cash Flows Provided By or Used In

Dividends Paid -6,23,000 -7,05,000 -9,13,000

Sale Purchase of Stock - - 5,00,000

Net Borrowings -3,33,000 1,95,000 1,95,000

Other Cash Flows from Financing Activities -1,06,000 -8,000 -1,24,000

Total Cash Flows From Financing Activities

-

13,78,000 -7,61,000 -5,72,000

Effect Of Exchange Rate Changes - 11,000 -11,000

Change In Cash and Cash Equivalents 3,76,000 -3,29,000

-

15,77,000

CORPORATE ACCOUNTING

been increased as a result of other cash flow from financing activities and amounts to

$376000 in 2017 that was -$329000 in 2016. The statement of cash flow is shown below for a

detailed review.

Cash Flow(All numbers in thousands)

Period Ending 2017 2016 2015

Net Income 9,29,000 6,25,000 7,28,000

Operating Activities, Cash Flows Provided By or Used In

Depreciation 1,09,000 1,16,000 1,47,000

Adjustments To Net Income 11,000 1,10,000 -32,000

Changes In Accounts Receivables - - -

Changes In Liabilities 2,10,000 -2,63,000 -2,69,000

Changes In Inventories - - -

Changes In Other Operating Activities -6,77,000

-

26,14,000 65,000

Total Cash Flow From Operating Activities 6,36,000

-

19,46,000 6,98,000

Investing Activities, Cash Flows Provided By or Used In

Capital Expenditures - - -

Investments 10,81,000 23,62,000

-

15,30,000

Other Cash flows from Investing Activities - - -

Total Cash Flows From Investing Activities 11,18,000 23,67,000

-

16,92,000

Financing Activities, Cash Flows Provided By or Used In

Dividends Paid -6,23,000 -7,05,000 -9,13,000

Sale Purchase of Stock - - 5,00,000

Net Borrowings -3,33,000 1,95,000 1,95,000

Other Cash Flows from Financing Activities -1,06,000 -8,000 -1,24,000

Total Cash Flows From Financing Activities

-

13,78,000 -7,61,000 -5,72,000

Effect Of Exchange Rate Changes - 11,000 -11,000

Change In Cash and Cash Equivalents 3,76,000 -3,29,000

-

15,77,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

Comparative analysis of the company’s three broad categories of cash flows that is

operating activities, investing activities and financing activities:

Comparative analysis of three different categories of cash flow:

2017 in $m 2016 in $m 2015 in $m

-2,000,000

-1,500,000

-1,000,000

-500,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

comparitive analysis of the categories of cash

flow

Net cash flow from operating activities Net cash flow from investing activities

Net cash flow from financing activities

Particular

2017 in $m 2016 in $m 2015 in $m

Net cash flow from operating

activities 6,36,000 -19,46,000 6,98,000

Net cash flow from investing

activities 11,18,000 23,67,000 -16,92,000

Net cash flow from financing

activities -13,78,000 -7,61,000 -5,72,000

As depicted in the above graph and table the comparative analysis of cash flow from

operating activities, financing activities and investing activities. Net cash flow from operating

activities remained more or less constant in 2015 and 2017 but rose drastically in the year of

CORPORATE ACCOUNTING

Comparative analysis of the company’s three broad categories of cash flows that is

operating activities, investing activities and financing activities:

Comparative analysis of three different categories of cash flow:

2017 in $m 2016 in $m 2015 in $m

-2,000,000

-1,500,000

-1,000,000

-500,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

comparitive analysis of the categories of cash

flow

Net cash flow from operating activities Net cash flow from investing activities

Net cash flow from financing activities

Particular

2017 in $m 2016 in $m 2015 in $m

Net cash flow from operating

activities 6,36,000 -19,46,000 6,98,000

Net cash flow from investing

activities 11,18,000 23,67,000 -16,92,000

Net cash flow from financing

activities -13,78,000 -7,61,000 -5,72,000

As depicted in the above graph and table the comparative analysis of cash flow from

operating activities, financing activities and investing activities. Net cash flow from operating

activities remained more or less constant in 2015 and 2017 but rose drastically in the year of

5

CORPORATE ACCOUNTING

2016 to -$1946000. However, in 2016 and 2017 the cash flow from investing activities

increased drastically from 2015 that was -$ 16, 92,000. There was net cash flow used in

financing activities in year 2017 at amount -$13, 78,000 compared to -$5, 72,000 in year

2015. On other hand, from investing activities, there was a fall in cash flow to $ 11,18,000 in

year 2017 as against -$16,92,000in 2015.

Items of Other Comprehensive Income Statement

The Comprehensive income statement of Insurance Australia Group Limited consists

of the net profit that has remained more or less constant in both the years of 2016 and 2017.

The items that are included are the net exchange difference from transaction of foreign

operations taken to equity, the amount of foreign current translation reserve that have been

transferred to net profit and fair value adjustment on cash flow hedges (Hartnett & Romcke,

2015). There also exists net income tax items that have been transferred to income statement.

Insightful explanation of each item of Other Comprehensive Income Statement

The Net exchange differences from translation of foreign operation taken to

translation reserve drastically from 2016 which was $65 m in 2016 to -$16 m. Then comes

the remeasurements of defined benefit plans that is transferred to net profit on disposal of

controlled entities that has taken place on 2017 at $25 m. There has also been a fair value

adjustment on other comprehensive income from $ 33 m in 2016 to $ 9 m on 2017. The

income tax on items was $25m in 2016 then reduced to -$16m in 2017.The total of

comprehensive income amounts to $1014 m in 2017 which was $735 m in 2016.

Reasons for the items have not been reported in Income Statement/Profit and Loss

Statement

Comprehensive income statement is used for the measurement of any change in

interest of owners in business. It incorporates the income and expenses that have not been yet

CORPORATE ACCOUNTING

2016 to -$1946000. However, in 2016 and 2017 the cash flow from investing activities

increased drastically from 2015 that was -$ 16, 92,000. There was net cash flow used in

financing activities in year 2017 at amount -$13, 78,000 compared to -$5, 72,000 in year

2015. On other hand, from investing activities, there was a fall in cash flow to $ 11,18,000 in

year 2017 as against -$16,92,000in 2015.

Items of Other Comprehensive Income Statement

The Comprehensive income statement of Insurance Australia Group Limited consists

of the net profit that has remained more or less constant in both the years of 2016 and 2017.

The items that are included are the net exchange difference from transaction of foreign

operations taken to equity, the amount of foreign current translation reserve that have been

transferred to net profit and fair value adjustment on cash flow hedges (Hartnett & Romcke,

2015). There also exists net income tax items that have been transferred to income statement.

Insightful explanation of each item of Other Comprehensive Income Statement

The Net exchange differences from translation of foreign operation taken to

translation reserve drastically from 2016 which was $65 m in 2016 to -$16 m. Then comes

the remeasurements of defined benefit plans that is transferred to net profit on disposal of

controlled entities that has taken place on 2017 at $25 m. There has also been a fair value

adjustment on other comprehensive income from $ 33 m in 2016 to $ 9 m on 2017. The

income tax on items was $25m in 2016 then reduced to -$16m in 2017.The total of

comprehensive income amounts to $1014 m in 2017 which was $735 m in 2016.

Reasons for the items have not been reported in Income Statement/Profit and Loss

Statement

Comprehensive income statement is used for the measurement of any change in

interest of owners in business. It incorporates the income and expenses that have not been yet

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

realized and it is used for bypassing the income statement (Du Plessis, Hargovan, & Harris,

2018). Other comprehensive income takes into account items such as losses and gains from

derivative instruments, debt security on unrealized losses and gains, adjustments in foreign

currency transactions and retirement plans or any pension losses or gains (Henderson, et al.,

2015).

Clear description of your firm’s income tax expense

The current tax expense in the year 2017 amounted to -$329 m in 2017 as stated in the

financial statement. The amount has been increased from -$218 as on 2016. The tax was

calculated as income tax expense divided by profit before income tax expense from

discontinued operations and continuing operations (Beekes, Brown & Zhang, 2015).

Verification of the figure of tax being same as the company tax rate times the firm’s

accounting income

Income tax amount is computed using the tax rates that have been enacted

considerably by the financial position statement. The current tax expense in the year 2017

amounted to -$329 m in 2017 as stated in the financial statement. The amount has been

increased from -$218 m as on 2016. Therefore, it cannot be evaluated whether the figures of

income tax expenses are same as the tax rate times the accounting income (McClure, Lanis &

Govendir, 2017).

Deferred tax that is reported in the balance sheet along with the reasons for the record

The Deferred tax is accounted by the method of balance sheet asset resulting from

temporary differences between the tax bases of liabilities and assets and their carrying

amount in the financial statements (Devos & Zackrisson, 2015). Recognition of deferred tax

assets are done to the extent that the availability of taxable profit in future is probable against

CORPORATE ACCOUNTING

realized and it is used for bypassing the income statement (Du Plessis, Hargovan, & Harris,

2018). Other comprehensive income takes into account items such as losses and gains from

derivative instruments, debt security on unrealized losses and gains, adjustments in foreign

currency transactions and retirement plans or any pension losses or gains (Henderson, et al.,

2015).

Clear description of your firm’s income tax expense

The current tax expense in the year 2017 amounted to -$329 m in 2017 as stated in the

financial statement. The amount has been increased from -$218 as on 2016. The tax was

calculated as income tax expense divided by profit before income tax expense from

discontinued operations and continuing operations (Beekes, Brown & Zhang, 2015).

Verification of the figure of tax being same as the company tax rate times the firm’s

accounting income

Income tax amount is computed using the tax rates that have been enacted

considerably by the financial position statement. The current tax expense in the year 2017

amounted to -$329 m in 2017 as stated in the financial statement. The amount has been

increased from -$218 m as on 2016. Therefore, it cannot be evaluated whether the figures of

income tax expenses are same as the tax rate times the accounting income (McClure, Lanis &

Govendir, 2017).

Deferred tax that is reported in the balance sheet along with the reasons for the record

The Deferred tax is accounted by the method of balance sheet asset resulting from

temporary differences between the tax bases of liabilities and assets and their carrying

amount in the financial statements (Devos & Zackrisson, 2015). Recognition of deferred tax

assets are done to the extent that the availability of taxable profit in future is probable against

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

the temporary differences that are deductible. In current year, there has been deferred tax

assets are -$545 m in 2017 and $603 m in 2016.

Current tax assets or income tax payable recorded by the company

In Insurance Australia Group Limited the income tax assets amounts to $66 m in 2017

and $ 69.4m in 2016. The Income tax expenses is the amount that is calculated based on the

standard accounting rules and on the amount of tax that is owed by company to tax

authorities. Income tax payable is the amount that the company owes in terms of tax based on

tax code rules. Until the company makes the payment of tax, the amount of income tax

payable appears on the balance sheet section as liability (Carnegie & O’Connell, 2014).

Verification of the income tax expense shown in the income statement same as the

income tax paid shown in the cash flow statement

The income tax expense shown in the income statement is not same as the income tax

paid shown in the cash flow statement that amounts to $137 m in 2017 and $ 388 m in 2016

The Income tax payments includes the impact of income tax of certain loss or gain relating to

financing or investing activities so that after tax cash flow is reflected in the subtotals of net

cash flow. On other hand Income tax expense is the amount that represents the recording of

income tax costs (Barth, 2015). However, the expense for income tax under the income

statement generally varies with the income tax expenses mentioned in the cash flow

statement. The main reason for this is that the tax expenses accounted for by the company

under the income tax payable records the amount after accounting for various expenses like,

operating expenses, administrative expenses, selling expenses, financing charges and various

other expenses, if any. The income left after meeting all these expenses are taxed at the rate

of 30% as per the Australian tax code (Leong, 2015). On the other hand, the income tax

CORPORATE ACCOUNTING

the temporary differences that are deductible. In current year, there has been deferred tax

assets are -$545 m in 2017 and $603 m in 2016.

Current tax assets or income tax payable recorded by the company

In Insurance Australia Group Limited the income tax assets amounts to $66 m in 2017

and $ 69.4m in 2016. The Income tax expenses is the amount that is calculated based on the

standard accounting rules and on the amount of tax that is owed by company to tax

authorities. Income tax payable is the amount that the company owes in terms of tax based on

tax code rules. Until the company makes the payment of tax, the amount of income tax

payable appears on the balance sheet section as liability (Carnegie & O’Connell, 2014).

Verification of the income tax expense shown in the income statement same as the

income tax paid shown in the cash flow statement

The income tax expense shown in the income statement is not same as the income tax

paid shown in the cash flow statement that amounts to $137 m in 2017 and $ 388 m in 2016

The Income tax payments includes the impact of income tax of certain loss or gain relating to

financing or investing activities so that after tax cash flow is reflected in the subtotals of net

cash flow. On other hand Income tax expense is the amount that represents the recording of

income tax costs (Barth, 2015). However, the expense for income tax under the income

statement generally varies with the income tax expenses mentioned in the cash flow

statement. The main reason for this is that the tax expenses accounted for by the company

under the income tax payable records the amount after accounting for various expenses like,

operating expenses, administrative expenses, selling expenses, financing charges and various

other expenses, if any. The income left after meeting all these expenses are taxed at the rate

of 30% as per the Australian tax code (Leong, 2015). On the other hand, the income tax

8

CORPORATE ACCOUNTING

recorded under the cash flow statement is the taxes applicable on the operating activities of

the company (Sivathaasan, 2016).

Unique characteristics in the financial statements, new insights, and other information

From the annual report analysis of the Australian company of Insurance Australia

Group Limited, it has been identified that charge for current income tax is made on the basis

of the adjusted profits that are attributable for any disallowed or non-assessable items (Tran,

2015). Moreover, the current tax is measured by referencing the income tax payable amount

or recoverable amount with regard to the tax loss or taxable profit for the accounting year

(Balakrishnan, Watts & Zuo, 2016). It is computed through using the tax laws and tax rates

that is the substantively enacted or enacted at the reporting date. Therefore, the company

follows all the requirements of ATO (Australian tax office) while treating various taxes under

the financial statement (Hoopes, Robinson & Slemrod, 2018).

CORPORATE ACCOUNTING

recorded under the cash flow statement is the taxes applicable on the operating activities of

the company (Sivathaasan, 2016).

Unique characteristics in the financial statements, new insights, and other information

From the annual report analysis of the Australian company of Insurance Australia

Group Limited, it has been identified that charge for current income tax is made on the basis

of the adjusted profits that are attributable for any disallowed or non-assessable items (Tran,

2015). Moreover, the current tax is measured by referencing the income tax payable amount

or recoverable amount with regard to the tax loss or taxable profit for the accounting year

(Balakrishnan, Watts & Zuo, 2016). It is computed through using the tax laws and tax rates

that is the substantively enacted or enacted at the reporting date. Therefore, the company

follows all the requirements of ATO (Australian tax office) while treating various taxes under

the financial statement (Hoopes, Robinson & Slemrod, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

References

Balakrishnan, K., Watts, R., & Zuo, L. (2016). The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), 513-542.

Barth, M. E. (2015). Financial accounting research, practice, and financial

accountability. Abacus, 51(4), 499-510.

Beekes, W., Brown, P., & Zhang, Q. (2015). Corporate governance and the informativeness

of disclosures in Australia: A re‐examination. Accounting & Finance, 55(4), 931-963.

Carnegie, G. D., & O’Connell, B. T. (2014). A longitudinal study of the interplay of

corporate collapse, accounting failure and governance change in Australia: Early

1890s to early 2000s. Critical Perspectives on Accounting, 25(6), 446-468.

Devos, K., & Zackrisson, M. (2015). Tax compliance and the public disclosure of tax

information: An Australia/Norway comparison. eJournal of Tax Research, 13(1), 108.

Du Plessis, J. J., Hargovan, A., & Harris, J. (2018). Principles of contemporary corporate

governance. Cambridge University Press.

Duff, A. (2016). Corporate social responsibility reporting in professional accounting

firms. The British Accounting Review, 48(1), 74-86.

Goodwin, J., Atilgan, Y., Simsir, S. A., & Ahmed, K. (2017). Investor reaction to accounting

misstatements under IFRS: Australian evidence.

Hartnett, N., & Romcke, J. (2015). The predictability of management forecast error: a study

of Australian IPO disclosures.

CORPORATE ACCOUNTING

References

Balakrishnan, K., Watts, R., & Zuo, L. (2016). The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), 513-542.

Barth, M. E. (2015). Financial accounting research, practice, and financial

accountability. Abacus, 51(4), 499-510.

Beekes, W., Brown, P., & Zhang, Q. (2015). Corporate governance and the informativeness

of disclosures in Australia: A re‐examination. Accounting & Finance, 55(4), 931-963.

Carnegie, G. D., & O’Connell, B. T. (2014). A longitudinal study of the interplay of

corporate collapse, accounting failure and governance change in Australia: Early

1890s to early 2000s. Critical Perspectives on Accounting, 25(6), 446-468.

Devos, K., & Zackrisson, M. (2015). Tax compliance and the public disclosure of tax

information: An Australia/Norway comparison. eJournal of Tax Research, 13(1), 108.

Du Plessis, J. J., Hargovan, A., & Harris, J. (2018). Principles of contemporary corporate

governance. Cambridge University Press.

Duff, A. (2016). Corporate social responsibility reporting in professional accounting

firms. The British Accounting Review, 48(1), 74-86.

Goodwin, J., Atilgan, Y., Simsir, S. A., & Ahmed, K. (2017). Investor reaction to accounting

misstatements under IFRS: Australian evidence.

Hartnett, N., & Romcke, J. (2015). The predictability of management forecast error: a study

of Australian IPO disclosures.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Hoopes, J. L., Robinson, L., & Slemrod, J. (2018). Public tax-return disclosure (No.

w24318). National Bureau of Economic Research.

Leong, R. (2015). Structuring an undergraduate accounting theory course to enhance the

learning experience of Australian students: Preliminary findings.

McClure, R., Lanis, R., & Govendir, B. (2017). Analysis of Tax Avoidance Strategies of Top

Foreign Multinationals Operating in Australia: An Expose.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Sivathaasan, N. (2016). Corporate governance and leverage in Australia: A pitch. Journal of

Accounting and Management Information Systems, 15(4), 819-825.

Tran, A. (2015). Can Taxable Income Be Estimated from Financial Reports of Listed

Companies in Australia. Austl. Tax F., 30, 569.

CORPORATE ACCOUNTING

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Hoopes, J. L., Robinson, L., & Slemrod, J. (2018). Public tax-return disclosure (No.

w24318). National Bureau of Economic Research.

Leong, R. (2015). Structuring an undergraduate accounting theory course to enhance the

learning experience of Australian students: Preliminary findings.

McClure, R., Lanis, R., & Govendir, B. (2017). Analysis of Tax Avoidance Strategies of Top

Foreign Multinationals Operating in Australia: An Expose.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Sivathaasan, N. (2016). Corporate governance and leverage in Australia: A pitch. Journal of

Accounting and Management Information Systems, 15(4), 819-825.

Tran, A. (2015). Can Taxable Income Be Estimated from Financial Reports of Listed

Companies in Australia. Austl. Tax F., 30, 569.

11

CORPORATE ACCOUNTING

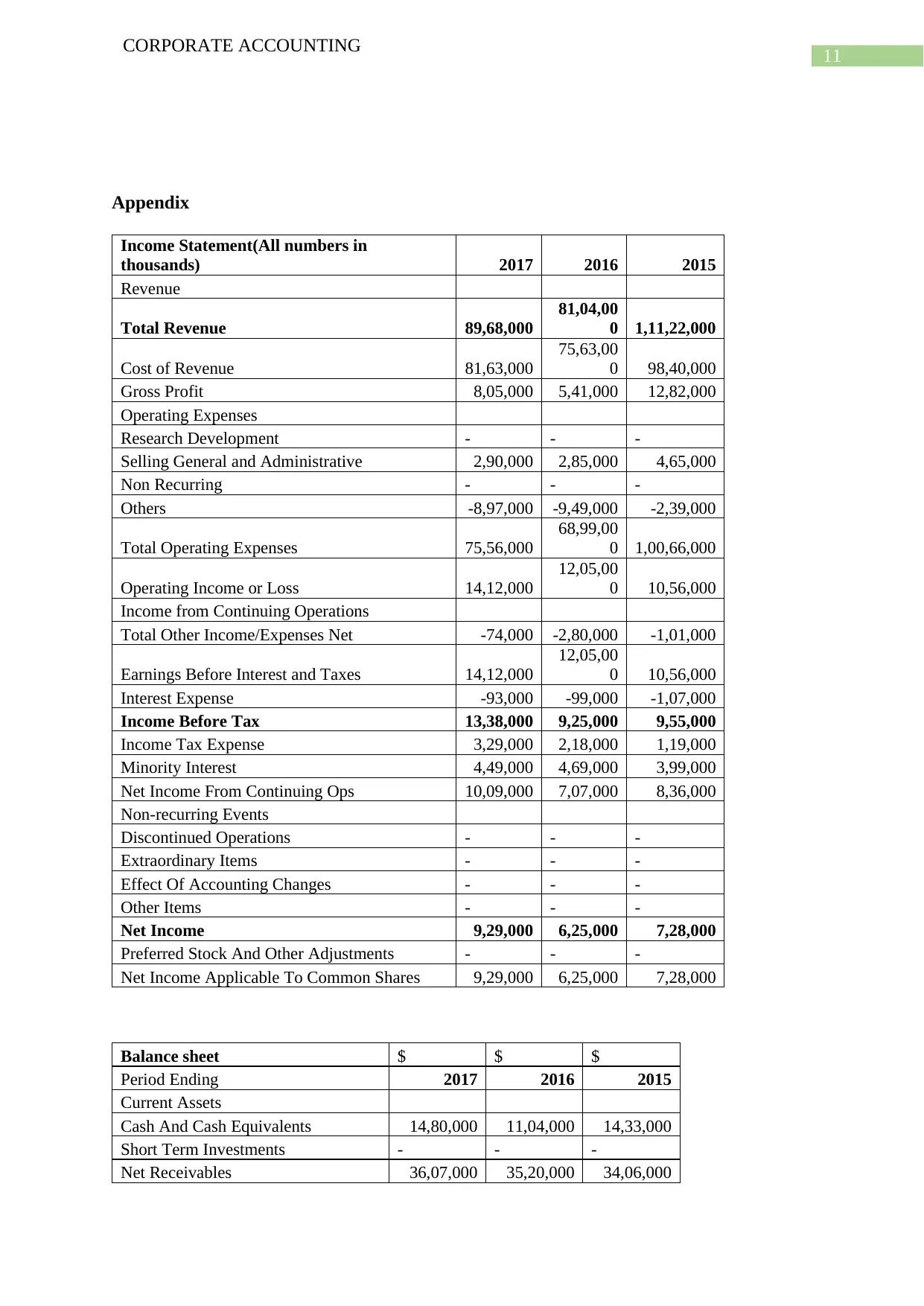

Appendix

Income Statement(All numbers in

thousands) 2017 2016 2015

Revenue

Total Revenue 89,68,000

81,04,00

0 1,11,22,000

Cost of Revenue 81,63,000

75,63,00

0 98,40,000

Gross Profit 8,05,000 5,41,000 12,82,000

Operating Expenses

Research Development - - -

Selling General and Administrative 2,90,000 2,85,000 4,65,000

Non Recurring - - -

Others -8,97,000 -9,49,000 -2,39,000

Total Operating Expenses 75,56,000

68,99,00

0 1,00,66,000

Operating Income or Loss 14,12,000

12,05,00

0 10,56,000

Income from Continuing Operations

Total Other Income/Expenses Net -74,000 -2,80,000 -1,01,000

Earnings Before Interest and Taxes 14,12,000

12,05,00

0 10,56,000

Interest Expense -93,000 -99,000 -1,07,000

Income Before Tax 13,38,000 9,25,000 9,55,000

Income Tax Expense 3,29,000 2,18,000 1,19,000

Minority Interest 4,49,000 4,69,000 3,99,000

Net Income From Continuing Ops 10,09,000 7,07,000 8,36,000

Non-recurring Events

Discontinued Operations - - -

Extraordinary Items - - -

Effect Of Accounting Changes - - -

Other Items - - -

Net Income 9,29,000 6,25,000 7,28,000

Preferred Stock And Other Adjustments - - -

Net Income Applicable To Common Shares 9,29,000 6,25,000 7,28,000

Balance sheet $ $ $

Period Ending 2017 2016 2015

Current Assets

Cash And Cash Equivalents 14,80,000 11,04,000 14,33,000

Short Term Investments - - -

Net Receivables 36,07,000 35,20,000 34,06,000

CORPORATE ACCOUNTING

Appendix

Income Statement(All numbers in

thousands) 2017 2016 2015

Revenue

Total Revenue 89,68,000

81,04,00

0 1,11,22,000

Cost of Revenue 81,63,000

75,63,00

0 98,40,000

Gross Profit 8,05,000 5,41,000 12,82,000

Operating Expenses

Research Development - - -

Selling General and Administrative 2,90,000 2,85,000 4,65,000

Non Recurring - - -

Others -8,97,000 -9,49,000 -2,39,000

Total Operating Expenses 75,56,000

68,99,00

0 1,00,66,000

Operating Income or Loss 14,12,000

12,05,00

0 10,56,000

Income from Continuing Operations

Total Other Income/Expenses Net -74,000 -2,80,000 -1,01,000

Earnings Before Interest and Taxes 14,12,000

12,05,00

0 10,56,000

Interest Expense -93,000 -99,000 -1,07,000

Income Before Tax 13,38,000 9,25,000 9,55,000

Income Tax Expense 3,29,000 2,18,000 1,19,000

Minority Interest 4,49,000 4,69,000 3,99,000

Net Income From Continuing Ops 10,09,000 7,07,000 8,36,000

Non-recurring Events

Discontinued Operations - - -

Extraordinary Items - - -

Effect Of Accounting Changes - - -

Other Items - - -

Net Income 9,29,000 6,25,000 7,28,000

Preferred Stock And Other Adjustments - - -

Net Income Applicable To Common Shares 9,29,000 6,25,000 7,28,000

Balance sheet $ $ $

Period Ending 2017 2016 2015

Current Assets

Cash And Cash Equivalents 14,80,000 11,04,000 14,33,000

Short Term Investments - - -

Net Receivables 36,07,000 35,20,000 34,06,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.