Analysis of Impairment of Assets and IAS 36 Accounting Standard

VerifiedAdded on 2020/03/04

|7

|2062

|48

Report

AI Summary

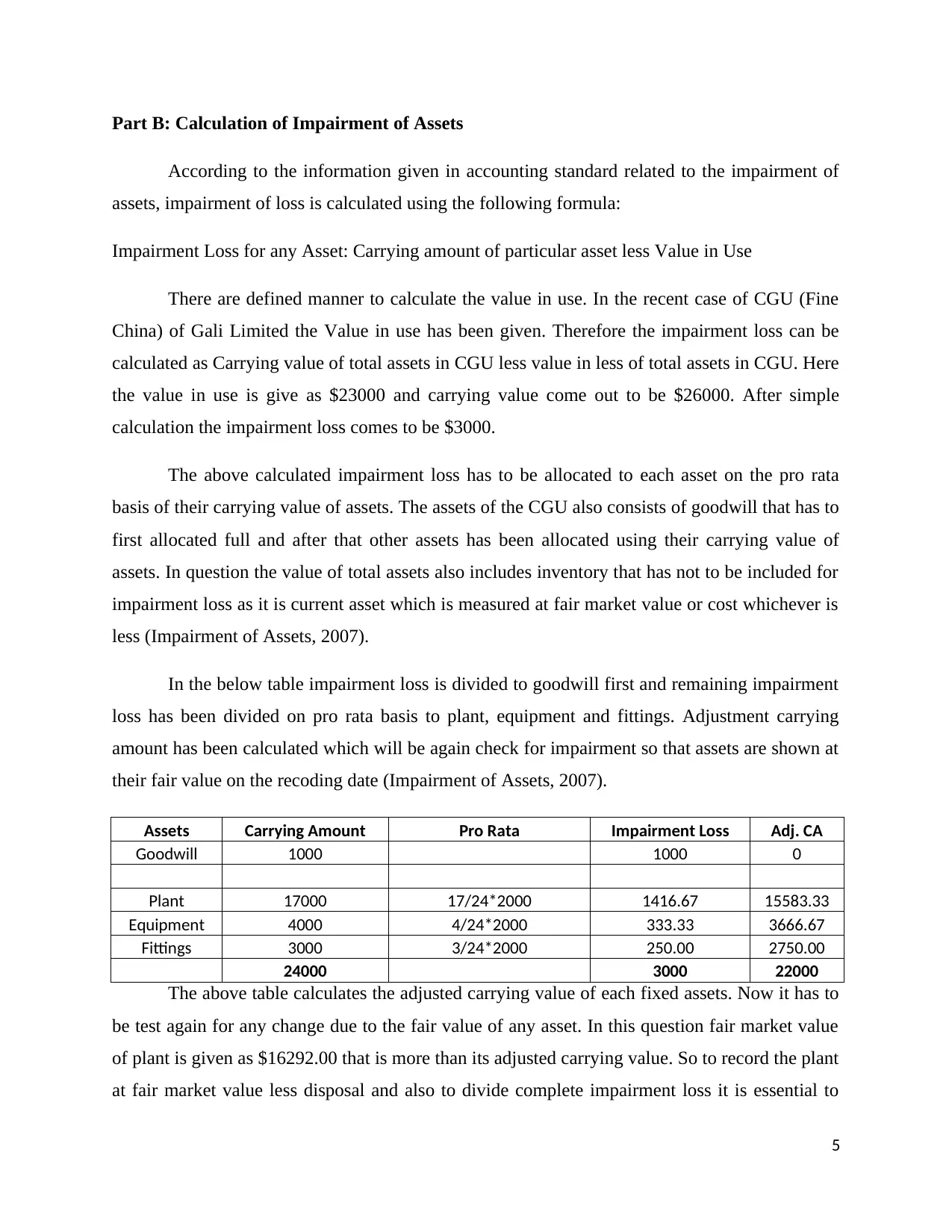

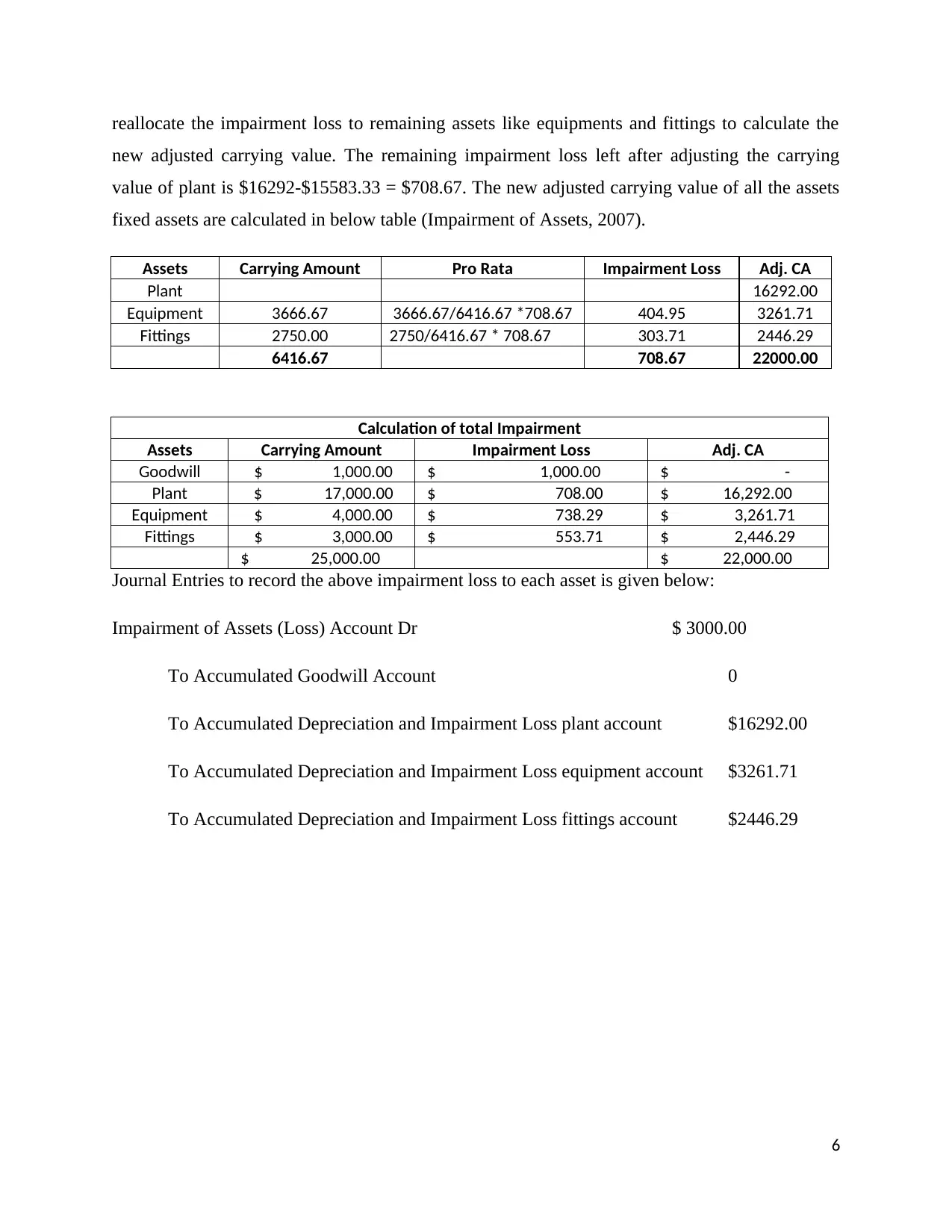

This report provides a comprehensive analysis of asset impairment, focusing on the IAS 36 accounting standard. Part A delves into the recognition and measurement of impairment losses for individual assets, defining key terms like carrying amount, recoverable amount, fair value, and value in use. It outlines the objective of IAS 36, which is to help organizations identify and account for damaged assets, ensuring assets are not valued higher than their recoverable amount. Part B presents a practical application of the standard, demonstrating the calculation of impairment losses for a Cash-Generating Unit (CGU), including the allocation of impairment to goodwill, plant, equipment, and fittings, and calculating the adjusted carrying values of these assets. The report includes journal entries to record the impairment loss and references to relevant accounting literature.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.