Analysis of Accounting Issues: IAS 8 and Exposure Drafts

VerifiedAdded on 2023/06/04

|15

|2300

|446

Report

AI Summary

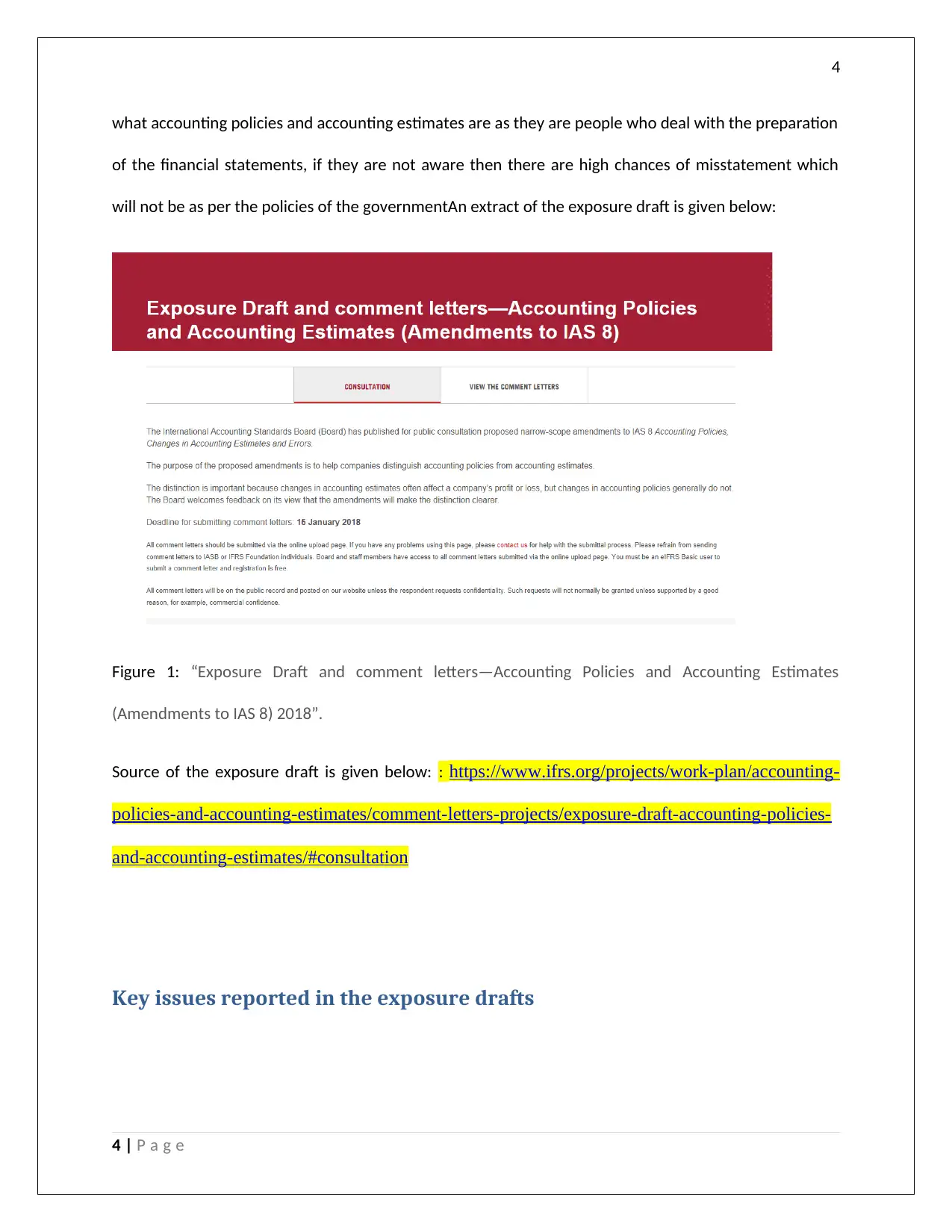

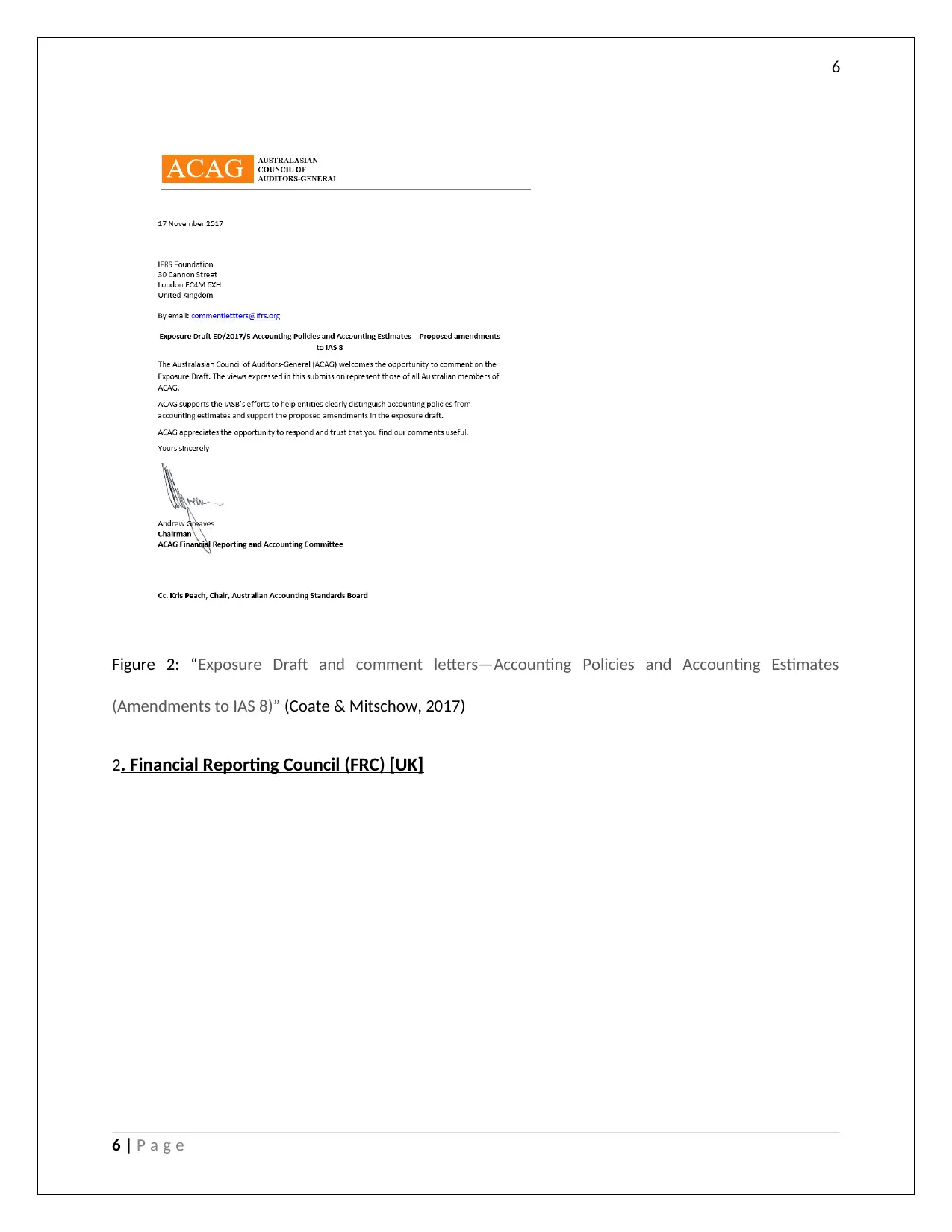

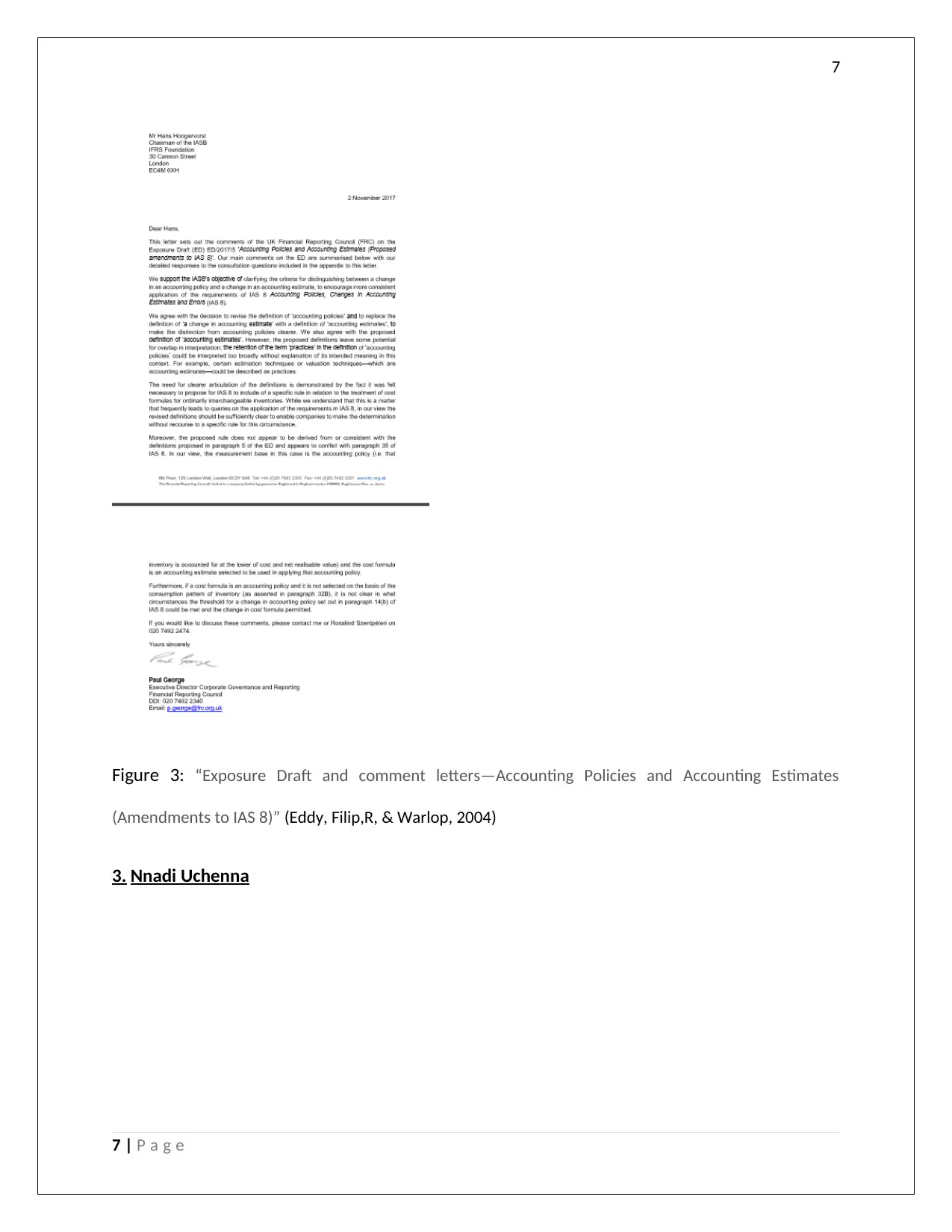

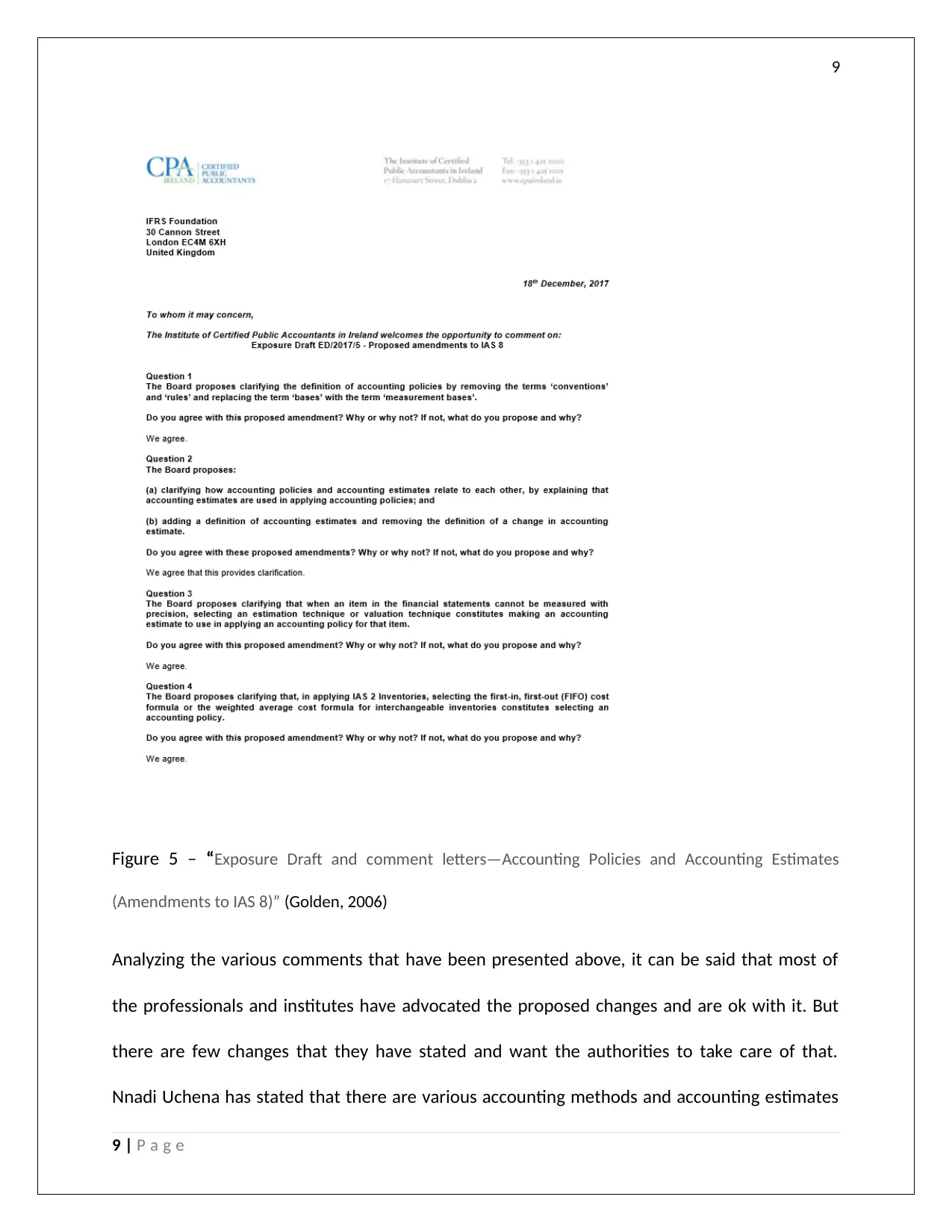

This report provides a detailed analysis of an assignment focused on an exposure draft related to IAS 8, concerning accounting policies, changes in accounting estimates, and errors. The assignment begins with an introduction to exposure drafts and their role in the accounting field, followed by an overview of the specific draft initiated in the context of IAS 8. The report then identifies key issues highlighted in the draft, such as the distinction between accounting estimates and accounting policies, and their implications for financial statements. It further examines the agreements and disagreements among professionals and institutions regarding the proposed changes. The report then explores arguments for and against the proposed regulations. Finally, it applies regulation theories, including public interest, private interest, and capture theory, to the context of the exposure draft, evaluating the underlying assumptions of these theories. The assignment concludes with a list of references used.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.