Comprehensive Report on Recoverable Amount Analysis - IAS 36/AASB 136

VerifiedAdded on 2023/06/12

|6

|1412

|426

Report

AI Summary

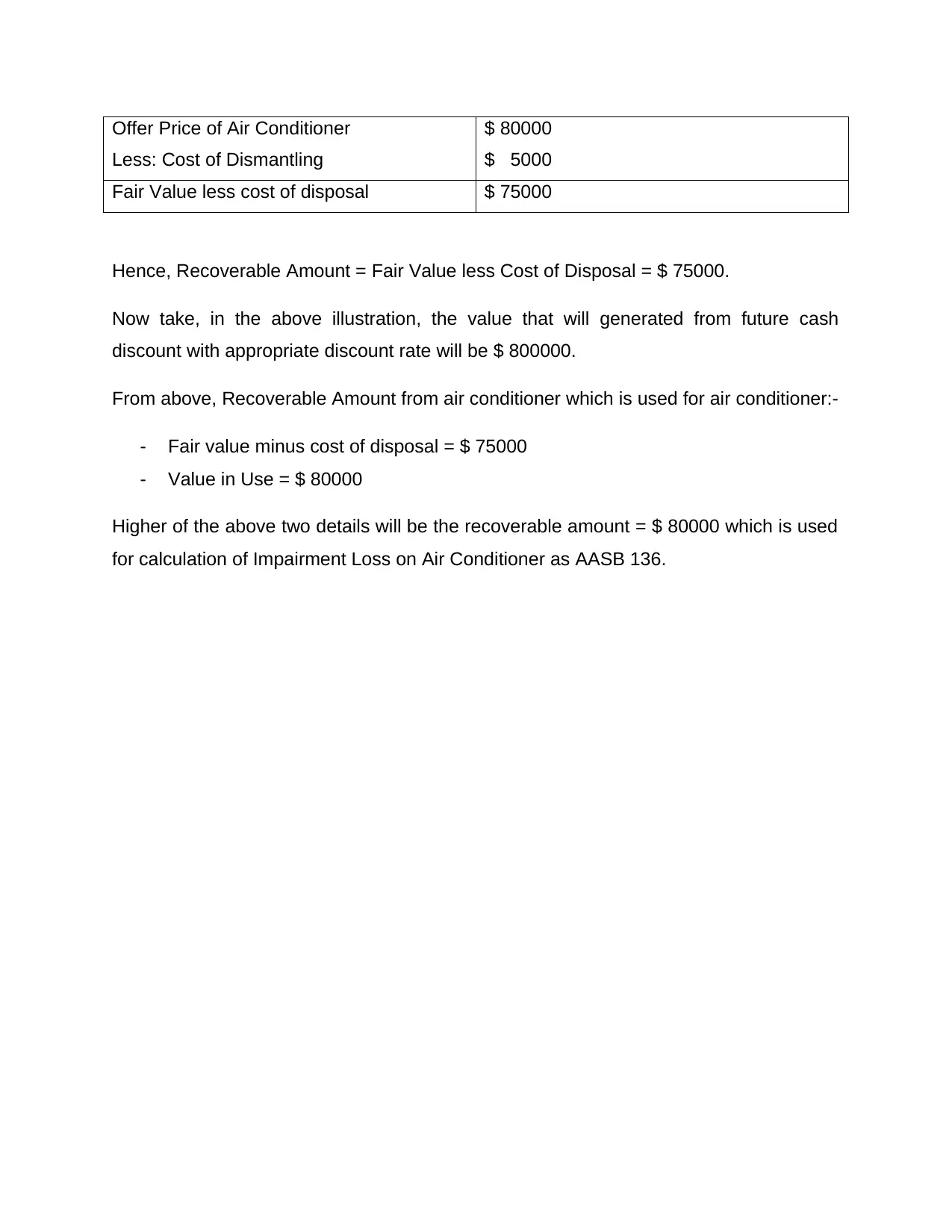

This report provides a detailed analysis of the concept of recoverable amount as defined under IAS 36 and AASB 136, which deal with the impairment of assets. It explains the significance of determining the recoverable amount for appropriately valuing non-current assets in financial statements. The report elaborates on how recoverable amount is calculated, emphasizing its role in impairment testing. It distinguishes between value in use (VIU) and fair value less cost of disposal, providing formulas and illustrations for calculating each. The document further explains fair value and cost of disposal, offering a practical example to demonstrate the calculation of net fair value and recoverable amount, highlighting the importance of these calculations in assessing impairment loss as per AASB 136. The report references relevant accounting standards and websites to support its analysis.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.