Content and Application of the IASB Conceptual Framework Report

VerifiedAdded on 2022/12/09

|10

|2213

|351

Report

AI Summary

This report provides a comprehensive overview of the IASB Conceptual Framework. It begins by outlining the framework's purpose, emphasizing its role in establishing accounting policies and resolving conflicts within existing standards. The report then delves into the content of the framework, detailing its objectives, fundamental principles, and qualitative characteristics used to evaluate financial statements. It also covers key concepts like recognition, measurement, and capital management. Finally, the report explores the application of the framework, demonstrating how its principles are applied to various financial transactions and the preparation of financial statements, ensuring fair and consistent reporting across different entities and industries. The report concludes by highlighting the significance of the IASB Conceptual Framework in promoting transparency and comparability in financial reporting.

WRITTEN REPORT: -

CONTENT AND

APPLICATION OF THE

IASB CONCEPTUAL

FRAMEWORK

CONTENT AND

APPLICATION OF THE

IASB CONCEPTUAL

FRAMEWORK

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION.....................................................................................................................................3

MAIN BODY.............................................................................................................................................3

Purpose of IASB Conceptual Framework................................................................................................3

Content of IASB Conceptual Framework................................................................................................4

Application of IASB Conceptual Framework..........................................................................................5

CONCLUSION..........................................................................................................................................5

REFERENCES..........................................................................................................................................6

APPENDICES...........................................................................................................................................6

INTRODUCTION.....................................................................................................................................3

MAIN BODY.............................................................................................................................................3

Purpose of IASB Conceptual Framework................................................................................................3

Content of IASB Conceptual Framework................................................................................................4

Application of IASB Conceptual Framework..........................................................................................5

CONCLUSION..........................................................................................................................................5

REFERENCES..........................................................................................................................................6

APPENDICES...........................................................................................................................................6

INTRODUCTION

The conceptual framework lays down the accounting policies that are to be followed by

the businesses in order to prepare their financial statements within the prescribed format and

presentation. These are developed by the International Accounting Standards Board which assists

and resolves conflicts over the existing accounting standards. This project shall be highlighting

the major purpose that is there for the formulation of these concepts and how this shall be

supporting the various organizations. Apart from that it also shows the contents that are

represented in the conceptual framework and are also to be shown in the financial statements of

the company. Further it demonstrates the application of these concepts in the preparation of the

financial statements thereby depicting true and fair view of the company.

MAIN BODY

Purpose of IASB Conceptual Framework

The International Accounting Standards Board (IASB) has developed the conceptual

framework which lays down the basics that needs to be used by the financial entities for the

purpose of financial reporting. This means that the conceptual framework assists in the

preparation of the financial statements and specifies the various accounting policies that are not

yet covered under the standards of accounting. Also on the basis of these policies under the

conceptual framework the IASB has been findings ways to develop the IFRS. So that the IFRS

can be used when there are conflicting theories under the conceptual framework.

The most significant purpose of conceptual framework is that it shows the way to apply

the various accounting standards that are formed to prepare the financial reports. These financial

reports are significant to the company in order to disclose their financial health and well-being in

front of the various users of such information (Van Mourik and Katsuo Asami, 2018). This helps

in maintaining the consistency among all the entities as they follow the similar formats,

accounting standards, policies to support the recording of the transactions. Also the conceptual

framework has been playing major role in solving the various accounting conflicts that arise due

to lack of availability of the standards of accounting. There are several events or the business

transactions regarding which proper information or explanations are not provided under the

prescribed accounting standards, the clarifications regarding that are also provided under the

conceptual framework that is developed by IASB authorities.

One of the most advantageous purpose that is solved by this conceptual framework is that

it has created a universal way of preparing the financial statements and so all the similar

accounting transactions are treated in similar manner by all the financial entities. This has also

facilitated the process of comparative analysis among the various business competitors in the

market or the inter departmental comparisons to grow the profitable segments and shut down the

loss making ventures of the business (Walton, 2018). It has also sorted to develop and highlight

the national and the international accounting standards of the company that can provide

assistance and support to the financial managers.

The development of the conceptual framework and the universally accepted principles

has solved one more purpose of the internal and the external users of the financial information

The conceptual framework lays down the accounting policies that are to be followed by

the businesses in order to prepare their financial statements within the prescribed format and

presentation. These are developed by the International Accounting Standards Board which assists

and resolves conflicts over the existing accounting standards. This project shall be highlighting

the major purpose that is there for the formulation of these concepts and how this shall be

supporting the various organizations. Apart from that it also shows the contents that are

represented in the conceptual framework and are also to be shown in the financial statements of

the company. Further it demonstrates the application of these concepts in the preparation of the

financial statements thereby depicting true and fair view of the company.

MAIN BODY

Purpose of IASB Conceptual Framework

The International Accounting Standards Board (IASB) has developed the conceptual

framework which lays down the basics that needs to be used by the financial entities for the

purpose of financial reporting. This means that the conceptual framework assists in the

preparation of the financial statements and specifies the various accounting policies that are not

yet covered under the standards of accounting. Also on the basis of these policies under the

conceptual framework the IASB has been findings ways to develop the IFRS. So that the IFRS

can be used when there are conflicting theories under the conceptual framework.

The most significant purpose of conceptual framework is that it shows the way to apply

the various accounting standards that are formed to prepare the financial reports. These financial

reports are significant to the company in order to disclose their financial health and well-being in

front of the various users of such information (Van Mourik and Katsuo Asami, 2018). This helps

in maintaining the consistency among all the entities as they follow the similar formats,

accounting standards, policies to support the recording of the transactions. Also the conceptual

framework has been playing major role in solving the various accounting conflicts that arise due

to lack of availability of the standards of accounting. There are several events or the business

transactions regarding which proper information or explanations are not provided under the

prescribed accounting standards, the clarifications regarding that are also provided under the

conceptual framework that is developed by IASB authorities.

One of the most advantageous purpose that is solved by this conceptual framework is that

it has created a universal way of preparing the financial statements and so all the similar

accounting transactions are treated in similar manner by all the financial entities. This has also

facilitated the process of comparative analysis among the various business competitors in the

market or the inter departmental comparisons to grow the profitable segments and shut down the

loss making ventures of the business (Walton, 2018). It has also sorted to develop and highlight

the national and the international accounting standards of the company that can provide

assistance and support to the financial managers.

The development of the conceptual framework and the universally accepted principles

has solved one more purpose of the internal and the external users of the financial information

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which is that they have developed the idea to compare and contrast the statements of entities and

post that form interpretations and judgements and formulate the decisions. It can also be used by

the auditors to form their opinion regarding the true and fair view of the financial statements and

that the representations are free from the material misstatements.

These are some of the major purposes for which the conceptual framework has been

created by the IASB and is been assisting and supporting in the preparation of the financial

statements by the various business entities so that the full disclosure can be made and the current

status and stature of the company can be known by the investors for the business (Kabir and

Rahman, 2018).

Content of IASB Conceptual Framework

The conceptual framework that is developed by the IASB has the contents related to the

accounting policies that are in support of the already established accounting standards that are

used by the company in the process of effective financial reporting. It has been highlighting the

basic objectives of accounting, the fundamental principles that are to be followed in the

accounting, accounting concepts like the recognition, measurement etc. that are to e followed

while deriving the financial results for the company. It also contains the qualitative aspects and

characters that are used to evaluate the financial statements and the information pertaining to it.

It also includes the various concepts related to the capital of the company, its acquisition

and utilization in the various financial activities (Gornik-Tomaszewski and Choi, 2018). Apart

from that how is it managed to conduct the capital appraisal in the entity and capitalized through

the utilization of the funds. One of the important contents in the conceptual framework as

developed by IASB is that it shows the disclosure policy regarding the material information that

the company needs to disclose in front of the users to financial statements to provide them with a

true and fair view of the current status of the entity. Further the guidelines have been issued in

relation to presentations that are to be made in respect of financial information, also the footnotes

that are to maintained, the different statements like balance sheet, income statement, cash flow

statement and changes in equity statement. The presentation that is affixed universally by this

conceptual framework facilitates comparison horizontally and vertically within the organization

as well as outside the organization.

Further it can be assessed that the contents of conceptual framework are also associated

with the issues that are not catered by the accounting standards that have been established prior

to this. There are many events, financial transactions, situations which re still untouched by the

accounting standards but which are met by these conceptual framework (Craig, Smieliauskas and

Amernic, 2017). Moreover there are even accounting conflicts that arise due to lack of

information but then are further resolved by these conceptual understandings. The content can

also be referred to by these authorities like IASB for future reference in deriving the IFRS and

modifications in the existing set of accounting standards.

post that form interpretations and judgements and formulate the decisions. It can also be used by

the auditors to form their opinion regarding the true and fair view of the financial statements and

that the representations are free from the material misstatements.

These are some of the major purposes for which the conceptual framework has been

created by the IASB and is been assisting and supporting in the preparation of the financial

statements by the various business entities so that the full disclosure can be made and the current

status and stature of the company can be known by the investors for the business (Kabir and

Rahman, 2018).

Content of IASB Conceptual Framework

The conceptual framework that is developed by the IASB has the contents related to the

accounting policies that are in support of the already established accounting standards that are

used by the company in the process of effective financial reporting. It has been highlighting the

basic objectives of accounting, the fundamental principles that are to be followed in the

accounting, accounting concepts like the recognition, measurement etc. that are to e followed

while deriving the financial results for the company. It also contains the qualitative aspects and

characters that are used to evaluate the financial statements and the information pertaining to it.

It also includes the various concepts related to the capital of the company, its acquisition

and utilization in the various financial activities (Gornik-Tomaszewski and Choi, 2018). Apart

from that how is it managed to conduct the capital appraisal in the entity and capitalized through

the utilization of the funds. One of the important contents in the conceptual framework as

developed by IASB is that it shows the disclosure policy regarding the material information that

the company needs to disclose in front of the users to financial statements to provide them with a

true and fair view of the current status of the entity. Further the guidelines have been issued in

relation to presentations that are to be made in respect of financial information, also the footnotes

that are to maintained, the different statements like balance sheet, income statement, cash flow

statement and changes in equity statement. The presentation that is affixed universally by this

conceptual framework facilitates comparison horizontally and vertically within the organization

as well as outside the organization.

Further it can be assessed that the contents of conceptual framework are also associated

with the issues that are not catered by the accounting standards that have been established prior

to this. There are many events, financial transactions, situations which re still untouched by the

accounting standards but which are met by these conceptual framework (Craig, Smieliauskas and

Amernic, 2017). Moreover there are even accounting conflicts that arise due to lack of

information but then are further resolved by these conceptual understandings. The content can

also be referred to by these authorities like IASB for future reference in deriving the IFRS and

modifications in the existing set of accounting standards.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Therefore it can be ascertained that the contents of this framework has been very helpful

in the preparation of the financial statements and indicating the financial position of the

company.

Application of IASB Conceptual Framework

The application of these accounting policies and procedures are based on the type of the

financial transactions that are undertaken in a particular entity and based on that the relevant

concept of accounting and its presentation shall be applied to generate the reasonable financial

statements of the business. These concepts are applied by all the profit making, non profit or any

other specific type of business which is preparing the books of accounts and the various type of

statement to disclose the financial results in the market. The application is similar for all the

users and therefore makes its presentation similar and simple to understand. It can also be

assessed that majority of its application is in the case where the relevant accounting standards

have not yet been decided.

Further the application is based on the fundamental concepts like recognition, de-

recognition and the measurement concept. Also apart from that there are qualitative

characteristics that are likely to assess the financial position of the business (Pelger, 2020). The

valuation concepts like inventory valuation, fixed asset pricing, method of depreciation etc.

which can only be manipulated if it is prudent to so in respect of the business development.

The application is also in terms of separate presentation of all the results like the financial

position, liquidity position, profitability position and change in the equity. The separate

statements show separate results and are formulated from different perspectives for the different

groups of users.

Therefore it has been ascertained that this application has been meaningful for the

company and generation of its financial statements so as to drive fair analysis and also

synchronization among the various competitors businesses in the market place.

CONCLUSION

It can be summarized from the above project that the internationally acceptable

accounting policies and principles are the key to the preparation of the financial statements by

the various entities. They must be prepared following the full disclosure policy which states that

all the material information to the statement of accounts must be presented in front of the users

which is capable of altering the financial decision. It has been seen that these work in support to

the accounting standards which are the base for the treatment of any business transaction. It can

further be noticed that they are multi purpose can solve various accounting conflicts.

Significantly it has been universally accepted and so internationally businesses can be flourished

using these principles.

in the preparation of the financial statements and indicating the financial position of the

company.

Application of IASB Conceptual Framework

The application of these accounting policies and procedures are based on the type of the

financial transactions that are undertaken in a particular entity and based on that the relevant

concept of accounting and its presentation shall be applied to generate the reasonable financial

statements of the business. These concepts are applied by all the profit making, non profit or any

other specific type of business which is preparing the books of accounts and the various type of

statement to disclose the financial results in the market. The application is similar for all the

users and therefore makes its presentation similar and simple to understand. It can also be

assessed that majority of its application is in the case where the relevant accounting standards

have not yet been decided.

Further the application is based on the fundamental concepts like recognition, de-

recognition and the measurement concept. Also apart from that there are qualitative

characteristics that are likely to assess the financial position of the business (Pelger, 2020). The

valuation concepts like inventory valuation, fixed asset pricing, method of depreciation etc.

which can only be manipulated if it is prudent to so in respect of the business development.

The application is also in terms of separate presentation of all the results like the financial

position, liquidity position, profitability position and change in the equity. The separate

statements show separate results and are formulated from different perspectives for the different

groups of users.

Therefore it has been ascertained that this application has been meaningful for the

company and generation of its financial statements so as to drive fair analysis and also

synchronization among the various competitors businesses in the market place.

CONCLUSION

It can be summarized from the above project that the internationally acceptable

accounting policies and principles are the key to the preparation of the financial statements by

the various entities. They must be prepared following the full disclosure policy which states that

all the material information to the statement of accounts must be presented in front of the users

which is capable of altering the financial decision. It has been seen that these work in support to

the accounting standards which are the base for the treatment of any business transaction. It can

further be noticed that they are multi purpose can solve various accounting conflicts.

Significantly it has been universally accepted and so internationally businesses can be flourished

using these principles.

REFERENCES

Van Mourik, C. and Katsuo Asami, Y., 2018. Articulation, profit or loss and OCI in the IASB

conceptual framework: Different shades of clean (or dirty) surplus. Accounting in Europe. 15(2).

pp.167-192.

Walton, P., 2018. Discussion of barker and Teixeira ([2018]. Gaps in the IFRS conceptual

framework. Accounting in Europe, 15) and Van Mourik and Katsuo ([2018]. Profit or loss in the

IASB conceptual framework. Accounting in Europe, 15). Accounting in Europe. 15(2). pp.193-

199.

Kabir, H. and Rahman, A., 2018. How Does the IASB Use the Conceptual Framework in

Developing IFRSs? An Examination of the Development of IFRS 16 Leases. Journal of

Financial Reporting. 3(1). pp.93-116.

Gornik-Tomaszewski, S. and Choi, Y. C., 2018. The conceptual framework: past, present, and

future. Review of Business. 38(1). pp.47-58.

Craig, R., Smieliauskas, W. and Amernic, J., 2017. Estimation uncertainty and the IASB’s

proposed conceptual framework. Australian Accounting Review. 27(1). pp.112-114.

Pelger, C., 2020. The Return of Stewardship, Reliability and Prudence–A Commentary on the

IASB’s New Conceptual Framework. Accounting in Europe. 17(1). pp.33-51.

APPENDICES

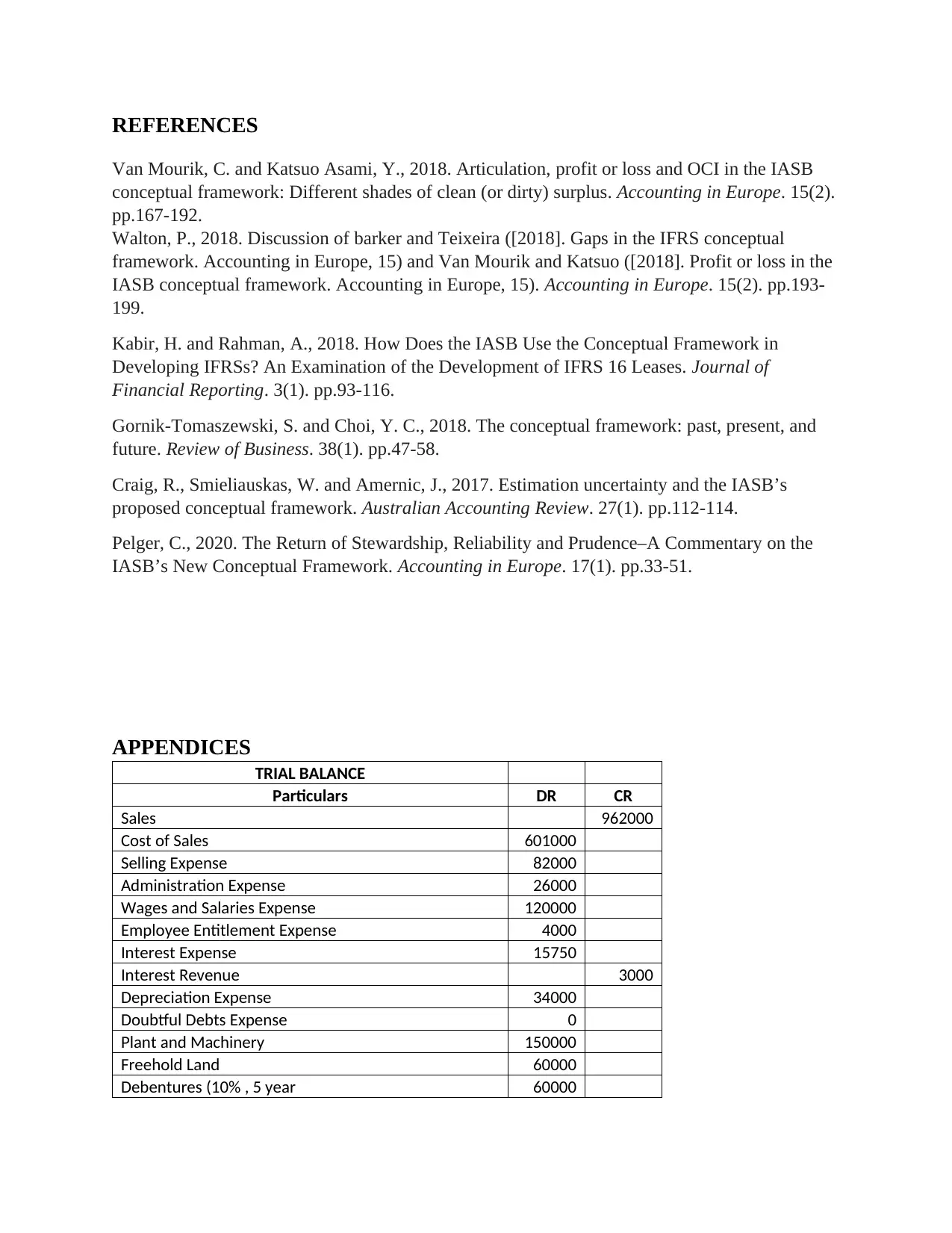

TRIAL BALANCE

Particulars DR CR

Sales 962000

Cost of Sales 601000

Selling Expense 82000

Administration Expense 26000

Wages and Salaries Expense 120000

Employee Entitlement Expense 4000

Interest Expense 15750

Interest Revenue 3000

Depreciation Expense 34000

Doubtful Debts Expense 0

Plant and Machinery 150000

Freehold Land 60000

Debentures (10% , 5 year 60000

Van Mourik, C. and Katsuo Asami, Y., 2018. Articulation, profit or loss and OCI in the IASB

conceptual framework: Different shades of clean (or dirty) surplus. Accounting in Europe. 15(2).

pp.167-192.

Walton, P., 2018. Discussion of barker and Teixeira ([2018]. Gaps in the IFRS conceptual

framework. Accounting in Europe, 15) and Van Mourik and Katsuo ([2018]. Profit or loss in the

IASB conceptual framework. Accounting in Europe, 15). Accounting in Europe. 15(2). pp.193-

199.

Kabir, H. and Rahman, A., 2018. How Does the IASB Use the Conceptual Framework in

Developing IFRSs? An Examination of the Development of IFRS 16 Leases. Journal of

Financial Reporting. 3(1). pp.93-116.

Gornik-Tomaszewski, S. and Choi, Y. C., 2018. The conceptual framework: past, present, and

future. Review of Business. 38(1). pp.47-58.

Craig, R., Smieliauskas, W. and Amernic, J., 2017. Estimation uncertainty and the IASB’s

proposed conceptual framework. Australian Accounting Review. 27(1). pp.112-114.

Pelger, C., 2020. The Return of Stewardship, Reliability and Prudence–A Commentary on the

IASB’s New Conceptual Framework. Accounting in Europe. 17(1). pp.33-51.

APPENDICES

TRIAL BALANCE

Particulars DR CR

Sales 962000

Cost of Sales 601000

Selling Expense 82000

Administration Expense 26000

Wages and Salaries Expense 120000

Employee Entitlement Expense 4000

Interest Expense 15750

Interest Revenue 3000

Depreciation Expense 34000

Doubtful Debts Expense 0

Plant and Machinery 150000

Freehold Land 60000

Debentures (10% , 5 year 60000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

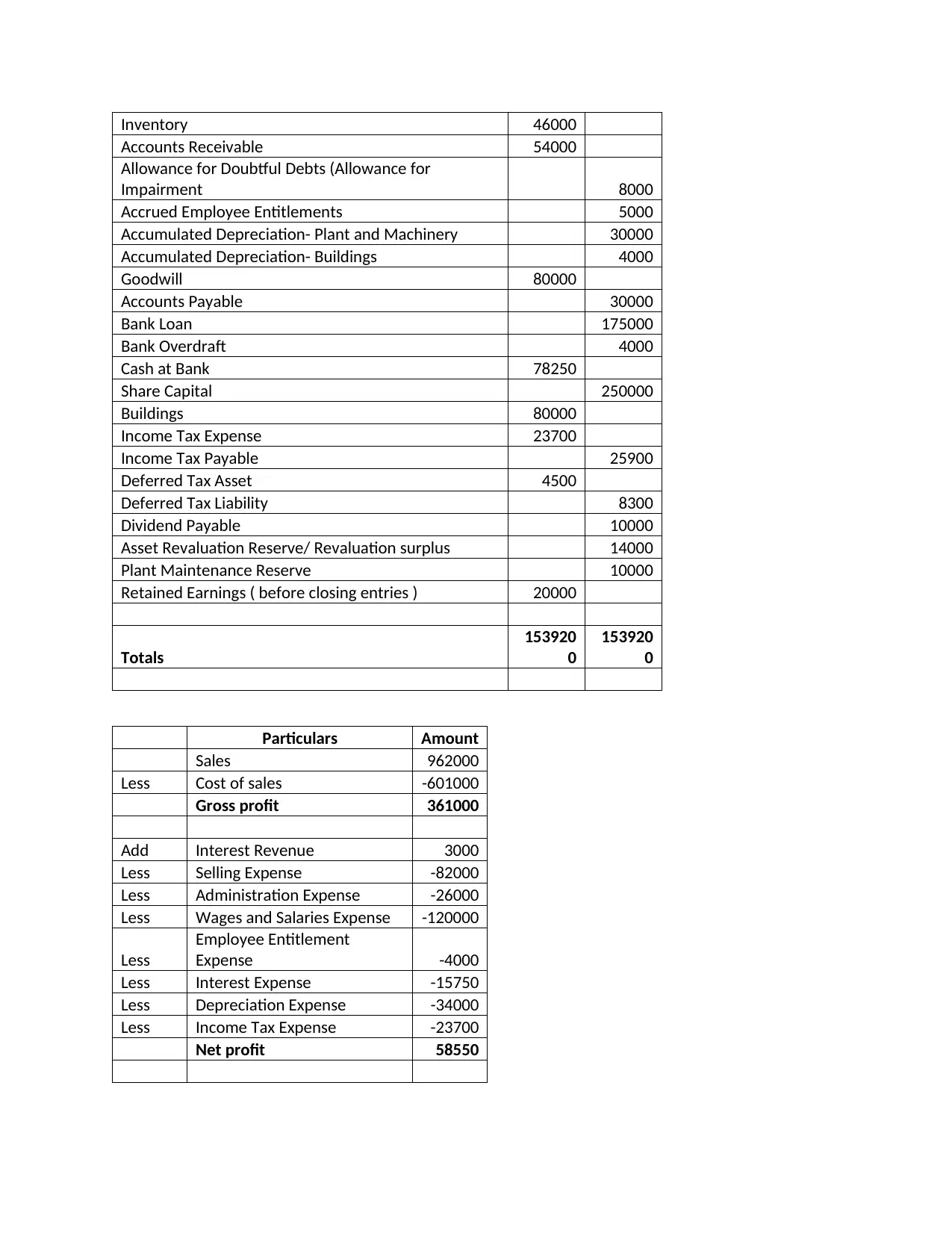

Inventory 46000

Accounts Receivable 54000

Allowance for Doubtful Debts (Allowance for

Impairment 8000

Accrued Employee Entitlements 5000

Accumulated Depreciation- Plant and Machinery 30000

Accumulated Depreciation- Buildings 4000

Goodwill 80000

Accounts Payable 30000

Bank Loan 175000

Bank Overdraft 4000

Cash at Bank 78250

Share Capital 250000

Buildings 80000

Income Tax Expense 23700

Income Tax Payable 25900

Deferred Tax Asset 4500

Deferred Tax Liability 8300

Dividend Payable 10000

Asset Revaluation Reserve/ Revaluation surplus 14000

Plant Maintenance Reserve 10000

Retained Earnings ( before closing entries ) 20000

Totals

153920

0

153920

0

Particulars Amount

Sales 962000

Less Cost of sales -601000

Gross profit 361000

Add Interest Revenue 3000

Less Selling Expense -82000

Less Administration Expense -26000

Less Wages and Salaries Expense -120000

Less

Employee Entitlement

Expense -4000

Less Interest Expense -15750

Less Depreciation Expense -34000

Less Income Tax Expense -23700

Net profit 58550

Accounts Receivable 54000

Allowance for Doubtful Debts (Allowance for

Impairment 8000

Accrued Employee Entitlements 5000

Accumulated Depreciation- Plant and Machinery 30000

Accumulated Depreciation- Buildings 4000

Goodwill 80000

Accounts Payable 30000

Bank Loan 175000

Bank Overdraft 4000

Cash at Bank 78250

Share Capital 250000

Buildings 80000

Income Tax Expense 23700

Income Tax Payable 25900

Deferred Tax Asset 4500

Deferred Tax Liability 8300

Dividend Payable 10000

Asset Revaluation Reserve/ Revaluation surplus 14000

Plant Maintenance Reserve 10000

Retained Earnings ( before closing entries ) 20000

Totals

153920

0

153920

0

Particulars Amount

Sales 962000

Less Cost of sales -601000

Gross profit 361000

Add Interest Revenue 3000

Less Selling Expense -82000

Less Administration Expense -26000

Less Wages and Salaries Expense -120000

Less

Employee Entitlement

Expense -4000

Less Interest Expense -15750

Less Depreciation Expense -34000

Less Income Tax Expense -23700

Net profit 58550

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Amount

ASSETS

Fixed Assets

Plant and Machinery 150000 120000

Less Accumulated Depreciation- Plant and Machinery -30000

Freehold Land 60000

Debentures (10% , 5 year 60000

Buildings 80000 76000

Less Accumulated Depreciation- Buildings -4000

Goodwill 80000

Current Assets

Inventory 46000

Accounts Receivable 54000

Cash at Bank 78250

Retained Earnings ( before closing entries ) 20000

Deferred Tax Asset 4500

Total Assets 598750

LIABILITIES

Non-current liabilities

Bank Loan 175000

Current liabilities

Allowance for Doubtful Debts (Allowance for Impairment 8000

Accrued Employee Entitlements 5000

Accounts Payable 30000

Bank Overdraft 4000

Income Tax Payable 25900

Deferred Tax Liability 8300

Dividend Payable 10000

Share capital

Share Capital 250000

Asset Revaluation Reserve/ Revaluation surplus 14000

Plant Maintenance Reserve 10000

Net profit 58550

Total liabilities 598750

Share capital

Share Capital 250000

Asset Revaluation Reserve/ Revaluation surplus 14000

Plant Maintenance Reserve 10000

Net profit 58550

Total Shareholder’s equity 332550

Fixed Assets

Plant and Machinery 150000 120000

Less Accumulated Depreciation- Plant and Machinery -30000

Freehold Land 60000

Debentures (10% , 5 year 60000

Buildings 80000 76000

Less Accumulated Depreciation- Buildings -4000

Goodwill 80000

Current Assets

Inventory 46000

Accounts Receivable 54000

Cash at Bank 78250

Retained Earnings ( before closing entries ) 20000

Deferred Tax Asset 4500

Total Assets 598750

LIABILITIES

Non-current liabilities

Bank Loan 175000

Current liabilities

Allowance for Doubtful Debts (Allowance for Impairment 8000

Accrued Employee Entitlements 5000

Accounts Payable 30000

Bank Overdraft 4000

Income Tax Payable 25900

Deferred Tax Liability 8300

Dividend Payable 10000

Share capital

Share Capital 250000

Asset Revaluation Reserve/ Revaluation surplus 14000

Plant Maintenance Reserve 10000

Net profit 58550

Total liabilities 598750

Share capital

Share Capital 250000

Asset Revaluation Reserve/ Revaluation surplus 14000

Plant Maintenance Reserve 10000

Net profit 58550

Total Shareholder’s equity 332550

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.