ICAI's Detailed Response to IASB Exposure Draft on Onerous Contracts

VerifiedAdded on 2022/11/14

|3

|612

|185

Report

AI Summary

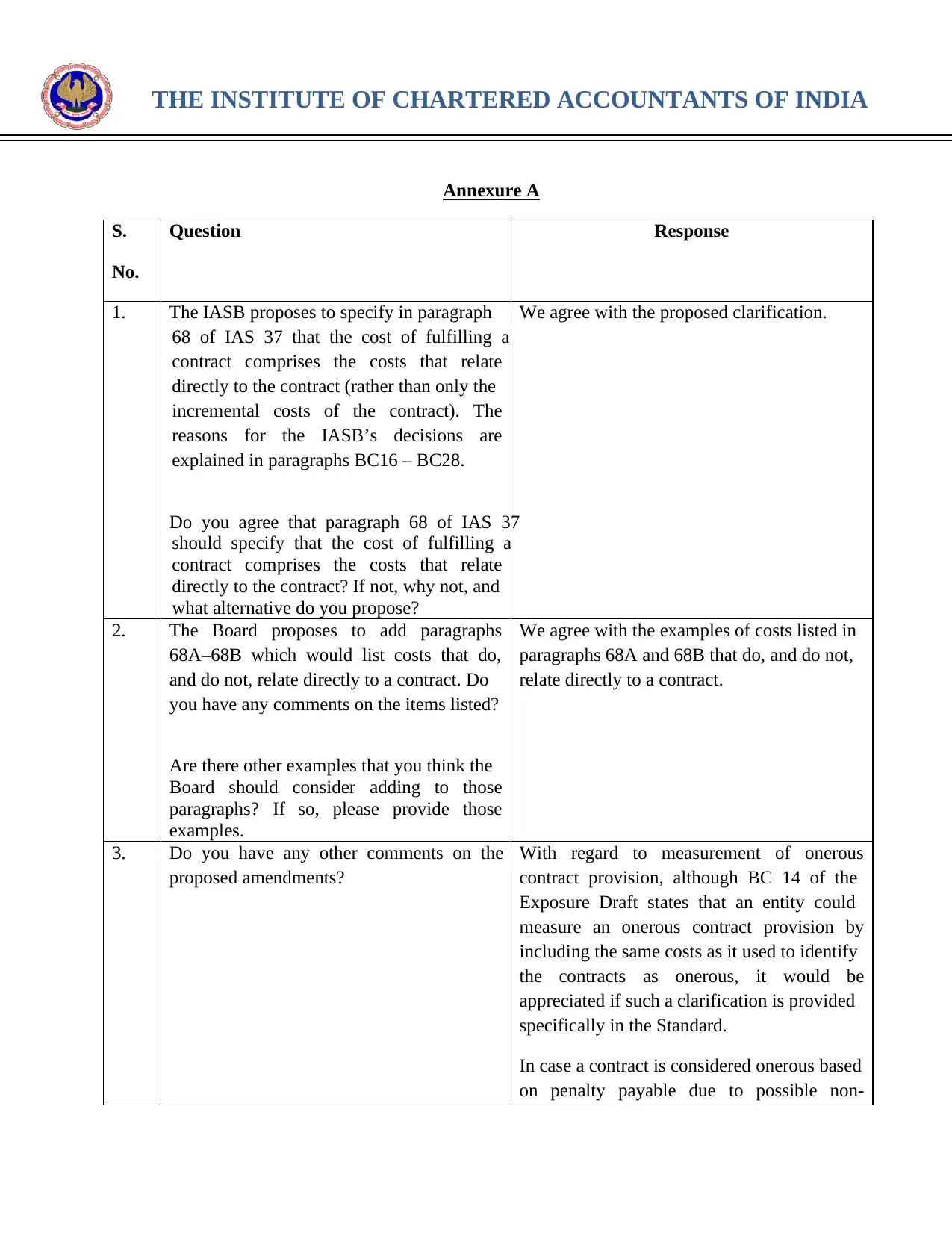

This document presents the comments of The Institute of Chartered Accountants of India (ICAI) on the International Accounting Standards Board's (IASB) Exposure Draft 'Onerous Contracts- Cost of fulfilling a contract - Proposed amendments to IAS 37'. The ICAI broadly agrees with the proposed clarifications and provides detailed responses to specific questions raised in the Exposure Draft. The document highlights the applicability of Ind AS Standards in India, which are converged with IFRS, and provides an annexure with a structured response to the IASB's queries. The ICAI's comments cover aspects like the definition of costs directly related to a contract, examples of such costs, and considerations for measuring onerous contract provisions, including whether economic benefits should be considered zero in cases of penalties for non-fulfillment. The document emphasizes the due process followed by the ICAI, including stakeholder consultations, in formulating its response. The ICAI's response aims to provide clarity and contribute to the refinement of the IASB's proposed amendments to IAS 37.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.