Implications of IFRS 16 on Lease Accounting and Financial Ratios

VerifiedAdded on 2020/05/16

|15

|3015

|48

AI Summary

The adoption of International Financial Reporting Standards (IFRS) is a significant move in the world of international finance, aimed at enhancing financial transparency and comparability across borders. This analysis explores the various advantages such as increased consistency, investor confidence, and streamlined reporting processes that IFRS brings to global markets. However, it also delves into the challenges faced during adoption, including implementation costs, training needs for accounting professionals, and variations in legal environments. The convergence towards a single set of global standards is a complex process requiring coordination among nations with diverse economic backgrounds. This study further investigates how IFRS impacts financial reporting, corporate governance, and market efficiency. By analyzing different case studies and scholarly articles, such as those by Bhat et al. (2014) and Florou & Kosi (2015), the assignment provides a comprehensive understanding of the implications of IFRS adoption for businesses, investors, and regulators worldwide.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced financial accounting

Name of the university

Name of the student

Authors note

Advanced financial accounting

Name of the university

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Part A:..............................................................................................................................................3

Requirement i).................................................................................................................................3

Requirement ii)................................................................................................................................3

Requirement iii)...............................................................................................................................3

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................3

Requirement vii)..............................................................................................................................3

Requirement viii).............................................................................................................................3

Part B:..............................................................................................................................................4

Requirement i).................................................................................................................................4

Requirement ii)................................................................................................................................4

Requirement iii)...............................................................................................................................4

Requirement iv)...............................................................................................................................4

Requirement v)................................................................................................................................4

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Part A:..............................................................................................................................................3

Requirement i).................................................................................................................................3

Requirement ii)................................................................................................................................3

Requirement iii)...............................................................................................................................3

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................3

Requirement vii)..............................................................................................................................3

Requirement viii).............................................................................................................................3

Part B:..............................................................................................................................................4

Requirement i).................................................................................................................................4

Requirement ii)................................................................................................................................4

Requirement iii)...............................................................................................................................4

Requirement iv)...............................................................................................................................4

Requirement v)................................................................................................................................4

2

ADVANCED FINANCIAL ACCOUNTING

Part A:

Requirement i)

Fair fax media limited has conducted the impairment of assets such as investments that

accounted for using the method of equity. Such investments are tested for impairment at each

reporting date when there is indication of impairment. At the end of each reporting period, assets

that suffered impairment are reviewed for reversal impairment. Some of the intangible assets of

organization such as trade names and mastheads having indefinite lives are tested on annual basis

for impairment. Goodwill is also tested for impairment on annual basis along with other assets

such as radio licenses, database, software and websites. The indication of existence of

impairment is provided due to occurrence of one or more events in relation to any particular

assets (fairfaxmedia.com.au 2018).

ADVANCED FINANCIAL ACCOUNTING

Part A:

Requirement i)

Fair fax media limited has conducted the impairment of assets such as investments that

accounted for using the method of equity. Such investments are tested for impairment at each

reporting date when there is indication of impairment. At the end of each reporting period, assets

that suffered impairment are reviewed for reversal impairment. Some of the intangible assets of

organization such as trade names and mastheads having indefinite lives are tested on annual basis

for impairment. Goodwill is also tested for impairment on annual basis along with other assets

such as radio licenses, database, software and websites. The indication of existence of

impairment is provided due to occurrence of one or more events in relation to any particular

assets (fairfaxmedia.com.au 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ADVANCED FINANCIAL ACCOUNTING

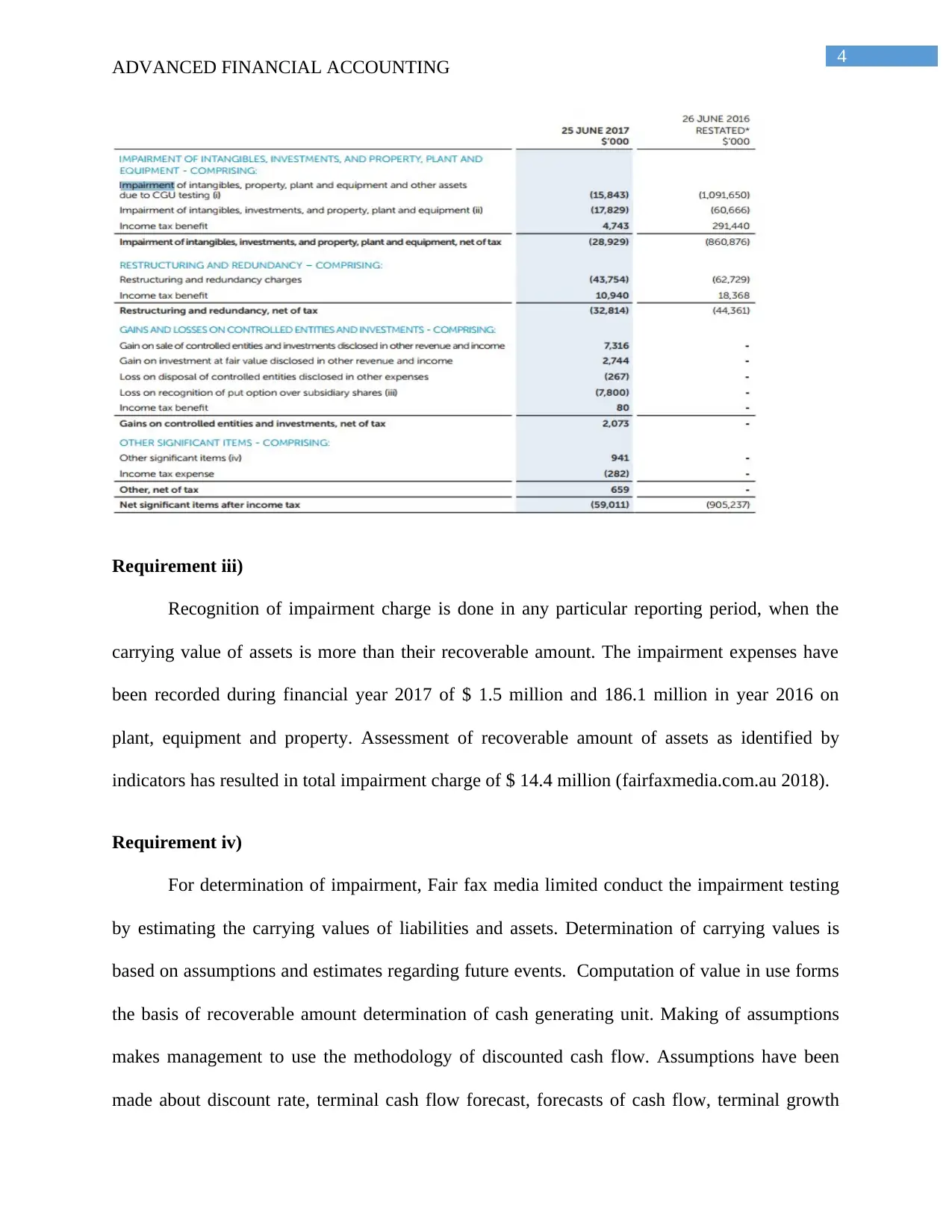

Requirement ii)

The process of allocation of such assets that is goodwill and intangible assets to cash

generating units does impairment testing of indefinite lives of intangible. It is required by group

to assess recoverable amount of cash generating unit in association with making considerable

judgments regarding the factors such as forecasting of cash flows, conditions of industry, decline

and growth rate, terminal growth rate and discount rates. Assets that are impaired through testing

of cash generating unit involves property, equipment and plan worth $ 1.1 million and

intangibles worth $ 14.7 million (fairfaxmedia.com.au 2018). Impairment of other assets such as

plant, equipment and property is carried by reviewing the carrying value of such assets on annual

basis whether they are exceeding the recoverable amount or not. Present value of expected future

cash flow forms the basis of estimating the recoverable amount. Amount of impairment of plant

and equipment along with intangibles is recorded at $ 28.9 million. Total amount of impairment

for investments, intangibles and property, equipment and plants for the financial year 2016 and

2017 is recorded at $ 1153087 million and 34124 million respectively (fairfaxmedia.com.au

2018).

ADVANCED FINANCIAL ACCOUNTING

Requirement ii)

The process of allocation of such assets that is goodwill and intangible assets to cash

generating units does impairment testing of indefinite lives of intangible. It is required by group

to assess recoverable amount of cash generating unit in association with making considerable

judgments regarding the factors such as forecasting of cash flows, conditions of industry, decline

and growth rate, terminal growth rate and discount rates. Assets that are impaired through testing

of cash generating unit involves property, equipment and plan worth $ 1.1 million and

intangibles worth $ 14.7 million (fairfaxmedia.com.au 2018). Impairment of other assets such as

plant, equipment and property is carried by reviewing the carrying value of such assets on annual

basis whether they are exceeding the recoverable amount or not. Present value of expected future

cash flow forms the basis of estimating the recoverable amount. Amount of impairment of plant

and equipment along with intangibles is recorded at $ 28.9 million. Total amount of impairment

for investments, intangibles and property, equipment and plants for the financial year 2016 and

2017 is recorded at $ 1153087 million and 34124 million respectively (fairfaxmedia.com.au

2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ADVANCED FINANCIAL ACCOUNTING

Requirement iii)

Recognition of impairment charge is done in any particular reporting period, when the

carrying value of assets is more than their recoverable amount. The impairment expenses have

been recorded during financial year 2017 of $ 1.5 million and 186.1 million in year 2016 on

plant, equipment and property. Assessment of recoverable amount of assets as identified by

indicators has resulted in total impairment charge of $ 14.4 million (fairfaxmedia.com.au 2018).

Requirement iv)

For determination of impairment, Fair fax media limited conduct the impairment testing

by estimating the carrying values of liabilities and assets. Determination of carrying values is

based on assumptions and estimates regarding future events. Computation of value in use forms

the basis of recoverable amount determination of cash generating unit. Making of assumptions

makes management to use the methodology of discounted cash flow. Assumptions have been

made about discount rate, terminal cash flow forecast, forecasts of cash flow, terminal growth

ADVANCED FINANCIAL ACCOUNTING

Requirement iii)

Recognition of impairment charge is done in any particular reporting period, when the

carrying value of assets is more than their recoverable amount. The impairment expenses have

been recorded during financial year 2017 of $ 1.5 million and 186.1 million in year 2016 on

plant, equipment and property. Assessment of recoverable amount of assets as identified by

indicators has resulted in total impairment charge of $ 14.4 million (fairfaxmedia.com.au 2018).

Requirement iv)

For determination of impairment, Fair fax media limited conduct the impairment testing

by estimating the carrying values of liabilities and assets. Determination of carrying values is

based on assumptions and estimates regarding future events. Computation of value in use forms

the basis of recoverable amount determination of cash generating unit. Making of assumptions

makes management to use the methodology of discounted cash flow. Assumptions have been

made about discount rate, terminal cash flow forecast, forecasts of cash flow, terminal growth

5

ADVANCED FINANCIAL ACCOUNTING

rates and terminal cash flow forecasts. Any sort of changes in assumptions might lead to

impairment, as it would cause the carrying amount to be more than their recoverable amount.

Furthermore, assumptions are made by management in relation to earnings multiple, forecasted

revenue and any recent investments that are made by third parties (fairfaxmedia.com.au 2018).

Requirement v)

Practice and involvement of subjectivity in the methodology of impairment testing may

fail to produce reliable and relevant benefits, as the information might be skewed or inaccurate.

Some of the organizations do the allocation and measurement of reporting unit in conducting

annual impairment testing of goodwill might allow for subjectivity and possible earnings

management. Subjectivity in the valuation process is also attributable to unobservable and

observable inputs. Estimates and extents of subjectivity will affect the impairment testing

accuracy (Alfredson et al. 2015). Management making judgments in respect of information and

inputs has the likelihood of exercising subjectivity that might not provide users with appropriate

depiction about impairment.

From the analysis of section of key and audit matters of Fair fax limited, it has been

found that auditors make the assessment whether organization meets the criteria of incorporating

substantial subjectivity in the process of impairment testing (fairfaxmedia.com.au 2018).

Therefore, after evaluating this particular aspect, it can be said that Fair Fax limited has

exercised some degree of subjectivity and performed the testing methodology opportunistically.

ADVANCED FINANCIAL ACCOUNTING

rates and terminal cash flow forecasts. Any sort of changes in assumptions might lead to

impairment, as it would cause the carrying amount to be more than their recoverable amount.

Furthermore, assumptions are made by management in relation to earnings multiple, forecasted

revenue and any recent investments that are made by third parties (fairfaxmedia.com.au 2018).

Requirement v)

Practice and involvement of subjectivity in the methodology of impairment testing may

fail to produce reliable and relevant benefits, as the information might be skewed or inaccurate.

Some of the organizations do the allocation and measurement of reporting unit in conducting

annual impairment testing of goodwill might allow for subjectivity and possible earnings

management. Subjectivity in the valuation process is also attributable to unobservable and

observable inputs. Estimates and extents of subjectivity will affect the impairment testing

accuracy (Alfredson et al. 2015). Management making judgments in respect of information and

inputs has the likelihood of exercising subjectivity that might not provide users with appropriate

depiction about impairment.

From the analysis of section of key and audit matters of Fair fax limited, it has been

found that auditors make the assessment whether organization meets the criteria of incorporating

substantial subjectivity in the process of impairment testing (fairfaxmedia.com.au 2018).

Therefore, after evaluating this particular aspect, it can be said that Fair Fax limited has

exercised some degree of subjectivity and performed the testing methodology opportunistically.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ADVANCED FINANCIAL ACCOUNTING

Requirement vi)

Conducting the evaluation of impairment testing methodology of Fair Fax limited, it is

ascertained that testing process is interesting and surprising. All the information concerning the

impairment is presented by properly segregating it in different sections. One interesting fact

about the impairment was that recognition and measurement of each individual assets whether

intangibles and tangibles are presented separately. Accounting policy used in estimation of

recoverable and carrying amount of all assets is explained in detail. All the impaired assets are

provided with estimates recoverable values that are based on assumptions made by management

(fairfaxmedia.com.au 2018). The auditor’s report also assesses the impairment of assets and

whether the methodology meets the requirement of AASB 136 of Impairment of assets”.

Requirement vii)

Group has conducted the sensitivity analysis relating to its cash-generating unit for

assessing the requirement of conducting impairment if there recoverable amount is lower than

their carrying amount. Estimates and judgments regarding the assets impairment are assessed for

the adequacy of information. Impairment of Fair Fax limited also involved related party loan

receivable, equity accounted investments along with intangible assets (fairfaxmedia.com.au

2018).

Requirement viii)

Hedge accounting of group takes into account hedges of fair value of recognized

liabilities and assets or commitment of firms. Determination of interest swap fair value is done

by referring to market values of similar instruments.

ADVANCED FINANCIAL ACCOUNTING

Requirement vi)

Conducting the evaluation of impairment testing methodology of Fair Fax limited, it is

ascertained that testing process is interesting and surprising. All the information concerning the

impairment is presented by properly segregating it in different sections. One interesting fact

about the impairment was that recognition and measurement of each individual assets whether

intangibles and tangibles are presented separately. Accounting policy used in estimation of

recoverable and carrying amount of all assets is explained in detail. All the impaired assets are

provided with estimates recoverable values that are based on assumptions made by management

(fairfaxmedia.com.au 2018). The auditor’s report also assesses the impairment of assets and

whether the methodology meets the requirement of AASB 136 of Impairment of assets”.

Requirement vii)

Group has conducted the sensitivity analysis relating to its cash-generating unit for

assessing the requirement of conducting impairment if there recoverable amount is lower than

their carrying amount. Estimates and judgments regarding the assets impairment are assessed for

the adequacy of information. Impairment of Fair Fax limited also involved related party loan

receivable, equity accounted investments along with intangible assets (fairfaxmedia.com.au

2018).

Requirement viii)

Hedge accounting of group takes into account hedges of fair value of recognized

liabilities and assets or commitment of firms. Determination of interest swap fair value is done

by referring to market values of similar instruments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCED FINANCIAL ACCOUNTING

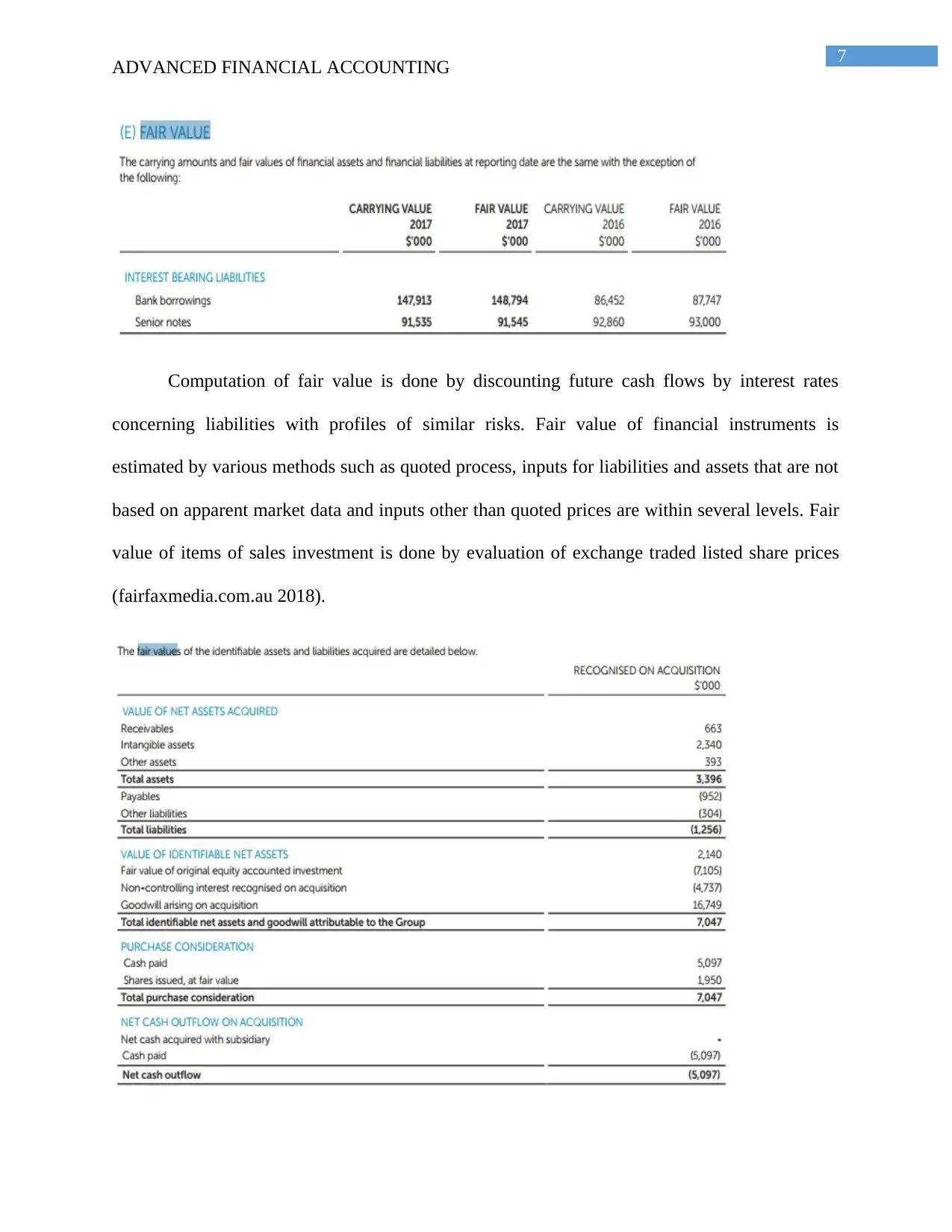

Computation of fair value is done by discounting future cash flows by interest rates

concerning liabilities with profiles of similar risks. Fair value of financial instruments is

estimated by various methods such as quoted process, inputs for liabilities and assets that are not

based on apparent market data and inputs other than quoted prices are within several levels. Fair

value of items of sales investment is done by evaluation of exchange traded listed share prices

(fairfaxmedia.com.au 2018).

ADVANCED FINANCIAL ACCOUNTING

Computation of fair value is done by discounting future cash flows by interest rates

concerning liabilities with profiles of similar risks. Fair value of financial instruments is

estimated by various methods such as quoted process, inputs for liabilities and assets that are not

based on apparent market data and inputs other than quoted prices are within several levels. Fair

value of items of sales investment is done by evaluation of exchange traded listed share prices

(fairfaxmedia.com.au 2018).

8

ADVANCED FINANCIAL ACCOUNTING

Part B:

Requirement i)

The main factor that is associated with not reflecting economic reality under the former

lease standard is related to incentives given by companies to classify lease contracts as operating

lease. Principle underlying the standard does not obliges company to disclose the leases

liabilities and assets under operating lease in the balance sheet. Rather they are disclosed as

expenses relating to rental arrangement in the notes to financial statements and this keep the

balance sheet profiles unchanged (Espinosa et al. 2015). In reality, companies might have actual

liabilities concerning lease that might be more than the lease reported off balance sheets. It is

estimated by IASB that out of $ 3.3 million worth of lease, only 25% of lease commitments is

reported on balance sheets (Christensen et al. 2015). Therefore, the actual worth of lease

commitments is not disclosed and this is the reason why the existing standard does not reflect

true economic reality.

Requirement ii)

One of the major flaws of IAS 17 is associated with the incentive given to company for

treating lease as operating lease. Treating lease as operating lease does not increase the balance

sheet as the expenses concerning such lease are mentioned in the notes of financial statements.

On other hand, financing lease impacts the balance sheets as it gives rise to liabilities and assets.

Organizations have their debt to equity ratio worsen if they treat lease as financing lease and it is

considered more favorable to classify lease as operating lease rather than financing lease (Bhat et

al. 2014). Therefore, organization that classifies lease as operating will have actual lease

ADVANCED FINANCIAL ACCOUNTING

Part B:

Requirement i)

The main factor that is associated with not reflecting economic reality under the former

lease standard is related to incentives given by companies to classify lease contracts as operating

lease. Principle underlying the standard does not obliges company to disclose the leases

liabilities and assets under operating lease in the balance sheet. Rather they are disclosed as

expenses relating to rental arrangement in the notes to financial statements and this keep the

balance sheet profiles unchanged (Espinosa et al. 2015). In reality, companies might have actual

liabilities concerning lease that might be more than the lease reported off balance sheets. It is

estimated by IASB that out of $ 3.3 million worth of lease, only 25% of lease commitments is

reported on balance sheets (Christensen et al. 2015). Therefore, the actual worth of lease

commitments is not disclosed and this is the reason why the existing standard does not reflect

true economic reality.

Requirement ii)

One of the major flaws of IAS 17 is associated with the incentive given to company for

treating lease as operating lease. Treating lease as operating lease does not increase the balance

sheet as the expenses concerning such lease are mentioned in the notes of financial statements.

On other hand, financing lease impacts the balance sheets as it gives rise to liabilities and assets.

Organizations have their debt to equity ratio worsen if they treat lease as financing lease and it is

considered more favorable to classify lease as operating lease rather than financing lease (Bhat et

al. 2014). Therefore, organization that classifies lease as operating will have actual lease

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ADVANCED FINANCIAL ACCOUNTING

commitments and liabilities that might be more than the total amount of debt that is represented

in the balance sheets. It is prepared for enabling their financial position to look more attractive to

investors that they essentially are. Total liabilities of companies might be more than on balance

sheets liabilities and the flaw of former standard helps in explaining why the debt reported on

balance sheets is 66 times more than off balance sheet liabilities.

Requirement iii)

Former lease accounting standard IAS 17 had ongoing controversy related to

classification of lease as operating and financing lease. Under the existing or former standard, it

is not essential for organization to reveal their operating lease commitments on balance sheets as

against operating lease. Airline companies either lease most of their aircraft fleets or they

purchase their fleets, and this might make look financial position of organization different

(Kajüter and Meinhövel 2016). It can be explained with the help of an instance, German airline

Lufthansa buys most of their fleets and its competitors Emirates airlines acquires most of their

fleets by leasing them and this might create difference in financial position of such companies.

However, in actual there might be similarity between financial position. Companies leasing few

of their aircraft fleets have higher leverage and assets base against companies having lower or

leasing few of their aircraft fleets (Feldmann and Le 2017). This depicts why there was no level

playing field between airline companies under the former lease standard.

Requirement iv)

Some of the companies especially who relies more on operating lease will have their

financial position being influenced considerably with the implementation of the new lease

accounting standard. Knock on effects of new standard is affecting several key performance

indicators, as balance sheets will be more expanded due to recognition of leased liabilities and

ADVANCED FINANCIAL ACCOUNTING

commitments and liabilities that might be more than the total amount of debt that is represented

in the balance sheets. It is prepared for enabling their financial position to look more attractive to

investors that they essentially are. Total liabilities of companies might be more than on balance

sheets liabilities and the flaw of former standard helps in explaining why the debt reported on

balance sheets is 66 times more than off balance sheet liabilities.

Requirement iii)

Former lease accounting standard IAS 17 had ongoing controversy related to

classification of lease as operating and financing lease. Under the existing or former standard, it

is not essential for organization to reveal their operating lease commitments on balance sheets as

against operating lease. Airline companies either lease most of their aircraft fleets or they

purchase their fleets, and this might make look financial position of organization different

(Kajüter and Meinhövel 2016). It can be explained with the help of an instance, German airline

Lufthansa buys most of their fleets and its competitors Emirates airlines acquires most of their

fleets by leasing them and this might create difference in financial position of such companies.

However, in actual there might be similarity between financial position. Companies leasing few

of their aircraft fleets have higher leverage and assets base against companies having lower or

leasing few of their aircraft fleets (Feldmann and Le 2017). This depicts why there was no level

playing field between airline companies under the former lease standard.

Requirement iv)

Some of the companies especially who relies more on operating lease will have their

financial position being influenced considerably with the implementation of the new lease

accounting standard. Knock on effects of new standard is affecting several key performance

indicators, as balance sheets will be more expanded due to recognition of leased liabilities and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ADVANCED FINANCIAL ACCOUNTING

assets. Now days, credit given by banks are associated with debt covenants that are tied to

various financial ratios (Donkersley et al. 2017). Hence, there needs to be a renegotiation of

existing debt covenants. Organizations might be keen on using short-term lease, as it would not

influence the balance sheet to a considerable extent. Increase in size of debt structure and balance

sheets would lead to organizations facing difficulties in receiving credit and experience problems

with creditors. Consequence of higher cost of transition and administrative burden on

management is another reason for making new lease standard unpopular. Alterations in lease

accounting will need educational efforts from top-level management and all way to

organization’s local parts as most of lease contracts are entered on local level (Bassemir 2017).

Some of the administrative burden on organization will be witnessed in terms of increased cost

and complexities of reporting, updating of accounting system and installation of new IT system.

Increased investment will be needed on part of management in new system and consumption of

time, as they will have to make detailed estimation concerning lease that is right to use and lease

liabilities compared to former lease standard.

Requirement v)

Application of new lease standard IFRS 16 makes it mandatory for all companies in

essence for all leases to make the disclosure of all leased liabilities and assets on their balance

sheets at the present value of future lease payments that are not avoidable. Recognition of

interest payable on leased liabilities and depreciation related to lease assets are depicted in the

income statement. New standard will have impact on some key financial ratios are highly crucial

to some companies. Investors will be provided with the information about the change in structure

of debt in the annual report of company. Disclosure of operating lease on the balance sheets will

have considerable impact on operating profits, asset turnover, interest cover, cash flows and

ADVANCED FINANCIAL ACCOUNTING

assets. Now days, credit given by banks are associated with debt covenants that are tied to

various financial ratios (Donkersley et al. 2017). Hence, there needs to be a renegotiation of

existing debt covenants. Organizations might be keen on using short-term lease, as it would not

influence the balance sheet to a considerable extent. Increase in size of debt structure and balance

sheets would lead to organizations facing difficulties in receiving credit and experience problems

with creditors. Consequence of higher cost of transition and administrative burden on

management is another reason for making new lease standard unpopular. Alterations in lease

accounting will need educational efforts from top-level management and all way to

organization’s local parts as most of lease contracts are entered on local level (Bassemir 2017).

Some of the administrative burden on organization will be witnessed in terms of increased cost

and complexities of reporting, updating of accounting system and installation of new IT system.

Increased investment will be needed on part of management in new system and consumption of

time, as they will have to make detailed estimation concerning lease that is right to use and lease

liabilities compared to former lease standard.

Requirement v)

Application of new lease standard IFRS 16 makes it mandatory for all companies in

essence for all leases to make the disclosure of all leased liabilities and assets on their balance

sheets at the present value of future lease payments that are not avoidable. Recognition of

interest payable on leased liabilities and depreciation related to lease assets are depicted in the

income statement. New standard will have impact on some key financial ratios are highly crucial

to some companies. Investors will be provided with the information about the change in structure

of debt in the annual report of company. Disclosure of operating lease on the balance sheets will

have considerable impact on operating profits, asset turnover, interest cover, cash flows and

11

ADVANCED FINANCIAL ACCOUNTING

other financial ratios (Findeisen and Adolph 2016). It would help in depicting actual scenario

and financial position of companies and there will be decision that is more informed since this

will lead to actual reflection of lease commitments. For evaluation of financial performance of

any business requires outsiders of companies and users of financial statements to make

guesswork and rough computation and calculations for estimating actual lease commitments in

the existing lease standard. Such process might lead to occurrence of errors and there exists

possibility of reflection of financial scenario that does not exist. IFRS 16 will help in brining

much needed transparency and facilitating comparisons between different companies (Florou and

Kosi 2015). There will be clear and enhanced understanding of actual liabilities relating to lease

commitments. Furthermore, new standard implementation will help in better allocation of capital

and making analysts and investors with enhanced leasing methods and will help in making

balanced leased versus buy decision on part of management.

ADVANCED FINANCIAL ACCOUNTING

other financial ratios (Findeisen and Adolph 2016). It would help in depicting actual scenario

and financial position of companies and there will be decision that is more informed since this

will lead to actual reflection of lease commitments. For evaluation of financial performance of

any business requires outsiders of companies and users of financial statements to make

guesswork and rough computation and calculations for estimating actual lease commitments in

the existing lease standard. Such process might lead to occurrence of errors and there exists

possibility of reflection of financial scenario that does not exist. IFRS 16 will help in brining

much needed transparency and facilitating comparisons between different companies (Florou and

Kosi 2015). There will be clear and enhanced understanding of actual liabilities relating to lease

commitments. Furthermore, new standard implementation will help in better allocation of capital

and making analysts and investors with enhanced leasing methods and will help in making

balanced leased versus buy decision on part of management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.