Advance Financial Accounting: IFRS 16 and its Requirements

VerifiedAdded on 2020/04/21

|9

|2847

|90

Report

AI Summary

This report delves into the intricacies of IFRS 16, the new international financial reporting standard established by the IASB, focusing on lease accounting. It outlines the standard's core objective: to provide accurate and transparent reporting of lease transactions. The report details the key requirements for both lessees and lessors, emphasizing the shift to a single lessee accounting model where almost all leases, particularly those exceeding 12 months, are recognized on the balance sheet. It contrasts this with the previous IAS 17, which distinguished between finance and operating leases. The report also examines the effects of IFRS 16 on financial statements, including changes in balance sheets, income statements, and cash flow statements. It provides an analysis of the impact on key financial ratios and performance metrics. Furthermore, the report explores the specific effects of IFRS 16 on Great Eastern Holdings Ltd., an insurance company, highlighting how the new standard will influence its financial reporting practices, especially regarding operating lease commitments. The report concludes by summarizing the overall impact and importance of the new lease standard.

Running Head: ADVANCED FINANCIAL ACCOUNTING

ifrs 16

The new lease standard

ifrs 16

The new lease standard

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advance Financial Accounting 1

Contents

Introduction...........................................................................................................................................2

IFRS 16 and its Requirements...............................................................................................................2

Lessee................................................................................................................................................2

Lessor................................................................................................................................................3

Changes in accounting environment......................................................................................................3

Lessee Accounting.............................................................................................................................3

Lessor accounting..............................................................................................................................4

Effects on financial statements..............................................................................................................4

Effects on Great Eastern Holdings Ltd..................................................................................................5

Conclusion.............................................................................................................................................6

References.............................................................................................................................................7

Contents

Introduction...........................................................................................................................................2

IFRS 16 and its Requirements...............................................................................................................2

Lessee................................................................................................................................................2

Lessor................................................................................................................................................3

Changes in accounting environment......................................................................................................3

Lessee Accounting.............................................................................................................................3

Lessor accounting..............................................................................................................................4

Effects on financial statements..............................................................................................................4

Effects on Great Eastern Holdings Ltd..................................................................................................5

Conclusion.............................................................................................................................................6

References.............................................................................................................................................7

Advance Financial Accounting 2

Introduction

IFRS 16 is an International Financial Reporting Standard, developed by IASB (International

Accounting Standard Board). This standard provide the guidelines for the lease accounting. The

main motive of the standard is to report that data which shows the accurate information about the

lease transactions ("IFRS", 2017). It introduces a single lessee accounting model and requires that

all the leases should be reported on the balance sheet and the lessee has to recognize all the assets

and liabilities for almost all leases with a period of more than 12 months. Once applicable, it will

replace IAS 17 ("IFRS 16 — Leases", 2017).

Great Eastern Holdings Ltd. was founded in 1908, is a life insurance group in Singapore and

Malaysia. It is the oldest insurance company in Asia listed on Singapore Exchange. It provides

services like banking, insurance and asset management. The mission of the company is to provide

financial security to its clients ("Great Eastern", 2017). This report is about the requirements of the

new lease standard for the lessee and lessor. It also explains the effects of IFRS 16 on the Great

Eastern Ltd.

IFRS 16 and its Requirements

The new standard for lease was published by IASB in January 2016 and will come in effect from

January 1, 2019. It defines the principles for the measurement and disclosure of the leases. The

companies who have applied for IFRS 15 Revenue from Contracts with Customers can choose to

apply for IFRS 16 before its effective date. The main objective of IASB to introduce this new

standard, is to improve the financial reporting of lease. Under IFRS 16, a leases is defined as a

contract that provides right to the customer (“lessee”) to use an asset for a particular period of time

in exchange of some consideration. The requirements of the definition of lease has also changed

from those in IAS 17. The new standard brings a significant change in the approach and will effect

several industries. The enterprises which will be mainly affected by IFRS 16 are retail and

consumer, telecommunications, banking and financial institutions, metals and mining, oil and gas

and insurance entities. Once the new standard became effective, it will replace the old standard of

lease that is IAS 17. It will eliminate the classification of leases as financial lease and operating

lease and all of them are treated in a similar way ("IFRS 16 Leases | Deloitte UK", 2017).

Lessee

As the new standard provide a single lessee accounting model, the lessee is required to:

Recognize assets and liabilities of most of the leases with a time period of more than 12

months. The exemption is provided for assets having low value.

Separation of the depreciation charged on lease assets from the interest on lease liabilities.

Previously, according to the IAS 17, the focus was mainly on identifying the finance lease that is

required to be reported in the balance sheet. The lease which is economically similar to the

purchasing of a leased asset is considered to be finance lease. All the other leases were termed as

operating leases and were not required to be shown on balance sheet. They were known as off

balance sheet leases. Now, as per IFRS 16, lessees are require to report all the leases on their

balance sheet, irrespective of the industry in which the entity works. The whole accounting

treatment of leases done by lessees will change fundamentally. It will completely remove the

current dual accounting model which distinguishes between the on balance sheet leases and off

balance sheet leases.

Introduction

IFRS 16 is an International Financial Reporting Standard, developed by IASB (International

Accounting Standard Board). This standard provide the guidelines for the lease accounting. The

main motive of the standard is to report that data which shows the accurate information about the

lease transactions ("IFRS", 2017). It introduces a single lessee accounting model and requires that

all the leases should be reported on the balance sheet and the lessee has to recognize all the assets

and liabilities for almost all leases with a period of more than 12 months. Once applicable, it will

replace IAS 17 ("IFRS 16 — Leases", 2017).

Great Eastern Holdings Ltd. was founded in 1908, is a life insurance group in Singapore and

Malaysia. It is the oldest insurance company in Asia listed on Singapore Exchange. It provides

services like banking, insurance and asset management. The mission of the company is to provide

financial security to its clients ("Great Eastern", 2017). This report is about the requirements of the

new lease standard for the lessee and lessor. It also explains the effects of IFRS 16 on the Great

Eastern Ltd.

IFRS 16 and its Requirements

The new standard for lease was published by IASB in January 2016 and will come in effect from

January 1, 2019. It defines the principles for the measurement and disclosure of the leases. The

companies who have applied for IFRS 15 Revenue from Contracts with Customers can choose to

apply for IFRS 16 before its effective date. The main objective of IASB to introduce this new

standard, is to improve the financial reporting of lease. Under IFRS 16, a leases is defined as a

contract that provides right to the customer (“lessee”) to use an asset for a particular period of time

in exchange of some consideration. The requirements of the definition of lease has also changed

from those in IAS 17. The new standard brings a significant change in the approach and will effect

several industries. The enterprises which will be mainly affected by IFRS 16 are retail and

consumer, telecommunications, banking and financial institutions, metals and mining, oil and gas

and insurance entities. Once the new standard became effective, it will replace the old standard of

lease that is IAS 17. It will eliminate the classification of leases as financial lease and operating

lease and all of them are treated in a similar way ("IFRS 16 Leases | Deloitte UK", 2017).

Lessee

As the new standard provide a single lessee accounting model, the lessee is required to:

Recognize assets and liabilities of most of the leases with a time period of more than 12

months. The exemption is provided for assets having low value.

Separation of the depreciation charged on lease assets from the interest on lease liabilities.

Previously, according to the IAS 17, the focus was mainly on identifying the finance lease that is

required to be reported in the balance sheet. The lease which is economically similar to the

purchasing of a leased asset is considered to be finance lease. All the other leases were termed as

operating leases and were not required to be shown on balance sheet. They were known as off

balance sheet leases. Now, as per IFRS 16, lessees are require to report all the leases on their

balance sheet, irrespective of the industry in which the entity works. The whole accounting

treatment of leases done by lessees will change fundamentally. It will completely remove the

current dual accounting model which distinguishes between the on balance sheet leases and off

balance sheet leases.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advance Financial Accounting 3

Another requirement for the lessee is to separate lease components and the non-lease components

of their contracts. After identifying the components, they are require to provide consideration for

each component. Lessees who do not make an accounting policy election are required to allocate

the consideration to the separated components on the basis of standalone selling price ("IFRS 16:

The leases standard is changing", 2016).

Lessor

The requirements for the lessor, stated under IFRS 16 are same as to IAS 17. The classification of

leases is done in the similar way that is operating and finance leases by the lessor in order to report

them differently. The requirements of lessor accounting are not fundamentally changed like those

of lessee accounting.

Changes in accounting environment

Implementation of IFRS 16 has brought number of changes in the accounting environment of

leases. It brings dramatic changes in the balance sheet of lessees, whereas lessor accounting is

slightly changed.

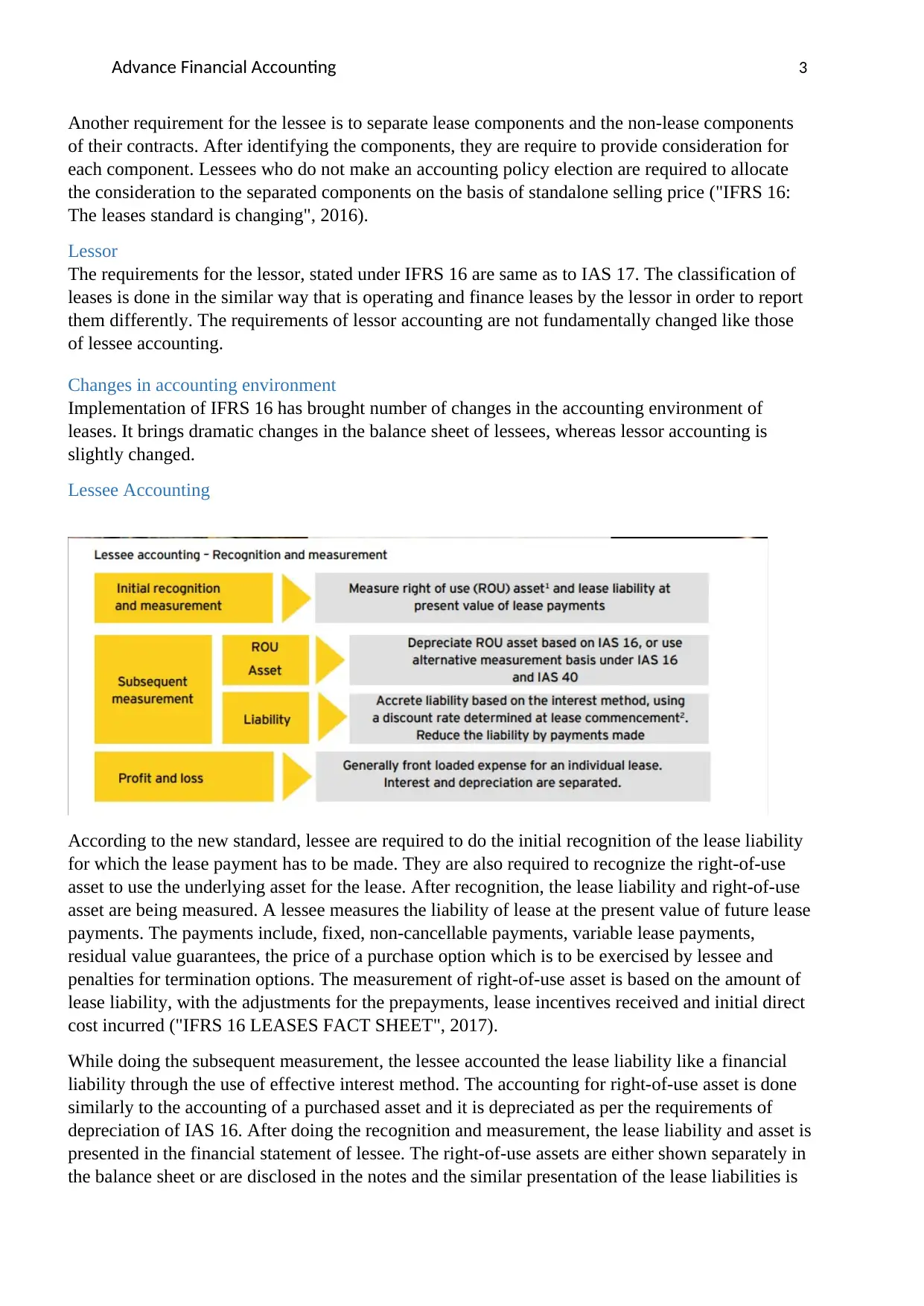

Lessee Accounting

According to the new standard, lessee are required to do the initial recognition of the lease liability

for which the lease payment has to be made. They are also required to recognize the right-of-use

asset to use the underlying asset for the lease. After recognition, the lease liability and right-of-use

asset are being measured. A lessee measures the liability of lease at the present value of future lease

payments. The payments include, fixed, non-cancellable payments, variable lease payments,

residual value guarantees, the price of a purchase option which is to be exercised by lessee and

penalties for termination options. The measurement of right-of-use asset is based on the amount of

lease liability, with the adjustments for the prepayments, lease incentives received and initial direct

cost incurred ("IFRS 16 LEASES FACT SHEET", 2017).

While doing the subsequent measurement, the lessee accounted the lease liability like a financial

liability through the use of effective interest method. The accounting for right-of-use asset is done

similarly to the accounting of a purchased asset and it is depreciated as per the requirements of

depreciation of IAS 16. After doing the recognition and measurement, the lease liability and asset is

presented in the financial statement of lessee. The right-of-use assets are either shown separately in

the balance sheet or are disclosed in the notes and the similar presentation of the lease liabilities is

Another requirement for the lessee is to separate lease components and the non-lease components

of their contracts. After identifying the components, they are require to provide consideration for

each component. Lessees who do not make an accounting policy election are required to allocate

the consideration to the separated components on the basis of standalone selling price ("IFRS 16:

The leases standard is changing", 2016).

Lessor

The requirements for the lessor, stated under IFRS 16 are same as to IAS 17. The classification of

leases is done in the similar way that is operating and finance leases by the lessor in order to report

them differently. The requirements of lessor accounting are not fundamentally changed like those

of lessee accounting.

Changes in accounting environment

Implementation of IFRS 16 has brought number of changes in the accounting environment of

leases. It brings dramatic changes in the balance sheet of lessees, whereas lessor accounting is

slightly changed.

Lessee Accounting

According to the new standard, lessee are required to do the initial recognition of the lease liability

for which the lease payment has to be made. They are also required to recognize the right-of-use

asset to use the underlying asset for the lease. After recognition, the lease liability and right-of-use

asset are being measured. A lessee measures the liability of lease at the present value of future lease

payments. The payments include, fixed, non-cancellable payments, variable lease payments,

residual value guarantees, the price of a purchase option which is to be exercised by lessee and

penalties for termination options. The measurement of right-of-use asset is based on the amount of

lease liability, with the adjustments for the prepayments, lease incentives received and initial direct

cost incurred ("IFRS 16 LEASES FACT SHEET", 2017).

While doing the subsequent measurement, the lessee accounted the lease liability like a financial

liability through the use of effective interest method. The accounting for right-of-use asset is done

similarly to the accounting of a purchased asset and it is depreciated as per the requirements of

depreciation of IAS 16. After doing the recognition and measurement, the lease liability and asset is

presented in the financial statement of lessee. The right-of-use assets are either shown separately in

the balance sheet or are disclosed in the notes and the similar presentation of the lease liabilities is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advance Financial Accounting 4

done. Expenses related to depreciation and interest are shown separately in the income statement.

Payments of lease liabilities are presented in financing activities in cash flow statement and interest

payments are presented on the basis of accounting policy election in compliance with IAS 7.

Lessor accounting

The accounting of lessor is not changed under the new standard. It remains the same from current

accounting in IAS 17. Lessors classify all the leases as per the classification mentioned in IAS 17

and categorize the leases in operating and finance leases. In operating lease, the lessor continues to

recognize underlying asset and for finance lease, lessor derecognize the underlying asset and

recognize a finance lease receivable according today’s requirements (2016).

At time of subsequent measurements:

Operating lease: lessor measure the income from lease on straight-line basis or on another basis

which shows a reduced benefit derived from the use of underlying asset.

Finance lease: for the accumulation of the net investment in lease, lessor measures the interest

income and reduce that investment for the received payments.

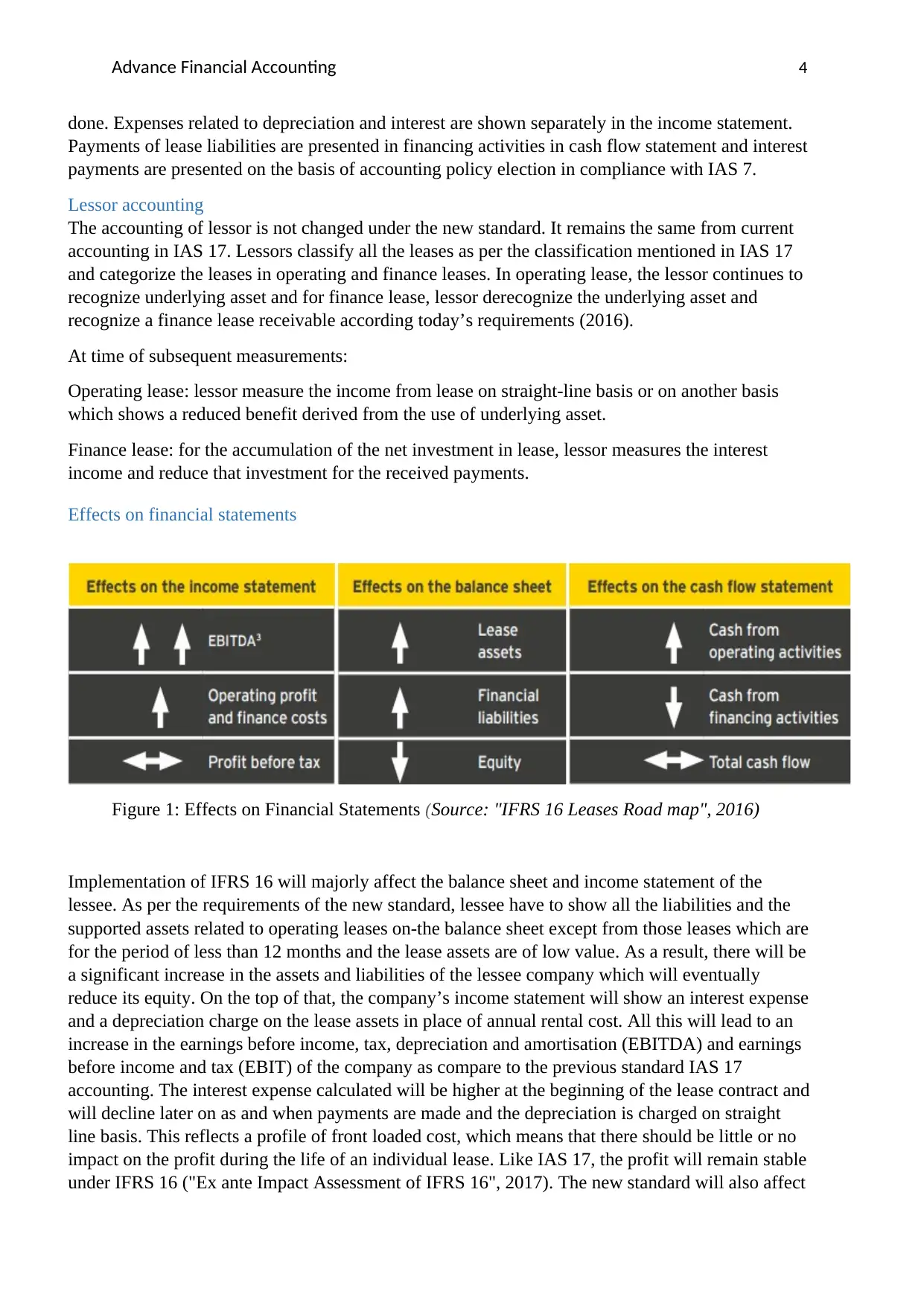

Effects on financial statements

Figure 1: Effects on Financial Statements (Source: "IFRS 16 Leases Road map", 2016)

Implementation of IFRS 16 will majorly affect the balance sheet and income statement of the

lessee. As per the requirements of the new standard, lessee have to show all the liabilities and the

supported assets related to operating leases on-the balance sheet except from those leases which are

for the period of less than 12 months and the lease assets are of low value. As a result, there will be

a significant increase in the assets and liabilities of the lessee company which will eventually

reduce its equity. On the top of that, the company’s income statement will show an interest expense

and a depreciation charge on the lease assets in place of annual rental cost. All this will lead to an

increase in the earnings before income, tax, depreciation and amortisation (EBITDA) and earnings

before income and tax (EBIT) of the company as compare to the previous standard IAS 17

accounting. The interest expense calculated will be higher at the beginning of the lease contract and

will decline later on as and when payments are made and the depreciation is charged on straight

line basis. This reflects a profile of front loaded cost, which means that there should be little or no

impact on the profit during the life of an individual lease. Like IAS 17, the profit will remain stable

under IFRS 16 ("Ex ante Impact Assessment of IFRS 16", 2017). The new standard will also affect

done. Expenses related to depreciation and interest are shown separately in the income statement.

Payments of lease liabilities are presented in financing activities in cash flow statement and interest

payments are presented on the basis of accounting policy election in compliance with IAS 7.

Lessor accounting

The accounting of lessor is not changed under the new standard. It remains the same from current

accounting in IAS 17. Lessors classify all the leases as per the classification mentioned in IAS 17

and categorize the leases in operating and finance leases. In operating lease, the lessor continues to

recognize underlying asset and for finance lease, lessor derecognize the underlying asset and

recognize a finance lease receivable according today’s requirements (2016).

At time of subsequent measurements:

Operating lease: lessor measure the income from lease on straight-line basis or on another basis

which shows a reduced benefit derived from the use of underlying asset.

Finance lease: for the accumulation of the net investment in lease, lessor measures the interest

income and reduce that investment for the received payments.

Effects on financial statements

Figure 1: Effects on Financial Statements (Source: "IFRS 16 Leases Road map", 2016)

Implementation of IFRS 16 will majorly affect the balance sheet and income statement of the

lessee. As per the requirements of the new standard, lessee have to show all the liabilities and the

supported assets related to operating leases on-the balance sheet except from those leases which are

for the period of less than 12 months and the lease assets are of low value. As a result, there will be

a significant increase in the assets and liabilities of the lessee company which will eventually

reduce its equity. On the top of that, the company’s income statement will show an interest expense

and a depreciation charge on the lease assets in place of annual rental cost. All this will lead to an

increase in the earnings before income, tax, depreciation and amortisation (EBITDA) and earnings

before income and tax (EBIT) of the company as compare to the previous standard IAS 17

accounting. The interest expense calculated will be higher at the beginning of the lease contract and

will decline later on as and when payments are made and the depreciation is charged on straight

line basis. This reflects a profile of front loaded cost, which means that there should be little or no

impact on the profit during the life of an individual lease. Like IAS 17, the profit will remain stable

under IFRS 16 ("Ex ante Impact Assessment of IFRS 16", 2017). The new standard will also affect

Advance Financial Accounting 5

the cash flow statement of the company. As such the cash outflow will have no impact, but the

structure of cash flow statement changes. The net cash flow generated from financing activities

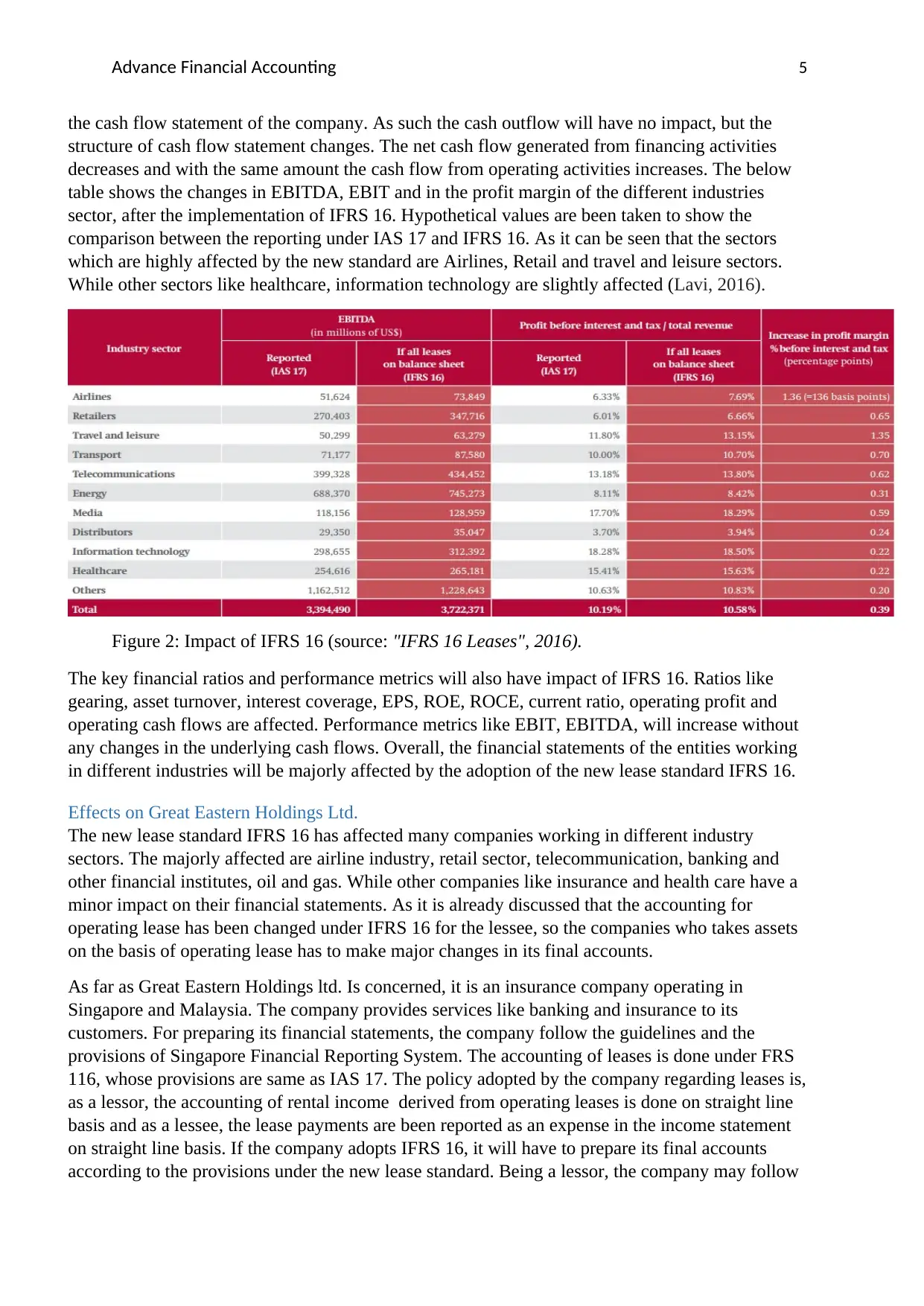

decreases and with the same amount the cash flow from operating activities increases. The below

table shows the changes in EBITDA, EBIT and in the profit margin of the different industries

sector, after the implementation of IFRS 16. Hypothetical values are been taken to show the

comparison between the reporting under IAS 17 and IFRS 16. As it can be seen that the sectors

which are highly affected by the new standard are Airlines, Retail and travel and leisure sectors.

While other sectors like healthcare, information technology are slightly affected (Lavi, 2016).

Figure 2: Impact of IFRS 16 (source: "IFRS 16 Leases", 2016).

The key financial ratios and performance metrics will also have impact of IFRS 16. Ratios like

gearing, asset turnover, interest coverage, EPS, ROE, ROCE, current ratio, operating profit and

operating cash flows are affected. Performance metrics like EBIT, EBITDA, will increase without

any changes in the underlying cash flows. Overall, the financial statements of the entities working

in different industries will be majorly affected by the adoption of the new lease standard IFRS 16.

Effects on Great Eastern Holdings Ltd.

The new lease standard IFRS 16 has affected many companies working in different industry

sectors. The majorly affected are airline industry, retail sector, telecommunication, banking and

other financial institutes, oil and gas. While other companies like insurance and health care have a

minor impact on their financial statements. As it is already discussed that the accounting for

operating lease has been changed under IFRS 16 for the lessee, so the companies who takes assets

on the basis of operating lease has to make major changes in its final accounts.

As far as Great Eastern Holdings ltd. Is concerned, it is an insurance company operating in

Singapore and Malaysia. The company provides services like banking and insurance to its

customers. For preparing its financial statements, the company follow the guidelines and the

provisions of Singapore Financial Reporting System. The accounting of leases is done under FRS

116, whose provisions are same as IAS 17. The policy adopted by the company regarding leases is,

as a lessor, the accounting of rental income derived from operating leases is done on straight line

basis and as a lessee, the lease payments are been reported as an expense in the income statement

on straight line basis. If the company adopts IFRS 16, it will have to prepare its final accounts

according to the provisions under the new lease standard. Being a lessor, the company may follow

the cash flow statement of the company. As such the cash outflow will have no impact, but the

structure of cash flow statement changes. The net cash flow generated from financing activities

decreases and with the same amount the cash flow from operating activities increases. The below

table shows the changes in EBITDA, EBIT and in the profit margin of the different industries

sector, after the implementation of IFRS 16. Hypothetical values are been taken to show the

comparison between the reporting under IAS 17 and IFRS 16. As it can be seen that the sectors

which are highly affected by the new standard are Airlines, Retail and travel and leisure sectors.

While other sectors like healthcare, information technology are slightly affected (Lavi, 2016).

Figure 2: Impact of IFRS 16 (source: "IFRS 16 Leases", 2016).

The key financial ratios and performance metrics will also have impact of IFRS 16. Ratios like

gearing, asset turnover, interest coverage, EPS, ROE, ROCE, current ratio, operating profit and

operating cash flows are affected. Performance metrics like EBIT, EBITDA, will increase without

any changes in the underlying cash flows. Overall, the financial statements of the entities working

in different industries will be majorly affected by the adoption of the new lease standard IFRS 16.

Effects on Great Eastern Holdings Ltd.

The new lease standard IFRS 16 has affected many companies working in different industry

sectors. The majorly affected are airline industry, retail sector, telecommunication, banking and

other financial institutes, oil and gas. While other companies like insurance and health care have a

minor impact on their financial statements. As it is already discussed that the accounting for

operating lease has been changed under IFRS 16 for the lessee, so the companies who takes assets

on the basis of operating lease has to make major changes in its final accounts.

As far as Great Eastern Holdings ltd. Is concerned, it is an insurance company operating in

Singapore and Malaysia. The company provides services like banking and insurance to its

customers. For preparing its financial statements, the company follow the guidelines and the

provisions of Singapore Financial Reporting System. The accounting of leases is done under FRS

116, whose provisions are same as IAS 17. The policy adopted by the company regarding leases is,

as a lessor, the accounting of rental income derived from operating leases is done on straight line

basis and as a lessee, the lease payments are been reported as an expense in the income statement

on straight line basis. If the company adopts IFRS 16, it will have to prepare its final accounts

according to the provisions under the new lease standard. Being a lessor, the company may follow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advance Financial Accounting 6

the concepts of IAS 17 for doing the lease accounting. But when working as a lessee, it has to make

certain changes in its financial reporting.

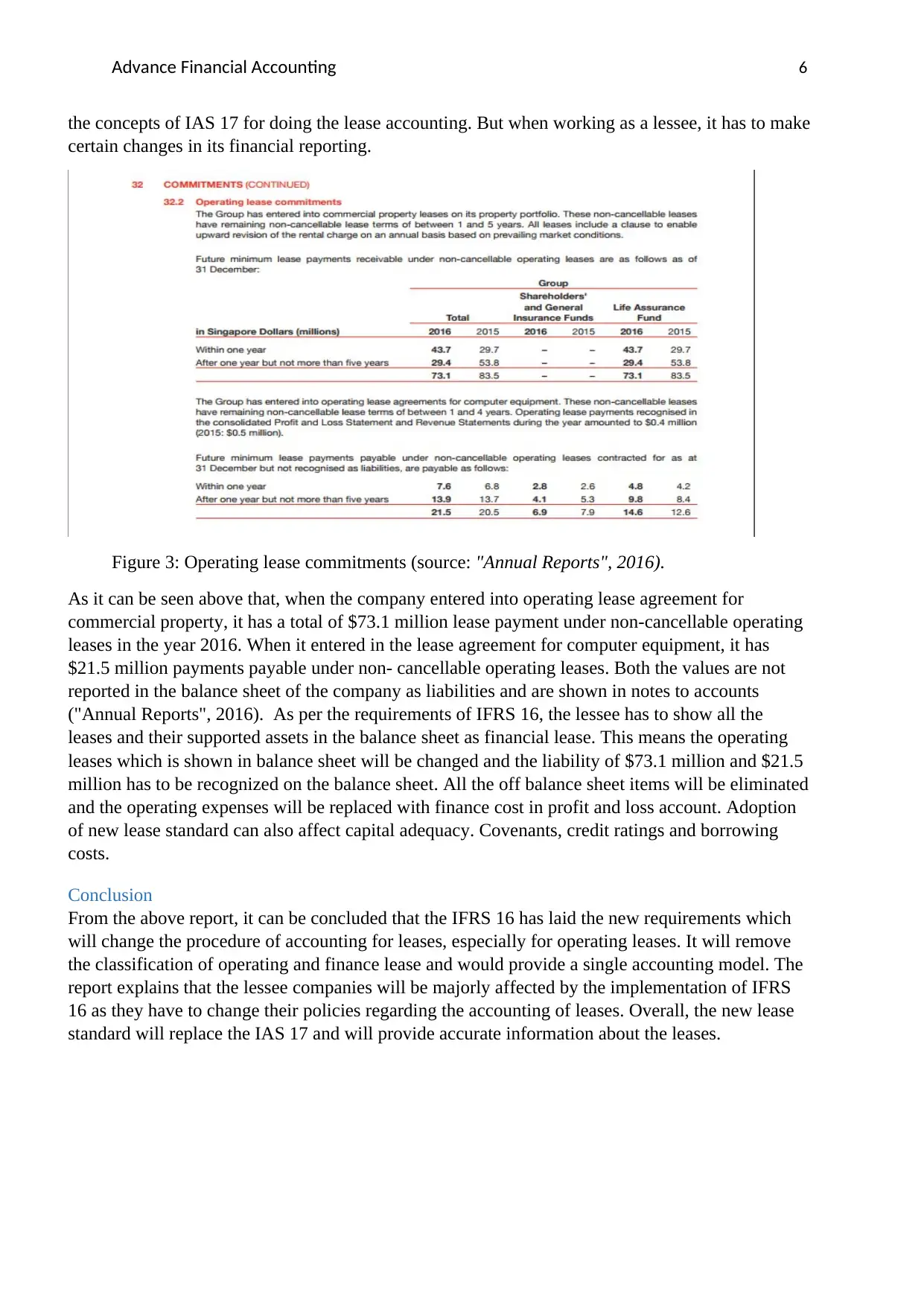

Figure 3: Operating lease commitments (source: "Annual Reports", 2016).

As it can be seen above that, when the company entered into operating lease agreement for

commercial property, it has a total of $73.1 million lease payment under non-cancellable operating

leases in the year 2016. When it entered in the lease agreement for computer equipment, it has

$21.5 million payments payable under non- cancellable operating leases. Both the values are not

reported in the balance sheet of the company as liabilities and are shown in notes to accounts

("Annual Reports", 2016). As per the requirements of IFRS 16, the lessee has to show all the

leases and their supported assets in the balance sheet as financial lease. This means the operating

leases which is shown in balance sheet will be changed and the liability of $73.1 million and $21.5

million has to be recognized on the balance sheet. All the off balance sheet items will be eliminated

and the operating expenses will be replaced with finance cost in profit and loss account. Adoption

of new lease standard can also affect capital adequacy. Covenants, credit ratings and borrowing

costs.

Conclusion

From the above report, it can be concluded that the IFRS 16 has laid the new requirements which

will change the procedure of accounting for leases, especially for operating leases. It will remove

the classification of operating and finance lease and would provide a single accounting model. The

report explains that the lessee companies will be majorly affected by the implementation of IFRS

16 as they have to change their policies regarding the accounting of leases. Overall, the new lease

standard will replace the IAS 17 and will provide accurate information about the leases.

the concepts of IAS 17 for doing the lease accounting. But when working as a lessee, it has to make

certain changes in its financial reporting.

Figure 3: Operating lease commitments (source: "Annual Reports", 2016).

As it can be seen above that, when the company entered into operating lease agreement for

commercial property, it has a total of $73.1 million lease payment under non-cancellable operating

leases in the year 2016. When it entered in the lease agreement for computer equipment, it has

$21.5 million payments payable under non- cancellable operating leases. Both the values are not

reported in the balance sheet of the company as liabilities and are shown in notes to accounts

("Annual Reports", 2016). As per the requirements of IFRS 16, the lessee has to show all the

leases and their supported assets in the balance sheet as financial lease. This means the operating

leases which is shown in balance sheet will be changed and the liability of $73.1 million and $21.5

million has to be recognized on the balance sheet. All the off balance sheet items will be eliminated

and the operating expenses will be replaced with finance cost in profit and loss account. Adoption

of new lease standard can also affect capital adequacy. Covenants, credit ratings and borrowing

costs.

Conclusion

From the above report, it can be concluded that the IFRS 16 has laid the new requirements which

will change the procedure of accounting for leases, especially for operating leases. It will remove

the classification of operating and finance lease and would provide a single accounting model. The

report explains that the lessee companies will be majorly affected by the implementation of IFRS

16 as they have to change their policies regarding the accounting of leases. Overall, the new lease

standard will replace the IAS 17 and will provide accurate information about the leases.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advance Financial Accounting 7

References

IFRS 16 — Leases. (2017). Iasplus.com. Retrieved 13 November 2017, from

https://www.iasplus.com/en/standards/ifrs/ifrs-16

(2016). KPMG. Retrieved 14 November 2017, from https://www.in.kpmg.com/ifrs/files/first-

impressions-leases-IFRS16.pdf

Annual Reports. (2016). Great Eastern, Singapore. Retrieved 15 November 2017, from

https://www.greateasternlife.com/sg/en/about-us/investor-relations/annual-reports.html

Ex ante Impact Assessment of IFRS 16. (2017). Efrag.org. Retrieved 15 November 2017, from

https://www.efrag.org/Assets/Download?Asseturl=%2Fsites%2Fwebpublishing%2fsiteassets

%2FIFRS%252016%2520-%2520Europe%2520Economics%2520-%2520Ex%2520ante

%2520Impact%2520Assessment%2520%2822%2520February

%25202017%29.pdf&aspxautodetectcookiesupport=1

Great Eastern. (2017). Great Eastern, Singapore. Retrieved 13 November 2017, from

https://www.greateasternlife.com/sg/en/about-us.html

IFRS 16 Leases | Deloitte UK. (2017). Deloitte United Kingdom. Retrieved 15 November 2017,

from https://www2.deloitte.com/uk/en/pages/audit/articles/ifrs-16-leases.html

IFRS 16 LEASES FACT SHEET. (2017). Cpaaustralia.com.au. Retrieved 14 November 2017, from

https://www.cpaaustralia.com.au/~/media/corporate/allfiles/document/professional-resources/

reporting/factsheet-ifrs16-leases

IFRS 16 Leases Road map. (2016). Ey.com. Retrieved 15 November 2017, from

http://www.ey.com/Publication/vwLUAssets/ey-leases-a-summary-of-ifrs-16/$FILE/ey-leases-a-

summary-of-ifrs-16.pdf

IFRS 16 Leases. (2016). Ifrs.org. Retrieved 15 November 2017, from

http://www.ifrs.org/-/media/project/leases/ifrs/published-documents/ifrs16-effects-analysis.pdf

IFRS 16: The leases standard is changing. (2016). Pwc.com. Retrieved 15 November 2017, from

https://www.pwc.com/gx/en/services/audit-assurance/assets/ifrs-16-new-leases.pdf

IFRS. (2017). Ifrs.org. Retrieved 15 November 2017, from

http://www.ifrs.org/issued-standards/list-of-standards/ifrs-16-leases/

Lavi, M. R. (2016). The impact of IFRS on industry. John Wiley & Sons.

Morales-Díaz, J., & Zamora-Ramírez, C. (2017). Effects of IFRS 16 on Key Financial Ratios: A

New Methological Approach.

References

IFRS 16 — Leases. (2017). Iasplus.com. Retrieved 13 November 2017, from

https://www.iasplus.com/en/standards/ifrs/ifrs-16

(2016). KPMG. Retrieved 14 November 2017, from https://www.in.kpmg.com/ifrs/files/first-

impressions-leases-IFRS16.pdf

Annual Reports. (2016). Great Eastern, Singapore. Retrieved 15 November 2017, from

https://www.greateasternlife.com/sg/en/about-us/investor-relations/annual-reports.html

Ex ante Impact Assessment of IFRS 16. (2017). Efrag.org. Retrieved 15 November 2017, from

https://www.efrag.org/Assets/Download?Asseturl=%2Fsites%2Fwebpublishing%2fsiteassets

%2FIFRS%252016%2520-%2520Europe%2520Economics%2520-%2520Ex%2520ante

%2520Impact%2520Assessment%2520%2822%2520February

%25202017%29.pdf&aspxautodetectcookiesupport=1

Great Eastern. (2017). Great Eastern, Singapore. Retrieved 13 November 2017, from

https://www.greateasternlife.com/sg/en/about-us.html

IFRS 16 Leases | Deloitte UK. (2017). Deloitte United Kingdom. Retrieved 15 November 2017,

from https://www2.deloitte.com/uk/en/pages/audit/articles/ifrs-16-leases.html

IFRS 16 LEASES FACT SHEET. (2017). Cpaaustralia.com.au. Retrieved 14 November 2017, from

https://www.cpaaustralia.com.au/~/media/corporate/allfiles/document/professional-resources/

reporting/factsheet-ifrs16-leases

IFRS 16 Leases Road map. (2016). Ey.com. Retrieved 15 November 2017, from

http://www.ey.com/Publication/vwLUAssets/ey-leases-a-summary-of-ifrs-16/$FILE/ey-leases-a-

summary-of-ifrs-16.pdf

IFRS 16 Leases. (2016). Ifrs.org. Retrieved 15 November 2017, from

http://www.ifrs.org/-/media/project/leases/ifrs/published-documents/ifrs16-effects-analysis.pdf

IFRS 16: The leases standard is changing. (2016). Pwc.com. Retrieved 15 November 2017, from

https://www.pwc.com/gx/en/services/audit-assurance/assets/ifrs-16-new-leases.pdf

IFRS. (2017). Ifrs.org. Retrieved 15 November 2017, from

http://www.ifrs.org/issued-standards/list-of-standards/ifrs-16-leases/

Lavi, M. R. (2016). The impact of IFRS on industry. John Wiley & Sons.

Morales-Díaz, J., & Zamora-Ramírez, C. (2017). Effects of IFRS 16 on Key Financial Ratios: A

New Methological Approach.

Advance Financial Accounting 8

Singer, R., Pfaff, A., Winiarski, H., & Winiarski, M. (2017). Accounting for Leases under the New

Standard, Part 1 - The CPA Journal. The CPA Journal. Retrieved 14 November 2017, from

https://www.cpajournal.com/2017/08/23/accounting-leases-new-standard-part-1/

Singer, R., Pfaff, A., Winiarski, H., & Winiarski, M. (2017). Accounting for Leases under the New

Standard, Part 1 - The CPA Journal. The CPA Journal. Retrieved 14 November 2017, from

https://www.cpajournal.com/2017/08/23/accounting-leases-new-standard-part-1/

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.