HI6025 Accounting: IFRS Adoption Implications in Australia Report

VerifiedAdded on 2023/06/11

|9

|938

|477

Report

AI Summary

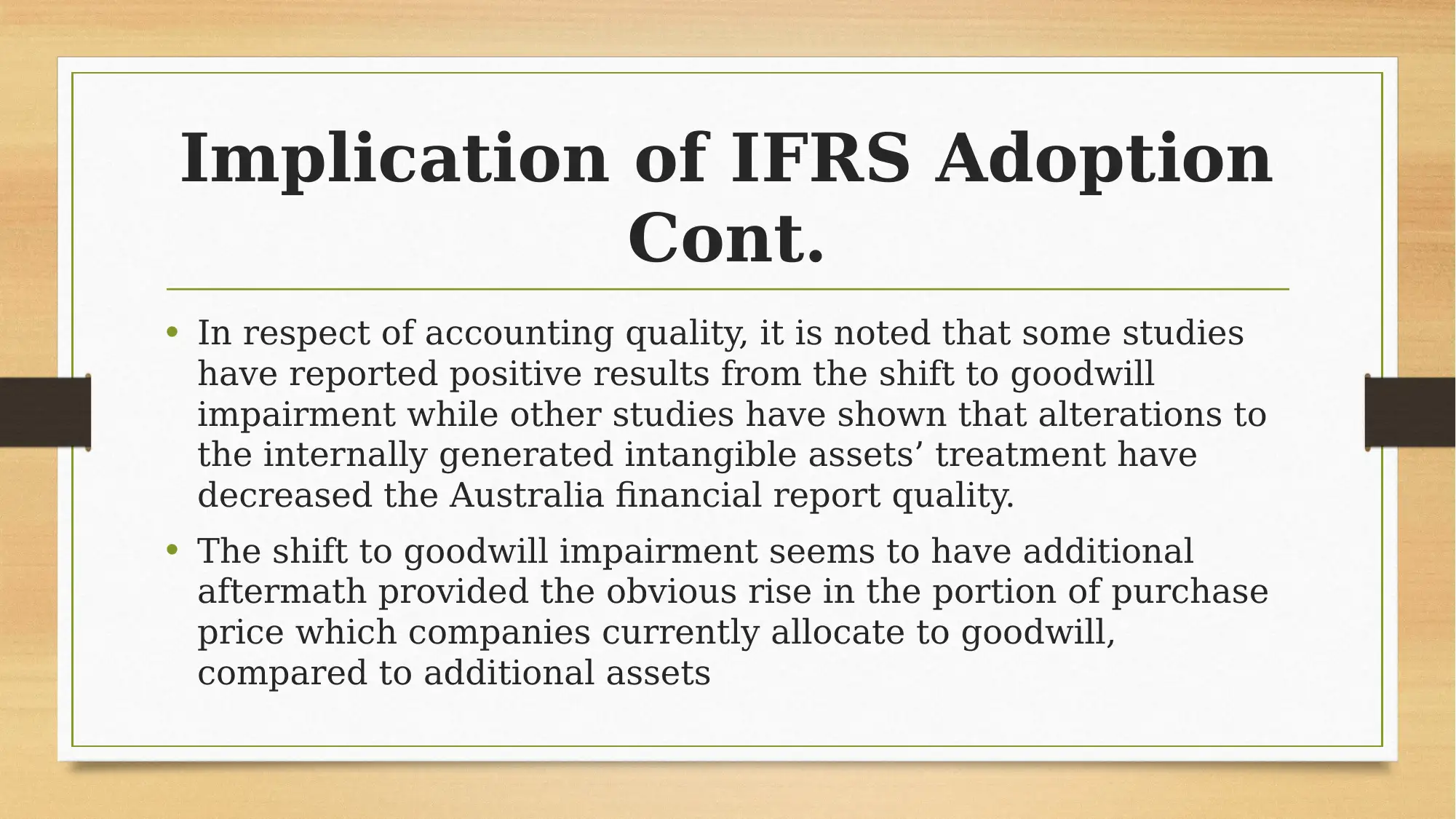

This report examines the implications of IFRS adoption in Australia, drawing on AASB Research Report No. 3. It highlights the positive impacts of IFRS adoption on investors and analysts, including enhanced analyst following and forecast accuracy. The report also addresses concerns regarding accounting quality, particularly related to goodwill impairment and internally generated intangible assets. Furthermore, it discusses the impact on the readability of financial information and earnings management practices, noting a decrease in firms engaging in earnings management under IFRS. The analysis connects these findings to broader literature on IFRS and accounting quality, emphasizing the need for integrating IFRS into the Australian Reporting Framework. Desklib provides access to this report and a wealth of other solved assignments and study resources for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.