Critical Review of IFRS Adoption: Australia and Nigeria - HI6025

VerifiedAdded on 2022/09/02

|13

|2170

|23

Report

AI Summary

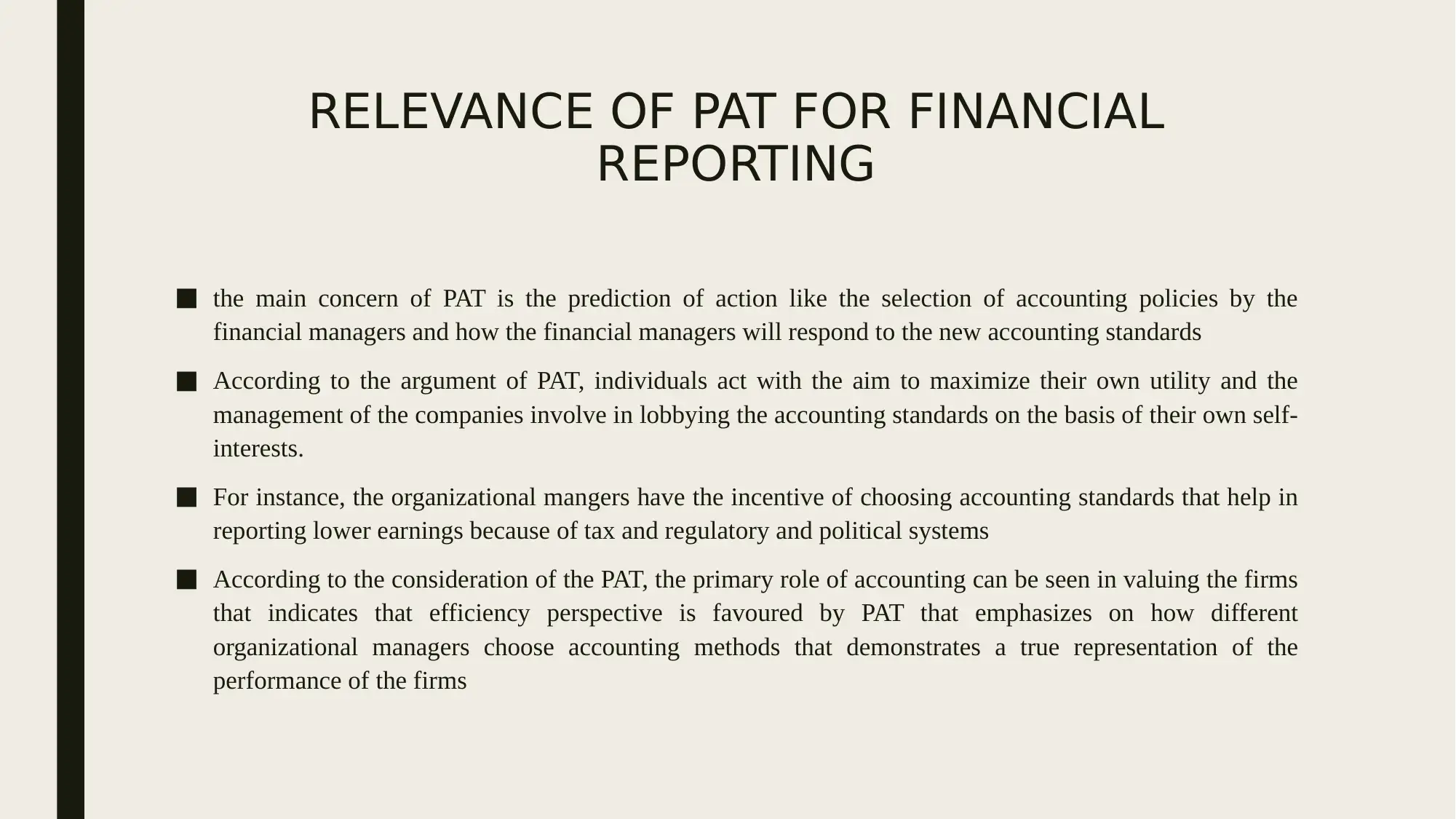

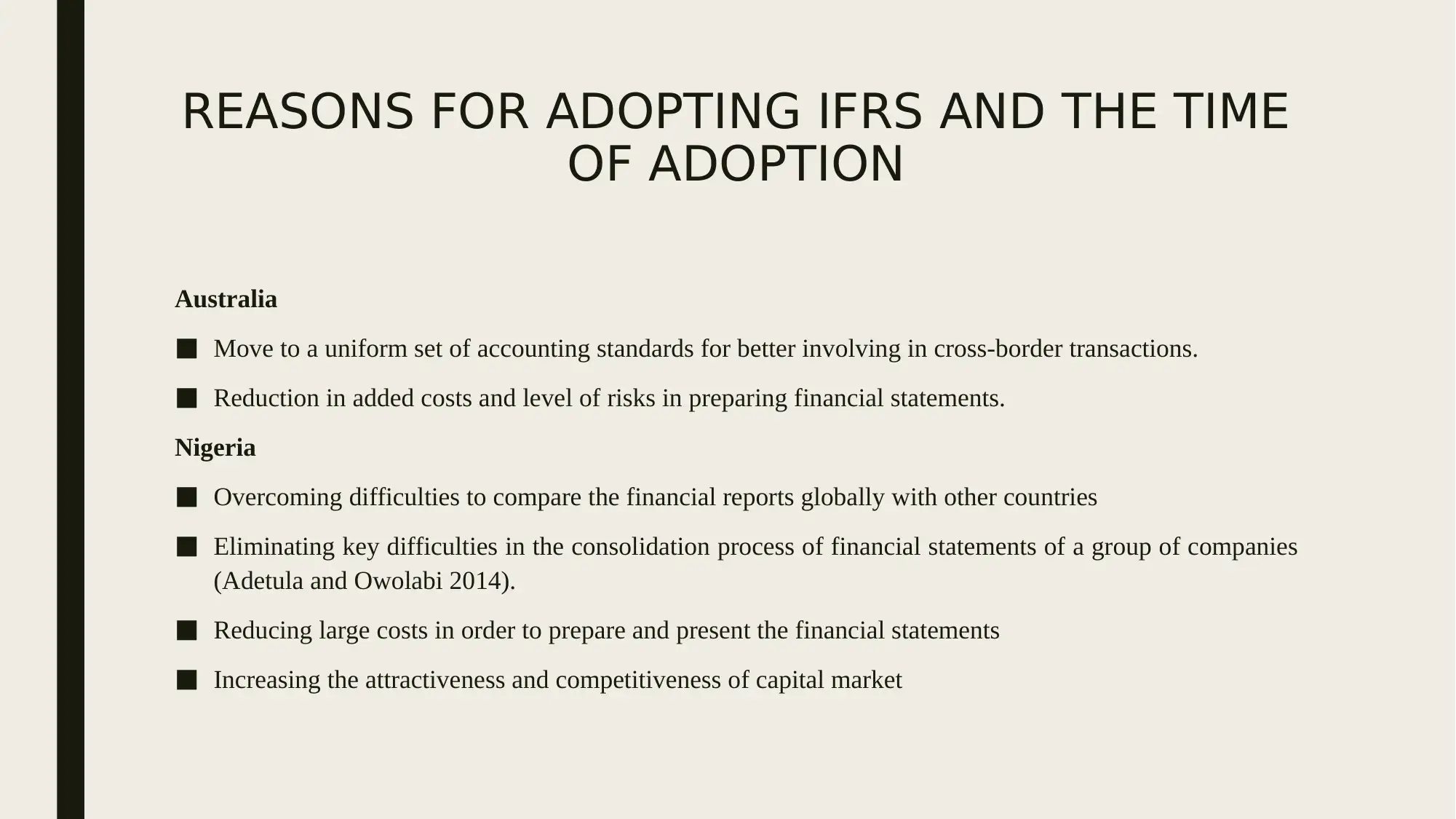

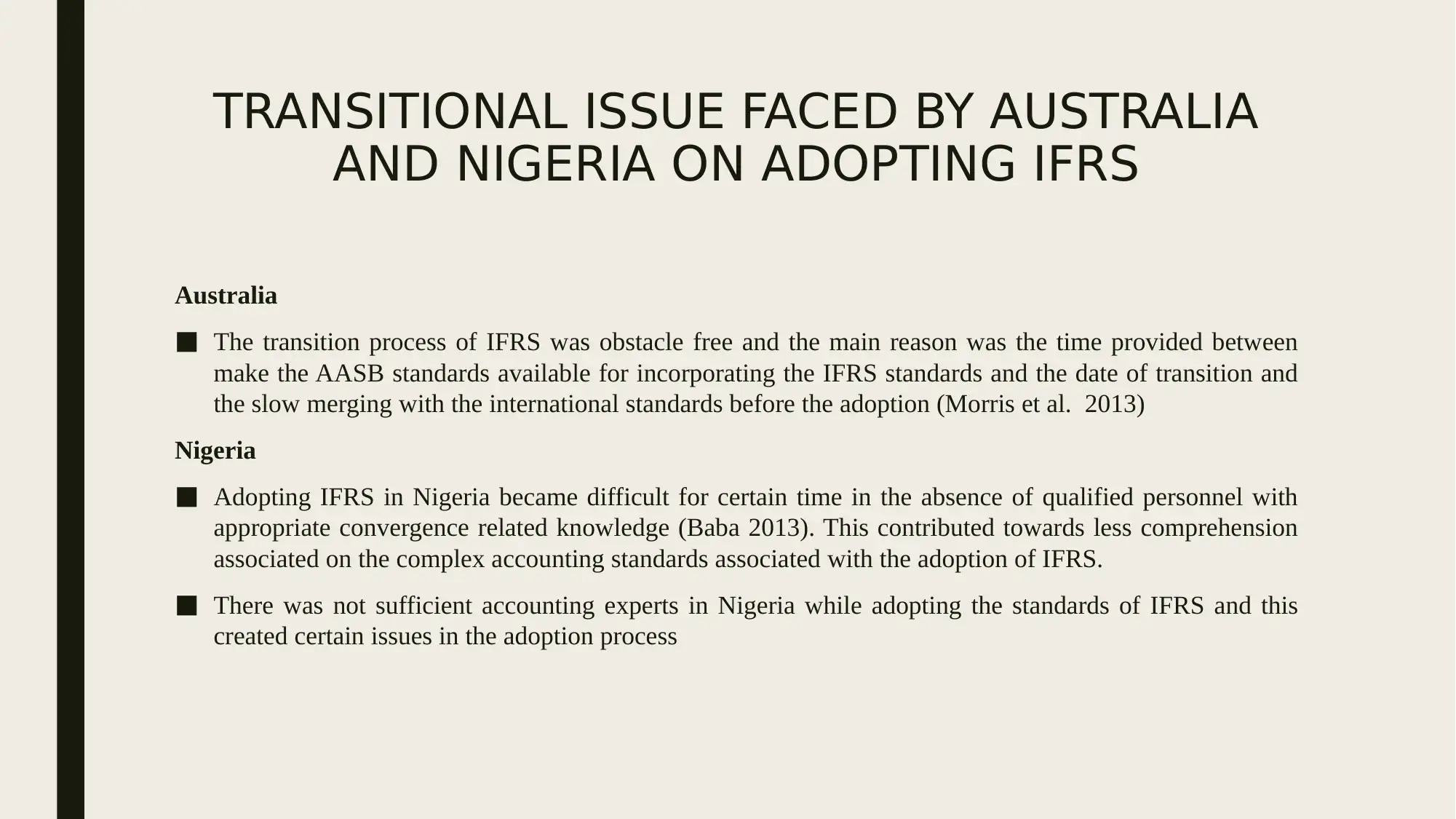

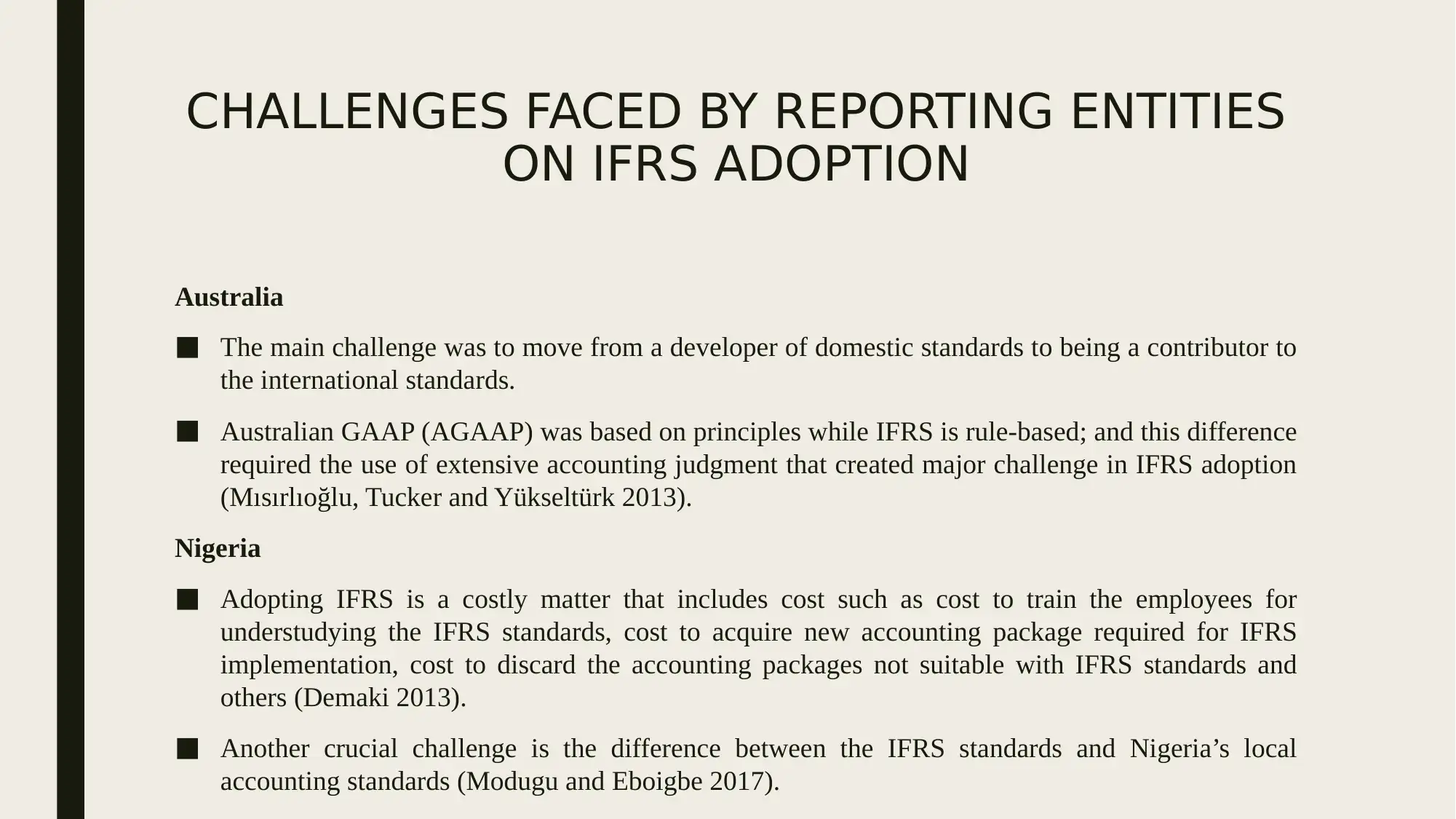

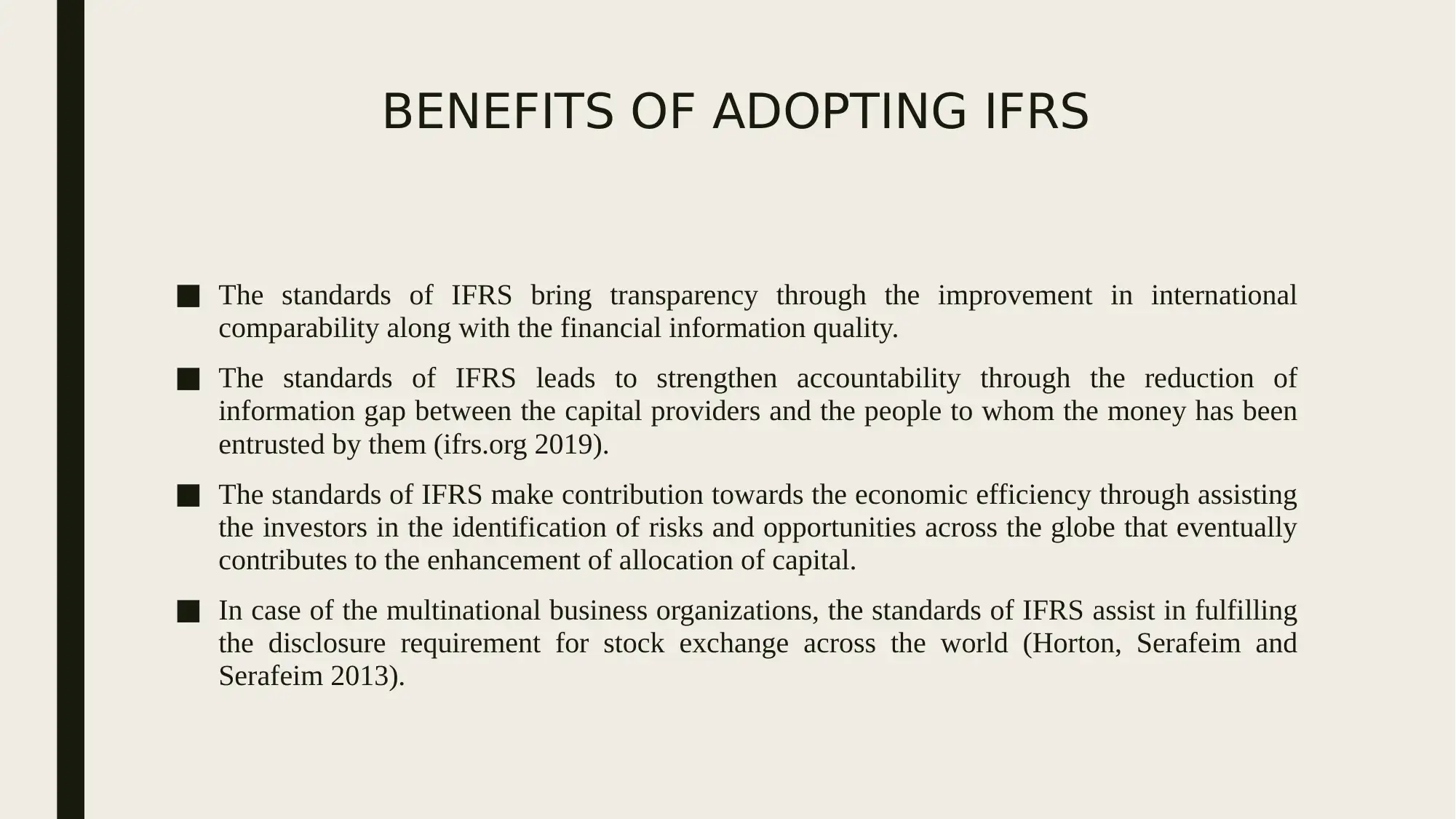

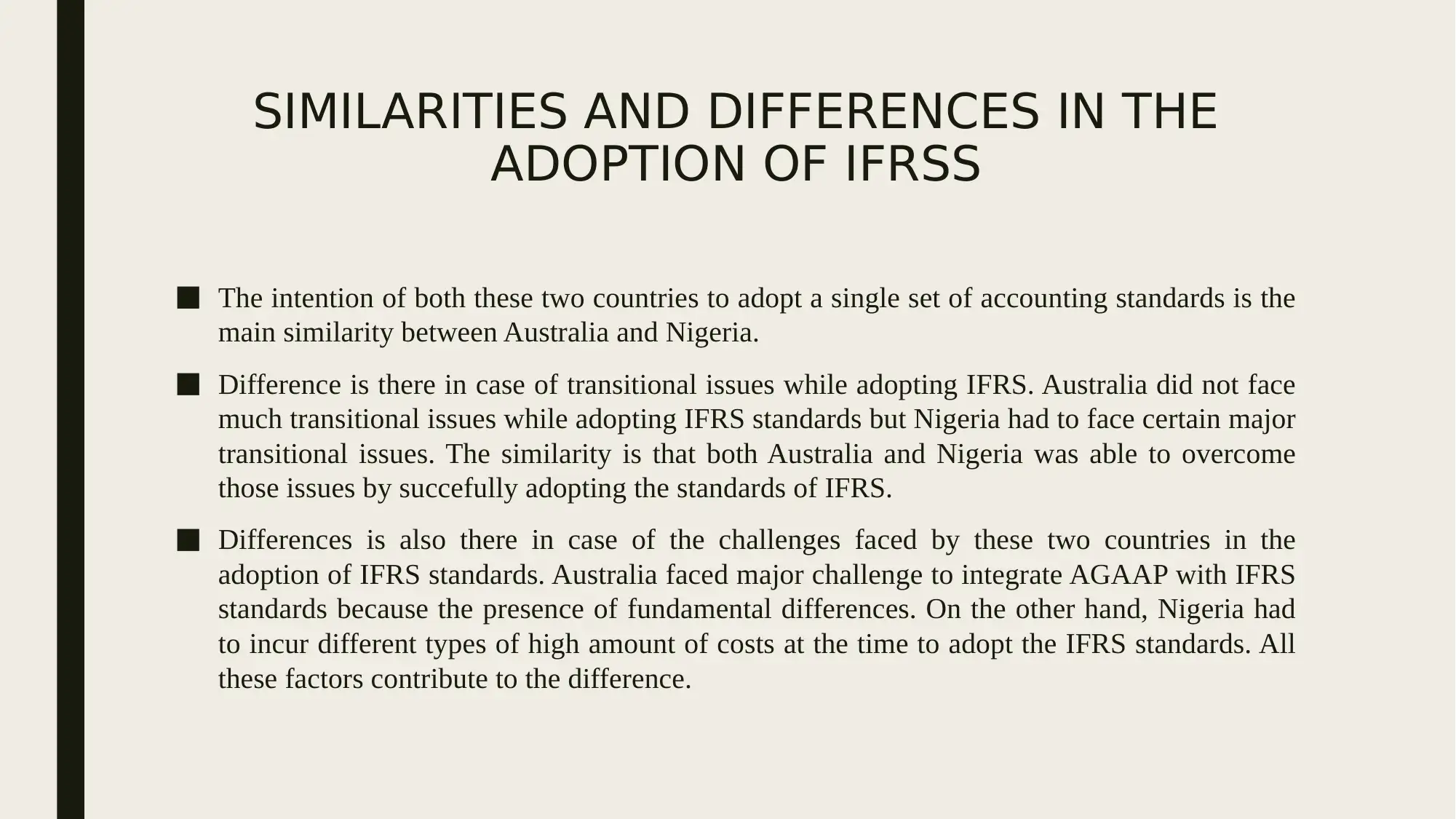

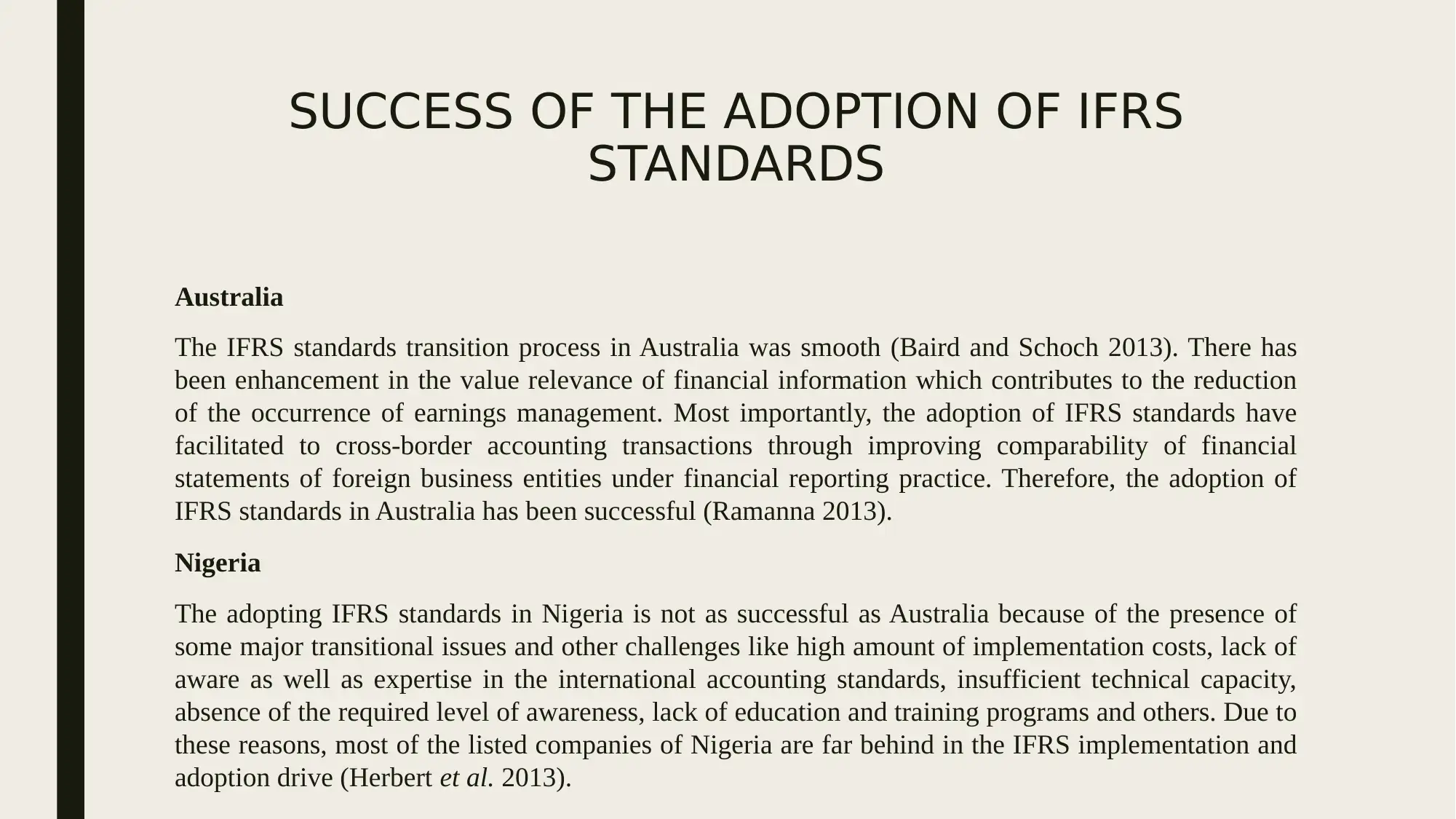

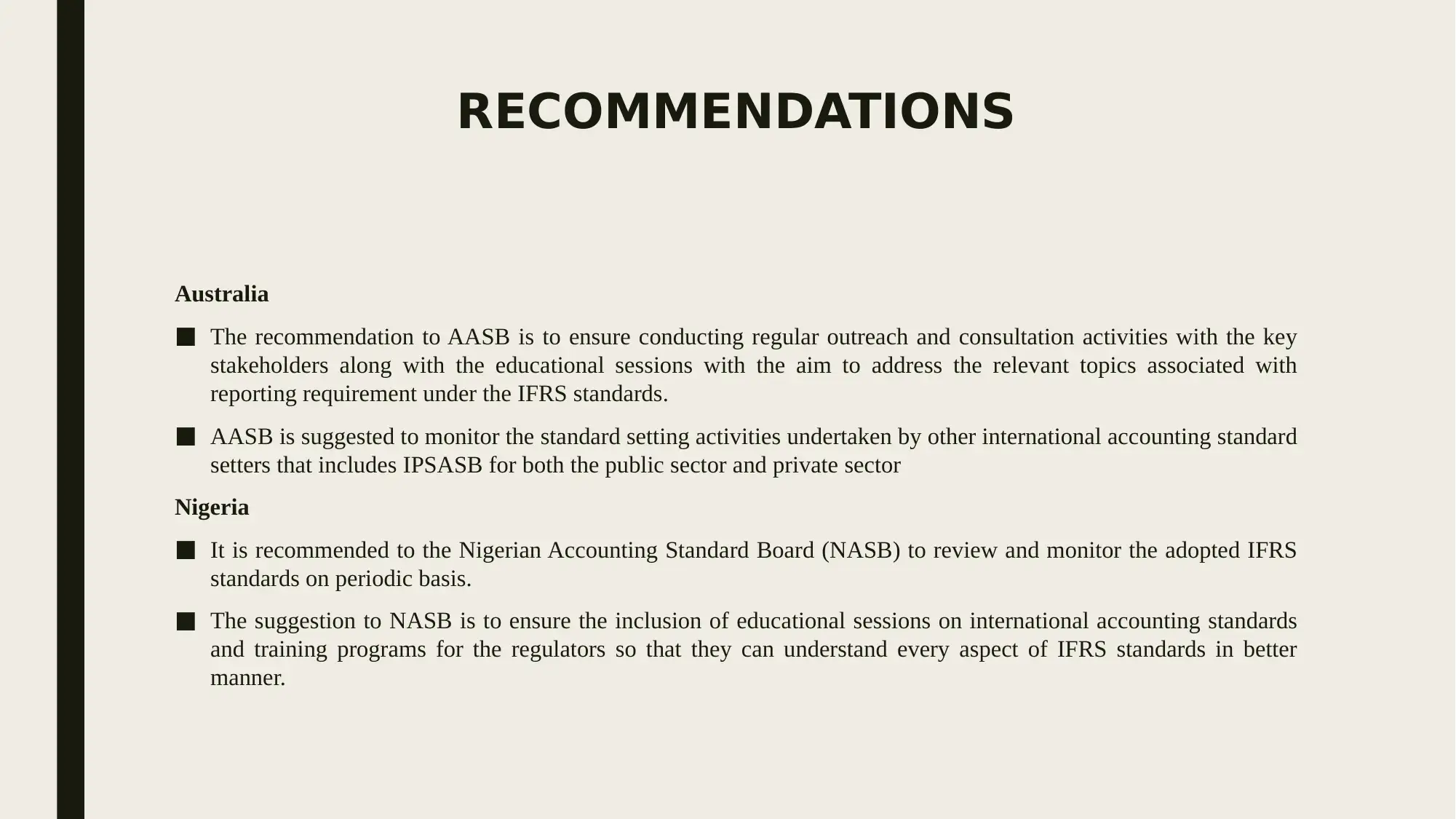

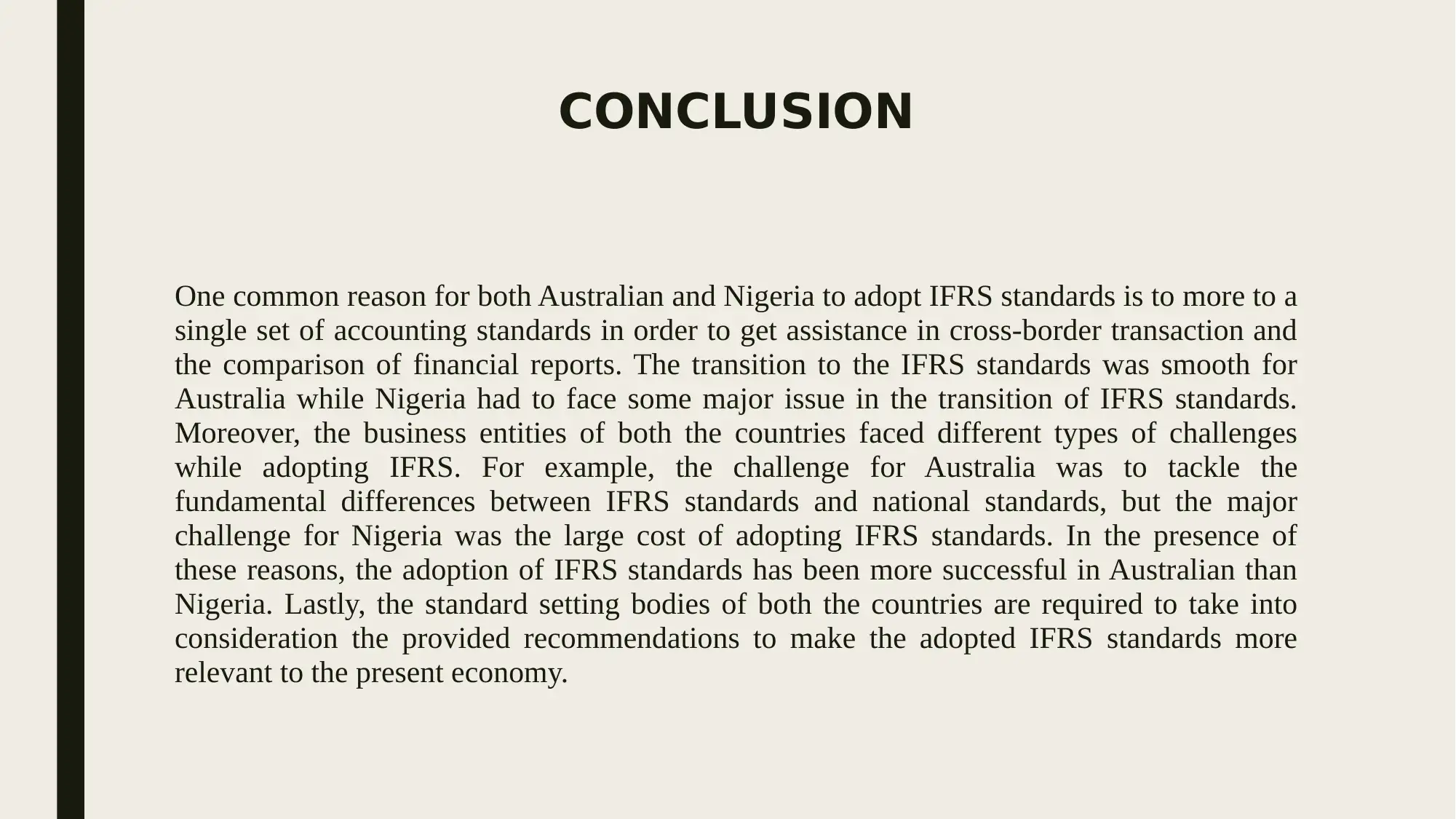

This report provides a critical review of the adoption of International Financial Reporting Standards (IFRS) in Australia and Nigeria. It begins by highlighting the significance of financial reporting in the accounting profession and the relevance of Positive Accounting Theory (PAT) in predicting financial managers' actions. The report then delves into the reasons behind the adoption of IFRS by both countries, emphasizing the benefits such as improved cross-border transactions and comparability of financial statements. It further examines the transitional issues faced, including the challenges encountered by reporting entities during the adoption process, such as moving from principle-based to rule-based accounting in Australia and the high implementation costs in Nigeria. The report also discusses the benefits of IFRS adoption, including increased transparency, strengthened accountability, and contributions to economic efficiency. It draws comparisons between the two countries, highlighting similarities in their goals and differences in the challenges faced, and assesses the success of IFRS adoption in each country. Finally, the report offers recommendations to accounting standard setting bodies in both countries and concludes by emphasizing the importance of adapting IFRS standards to the present economic conditions.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.