Accounting Theory: IFRS Adoption and Information Relevance Report

VerifiedAdded on 2023/06/12

|15

|1207

|55

Report

AI Summary

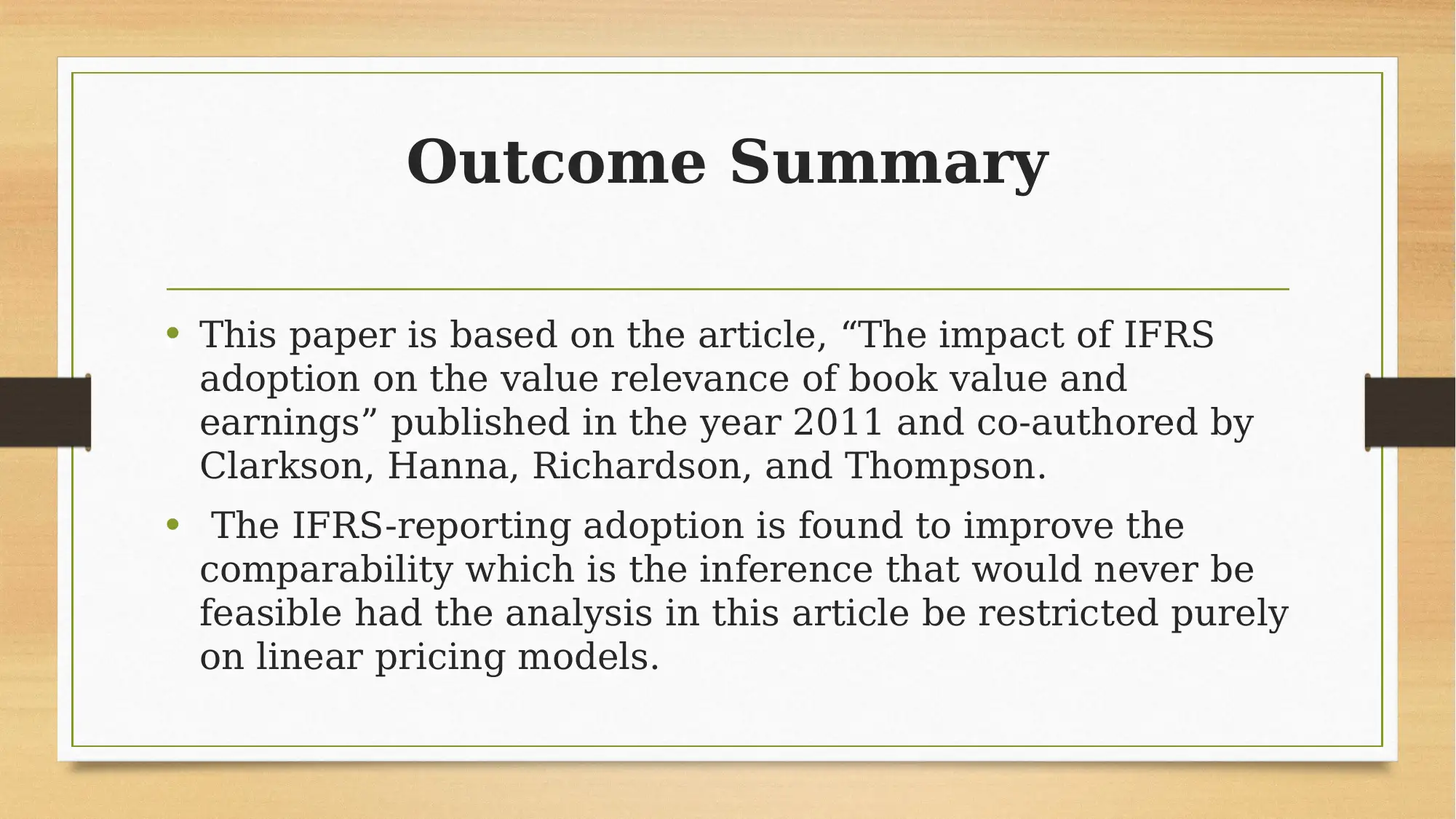

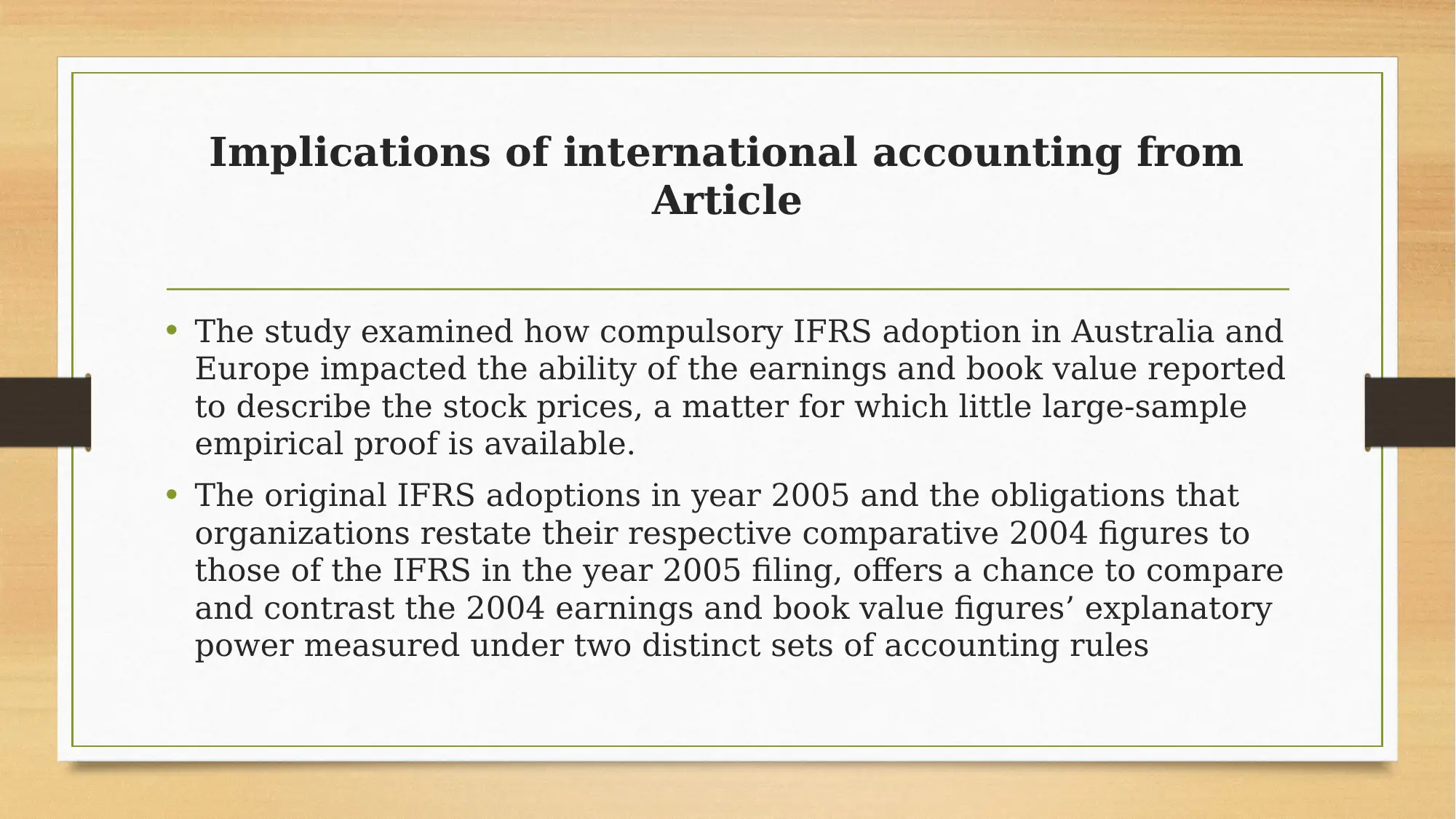

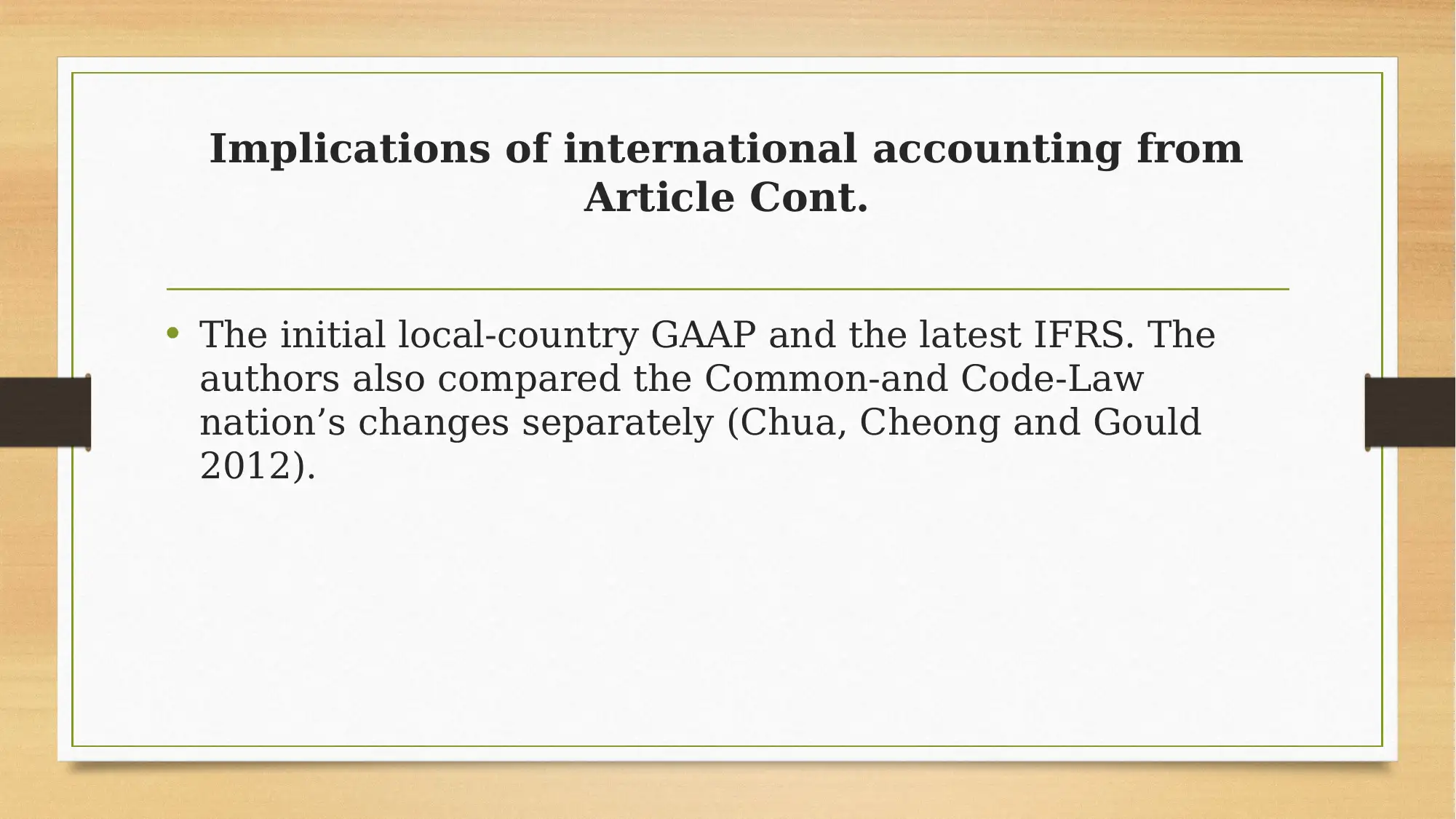

This report examines the implications of International Financial Reporting Standards (IFRS) adoption, focusing on its impact on the value relevance of book value and earnings. It references a study analyzing the compulsory IFRS adoption in Australia and Europe, highlighting the changes in earnings and book value's ability to describe stock prices. The report discusses the effects on Common and Code Law countries, noting a decline in BVPS and EPS value relevance following IFRS adoption under certain models. It also explores the potential for measurement error heteroscedasticity in Code Law countries due to IFRS. The study concludes that IFRS adoption has generally increased the value relevance of accounting information since its launch in 2005, contributing to the understanding of current issues in accounting.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.