Report on the Impact of IFRS Implementation in Australian Accounting

VerifiedAdded on 2023/06/09

|13

|2962

|186

Report

AI Summary

This report examines the impact of International Financial Reporting Standards (IFRS) implementation on Australian entities, particularly focusing on intangible assets. The study analyzes the changes introduced by AASB 138, highlighting the effects on business combinations, goodwill, and impairment. The report uses excerpts from Wesfarmers annual reports and articles from 'The Australian' newspaper to illustrate the practical implications of these changes. It discusses the concerns of Australian companies regarding the new standards and the potential impact on their balance sheets, including the treatment of deferred tax liabilities and the recognition of intangible assets. The report further explores the materialization of these concerns, referencing IAS 38 disclosures and the changes introduced by CPA. Overall, the study concludes that the implementation of IFRS has led to significant changes in accounting practices, affecting the valuation and recognition of intangible assets and impacting the financial reporting of Australian companies.

Running head: FOUNDATIONS IN ACCOUNTING

Foundations in Accounting

Name of Student:

Name of University:

Author’s Note:

Foundations in Accounting

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FOUNDATIONS IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

2FOUNDATIONS IN ACCOUNTING

Introduction

On 1st January 2005, it was declared by “Financial Reporting Council (FRC)” that the

Australian entities needed to mandatorily adhere to the international accounting standards. In

previous years the companies needed to comply with only Corporations Act, which was only

standard to be followed for the Australian organisations. Therefore, AASB took the decision to

introduce the different types of the standards associated to the “International Financial

Reporting Standards (IFRS)”. However, the impact of the IFRS implementation was seen to be

based on the changes in the reporting associated the liabilities, assets, equities and the surplus of

the local government companies in Australia (Epstein, 2018).

The main discourse of the study is focused on evaluating the net impact of the

implementation of IFRS in the Australian entities. The study has used excerpts from Wesfarmers

annual report to support the findings regarding the impact of IFRS in relation to intangibles. The

report has also focused on the impact of the IFRS in relation to the intangible assets. The latter

part of the study has also commented on whether these concerns may be materialised (Karadag,

2015).

Introduction

On 1st January 2005, it was declared by “Financial Reporting Council (FRC)” that the

Australian entities needed to mandatorily adhere to the international accounting standards. In

previous years the companies needed to comply with only Corporations Act, which was only

standard to be followed for the Australian organisations. Therefore, AASB took the decision to

introduce the different types of the standards associated to the “International Financial

Reporting Standards (IFRS)”. However, the impact of the IFRS implementation was seen to be

based on the changes in the reporting associated the liabilities, assets, equities and the surplus of

the local government companies in Australia (Epstein, 2018).

The main discourse of the study is focused on evaluating the net impact of the

implementation of IFRS in the Australian entities. The study has used excerpts from Wesfarmers

annual report to support the findings regarding the impact of IFRS in relation to intangibles. The

report has also focused on the impact of the IFRS in relation to the intangible assets. The latter

part of the study has also commented on whether these concerns may be materialised (Karadag,

2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FOUNDATIONS IN ACCOUNTING

Discussion

The objectives of the IAS 38 were seen to be depicted with the accounting treatment for

the intangible which were not dealt with as per the specification of IAS. This standard was

required for the enterprise to identify the intangible assets only in case certain criteria was not

met. The standard has been also able to identify the measures to show the intangible assets

recognition carried out with certain disclosures related to the intangible assets (Allais & Gobert,

2016). The scope of the IAS is seen to be applicable to the intangible assets other than the

financial assets. The accounting standard has been further related to the significant nature of the

consideration associated to the mineral rights and exploration along with the developmental costs

as per the gas companies and miming oil (Paul, Parthasarathy & Gupta, 2017).

The criterion of the categorization of the information as per the intangible assets has been

also seen to be depicted with the different types of the consideration as per the non-monetary

asset which is not seen with physical evidence. The asset is also depicted with the past events

and future economic benefits. The three main critical attributes are seen to be based on the

identifiability, future economic benefits and control factor (Bello et al., 2016).

The main concerns of the impact pertaining to the IFRS in this section relates to the

introduction of “AASB 138, Intangible Assets” by the international accounting standards. The

implementation of the IFRS is depicted to write off a substantial amount of the intangibles which

was previously capitalised and revalued as per the Corporations Act. The significant nature of

the identifiable assets acquired in a business combination needed to recognise the goodwill

separately. The IFRS needed the intangible asset to recognise the opening of the retained

Discussion

The objectives of the IAS 38 were seen to be depicted with the accounting treatment for

the intangible which were not dealt with as per the specification of IAS. This standard was

required for the enterprise to identify the intangible assets only in case certain criteria was not

met. The standard has been also able to identify the measures to show the intangible assets

recognition carried out with certain disclosures related to the intangible assets (Allais & Gobert,

2016). The scope of the IAS is seen to be applicable to the intangible assets other than the

financial assets. The accounting standard has been further related to the significant nature of the

consideration associated to the mineral rights and exploration along with the developmental costs

as per the gas companies and miming oil (Paul, Parthasarathy & Gupta, 2017).

The criterion of the categorization of the information as per the intangible assets has been

also seen to be depicted with the different types of the consideration as per the non-monetary

asset which is not seen with physical evidence. The asset is also depicted with the past events

and future economic benefits. The three main critical attributes are seen to be based on the

identifiability, future economic benefits and control factor (Bello et al., 2016).

The main concerns of the impact pertaining to the IFRS in this section relates to the

introduction of “AASB 138, Intangible Assets” by the international accounting standards. The

implementation of the IFRS is depicted to write off a substantial amount of the intangibles which

was previously capitalised and revalued as per the Corporations Act. The significant nature of

the identifiable assets acquired in a business combination needed to recognise the goodwill

separately. The IFRS needed the intangible asset to recognise the opening of the retained

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FOUNDATIONS IN ACCOUNTING

earnings which are included in opening balance of the retained earnings (Eniola, Entebang &

Sakariyau, 2015).

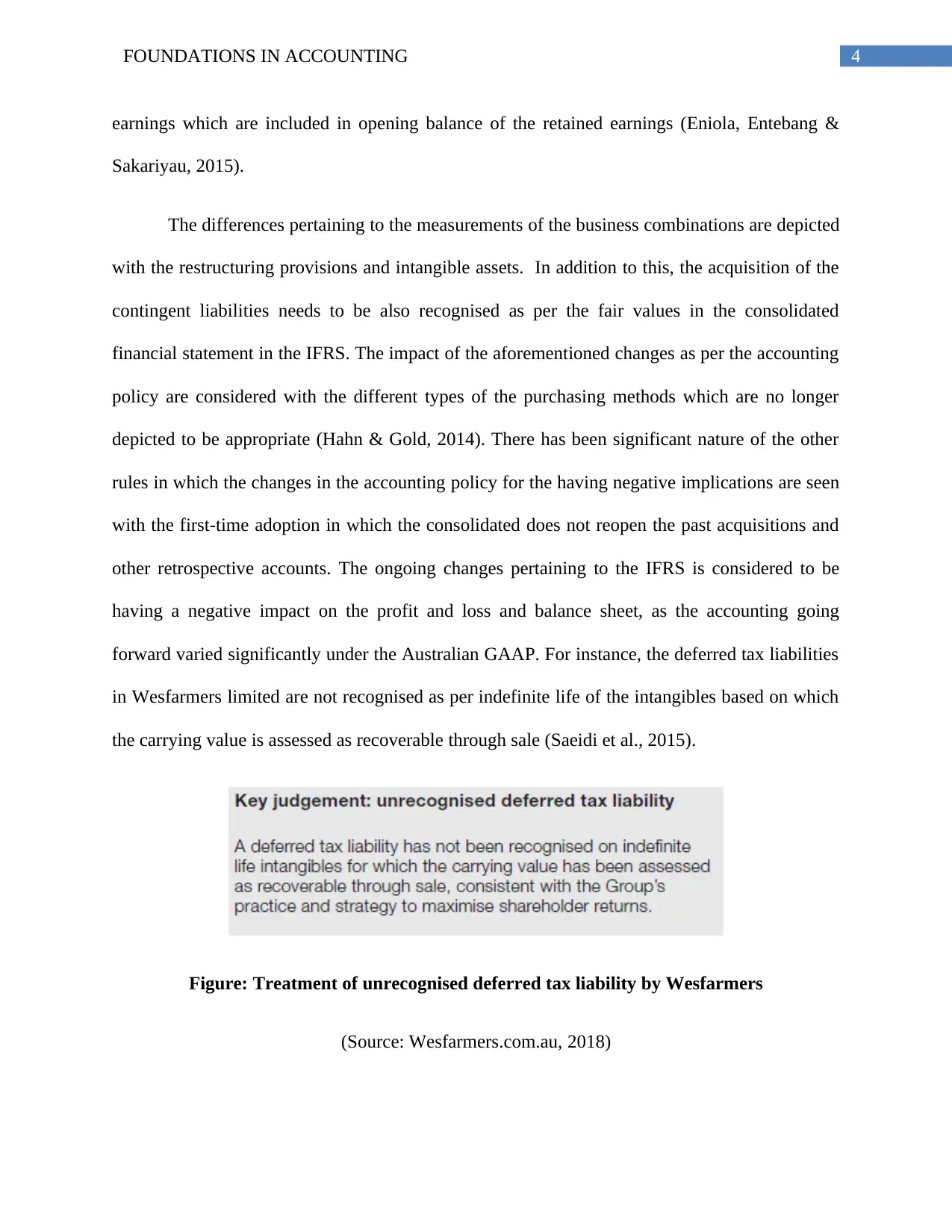

The differences pertaining to the measurements of the business combinations are depicted

with the restructuring provisions and intangible assets. In addition to this, the acquisition of the

contingent liabilities needs to be also recognised as per the fair values in the consolidated

financial statement in the IFRS. The impact of the aforementioned changes as per the accounting

policy are considered with the different types of the purchasing methods which are no longer

depicted to be appropriate (Hahn & Gold, 2014). There has been significant nature of the other

rules in which the changes in the accounting policy for the having negative implications are seen

with the first-time adoption in which the consolidated does not reopen the past acquisitions and

other retrospective accounts. The ongoing changes pertaining to the IFRS is considered to be

having a negative impact on the profit and loss and balance sheet, as the accounting going

forward varied significantly under the Australian GAAP. For instance, the deferred tax liabilities

in Wesfarmers limited are not recognised as per indefinite life of the intangibles based on which

the carrying value is assessed as recoverable through sale (Saeidi et al., 2015).

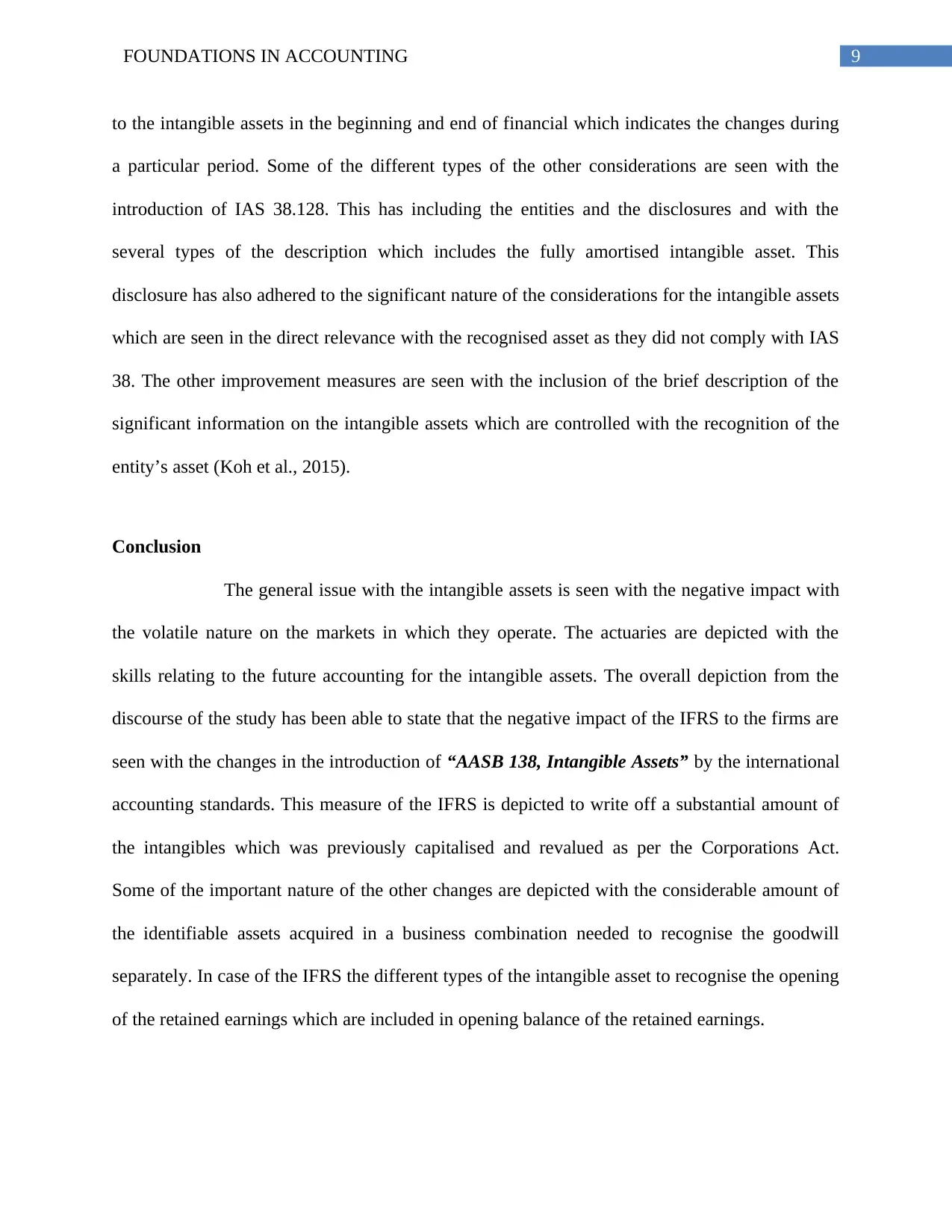

Figure: Treatment of unrecognised deferred tax liability by Wesfarmers

(Source: Wesfarmers.com.au, 2018)

earnings which are included in opening balance of the retained earnings (Eniola, Entebang &

Sakariyau, 2015).

The differences pertaining to the measurements of the business combinations are depicted

with the restructuring provisions and intangible assets. In addition to this, the acquisition of the

contingent liabilities needs to be also recognised as per the fair values in the consolidated

financial statement in the IFRS. The impact of the aforementioned changes as per the accounting

policy are considered with the different types of the purchasing methods which are no longer

depicted to be appropriate (Hahn & Gold, 2014). There has been significant nature of the other

rules in which the changes in the accounting policy for the having negative implications are seen

with the first-time adoption in which the consolidated does not reopen the past acquisitions and

other retrospective accounts. The ongoing changes pertaining to the IFRS is considered to be

having a negative impact on the profit and loss and balance sheet, as the accounting going

forward varied significantly under the Australian GAAP. For instance, the deferred tax liabilities

in Wesfarmers limited are not recognised as per indefinite life of the intangibles based on which

the carrying value is assessed as recoverable through sale (Saeidi et al., 2015).

Figure: Treatment of unrecognised deferred tax liability by Wesfarmers

(Source: Wesfarmers.com.au, 2018)

5FOUNDATIONS IN ACCOUNTING

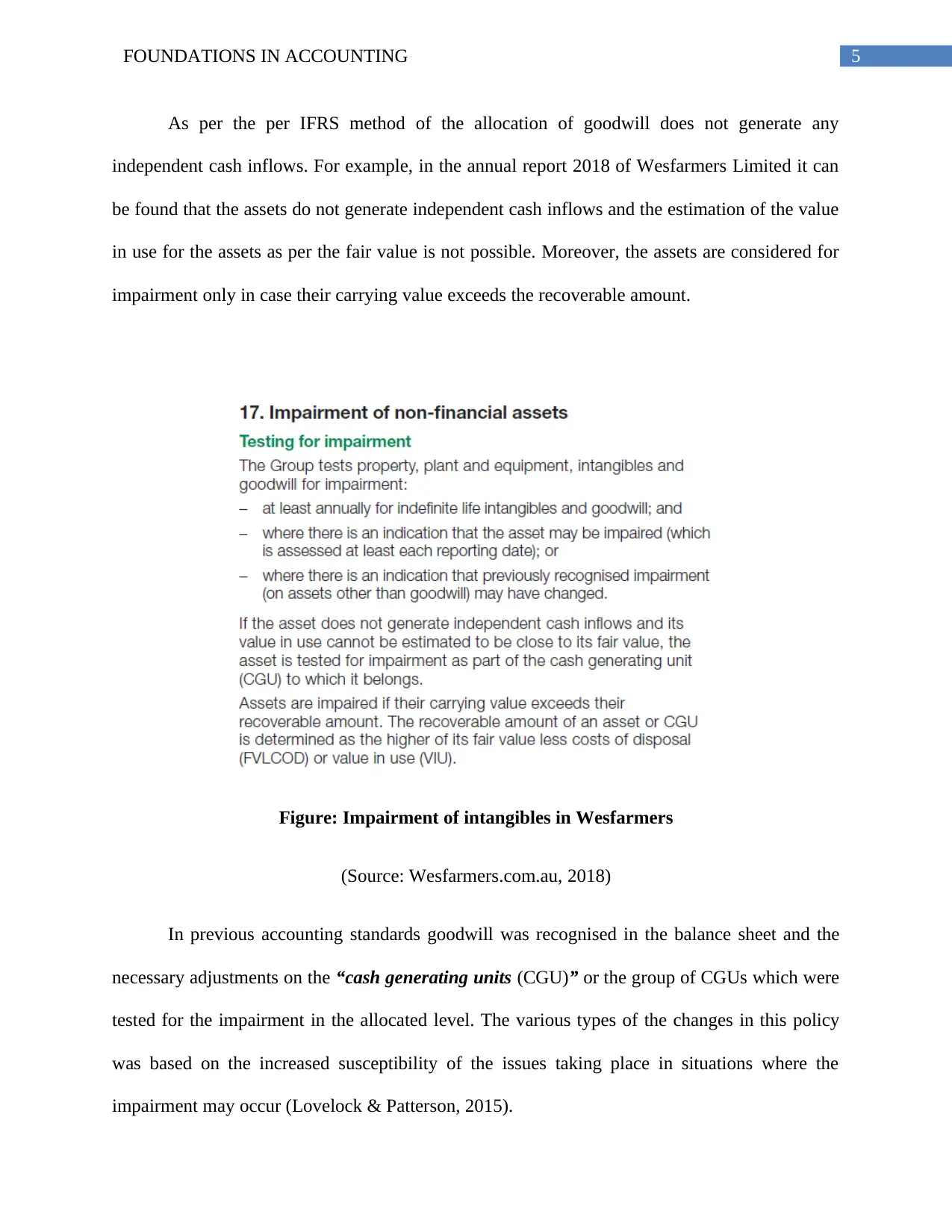

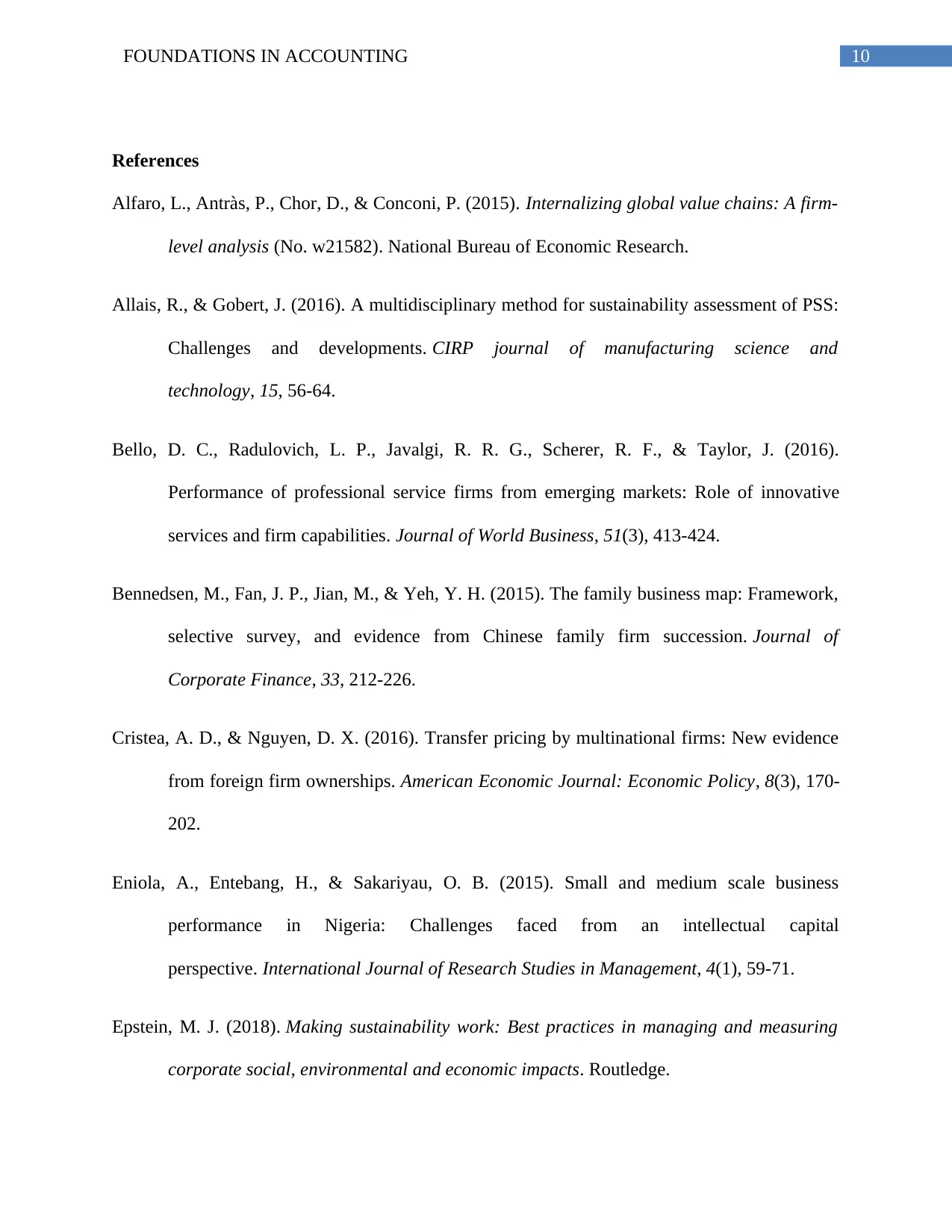

As per the per IFRS method of the allocation of goodwill does not generate any

independent cash inflows. For example, in the annual report 2018 of Wesfarmers Limited it can

be found that the assets do not generate independent cash inflows and the estimation of the value

in use for the assets as per the fair value is not possible. Moreover, the assets are considered for

impairment only in case their carrying value exceeds the recoverable amount.

Figure: Impairment of intangibles in Wesfarmers

(Source: Wesfarmers.com.au, 2018)

In previous accounting standards goodwill was recognised in the balance sheet and the

necessary adjustments on the “cash generating units (CGU)” or the group of CGUs which were

tested for the impairment in the allocated level. The various types of the changes in this policy

was based on the increased susceptibility of the issues taking place in situations where the

impairment may occur (Lovelock & Patterson, 2015).

As per the per IFRS method of the allocation of goodwill does not generate any

independent cash inflows. For example, in the annual report 2018 of Wesfarmers Limited it can

be found that the assets do not generate independent cash inflows and the estimation of the value

in use for the assets as per the fair value is not possible. Moreover, the assets are considered for

impairment only in case their carrying value exceeds the recoverable amount.

Figure: Impairment of intangibles in Wesfarmers

(Source: Wesfarmers.com.au, 2018)

In previous accounting standards goodwill was recognised in the balance sheet and the

necessary adjustments on the “cash generating units (CGU)” or the group of CGUs which were

tested for the impairment in the allocated level. The various types of the changes in this policy

was based on the increased susceptibility of the issues taking place in situations where the

impairment may occur (Lovelock & Patterson, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FOUNDATIONS IN ACCOUNTING

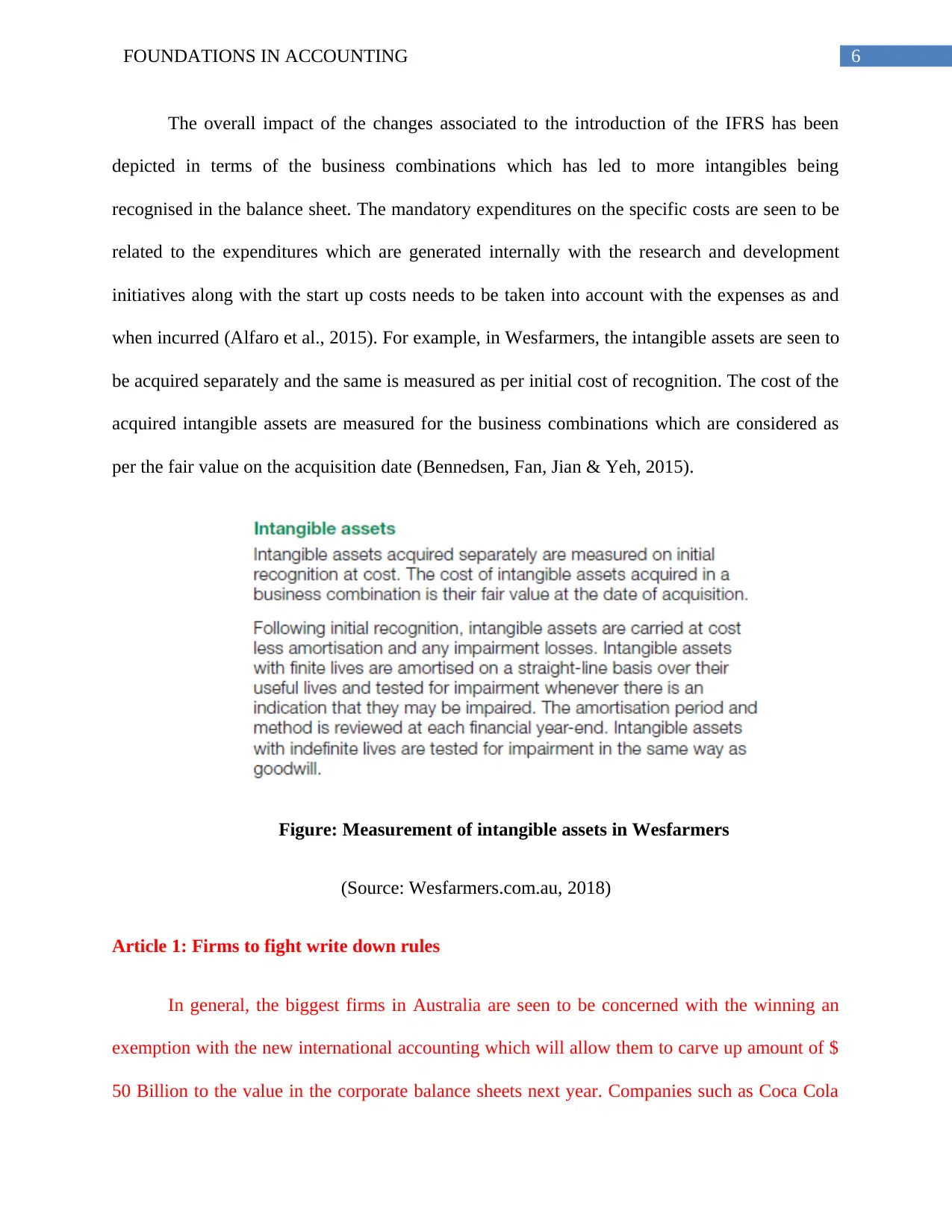

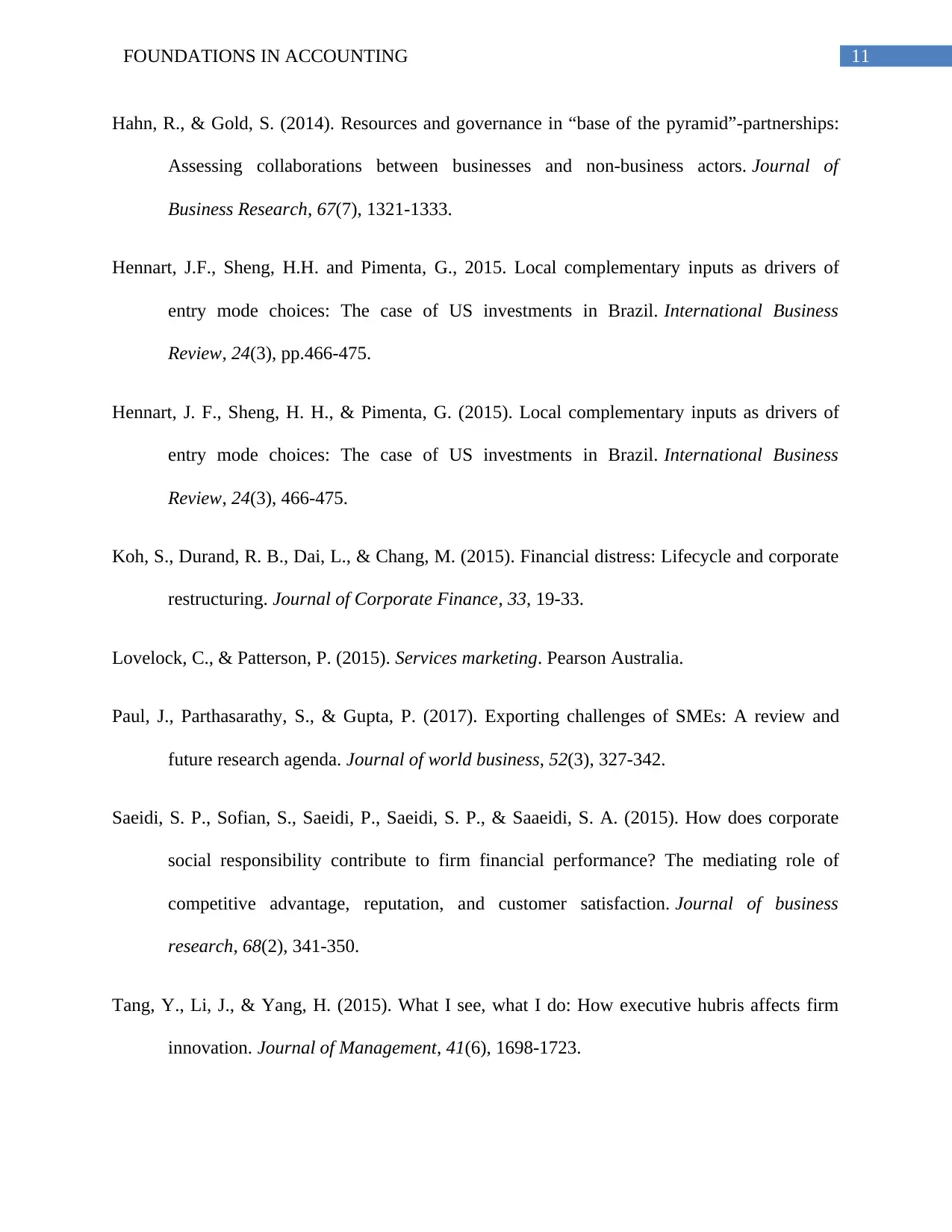

The overall impact of the changes associated to the introduction of the IFRS has been

depicted in terms of the business combinations which has led to more intangibles being

recognised in the balance sheet. The mandatory expenditures on the specific costs are seen to be

related to the expenditures which are generated internally with the research and development

initiatives along with the start up costs needs to be taken into account with the expenses as and

when incurred (Alfaro et al., 2015). For example, in Wesfarmers, the intangible assets are seen to

be acquired separately and the same is measured as per initial cost of recognition. The cost of the

acquired intangible assets are measured for the business combinations which are considered as

per the fair value on the acquisition date (Bennedsen, Fan, Jian & Yeh, 2015).

Figure: Measurement of intangible assets in Wesfarmers

(Source: Wesfarmers.com.au, 2018)

Article 1: Firms to fight write down rules

In general, the biggest firms in Australia are seen to be concerned with the winning an

exemption with the new international accounting which will allow them to carve up amount of $

50 Billion to the value in the corporate balance sheets next year. Companies such as Coca Cola

The overall impact of the changes associated to the introduction of the IFRS has been

depicted in terms of the business combinations which has led to more intangibles being

recognised in the balance sheet. The mandatory expenditures on the specific costs are seen to be

related to the expenditures which are generated internally with the research and development

initiatives along with the start up costs needs to be taken into account with the expenses as and

when incurred (Alfaro et al., 2015). For example, in Wesfarmers, the intangible assets are seen to

be acquired separately and the same is measured as per initial cost of recognition. The cost of the

acquired intangible assets are measured for the business combinations which are considered as

per the fair value on the acquisition date (Bennedsen, Fan, Jian & Yeh, 2015).

Figure: Measurement of intangible assets in Wesfarmers

(Source: Wesfarmers.com.au, 2018)

Article 1: Firms to fight write down rules

In general, the biggest firms in Australia are seen to be concerned with the winning an

exemption with the new international accounting which will allow them to carve up amount of $

50 Billion to the value in the corporate balance sheets next year. Companies such as Coca Cola

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FOUNDATIONS IN ACCOUNTING

and Foster's Lion Nathan are concerned with the writing off the values for adopted as per the

standards on the valuation on the intangible assets. The main changes are concerned to be

affecting the company’s and revaluing the intangible assets in which there has been no active and

liquid market present. Some of these are considered with the inclusion of the newspaper

mastheads and license agreements along with management of the rights at the property trusts.

Implementation of the G 100 standards is seen to be having a significant effect on the balance

sheet of the company which are associated to the implementation of the new rules. The

intangible assets are seen to be considered with the carrying cost as there will be no write down.

However, in case an asset is depicted to be generated as per the internal revaluation it is

mandatory to write it off. The PBL annual report is seen to be considered as per the cost

valuation and the cost considerations which are seen with the written down value (Tang, Li . &

Yang, 2015).

AASB chairman David Boymal was seeking for exemption from the standards. The

different types of the other standards as per the AASB was obliged with the directives of the

FRC along with the international regulators and monitoring the accounting standards. in various

cases the considerations for the FRC is seen to be having the sympathy for the plight of the

corporates. Despite of this, it needs to be discerned that the new standards has overridden the

demand pertaining to the exemption (Cristea & Nguyen, 2016).

The recognition of the various types of the intangible assets for the company is also

categorised into concerns leading to impact on the volatile nature of the market. In general, the

relevance of the intangible assets is seen with the negative impact with the volatile nature on the

markets in which they operate. The actuaries in particular are depicted with the skills relating to

the future accounting for the intangible assets (Hennart, Sheng & Pimenta, 2015).

and Foster's Lion Nathan are concerned with the writing off the values for adopted as per the

standards on the valuation on the intangible assets. The main changes are concerned to be

affecting the company’s and revaluing the intangible assets in which there has been no active and

liquid market present. Some of these are considered with the inclusion of the newspaper

mastheads and license agreements along with management of the rights at the property trusts.

Implementation of the G 100 standards is seen to be having a significant effect on the balance

sheet of the company which are associated to the implementation of the new rules. The

intangible assets are seen to be considered with the carrying cost as there will be no write down.

However, in case an asset is depicted to be generated as per the internal revaluation it is

mandatory to write it off. The PBL annual report is seen to be considered as per the cost

valuation and the cost considerations which are seen with the written down value (Tang, Li . &

Yang, 2015).

AASB chairman David Boymal was seeking for exemption from the standards. The

different types of the other standards as per the AASB was obliged with the directives of the

FRC along with the international regulators and monitoring the accounting standards. in various

cases the considerations for the FRC is seen to be having the sympathy for the plight of the

corporates. Despite of this, it needs to be discerned that the new standards has overridden the

demand pertaining to the exemption (Cristea & Nguyen, 2016).

The recognition of the various types of the intangible assets for the company is also

categorised into concerns leading to impact on the volatile nature of the market. In general, the

relevance of the intangible assets is seen with the negative impact with the volatile nature on the

markets in which they operate. The actuaries in particular are depicted with the skills relating to

the future accounting for the intangible assets (Hennart, Sheng & Pimenta, 2015).

8FOUNDATIONS IN ACCOUNTING

Article 2: Media to feel IFRS cut the deepest

The impact of IFRS among the media companies is expected to be more than $ 1 Billion

pertaining to the non-cash write-downs at the time of adoption of new accounting standards. The

problem is more evident among the media groups as the hybrid securities such as Seven Network

must be able to reclassify the securities as debt for increasing the financial gearing ratio. Such a

measure was not needed in the traditional accounting standards. Moreover, in case the intangible

assets are carried at cost then no write-offs will be taken into account, only the assets generated

from the internal revaluation will be written down. The television companies such as Seven

reported in its annual report that needs to write back an amount of $480 million for increasing

the independent valuer applied to its TV licences in 1998. This will significant increase the debt

of the company by $315 million when TELYS (hybrid security) are reclassified as debt.

Materialisation of the concerns

The IFRS has comprehensively dealt with the initial recognition and the subsequent

expenditure and the derecognition of the intangible assets. The various types of steps taken to

materialise the present state of the concerns are seen with the IAS 38.124 disclosure. This stated

that in case intangible assets are revalued then the entity needs to be considered with the various

class of the intangible assets. The main implementation for this is seen with the effective data of

the revaluation and carrying amount based on the revaluation of the intangible assets. In addition

to this, CPA is introducing several types of the changes which will be focusing on the carrying

value which will have to be recognised as per the revalued class of the intangible assets and

measured after the recognition of the cost model. In addition to this, the revaluation amount has

been depicted with the significant consideration of the reserved which are depicted to be related

Article 2: Media to feel IFRS cut the deepest

The impact of IFRS among the media companies is expected to be more than $ 1 Billion

pertaining to the non-cash write-downs at the time of adoption of new accounting standards. The

problem is more evident among the media groups as the hybrid securities such as Seven Network

must be able to reclassify the securities as debt for increasing the financial gearing ratio. Such a

measure was not needed in the traditional accounting standards. Moreover, in case the intangible

assets are carried at cost then no write-offs will be taken into account, only the assets generated

from the internal revaluation will be written down. The television companies such as Seven

reported in its annual report that needs to write back an amount of $480 million for increasing

the independent valuer applied to its TV licences in 1998. This will significant increase the debt

of the company by $315 million when TELYS (hybrid security) are reclassified as debt.

Materialisation of the concerns

The IFRS has comprehensively dealt with the initial recognition and the subsequent

expenditure and the derecognition of the intangible assets. The various types of steps taken to

materialise the present state of the concerns are seen with the IAS 38.124 disclosure. This stated

that in case intangible assets are revalued then the entity needs to be considered with the various

class of the intangible assets. The main implementation for this is seen with the effective data of

the revaluation and carrying amount based on the revaluation of the intangible assets. In addition

to this, CPA is introducing several types of the changes which will be focusing on the carrying

value which will have to be recognised as per the revalued class of the intangible assets and

measured after the recognition of the cost model. In addition to this, the revaluation amount has

been depicted with the significant consideration of the reserved which are depicted to be related

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FOUNDATIONS IN ACCOUNTING

to the intangible assets in the beginning and end of financial which indicates the changes during

a particular period. Some of the different types of the other considerations are seen with the

introduction of IAS 38.128. This has including the entities and the disclosures and with the

several types of the description which includes the fully amortised intangible asset. This

disclosure has also adhered to the significant nature of the considerations for the intangible assets

which are seen in the direct relevance with the recognised asset as they did not comply with IAS

38. The other improvement measures are seen with the inclusion of the brief description of the

significant information on the intangible assets which are controlled with the recognition of the

entity’s asset (Koh et al., 2015).

Conclusion

The general issue with the intangible assets is seen with the negative impact with

the volatile nature on the markets in which they operate. The actuaries are depicted with the

skills relating to the future accounting for the intangible assets. The overall depiction from the

discourse of the study has been able to state that the negative impact of the IFRS to the firms are

seen with the changes in the introduction of “AASB 138, Intangible Assets” by the international

accounting standards. This measure of the IFRS is depicted to write off a substantial amount of

the intangibles which was previously capitalised and revalued as per the Corporations Act.

Some of the important nature of the other changes are depicted with the considerable amount of

the identifiable assets acquired in a business combination needed to recognise the goodwill

separately. In case of the IFRS the different types of the intangible asset to recognise the opening

of the retained earnings which are included in opening balance of the retained earnings.

to the intangible assets in the beginning and end of financial which indicates the changes during

a particular period. Some of the different types of the other considerations are seen with the

introduction of IAS 38.128. This has including the entities and the disclosures and with the

several types of the description which includes the fully amortised intangible asset. This

disclosure has also adhered to the significant nature of the considerations for the intangible assets

which are seen in the direct relevance with the recognised asset as they did not comply with IAS

38. The other improvement measures are seen with the inclusion of the brief description of the

significant information on the intangible assets which are controlled with the recognition of the

entity’s asset (Koh et al., 2015).

Conclusion

The general issue with the intangible assets is seen with the negative impact with

the volatile nature on the markets in which they operate. The actuaries are depicted with the

skills relating to the future accounting for the intangible assets. The overall depiction from the

discourse of the study has been able to state that the negative impact of the IFRS to the firms are

seen with the changes in the introduction of “AASB 138, Intangible Assets” by the international

accounting standards. This measure of the IFRS is depicted to write off a substantial amount of

the intangibles which was previously capitalised and revalued as per the Corporations Act.

Some of the important nature of the other changes are depicted with the considerable amount of

the identifiable assets acquired in a business combination needed to recognise the goodwill

separately. In case of the IFRS the different types of the intangible asset to recognise the opening

of the retained earnings which are included in opening balance of the retained earnings.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FOUNDATIONS IN ACCOUNTING

References

Alfaro, L., Antràs, P., Chor, D., & Conconi, P. (2015). Internalizing global value chains: A firm-

level analysis (No. w21582). National Bureau of Economic Research.

Allais, R., & Gobert, J. (2016). A multidisciplinary method for sustainability assessment of PSS:

Challenges and developments. CIRP journal of manufacturing science and

technology, 15, 56-64.

Bello, D. C., Radulovich, L. P., Javalgi, R. R. G., Scherer, R. F., & Taylor, J. (2016).

Performance of professional service firms from emerging markets: Role of innovative

services and firm capabilities. Journal of World Business, 51(3), 413-424.

Bennedsen, M., Fan, J. P., Jian, M., & Yeh, Y. H. (2015). The family business map: Framework,

selective survey, and evidence from Chinese family firm succession. Journal of

Corporate Finance, 33, 212-226.

Cristea, A. D., & Nguyen, D. X. (2016). Transfer pricing by multinational firms: New evidence

from foreign firm ownerships. American Economic Journal: Economic Policy, 8(3), 170-

202.

Eniola, A., Entebang, H., & Sakariyau, O. B. (2015). Small and medium scale business

performance in Nigeria: Challenges faced from an intellectual capital

perspective. International Journal of Research Studies in Management, 4(1), 59-71.

Epstein, M. J. (2018). Making sustainability work: Best practices in managing and measuring

corporate social, environmental and economic impacts. Routledge.

References

Alfaro, L., Antràs, P., Chor, D., & Conconi, P. (2015). Internalizing global value chains: A firm-

level analysis (No. w21582). National Bureau of Economic Research.

Allais, R., & Gobert, J. (2016). A multidisciplinary method for sustainability assessment of PSS:

Challenges and developments. CIRP journal of manufacturing science and

technology, 15, 56-64.

Bello, D. C., Radulovich, L. P., Javalgi, R. R. G., Scherer, R. F., & Taylor, J. (2016).

Performance of professional service firms from emerging markets: Role of innovative

services and firm capabilities. Journal of World Business, 51(3), 413-424.

Bennedsen, M., Fan, J. P., Jian, M., & Yeh, Y. H. (2015). The family business map: Framework,

selective survey, and evidence from Chinese family firm succession. Journal of

Corporate Finance, 33, 212-226.

Cristea, A. D., & Nguyen, D. X. (2016). Transfer pricing by multinational firms: New evidence

from foreign firm ownerships. American Economic Journal: Economic Policy, 8(3), 170-

202.

Eniola, A., Entebang, H., & Sakariyau, O. B. (2015). Small and medium scale business

performance in Nigeria: Challenges faced from an intellectual capital

perspective. International Journal of Research Studies in Management, 4(1), 59-71.

Epstein, M. J. (2018). Making sustainability work: Best practices in managing and measuring

corporate social, environmental and economic impacts. Routledge.

11FOUNDATIONS IN ACCOUNTING

Hahn, R., & Gold, S. (2014). Resources and governance in “base of the pyramid”-partnerships:

Assessing collaborations between businesses and non-business actors. Journal of

Business Research, 67(7), 1321-1333.

Hennart, J.F., Sheng, H.H. and Pimenta, G., 2015. Local complementary inputs as drivers of

entry mode choices: The case of US investments in Brazil. International Business

Review, 24(3), pp.466-475.

Hennart, J. F., Sheng, H. H., & Pimenta, G. (2015). Local complementary inputs as drivers of

entry mode choices: The case of US investments in Brazil. International Business

Review, 24(3), 466-475.

Koh, S., Durand, R. B., Dai, L., & Chang, M. (2015). Financial distress: Lifecycle and corporate

restructuring. Journal of Corporate Finance, 33, 19-33.

Lovelock, C., & Patterson, P. (2015). Services marketing. Pearson Australia.

Paul, J., Parthasarathy, S., & Gupta, P. (2017). Exporting challenges of SMEs: A review and

future research agenda. Journal of world business, 52(3), 327-342.

Saeidi, S. P., Sofian, S., Saeidi, P., Saeidi, S. P., & Saaeidi, S. A. (2015). How does corporate

social responsibility contribute to firm financial performance? The mediating role of

competitive advantage, reputation, and customer satisfaction. Journal of business

research, 68(2), 341-350.

Tang, Y., Li, J., & Yang, H. (2015). What I see, what I do: How executive hubris affects firm

innovation. Journal of Management, 41(6), 1698-1723.

Hahn, R., & Gold, S. (2014). Resources and governance in “base of the pyramid”-partnerships:

Assessing collaborations between businesses and non-business actors. Journal of

Business Research, 67(7), 1321-1333.

Hennart, J.F., Sheng, H.H. and Pimenta, G., 2015. Local complementary inputs as drivers of

entry mode choices: The case of US investments in Brazil. International Business

Review, 24(3), pp.466-475.

Hennart, J. F., Sheng, H. H., & Pimenta, G. (2015). Local complementary inputs as drivers of

entry mode choices: The case of US investments in Brazil. International Business

Review, 24(3), 466-475.

Koh, S., Durand, R. B., Dai, L., & Chang, M. (2015). Financial distress: Lifecycle and corporate

restructuring. Journal of Corporate Finance, 33, 19-33.

Lovelock, C., & Patterson, P. (2015). Services marketing. Pearson Australia.

Paul, J., Parthasarathy, S., & Gupta, P. (2017). Exporting challenges of SMEs: A review and

future research agenda. Journal of world business, 52(3), 327-342.

Saeidi, S. P., Sofian, S., Saeidi, P., Saeidi, S. P., & Saaeidi, S. A. (2015). How does corporate

social responsibility contribute to firm financial performance? The mediating role of

competitive advantage, reputation, and customer satisfaction. Journal of business

research, 68(2), 341-350.

Tang, Y., Li, J., & Yang, H. (2015). What I see, what I do: How executive hubris affects firm

innovation. Journal of Management, 41(6), 1698-1723.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.