IFRS Compliance: Flight Centre Travel's Contemporary Accounting Issues

VerifiedAdded on 2023/06/13

|15

|2275

|299

Report

AI Summary

This report analyzes Flight Centre Travel's adherence to the conceptual framework of the Australian Accounting Standards Board (AASB) and International Financial Reporting Standards (IFRS). It assesses the company's financial reporting practices, focusing on the reliability of financial information, analysis of uncertainties, and presentation of company resources. The report examines how Flight Centre Travel aligns with recognition criteria for assets, liabilities, equity, expenses, and revenue, as well as qualitative aspects like faithful representation, relevance, verifiability, comparability, understandability, and timeliness. The analysis confirms that Flight Centre Travel complies with IFRS regulations and provides valuable information to investors through its financial statements.

Running head: CONTEMPORARY ACCOUNTING ISSUES

Contemporary Accounting Issues

Name of the University:

Name of the Student:

Authors Note:

Contemporary Accounting Issues

Name of the University:

Name of the Student:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CONTEMPORARY ACCOUNTING ISSUES

Table of Contents

Introduction..........................................................................................................................2

Attaining conceptual framework objectives........................................................................2

Attaining conceptual framework-based recognition criteria...............................................5

Equity...............................................................................................................................6

Assets...............................................................................................................................6

Liabilities.........................................................................................................................7

Expense............................................................................................................................8

Revenue...........................................................................................................................9

Addressing qualitative aspects of conceptual framework...................................................9

Faithful Representation....................................................................................................9

Relevance.......................................................................................................................10

Verifiability....................................................................................................................10

Comparability................................................................................................................10

Understandability...........................................................................................................11

Timeliness......................................................................................................................11

Conclusion.........................................................................................................................11

References..........................................................................................................................13

Table of Contents

Introduction..........................................................................................................................2

Attaining conceptual framework objectives........................................................................2

Attaining conceptual framework-based recognition criteria...............................................5

Equity...............................................................................................................................6

Assets...............................................................................................................................6

Liabilities.........................................................................................................................7

Expense............................................................................................................................8

Revenue...........................................................................................................................9

Addressing qualitative aspects of conceptual framework...................................................9

Faithful Representation....................................................................................................9

Relevance.......................................................................................................................10

Verifiability....................................................................................................................10

Comparability................................................................................................................10

Understandability...........................................................................................................11

Timeliness......................................................................................................................11

Conclusion.........................................................................................................................11

References..........................................................................................................................13

2CONTEMPORARY ACCOUNTING ISSUES

Introduction

For developing the financial statements, the conceptual framework associated with the

financial reporting is vital for the companies in the recent years. This is due to the fact that it

offers significant course of action as well as the principles along with techniques required to

prepare all the financial reports (Biondi and Lapsley 2014). In addition to the fact that, the

conceptual framework might facilitate in dealing with several concerns of the corporate firms. In

order to improve the quality of the report Flight center travel company is chosen that is listed in

ASX top 100 companies. The objective of the report is to analyze the adherence of this company

in alignment with the conceptual framework.

Attaining conceptual framework objectives

The conceptual framework has an important function to play in dealing with the financial

factors of the companies. For addressing the needs of the financial reporting, such framework

was developed from the behalf of the “International Accounting Standards Board (IASB)” in the

year 1989 (Brown, Preiato and Tarca 2014). For this reason, the conceptual framework can

support in dealing with an organization’s financial aspects. Based on the company’s recent

annual report of 2017, the principles are presented within “Corporation Act 2001” and AASB are

ensured for general purpose financial reporting. Along with the same, the consolidated financial

statements are prepared relied on standards and principles of “International Financial Reporting

Standards (IFRS)” as well as “International Accounting Standards Board (IASB)”. For this

reason, the organization totally confirms with the regulations of financial reporting conceptual

framework of IFRS (Christensen, Lee Walker and Zeng 2015). For aligning with such

framework, it is also vital for the companies to address three specific objectives. These

Introduction

For developing the financial statements, the conceptual framework associated with the

financial reporting is vital for the companies in the recent years. This is due to the fact that it

offers significant course of action as well as the principles along with techniques required to

prepare all the financial reports (Biondi and Lapsley 2014). In addition to the fact that, the

conceptual framework might facilitate in dealing with several concerns of the corporate firms. In

order to improve the quality of the report Flight center travel company is chosen that is listed in

ASX top 100 companies. The objective of the report is to analyze the adherence of this company

in alignment with the conceptual framework.

Attaining conceptual framework objectives

The conceptual framework has an important function to play in dealing with the financial

factors of the companies. For addressing the needs of the financial reporting, such framework

was developed from the behalf of the “International Accounting Standards Board (IASB)” in the

year 1989 (Brown, Preiato and Tarca 2014). For this reason, the conceptual framework can

support in dealing with an organization’s financial aspects. Based on the company’s recent

annual report of 2017, the principles are presented within “Corporation Act 2001” and AASB are

ensured for general purpose financial reporting. Along with the same, the consolidated financial

statements are prepared relied on standards and principles of “International Financial Reporting

Standards (IFRS)” as well as “International Accounting Standards Board (IASB)”. For this

reason, the organization totally confirms with the regulations of financial reporting conceptual

framework of IFRS (Christensen, Lee Walker and Zeng 2015). For aligning with such

framework, it is also vital for the companies to address three specific objectives. These

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CONTEMPORARY ACCOUNTING ISSUES

objectives along with the degree to which the organization aligns with such objectives are

examined below:

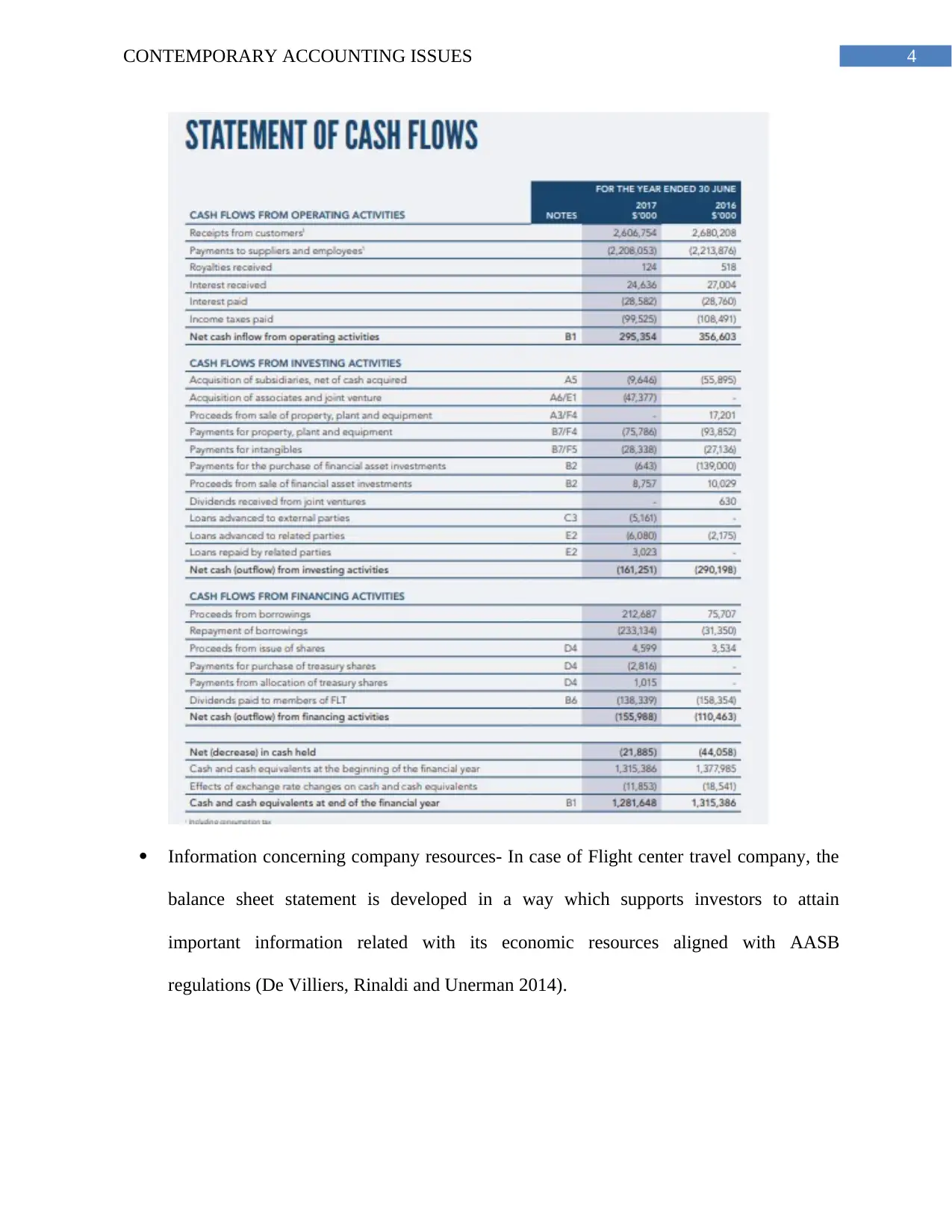

Reliable financial information- The annual report of the company indicates that it offers

timely information regarding financial statements to its investors to make effective

investment decisions (Crawford et al. 2014).

Analysis of amount, timing and uncertainties- It is important to offer important

information to its investors in evaluating amount, uncertainties and timing that is aligned

with Flight center travel company’s cash flow.

objectives along with the degree to which the organization aligns with such objectives are

examined below:

Reliable financial information- The annual report of the company indicates that it offers

timely information regarding financial statements to its investors to make effective

investment decisions (Crawford et al. 2014).

Analysis of amount, timing and uncertainties- It is important to offer important

information to its investors in evaluating amount, uncertainties and timing that is aligned

with Flight center travel company’s cash flow.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CONTEMPORARY ACCOUNTING ISSUES

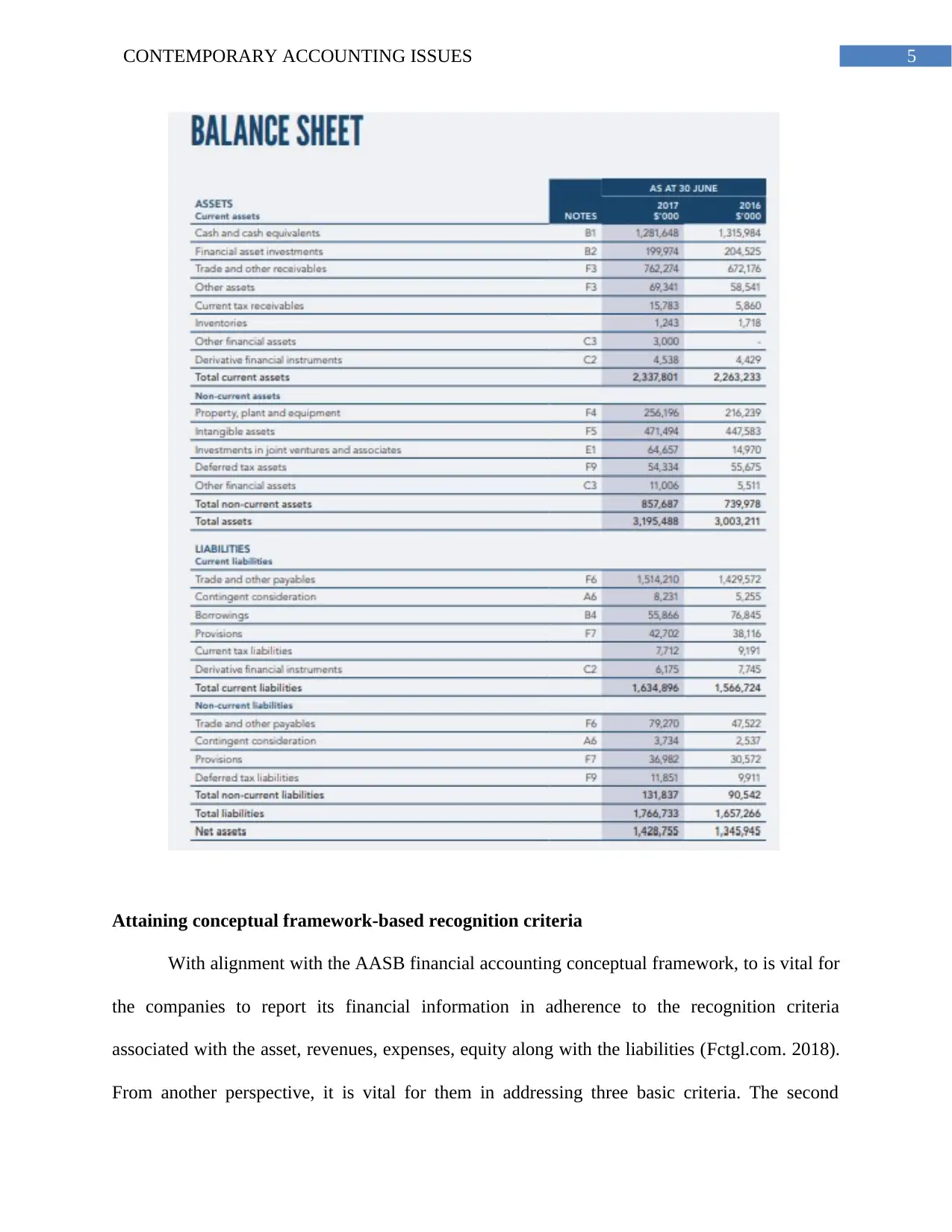

Information concerning company resources- In case of Flight center travel company, the

balance sheet statement is developed in a way which supports investors to attain

important information related with its economic resources aligned with AASB

regulations (De Villiers, Rinaldi and Unerman 2014).

Information concerning company resources- In case of Flight center travel company, the

balance sheet statement is developed in a way which supports investors to attain

important information related with its economic resources aligned with AASB

regulations (De Villiers, Rinaldi and Unerman 2014).

5CONTEMPORARY ACCOUNTING ISSUES

Attaining conceptual framework-based recognition criteria

With alignment with the AASB financial accounting conceptual framework, to is vital for

the companies to report its financial information in adherence to the recognition criteria

associated with the asset, revenues, expenses, equity along with the liabilities (Fctgl.com. 2018).

From another perspective, it is vital for them in addressing three basic criteria. The second

Attaining conceptual framework-based recognition criteria

With alignment with the AASB financial accounting conceptual framework, to is vital for

the companies to report its financial information in adherence to the recognition criteria

associated with the asset, revenues, expenses, equity along with the liabilities (Fctgl.com. 2018).

From another perspective, it is vital for them in addressing three basic criteria. The second

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CONTEMPORARY ACCOUNTING ISSUES

criteria are to offer a viewpoint on the financial aspects that have important information in a

faithful manner. The final criteria are to enhance the usefulness of such aspects for the investors.

Such criteria are analyzed with respect to Flight center travel company in order to determine its

adherence with AASB conceptual framework that is explained below:

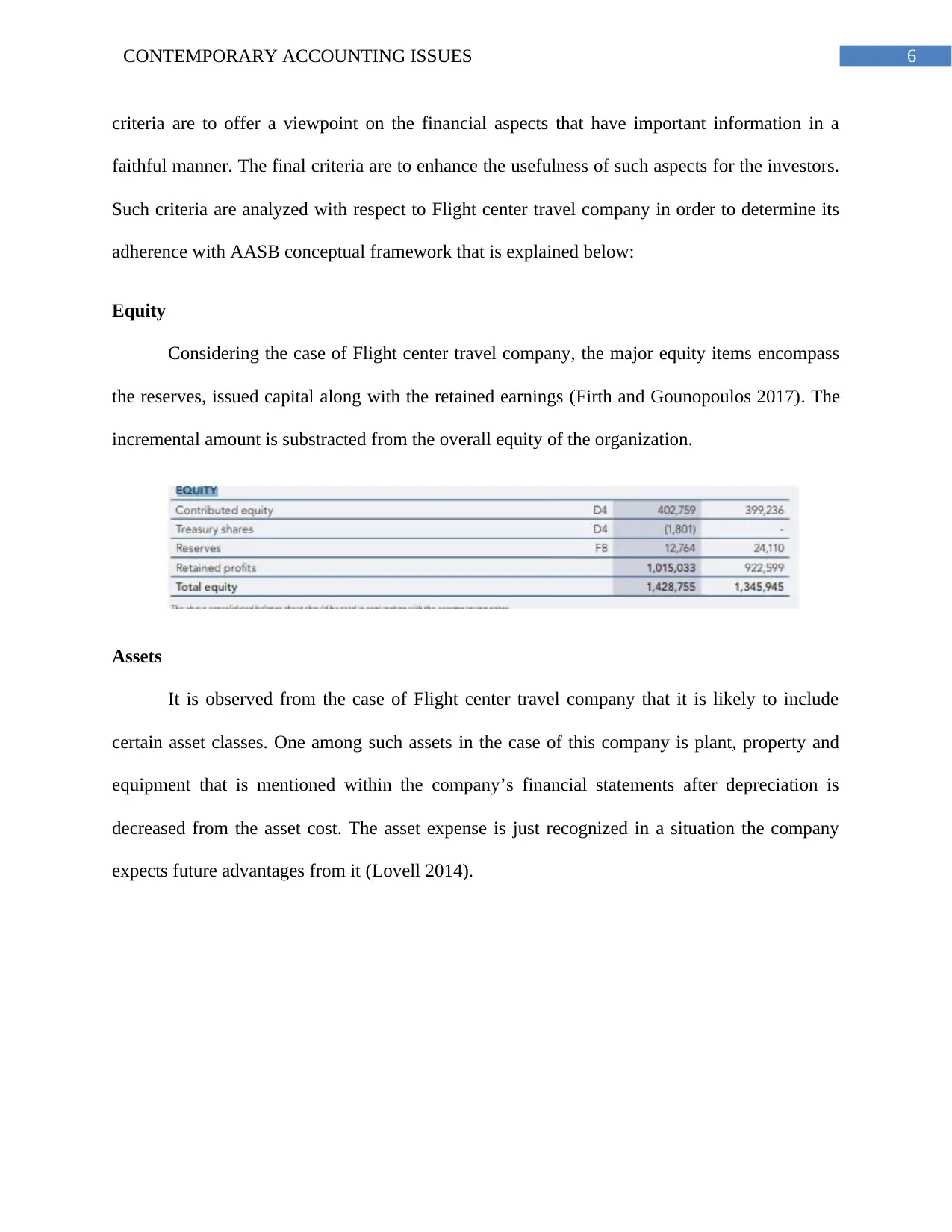

Equity

Considering the case of Flight center travel company, the major equity items encompass

the reserves, issued capital along with the retained earnings (Firth and Gounopoulos 2017). The

incremental amount is substracted from the overall equity of the organization.

Assets

It is observed from the case of Flight center travel company that it is likely to include

certain asset classes. One among such assets in the case of this company is plant, property and

equipment that is mentioned within the company’s financial statements after depreciation is

decreased from the asset cost. The asset expense is just recognized in a situation the company

expects future advantages from it (Lovell 2014).

criteria are to offer a viewpoint on the financial aspects that have important information in a

faithful manner. The final criteria are to enhance the usefulness of such aspects for the investors.

Such criteria are analyzed with respect to Flight center travel company in order to determine its

adherence with AASB conceptual framework that is explained below:

Equity

Considering the case of Flight center travel company, the major equity items encompass

the reserves, issued capital along with the retained earnings (Firth and Gounopoulos 2017). The

incremental amount is substracted from the overall equity of the organization.

Assets

It is observed from the case of Flight center travel company that it is likely to include

certain asset classes. One among such assets in the case of this company is plant, property and

equipment that is mentioned within the company’s financial statements after depreciation is

decreased from the asset cost. The asset expense is just recognized in a situation the company

expects future advantages from it (Lovell 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY ACCOUNTING ISSUES

Liabilities

Flight center travel company has two distinct capability types that is evident from its

annual report. It identifies the deferred tax liabilities relied on the variations in the tax rate.

Through observing the contingent liabilities, the major items are taken into account in case the

company includes guarantees, capital expenses, joint expenses as well as legal along with

regulatory surroundings (Mayne 2017). As per the views of Flight center travel company’s

management the company do not need any provision for such obligations because of the

Liabilities

Flight center travel company has two distinct capability types that is evident from its

annual report. It identifies the deferred tax liabilities relied on the variations in the tax rate.

Through observing the contingent liabilities, the major items are taken into account in case the

company includes guarantees, capital expenses, joint expenses as well as legal along with

regulatory surroundings (Mayne 2017). As per the views of Flight center travel company’s

management the company do not need any provision for such obligations because of the

8CONTEMPORARY ACCOUNTING ISSUES

decreased chance that economic advantages can get decreased in future or unreliable amount

measurement might take place.

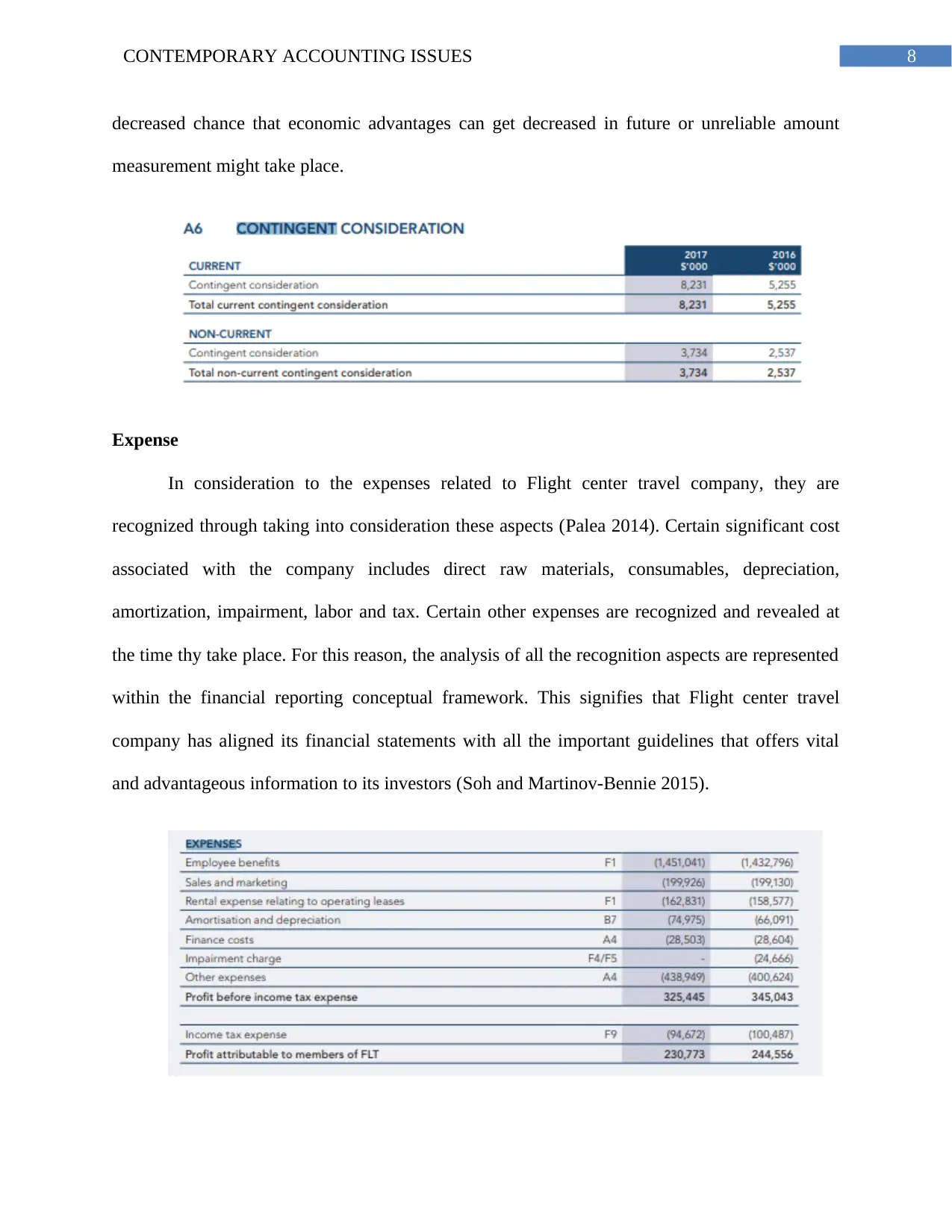

Expense

In consideration to the expenses related to Flight center travel company, they are

recognized through taking into consideration these aspects (Palea 2014). Certain significant cost

associated with the company includes direct raw materials, consumables, depreciation,

amortization, impairment, labor and tax. Certain other expenses are recognized and revealed at

the time thy take place. For this reason, the analysis of all the recognition aspects are represented

within the financial reporting conceptual framework. This signifies that Flight center travel

company has aligned its financial statements with all the important guidelines that offers vital

and advantageous information to its investors (Soh and Martinov-Bennie 2015).

decreased chance that economic advantages can get decreased in future or unreliable amount

measurement might take place.

Expense

In consideration to the expenses related to Flight center travel company, they are

recognized through taking into consideration these aspects (Palea 2014). Certain significant cost

associated with the company includes direct raw materials, consumables, depreciation,

amortization, impairment, labor and tax. Certain other expenses are recognized and revealed at

the time thy take place. For this reason, the analysis of all the recognition aspects are represented

within the financial reporting conceptual framework. This signifies that Flight center travel

company has aligned its financial statements with all the important guidelines that offers vital

and advantageous information to its investors (Soh and Martinov-Bennie 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CONTEMPORARY ACCOUNTING ISSUES

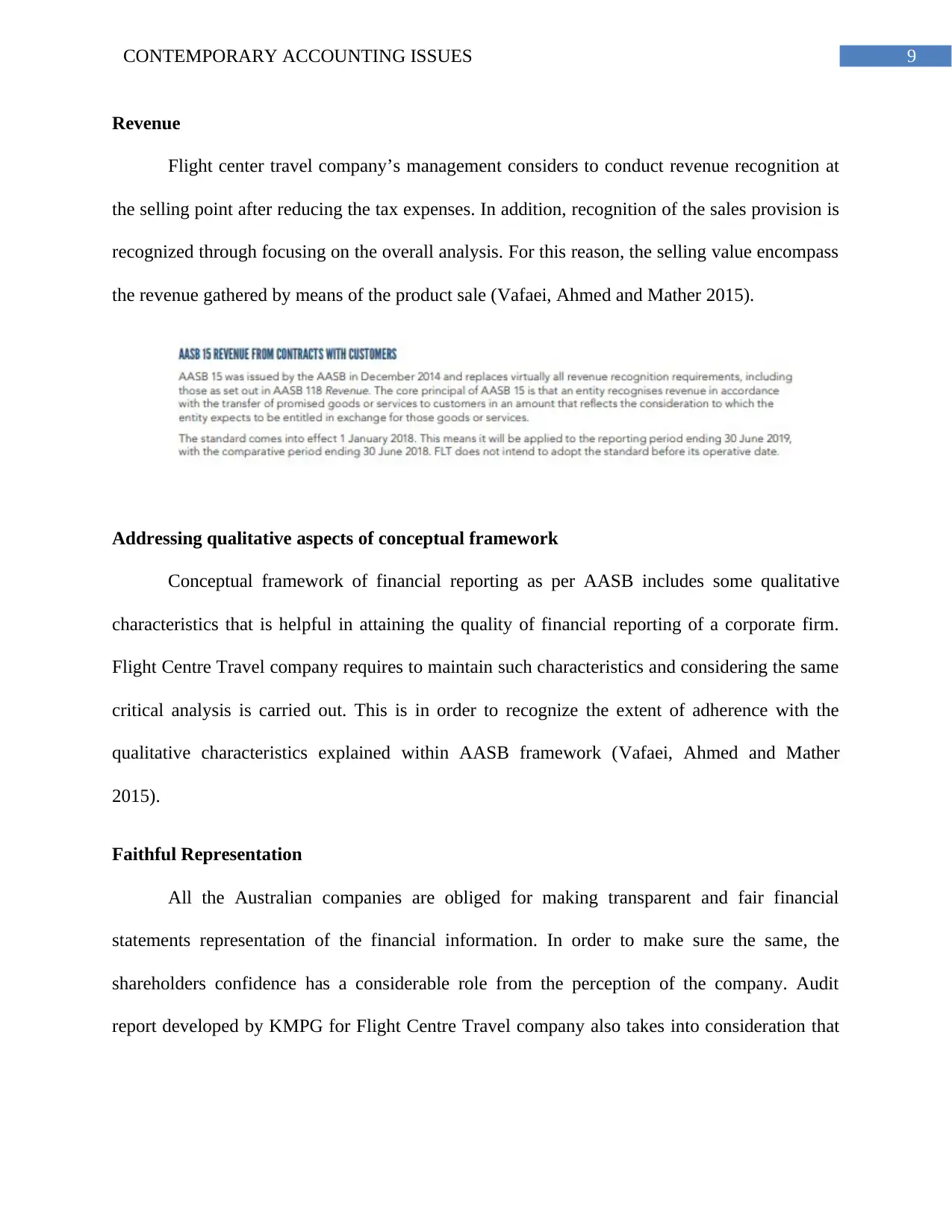

Revenue

Flight center travel company’s management considers to conduct revenue recognition at

the selling point after reducing the tax expenses. In addition, recognition of the sales provision is

recognized through focusing on the overall analysis. For this reason, the selling value encompass

the revenue gathered by means of the product sale (Vafaei, Ahmed and Mather 2015).

Addressing qualitative aspects of conceptual framework

Conceptual framework of financial reporting as per AASB includes some qualitative

characteristics that is helpful in attaining the quality of financial reporting of a corporate firm.

Flight Centre Travel company requires to maintain such characteristics and considering the same

critical analysis is carried out. This is in order to recognize the extent of adherence with the

qualitative characteristics explained within AASB framework (Vafaei, Ahmed and Mather

2015).

Faithful Representation

All the Australian companies are obliged for making transparent and fair financial

statements representation of the financial information. In order to make sure the same, the

shareholders confidence has a considerable role from the perception of the company. Audit

report developed by KMPG for Flight Centre Travel company also takes into consideration that

Revenue

Flight center travel company’s management considers to conduct revenue recognition at

the selling point after reducing the tax expenses. In addition, recognition of the sales provision is

recognized through focusing on the overall analysis. For this reason, the selling value encompass

the revenue gathered by means of the product sale (Vafaei, Ahmed and Mather 2015).

Addressing qualitative aspects of conceptual framework

Conceptual framework of financial reporting as per AASB includes some qualitative

characteristics that is helpful in attaining the quality of financial reporting of a corporate firm.

Flight Centre Travel company requires to maintain such characteristics and considering the same

critical analysis is carried out. This is in order to recognize the extent of adherence with the

qualitative characteristics explained within AASB framework (Vafaei, Ahmed and Mather

2015).

Faithful Representation

All the Australian companies are obliged for making transparent and fair financial

statements representation of the financial information. In order to make sure the same, the

shareholders confidence has a considerable role from the perception of the company. Audit

report developed by KMPG for Flight Centre Travel company also takes into consideration that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CONTEMPORARY ACCOUNTING ISSUES

faithful representation of the financial report is maintained for the reason that it has dealt with

vital accounting standards considerably and faithfully.

Relevance

As per this factor, relevancy is deemed to be important for information offered for

enhancing the decision-making process of the company. Considering the case of Flight Centre

Travel company, alignment was observed in consideration to AASB, IFRS and Corporations Act

2001 (Brown, Preiato and Tarca 2014). Additionally, it also takes into account the recent rates of

depreciation, tax and few more. For this reason, efficient financial decisions might be considered

as Flight Centre Travel company offers valuable information within the company’s financial

statements.

Verifiability

It is needed or all the corporate firms to reveal their financial data in a way that its

investors are capable to verify them in a better manner. For making sure of this particular

characteristic, Flight Centre Travel company segments all its business conducts through offering

notes within the annual report of a company and its financial statements (Soh and Martina-

Bennie 2015).

Comparability

This factor offers increased opportunities to its stakeholders that can facilitate in realizing

the similarities along with deviations within the financial information among several financial

reports. The important information is offered to the users by representing by means of charts and

tables for better understanding (Soh and Martinov-Bennie 2015). For this reason, the financial

faithful representation of the financial report is maintained for the reason that it has dealt with

vital accounting standards considerably and faithfully.

Relevance

As per this factor, relevancy is deemed to be important for information offered for

enhancing the decision-making process of the company. Considering the case of Flight Centre

Travel company, alignment was observed in consideration to AASB, IFRS and Corporations Act

2001 (Brown, Preiato and Tarca 2014). Additionally, it also takes into account the recent rates of

depreciation, tax and few more. For this reason, efficient financial decisions might be considered

as Flight Centre Travel company offers valuable information within the company’s financial

statements.

Verifiability

It is needed or all the corporate firms to reveal their financial data in a way that its

investors are capable to verify them in a better manner. For making sure of this particular

characteristic, Flight Centre Travel company segments all its business conducts through offering

notes within the annual report of a company and its financial statements (Soh and Martina-

Bennie 2015).

Comparability

This factor offers increased opportunities to its stakeholders that can facilitate in realizing

the similarities along with deviations within the financial information among several financial

reports. The important information is offered to the users by representing by means of charts and

tables for better understanding (Soh and Martinov-Bennie 2015). For this reason, the financial

11CONTEMPORARY ACCOUNTING ISSUES

report of Flight Centre Travel company can be compared with all its market rivals for attaining a

viewpoint regarding real financial position of the company.

Understandability

Through attaining the aspects of this factor, the financial information requires being

reported in a manner that it turns out to be simple for the investors to understand the same in a

better manner (Brown, Preiato and Tarca 2014). Flight Centre Travel company reports its

financial information in aa format that is aligned with the financial reporting conceptual

framework that facilitates all its investors to understand them in a better manner.

Timeliness

All the companies require to maintain a fixed timeframe for indicating its financial

information to all its investors. Annual and quarterly financial reports are observed to be offers to

be investors in the situation of Flight Centre Travel company. For this reason, timely information

disclosure might facilitate in attaining the users trust as this might facilitate in attaining a fair

perception regarding the position and performance of the company within the market (Vafaei,

Ahmed and Mather 2015).

Conclusion

The objective of the report is to analyze the adherence of Flight Centre Travel company

in alignment with the conceptual framework of AASB. It is gathered from the paper that the

organization totally confirms with the regulations of financial reporting conceptual framework of

IFRS. Moreover, in case of Flight center travel company, the balance sheet statement is

developed in a way which supports investors to attain important information related with its

economic resources aligned with AASB regulations. The annual report of the company indicates

report of Flight Centre Travel company can be compared with all its market rivals for attaining a

viewpoint regarding real financial position of the company.

Understandability

Through attaining the aspects of this factor, the financial information requires being

reported in a manner that it turns out to be simple for the investors to understand the same in a

better manner (Brown, Preiato and Tarca 2014). Flight Centre Travel company reports its

financial information in aa format that is aligned with the financial reporting conceptual

framework that facilitates all its investors to understand them in a better manner.

Timeliness

All the companies require to maintain a fixed timeframe for indicating its financial

information to all its investors. Annual and quarterly financial reports are observed to be offers to

be investors in the situation of Flight Centre Travel company. For this reason, timely information

disclosure might facilitate in attaining the users trust as this might facilitate in attaining a fair

perception regarding the position and performance of the company within the market (Vafaei,

Ahmed and Mather 2015).

Conclusion

The objective of the report is to analyze the adherence of Flight Centre Travel company

in alignment with the conceptual framework of AASB. It is gathered from the paper that the

organization totally confirms with the regulations of financial reporting conceptual framework of

IFRS. Moreover, in case of Flight center travel company, the balance sheet statement is

developed in a way which supports investors to attain important information related with its

economic resources aligned with AASB regulations. The annual report of the company indicates

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.