Holmes Institute HI6025: IFRS and CSR Reporting in Accounting Theory

VerifiedAdded on 2023/01/06

|17

|4207

|99

Report

AI Summary

This report critically examines the adoption of International Financial Reporting Standards (IFRS) and Corporate Social Responsibility (CSR) reporting. Part A delves into the adoption of IFRS in Australia, exploring the timeline of implementation, benefits, and challenges. It analyzes changes in financial disclosures, particularly regarding non-current and intangible assets, comparing BHP Billiton's financial statements before and after IFRS adoption. Part B focuses on CSR trends, evaluating a company's CSR reporting practices, and recommending improvements to the Australian Financial Reporting regulator. The report covers key trends in CSR, evaluation of CSR reporting of a company and recommendation to the Australia Financial Reporting regulatory about the future of CSR that can guide the companies in future. The analysis incorporates relevant accounting theory to explain the development of CSR disclosures and suggests improvements for future reporting. The report concludes with recommendations for the future of CSR reporting, aiming to guide Australian public entities. Desklib provides this solved assignment to help students understand accounting theory and real-world applications.

Accounting Theory and

Current Issues

Current Issues

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. (I) In which year the country adopted IFRS............................................................................1

1. (II) All the IFRS were introduced together or gradually into the local accounting standards

of the chosen country along with the explanation of the possible reason....................................1

1. (III) Discussion of the benefits and challenges reported in the literature about the adoption

of IFRS in the country..................................................................................................................2

2. (I) Identification and discussion of the remarkable changes to the disclosures related to

different financial aspects............................................................................................................3

2. (II) Expressing the opinion about the usefulness of the new format of disclosures compared

to the disclosures at the pre adoption of IFRS.............................................................................4

PART B............................................................................................................................................4

1. Discussion of the key trends in corporate social responsibility as reviewed in the past 5

years.............................................................................................................................................4

2. (I) Evaluation of the company's extent of CSR reporting........................................................6

2. (II) Use of relevant accounting theory and explanation of reason for development of CSR

disclosure made by the company.................................................................................................6

2. (III) Scope for improvement in CSR reporting by the company.............................................7

3. Recommendation to the Australian Financial Reporting regulator about the future of CSR

reporting that will guide Australian public entities in the future.................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. (I) In which year the country adopted IFRS............................................................................1

1. (II) All the IFRS were introduced together or gradually into the local accounting standards

of the chosen country along with the explanation of the possible reason....................................1

1. (III) Discussion of the benefits and challenges reported in the literature about the adoption

of IFRS in the country..................................................................................................................2

2. (I) Identification and discussion of the remarkable changes to the disclosures related to

different financial aspects............................................................................................................3

2. (II) Expressing the opinion about the usefulness of the new format of disclosures compared

to the disclosures at the pre adoption of IFRS.............................................................................4

PART B............................................................................................................................................4

1. Discussion of the key trends in corporate social responsibility as reviewed in the past 5

years.............................................................................................................................................4

2. (I) Evaluation of the company's extent of CSR reporting........................................................6

2. (II) Use of relevant accounting theory and explanation of reason for development of CSR

disclosure made by the company.................................................................................................6

2. (III) Scope for improvement in CSR reporting by the company.............................................7

3. Recommendation to the Australian Financial Reporting regulator about the future of CSR

reporting that will guide Australian public entities in the future.................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Accounting theory could be defined as the theories which are required to be focused by

all the businesses for the purpose of making sure that they are able to formulate all the financial

records properly. If the business entities will not be following all the accounting principles then it

will be very difficult for the companies to meet all the long as well as short-term business goals.

Present report is focused with evaluation of IFRS and CSR. There are two different parts in this

report first one of focused with adoption of IFRS by a country and the second apart of the report

is related to the trends in CSR (Arora and Soral, 2017). This assignment covers various topics

such as introduction of IFRS in a country, discussion of benefits and challenges for the adoption,

comparison of annual report to two years of a company and opinion about of usefulness of new

format of disclosure. Additionally, key trends on CSR, evaluation of CSR reporting of a

company and recommendation to the Australia Financial Reporting regulatory about the future of

CSR that can guide the companies in future is also covered in this report.

PART A

1. (I) In which year the country adopted IFRS

IFRS are the international financial reporting standards which are required to be followed

by all the companies which are operating business in more than one country. With the help of

them, it will be very easy for the investors of different nations to understand the final accounts of

the companies and make decisions regarding making investment. Currently different countries

are using IFRS as it facilitates them to attract large number of investors for the businesses. These

countries are UAE, Australia, Austria, Belgium, China, Chile, Egypt, Germany, Hungary,

Iceland, India, Japan, Thailand, Turkey, UK, US etc. One of the countries which is selected for

this part is Australia. The organisation adopted IFRS on 1st January 2005. With the adoption of

IFRS in Australia all the companies which are domestic entities are required to follow all the

IFRS (Baker, 2017).

1. (II) All the IFRS were introduced together or gradually into the local accounting standards of

the chosen country along with the explanation of the possible reason

IFRS were adopted by Australia in 2005 and at the initial level it was adopted by the

application of IFRS 1 which is related to the first time adoption of International Financial

Reporting Standards. At 1st January 2005 IFRS 1 to IFRS 6 were applied by the Australian

1

Accounting theory could be defined as the theories which are required to be focused by

all the businesses for the purpose of making sure that they are able to formulate all the financial

records properly. If the business entities will not be following all the accounting principles then it

will be very difficult for the companies to meet all the long as well as short-term business goals.

Present report is focused with evaluation of IFRS and CSR. There are two different parts in this

report first one of focused with adoption of IFRS by a country and the second apart of the report

is related to the trends in CSR (Arora and Soral, 2017). This assignment covers various topics

such as introduction of IFRS in a country, discussion of benefits and challenges for the adoption,

comparison of annual report to two years of a company and opinion about of usefulness of new

format of disclosure. Additionally, key trends on CSR, evaluation of CSR reporting of a

company and recommendation to the Australia Financial Reporting regulatory about the future of

CSR that can guide the companies in future is also covered in this report.

PART A

1. (I) In which year the country adopted IFRS

IFRS are the international financial reporting standards which are required to be followed

by all the companies which are operating business in more than one country. With the help of

them, it will be very easy for the investors of different nations to understand the final accounts of

the companies and make decisions regarding making investment. Currently different countries

are using IFRS as it facilitates them to attract large number of investors for the businesses. These

countries are UAE, Australia, Austria, Belgium, China, Chile, Egypt, Germany, Hungary,

Iceland, India, Japan, Thailand, Turkey, UK, US etc. One of the countries which is selected for

this part is Australia. The organisation adopted IFRS on 1st January 2005. With the adoption of

IFRS in Australia all the companies which are domestic entities are required to follow all the

IFRS (Baker, 2017).

1. (II) All the IFRS were introduced together or gradually into the local accounting standards of

the chosen country along with the explanation of the possible reason

IFRS were adopted by Australia in 2005 and at the initial level it was adopted by the

application of IFRS 1 which is related to the first time adoption of International Financial

Reporting Standards. At 1st January 2005 IFRS 1 to IFRS 6 were applied by the Australian

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Board. IFRS 7 was introduced on 1st January 2007 and all the companies were

required to comply with it on or after the same date. IFRS 8 was applied in Australia on 1 st

January 2009. The Australian government expected to issue IFRS 9 by the end of year 2014 but

it was not issues at that time and it was applied on 1st January 2018. IFRS 10 was applied on 1st

January 2013 and it also amends IFRS 11, 12, 13 IAS 27 and 28. IFRS 14 was applied on 1st of

January month of year 2016 and IFRS 15 was issues in Australia on 1st Jan. 2018. The IFRS 16 is

effective in Australia Since 1st January 2019. It has been expected that IFRS 17 will be effective

in Australia from January 2021 (Baker and Wick, 2020).

The above discussion reflects that all the IFRS were not introduced in Australia together.

The main reason for the same is that the Australian Accounting Board was willing to analyse that

IFRS adoption will be beneficial for the domestic companies or not. All of them were introduced

with the need of them along with time.

1. (III) Discussion of the benefits and challenges reported in the literature about the adoption of

IFRS in the country

IFRS are the international financial reporting standards that are adopted by countries for

facilitating the domestic companies to attract foreign investment. There are various types of

benefits as well as challenges of adoption of IFRS. All of them are discussed below:

Benefits of adoption of IFRS:

If IFRS will be adopted by the countries then it will facilitate the companies to have one

accounting system which will result in less complications in the accounting.

The adoption of IFRS can facilitate the businesses of the countries which have adopted

them because knowledge of it is very important for all the companies that are operating

business internationally (Bell, 2018).

IFRS are the reporting standards that can facilitate the investors to analyse the financial

statements of international companies so that they can make the decisions of investments

effectively.

Adoption of IFRS will benefit the economy of the countries by making sure that the

growth of international business is increased.

If a country will adopt IFRS then it will encourage foreign investment which will also

result in the foreign capital inflows in the nation.

2

required to comply with it on or after the same date. IFRS 8 was applied in Australia on 1 st

January 2009. The Australian government expected to issue IFRS 9 by the end of year 2014 but

it was not issues at that time and it was applied on 1st January 2018. IFRS 10 was applied on 1st

January 2013 and it also amends IFRS 11, 12, 13 IAS 27 and 28. IFRS 14 was applied on 1st of

January month of year 2016 and IFRS 15 was issues in Australia on 1st Jan. 2018. The IFRS 16 is

effective in Australia Since 1st January 2019. It has been expected that IFRS 17 will be effective

in Australia from January 2021 (Baker and Wick, 2020).

The above discussion reflects that all the IFRS were not introduced in Australia together.

The main reason for the same is that the Australian Accounting Board was willing to analyse that

IFRS adoption will be beneficial for the domestic companies or not. All of them were introduced

with the need of them along with time.

1. (III) Discussion of the benefits and challenges reported in the literature about the adoption of

IFRS in the country

IFRS are the international financial reporting standards that are adopted by countries for

facilitating the domestic companies to attract foreign investment. There are various types of

benefits as well as challenges of adoption of IFRS. All of them are discussed below:

Benefits of adoption of IFRS:

If IFRS will be adopted by the countries then it will facilitate the companies to have one

accounting system which will result in less complications in the accounting.

The adoption of IFRS can facilitate the businesses of the countries which have adopted

them because knowledge of it is very important for all the companies that are operating

business internationally (Bell, 2018).

IFRS are the reporting standards that can facilitate the investors to analyse the financial

statements of international companies so that they can make the decisions of investments

effectively.

Adoption of IFRS will benefit the economy of the countries by making sure that the

growth of international business is increased.

If a country will adopt IFRS then it will encourage foreign investment which will also

result in the foreign capital inflows in the nation.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The cost of compliance will be reduced if the businesses will comply with IFRS (Bloom,

2018).

Challenges of adoption of IFRS:

If a country will decide to adopt IFRS then there are various types of factors which may

leave negative impact upon the application of the standards. These are culture, legal

system, language etc.

A company which will be operating in different countries will be required to compare all

the final accounts generated by subsidiaries operating in other nations. If some of them

will interpret IFRS differently then the final accounts of them could not be compared.

2. (I) Identification and discussion of the remarkable changes to the disclosures related to

different financial aspects

One of the largest companies of Australia is BHP Billiton. It is an Australian mining

company which is established in Melbourne, Australia. It was founded in year 1885 by Phillip

Charly. As it is an Australia company so it is following IFRS since year 2005 and before that it

was formulating all its final accounts according to the Australian Accounting Standards. With the

introduction of IFRS within the country various remarkable changes took place in the disclosures

of different elements of financial statements (Christensen, 2018). From the annual report of BHP

Billiton for year 2004 and 2019 different changes are in the disclosure of various elements of

financial statements are analysed. All of them are as follows:

Non-current assets: From the balance sheet of year 2004 it has been analysed that the

information of all the non current assets is very general and no detailed note to determine the full

disclosure of all of them is not provided (Annual report of BHP Billiton, 2004). On the other

hand, the financial statement of 2019 is reflecting that the information about non-current is

provided in detail. All the factors that are resulting in in changes in the assets are mentioned in

the annual report. As the company is having assets in different locations so the compliance of

IFRS 5 states that all the companies are required to share detailed information of assets in

different countries. The annual report for year 2019 of BHP is showing that there are various

countries in which the enterprise is having non-current assets. These countries are Australia,

North America, South America and rest of the world. The annual report for year 2019 is showing

that company is disclosing detailed information about all the non-current assets which is required

by the IFRS 5 or AASB 5 (Lodhia and Sharma, 2019).

3

2018).

Challenges of adoption of IFRS:

If a country will decide to adopt IFRS then there are various types of factors which may

leave negative impact upon the application of the standards. These are culture, legal

system, language etc.

A company which will be operating in different countries will be required to compare all

the final accounts generated by subsidiaries operating in other nations. If some of them

will interpret IFRS differently then the final accounts of them could not be compared.

2. (I) Identification and discussion of the remarkable changes to the disclosures related to

different financial aspects

One of the largest companies of Australia is BHP Billiton. It is an Australian mining

company which is established in Melbourne, Australia. It was founded in year 1885 by Phillip

Charly. As it is an Australia company so it is following IFRS since year 2005 and before that it

was formulating all its final accounts according to the Australian Accounting Standards. With the

introduction of IFRS within the country various remarkable changes took place in the disclosures

of different elements of financial statements (Christensen, 2018). From the annual report of BHP

Billiton for year 2004 and 2019 different changes are in the disclosure of various elements of

financial statements are analysed. All of them are as follows:

Non-current assets: From the balance sheet of year 2004 it has been analysed that the

information of all the non current assets is very general and no detailed note to determine the full

disclosure of all of them is not provided (Annual report of BHP Billiton, 2004). On the other

hand, the financial statement of 2019 is reflecting that the information about non-current is

provided in detail. All the factors that are resulting in in changes in the assets are mentioned in

the annual report. As the company is having assets in different locations so the compliance of

IFRS 5 states that all the companies are required to share detailed information of assets in

different countries. The annual report for year 2019 of BHP is showing that there are various

countries in which the enterprise is having non-current assets. These countries are Australia,

North America, South America and rest of the world. The annual report for year 2019 is showing

that company is disclosing detailed information about all the non-current assets which is required

by the IFRS 5 or AASB 5 (Lodhia and Sharma, 2019).

3

Intangible assets: According to IFRS 5 all the assets that are part of non-current assets

are require to be disclosed in detail so that the analysers of financial statements can determine

actual position of the company. As IFRS were launched in Australia in year 2005 so to determine

the changes in the disclosure of all the intangible assets in the balance sheet annual reports of

2004 and 2019 are analysed (Annual report of BHP Billiton, 2019). The financial statements in

the report of 2004 no detailed analysis is represented for the intangible assets. On the other hand,

the annual report of year 2019 is reflecting highly detailed information about all the intangible

assets. For the purpose of valuation of all of them proper calculations are disclosed under the

note 10. It reflects that the adoption of IFRS changed the way in which company used to disclose

the details of elements of balance sheet.

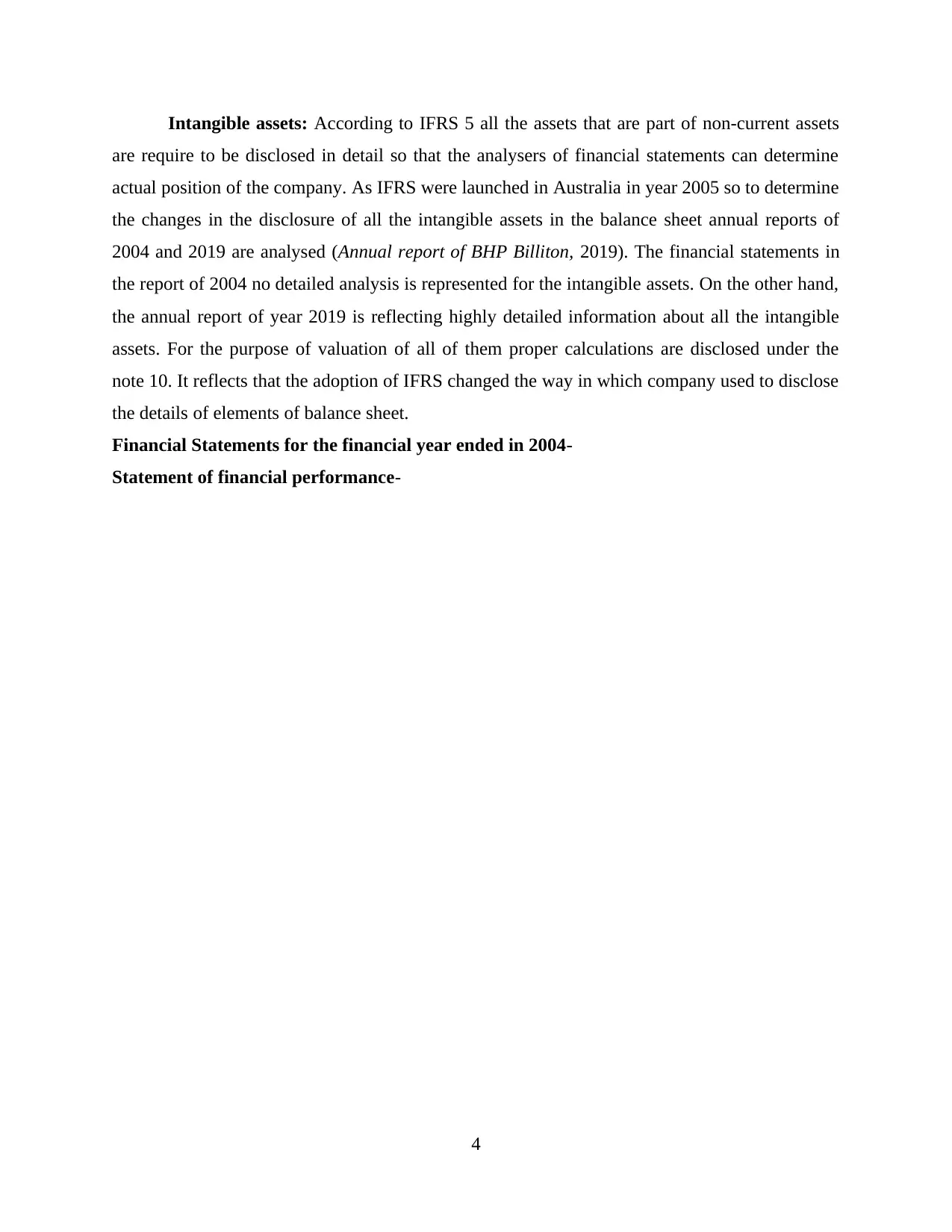

Financial Statements for the financial year ended in 2004-

Statement of financial performance-

4

are require to be disclosed in detail so that the analysers of financial statements can determine

actual position of the company. As IFRS were launched in Australia in year 2005 so to determine

the changes in the disclosure of all the intangible assets in the balance sheet annual reports of

2004 and 2019 are analysed (Annual report of BHP Billiton, 2019). The financial statements in

the report of 2004 no detailed analysis is represented for the intangible assets. On the other hand,

the annual report of year 2019 is reflecting highly detailed information about all the intangible

assets. For the purpose of valuation of all of them proper calculations are disclosed under the

note 10. It reflects that the adoption of IFRS changed the way in which company used to disclose

the details of elements of balance sheet.

Financial Statements for the financial year ended in 2004-

Statement of financial performance-

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Screenshot from 2020-09-22 17-11-56

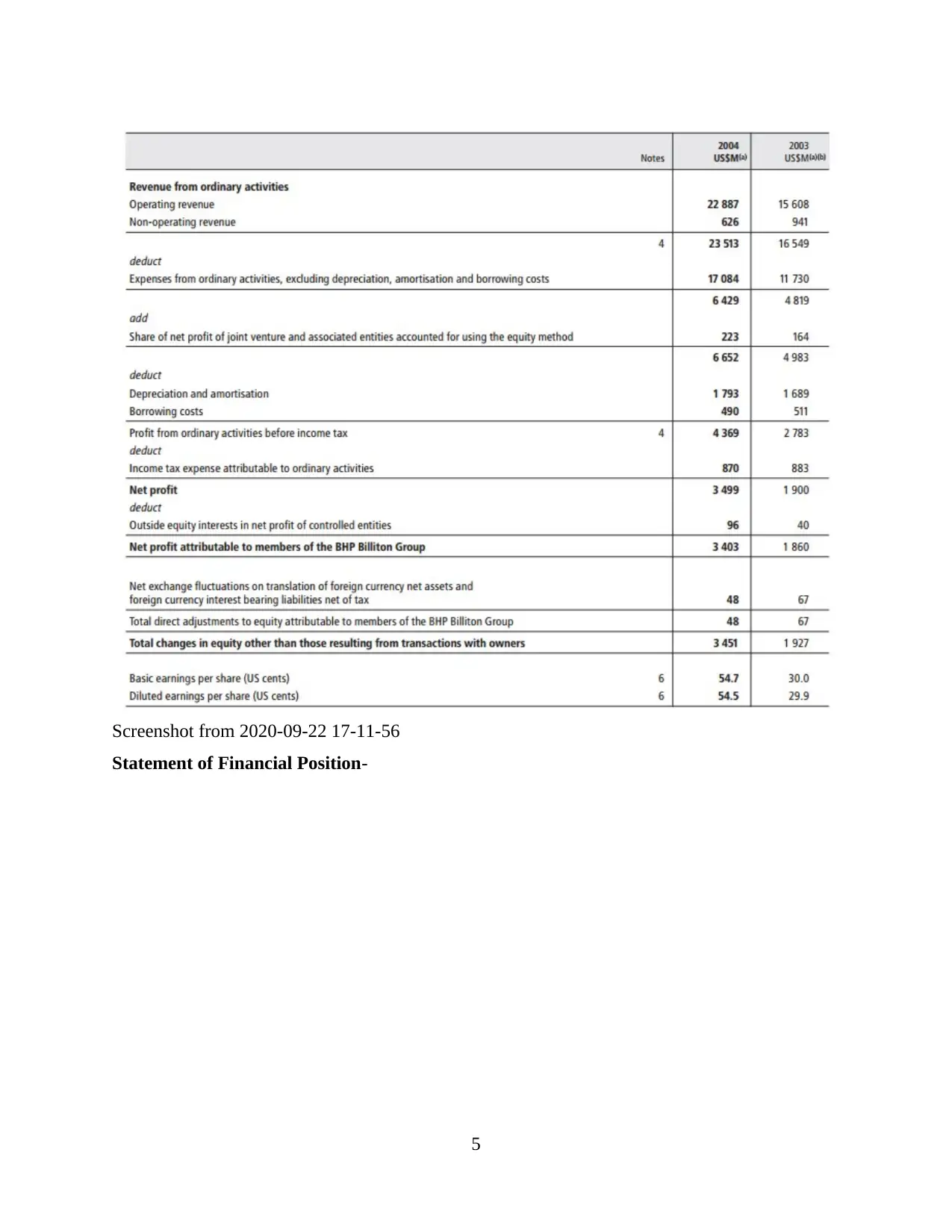

Statement of Financial Position-

5

Statement of Financial Position-

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

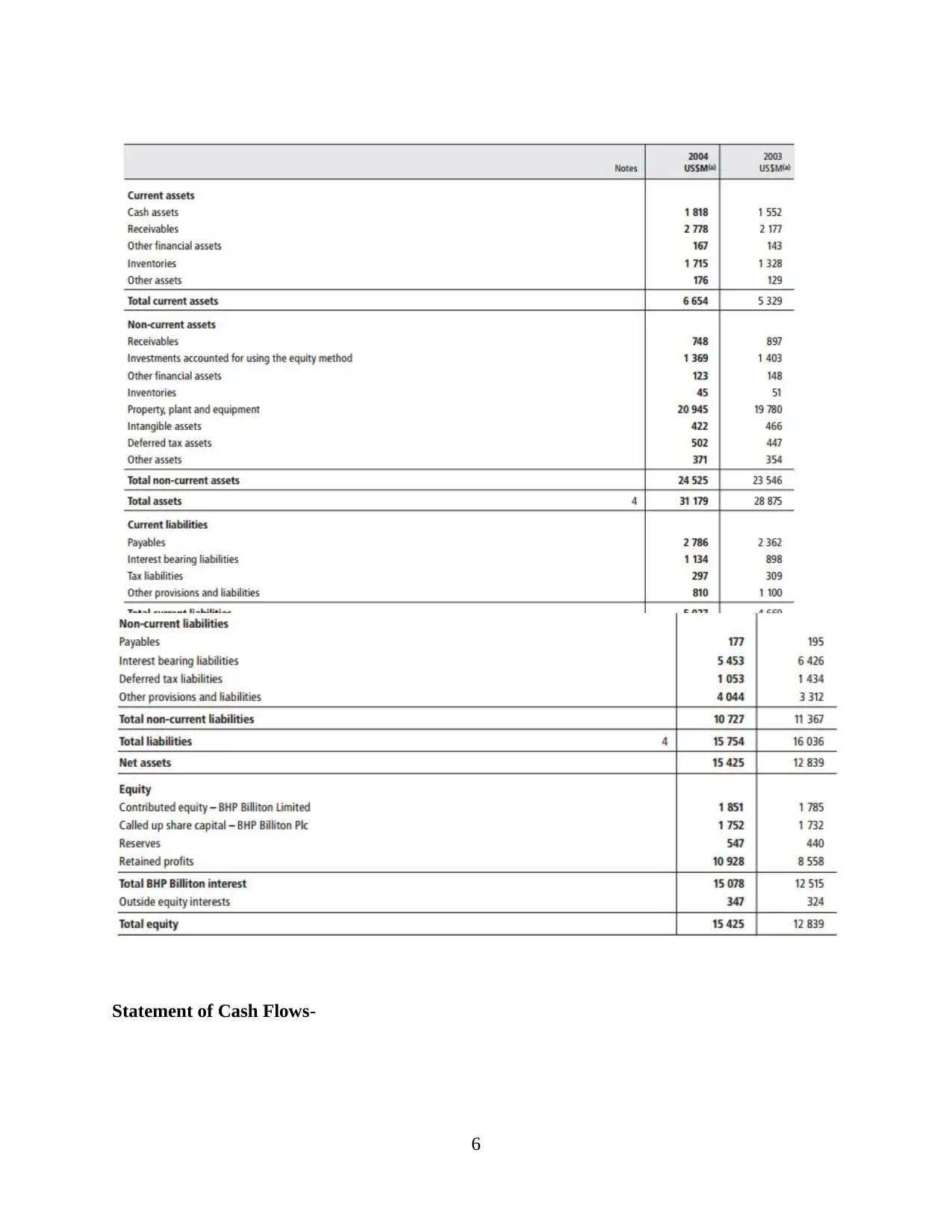

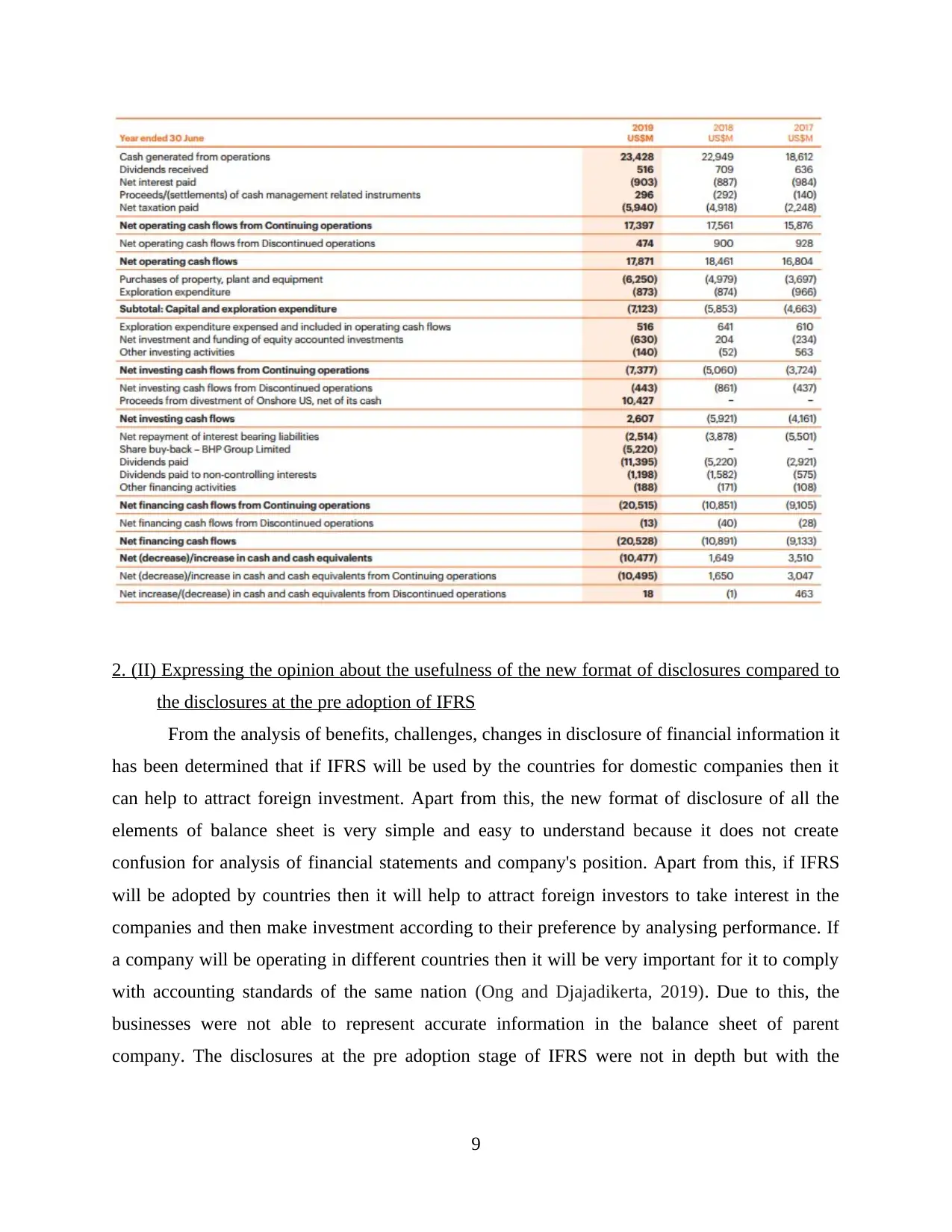

Statement of Cash Flows-

6

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

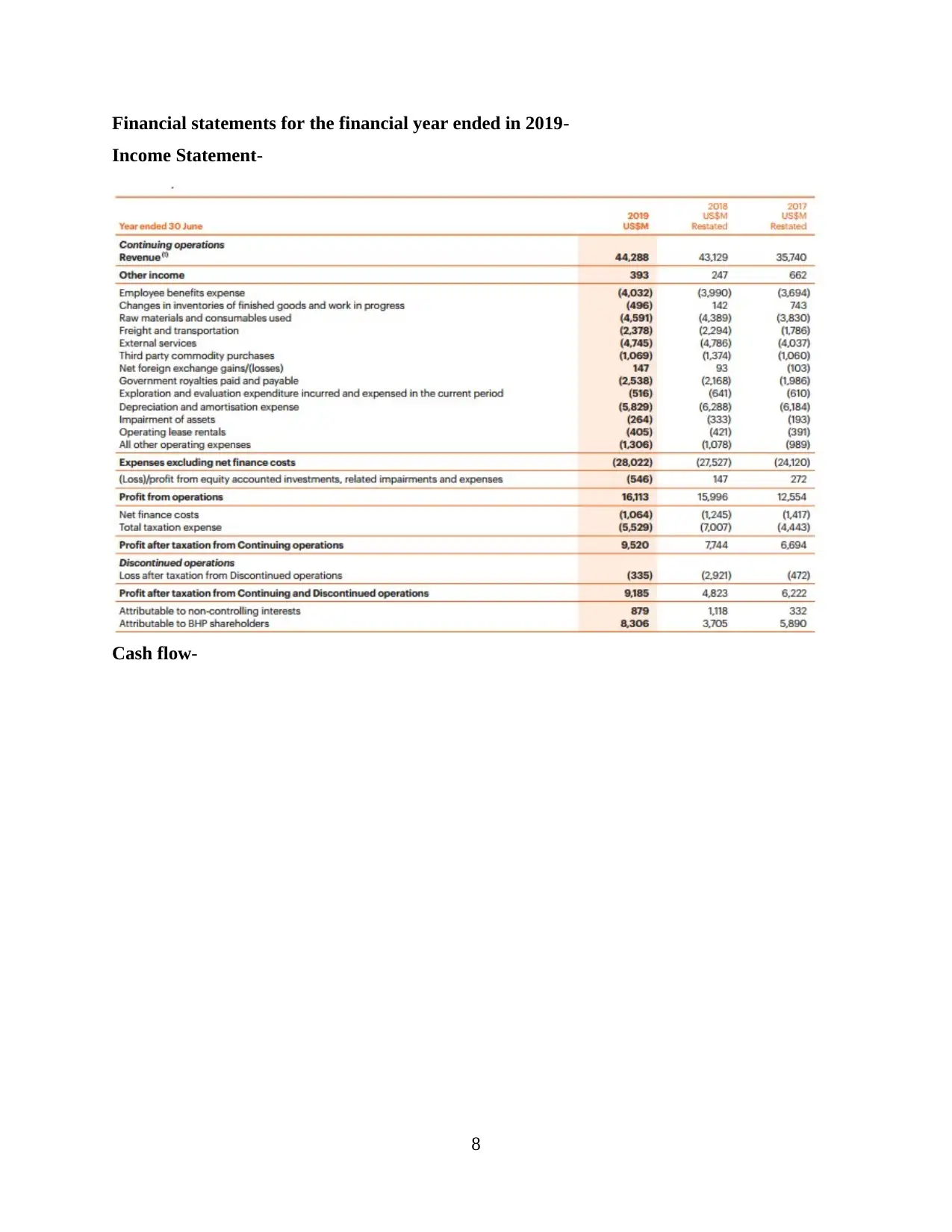

Financial statements for the financial year ended in 2019-

Income Statement-

Cash flow-

8

Income Statement-

Cash flow-

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. (II) Expressing the opinion about the usefulness of the new format of disclosures compared to

the disclosures at the pre adoption of IFRS

From the analysis of benefits, challenges, changes in disclosure of financial information it

has been determined that if IFRS will be used by the countries for domestic companies then it

can help to attract foreign investment. Apart from this, the new format of disclosure of all the

elements of balance sheet is very simple and easy to understand because it does not create

confusion for analysis of financial statements and company's position. Apart from this, if IFRS

will be adopted by countries then it will help to attract foreign investors to take interest in the

companies and then make investment according to their preference by analysing performance. If

a company will be operating in different countries then it will be very important for it to comply

with accounting standards of the same nation (Ong and Djajadikerta, 2019). Due to this, the

businesses were not able to represent accurate information in the balance sheet of parent

company. The disclosures at the pre adoption stage of IFRS were not in depth but with the

9

the disclosures at the pre adoption of IFRS

From the analysis of benefits, challenges, changes in disclosure of financial information it

has been determined that if IFRS will be used by the countries for domestic companies then it

can help to attract foreign investment. Apart from this, the new format of disclosure of all the

elements of balance sheet is very simple and easy to understand because it does not create

confusion for analysis of financial statements and company's position. Apart from this, if IFRS

will be adopted by countries then it will help to attract foreign investors to take interest in the

companies and then make investment according to their preference by analysing performance. If

a company will be operating in different countries then it will be very important for it to comply

with accounting standards of the same nation (Ong and Djajadikerta, 2019). Due to this, the

businesses were not able to represent accurate information in the balance sheet of parent

company. The disclosures at the pre adoption stage of IFRS were not in depth but with the

9

adoption of IFRS the businesses such as BHP Billiton are disclosing detailed information to the

stakeholders. It enhances the possibility of attracting large number of foreign investors.

PART B

1. Discussion of the key trends in corporate social responsibility as reviewed in the past 5 years

Corporate social responsibility- This can be understood as a form of model which

contributes for a firm to become liable towards society or environment in which they exist

(Crane, Matten and Spence, 2019). Basically, a company has to complete its responsibilities

towards each and every aspect including shareholders, employees, public etc. In other words,

companies are liable for those aspects which are connected by their activities in both direct or

indirect manner. It is almost mandatory for each type of business to consider and apply this

model in order to perform their activities in more effective manner. In recent time, there are

many changes which happened in this model such as:

Green technology- In current time period, it is the duty of all types of companies to

perform their business activities without harming to environment. Different nations’

government had set a level at which companies can produce carbon or other harmful

gases. The reason for which government set the limit because of rapidly reduction of

natural resources. So it is the new trend which has been applied by government of

different nations and companies are accountable to follow.

Transparency- This is also a key trend of corporate social responsibility that is related to

make an environment of transparent communication inside an organization (Lin,

Padliansyah and Lin, 2019). There should not be any hidden information between internal

parties of business. Apart from it, this is the duty for a company to publish their financial

reports publically so that stakeholders can become aware about performance. Basically,

this types of trend are directly towards employees and stakeholders.

Diversity and inclusion- This trend of CSR is regarding to considering those candidates

or applicants for hiring who are poor financial background. The objective of this new

trend is to empowering new talent in companies which may lead to beneficial outcome

for companies as well as for employees. Due to this new trend, it becomes responsibility

10

stakeholders. It enhances the possibility of attracting large number of foreign investors.

PART B

1. Discussion of the key trends in corporate social responsibility as reviewed in the past 5 years

Corporate social responsibility- This can be understood as a form of model which

contributes for a firm to become liable towards society or environment in which they exist

(Crane, Matten and Spence, 2019). Basically, a company has to complete its responsibilities

towards each and every aspect including shareholders, employees, public etc. In other words,

companies are liable for those aspects which are connected by their activities in both direct or

indirect manner. It is almost mandatory for each type of business to consider and apply this

model in order to perform their activities in more effective manner. In recent time, there are

many changes which happened in this model such as:

Green technology- In current time period, it is the duty of all types of companies to

perform their business activities without harming to environment. Different nations’

government had set a level at which companies can produce carbon or other harmful

gases. The reason for which government set the limit because of rapidly reduction of

natural resources. So it is the new trend which has been applied by government of

different nations and companies are accountable to follow.

Transparency- This is also a key trend of corporate social responsibility that is related to

make an environment of transparent communication inside an organization (Lin,

Padliansyah and Lin, 2019). There should not be any hidden information between internal

parties of business. Apart from it, this is the duty for a company to publish their financial

reports publically so that stakeholders can become aware about performance. Basically,

this types of trend are directly towards employees and stakeholders.

Diversity and inclusion- This trend of CSR is regarding to considering those candidates

or applicants for hiring who are poor financial background. The objective of this new

trend is to empowering new talent in companies which may lead to beneficial outcome

for companies as well as for employees. Due to this new trend, it becomes responsibility

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.