Current Issues in Financial Reporting: Dynamics Co. Ltd IFRS Case

VerifiedAdded on 2023/05/30

|11

|3398

|197

Case Study

AI Summary

This assignment addresses financial reporting issues faced by Dynamics Co. Ltd, a listed company, focusing on revenue recognition (IFRS 15) and intangible assets (IAS 38). It calculates revenue recognition for a promotional offer involving free maintenance services and examines the accounting treatment of a purchased customer list, including amortization and potential revaluation. The analysis includes adjusting journal entries and a discussion of the international framework for financial reporting, highlighting its role in standardizing accounting practices and improving the comparability of financial statements across different regions. The document emphasizes the importance of a conceptual framework for reliable financial reporting and addresses shortcomings of rule-based accounting systems. Desklib provides access to this and similar solved assignments for students.

CURRENT ISSUES IN

FINANCIAL

REPORTING

ASSIGNMENT

FINANCIAL

REPORTING

ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Table of Contents

Background and Abstract............................................................................................................................3

Question 1: Outstanding issues in Dynamics Co. Ltd financial statements..................................................3

Question 2: International framework for financial reporting......................................................................5

References...................................................................................................................................................8

2 | P a g e

Table of Contents

Background and Abstract............................................................................................................................3

Question 1: Outstanding issues in Dynamics Co. Ltd financial statements..................................................3

Question 2: International framework for financial reporting......................................................................5

References...................................................................................................................................................8

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Background and Abstract

In the given assignment, various accounting issues being faced by Dynamics Co. Ltd., one of the listed

companies manufacturing and distributing premium security equipment has been mentioned. Though

the company has prepared its annual financial statements in accordance with the International Financial

Reporting Standards (IFRSs) but there are some outstanding issues relating to revenue recognition and

the measurement and recognition of the intangible assets in the books of accounts, all of which has

been discussed and analysed along with the calculations1. Furthermore, in the second section of the

assignment, it has been highlighted as to how the international framework for financial accounting and

reporting helps in resolving the current accounting issues being faced by regulators and practitioners.

Question 1: Outstanding issues in Dynamics Co. Ltd financial statements

a. In the given case, the company has introduced a special promotion strategy named as

“Something for free” as per which free maintenance services will be provided to the customer

for the first 2 years. On 1st October 2017, the company sold goods to hypermart chain for an

amount of $4.4 million whereas the list price would have been $5 million normally2. A two-year

maintenance contract normally is sold for $0.5 million. The case is governed by IFRS 15 on

revenue recognition for the companies. As per the standard, there can be multiple elements in a

single contract of sales and each of them needs to be recognised separately. Since the

maintenance contract has been agreed off only for 24 months out of which only 3 months have

passed, therefore revenue to the extent of 3/24th portion of the maintenance should only be

recognised as revenue in the year ending on 31st December, 2017. The remainder of the

amount should be treated as a part of deferred revenue and should be shown in the

consolidated statement of financial position as the services will be provided gradually over the

period of time3. On the other hand, the revenue from the sales of goods should be recognised as

revenue in the income statement immediately as the risk and reward of ownership of the goods

passes to the buyer on delivering the goods.

Here, in the given case the fair value of the sales contract exceeds the overall price of the

contract when the elements of contract are being seen individually and hence it can be

concluded that the discount has been given. Since it is not known that what percentage of

discount has been offered on each of the elements of the contract, it would be reasonable to

apply the same percentage of the discount on both the elements of the contracts4. The

calculation for the same has been shown below:

1 DeZoort, F., & Harrison, P. (2016). Understanding Auditors sense of Responsibility for detecting

fraud within organization. Journal of Business Ethics, 1-18.

2 Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education,

71(4), 411-431.

3 Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management

of attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved

from http://psycnet.apa.org/buy/2016-21263-001

3 | P a g e

Background and Abstract

In the given assignment, various accounting issues being faced by Dynamics Co. Ltd., one of the listed

companies manufacturing and distributing premium security equipment has been mentioned. Though

the company has prepared its annual financial statements in accordance with the International Financial

Reporting Standards (IFRSs) but there are some outstanding issues relating to revenue recognition and

the measurement and recognition of the intangible assets in the books of accounts, all of which has

been discussed and analysed along with the calculations1. Furthermore, in the second section of the

assignment, it has been highlighted as to how the international framework for financial accounting and

reporting helps in resolving the current accounting issues being faced by regulators and practitioners.

Question 1: Outstanding issues in Dynamics Co. Ltd financial statements

a. In the given case, the company has introduced a special promotion strategy named as

“Something for free” as per which free maintenance services will be provided to the customer

for the first 2 years. On 1st October 2017, the company sold goods to hypermart chain for an

amount of $4.4 million whereas the list price would have been $5 million normally2. A two-year

maintenance contract normally is sold for $0.5 million. The case is governed by IFRS 15 on

revenue recognition for the companies. As per the standard, there can be multiple elements in a

single contract of sales and each of them needs to be recognised separately. Since the

maintenance contract has been agreed off only for 24 months out of which only 3 months have

passed, therefore revenue to the extent of 3/24th portion of the maintenance should only be

recognised as revenue in the year ending on 31st December, 2017. The remainder of the

amount should be treated as a part of deferred revenue and should be shown in the

consolidated statement of financial position as the services will be provided gradually over the

period of time3. On the other hand, the revenue from the sales of goods should be recognised as

revenue in the income statement immediately as the risk and reward of ownership of the goods

passes to the buyer on delivering the goods.

Here, in the given case the fair value of the sales contract exceeds the overall price of the

contract when the elements of contract are being seen individually and hence it can be

concluded that the discount has been given. Since it is not known that what percentage of

discount has been offered on each of the elements of the contract, it would be reasonable to

apply the same percentage of the discount on both the elements of the contracts4. The

calculation for the same has been shown below:

1 DeZoort, F., & Harrison, P. (2016). Understanding Auditors sense of Responsibility for detecting

fraud within organization. Journal of Business Ethics, 1-18.

2 Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education,

71(4), 411-431.

3 Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management

of attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved

from http://psycnet.apa.org/buy/2016-21263-001

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

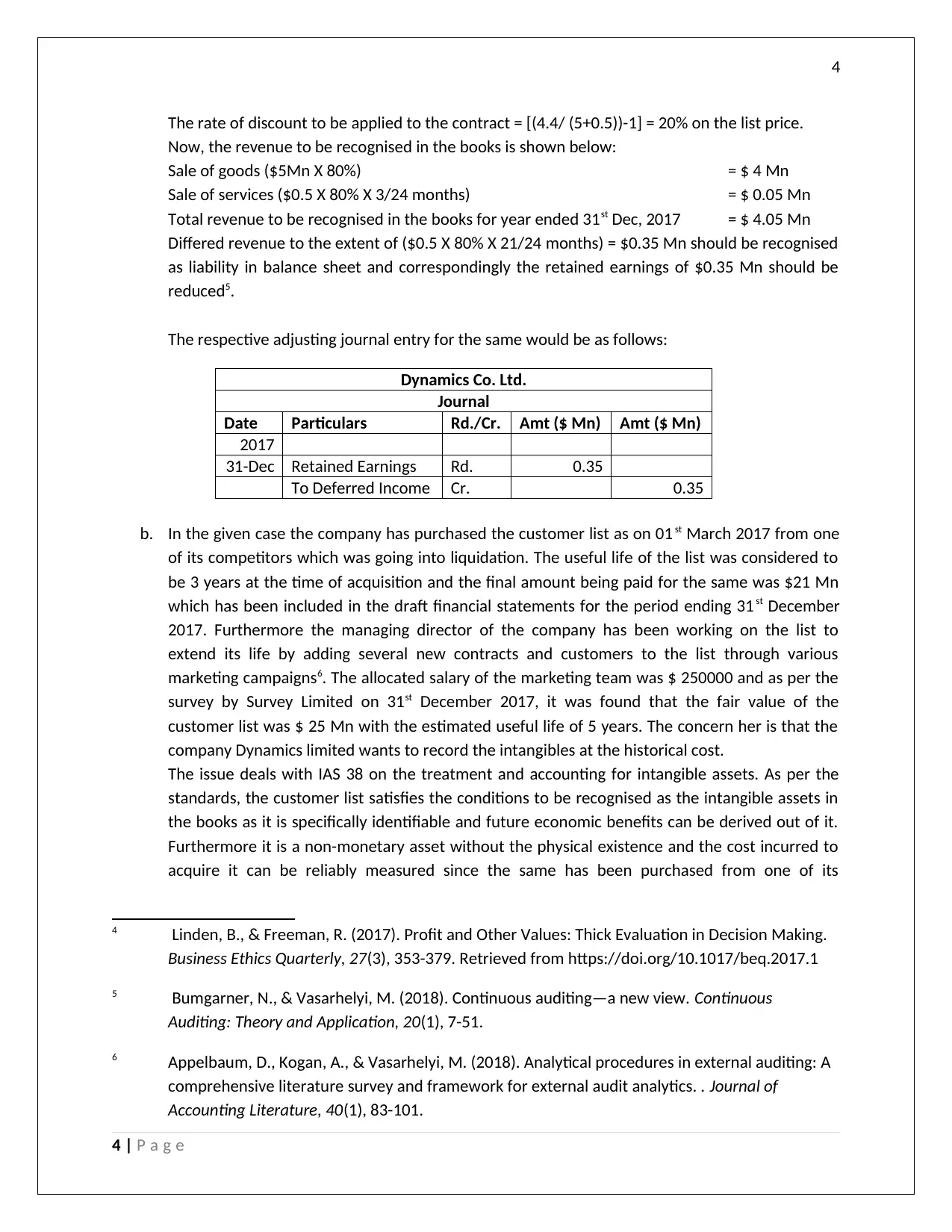

The rate of discount to be applied to the contract = [(4.4/ (5+0.5))-1] = 20% on the list price.

Now, the revenue to be recognised in the books is shown below:

Sale of goods ($5Mn X 80%) = $ 4 Mn

Sale of services ($0.5 X 80% X 3/24 months) = $ 0.05 Mn

Total revenue to be recognised in the books for year ended 31st Dec, 2017 = $ 4.05 Mn

Differed revenue to the extent of ($0.5 X 80% X 21/24 months) = $0.35 Mn should be recognised

as liability in balance sheet and correspondingly the retained earnings of $0.35 Mn should be

reduced5.

The respective adjusting journal entry for the same would be as follows:

Dynamics Co. Ltd.

Journal

Date Particulars Rd./Cr. Amt ($ Mn) Amt ($ Mn)

2017

31-Dec Retained Earnings Rd. 0.35

To Deferred Income Cr. 0.35

b. In the given case the company has purchased the customer list as on 01 st March 2017 from one

of its competitors which was going into liquidation. The useful life of the list was considered to

be 3 years at the time of acquisition and the final amount being paid for the same was $21 Mn

which has been included in the draft financial statements for the period ending 31 st December

2017. Furthermore the managing director of the company has been working on the list to

extend its life by adding several new contracts and customers to the list through various

marketing campaigns6. The allocated salary of the marketing team was $ 250000 and as per the

survey by Survey Limited on 31st December 2017, it was found that the fair value of the

customer list was $ 25 Mn with the estimated useful life of 5 years. The concern her is that the

company Dynamics limited wants to record the intangibles at the historical cost.

The issue deals with IAS 38 on the treatment and accounting for intangible assets. As per the

standards, the customer list satisfies the conditions to be recognised as the intangible assets in

the books as it is specifically identifiable and future economic benefits can be derived out of it.

Furthermore it is a non-monetary asset without the physical existence and the cost incurred to

acquire it can be reliably measured since the same has been purchased from one of its

4 Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making.

Business Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

5 Bumgarner, N., & Vasarhelyi, M. (2018). Continuous auditing—a new view. Continuous

Auditing: Theory and Application, 20(1), 7-51.

6 Appelbaum, D., Kogan, A., & Vasarhelyi, M. (2018). Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics. . Journal of

Accounting Literature, 40(1), 83-101.

4 | P a g e

The rate of discount to be applied to the contract = [(4.4/ (5+0.5))-1] = 20% on the list price.

Now, the revenue to be recognised in the books is shown below:

Sale of goods ($5Mn X 80%) = $ 4 Mn

Sale of services ($0.5 X 80% X 3/24 months) = $ 0.05 Mn

Total revenue to be recognised in the books for year ended 31st Dec, 2017 = $ 4.05 Mn

Differed revenue to the extent of ($0.5 X 80% X 21/24 months) = $0.35 Mn should be recognised

as liability in balance sheet and correspondingly the retained earnings of $0.35 Mn should be

reduced5.

The respective adjusting journal entry for the same would be as follows:

Dynamics Co. Ltd.

Journal

Date Particulars Rd./Cr. Amt ($ Mn) Amt ($ Mn)

2017

31-Dec Retained Earnings Rd. 0.35

To Deferred Income Cr. 0.35

b. In the given case the company has purchased the customer list as on 01 st March 2017 from one

of its competitors which was going into liquidation. The useful life of the list was considered to

be 3 years at the time of acquisition and the final amount being paid for the same was $21 Mn

which has been included in the draft financial statements for the period ending 31 st December

2017. Furthermore the managing director of the company has been working on the list to

extend its life by adding several new contracts and customers to the list through various

marketing campaigns6. The allocated salary of the marketing team was $ 250000 and as per the

survey by Survey Limited on 31st December 2017, it was found that the fair value of the

customer list was $ 25 Mn with the estimated useful life of 5 years. The concern her is that the

company Dynamics limited wants to record the intangibles at the historical cost.

The issue deals with IAS 38 on the treatment and accounting for intangible assets. As per the

standards, the customer list satisfies the conditions to be recognised as the intangible assets in

the books as it is specifically identifiable and future economic benefits can be derived out of it.

Furthermore it is a non-monetary asset without the physical existence and the cost incurred to

acquire it can be reliably measured since the same has been purchased from one of its

4 Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making.

Business Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

5 Bumgarner, N., & Vasarhelyi, M. (2018). Continuous auditing—a new view. Continuous

Auditing: Theory and Application, 20(1), 7-51.

6 Appelbaum, D., Kogan, A., & Vasarhelyi, M. (2018). Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics. . Journal of

Accounting Literature, 40(1), 83-101.

4 | P a g e

5

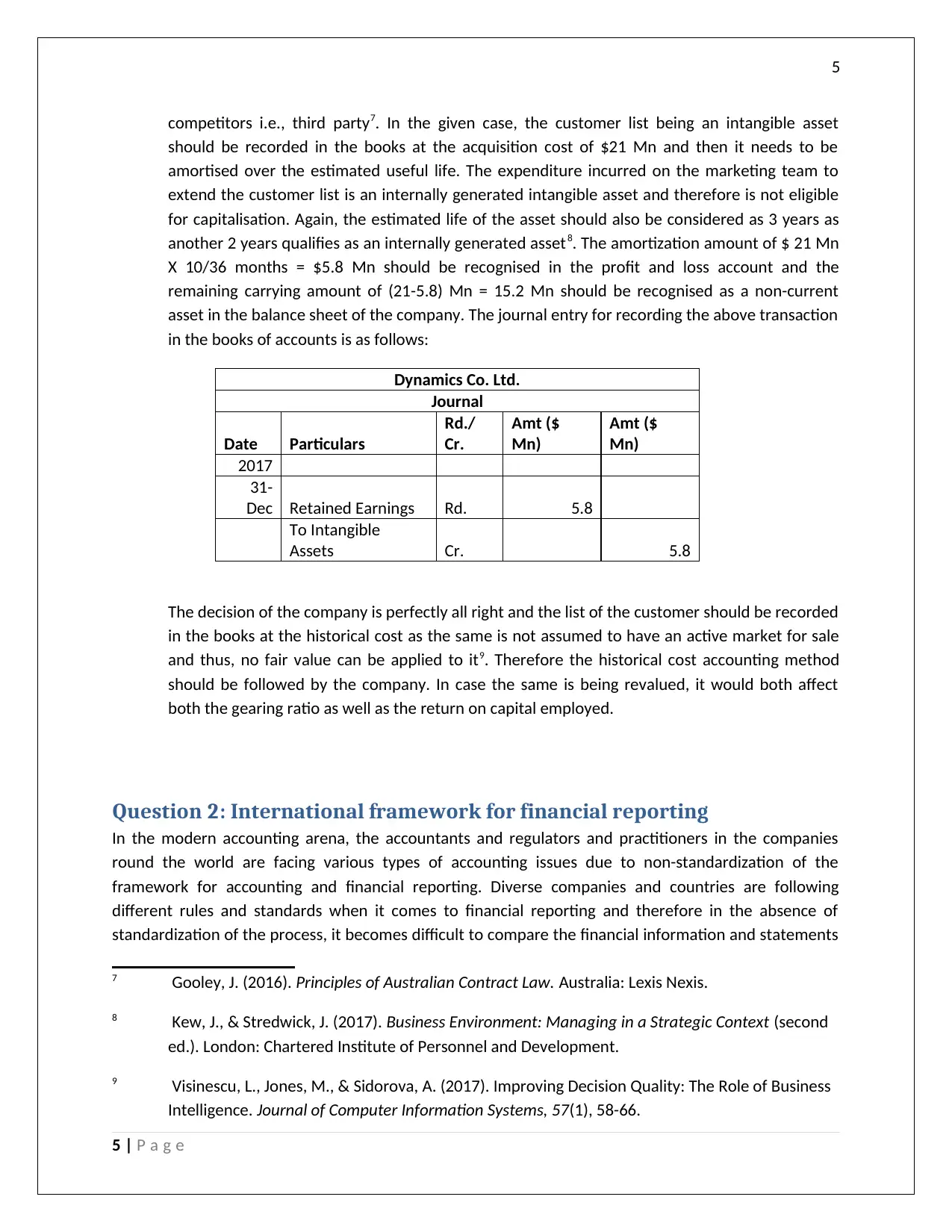

competitors i.e., third party7. In the given case, the customer list being an intangible asset

should be recorded in the books at the acquisition cost of $21 Mn and then it needs to be

amortised over the estimated useful life. The expenditure incurred on the marketing team to

extend the customer list is an internally generated intangible asset and therefore is not eligible

for capitalisation. Again, the estimated life of the asset should also be considered as 3 years as

another 2 years qualifies as an internally generated asset8. The amortization amount of $ 21 Mn

X 10/36 months = $5.8 Mn should be recognised in the profit and loss account and the

remaining carrying amount of (21-5.8) Mn = 15.2 Mn should be recognised as a non-current

asset in the balance sheet of the company. The journal entry for recording the above transaction

in the books of accounts is as follows:

Dynamics Co. Ltd.

Journal

Date Particulars

Rd./

Cr.

Amt ($

Mn)

Amt ($

Mn)

2017

31-

Dec Retained Earnings Rd. 5.8

To Intangible

Assets Cr. 5.8

The decision of the company is perfectly all right and the list of the customer should be recorded

in the books at the historical cost as the same is not assumed to have an active market for sale

and thus, no fair value can be applied to it9. Therefore the historical cost accounting method

should be followed by the company. In case the same is being revalued, it would both affect

both the gearing ratio as well as the return on capital employed.

Question 2: International framework for financial reporting

In the modern accounting arena, the accountants and regulators and practitioners in the companies

round the world are facing various types of accounting issues due to non-standardization of the

framework for accounting and financial reporting. Diverse companies and countries are following

different rules and standards when it comes to financial reporting and therefore in the absence of

standardization of the process, it becomes difficult to compare the financial information and statements

7 Gooley, J. (2016). Principles of Australian Contract Law. Australia: Lexis Nexis.

8 Kew, J., & Stredwick, J. (2017). Business Environment: Managing in a Strategic Context (second

ed.). London: Chartered Institute of Personnel and Development.

9 Visinescu, L., Jones, M., & Sidorova, A. (2017). Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), 58-66.

5 | P a g e

competitors i.e., third party7. In the given case, the customer list being an intangible asset

should be recorded in the books at the acquisition cost of $21 Mn and then it needs to be

amortised over the estimated useful life. The expenditure incurred on the marketing team to

extend the customer list is an internally generated intangible asset and therefore is not eligible

for capitalisation. Again, the estimated life of the asset should also be considered as 3 years as

another 2 years qualifies as an internally generated asset8. The amortization amount of $ 21 Mn

X 10/36 months = $5.8 Mn should be recognised in the profit and loss account and the

remaining carrying amount of (21-5.8) Mn = 15.2 Mn should be recognised as a non-current

asset in the balance sheet of the company. The journal entry for recording the above transaction

in the books of accounts is as follows:

Dynamics Co. Ltd.

Journal

Date Particulars

Rd./

Cr.

Amt ($

Mn)

Amt ($

Mn)

2017

31-

Dec Retained Earnings Rd. 5.8

To Intangible

Assets Cr. 5.8

The decision of the company is perfectly all right and the list of the customer should be recorded

in the books at the historical cost as the same is not assumed to have an active market for sale

and thus, no fair value can be applied to it9. Therefore the historical cost accounting method

should be followed by the company. In case the same is being revalued, it would both affect

both the gearing ratio as well as the return on capital employed.

Question 2: International framework for financial reporting

In the modern accounting arena, the accountants and regulators and practitioners in the companies

round the world are facing various types of accounting issues due to non-standardization of the

framework for accounting and financial reporting. Diverse companies and countries are following

different rules and standards when it comes to financial reporting and therefore in the absence of

standardization of the process, it becomes difficult to compare the financial information and statements

7 Gooley, J. (2016). Principles of Australian Contract Law. Australia: Lexis Nexis.

8 Kew, J., & Stredwick, J. (2017). Business Environment: Managing in a Strategic Context (second

ed.). London: Chartered Institute of Personnel and Development.

9 Visinescu, L., Jones, M., & Sidorova, A. (2017). Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), 58-66.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

across geographies. Due to this shortcoming, there have been various qualitative characteristics of the

financial statements which are not being fulfilled10. The international framework for financial reporting

aims to overcome all these issues and difficulties and present the information to the user in the best

available form in comparable formats. The International Financial reporting standards was introduced to

over this shortcoming such that the same standard is being used all over the world for accounting and

reporting and that would make the financial statements interactive.

To understand the basis of international framework, it is important to understand the meaning of

conceptual framework. It is an attempt to define the very nature and the purpose of accounting which

includes all the theoretical and conceptual issues and all this cumulatively lays the foundation of the

accounting standards to the consistent reporting practices. Conceptual framework is something which

can be applied to many disciplines and when the same is applied with respect to the reporting practices,

it is called the statement of generally accepted accounting principles11. It is basically the best practices in

reporting and consist of the existing ones and lays the foundation for development of new ones. The

purpose of financial reporting has always been to communicate the financial information to the user for

economic decision making and thus the framework forms the theoretical basis how the information

should be reported, whether at historical cost or at market value. It has often been debated by the

accountants round the world that whether the conceptual framework for reporting is necessary for

reliable results and it was seen that in the absence of such a framework, the accounting standards which

were developed had serious defects. Some of them are:

1. The accounting standards were not consistent worldwide in terms of prudence versus accrual or

the matching concept;

2. Since they were inconsistent internally, the effect of any financial transaction on the statement

of financial position was considered to be more important and critical instead of its effect on the

statement of income12.

3. Standards were not produced in a planned fashion taking care of all the loopholes and issues

that might arise later, instead they were being developed on the fire-fighting approach in

reaction to any corporate failure, issue or scandal, rather than being proactive in its approach.

4. Since the accounting standards for any country was being set locally, the standard setting

committee was biased in terms of its composition (not including representative from all the user

groups which directly influenced the quality of accounting standards13.

10 Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional

Law, and Organic Documents. SSRN, 1-35.

11 Chron. (2017). five-common-features-internal-control-system-business. Retrieved december 07,

2017, from http://smallbusiness.chron.com/five-common-features-internal-control-system-

business-430.html

12 Lessambo, F. (2018). Audit Risks: Identification and Procedures. Auditing, Assurance Services,

and Forensics, 3(1), 183-202.

6 | P a g e

across geographies. Due to this shortcoming, there have been various qualitative characteristics of the

financial statements which are not being fulfilled10. The international framework for financial reporting

aims to overcome all these issues and difficulties and present the information to the user in the best

available form in comparable formats. The International Financial reporting standards was introduced to

over this shortcoming such that the same standard is being used all over the world for accounting and

reporting and that would make the financial statements interactive.

To understand the basis of international framework, it is important to understand the meaning of

conceptual framework. It is an attempt to define the very nature and the purpose of accounting which

includes all the theoretical and conceptual issues and all this cumulatively lays the foundation of the

accounting standards to the consistent reporting practices. Conceptual framework is something which

can be applied to many disciplines and when the same is applied with respect to the reporting practices,

it is called the statement of generally accepted accounting principles11. It is basically the best practices in

reporting and consist of the existing ones and lays the foundation for development of new ones. The

purpose of financial reporting has always been to communicate the financial information to the user for

economic decision making and thus the framework forms the theoretical basis how the information

should be reported, whether at historical cost or at market value. It has often been debated by the

accountants round the world that whether the conceptual framework for reporting is necessary for

reliable results and it was seen that in the absence of such a framework, the accounting standards which

were developed had serious defects. Some of them are:

1. The accounting standards were not consistent worldwide in terms of prudence versus accrual or

the matching concept;

2. Since they were inconsistent internally, the effect of any financial transaction on the statement

of financial position was considered to be more important and critical instead of its effect on the

statement of income12.

3. Standards were not produced in a planned fashion taking care of all the loopholes and issues

that might arise later, instead they were being developed on the fire-fighting approach in

reaction to any corporate failure, issue or scandal, rather than being proactive in its approach.

4. Since the accounting standards for any country was being set locally, the standard setting

committee was biased in terms of its composition (not including representative from all the user

groups which directly influenced the quality of accounting standards13.

10 Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional

Law, and Organic Documents. SSRN, 1-35.

11 Chron. (2017). five-common-features-internal-control-system-business. Retrieved december 07,

2017, from http://smallbusiness.chron.com/five-common-features-internal-control-system-

business-430.html

12 Lessambo, F. (2018). Audit Risks: Identification and Procedures. Auditing, Assurance Services,

and Forensics, 3(1), 183-202.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

5. The same theoretical issues were revisited again and again without the solution and standards

were introduced successively. Example – Does a given transaction gives rise to asset (research or

development)

Thus, it can be seen that the lack of conceptual framework led to formation of the rule based accounting

systems, the very objective of which was only treatment of a given accounting transaction. It is thus very

prescriptive and inflexible in nature and makes the financial statements comparable and consistent 14.

However, the existence of the conceptual framework forms the base of principle based accounting

system where standards were developed with the specific objective and this led to the formation of

International Accounting Standards Board (IASB) which was responsible for the creation of the

International Financial Reporting Standards (IFRSs). The main purpose of the framework included:

1. Development of the new accounting standards and reviewing the existing ones for changes, if

required.

2. Promotion of the harmonization of the regulation and standards by reduction in the number of

permitted alterations.

3. Assisting in the preparation of the financial statements through IFRS for which the accounting

standard is not in place15.

The framework would include the below details mainly:

1. The objective of the financial statements

2. The reporting entity

3. The parties who will be using the financial statements

4. The qualitative characteristics which render the financial statements useful

5. The elements of the financial statements like that of assets, liability, incomes and expenses and

the relevant treatment.

The IFRS is a world class accounting standard produced by IASB has the following advantages for the

companies adopting them:

1. It is a set of widely accepted and transparent standards which help in producing high quality and

consistent and comparable financial statements all over the world.

13 Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

14 DeZoort, F., & Harrison, P. (2016). Understanding Auditors sense of Responsibility for detecting

fraud within organization. Journal of Business Ethics, 1-18.

15 Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (fourth ed.). New York:

Routledge.

7 | P a g e

5. The same theoretical issues were revisited again and again without the solution and standards

were introduced successively. Example – Does a given transaction gives rise to asset (research or

development)

Thus, it can be seen that the lack of conceptual framework led to formation of the rule based accounting

systems, the very objective of which was only treatment of a given accounting transaction. It is thus very

prescriptive and inflexible in nature and makes the financial statements comparable and consistent 14.

However, the existence of the conceptual framework forms the base of principle based accounting

system where standards were developed with the specific objective and this led to the formation of

International Accounting Standards Board (IASB) which was responsible for the creation of the

International Financial Reporting Standards (IFRSs). The main purpose of the framework included:

1. Development of the new accounting standards and reviewing the existing ones for changes, if

required.

2. Promotion of the harmonization of the regulation and standards by reduction in the number of

permitted alterations.

3. Assisting in the preparation of the financial statements through IFRS for which the accounting

standard is not in place15.

The framework would include the below details mainly:

1. The objective of the financial statements

2. The reporting entity

3. The parties who will be using the financial statements

4. The qualitative characteristics which render the financial statements useful

5. The elements of the financial statements like that of assets, liability, incomes and expenses and

the relevant treatment.

The IFRS is a world class accounting standard produced by IASB has the following advantages for the

companies adopting them:

1. It is a set of widely accepted and transparent standards which help in producing high quality and

consistent and comparable financial statements all over the world.

13 Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

14 DeZoort, F., & Harrison, P. (2016). Understanding Auditors sense of Responsibility for detecting

fraud within organization. Journal of Business Ethics, 1-18.

15 Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (fourth ed.). New York:

Routledge.

7 | P a g e

8

2. They have been prepared in consultation with the internationally renowned standard setters

with an objective of achieving global convergence and providing adequate flexibility to the

accountants round the world16.

3. Companies which prepare their financial statements in accordance with the IFRS and get their

accounts audited in line with ISA do have enhanced status and reputation.

4. Companies which do have subsidiaries do find it easy for consolidation of the subsidiaries

accounts under IFRS rules17.

5. Companies using the IFRS for accounting do find the financial statements comparable, this

removes the need for further reconciliation between the local GAAP and the IFRS.

Bibliography

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

16 Dumay, J., & Baard, V. (2017). An introduction to interventionist research in accounting. The

Routledge Companion to Qualitative Accounting Research Methods, 265.

17 Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25(1), 57-80.

8 | P a g e

2. They have been prepared in consultation with the internationally renowned standard setters

with an objective of achieving global convergence and providing adequate flexibility to the

accountants round the world16.

3. Companies which prepare their financial statements in accordance with the IFRS and get their

accounts audited in line with ISA do have enhanced status and reputation.

4. Companies which do have subsidiaries do find it easy for consolidation of the subsidiaries

accounts under IFRS rules17.

5. Companies using the IFRS for accounting do find the financial statements comparable, this

removes the need for further reconciliation between the local GAAP and the IFRS.

Bibliography

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

16 Dumay, J., & Baard, V. (2017). An introduction to interventionist research in accounting. The

Routledge Companion to Qualitative Accounting Research Methods, 265.

17 Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25(1), 57-80.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Appelbaum, D., Kogan, A., & Vasarhelyi, M. (2018). Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics. . Journal of

Accounting Literature, 40(1), 83-101.

Bumgarner, N., & Vasarhelyi, M. (2018). Continuous auditing—a new view. Continuous Auditing: Theory

and Application, 20(1), 7-51.

Chron. (2017). five-common-features-internal-control-system-business. Retrieved december 07, 2017,

from http://smallbusiness.chron.com/five-common-features-internal-control-system-business-

430.html

DeZoort, F., & Harrison, P. (2016). Understanding Auditors sense of Responsibility for detecting fraud

within organization. Journal of Business Ethics, 1-18.

Dumay, J., & Baard, V. (2017). An introduction to interventionist research in accounting. The Routledge

Companion to Qualitative Accounting Research Methods, 265. Retrieved from

https://books.google.co.in/books?

hl=en&lr=&id=PzQlDwAAQBAJ&oi=fnd&pg=PA265&dq=Dumay,+J.,+%26+Baard,+V.+(2017).

+An+introduction+to+interventionist+research+in+accounting.

+The+Routledge+Companion+to+Qualitative+Accounting+Research+Methods,

+265.&ots=ta1isTHB

Gooley, J. (2016). Principles of Australian Contract Law. Australia: Lexis Nexis.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, 1-35.

Kew, J., & Stredwick, J. (2017). Business Environment: Managing in a Strategic Context (second ed.).

London: Chartered Institute of Personnel and Development.

Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (fourth ed.). New York: Routledge.

Lessambo, F. (2018). Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), 183-202.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved from

http://psycnet.apa.org/buy/2016-21263-001

9 | P a g e

Appelbaum, D., Kogan, A., & Vasarhelyi, M. (2018). Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics. . Journal of

Accounting Literature, 40(1), 83-101.

Bumgarner, N., & Vasarhelyi, M. (2018). Continuous auditing—a new view. Continuous Auditing: Theory

and Application, 20(1), 7-51.

Chron. (2017). five-common-features-internal-control-system-business. Retrieved december 07, 2017,

from http://smallbusiness.chron.com/five-common-features-internal-control-system-business-

430.html

DeZoort, F., & Harrison, P. (2016). Understanding Auditors sense of Responsibility for detecting fraud

within organization. Journal of Business Ethics, 1-18.

Dumay, J., & Baard, V. (2017). An introduction to interventionist research in accounting. The Routledge

Companion to Qualitative Accounting Research Methods, 265. Retrieved from

https://books.google.co.in/books?

hl=en&lr=&id=PzQlDwAAQBAJ&oi=fnd&pg=PA265&dq=Dumay,+J.,+%26+Baard,+V.+(2017).

+An+introduction+to+interventionist+research+in+accounting.

+The+Routledge+Companion+to+Qualitative+Accounting+Research+Methods,

+265.&ots=ta1isTHB

Gooley, J. (2016). Principles of Australian Contract Law. Australia: Lexis Nexis.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, 1-35.

Kew, J., & Stredwick, J. (2017). Business Environment: Managing in a Strategic Context (second ed.).

London: Chartered Institute of Personnel and Development.

Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (fourth ed.). New York: Routledge.

Lessambo, F. (2018). Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), 183-202.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved from

http://psycnet.apa.org/buy/2016-21263-001

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Visinescu, L., Jones, M., & Sidorova, A. (2017). Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), 58-66.

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25(1), 57-80.

10 | P a g e

Visinescu, L., Jones, M., & Sidorova, A. (2017). Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), 58-66.

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25(1), 57-80.

10 | P a g e

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.