Evaluating the Impact of IFRS on Global Financial Reporting Practices

VerifiedAdded on 2020/06/03

|15

|3277

|115

Essay

AI Summary

Financial reporting is a critical tool for businesses worldwide, providing essential information to stakeholders about an organization's financial health. The adoption of International Financial Reporting Standards (IFRS) plays a pivotal role in enhancing transparency and trust. IFRS aims to standardize financial statements across different countries, making it easier for investors, creditors, and other stakeholders to compare and analyze financial data. This essay delves into the importance of financial reporting, examining how scandals can be mitigated by adhering to these standards. It highlights case studies from various regions, including the Middle East North Africa (MENA) region, where macroeconomic factors influence IFRS adoption. Additionally, it explores the cultural impacts on financial statement comparability and the transition challenges faced by developing countries like Indonesia. The essay concludes that robust financial reporting practices are indispensable for building stakeholder trust and ensuring informed decision-making.

International Financial

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1. Purpose of financial reporting............................................................................................1

2. Outline conceptual framework and qualitative characteristics of financial information . .2

3. Important stakeholders of company...................................................................................2

4. Highlighting value of financial reporting ..........................................................................3

5. Producing financial statements ..........................................................................................4

6. Presenting financial ratios..................................................................................................7

7. Difference between IAS and IFRS.....................................................................................8

8. Benefits of IFRS.................................................................................................................9

9. Varying degrees of compliance with IFRS......................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

1. Purpose of financial reporting............................................................................................1

2. Outline conceptual framework and qualitative characteristics of financial information . .2

3. Important stakeholders of company...................................................................................2

4. Highlighting value of financial reporting ..........................................................................3

5. Producing financial statements ..........................................................................................4

6. Presenting financial ratios..................................................................................................7

7. Difference between IAS and IFRS.....................................................................................8

8. Benefits of IFRS.................................................................................................................9

9. Varying degrees of compliance with IFRS......................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial reporting plays vital role in providing effective information to stakeholders' to

take enhanced decisions with much ease. The enclosed report deals with importance of financial

reporting to organisations. The financial statements prepared by accountants are governed by

professional bodies which has accuracy in such statements. The report also discusses about the

professional bodies such as IAS and IFRS which have immense benefits to organisation as well

as stakeholders'. On the other hand, financial ratios are also computed for the company. The

qualitative characteristics of financial information are also discussed which provides clarity to

users of accounting information to assess financial health of organisation.

1. Purpose of financial reporting

Financial reporting is important for various stakeholders as it provides much needed

information to them in the best possible way. The preparation of financial reports is not an easy

task as talented accounting professionals are required (Stent, Bradbury and Hooks, 2017). This

report helps company to ascertain whether profit is made or loss has been incurred in a particular

period. As such, it is relevant for stakeholders as well as management of the company to take

better and effective decisions.

Another purpose is that investors and creditors require such information to assess whether

to provide funds to organisation or not. If financial position of organisation is strong, this means

that higher returns will be provided to investors. On the other hand, creditors analyse financial

reports by determining debt paying capacity of company and as such, these stakeholders' seeks

financial reports to analyse financial health of company.

Financial reporting is used to prevent scandals which are prevailing internationally. As

such, fair reports are prepared by company which is then provided to stakeholders' and as a

result, they seek reports for assessing financial position of organisation quite effectively (Graham

and et.al, 2017). It has sectioned of liabilities and assets which is much relevant to stakeholders.

Moreover, financial reports are also used for the purpose of imparting information to

stakeholders about the capital which is sufficient for future growth or not. As such, clarity is

observed as lenders and investors seeks financial reports.

The elements of financial reporting are balance sheet, cash flow statement, income

statement, changes in stockholder’s' equity. These financial statements are important to be

1

Financial reporting plays vital role in providing effective information to stakeholders' to

take enhanced decisions with much ease. The enclosed report deals with importance of financial

reporting to organisations. The financial statements prepared by accountants are governed by

professional bodies which has accuracy in such statements. The report also discusses about the

professional bodies such as IAS and IFRS which have immense benefits to organisation as well

as stakeholders'. On the other hand, financial ratios are also computed for the company. The

qualitative characteristics of financial information are also discussed which provides clarity to

users of accounting information to assess financial health of organisation.

1. Purpose of financial reporting

Financial reporting is important for various stakeholders as it provides much needed

information to them in the best possible way. The preparation of financial reports is not an easy

task as talented accounting professionals are required (Stent, Bradbury and Hooks, 2017). This

report helps company to ascertain whether profit is made or loss has been incurred in a particular

period. As such, it is relevant for stakeholders as well as management of the company to take

better and effective decisions.

Another purpose is that investors and creditors require such information to assess whether

to provide funds to organisation or not. If financial position of organisation is strong, this means

that higher returns will be provided to investors. On the other hand, creditors analyse financial

reports by determining debt paying capacity of company and as such, these stakeholders' seeks

financial reports to analyse financial health of company.

Financial reporting is used to prevent scandals which are prevailing internationally. As

such, fair reports are prepared by company which is then provided to stakeholders' and as a

result, they seek reports for assessing financial position of organisation quite effectively (Graham

and et.al, 2017). It has sectioned of liabilities and assets which is much relevant to stakeholders.

Moreover, financial reports are also used for the purpose of imparting information to

stakeholders about the capital which is sufficient for future growth or not. As such, clarity is

observed as lenders and investors seeks financial reports.

The elements of financial reporting are balance sheet, cash flow statement, income

statement, changes in stockholder’s' equity. These financial statements are important to be

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

prepared carefully as it is reflected in financial reports. Moreover, it is also used for bidding and

labour contracts as well. Thus, financial reports are useful tool for exhibiting true financial

information of the company quite effectively.

2. Outline conceptual framework and qualitative characteristics of financial information

Conceptual framework are used to distinct and organise the various ideas having all the

information which is important and real so that they could be easily remembered. This is also

regarded to as the generally accepted theoretical principles forming the important part of

particular field of enquiry (A conceptual and regulatory framework, 2018). There are mainly 4

characteristics of this framework which are relevance, reliability, comparability and

understandability this will be helping the financial information to b more accurate and reliable.

Purpose-

The main purpose of the financial information systems is to provide useful data which

will be the base of economic decision making for the company. This framework is also providing

rule and standard for accounting so that this could set a limit and lead to creation of set of rule.

One of the primary function of conceptual framework is to assist IASB so that they could

develop for future IFRS and could review the existing one.

The characteristics which are stated will be making financial information more reliable as

the framework would be relevant, reliable, comparable and understandable to the user of the

information. Thus, this will be helping in furthermore accuracy of data which is given.

Regulatory framework-

This is the policy and guidelines which are governing the control and implementation of

adopted action plan and principles. The International Accounting Standards Board (IASC) will

be providing the framework (A conceptual and regulatory framework, 2018). This is also a rule

based standards of accounting which is regulated by specified piece of legislation like that

protection of environment.

3. Important stakeholders of company

Stakeholders are the people who are whether directly or indirectly connected to the

business with some or the other motive they are having some interest in the financial information

or performance of the organisation. Some stakeholders of business are as follows:

2

labour contracts as well. Thus, financial reports are useful tool for exhibiting true financial

information of the company quite effectively.

2. Outline conceptual framework and qualitative characteristics of financial information

Conceptual framework are used to distinct and organise the various ideas having all the

information which is important and real so that they could be easily remembered. This is also

regarded to as the generally accepted theoretical principles forming the important part of

particular field of enquiry (A conceptual and regulatory framework, 2018). There are mainly 4

characteristics of this framework which are relevance, reliability, comparability and

understandability this will be helping the financial information to b more accurate and reliable.

Purpose-

The main purpose of the financial information systems is to provide useful data which

will be the base of economic decision making for the company. This framework is also providing

rule and standard for accounting so that this could set a limit and lead to creation of set of rule.

One of the primary function of conceptual framework is to assist IASB so that they could

develop for future IFRS and could review the existing one.

The characteristics which are stated will be making financial information more reliable as

the framework would be relevant, reliable, comparable and understandable to the user of the

information. Thus, this will be helping in furthermore accuracy of data which is given.

Regulatory framework-

This is the policy and guidelines which are governing the control and implementation of

adopted action plan and principles. The International Accounting Standards Board (IASC) will

be providing the framework (A conceptual and regulatory framework, 2018). This is also a rule

based standards of accounting which is regulated by specified piece of legislation like that

protection of environment.

3. Important stakeholders of company

Stakeholders are the people who are whether directly or indirectly connected to the

business with some or the other motive they are having some interest in the financial information

or performance of the organisation. Some stakeholders of business are as follows:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Employees- they are internal stakeholders of the company who are been employed into

organisation so that profits could be achieved and targets are fulfilled (The Importance of

Stakeholders, 2018).. They will be in use of financial information so that they could determine

that whether they would be getting their salary or bonus this year or not. They will be affected by

the financial performance of business in both direct and indirect manner.

Shareholders- they are the main stakeholders of company as they are the one who invest their

money into company in order to earn profits in form of dividend. For analysing in which

company and in what amount to invest they will be in need of financial information of that

business. Shareholders are the source of investment for any firm so they are likely to see and

analyse the accounts of company.

Suppliers- they are external stakeholders of the company who are making available all type of

raw materials and machines for the company (The Importance of Stakeholders, 2018). Suppliers

are also having interest within the financial information of company for the purpose to analyse

that whether they will be getting the money in return to the raw materials which they are

supplying to firm. As suppliers are the creditors of firm so they are interested in financial

information.

Customers- they are also important stakeholders of firm who will be determining the profits and

sales for company and customers are in need of statements so that they could make the decision

of purchasing product and service of that company.

4. Highlighting value of financial reporting

All the stakeholders of the company are in need of financial reporting for different

reasons which are as under:

This will be important as will be facilitating statutory audit of the firm and auditor will be

expressing their opinion (Importance of Financial Reporting, 2018)

This financial reporting is backbone to financial plan, analysis and making decision making and

are used by various stakeholders.

The whole public will be analysing performance of businesses and that of management.

The firm will be able to comply with statues and regulatory requirements and then filling the

financial statements to ROC and government agencies as well.

3

organisation so that profits could be achieved and targets are fulfilled (The Importance of

Stakeholders, 2018).. They will be in use of financial information so that they could determine

that whether they would be getting their salary or bonus this year or not. They will be affected by

the financial performance of business in both direct and indirect manner.

Shareholders- they are the main stakeholders of company as they are the one who invest their

money into company in order to earn profits in form of dividend. For analysing in which

company and in what amount to invest they will be in need of financial information of that

business. Shareholders are the source of investment for any firm so they are likely to see and

analyse the accounts of company.

Suppliers- they are external stakeholders of the company who are making available all type of

raw materials and machines for the company (The Importance of Stakeholders, 2018). Suppliers

are also having interest within the financial information of company for the purpose to analyse

that whether they will be getting the money in return to the raw materials which they are

supplying to firm. As suppliers are the creditors of firm so they are interested in financial

information.

Customers- they are also important stakeholders of firm who will be determining the profits and

sales for company and customers are in need of statements so that they could make the decision

of purchasing product and service of that company.

4. Highlighting value of financial reporting

All the stakeholders of the company are in need of financial reporting for different

reasons which are as under:

This will be important as will be facilitating statutory audit of the firm and auditor will be

expressing their opinion (Importance of Financial Reporting, 2018)

This financial reporting is backbone to financial plan, analysis and making decision making and

are used by various stakeholders.

The whole public will be analysing performance of businesses and that of management.

The firm will be able to comply with statues and regulatory requirements and then filling the

financial statements to ROC and government agencies as well.

3

This will also be important for filling the stock exchange and published their annual results are

required.

They will also be helpful in purpose of bidding and labour markets as company will be able to

furnish their financial reports and statements.

They will also be including the financial performance of the firm and telling how they are

earning profits and sales revenue for the firm (Importance of Financial Reporting, 2018) .

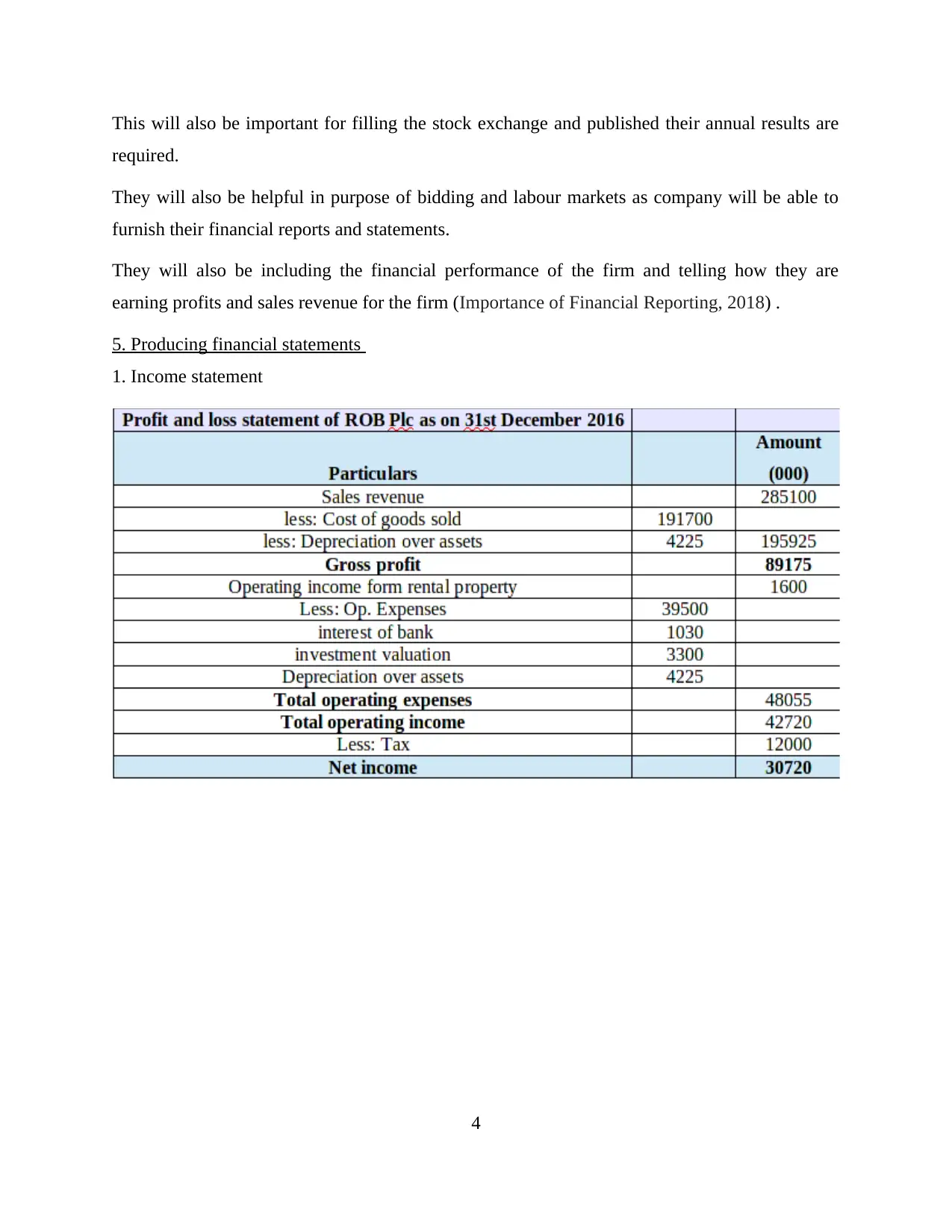

5. Producing financial statements

1. Income statement

4

required.

They will also be helpful in purpose of bidding and labour markets as company will be able to

furnish their financial reports and statements.

They will also be including the financial performance of the firm and telling how they are

earning profits and sales revenue for the firm (Importance of Financial Reporting, 2018) .

5. Producing financial statements

1. Income statement

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

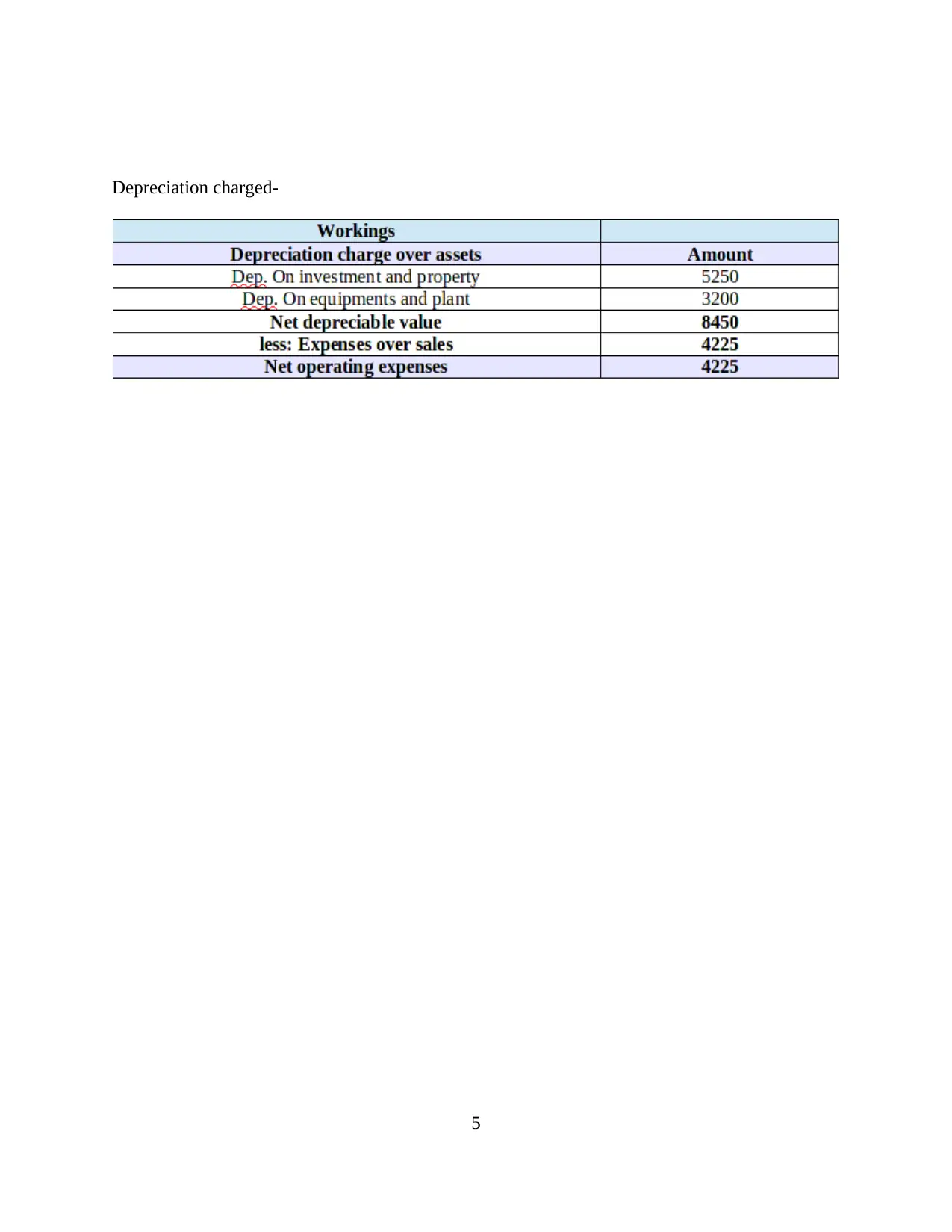

Depreciation charged-

5

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

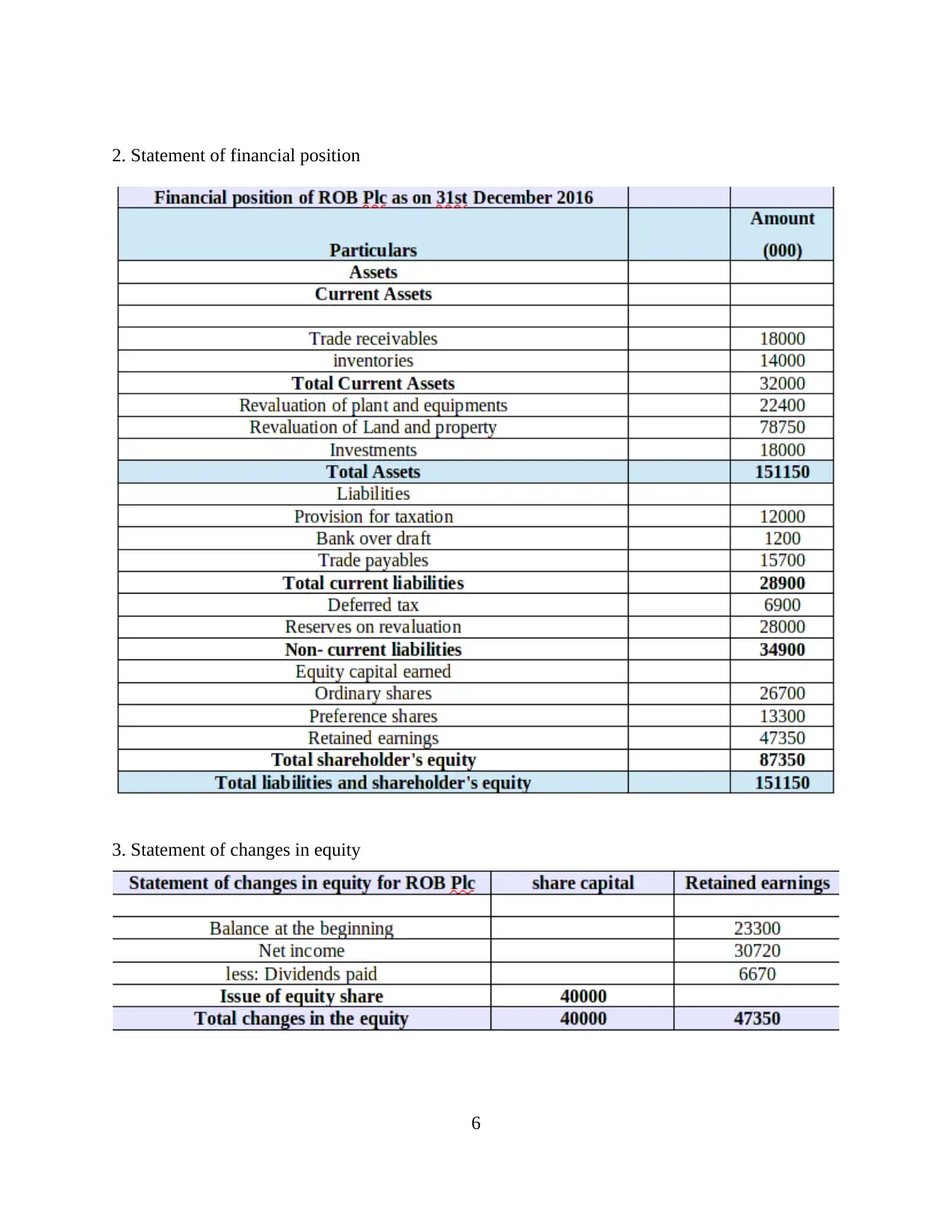

2. Statement of financial position

3. Statement of changes in equity

6

3. Statement of changes in equity

6

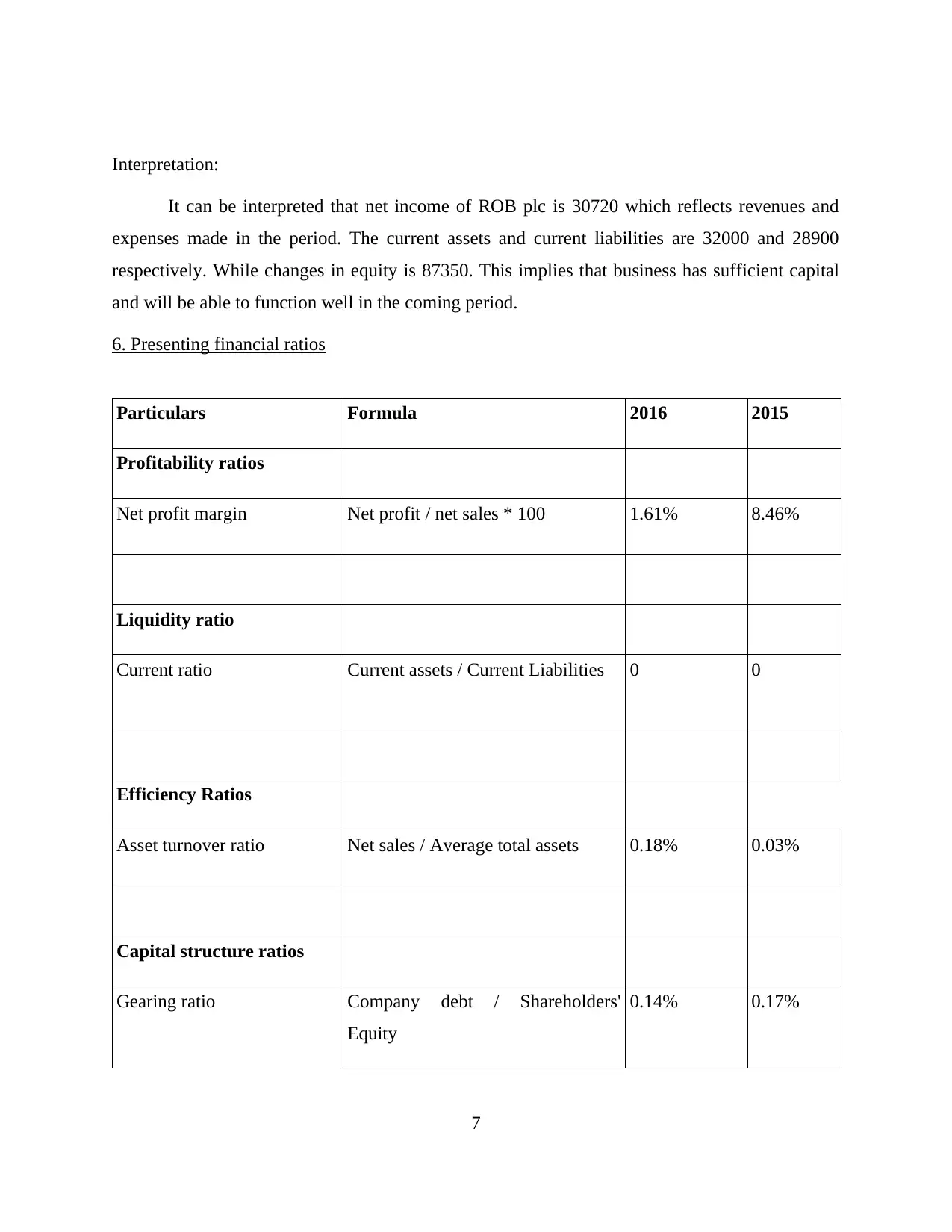

Interpretation:

It can be interpreted that net income of ROB plc is 30720 which reflects revenues and

expenses made in the period. The current assets and current liabilities are 32000 and 28900

respectively. While changes in equity is 87350. This implies that business has sufficient capital

and will be able to function well in the coming period.

6. Presenting financial ratios

Particulars Formula 2016 2015

Profitability ratios

Net profit margin Net profit / net sales * 100 1.61% 8.46%

Liquidity ratio

Current ratio Current assets / Current Liabilities 0 0

Efficiency Ratios

Asset turnover ratio Net sales / Average total assets 0.18% 0.03%

Capital structure ratios

Gearing ratio Company debt / Shareholders'

Equity

0.14% 0.17%

7

It can be interpreted that net income of ROB plc is 30720 which reflects revenues and

expenses made in the period. The current assets and current liabilities are 32000 and 28900

respectively. While changes in equity is 87350. This implies that business has sufficient capital

and will be able to function well in the coming period.

6. Presenting financial ratios

Particulars Formula 2016 2015

Profitability ratios

Net profit margin Net profit / net sales * 100 1.61% 8.46%

Liquidity ratio

Current ratio Current assets / Current Liabilities 0 0

Efficiency Ratios

Asset turnover ratio Net sales / Average total assets 0.18% 0.03%

Capital structure ratios

Gearing ratio Company debt / Shareholders'

Equity

0.14% 0.17%

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the above calculated ratios, financial position of Legal and General group plc has

been highlighted quite effectively. The profitability, efficiency, liquidity ratios are being

calculated which shows that financial position of the company is not good. Starting with the

profitability ratios such as net profit margin reflects that net profit was good in 2015 which has

declined in 2016 financial year with huge margin. As in 2015 year, net profit margin was 8.46 %

and in 2016 year, it has come to 1.61 %. This implies that Legal and General group is not able to

control expenditures which has resulted into decreased profits (Graham and et.al, 2017).

Furthermore, liquidity ratio such as current ratio is also not good as in both financial

years, it is 0. This means that financial position is not good of the company as liabilities are more

than assets and as such, assets are absorbed by such liabilities. This should be dealt by company

in effective way so that it may come to ideal ratio of 2 : 1. Coming to efficiency ratios such as

asset turnover ratio which is little bit increased from the past year as in 2015 was 0.03 % and in

2016 is 0.18 %. This implies that company is not efficiently utilising assets to generate sales

which has resulted into decreased asset turnover ratio. Capital gearing ratio in 2015 year is 0.17

% and in 2016 is 0.14 % which shows that company is not using debt in functioning daily

activities. However, it should take blend of debt and equity to carry out activities (Kettunen,

2017).

7. Difference between IAS and IFRS

IAS IFRS

1. IAS (International Accounting Standards) is

a professional body which guides accountants

to prepare effective books of accounts by

recording proper entries by complying with

guidelines provided by it.

2. In event of any contradictions, principles

governed by IAS are dropped and is passed on

to IFRS to resolve the same.

3. IAS has limited scope with respect to IFRS

1. IFRS (International Financial Reporting

Standards) is also professional body but

completely differs from IAS. It is based on the

principle that accountants must follow legal

framework provided by it so that true and fair

financial information may be imparted to users

of accounting information.

2. In such contradictions, IFRS guides and

resolve the underlying issues.

8

been highlighted quite effectively. The profitability, efficiency, liquidity ratios are being

calculated which shows that financial position of the company is not good. Starting with the

profitability ratios such as net profit margin reflects that net profit was good in 2015 which has

declined in 2016 financial year with huge margin. As in 2015 year, net profit margin was 8.46 %

and in 2016 year, it has come to 1.61 %. This implies that Legal and General group is not able to

control expenditures which has resulted into decreased profits (Graham and et.al, 2017).

Furthermore, liquidity ratio such as current ratio is also not good as in both financial

years, it is 0. This means that financial position is not good of the company as liabilities are more

than assets and as such, assets are absorbed by such liabilities. This should be dealt by company

in effective way so that it may come to ideal ratio of 2 : 1. Coming to efficiency ratios such as

asset turnover ratio which is little bit increased from the past year as in 2015 was 0.03 % and in

2016 is 0.18 %. This implies that company is not efficiently utilising assets to generate sales

which has resulted into decreased asset turnover ratio. Capital gearing ratio in 2015 year is 0.17

% and in 2016 is 0.14 % which shows that company is not using debt in functioning daily

activities. However, it should take blend of debt and equity to carry out activities (Kettunen,

2017).

7. Difference between IAS and IFRS

IAS IFRS

1. IAS (International Accounting Standards) is

a professional body which guides accountants

to prepare effective books of accounts by

recording proper entries by complying with

guidelines provided by it.

2. In event of any contradictions, principles

governed by IAS are dropped and is passed on

to IFRS to resolve the same.

3. IAS has limited scope with respect to IFRS

1. IFRS (International Financial Reporting

Standards) is also professional body but

completely differs from IAS. It is based on the

principle that accountants must follow legal

framework provided by it so that true and fair

financial information may be imparted to users

of accounting information.

2. In such contradictions, IFRS guides and

resolve the underlying issues.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Janowicz, 2017).

4. IASC (International Accounting Standards

Committee) has issued standards to IAS which

is now completely replaced by IASB

(International Accounting Standards Board).

5. The accounting standards provided by IAS

guides accountants to maintain proper

accounting records in effective manner. This

provides accuracy in financial reporting quite

effectively.

6. Classification of equity instruments are done

through FVPL (Fair Value Through Profit and

Loss)

3. The scope of IFRS is much wider than IAS.

4. On the other hand, standards of IFRS is

issued by IASB.

5. On the other hand, standards of IFRS differ

from IAS. It provides legal framework which is

required so that transparency in financial

reporting may be imparted to users of such

information. As such, rules and regulations are

required to be followed by accountants.

6. While in this, instruments are classified

according to Fair Value Through

Comprehensive Income.

8. Benefits of IFRS

IFRS have enough benefits to organisations. The benefits are listed below:

1. Shareholders' are benefited because company is legally imbibed to follow rules and

regulations provided by IFRS. The shareholders' are benefited as information with reference to

dividend policies are produced by organisation and this highlights clarity to them (Ward and

Lowe, 2017). The financial position if strong, then more subscribers will be attracted to company

and as such, company will also be benefited by having larger capital for carrying out day to day

activities with much ease.

2. The benefits are being provided to investors and creditors as well. Investors are benefited as

they come to know about the financial health of firm and as such, they have clarity whether to

invest in the company or not. While, creditors make out decisions whether debt should be

provided to company or not. This is done to analyse debt paying capacity of firm. As such, IFRS

provides clarity to these stakeholders' as well.

3. The legal framework provided by IFRS are universally accepted by companies and as such,

transparency and clarity in financial information is done which is then reflected in financial

9

4. IASC (International Accounting Standards

Committee) has issued standards to IAS which

is now completely replaced by IASB

(International Accounting Standards Board).

5. The accounting standards provided by IAS

guides accountants to maintain proper

accounting records in effective manner. This

provides accuracy in financial reporting quite

effectively.

6. Classification of equity instruments are done

through FVPL (Fair Value Through Profit and

Loss)

3. The scope of IFRS is much wider than IAS.

4. On the other hand, standards of IFRS is

issued by IASB.

5. On the other hand, standards of IFRS differ

from IAS. It provides legal framework which is

required so that transparency in financial

reporting may be imparted to users of such

information. As such, rules and regulations are

required to be followed by accountants.

6. While in this, instruments are classified

according to Fair Value Through

Comprehensive Income.

8. Benefits of IFRS

IFRS have enough benefits to organisations. The benefits are listed below:

1. Shareholders' are benefited because company is legally imbibed to follow rules and

regulations provided by IFRS. The shareholders' are benefited as information with reference to

dividend policies are produced by organisation and this highlights clarity to them (Ward and

Lowe, 2017). The financial position if strong, then more subscribers will be attracted to company

and as such, company will also be benefited by having larger capital for carrying out day to day

activities with much ease.

2. The benefits are being provided to investors and creditors as well. Investors are benefited as

they come to know about the financial health of firm and as such, they have clarity whether to

invest in the company or not. While, creditors make out decisions whether debt should be

provided to company or not. This is done to analyse debt paying capacity of firm. As such, IFRS

provides clarity to these stakeholders' as well.

3. The legal framework provided by IFRS are universally accepted by companies and as such,

transparency and clarity in financial information is done which is then reflected in financial

9

reports. Stakeholders such as external or internal are much benefited by such guidelines of

professional body. Such information is utilised by stakeholders to take better and effective

decisions (Stent, Bradbury and Hooks, 2017).

4. IFRS guidelines are also helpful for companies as through this, it is able to provide correct and

accurate financial information to users of financial information. As such, company provides

clarity of financial health to stakeholders' which in turn helps company to generate high funds as

shareholders' subscribes to shares of the organisation.

5. The financial reports are provided with qualitative characteristics of financial information

such as comparability, understandability, reliability and timeliness which is helpful to investors

and creditors to take better and enhanced decisions with much ease.

6. The investors can easily compare financial statements of two different companies as they are

following same financial statements format. This means that gross profit, operating income and

net profit fall under same category and as such, financial statements are easier to evaluate even to

two different organisations quite effectively.

9. Varying degrees of compliance with IFRS

The above examples of ROB plc and Legal and General group plc, it can be conveyed

that both are using effective legal framework by complying with rules and regulations in

effectual manner. This is required so that financial reports are prepared with much ease and

highlights financial health of company (Maradona and Chand, 2017). This is required so that

proper information may be provided to users of accounting information having transparency and

accuracy so that they may take effective and enhanced decisions. This also helps company to

have legal identity and as a result, stakeholders' rely on such financial reports to take decisions.

According to IAS 38 which states that customers' lists and publishing titles are restricted

or prohibited which is required by companies to follow so that they may function effectively by

providing relevant information only. This impacts organisation as it has to abide by such rules. In

addition to this, IAS 29 A states that financial statements such as balance sheet, cash flow

statement and income statement must be prepared by adopting legal framework so that reliable

information may be provided to users of accounting information quite effectively (Financial

reporting). This should be followed by organisation, if it does not follow this, reliability of

financial information is lost. This means that business transactions should be listed in ongoing

period and as such, transparency is completely observed.

10

professional body. Such information is utilised by stakeholders to take better and effective

decisions (Stent, Bradbury and Hooks, 2017).

4. IFRS guidelines are also helpful for companies as through this, it is able to provide correct and

accurate financial information to users of financial information. As such, company provides

clarity of financial health to stakeholders' which in turn helps company to generate high funds as

shareholders' subscribes to shares of the organisation.

5. The financial reports are provided with qualitative characteristics of financial information

such as comparability, understandability, reliability and timeliness which is helpful to investors

and creditors to take better and enhanced decisions with much ease.

6. The investors can easily compare financial statements of two different companies as they are

following same financial statements format. This means that gross profit, operating income and

net profit fall under same category and as such, financial statements are easier to evaluate even to

two different organisations quite effectively.

9. Varying degrees of compliance with IFRS

The above examples of ROB plc and Legal and General group plc, it can be conveyed

that both are using effective legal framework by complying with rules and regulations in

effectual manner. This is required so that financial reports are prepared with much ease and

highlights financial health of company (Maradona and Chand, 2017). This is required so that

proper information may be provided to users of accounting information having transparency and

accuracy so that they may take effective and enhanced decisions. This also helps company to

have legal identity and as a result, stakeholders' rely on such financial reports to take decisions.

According to IAS 38 which states that customers' lists and publishing titles are restricted

or prohibited which is required by companies to follow so that they may function effectively by

providing relevant information only. This impacts organisation as it has to abide by such rules. In

addition to this, IAS 29 A states that financial statements such as balance sheet, cash flow

statement and income statement must be prepared by adopting legal framework so that reliable

information may be provided to users of accounting information quite effectively (Financial

reporting). This should be followed by organisation, if it does not follow this, reliability of

financial information is lost. This means that business transactions should be listed in ongoing

period and as such, transparency is completely observed.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.