Financial Reporting: IFRS 16, IAS 17, IAS 16, and IAS 2 Analysis

VerifiedAdded on 2023/01/09

|20

|3397

|2

Report

AI Summary

This report provides a detailed analysis of key International Financial Reporting Standards (IFRS), focusing on IFRS 16 (Leases), IAS 17, IAS 16 (Property, Plant and Equipment), and IAS 2 (Inventories). The report begins by explaining IFRS 16 and its impact on lease accounting, differentiating between finance and operating leases, and outlining the accounting treatments for both lessors and lessees. It then delves into the accounting for property, plant, and equipment under IAS 16, clarifying the distinction between capital and revenue expenditures, and demonstrating the calculation of asset costs. Finally, the report examines IAS 2, explaining how the cost of inventories should be determined. The report includes practical calculations, such as implicit interest rate calculations and journal entries, to illustrate the application of these standards. The content covers the key elements of each standard, providing a comprehensive overview for financial reporting and accounting students.

International Financial

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.....................................................................................................................................3

MAIN BODY.............................................................................................................................................3

PART 1: LEASE-IFRS 16/IAS 17..........................................................................................................3

PART 2: PROPERTY, PLANTS AND EQUIPMENTS – IAS 16..........................................................9

PART 3: INVENTORIES – IAS 2........................................................................................................12

CONCLUSION........................................................................................................................................19

REFERENCES........................................................................................................................................20

INTRODUCTION.....................................................................................................................................3

MAIN BODY.............................................................................................................................................3

PART 1: LEASE-IFRS 16/IAS 17..........................................................................................................3

PART 2: PROPERTY, PLANTS AND EQUIPMENTS – IAS 16..........................................................9

PART 3: INVENTORIES – IAS 2........................................................................................................12

CONCLUSION........................................................................................................................................19

REFERENCES........................................................................................................................................20

INTRODUCTION

In order to record financial transactions and preparation of financial reports, there are a

range of standards which need to be followed by companies who are operating at global level.

The international financial reporting can be defined as a process of presenting financial

statements in a manner that is adopted commonly by all companies at international stage (Eng

and Neiva De Figueiredo, 2019). There are different kinds of standards which need to be

consider various types of transactions. The project report consists three parts and each of them is

based on various IAS (International accounting standards). The part one is related to lease

transactions and for which IFRS 16/IAS 17 are described. Part two is related to property, plants

and equipment transactions while the last part of report covers information about IAS 2 which

linked to inventories.

MAIN BODY

PART 1: LEASE-IFRS 16/IAS 17

(a) Discuss the IFRS 16 required lease accounting treatment and reporting by lessor for

finance leases and operating leases as carried forward by IAS 17.

IFRS 16 is a reformed accounting standard which was evolved by IASB (International

accounting standards board) in January 2016. This accounting standard replace the

previous standard IAS 17 (Segal, and Naik, 2019). The objective of this accounting

standard to provide way through which companies can record their lease transactions at

the time of financial disclosure. IFRS 16 enables a specific lessee accounting approach

and needs a lessee to identify assets and liabilities for all leases whose durability is more

than one year. As per this standard, it is essential for lessee to identify a right of use

assets presenting the right to use the underlying leased assets. As well as lease liability

presenting the obligation in order to do payment of leases.

Reason to replace IAS 17: IAS 17 divided leases in two forms which are finance and

operating leases. As per this standard, finance lease was exploited in the balance sheet

and reported in the profit & loss statement as an interest and depreciation expense. On the

In order to record financial transactions and preparation of financial reports, there are a

range of standards which need to be followed by companies who are operating at global level.

The international financial reporting can be defined as a process of presenting financial

statements in a manner that is adopted commonly by all companies at international stage (Eng

and Neiva De Figueiredo, 2019). There are different kinds of standards which need to be

consider various types of transactions. The project report consists three parts and each of them is

based on various IAS (International accounting standards). The part one is related to lease

transactions and for which IFRS 16/IAS 17 are described. Part two is related to property, plants

and equipment transactions while the last part of report covers information about IAS 2 which

linked to inventories.

MAIN BODY

PART 1: LEASE-IFRS 16/IAS 17

(a) Discuss the IFRS 16 required lease accounting treatment and reporting by lessor for

finance leases and operating leases as carried forward by IAS 17.

IFRS 16 is a reformed accounting standard which was evolved by IASB (International

accounting standards board) in January 2016. This accounting standard replace the

previous standard IAS 17 (Segal, and Naik, 2019). The objective of this accounting

standard to provide way through which companies can record their lease transactions at

the time of financial disclosure. IFRS 16 enables a specific lessee accounting approach

and needs a lessee to identify assets and liabilities for all leases whose durability is more

than one year. As per this standard, it is essential for lessee to identify a right of use

assets presenting the right to use the underlying leased assets. As well as lease liability

presenting the obligation in order to do payment of leases.

Reason to replace IAS 17: IAS 17 divided leases in two forms which are finance and

operating leases. As per this standard, finance lease was exploited in the balance sheet

and reported in the profit & loss statement as an interest and depreciation expense. On the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

other hands, operating lease was reported in the working notes of financial statements and

not exploited in the balance sheet. In addition to this, the traditional method of reporting

operating lease reduced accuracy in actual financial position of firms. As a consequence,

this was not easy for investors to assess actual value of a company so that they can make

investment accordingly.

Reporting by lessor for finance leases and operating leases: The difference between

operating and finance lease is reduced for lessees and a new lease assets and liabilities are

identifying for all leases. As above discussed that lessees must recognize a right of use of

assets and liabilities which are based on discounted pay and needed to the lease. In order

to determine lease term will need judgement that was not required before operating lease

because it did not change the expense recognition. Lessor accounting does not change

and continue to reflect the underlying assets that is subject to lease management in the

balance sheet for leases which are divided as operating. In order to financial

arrangements, the balance sheet informs a lease receivable as well as residual interest of

lessor. It consists some key elements which are needed to followed by lessor such as:

ACCOUNTING FOR FINANCE LEASE BY LESSOR: For lessor, finance lease is

divided in two types. The first one is that if present value of all lease payments is similar

to carrying value of leased assets that is known as direct financing lease (Tóth, 2019).

The second type is that if present value of lease payments is more than carrying value of

leased assets which is known as sales type lease. These both types of finance lease are

recorded by lessor in different financial statements in such manner:

Balance sheet: The value of receivables from lease is recorded along with the assets

which are decreased by book value of leased assets.

Income statement: The value of interest revenue is recorded which is computed in

accordance of lease receivables.

Cash flow statement: The value of interest aspect of lease revenue is recorded in the

operating activity and principle aspect is recorded in investing activities in cash flow.

ACCOUNTING FOR OPERATING LEASE BY LESSOR:

Balance sheet: Under it, leased assets is recorded.

not exploited in the balance sheet. In addition to this, the traditional method of reporting

operating lease reduced accuracy in actual financial position of firms. As a consequence,

this was not easy for investors to assess actual value of a company so that they can make

investment accordingly.

Reporting by lessor for finance leases and operating leases: The difference between

operating and finance lease is reduced for lessees and a new lease assets and liabilities are

identifying for all leases. As above discussed that lessees must recognize a right of use of

assets and liabilities which are based on discounted pay and needed to the lease. In order

to determine lease term will need judgement that was not required before operating lease

because it did not change the expense recognition. Lessor accounting does not change

and continue to reflect the underlying assets that is subject to lease management in the

balance sheet for leases which are divided as operating. In order to financial

arrangements, the balance sheet informs a lease receivable as well as residual interest of

lessor. It consists some key elements which are needed to followed by lessor such as:

ACCOUNTING FOR FINANCE LEASE BY LESSOR: For lessor, finance lease is

divided in two types. The first one is that if present value of all lease payments is similar

to carrying value of leased assets that is known as direct financing lease (Tóth, 2019).

The second type is that if present value of lease payments is more than carrying value of

leased assets which is known as sales type lease. These both types of finance lease are

recorded by lessor in different financial statements in such manner:

Balance sheet: The value of receivables from lease is recorded along with the assets

which are decreased by book value of leased assets.

Income statement: The value of interest revenue is recorded which is computed in

accordance of lease receivables.

Cash flow statement: The value of interest aspect of lease revenue is recorded in the

operating activity and principle aspect is recorded in investing activities in cash flow.

ACCOUNTING FOR OPERATING LEASE BY LESSOR:

Balance sheet: Under it, leased assets is recorded.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

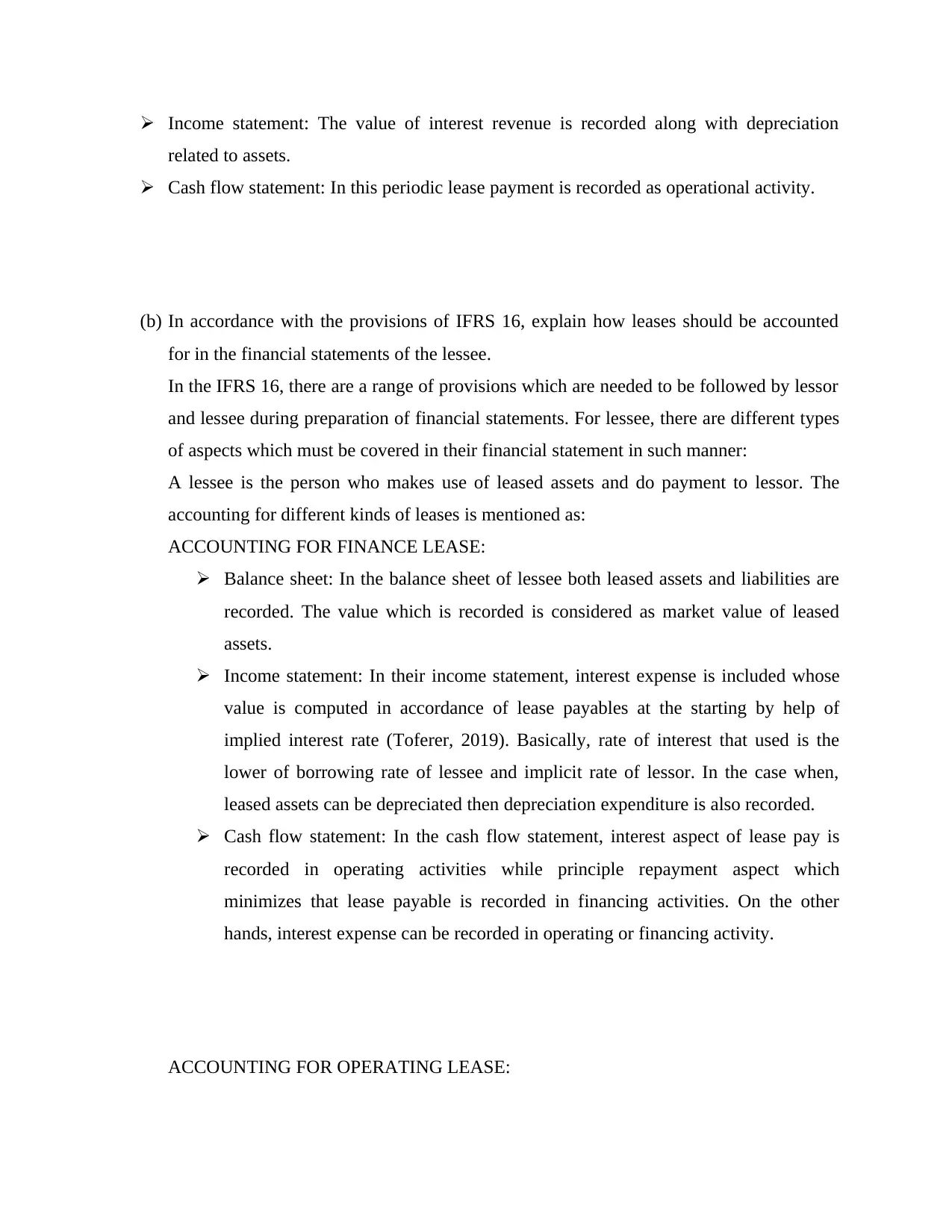

Income statement: The value of interest revenue is recorded along with depreciation

related to assets.

Cash flow statement: In this periodic lease payment is recorded as operational activity.

(b) In accordance with the provisions of IFRS 16, explain how leases should be accounted

for in the financial statements of the lessee.

In the IFRS 16, there are a range of provisions which are needed to be followed by lessor

and lessee during preparation of financial statements. For lessee, there are different types

of aspects which must be covered in their financial statement in such manner:

A lessee is the person who makes use of leased assets and do payment to lessor. The

accounting for different kinds of leases is mentioned as:

ACCOUNTING FOR FINANCE LEASE:

Balance sheet: In the balance sheet of lessee both leased assets and liabilities are

recorded. The value which is recorded is considered as market value of leased

assets.

Income statement: In their income statement, interest expense is included whose

value is computed in accordance of lease payables at the starting by help of

implied interest rate (Toferer, 2019). Basically, rate of interest that used is the

lower of borrowing rate of lessee and implicit rate of lessor. In the case when,

leased assets can be depreciated then depreciation expenditure is also recorded.

Cash flow statement: In the cash flow statement, interest aspect of lease pay is

recorded in operating activities while principle repayment aspect which

minimizes that lease payable is recorded in financing activities. On the other

hands, interest expense can be recorded in operating or financing activity.

ACCOUNTING FOR OPERATING LEASE:

related to assets.

Cash flow statement: In this periodic lease payment is recorded as operational activity.

(b) In accordance with the provisions of IFRS 16, explain how leases should be accounted

for in the financial statements of the lessee.

In the IFRS 16, there are a range of provisions which are needed to be followed by lessor

and lessee during preparation of financial statements. For lessee, there are different types

of aspects which must be covered in their financial statement in such manner:

A lessee is the person who makes use of leased assets and do payment to lessor. The

accounting for different kinds of leases is mentioned as:

ACCOUNTING FOR FINANCE LEASE:

Balance sheet: In the balance sheet of lessee both leased assets and liabilities are

recorded. The value which is recorded is considered as market value of leased

assets.

Income statement: In their income statement, interest expense is included whose

value is computed in accordance of lease payables at the starting by help of

implied interest rate (Toferer, 2019). Basically, rate of interest that used is the

lower of borrowing rate of lessee and implicit rate of lessor. In the case when,

leased assets can be depreciated then depreciation expenditure is also recorded.

Cash flow statement: In the cash flow statement, interest aspect of lease pay is

recorded in operating activities while principle repayment aspect which

minimizes that lease payable is recorded in financing activities. On the other

hands, interest expense can be recorded in operating or financing activity.

ACCOUNTING FOR OPERATING LEASE:

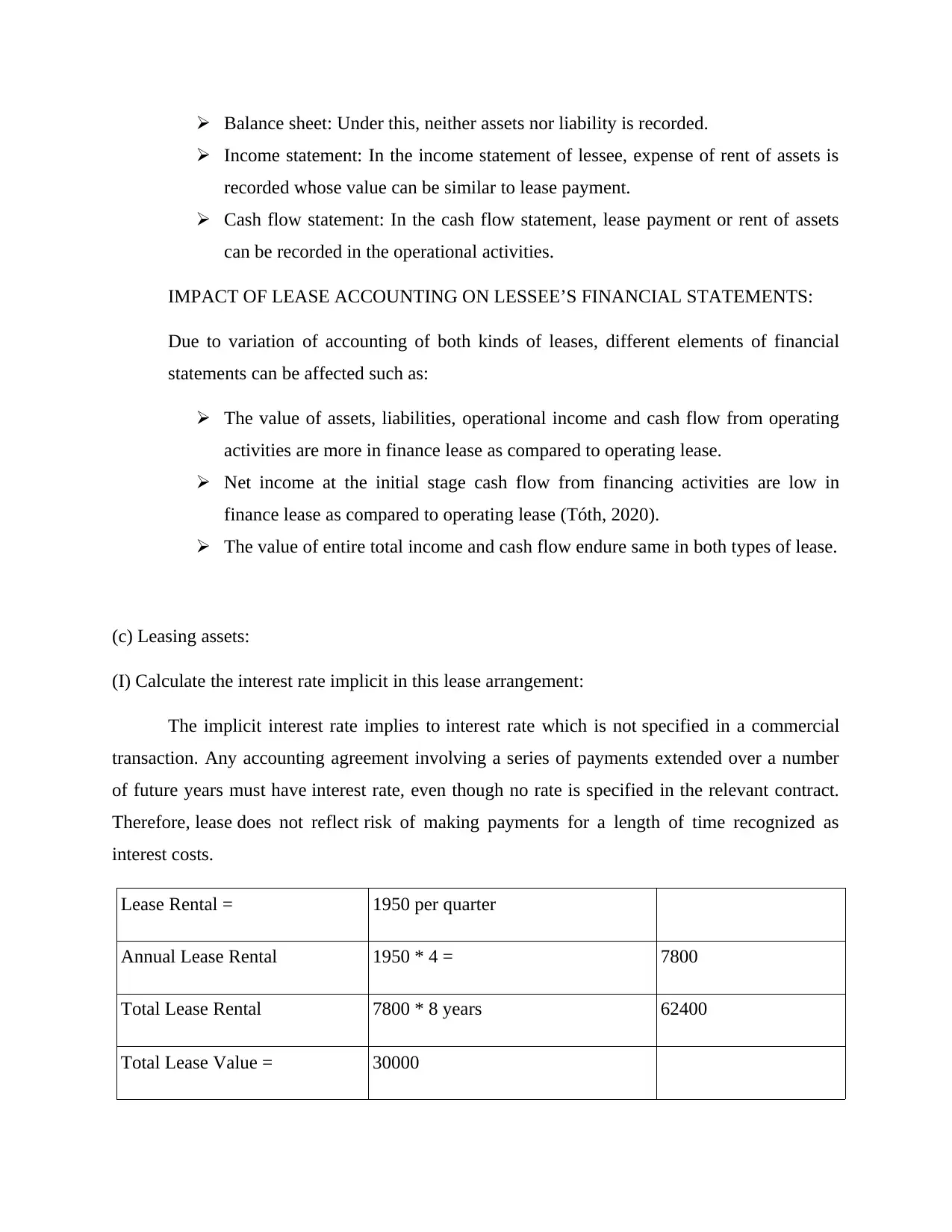

Balance sheet: Under this, neither assets nor liability is recorded.

Income statement: In the income statement of lessee, expense of rent of assets is

recorded whose value can be similar to lease payment.

Cash flow statement: In the cash flow statement, lease payment or rent of assets

can be recorded in the operational activities.

IMPACT OF LEASE ACCOUNTING ON LESSEE’S FINANCIAL STATEMENTS:

Due to variation of accounting of both kinds of leases, different elements of financial

statements can be affected such as:

The value of assets, liabilities, operational income and cash flow from operating

activities are more in finance lease as compared to operating lease.

Net income at the initial stage cash flow from financing activities are low in

finance lease as compared to operating lease (Tóth, 2020).

The value of entire total income and cash flow endure same in both types of lease.

(c) Leasing assets:

(I) Calculate the interest rate implicit in this lease arrangement:

The implicit interest rate implies to interest rate which is not specified in a commercial

transaction. Any accounting agreement involving a series of payments extended over a number

of future years must have interest rate, even though no rate is specified in the relevant contract.

Therefore, lease does not reflect risk of making payments for a length of time recognized as

interest costs.

Lease Rental = 1950 per quarter

Annual Lease Rental 1950 * 4 = 7800

Total Lease Rental 7800 * 8 years 62400

Total Lease Value = 30000

Income statement: In the income statement of lessee, expense of rent of assets is

recorded whose value can be similar to lease payment.

Cash flow statement: In the cash flow statement, lease payment or rent of assets

can be recorded in the operational activities.

IMPACT OF LEASE ACCOUNTING ON LESSEE’S FINANCIAL STATEMENTS:

Due to variation of accounting of both kinds of leases, different elements of financial

statements can be affected such as:

The value of assets, liabilities, operational income and cash flow from operating

activities are more in finance lease as compared to operating lease.

Net income at the initial stage cash flow from financing activities are low in

finance lease as compared to operating lease (Tóth, 2020).

The value of entire total income and cash flow endure same in both types of lease.

(c) Leasing assets:

(I) Calculate the interest rate implicit in this lease arrangement:

The implicit interest rate implies to interest rate which is not specified in a commercial

transaction. Any accounting agreement involving a series of payments extended over a number

of future years must have interest rate, even though no rate is specified in the relevant contract.

Therefore, lease does not reflect risk of making payments for a length of time recognized as

interest costs.

Lease Rental = 1950 per quarter

Annual Lease Rental 1950 * 4 = 7800

Total Lease Rental 7800 * 8 years 62400

Total Lease Value = 30000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

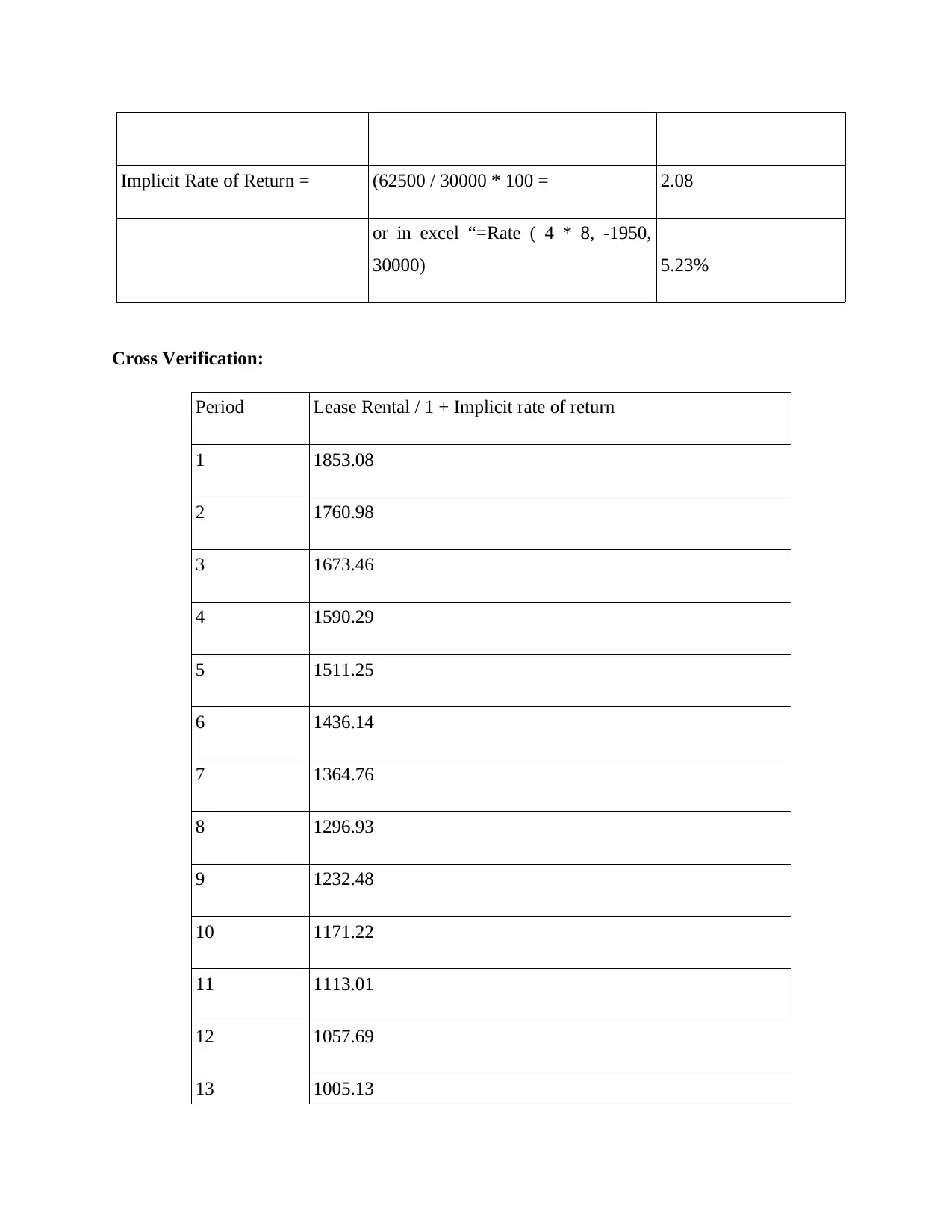

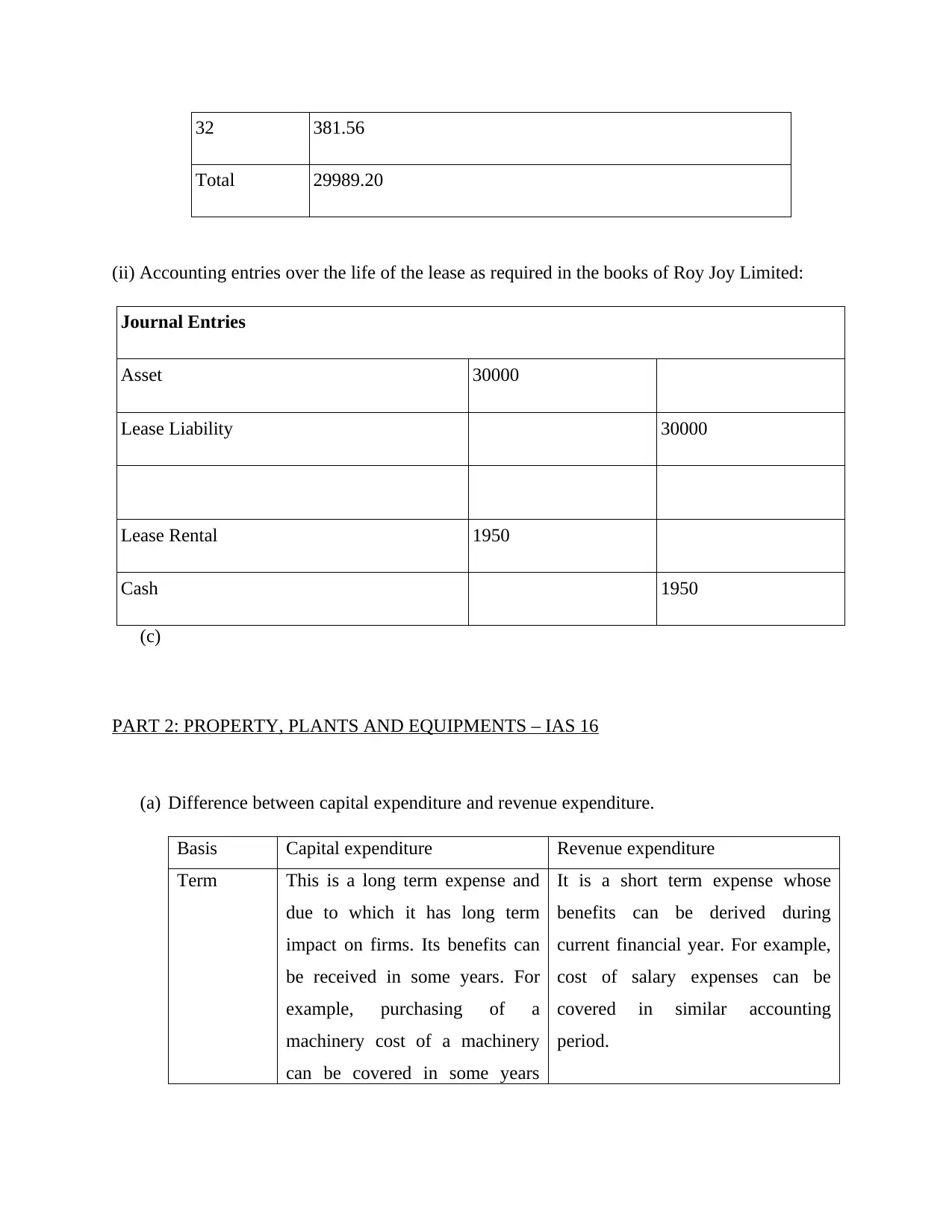

Implicit Rate of Return = (62500 / 30000 * 100 = 2.08

or in excel “=Rate ( 4 * 8, -1950,

30000) 5.23%

Cross Verification:

Period Lease Rental / 1 + Implicit rate of return

1 1853.08

2 1760.98

3 1673.46

4 1590.29

5 1511.25

6 1436.14

7 1364.76

8 1296.93

9 1232.48

10 1171.22

11 1113.01

12 1057.69

13 1005.13

or in excel “=Rate ( 4 * 8, -1950,

30000) 5.23%

Cross Verification:

Period Lease Rental / 1 + Implicit rate of return

1 1853.08

2 1760.98

3 1673.46

4 1590.29

5 1511.25

6 1436.14

7 1364.76

8 1296.93

9 1232.48

10 1171.22

11 1113.01

12 1057.69

13 1005.13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

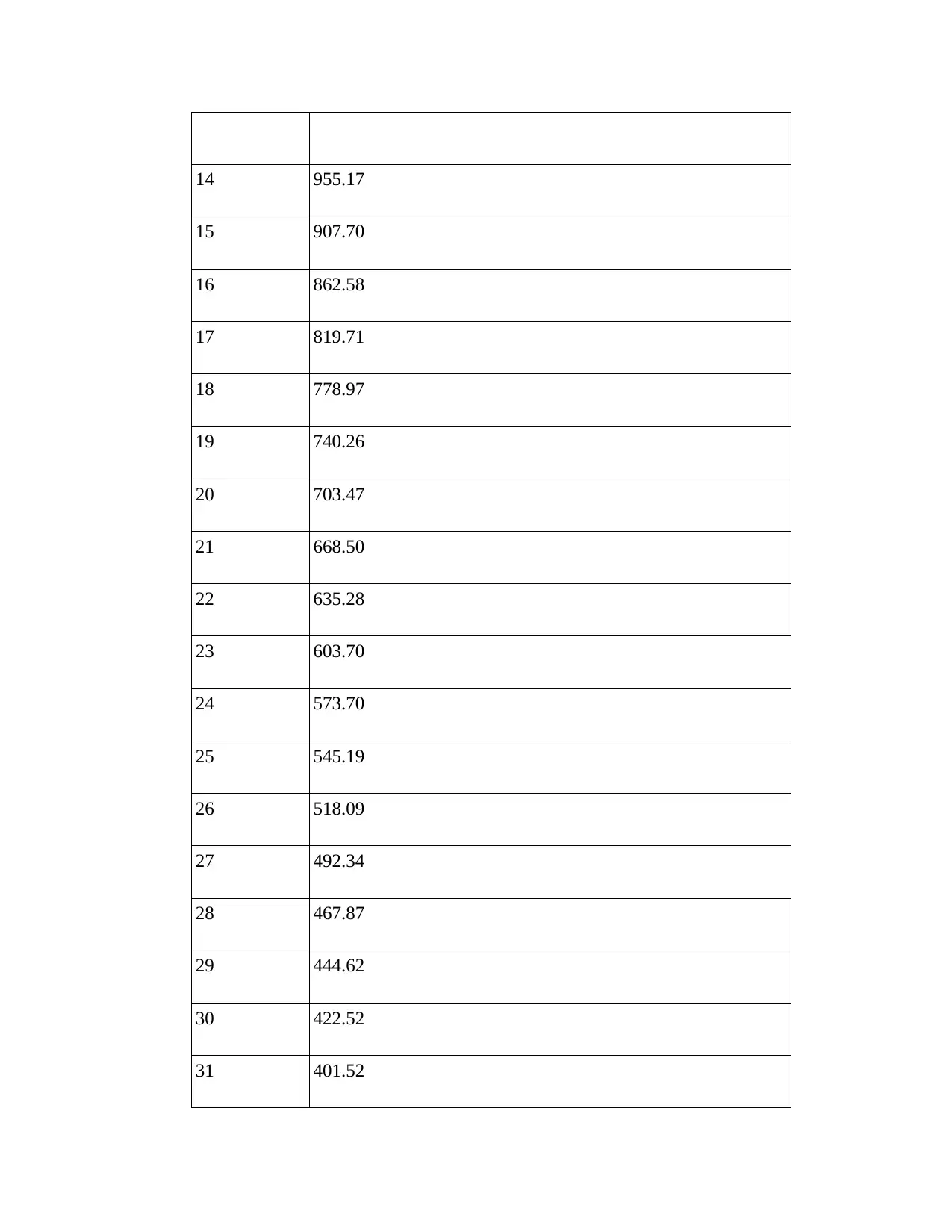

14 955.17

15 907.70

16 862.58

17 819.71

18 778.97

19 740.26

20 703.47

21 668.50

22 635.28

23 603.70

24 573.70

25 545.19

26 518.09

27 492.34

28 467.87

29 444.62

30 422.52

31 401.52

15 907.70

16 862.58

17 819.71

18 778.97

19 740.26

20 703.47

21 668.50

22 635.28

23 603.70

24 573.70

25 545.19

26 518.09

27 492.34

28 467.87

29 444.62

30 422.52

31 401.52

32 381.56

Total 29989.20

(ii) Accounting entries over the life of the lease as required in the books of Roy Joy Limited:

Journal Entries

Asset 30000

Lease Liability 30000

Lease Rental 1950

Cash 1950

(c)

PART 2: PROPERTY, PLANTS AND EQUIPMENTS – IAS 16

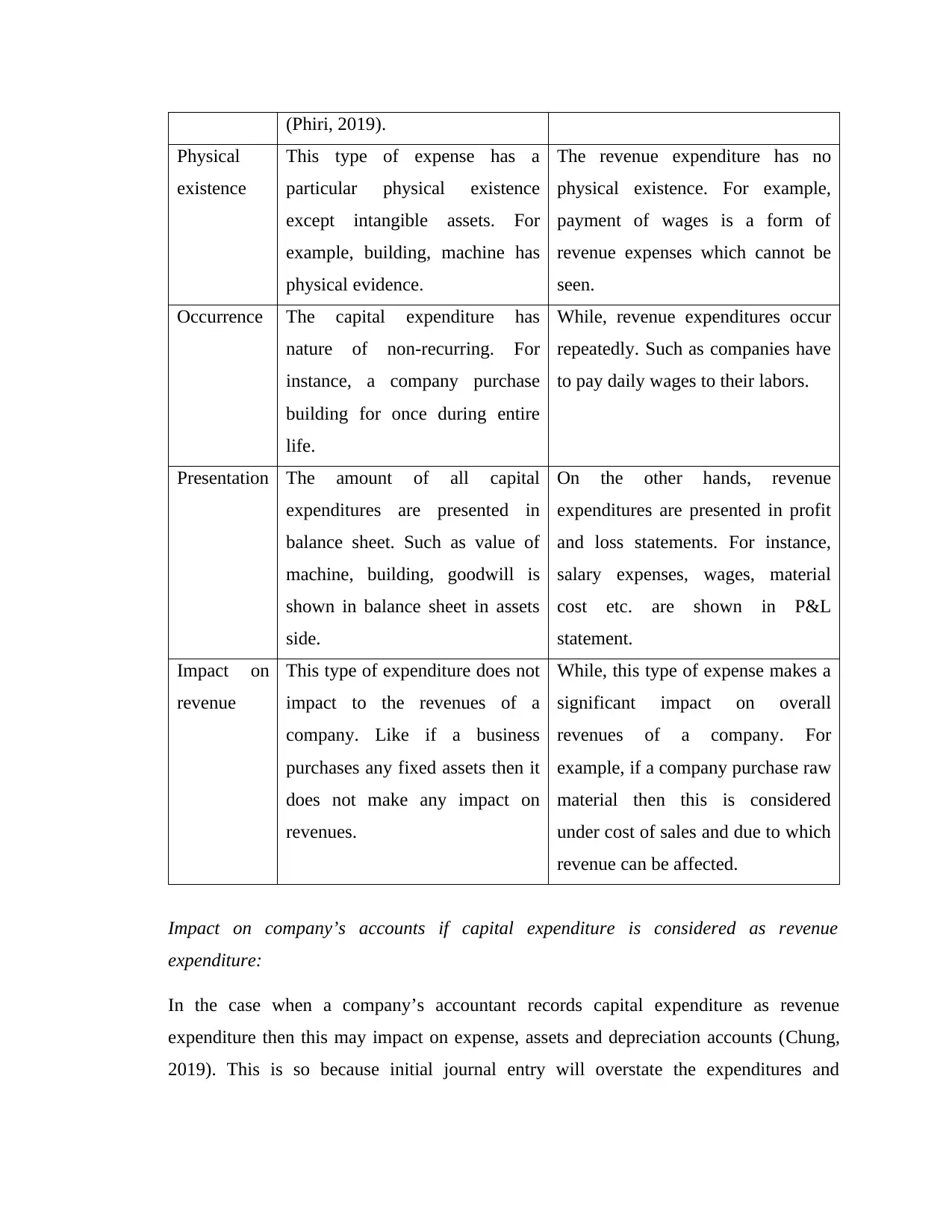

(a) Difference between capital expenditure and revenue expenditure.

Basis Capital expenditure Revenue expenditure

Term This is a long term expense and

due to which it has long term

impact on firms. Its benefits can

be received in some years. For

example, purchasing of a

machinery cost of a machinery

can be covered in some years

It is a short term expense whose

benefits can be derived during

current financial year. For example,

cost of salary expenses can be

covered in similar accounting

period.

Total 29989.20

(ii) Accounting entries over the life of the lease as required in the books of Roy Joy Limited:

Journal Entries

Asset 30000

Lease Liability 30000

Lease Rental 1950

Cash 1950

(c)

PART 2: PROPERTY, PLANTS AND EQUIPMENTS – IAS 16

(a) Difference between capital expenditure and revenue expenditure.

Basis Capital expenditure Revenue expenditure

Term This is a long term expense and

due to which it has long term

impact on firms. Its benefits can

be received in some years. For

example, purchasing of a

machinery cost of a machinery

can be covered in some years

It is a short term expense whose

benefits can be derived during

current financial year. For example,

cost of salary expenses can be

covered in similar accounting

period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Phiri, 2019).

Physical

existence

This type of expense has a

particular physical existence

except intangible assets. For

example, building, machine has

physical evidence.

The revenue expenditure has no

physical existence. For example,

payment of wages is a form of

revenue expenses which cannot be

seen.

Occurrence The capital expenditure has

nature of non-recurring. For

instance, a company purchase

building for once during entire

life.

While, revenue expenditures occur

repeatedly. Such as companies have

to pay daily wages to their labors.

Presentation The amount of all capital

expenditures are presented in

balance sheet. Such as value of

machine, building, goodwill is

shown in balance sheet in assets

side.

On the other hands, revenue

expenditures are presented in profit

and loss statements. For instance,

salary expenses, wages, material

cost etc. are shown in P&L

statement.

Impact on

revenue

This type of expenditure does not

impact to the revenues of a

company. Like if a business

purchases any fixed assets then it

does not make any impact on

revenues.

While, this type of expense makes a

significant impact on overall

revenues of a company. For

example, if a company purchase raw

material then this is considered

under cost of sales and due to which

revenue can be affected.

Impact on company’s accounts if capital expenditure is considered as revenue

expenditure:

In the case when a company’s accountant records capital expenditure as revenue

expenditure then this may impact on expense, assets and depreciation accounts (Chung,

2019). This is so because initial journal entry will overstate the expenditures and

Physical

existence

This type of expense has a

particular physical existence

except intangible assets. For

example, building, machine has

physical evidence.

The revenue expenditure has no

physical existence. For example,

payment of wages is a form of

revenue expenses which cannot be

seen.

Occurrence The capital expenditure has

nature of non-recurring. For

instance, a company purchase

building for once during entire

life.

While, revenue expenditures occur

repeatedly. Such as companies have

to pay daily wages to their labors.

Presentation The amount of all capital

expenditures are presented in

balance sheet. Such as value of

machine, building, goodwill is

shown in balance sheet in assets

side.

On the other hands, revenue

expenditures are presented in profit

and loss statements. For instance,

salary expenses, wages, material

cost etc. are shown in P&L

statement.

Impact on

revenue

This type of expenditure does not

impact to the revenues of a

company. Like if a business

purchases any fixed assets then it

does not make any impact on

revenues.

While, this type of expense makes a

significant impact on overall

revenues of a company. For

example, if a company purchase raw

material then this is considered

under cost of sales and due to which

revenue can be affected.

Impact on company’s accounts if capital expenditure is considered as revenue

expenditure:

In the case when a company’s accountant records capital expenditure as revenue

expenditure then this may impact on expense, assets and depreciation accounts (Chung,

2019). This is so because initial journal entry will overstate the expenditures and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

understate the assets. For instance, if a company makes a capital expense then the journal

entry will be as:

Assets a/c DR

To cash a/c

In the case when capital expense is considered as revenue expense then this will change

the journal entry that will be as:

Expense a/c DR

To cash a/c

Due to this wrong entry, depreciation value will also wrong as well as tax value will also

affected. As a result, company’s income statement, trial balance and balance sheet will be

wrong for all years till business run. This is so because capital expenditure is a huge

expense which is done usually for once in entire business life (Moudud-Ul-Huq, 2019).

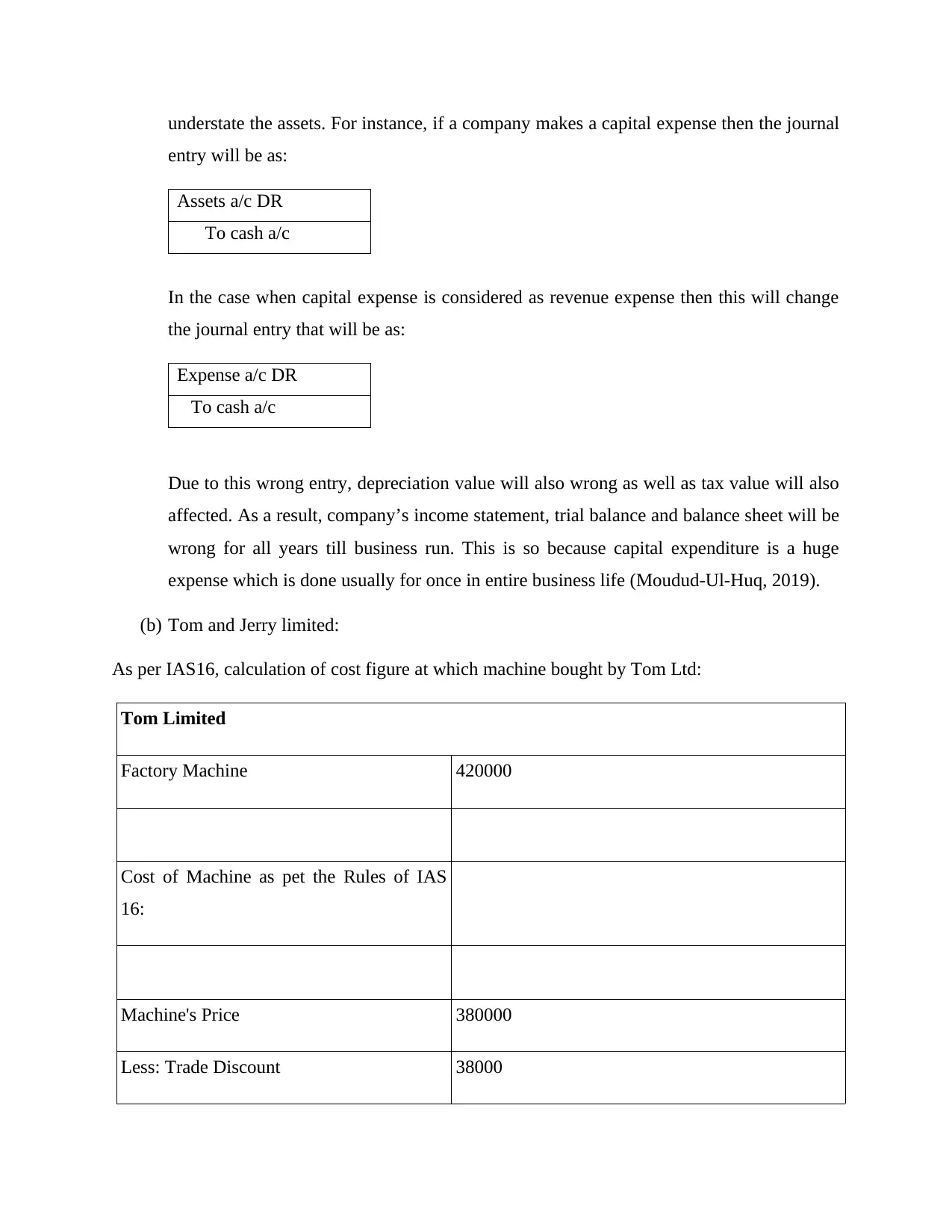

(b) Tom and Jerry limited:

As per IAS16, calculation of cost figure at which machine bought by Tom Ltd:

Tom Limited

Factory Machine 420000

Cost of Machine as pet the Rules of IAS

16:

Machine's Price 380000

Less: Trade Discount 38000

entry will be as:

Assets a/c DR

To cash a/c

In the case when capital expense is considered as revenue expense then this will change

the journal entry that will be as:

Expense a/c DR

To cash a/c

Due to this wrong entry, depreciation value will also wrong as well as tax value will also

affected. As a result, company’s income statement, trial balance and balance sheet will be

wrong for all years till business run. This is so because capital expenditure is a huge

expense which is done usually for once in entire business life (Moudud-Ul-Huq, 2019).

(b) Tom and Jerry limited:

As per IAS16, calculation of cost figure at which machine bought by Tom Ltd:

Tom Limited

Factory Machine 420000

Cost of Machine as pet the Rules of IAS

16:

Machine's Price 380000

Less: Trade Discount 38000

342000

Delivery Charges 6800

Installation Cost 29600

Spare Small Parts 14600

Total cost of Machinery 393000

Note 1: Maintenance annual costs are revenue expenses and not capital expenditure.

Note 2: Here it has been assumed that small spare parts are essential part of machine and will

provide future economic benefits. Thus this expense should be capitalized.

PART 3: INVENTORIES – IAS 2

(a) In accordance with IAS 2, explain how the cost of inventories should be determined.

The main aim of IAS 2 is to provide a way through which all transactions related to

inventories can be recorded in an effective manner (HAZAR, 2020). This provides

gaudiness which are essential to compute value of cost of stock.

Determination of cost of inventories:

In order to measure cost of stock, below mentioned cost need to be consider such as-

Type of cost Examples

Cost of purchase Taxation, transportation charges,

maintenance cost.

Conversion cost Fixed and variable manufacturing cost.

Other cost This includes cost which may occur in

Delivery Charges 6800

Installation Cost 29600

Spare Small Parts 14600

Total cost of Machinery 393000

Note 1: Maintenance annual costs are revenue expenses and not capital expenditure.

Note 2: Here it has been assumed that small spare parts are essential part of machine and will

provide future economic benefits. Thus this expense should be capitalized.

PART 3: INVENTORIES – IAS 2

(a) In accordance with IAS 2, explain how the cost of inventories should be determined.

The main aim of IAS 2 is to provide a way through which all transactions related to

inventories can be recorded in an effective manner (HAZAR, 2020). This provides

gaudiness which are essential to compute value of cost of stock.

Determination of cost of inventories:

In order to measure cost of stock, below mentioned cost need to be consider such as-

Type of cost Examples

Cost of purchase Taxation, transportation charges,

maintenance cost.

Conversion cost Fixed and variable manufacturing cost.

Other cost This includes cost which may occur in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.