HI6025 - IFRS Impact on Public Sector Financial Reporting

VerifiedAdded on 2023/06/12

|15

|713

|207

Report

AI Summary

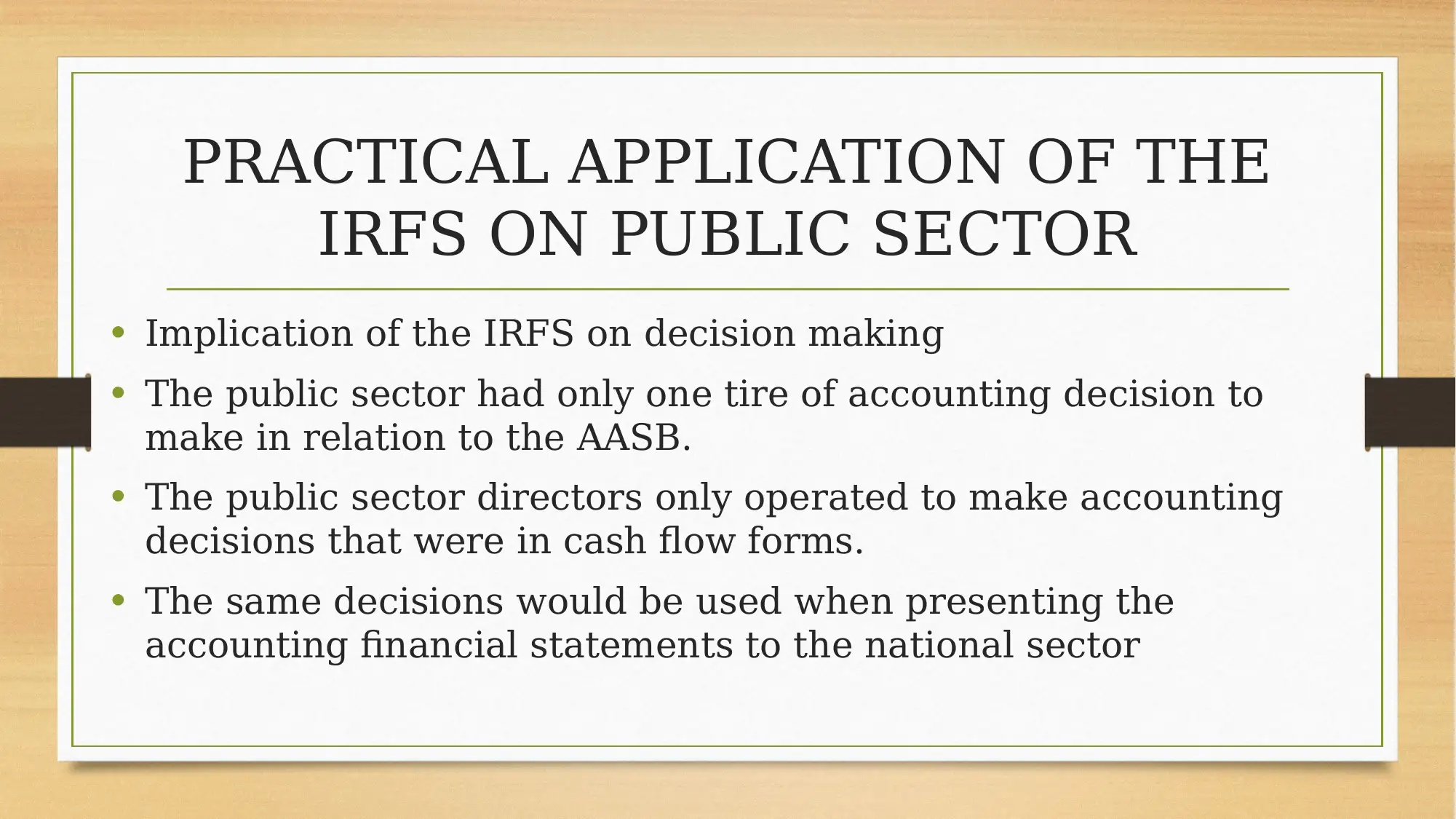

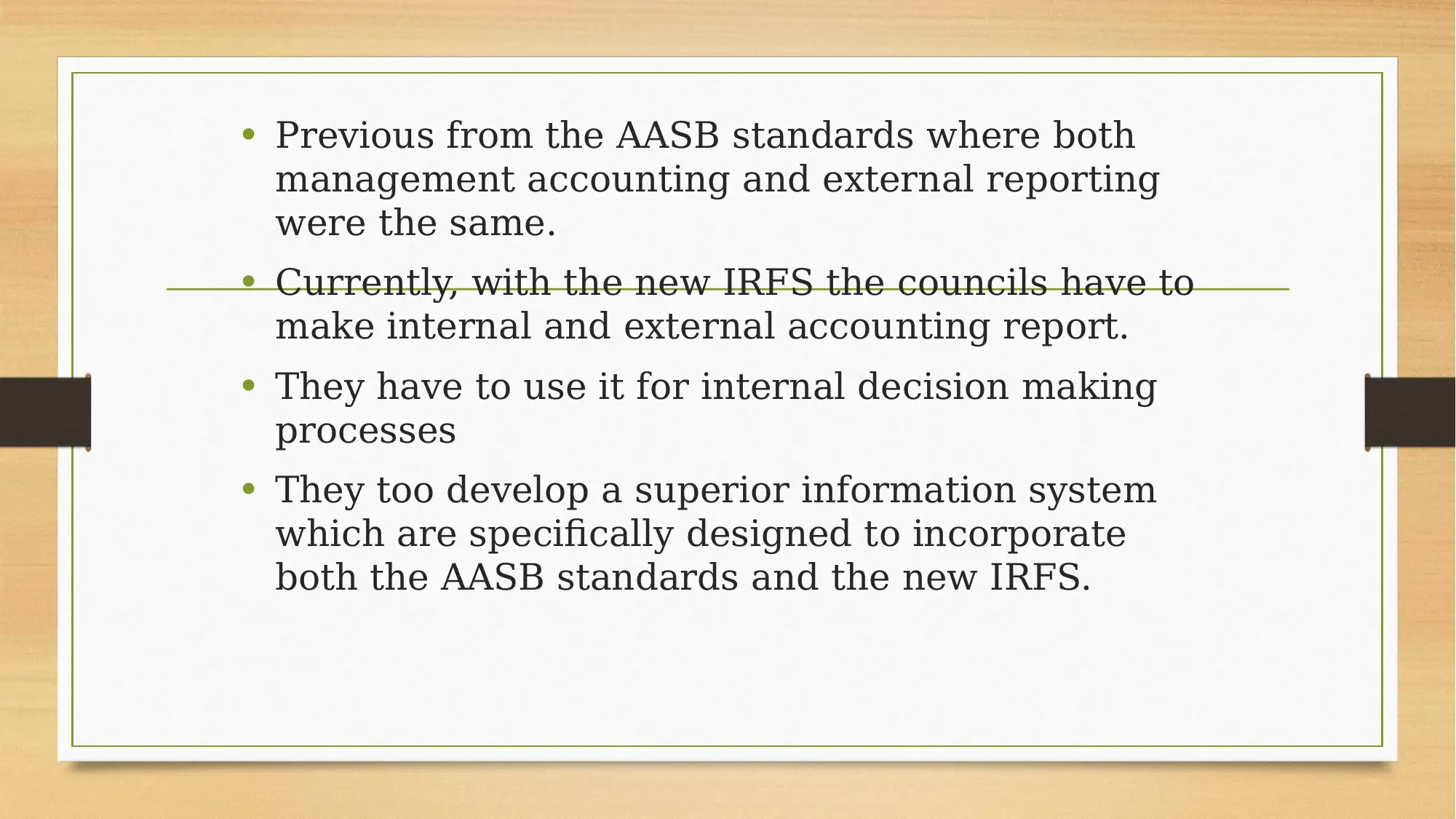

This report examines the impact of International Financial Reporting Standards (IFRS) adoption on the Australian public sector, focusing on a research paper by Kathryn Trewava. It discusses the practical application of IFRS, highlighting its implications on decision-making processes, particularly the shift from a single-tier accounting system to the need for separate internal and external reporting. The report also explores the impact of IFRS on accounting ethical standards, noting improvements in accountability and a reduction in corruption but also acknowledging challenges in asset valuation and resource allocation. Furthermore, it addresses the difficulties faced by rural public sector entities in accessing qualified accounting professionals and the necessary investments in infrastructure and technology for IFRS implementation. The report concludes that while IFRS has enhanced ethical standards and accountability, it has also led to slowed growth due to the time and resources required for compliance.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.