Analysis: International Accounting & IFRS in Australian Local Govts

VerifiedAdded on 2020/02/24

|12

|1870

|494

Report

AI Summary

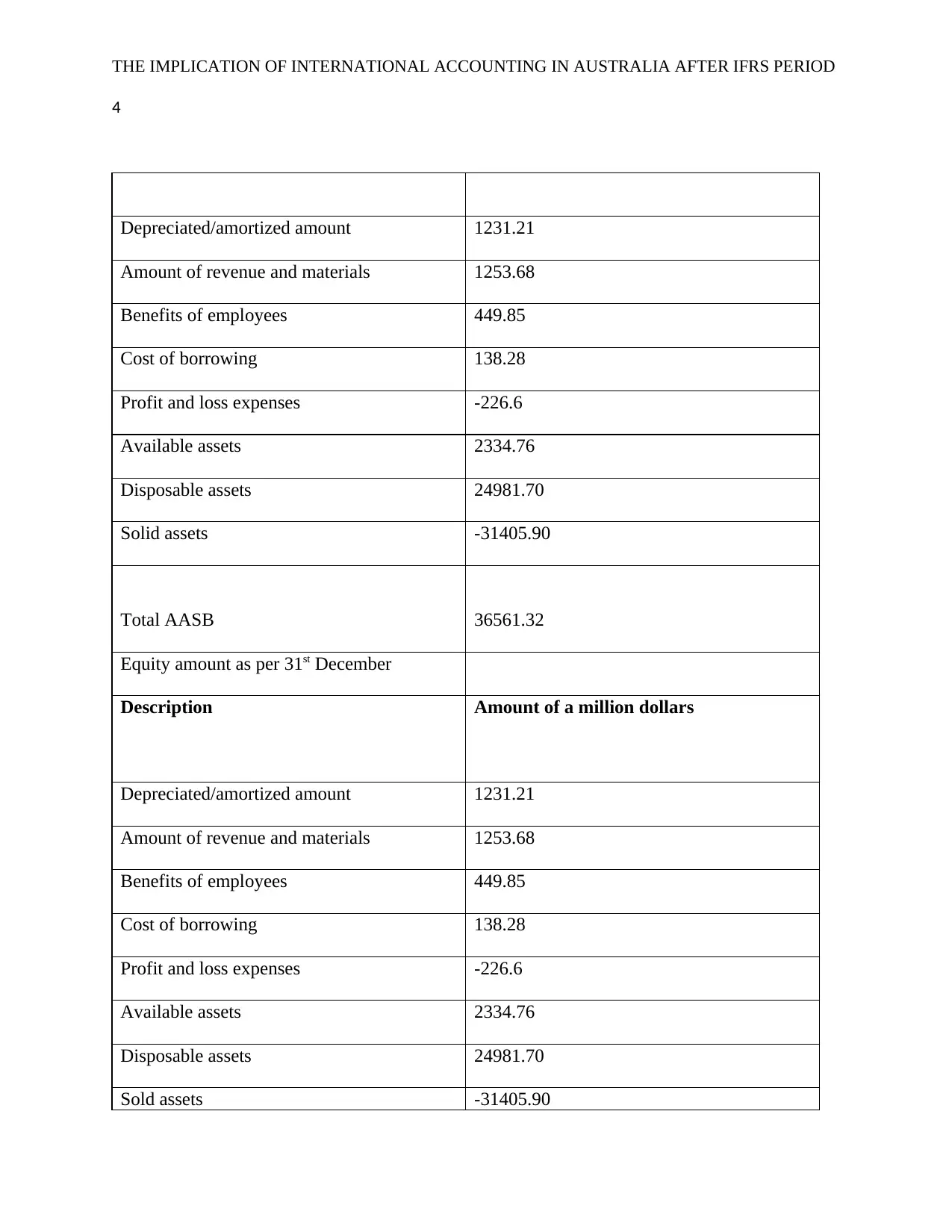

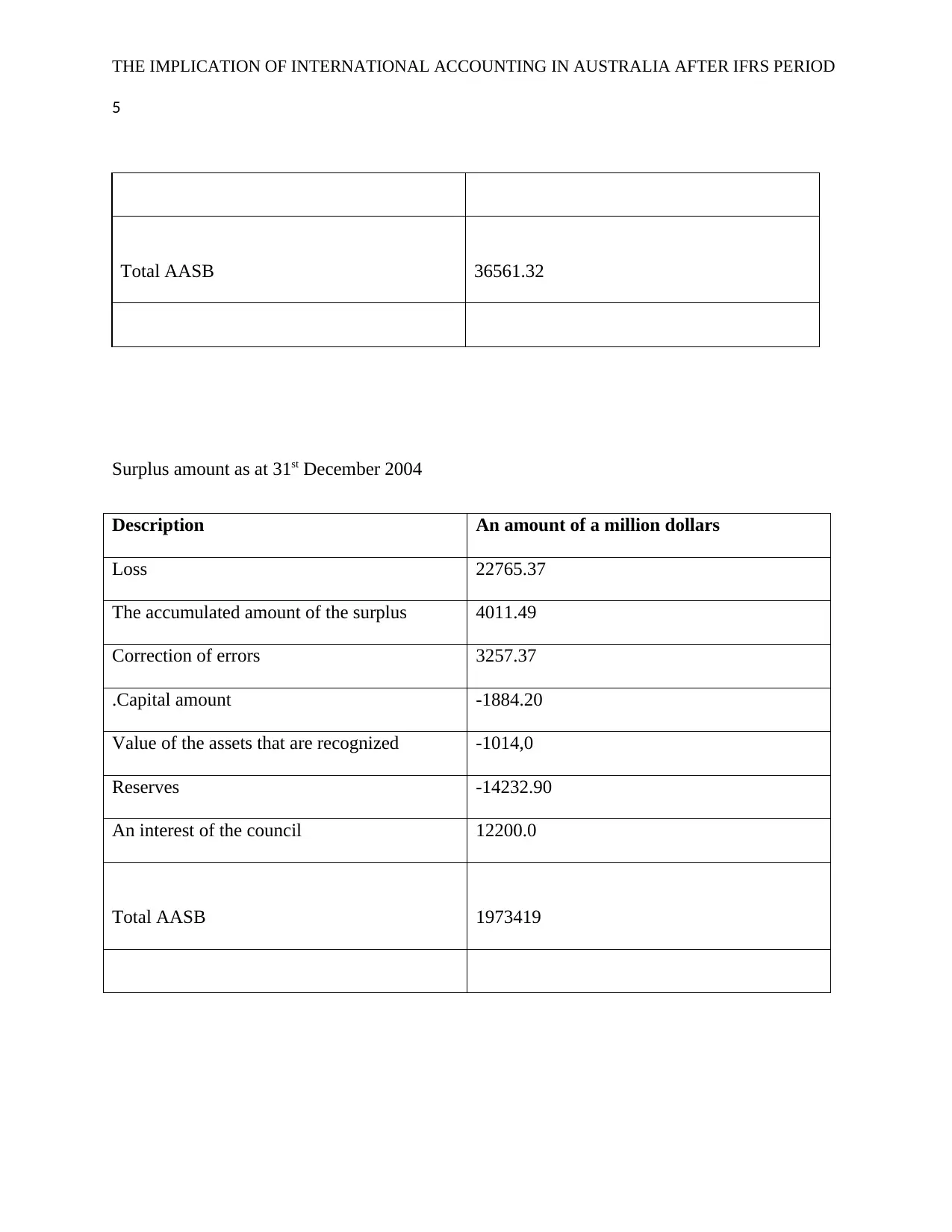

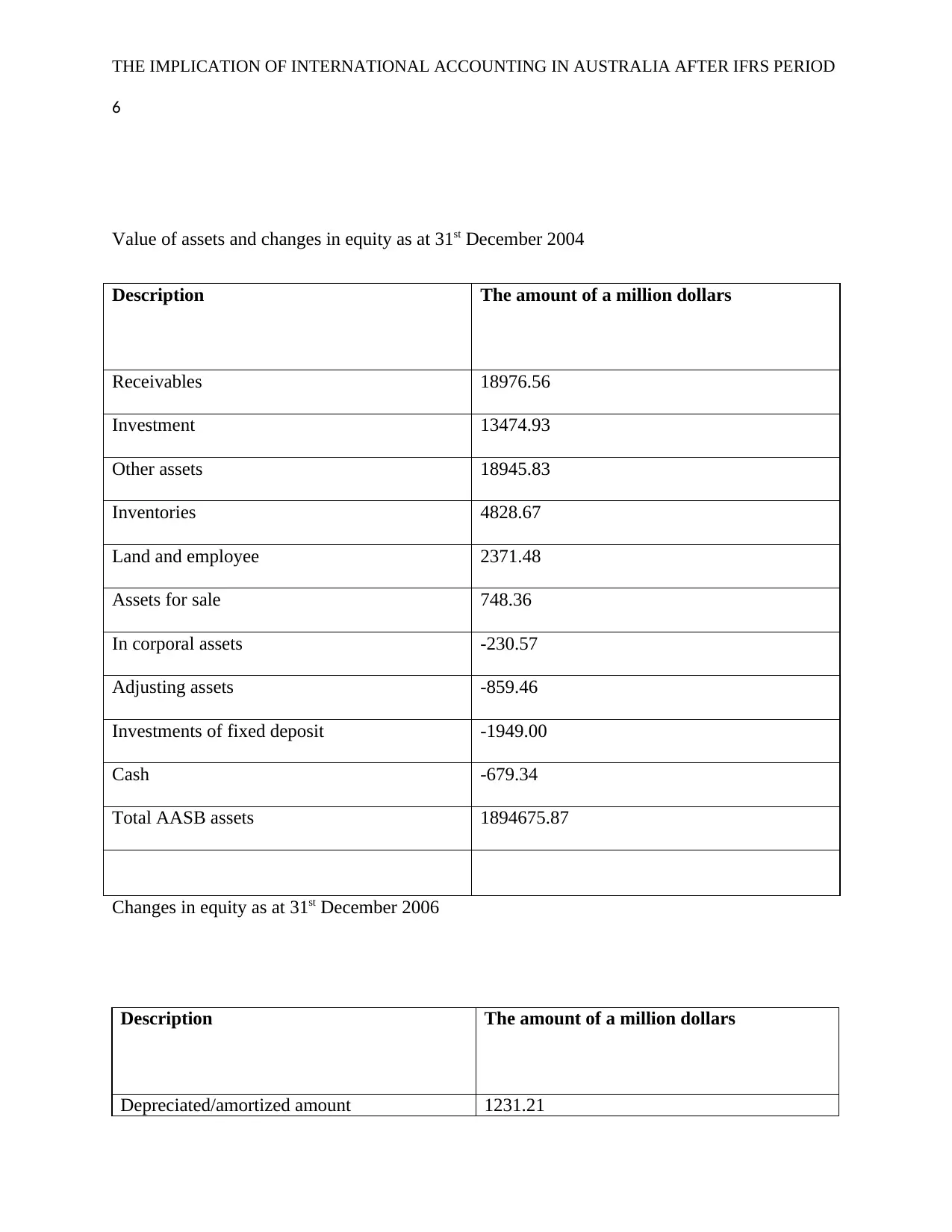

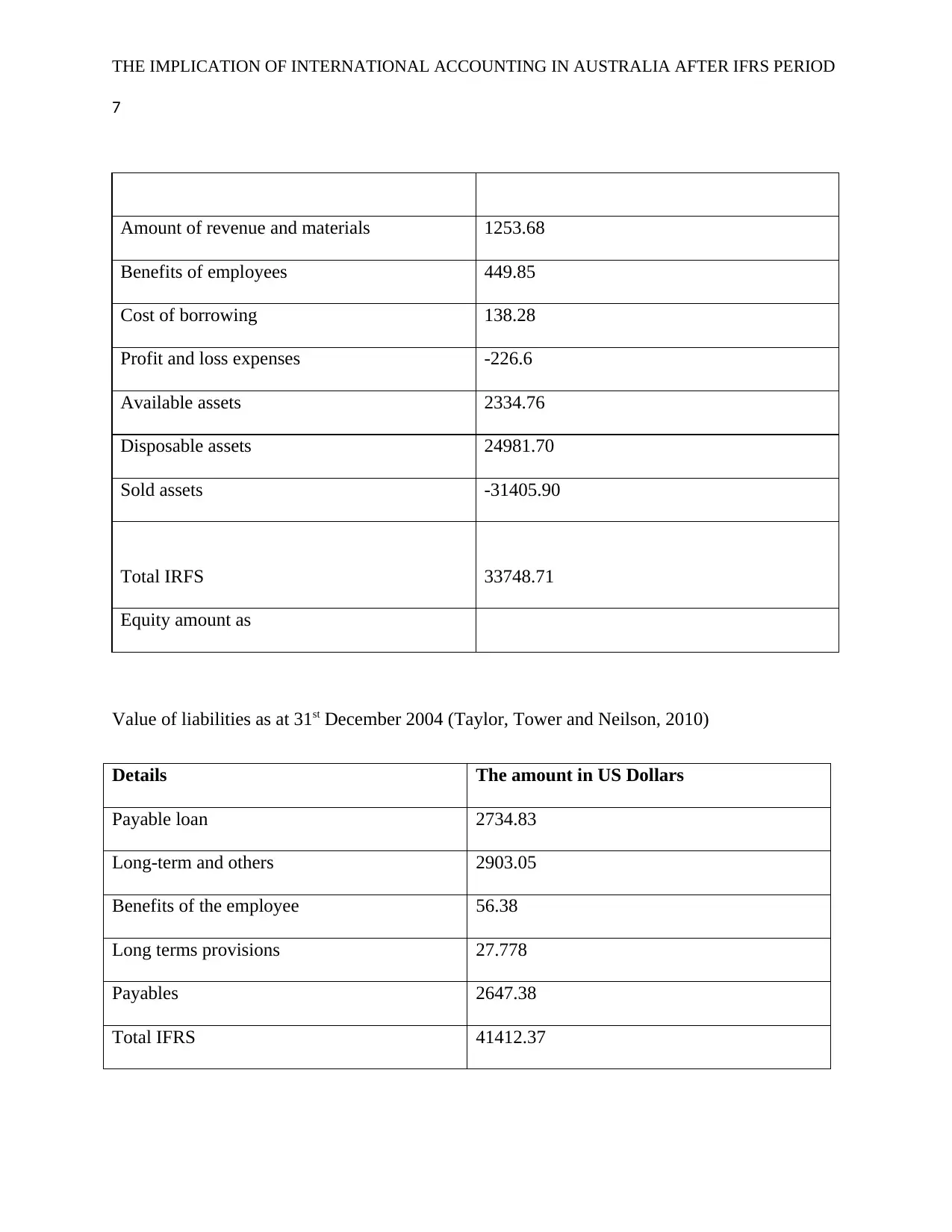

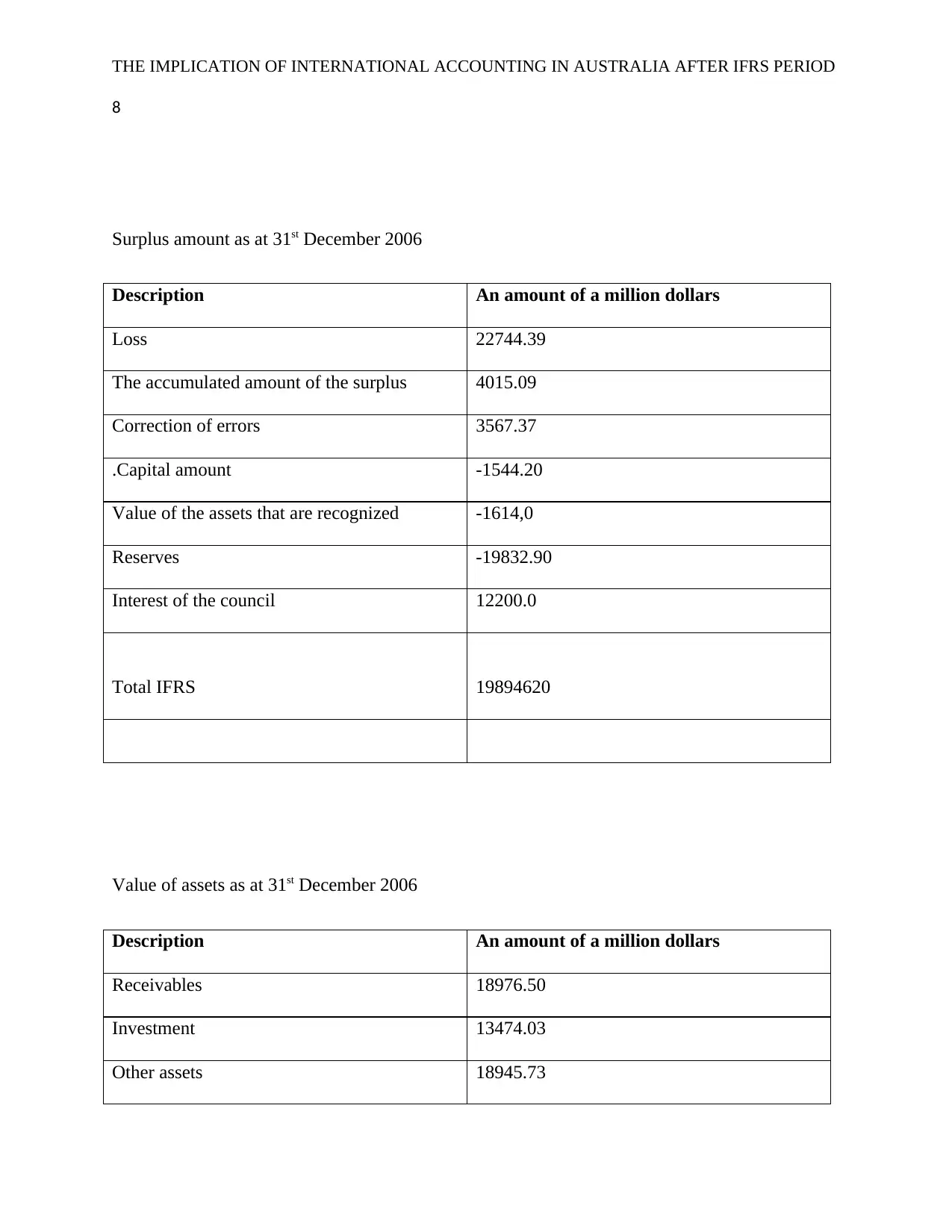

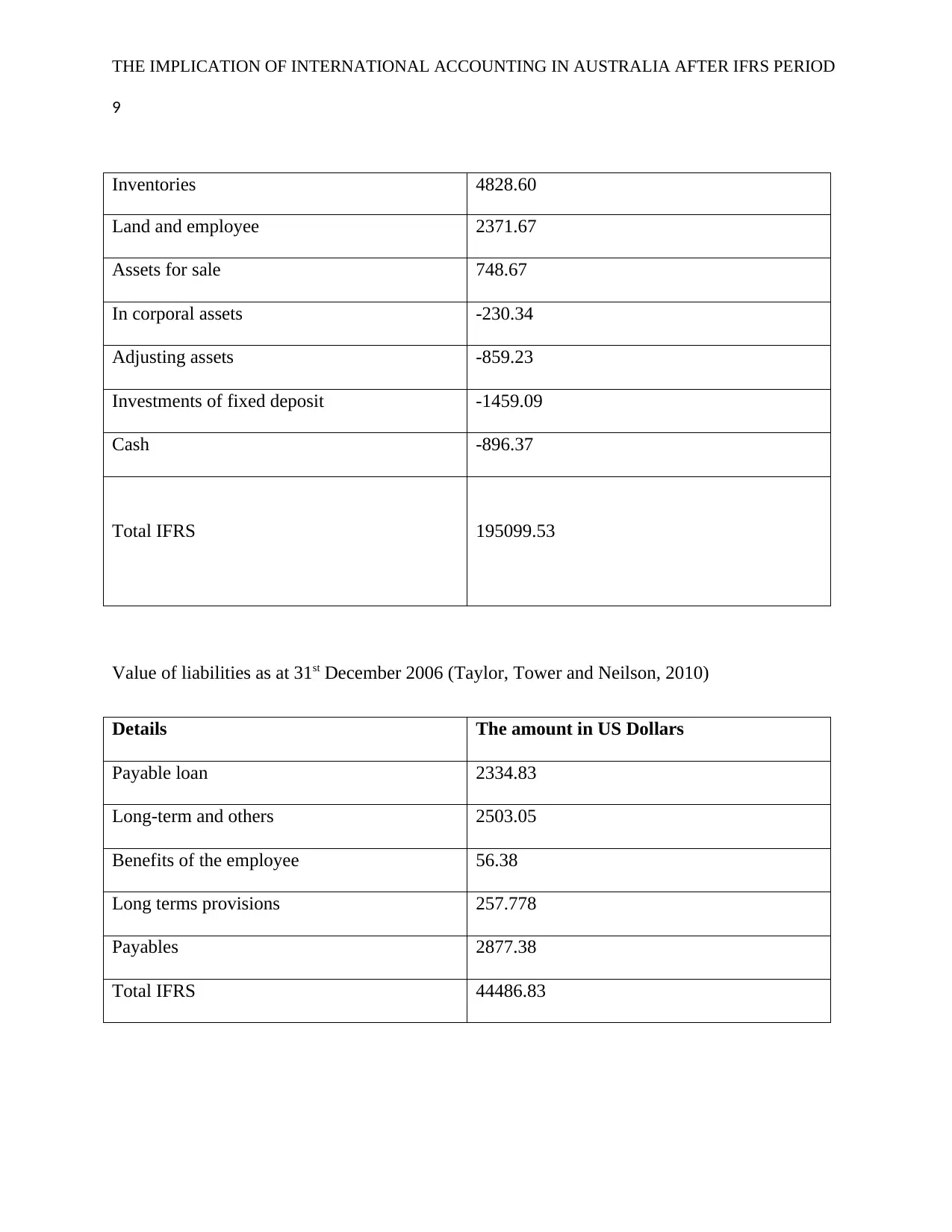

This report analyzes the implications of International Financial Reporting Standards (IFRS) implementation on Australian local government entities. The study examines the changes in accounting policies and financial reporting before and after the adoption of IFRS in 2004, using annual reports from 2004 and 2006. The research focuses on the impact of IFRS on revenue, equity, assets, and liabilities, comparing data prepared under the Australian Accounting Standards Board (AASB) and IFRS. The findings indicate positive effects of IFRS adoption, including increased equity, reduced surplus amounts (representing losses), and growth in assets and liabilities, suggesting improved financial positions for the entities. The report concludes that IFRS has enhanced financial reporting and improved the financial performance of Australian local governments, providing insights for other countries considering IFRS adoption.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.