University Finance Report: IFRS Analysis for Able Plc, 2017, APC311

VerifiedAdded on 2020/06/06

|14

|4227

|241

Report

AI Summary

This report provides a comprehensive analysis of International Financial Reporting Standards (IFRS) and its application. It begins with an introduction to IFRS and its importance in global business, followed by the preparation of an income statement for Able Plc for the year 2017, adhering to IFRS standards. The report then delves into the evaluation of accounting for intangible assets, focusing on International Accounting Standards (IAS) 38, with specific attention to capitalizing development and research costs. Furthermore, it addresses key issues in international financial reporting and the conceptual framework for accounting, including the valuation of inventories as per IAS 2. The report concludes with a summary of the findings and recommendations for financial reporting practices.

International

Financial Report

Financial Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Q1 Prepare Income statement of Able Plc for the year 2017 and explain International

Financial Reporting Standards....................................................................................................1

Q2. Evaluating accounting for intangible assets as per the International Accounting Standards

.....................................................................................................................................................3

Conclusion:.................................................................................................................................6

Q3 Inventories should be valued at “Lower of cost and net realisable value”? Explain?..........6

Conclusion: ................................................................................................................................8

CONCLUSION...........................................................................................................................8

REFERENCES..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

Q1 Prepare Income statement of Able Plc for the year 2017 and explain International

Financial Reporting Standards....................................................................................................1

Q2. Evaluating accounting for intangible assets as per the International Accounting Standards

.....................................................................................................................................................3

Conclusion:.................................................................................................................................6

Q3 Inventories should be valued at “Lower of cost and net realisable value”? Explain?..........6

Conclusion: ................................................................................................................................8

CONCLUSION...........................................................................................................................8

REFERENCES..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

International Financial reporting is usually known as IFRS and these standards are issued

by IFRS foundation and IASB which is International accounting standards board. It makes easy

for company and organizations by giving common language which is globally understood for

business affairs. The main motive of IFRS is that company accounts are being understandable

and comparable across the international and national boundaries. The present report is all about

IFRS and its application. The income statement on the basis of IFRS standard has been drawn

with some specific adjustments. In the next part there is critical understanding of international

accounting standards as per the module APC311. Accounting for intangible assets on the specific

area of capitalizing development and research costs has been explained in this report with the

proper application based example. Further, reports also depicts current key issues present in

international financial reporting and the conceptual framework for accounting. As per the IAS 2

inventories should be valued at lower cost and net realisable value has been justified in this.

Q1 Prepare Income statement of Able Plc for the year 2017 and explain International Financial

Reporting Standards

International Financial Reporting standards can be referred as a set of accounting

standards which are developed by not for profit and independent organisations. The main

objective of IFRS is to give a basic global framework that how organisations should prepare

financial statements and disclose them. It gives guidance or directions about preparing financial

statements instead of setting rules for specific industry reporting. International standards plays

vital role in big companies, multinational companies who have their subsidiaries in different

countries. If single set of worldwide standards will be adopted then it will simplify the

procedures of accounting by giving permission to a company for using throughout one reporting

language. And this single standard will give cohesive views of funds to investors and auditors.

The financial performance of an organization is been represented as statement of comprehensive

income whose sub parts can be statement of profit and loss and statement of comprehensive

income. It includes the elements as per IFRS standard such as revenue and expenses. While the

accounting period where inflows and enhancements of assets raise the economic benefit. Equity

is been raised if liabilities are decreased. Contributions made by equity are not included in

revenues such as partners, shareholders and owners. In the accounting period in the outflow s or

the depletions of assets decreases the economic benefit and more liabilities gives the result of

1

International Financial reporting is usually known as IFRS and these standards are issued

by IFRS foundation and IASB which is International accounting standards board. It makes easy

for company and organizations by giving common language which is globally understood for

business affairs. The main motive of IFRS is that company accounts are being understandable

and comparable across the international and national boundaries. The present report is all about

IFRS and its application. The income statement on the basis of IFRS standard has been drawn

with some specific adjustments. In the next part there is critical understanding of international

accounting standards as per the module APC311. Accounting for intangible assets on the specific

area of capitalizing development and research costs has been explained in this report with the

proper application based example. Further, reports also depicts current key issues present in

international financial reporting and the conceptual framework for accounting. As per the IAS 2

inventories should be valued at lower cost and net realisable value has been justified in this.

Q1 Prepare Income statement of Able Plc for the year 2017 and explain International Financial

Reporting Standards

International Financial Reporting standards can be referred as a set of accounting

standards which are developed by not for profit and independent organisations. The main

objective of IFRS is to give a basic global framework that how organisations should prepare

financial statements and disclose them. It gives guidance or directions about preparing financial

statements instead of setting rules for specific industry reporting. International standards plays

vital role in big companies, multinational companies who have their subsidiaries in different

countries. If single set of worldwide standards will be adopted then it will simplify the

procedures of accounting by giving permission to a company for using throughout one reporting

language. And this single standard will give cohesive views of funds to investors and auditors.

The financial performance of an organization is been represented as statement of comprehensive

income whose sub parts can be statement of profit and loss and statement of comprehensive

income. It includes the elements as per IFRS standard such as revenue and expenses. While the

accounting period where inflows and enhancements of assets raise the economic benefit. Equity

is been raised if liabilities are decreased. Contributions made by equity are not included in

revenues such as partners, shareholders and owners. In the accounting period in the outflow s or

the depletions of assets decreases the economic benefit and more liabilities gives the result of

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

equity decrement. Distributions are not been included in the equity participants. Some

circumstances related to comprehensive income can be: Number of assets and liabilities are

remeasured. The financial asset's fair value may increase or decrease which can be modified as

available for sale. Revaluation of intangible assets, property, plant may increase or decrease.

There is the requirement of faithful and fair representations for the effects of transactions

and all other events and the conditions which are according with recognised criteria for

liabilities, assets, income and expenses which are set in the framework. IFRS has generally

forbidden offsetting. As the standards require offsetting whenever some specific conditions are

satisfied. It requires the entity for comparative information in context of preceding year for all

amount which is mentioned in current year's financial statements. This comparative information

also provides descriptive and narrative information which is related to financial statements of

current year. The additional statement of financial position which is also known as balance sheet

of International accounting standard 1 when any organisation applies for accounting policy or if

it again classifies item of the financial statements. If the important changes in the nature of

organisation's operations or the preview of financial statements, that classifies more

appropriately with regard for choosing and selecting application of accounting policies.

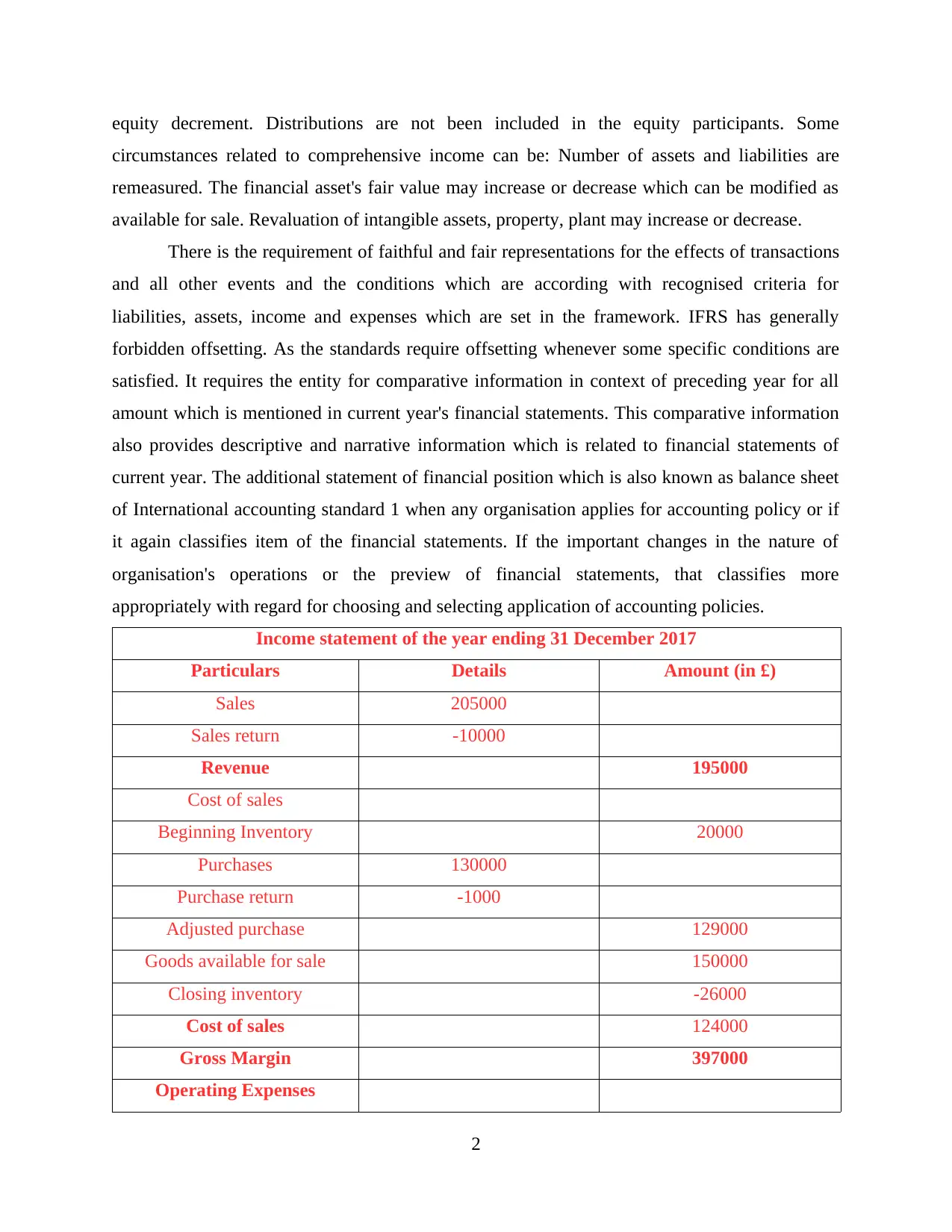

Income statement of the year ending 31 December 2017

Particulars Details Amount (in £)

Sales 205000

Sales return -10000

Revenue 195000

Cost of sales

Beginning Inventory 20000

Purchases 130000

Purchase return -1000

Adjusted purchase 129000

Goods available for sale 150000

Closing inventory -26000

Cost of sales 124000

Gross Margin 397000

Operating Expenses

2

circumstances related to comprehensive income can be: Number of assets and liabilities are

remeasured. The financial asset's fair value may increase or decrease which can be modified as

available for sale. Revaluation of intangible assets, property, plant may increase or decrease.

There is the requirement of faithful and fair representations for the effects of transactions

and all other events and the conditions which are according with recognised criteria for

liabilities, assets, income and expenses which are set in the framework. IFRS has generally

forbidden offsetting. As the standards require offsetting whenever some specific conditions are

satisfied. It requires the entity for comparative information in context of preceding year for all

amount which is mentioned in current year's financial statements. This comparative information

also provides descriptive and narrative information which is related to financial statements of

current year. The additional statement of financial position which is also known as balance sheet

of International accounting standard 1 when any organisation applies for accounting policy or if

it again classifies item of the financial statements. If the important changes in the nature of

organisation's operations or the preview of financial statements, that classifies more

appropriately with regard for choosing and selecting application of accounting policies.

Income statement of the year ending 31 December 2017

Particulars Details Amount (in £)

Sales 205000

Sales return -10000

Revenue 195000

Cost of sales

Beginning Inventory 20000

Purchases 130000

Purchase return -1000

Adjusted purchase 129000

Goods available for sale 150000

Closing inventory -26000

Cost of sales 124000

Gross Margin 397000

Operating Expenses

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

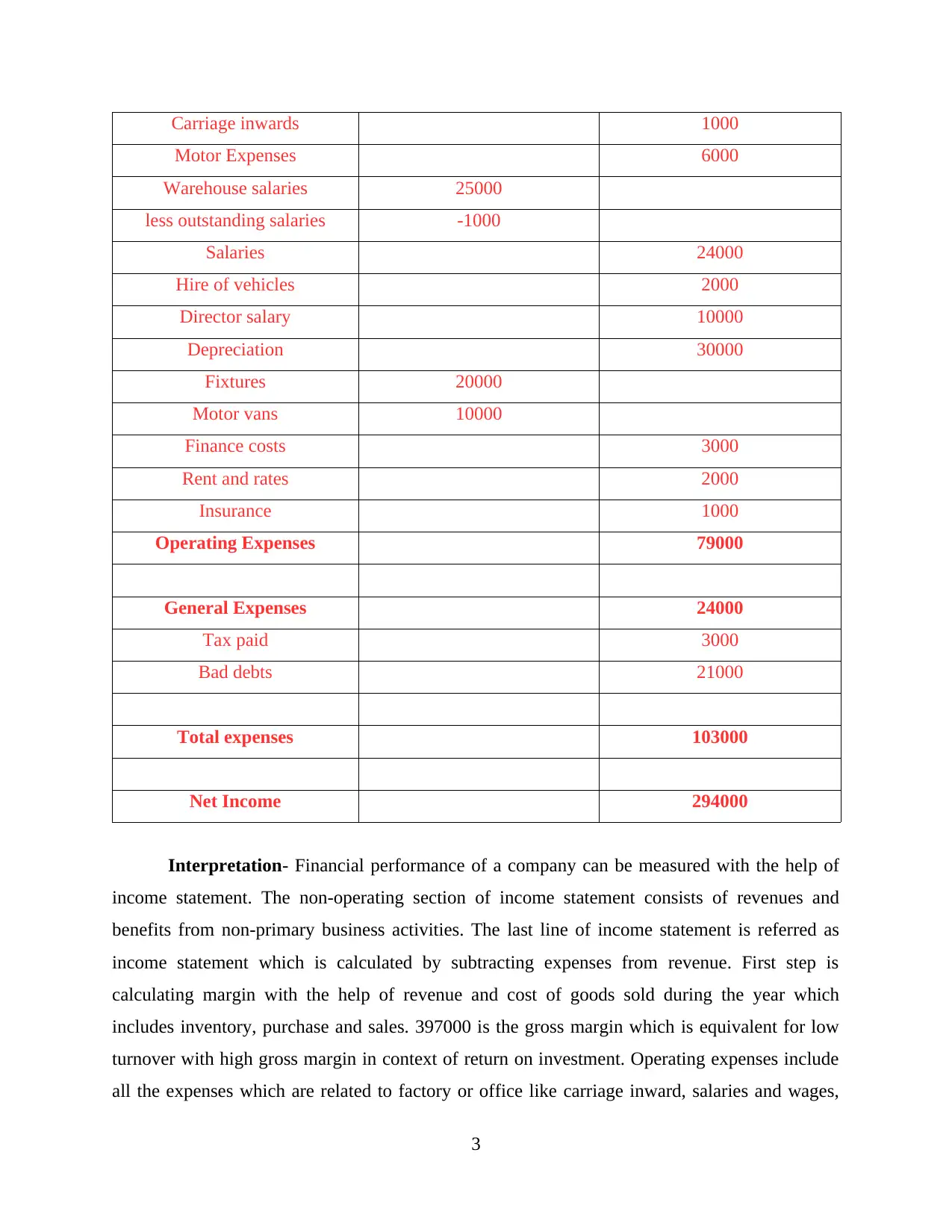

Carriage inwards 1000

Motor Expenses 6000

Warehouse salaries 25000

less outstanding salaries -1000

Salaries 24000

Hire of vehicles 2000

Director salary 10000

Depreciation 30000

Fixtures 20000

Motor vans 10000

Finance costs 3000

Rent and rates 2000

Insurance 1000

Operating Expenses 79000

General Expenses 24000

Tax paid 3000

Bad debts 21000

Total expenses 103000

Net Income 294000

Interpretation- Financial performance of a company can be measured with the help of

income statement. The non-operating section of income statement consists of revenues and

benefits from non-primary business activities. The last line of income statement is referred as

income statement which is calculated by subtracting expenses from revenue. First step is

calculating margin with the help of revenue and cost of goods sold during the year which

includes inventory, purchase and sales. 397000 is the gross margin which is equivalent for low

turnover with high gross margin in context of return on investment. Operating expenses include

all the expenses which are related to factory or office like carriage inward, salaries and wages,

3

Motor Expenses 6000

Warehouse salaries 25000

less outstanding salaries -1000

Salaries 24000

Hire of vehicles 2000

Director salary 10000

Depreciation 30000

Fixtures 20000

Motor vans 10000

Finance costs 3000

Rent and rates 2000

Insurance 1000

Operating Expenses 79000

General Expenses 24000

Tax paid 3000

Bad debts 21000

Total expenses 103000

Net Income 294000

Interpretation- Financial performance of a company can be measured with the help of

income statement. The non-operating section of income statement consists of revenues and

benefits from non-primary business activities. The last line of income statement is referred as

income statement which is calculated by subtracting expenses from revenue. First step is

calculating margin with the help of revenue and cost of goods sold during the year which

includes inventory, purchase and sales. 397000 is the gross margin which is equivalent for low

turnover with high gross margin in context of return on investment. Operating expenses include

all the expenses which are related to factory or office like carriage inward, salaries and wages,

3

etc. which are of 79000 and some general expenses like tax, interest are of 24000 so in this series

total expenses are of 103000 and net income has been calculated from gross margin and total

expenses as 294000. As a recommendation if company should reduce its expenses then it will be

gaining great advantage on the perspective of net income approach.

Q2. Evaluating accounting for intangible assets as per the International Accounting Standards

Valuation for tangible asset is very easy as compared to intangible assets. It is very

complex and different side in nature. In many cases, justified amount is required for the

subjective judgement. Any of the industries or company do not have fixed or standard fixed fee

structure for the valuation of intangibles. Valuation usually depends on client’s size, complexity

and expertise which is basic requirement for the outcome of project which has been expected.

While estimating fees for intangible valuation, major importance has been given to overall scope

of the project's valuation. Expertise knowledge is essentially required and even experts should be

available. As per accounting standards, intangible assets reflect positive impact on audit fees for

big banks because risk measurement is very important for cost of auditing due to risk litigation

which is against the auditor.

For compensating risk, auditor can also include margin in the fees of audit if he estimates

the value incorrectly of intangibles. Any individual or entity may face the risks which are

involved while estimating the value of intangibles. The unique characteristic of intangible assets

refers that there will be event in which some difficulties are considered in determining the value

of intangibles are faced by evaluators. Uncertainty and difficulty will be in the following areas

which are as follows: Identification of all intangible assets, usually this involves all the hurdles

while separating intangible assets or to identify the benefits which are cause by the intangibles

assets. For example if Delia has a strong brand name which has formed unique product, and

profit attribute of company is from the brand name of intangible asset. So in this scenario, this

unique product has given the strong brand name to the company so there is a need for

considering prospects of the product at the time of valuation.

IAS 38 helps in determining the valuation method for intangibles. If on intangible asset is

being valued by different valuation method then it will create many discrepancies and different

results. In this respect, IAS 38 gives the guidance that either select cost model or the revaluation

model. As if the values will be once verified by auditor than it may reduce risk related to

unjustified valuations. Comparison with same intangible assets can be used for sense check but it

4

total expenses are of 103000 and net income has been calculated from gross margin and total

expenses as 294000. As a recommendation if company should reduce its expenses then it will be

gaining great advantage on the perspective of net income approach.

Q2. Evaluating accounting for intangible assets as per the International Accounting Standards

Valuation for tangible asset is very easy as compared to intangible assets. It is very

complex and different side in nature. In many cases, justified amount is required for the

subjective judgement. Any of the industries or company do not have fixed or standard fixed fee

structure for the valuation of intangibles. Valuation usually depends on client’s size, complexity

and expertise which is basic requirement for the outcome of project which has been expected.

While estimating fees for intangible valuation, major importance has been given to overall scope

of the project's valuation. Expertise knowledge is essentially required and even experts should be

available. As per accounting standards, intangible assets reflect positive impact on audit fees for

big banks because risk measurement is very important for cost of auditing due to risk litigation

which is against the auditor.

For compensating risk, auditor can also include margin in the fees of audit if he estimates

the value incorrectly of intangibles. Any individual or entity may face the risks which are

involved while estimating the value of intangibles. The unique characteristic of intangible assets

refers that there will be event in which some difficulties are considered in determining the value

of intangibles are faced by evaluators. Uncertainty and difficulty will be in the following areas

which are as follows: Identification of all intangible assets, usually this involves all the hurdles

while separating intangible assets or to identify the benefits which are cause by the intangibles

assets. For example if Delia has a strong brand name which has formed unique product, and

profit attribute of company is from the brand name of intangible asset. So in this scenario, this

unique product has given the strong brand name to the company so there is a need for

considering prospects of the product at the time of valuation.

IAS 38 helps in determining the valuation method for intangibles. If on intangible asset is

being valued by different valuation method then it will create many discrepancies and different

results. In this respect, IAS 38 gives the guidance that either select cost model or the revaluation

model. As if the values will be once verified by auditor than it may reduce risk related to

unjustified valuations. Comparison with same intangible assets can be used for sense check but it

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is also difficult to find similar intangible assets for comparison. Some key parameters should be

identified for using calculations of valuation method. Whenever the discounted cash flow

method, cash flows, discount rate or time length which should be discounted might be very far

from objective for identification. Estimation will be subjective if cash flows are uncertain. The

rate of inflation and economic condition of the country will give dependency to the value of each

and every cash flow. As this will be increasing the complexity for identifying intangible asset's

fair value. Discount rate will also be affected by the rate of inflation. This is not a single thing

which affects the discount rate, risk free interest rate and premium also influenced by inflation

but major impact will be on discount rate along with valuation.

According to International Accounting Standard 38, lifetime of intangible asset should be

similar to time length for discounting cash flow and IAS 38 has also given method or way to

measure the lifetime. If the discounted present value will be less for the further cash flow then it

will have less impact on the intangible asset's value. If valuation has been performed regularly

then there is risk in fluctuation of the value of intangible assets but some of them requires regular

valuations of some intangible assets. For example: brand name of a multinational company like

Apple and Google might raise because of new and creative product's launch and vice versa due

to bad news like failed in some project of net worth 40 million. Evaluation is required for

intangible assets in every quarter or every half year. Investors and shareholders may not have

complete information for the best decision making.The major risk related to intangible asset's

price is overestimated and even write off might be required. This situation usually happens when

market conditions are changes or because of too optimistic estimate of previous year.

International accounting standard 38 sets the criteria for measurement of intangible assets

and even disclosures are being required (Horton, J, Serafeim, and Serafeim, 2013). It is a non

monetary asset which can be identifiable without physical substance. The assets which can be

separable, sold, licensed, transferred etc. intangible assets can be computer software, patents,

copyright, goodwill, licences and import quotas. Goodwill is in scope of IAS 38 but it is not

considered as identifiable resource. Any expenditure related to intangible asset will be

considered as an expense if the definition has been met of an intangible asset, future economic

benefit can be with asset and cost can be measured reliably. It is difficult to differ maintaining

cost or enhancing the operation of entity or goodwill. Because of these reason brands which are

generated internally, titles has been published, customer lists and alike items are not replicated as

5

identified for using calculations of valuation method. Whenever the discounted cash flow

method, cash flows, discount rate or time length which should be discounted might be very far

from objective for identification. Estimation will be subjective if cash flows are uncertain. The

rate of inflation and economic condition of the country will give dependency to the value of each

and every cash flow. As this will be increasing the complexity for identifying intangible asset's

fair value. Discount rate will also be affected by the rate of inflation. This is not a single thing

which affects the discount rate, risk free interest rate and premium also influenced by inflation

but major impact will be on discount rate along with valuation.

According to International Accounting Standard 38, lifetime of intangible asset should be

similar to time length for discounting cash flow and IAS 38 has also given method or way to

measure the lifetime. If the discounted present value will be less for the further cash flow then it

will have less impact on the intangible asset's value. If valuation has been performed regularly

then there is risk in fluctuation of the value of intangible assets but some of them requires regular

valuations of some intangible assets. For example: brand name of a multinational company like

Apple and Google might raise because of new and creative product's launch and vice versa due

to bad news like failed in some project of net worth 40 million. Evaluation is required for

intangible assets in every quarter or every half year. Investors and shareholders may not have

complete information for the best decision making.The major risk related to intangible asset's

price is overestimated and even write off might be required. This situation usually happens when

market conditions are changes or because of too optimistic estimate of previous year.

International accounting standard 38 sets the criteria for measurement of intangible assets

and even disclosures are being required (Horton, J, Serafeim, and Serafeim, 2013). It is a non

monetary asset which can be identifiable without physical substance. The assets which can be

separable, sold, licensed, transferred etc. intangible assets can be computer software, patents,

copyright, goodwill, licences and import quotas. Goodwill is in scope of IAS 38 but it is not

considered as identifiable resource. Any expenditure related to intangible asset will be

considered as an expense if the definition has been met of an intangible asset, future economic

benefit can be with asset and cost can be measured reliably. It is difficult to differ maintaining

cost or enhancing the operation of entity or goodwill. Because of these reason brands which are

generated internally, titles has been published, customer lists and alike items are not replicated as

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

intangible assets. The cost of internally generated intangible assets can be classified as into

development phase or research phase(Ganysa, 2017). Expenditure on research has been

considered as expense and expenditure on development which is able to meet specified criteria is

replicated as cost to an intangible asset. These are measured primarily at any cost and the

company measures the cost less accumulated amortisation of intangible asset. It also measures

the fair value of asset and fair value can be recognised by reference to active market. Any

intangible asset whose life is finite and is amortised and I context of impairment testing(Ahmed,

Neel and Wang, 2013). Asset which does not amortised has indefinite useful life but for

impairment it is tested annually and if any intangible asset has been disposed then profit, loss is

considered as gain or loss on disposal.

For example –A research and development project was developed as a new production

process by Jack and Jones Ltd on 1 January 2016. The last phase of research was on 30 April

2016 and a cost of 500 was incurred. On 1 May 2016 development phase was started which

incurred total expenditure of 2000 up to 31 December 2016 and 1500 was on 1 December 2016

and rest occurred between 1 December 2016 and 31 December 2016. The director of jack and

Jones ltd mentioned that on 1 December there production process met criteria for intangible

asset. In 2017, more expenditure incurred of 4000 and project was over successfully. In the year

end the amount to be recovered with new production process is been estimated of 3800. Explain

accounting for Year ended 31 December 2016.

31 December 2016, 500 was research expense up to 30 April 2016 and 1500 as Development

expenditure from 1 may 2016 to 1 December 2016 and it will be mentioned as expense in profit

and loss statement. If the capitalization criteria is been met on 1 December 2016 the development

cost of 500 from 1 December 2016 to 31 December 2016 will be capitalize on the basis of

intangible asset as per the year ended 31 December 2016.

Conclusion:

So from the above discussion, there will be possibilities where many difficulties will be

considered for determining intangible's value which are faced by the evaluators is a most

different characteristic of intangible assets. IAS 38 gives proper clarification about valuation

methods for intangibles. If any intangible is valued by other method then there will be many

discrepancies and unique results as IAS 38 provides proper guidance for selecting cost or

revaluation model so lifetime of asset should be similar to discounting cash flows time length.

6

development phase or research phase(Ganysa, 2017). Expenditure on research has been

considered as expense and expenditure on development which is able to meet specified criteria is

replicated as cost to an intangible asset. These are measured primarily at any cost and the

company measures the cost less accumulated amortisation of intangible asset. It also measures

the fair value of asset and fair value can be recognised by reference to active market. Any

intangible asset whose life is finite and is amortised and I context of impairment testing(Ahmed,

Neel and Wang, 2013). Asset which does not amortised has indefinite useful life but for

impairment it is tested annually and if any intangible asset has been disposed then profit, loss is

considered as gain or loss on disposal.

For example –A research and development project was developed as a new production

process by Jack and Jones Ltd on 1 January 2016. The last phase of research was on 30 April

2016 and a cost of 500 was incurred. On 1 May 2016 development phase was started which

incurred total expenditure of 2000 up to 31 December 2016 and 1500 was on 1 December 2016

and rest occurred between 1 December 2016 and 31 December 2016. The director of jack and

Jones ltd mentioned that on 1 December there production process met criteria for intangible

asset. In 2017, more expenditure incurred of 4000 and project was over successfully. In the year

end the amount to be recovered with new production process is been estimated of 3800. Explain

accounting for Year ended 31 December 2016.

31 December 2016, 500 was research expense up to 30 April 2016 and 1500 as Development

expenditure from 1 may 2016 to 1 December 2016 and it will be mentioned as expense in profit

and loss statement. If the capitalization criteria is been met on 1 December 2016 the development

cost of 500 from 1 December 2016 to 31 December 2016 will be capitalize on the basis of

intangible asset as per the year ended 31 December 2016.

Conclusion:

So from the above discussion, there will be possibilities where many difficulties will be

considered for determining intangible's value which are faced by the evaluators is a most

different characteristic of intangible assets. IAS 38 gives proper clarification about valuation

methods for intangibles. If any intangible is valued by other method then there will be many

discrepancies and unique results as IAS 38 provides proper guidance for selecting cost or

revaluation model so lifetime of asset should be similar to discounting cash flows time length.

6

Q3 Inventories should be valued at “Lower of cost and net realisable value”? Explain?

As per IAS 2 inventories should be valued as lower of cost and net realizable value. IAS

2 gives direction to identify cost of the inventories and the recognition of the cost which can be

referred as expense. The cost formulas which are used for assigning costs to all inventories.

Inventories are measure at the lower of cost and net realisable value(Oliveira, Rodrigues and

Craig, 2010). Cost formulas refers to cost of inventories of items that cannot be ordinarily

exchangeable and the services and goods which are produced and differentiated for some

specific projects shall be allocated by referring specific identification of their individual costs.

This identification of cost signifies particular cost which has been attributed items of the

inventory which is identified. For example, the operating segment uses the specific inventories

can be also used by different operating segment of the entity. So difference in location of

inventories are not sufficient for proper justification of uses of the different cost formula. If the

inventories are damaged then there cost may not be recoverable whether they have become

partially or wholly obsolete even the selling prices also declined. If the estimated costs of

completion and incurred cost for increasing sales (Kieso, Weygandt and Warfield, 2010.) . For

reducing inventories below the cost to net realisable value is as accurate with view that in excess

amount assets should not be carried.

Inventories are usually reduced from the net realisable value. In some cases it might be

appropriate to related or similar items. If inventories related to similar use, product line, purpose

are traded or marketed in same geographical area which cannot be evaluated in different ways

practically. On the basis of classification of inventories they cannot be write off for example, in a

particular operating segment's inventories and finished goods. Net realisable value are the most

reliable indication which is available when the estimates are prepared and fluctuations of price or

cost which is directly related to events who occurs after end of the period so that events give

confirmation for the conditions which exists at the end period. It also considers the purpose for

the inventory which is help. For example, the inventory's net realisable value for satisfying the

firm service or sales contract which is purely based on price of contract. If the inventory

quantities which are held more than sales contract then net realisable value which is excess is

based on selling prices. The cost of inventories usually includes all cost of conversion like direct

labour and production overhead, cost of purchase and other cost which has been occurred for

bringing all inventories to present condition and location. So the cost of inventories are assigned

7

As per IAS 2 inventories should be valued as lower of cost and net realizable value. IAS

2 gives direction to identify cost of the inventories and the recognition of the cost which can be

referred as expense. The cost formulas which are used for assigning costs to all inventories.

Inventories are measure at the lower of cost and net realisable value(Oliveira, Rodrigues and

Craig, 2010). Cost formulas refers to cost of inventories of items that cannot be ordinarily

exchangeable and the services and goods which are produced and differentiated for some

specific projects shall be allocated by referring specific identification of their individual costs.

This identification of cost signifies particular cost which has been attributed items of the

inventory which is identified. For example, the operating segment uses the specific inventories

can be also used by different operating segment of the entity. So difference in location of

inventories are not sufficient for proper justification of uses of the different cost formula. If the

inventories are damaged then there cost may not be recoverable whether they have become

partially or wholly obsolete even the selling prices also declined. If the estimated costs of

completion and incurred cost for increasing sales (Kieso, Weygandt and Warfield, 2010.) . For

reducing inventories below the cost to net realisable value is as accurate with view that in excess

amount assets should not be carried.

Inventories are usually reduced from the net realisable value. In some cases it might be

appropriate to related or similar items. If inventories related to similar use, product line, purpose

are traded or marketed in same geographical area which cannot be evaluated in different ways

practically. On the basis of classification of inventories they cannot be write off for example, in a

particular operating segment's inventories and finished goods. Net realisable value are the most

reliable indication which is available when the estimates are prepared and fluctuations of price or

cost which is directly related to events who occurs after end of the period so that events give

confirmation for the conditions which exists at the end period. It also considers the purpose for

the inventory which is help. For example, the inventory's net realisable value for satisfying the

firm service or sales contract which is purely based on price of contract. If the inventory

quantities which are held more than sales contract then net realisable value which is excess is

based on selling prices. The cost of inventories usually includes all cost of conversion like direct

labour and production overhead, cost of purchase and other cost which has been occurred for

bringing all inventories to present condition and location. So the cost of inventories are assigned

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by – FIFO, First in first out or (WACC) weighted average cost of capital formula for all

interchangeable items and specific identification of the items in inventory which are not

exchangeable. The carrying amount has been considered of inventories whenever the inventories

are sold n the expense where related revenue is recognised.

The international accounting standard is refers to the accounting treatment of the

inventories. It determines the cost of inventory and the related expenses, It should be determine

in cost formulas which is used to assign cost of inventory. In IAS2 measurement of inventories

are included cost of purchase net of trade discounts received, cost of conversion and other costs

which is bringing the inventories to their present location. The fundamental principle of IAS 2 is

inventories are required to stated that lower of cost and net realisable value. Inventory cost

should not to include abnormal waste, storage costs and selling costs, Interest cost when

inventories directly arising on the recent acquisition of inventories invoiced in foreign currency

Net realizable value is the net amount of that product or entity which expect to sell in the

market. It is an estimated selling price in the business. To estimates the net realizable value are

based on the most reliable entity available at the time where estimates are made of the amount

the inventory are expected to realize. When an item of inventory is carried at net realizable value

because its selling price has declined, this inventory is still on market in a subsequent period and

its selling price has increased. When the expected ultimate cost of the assets exceeds its net

realizable value, so the expected cost is low in accordance with the requirements of other

standards. Cost of inventory not be recoverable if the inventory is damaged. For example net

realizable value of the quantity of inventory held which is to satisfy the firm sales is abed on the

contract price. If those inventories quantities which is held the sales contracts are for those is less

than.

Conclusion:

In order to ascertaining the required level of inventories in the organization IAS 2 will act

as a funneling component which in turn will be effective and adequate as to analyses the costs of

inventories. It will be based on analyzing the holding costs with consideration EOQ

measurements and the reorder level of firm's inventories. Therefore, the main motive is to

engaged the business on the going purpose which will be assistive in terms of improving the

efficiency of the business. Thus, such information will help the accounting professionals in terms

of analyzing the costs of holding inventories as well as manufacturing expenses. The effective

8

interchangeable items and specific identification of the items in inventory which are not

exchangeable. The carrying amount has been considered of inventories whenever the inventories

are sold n the expense where related revenue is recognised.

The international accounting standard is refers to the accounting treatment of the

inventories. It determines the cost of inventory and the related expenses, It should be determine

in cost formulas which is used to assign cost of inventory. In IAS2 measurement of inventories

are included cost of purchase net of trade discounts received, cost of conversion and other costs

which is bringing the inventories to their present location. The fundamental principle of IAS 2 is

inventories are required to stated that lower of cost and net realisable value. Inventory cost

should not to include abnormal waste, storage costs and selling costs, Interest cost when

inventories directly arising on the recent acquisition of inventories invoiced in foreign currency

Net realizable value is the net amount of that product or entity which expect to sell in the

market. It is an estimated selling price in the business. To estimates the net realizable value are

based on the most reliable entity available at the time where estimates are made of the amount

the inventory are expected to realize. When an item of inventory is carried at net realizable value

because its selling price has declined, this inventory is still on market in a subsequent period and

its selling price has increased. When the expected ultimate cost of the assets exceeds its net

realizable value, so the expected cost is low in accordance with the requirements of other

standards. Cost of inventory not be recoverable if the inventory is damaged. For example net

realizable value of the quantity of inventory held which is to satisfy the firm sales is abed on the

contract price. If those inventories quantities which is held the sales contracts are for those is less

than.

Conclusion:

In order to ascertaining the required level of inventories in the organization IAS 2 will act

as a funneling component which in turn will be effective and adequate as to analyses the costs of

inventories. It will be based on analyzing the holding costs with consideration EOQ

measurements and the reorder level of firm's inventories. Therefore, the main motive is to

engaged the business on the going purpose which will be assistive in terms of improving the

efficiency of the business. Thus, such information will help the accounting professionals in terms

of analyzing the costs of holding inventories as well as manufacturing expenses. The effective

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and accurate decision will make changes in the business policies. Similarly, the impacts of such

guidance will result in effective business efficiency and growth for the longer period. In addition,

it presents the guidance and framework to analyses the various costs such as cost of purchase,

conversion as well as fixed and variable costs. Thus, the main motive of implicating such

techniques into business operations is that it will be helpful in managing the abnormal wastes,

storage costs, selling costs, overhead expenses on selling and administration etc. However, such

control and execution will help in improving the revenue generation of the business as well as

proper control over the costs of businesses.

CONCLUSION

From the above report it can be concluded that international financial reporting standards

are mandatory for all the organizations and especially the organisation who are operating

internationally. The objective of IFRS has been accomplished that company accounts are being

understandable and comparable across the international and national boundaries. Without IFRS

financial position of the company is not known. In this report the issues related to financial

reporting are cleared. Financial information leads to both pros and cons, whether the pros are

affecting market very positively. Decision making is becoming easy for investors and

shareholders because of single set standard. According to IFRS standards income statement has

been provided with the adjustments. It can be summarized from the report that Able Plc should

focus on reducing expenses for gaining more profit and growth. As per IAS 2 Inventories should

be valued at “Lower of cost and net realisable value”, this statement has been explained with the

reference.

9

guidance will result in effective business efficiency and growth for the longer period. In addition,

it presents the guidance and framework to analyses the various costs such as cost of purchase,

conversion as well as fixed and variable costs. Thus, the main motive of implicating such

techniques into business operations is that it will be helpful in managing the abnormal wastes,

storage costs, selling costs, overhead expenses on selling and administration etc. However, such

control and execution will help in improving the revenue generation of the business as well as

proper control over the costs of businesses.

CONCLUSION

From the above report it can be concluded that international financial reporting standards

are mandatory for all the organizations and especially the organisation who are operating

internationally. The objective of IFRS has been accomplished that company accounts are being

understandable and comparable across the international and national boundaries. Without IFRS

financial position of the company is not known. In this report the issues related to financial

reporting are cleared. Financial information leads to both pros and cons, whether the pros are

affecting market very positively. Decision making is becoming easy for investors and

shareholders because of single set standard. According to IFRS standards income statement has

been provided with the adjustments. It can be summarized from the report that Able Plc should

focus on reducing expenses for gaining more profit and growth. As per IAS 2 Inventories should

be valued at “Lower of cost and net realisable value”, this statement has been explained with the

reference.

9

REFERENCES

Books and Journals

Kieso, D. E., Weygandt, J. J. and Warfield, T. D., 2010. Intermediate accounting: IFRS

edition (Vol. 2). John Wiley & Sons.

Ahmed, A. S., Neel, M. and Wang, D., 2013. Does mandatory adoption of IFRS improve

accounting quality? Preliminary evidence. Contemporary Accounting Research. 30(4).

pp.1344-1372.

Horton, J., Serafeim, G. and Serafeim, I., 2013. Does mandatory IFRS adoption improve the

information environment?. Contemporary accounting research. 30(1). pp.388-423.

Christensen, H. B., Hail, L. and Leuz, C., 2013. Mandatory IFRS reporting and changes in

enforcement. Journal of Accounting and Economics. 56(2-3). pp.147-177.

De George, E. T., Ferguson, C. B. and Spear, N. A., 2012. How much does IFRS cost? IFRS

adoption and audit fees. The Accounting Review, 88(2). pp. 429-462.

Hamberg, M., Paananen, M. and Novak, J., 2011. The adoption of IFRS 3: The effects of

managerial discretion and stock market reactions. European Accounting Review. 20(2).

pp.263-288.

Cascino, S. and Gassen, J., 2015. What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies. 20(1). pp.242-282.

Andrić, M., Mijić, K. and Jakšić, D., 2011. Financial reporting and characteristics of impairment

of assets in the republic of Serbia, according to IAS/IFRS and national

regulation. Economic Annals. 56(189). pp.101-116.

Ganysa, D. D., 2017. The Influences Of Company Size, Audit Quality, Audit Tenure, And Audit

Pricing To The Going Concern Audit Opinion (Gcao) (Bachelor's thesis, Jakarta: Fakultas

Ekonomi Dan Bisnis UIN Syarif Hidayatullah.).

Oliveira, L., Rodrigues, L.L. and Craig, R., 2010. Intangible assets and value relevance:

Evidence from the Portuguese stock exchange. The British Accounting Review. 42(4).

pp.241-252.

Online

[Online]. Available through <>

10

Books and Journals

Kieso, D. E., Weygandt, J. J. and Warfield, T. D., 2010. Intermediate accounting: IFRS

edition (Vol. 2). John Wiley & Sons.

Ahmed, A. S., Neel, M. and Wang, D., 2013. Does mandatory adoption of IFRS improve

accounting quality? Preliminary evidence. Contemporary Accounting Research. 30(4).

pp.1344-1372.

Horton, J., Serafeim, G. and Serafeim, I., 2013. Does mandatory IFRS adoption improve the

information environment?. Contemporary accounting research. 30(1). pp.388-423.

Christensen, H. B., Hail, L. and Leuz, C., 2013. Mandatory IFRS reporting and changes in

enforcement. Journal of Accounting and Economics. 56(2-3). pp.147-177.

De George, E. T., Ferguson, C. B. and Spear, N. A., 2012. How much does IFRS cost? IFRS

adoption and audit fees. The Accounting Review, 88(2). pp. 429-462.

Hamberg, M., Paananen, M. and Novak, J., 2011. The adoption of IFRS 3: The effects of

managerial discretion and stock market reactions. European Accounting Review. 20(2).

pp.263-288.

Cascino, S. and Gassen, J., 2015. What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies. 20(1). pp.242-282.

Andrić, M., Mijić, K. and Jakšić, D., 2011. Financial reporting and characteristics of impairment

of assets in the republic of Serbia, according to IAS/IFRS and national

regulation. Economic Annals. 56(189). pp.101-116.

Ganysa, D. D., 2017. The Influences Of Company Size, Audit Quality, Audit Tenure, And Audit

Pricing To The Going Concern Audit Opinion (Gcao) (Bachelor's thesis, Jakarta: Fakultas

Ekonomi Dan Bisnis UIN Syarif Hidayatullah.).

Oliveira, L., Rodrigues, L.L. and Craig, R., 2010. Intangible assets and value relevance:

Evidence from the Portuguese stock exchange. The British Accounting Review. 42(4).

pp.241-252.

Online

[Online]. Available through <>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.