Analysis of IFRS Adoption Impact on International Financial Management

VerifiedAdded on 2023/04/24

|10

|1745

|224

Report

AI Summary

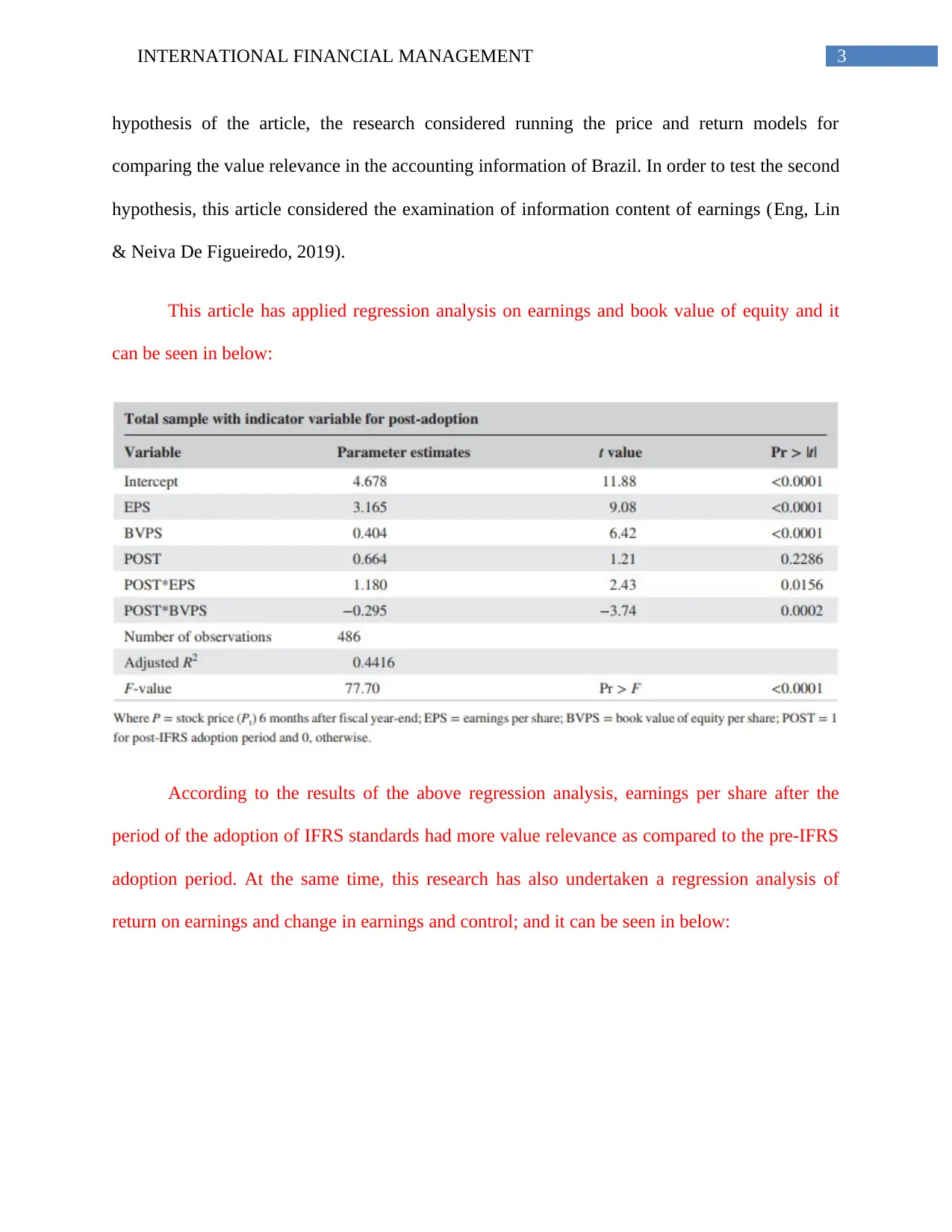

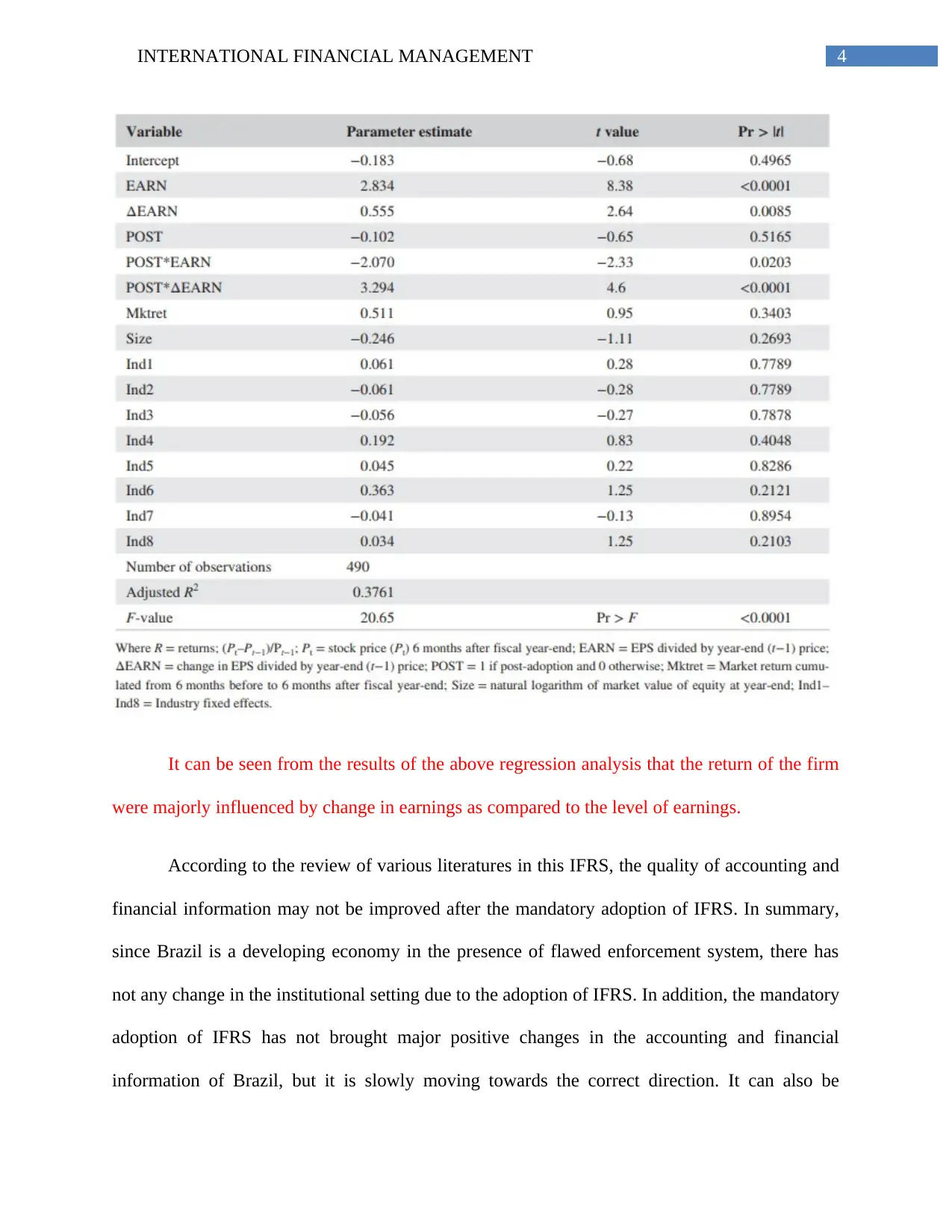

This report analyzes the article "International Financial Reporting Standards adoption and information quality: Evidence from Brazil" by Eng, Lin, and De Figueiredo. The study examines the impact of mandatory IFRS adoption in Brazil on accounting and financial information, focusing on value relevance, earnings information, and financial analyst activities. The research compares the periods before and after the adoption of IFRS to assess its effects. The report identifies the key concepts of international financial management, such as the establishment of a common accounting language, and discusses the implications of IFRS adoption on financial management, including the increased relevance of earnings and book value, information content, financial analyst coverage, and liquidity. The report concludes that while the mandatory adoption of IFRS has brought partial support to the accounting and financial information of Brazil, maintaining compliance with IFRS standards will increase the value relevance of accounting and financial information.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.