International Financial Reporting: A Detailed Review of IASB & IFRS1

VerifiedAdded on 2023/06/17

|15

|3941

|384

Report

AI Summary

This report provides a comprehensive overview of International Financial Reporting Standards (IFRS), focusing on the IASB's conceptual framework and the first-time adoption of IFRS (IFRS1). Part A details the purpose of the IASB's framework, assumptions in financial statement preparation, concepts of capital maintenance, qualitative characteristics of financial statements, and the concept of materiality. Part B discusses IFRS16 related to leases and IAS7 concerning the statement of cash flows. The report explains key terms like 'first IFRS reporting period' and 'date of transition' as defined by IFRS1, highlighting the requirements for first-time adopters. It emphasizes the importance of IFRS in creating uniform, clear, and comparable financial statements for accurate investment performance and true valuation of companies. The analysis aims to enhance understanding of IFRS and its practical application in financial reporting.

International Financial

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

PART A.........................................................................................................................................................3

Question 1 IASB's conceptual framework....................................................................................................3

(a) Main purpose of the IASB's conceptual framework document..........................................................3

(b) Assumptions of preparation of financial statements.........................................................................4

(c) Main concepts of capital maintenance, make references to the IASB's conceptual framework........4

(d) Five qualitative characteristics and attributes of financial statements in the IASB's conceptual

framework...............................................................................................................................................5

(e) Concept of materiality........................................................................................................................6

Question 2 IFRS1 - First-time Adoption of International Financial Reporting Standard...............................7

Explain the terms "first IFRS reporting period" and "date of transition" as defined by IFRS1.................7

Requirements of IFRS1............................................................................................................................7

PART B.........................................................................................................................................................8

Question 4 IFRS16 - Lease........................................................................................................................8

Question 6 : IAS7 - Statement of Cash Flows.........................................................................................10

CONCLUSION.............................................................................................................................................12

REFERENCES..............................................................................................................................................13

INTRODUCTION...........................................................................................................................................3

PART A.........................................................................................................................................................3

Question 1 IASB's conceptual framework....................................................................................................3

(a) Main purpose of the IASB's conceptual framework document..........................................................3

(b) Assumptions of preparation of financial statements.........................................................................4

(c) Main concepts of capital maintenance, make references to the IASB's conceptual framework........4

(d) Five qualitative characteristics and attributes of financial statements in the IASB's conceptual

framework...............................................................................................................................................5

(e) Concept of materiality........................................................................................................................6

Question 2 IFRS1 - First-time Adoption of International Financial Reporting Standard...............................7

Explain the terms "first IFRS reporting period" and "date of transition" as defined by IFRS1.................7

Requirements of IFRS1............................................................................................................................7

PART B.........................................................................................................................................................8

Question 4 IFRS16 - Lease........................................................................................................................8

Question 6 : IAS7 - Statement of Cash Flows.........................................................................................10

CONCLUSION.............................................................................................................................................12

REFERENCES..............................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The International Financial Reporting Standard (IFRS) is an accounting technique that

organizations use to structure their financial reports properly. This approach is used to create

financial statements that are uniform, clear, and comparative. Companies utilize IFRS to perform

out all investment performance and true value of the firm even according to the regulations.

Companies and organizations create income reports and display their real financial status using

the IFRS system. It also provides general recommendations for the preparing financial

statements rather than industry-specific requirements (Banu, Sayaduzzaman and Sil, 2021). Part

A and Part B of the report are divided into two sections. Describe the aim of the IASB's approach

and accounting information standards in Part A. Describe the qualitative qualities and aspects of

accounting records, as well as objectively define the idea of materiality in financial statements.

Check out all the details of the lease and the cash position in Part B to assess the current status of

the firm.

PART A

Question 1 IASB's conceptual framework

(a) Main purpose of the IASB's conceptual framework document

The IASB uses a conceptual technique to evaluate how it develops and revises IFRSs. This idea

is primarily utilized in the creation of revenue recognition, with a concentration on regions that

are not addressed by financial reporting and to help all users in understanding the IFRS. Various

purposes of conceptual model are suggested, including:

• The major goal of the IASB theoretical model is to analyses the growth of new IFRS and to

establish which IFRS are now in use.

• The conceptual framework is used to financial reporting and provides accounting standards for

recording transactions that are not extended to cover regulations.

• In rare situations, the IASB may request that IFRS be updated because they conflict with other

aspects of the theoretical model. As a result, the IASB requires that the divergence from the

standard be defined and explained as the foundation for findings (Shishkov, 2021) (Fiandrino

and Tonelli, 2021).

The International Financial Reporting Standard (IFRS) is an accounting technique that

organizations use to structure their financial reports properly. This approach is used to create

financial statements that are uniform, clear, and comparative. Companies utilize IFRS to perform

out all investment performance and true value of the firm even according to the regulations.

Companies and organizations create income reports and display their real financial status using

the IFRS system. It also provides general recommendations for the preparing financial

statements rather than industry-specific requirements (Banu, Sayaduzzaman and Sil, 2021). Part

A and Part B of the report are divided into two sections. Describe the aim of the IASB's approach

and accounting information standards in Part A. Describe the qualitative qualities and aspects of

accounting records, as well as objectively define the idea of materiality in financial statements.

Check out all the details of the lease and the cash position in Part B to assess the current status of

the firm.

PART A

Question 1 IASB's conceptual framework

(a) Main purpose of the IASB's conceptual framework document

The IASB uses a conceptual technique to evaluate how it develops and revises IFRSs. This idea

is primarily utilized in the creation of revenue recognition, with a concentration on regions that

are not addressed by financial reporting and to help all users in understanding the IFRS. Various

purposes of conceptual model are suggested, including:

• The major goal of the IASB theoretical model is to analyses the growth of new IFRS and to

establish which IFRS are now in use.

• The conceptual framework is used to financial reporting and provides accounting standards for

recording transactions that are not extended to cover regulations.

• In rare situations, the IASB may request that IFRS be updated because they conflict with other

aspects of the theoretical model. As a result, the IASB requires that the divergence from the

standard be defined and explained as the foundation for findings (Shishkov, 2021) (Fiandrino

and Tonelli, 2021).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

• Other function of the conceptual framework is to implement various standards for interpreting

odd activities. It also helps to increase general trustworthiness and activity measures.

(b) Assumptions of preparation of financial statements

The IASB premises outline how to generate genuine and successful financial information

that depict the real financial condition of a firm while financial reporting. The following is with

these hypotheses:

• Ongoing business: The organizations depend on these assumptions to generate financial

accounts and depict all operations in the coming years. It is a critical assumption since it is used

at the conclusion of the fiscal year, when all properties must be liquidated and the sale price

reported at market price (Thamrin, Djou and Sayang, 2021).

• Accrual basis: The major corporation uses this premise to reconcile all income and expenses in

a given financial period. There's really generated or spent not at the time of acceptance or

reimbursement.

• Timeframe assumption: This assumes that the firm will submit all relevant financial

information within a short of time, such as weeks, quarters, or years. Analyze and examine

activities quickly using this knowledge. Such details will be up to date and will aid in the

presentation of a true picture of a company.

(c) Main concepts of capital maintenance, make references to the IASB's conceptual framework

Capital maintenance is the most significant notion, which entails using capital only for the

purpose of generating revenue and managing money in a profit-oriented way. The IASB's

specific conceptual framework defines capital management as follows:

• Financial capital repairs: Profit is earned by a firm whenever the economic quantity of net

wealth increases at the conclusion of the financially year, as opposed to declaring total wealth

after excluding any payouts to contributions from shareholders at the close of the budget period.

For actual currency terms and buying hybrid engines, financial centre management is utilized

(Houcine, Zitouni and Srairi, 2021).

• Physical capital preservation: According to the notion, a profit is made by a firm whenever

physically economic output is used at the close of the budget season since it raises physical

odd activities. It also helps to increase general trustworthiness and activity measures.

(b) Assumptions of preparation of financial statements

The IASB premises outline how to generate genuine and successful financial information

that depict the real financial condition of a firm while financial reporting. The following is with

these hypotheses:

• Ongoing business: The organizations depend on these assumptions to generate financial

accounts and depict all operations in the coming years. It is a critical assumption since it is used

at the conclusion of the fiscal year, when all properties must be liquidated and the sale price

reported at market price (Thamrin, Djou and Sayang, 2021).

• Accrual basis: The major corporation uses this premise to reconcile all income and expenses in

a given financial period. There's really generated or spent not at the time of acceptance or

reimbursement.

• Timeframe assumption: This assumes that the firm will submit all relevant financial

information within a short of time, such as weeks, quarters, or years. Analyze and examine

activities quickly using this knowledge. Such details will be up to date and will aid in the

presentation of a true picture of a company.

(c) Main concepts of capital maintenance, make references to the IASB's conceptual framework

Capital maintenance is the most significant notion, which entails using capital only for the

purpose of generating revenue and managing money in a profit-oriented way. The IASB's

specific conceptual framework defines capital management as follows:

• Financial capital repairs: Profit is earned by a firm whenever the economic quantity of net

wealth increases at the conclusion of the financially year, as opposed to declaring total wealth

after excluding any payouts to contributions from shareholders at the close of the budget period.

For actual currency terms and buying hybrid engines, financial centre management is utilized

(Houcine, Zitouni and Srairi, 2021).

• Physical capital preservation: According to the notion, a profit is made by a firm whenever

physically economic output is used at the close of the budget season since it raises physical

production efficiency at the beginning of the fiscal year. This does not include any distributions

or contributions made by the employee.

(d) Five qualitative characteristics and attributes of financial statements in the IASB's conceptual

framework

Financial statements' qualitative characteristics: The primary goal of financial declarations is to

document all activities that occur within a given fiscal year in order to compute the company's

real profit and offer a clear image to investors. According to the IASB, the following are major

qualitative aspects of financial statements:

• Readability: The most crucial feature of a financial report is that some of the service it contains

should be readily comprehended by consumers and of relevance to stakeholders. Each

accounting records must be legible and understandable. In terms of comprehensibility, company

focused on regulatory facts as well as specialized data in order to effectively prepare financial

(Rayimovna, 2021).

• Relevant: Another feature that a disclosure accounting had to have is that some of the material

provided in the report is meaningful to the needs of the users. They make financial decisions in

terms of investing based on this knowledge. History, current, and future occurrences are all part

of this data interpretation. For instance, knowledge on dividends paid out last year is useful for

interested parties.

• Dependable: The financial statements must contain information that is both trustworthy and

legitimate. Since accounting records offer an accurate image of a firm's management, all data is

collected from reliable sources. These expenditures are displayed using the notion of caution,

and all activities and operations are presented.

• Comparable: The accounting records must be constructed in such a way that they may be

compared. It implies that the income statement is compared to the accounting records from the

previous year. Maintaining and assuring the organizational effectiveness that can be evaluated

and contrasted is critical. To effectively manage these features, financial rules and policies must

be adopted in an appropriate manner from time to time and throughout numerous dominions. The

need of comparison to current business capabilities and finances is an effective method. Once

or contributions made by the employee.

(d) Five qualitative characteristics and attributes of financial statements in the IASB's conceptual

framework

Financial statements' qualitative characteristics: The primary goal of financial declarations is to

document all activities that occur within a given fiscal year in order to compute the company's

real profit and offer a clear image to investors. According to the IASB, the following are major

qualitative aspects of financial statements:

• Readability: The most crucial feature of a financial report is that some of the service it contains

should be readily comprehended by consumers and of relevance to stakeholders. Each

accounting records must be legible and understandable. In terms of comprehensibility, company

focused on regulatory facts as well as specialized data in order to effectively prepare financial

(Rayimovna, 2021).

• Relevant: Another feature that a disclosure accounting had to have is that some of the material

provided in the report is meaningful to the needs of the users. They make financial decisions in

terms of investing based on this knowledge. History, current, and future occurrences are all part

of this data interpretation. For instance, knowledge on dividends paid out last year is useful for

interested parties.

• Dependable: The financial statements must contain information that is both trustworthy and

legitimate. Since accounting records offer an accurate image of a firm's management, all data is

collected from reliable sources. These expenditures are displayed using the notion of caution,

and all activities and operations are presented.

• Comparable: The accounting records must be constructed in such a way that they may be

compared. It implies that the income statement is compared to the accounting records from the

previous year. Maintaining and assuring the organizational effectiveness that can be evaluated

and contrasted is critical. To effectively manage these features, financial rules and policies must

be adopted in an appropriate manner from time to time and throughout numerous dominions. The

need of comparison to current business capabilities and finances is an effective method. Once

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

relevant and dependability are not genuine in a way that requires the continuation of the same

practices, they should be modified (Lestari, Putri and Devi, 2021).

• Timeliness: This is the final attribute that shows that all monetary facts are presented to the

organisation in a specific time frame. Yet all of fiscal year's revenue and spending are reported in

the very same year as well accounting results, not in the following year as well accounting

records. As a result, it will assist in making the best economic decisions and ensuring that you

have all relevant and higher information. As a result, these features need new assistance, and

postponed knowledge leads to poor decisions at the moment.

(e) Concept of materiality

Materiality is a set of accounting standards that businesses employ to govern every activity

or thing that has a direct impact on their financial reports. Every material component should be

represented in financial statements, according to this notion. These important factors are

evaluated on the basis of their inclusion or removal in the finance investor's judgment process.

Materiality is a subjective thing in accountancy; however it is critical for financial statements to

contain all relevant material data (Fathmaningrum and Anggarani, 2021). When comparing big

and small organizations, most characteristics of materiality are noticeable. The fundamental goal

of the accrual accounting is to analyses all market reports that has a direct impact on the thinking

of company's financial consumers. Materiality refers to the relative significance of some assets in

comparison to other things, as determined by the income statement and the magnitude of the

corporate organisation. According to the IASB, there is no specific rule for calculating the

materiality level.

• Pros: The major benefit of this approach is that it offers all of the material's knowledge and aids

in the judgment process. Materiality is a notion that aids people in understanding significant

exchange of goods and services. Because the money of the shareholders is involved in the firm,

they have the responsibility to information about important things so that they may rest certain

that their investment is protected.

• Drawbacks: Numerous times adjustments and exclusions make it difficult to quantify the

potential of materiality in a financial report. It may be necessary to retain an expert to determine

practices, they should be modified (Lestari, Putri and Devi, 2021).

• Timeliness: This is the final attribute that shows that all monetary facts are presented to the

organisation in a specific time frame. Yet all of fiscal year's revenue and spending are reported in

the very same year as well accounting results, not in the following year as well accounting

records. As a result, it will assist in making the best economic decisions and ensuring that you

have all relevant and higher information. As a result, these features need new assistance, and

postponed knowledge leads to poor decisions at the moment.

(e) Concept of materiality

Materiality is a set of accounting standards that businesses employ to govern every activity

or thing that has a direct impact on their financial reports. Every material component should be

represented in financial statements, according to this notion. These important factors are

evaluated on the basis of their inclusion or removal in the finance investor's judgment process.

Materiality is a subjective thing in accountancy; however it is critical for financial statements to

contain all relevant material data (Fathmaningrum and Anggarani, 2021). When comparing big

and small organizations, most characteristics of materiality are noticeable. The fundamental goal

of the accrual accounting is to analyses all market reports that has a direct impact on the thinking

of company's financial consumers. Materiality refers to the relative significance of some assets in

comparison to other things, as determined by the income statement and the magnitude of the

corporate organisation. According to the IASB, there is no specific rule for calculating the

materiality level.

• Pros: The major benefit of this approach is that it offers all of the material's knowledge and aids

in the judgment process. Materiality is a notion that aids people in understanding significant

exchange of goods and services. Because the money of the shareholders is involved in the firm,

they have the responsibility to information about important things so that they may rest certain

that their investment is protected.

• Drawbacks: Numerous times adjustments and exclusions make it difficult to quantify the

potential of materiality in a financial report. It may be necessary to retain an expert to determine

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

if a deal is substantial or immaterial, which can be costly for a small firm (NGUYEN, LE and

TRAN, 2021).

Question 2 IFRS1 - First-time Adoption of International Financial Reporting

Standard

Explain the terms "first IFRS reporting period" and "date of transition" as defined by IFRS1

Whenever businesses first adopt IFRS standards in their accounting records, they utilize

IFRS 1 to prepare their income reports for the first IFRS period ending and the previous year. In

order to publish IFRS financial statements, the firm includes certain accountancy codes and

principles in an actual economic period. Such accounting principles were in force at the

conclusion of the first IFRS reporting period for each standard. Certain exception to the

obligation to correct earlier years in key locations with the cost and going to improve the

advantage of the financial report consumers are included in IFRS 1. The fundamental goal of this

IFRS is to ensure that an institution's first IFRS accounting information, as well as its interim

income reports for the time represented by such accounting records includes collection.

According to IFRS 1, the date of transformation is described as the first time a firm

displays complete comparable information using IFRSs in its first IFRS financial reporting.

When a corporation adopts IFRS for the first year, initial accounting information is created on

the period end, and this initial balance sheet is provided in accordance with IFRS1, which

includes the general guidelines of retrospective application and substitute exclusion. This balance

sheet is not required to be included in accounting records, regardless of when it is used to

maintain records (Seabrooke and Tsingou, 2021).

Requirements of IFRS1

The International Financial Reporting Standards (IFRS) specify how organizations must

handle and publish their financial statements. It's being used by commercial entities to establish

financial statement and to aid in the achievement of worldwide financial reporting framework in

order to make successful financial decisions that are acceptable and adherent to different

countries in the world and sectors. The primary criteria of IFRS 1 are specified financial

statements that include both stated and unpracticed declarations of IFRS compliance. Whenever

TRAN, 2021).

Question 2 IFRS1 - First-time Adoption of International Financial Reporting

Standard

Explain the terms "first IFRS reporting period" and "date of transition" as defined by IFRS1

Whenever businesses first adopt IFRS standards in their accounting records, they utilize

IFRS 1 to prepare their income reports for the first IFRS period ending and the previous year. In

order to publish IFRS financial statements, the firm includes certain accountancy codes and

principles in an actual economic period. Such accounting principles were in force at the

conclusion of the first IFRS reporting period for each standard. Certain exception to the

obligation to correct earlier years in key locations with the cost and going to improve the

advantage of the financial report consumers are included in IFRS 1. The fundamental goal of this

IFRS is to ensure that an institution's first IFRS accounting information, as well as its interim

income reports for the time represented by such accounting records includes collection.

According to IFRS 1, the date of transformation is described as the first time a firm

displays complete comparable information using IFRSs in its first IFRS financial reporting.

When a corporation adopts IFRS for the first year, initial accounting information is created on

the period end, and this initial balance sheet is provided in accordance with IFRS1, which

includes the general guidelines of retrospective application and substitute exclusion. This balance

sheet is not required to be included in accounting records, regardless of when it is used to

maintain records (Seabrooke and Tsingou, 2021).

Requirements of IFRS1

The International Financial Reporting Standards (IFRS) specify how organizations must

handle and publish their financial statements. It's being used by commercial entities to establish

financial statement and to aid in the achievement of worldwide financial reporting framework in

order to make successful financial decisions that are acceptable and adherent to different

countries in the world and sectors. The primary criteria of IFRS 1 are specified financial

statements that include both stated and unpracticed declarations of IFRS compliance. Whenever

Prisca plc does not use IFRS, it runs into a number of issues, including the necessity to change

reporting requirements in IAS 8 or the need for special transitional procedures in other IFRs.

For the first time, IFRS 1 was used. The adoption of IFRS establishes a procedure that a

company must undertake whenever it agrees to use the accountancy laws and regulation of IFRS

1 on a timely manner in order to prepare its special purpose financial statements. It is limiting

expenditures based on public standards for the starting and conclusion of the IFRS period

(Anisere-Hameed, 2021). The following are the major standards of IFRS 1 for analyzing

financial reports:

• Three financial statements

• Two income reports for profit and loss account as well as other cash flows

• Prepare two distinct profit or loss accounts (if applicable)

• 2 distinct cash flow report

• Two cash flow reports

• Include any connected notes that include additional data

PART B

Question 4 IFRS16 - Lease

The IFRS 16 specifies how an IFRS reporters will recognize, analyses, summarize, and

disclose leases. The specification describes the singular lessee model approach that is used by

companies to determine financial assets for all contracts except if the lease period is specified at

12 months. Leasing companies continued to classify leases depends on the quantity less than the

low price of the asset commodities. The major goal of this principal cause by IFRS 16 for the

acknowledgment, measurement, presentation, and disclosure of leases is to ensure that lessees

and lessons submit all related data that is used truthfully to report relevant interactions (Parnicki,

Petrović and Tucaković, 2021).

(a) IFRS 16 refers to a contract or a portion of a contract that is used to demonstrate the rights to

use resources in a certain accounting statement and in the way in which money is exchanged.

reporting requirements in IAS 8 or the need for special transitional procedures in other IFRs.

For the first time, IFRS 1 was used. The adoption of IFRS establishes a procedure that a

company must undertake whenever it agrees to use the accountancy laws and regulation of IFRS

1 on a timely manner in order to prepare its special purpose financial statements. It is limiting

expenditures based on public standards for the starting and conclusion of the IFRS period

(Anisere-Hameed, 2021). The following are the major standards of IFRS 1 for analyzing

financial reports:

• Three financial statements

• Two income reports for profit and loss account as well as other cash flows

• Prepare two distinct profit or loss accounts (if applicable)

• 2 distinct cash flow report

• Two cash flow reports

• Include any connected notes that include additional data

PART B

Question 4 IFRS16 - Lease

The IFRS 16 specifies how an IFRS reporters will recognize, analyses, summarize, and

disclose leases. The specification describes the singular lessee model approach that is used by

companies to determine financial assets for all contracts except if the lease period is specified at

12 months. Leasing companies continued to classify leases depends on the quantity less than the

low price of the asset commodities. The major goal of this principal cause by IFRS 16 for the

acknowledgment, measurement, presentation, and disclosure of leases is to ensure that lessees

and lessons submit all related data that is used truthfully to report relevant interactions (Parnicki,

Petrović and Tucaković, 2021).

(a) IFRS 16 refers to a contract or a portion of a contract that is used to demonstrate the rights to

use resources in a certain accounting statement and in the way in which money is exchanged.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

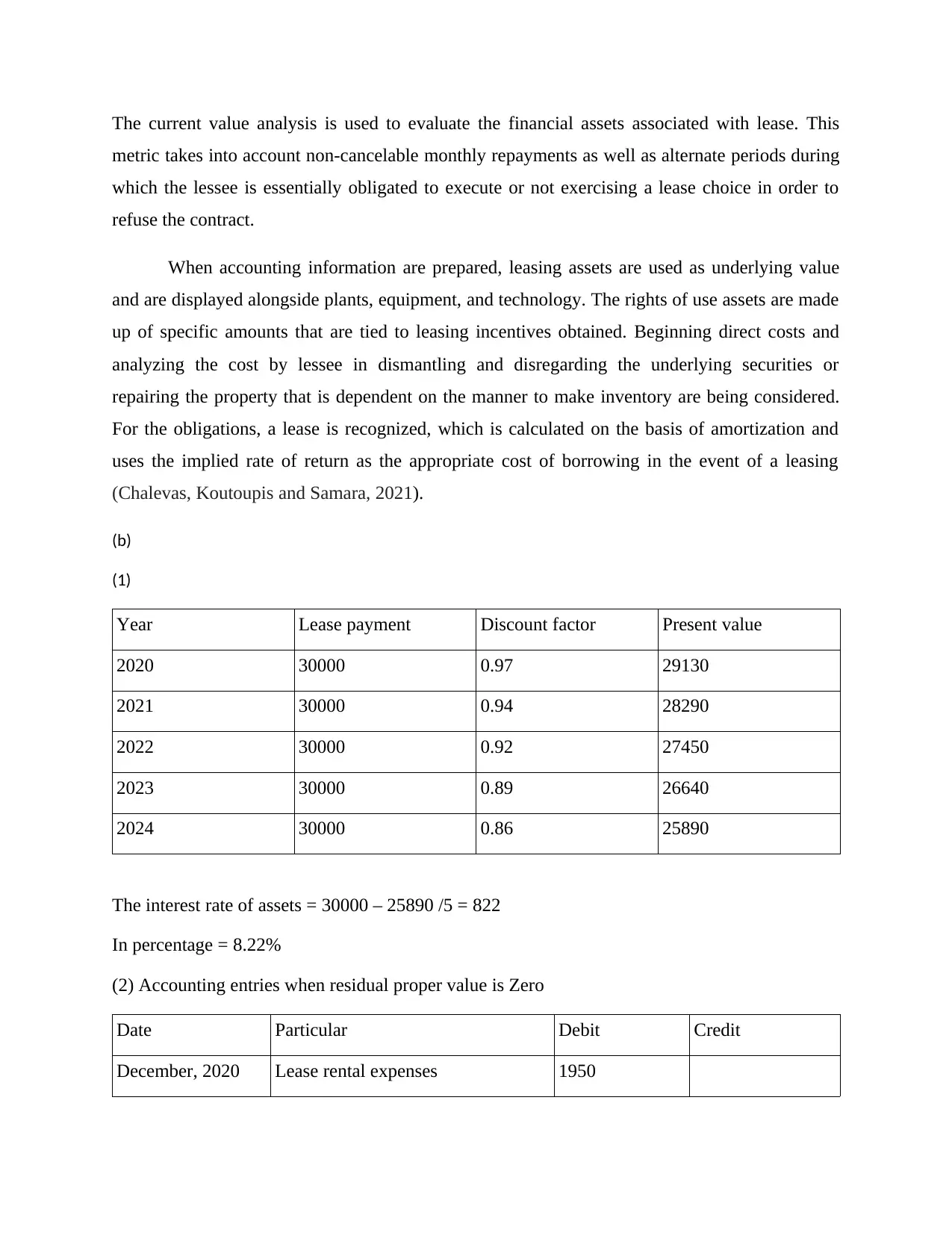

The current value analysis is used to evaluate the financial assets associated with lease. This

metric takes into account non-cancelable monthly repayments as well as alternate periods during

which the lessee is essentially obligated to execute or not exercising a lease choice in order to

refuse the contract.

When accounting information are prepared, leasing assets are used as underlying value

and are displayed alongside plants, equipment, and technology. The rights of use assets are made

up of specific amounts that are tied to leasing incentives obtained. Beginning direct costs and

analyzing the cost by lessee in dismantling and disregarding the underlying securities or

repairing the property that is dependent on the manner to make inventory are being considered.

For the obligations, a lease is recognized, which is calculated on the basis of amortization and

uses the implied rate of return as the appropriate cost of borrowing in the event of a leasing

(Chalevas, Koutoupis and Samara, 2021).

(b)

(1)

Year Lease payment Discount factor Present value

2020 30000 0.97 29130

2021 30000 0.94 28290

2022 30000 0.92 27450

2023 30000 0.89 26640

2024 30000 0.86 25890

The interest rate of assets = 30000 – 25890 /5 = 822

In percentage = 8.22%

(2) Accounting entries when residual proper value is Zero

Date Particular Debit Credit

December, 2020 Lease rental expenses 1950

metric takes into account non-cancelable monthly repayments as well as alternate periods during

which the lessee is essentially obligated to execute or not exercising a lease choice in order to

refuse the contract.

When accounting information are prepared, leasing assets are used as underlying value

and are displayed alongside plants, equipment, and technology. The rights of use assets are made

up of specific amounts that are tied to leasing incentives obtained. Beginning direct costs and

analyzing the cost by lessee in dismantling and disregarding the underlying securities or

repairing the property that is dependent on the manner to make inventory are being considered.

For the obligations, a lease is recognized, which is calculated on the basis of amortization and

uses the implied rate of return as the appropriate cost of borrowing in the event of a leasing

(Chalevas, Koutoupis and Samara, 2021).

(b)

(1)

Year Lease payment Discount factor Present value

2020 30000 0.97 29130

2021 30000 0.94 28290

2022 30000 0.92 27450

2023 30000 0.89 26640

2024 30000 0.86 25890

The interest rate of assets = 30000 – 25890 /5 = 822

In percentage = 8.22%

(2) Accounting entries when residual proper value is Zero

Date Particular Debit Credit

December, 2020 Lease rental expenses 1950

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

interest expenses 28050

To Cash (Paid to lessor) 30000

(Being paid amount of lease)

The lessee will recognize the lease as a responsibility and also an asset at the moment of the

lease, with the amount considered at the same levels as the inception of the lease goods.

Question 6 : IAS7 - Statement of Cash Flows

An organisation prepares an IAS 7 statement of cash flows to reflect the cash inflow and

outflow of a firm for a certain fiscal year. It is an essential component of every company

organisation that oversees all accounting operations. The cash flow statement is divided into

three areas, the first of which is operating, the second of which is spending, and the third of

which is funding. All interactions that have a monetary value are divided into three categories. It

is produced in two ways by entities: directly and indirectly, for the latter 2 groups mostly given

on a net basis. The following are the key principles indicated by IAS 7 for the creation of a

statement of cash flows:

• Operating operations: This is the major activity that considers the revenue-generating activities

of the firm. As a result, it primarily considers income receipts from clients, cash payments to

suppliers, and money provided to workers.

• Investment operations: All actions linked to the purchase and sale of long-term investment

properties that are not payable on demand are included.

• Financing activities: Such operations change depending on the company's capital reserves and

debt arrangement.

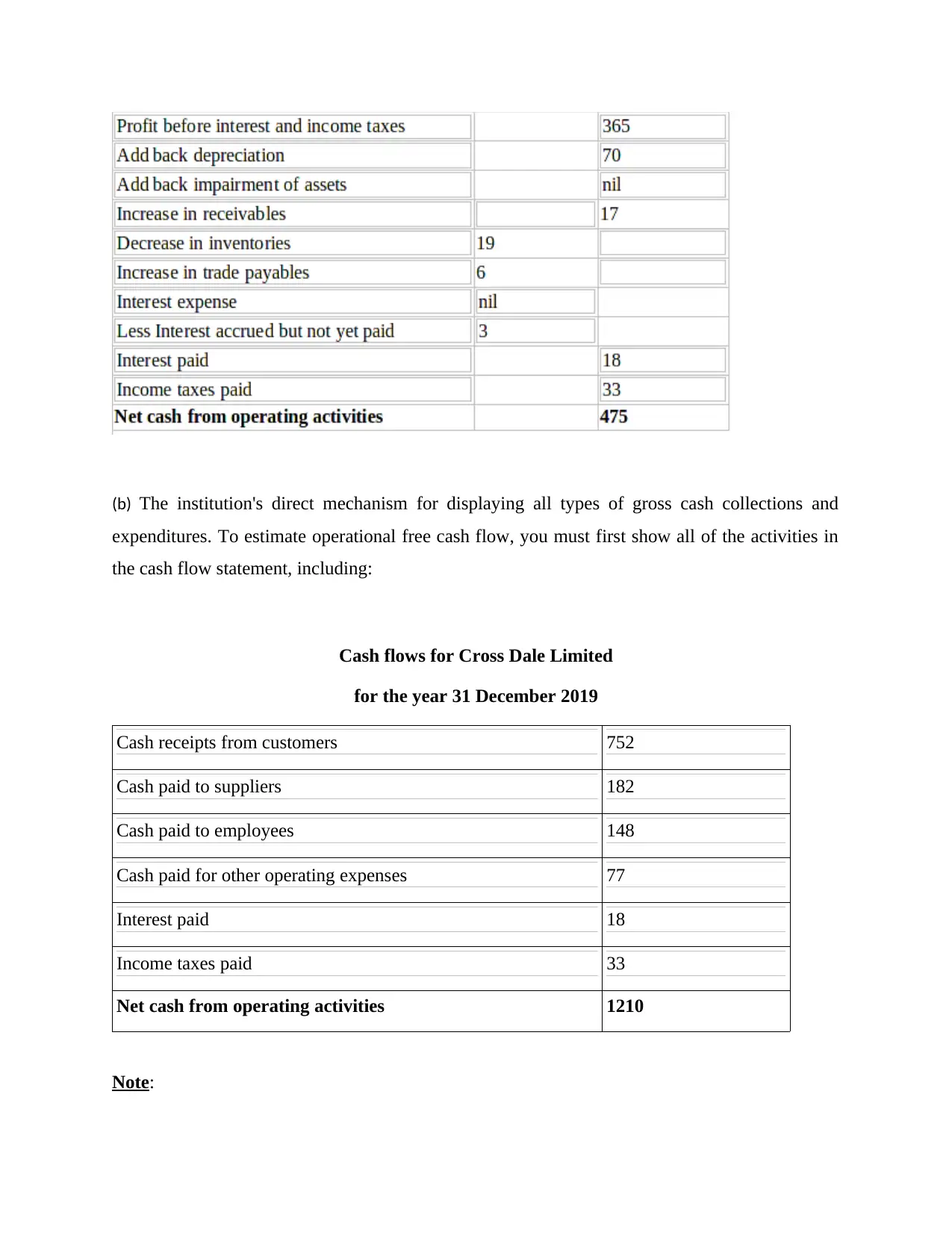

(a) The company's indirect technique of managing all accruals-based net profit and loss that

affect non-cash activities. Modify all activities in the operational working capital column

according to the format, like:

Cash flows for Cross Dale Limited

for the year 31 December 2019

To Cash (Paid to lessor) 30000

(Being paid amount of lease)

The lessee will recognize the lease as a responsibility and also an asset at the moment of the

lease, with the amount considered at the same levels as the inception of the lease goods.

Question 6 : IAS7 - Statement of Cash Flows

An organisation prepares an IAS 7 statement of cash flows to reflect the cash inflow and

outflow of a firm for a certain fiscal year. It is an essential component of every company

organisation that oversees all accounting operations. The cash flow statement is divided into

three areas, the first of which is operating, the second of which is spending, and the third of

which is funding. All interactions that have a monetary value are divided into three categories. It

is produced in two ways by entities: directly and indirectly, for the latter 2 groups mostly given

on a net basis. The following are the key principles indicated by IAS 7 for the creation of a

statement of cash flows:

• Operating operations: This is the major activity that considers the revenue-generating activities

of the firm. As a result, it primarily considers income receipts from clients, cash payments to

suppliers, and money provided to workers.

• Investment operations: All actions linked to the purchase and sale of long-term investment

properties that are not payable on demand are included.

• Financing activities: Such operations change depending on the company's capital reserves and

debt arrangement.

(a) The company's indirect technique of managing all accruals-based net profit and loss that

affect non-cash activities. Modify all activities in the operational working capital column

according to the format, like:

Cash flows for Cross Dale Limited

for the year 31 December 2019

(b) The institution's direct mechanism for displaying all types of gross cash collections and

expenditures. To estimate operational free cash flow, you must first show all of the activities in

the cash flow statement, including:

Cash flows for Cross Dale Limited

for the year 31 December 2019

Cash receipts from customers 752

Cash paid to suppliers 182

Cash paid to employees 148

Cash paid for other operating expenses 77

Interest paid 18

Income taxes paid 33

Net cash from operating activities 1210

Note:

expenditures. To estimate operational free cash flow, you must first show all of the activities in

the cash flow statement, including:

Cash flows for Cross Dale Limited

for the year 31 December 2019

Cash receipts from customers 752

Cash paid to suppliers 182

Cash paid to employees 148

Cash paid for other operating expenses 77

Interest paid 18

Income taxes paid 33

Net cash from operating activities 1210

Note:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.