Accounting for Finance Leases and Impairment Loss Journal Entries-IFRS

VerifiedAdded on 2023/06/04

|13

|2403

|367

Report

AI Summary

This report provides an overview of accounting for finance leases under IFRS 16, focusing on the specific treatment for manufacturer or dealer lessors. It details the initial recognition, subsequent measurement, and disclosure requirements for lessors, highlighting the differences from operating leases. Additionally, the report includes the preparation of journal entries for impairment losses, using the example of Gali Ltd., demonstrating the calculation and accounting adjustments required when an asset's carrying amount exceeds its recoverable amount. The analysis covers the allocation of impairment losses across different asset classes and the corresponding journal entries to reflect these adjustments.

1

Part A: Accounting of leases

Part A: Accounting of leases

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

The main purpose of this assessment is to undertake an essay in relation to the accounting

for finance leases. In this context, it has provided an insight into the new leases standard of IFRS

16 that is developed by the IASB to report the accounting transactions relating to both the

operating and finance leases. The report ahs specifically examined the difference between the

accounting treatment of leases for manufactures or dealer lessors. This has facilitated in gaining

an adequate understanding of the finance leases and the specific requirements that need to be met

by the manufacturer during their accounting. Also, it has provided knowledge in context of the

method of preparation of journal entries for reporting the impairment losses during financial

reporting.

Executive Summary

The main purpose of this assessment is to undertake an essay in relation to the accounting

for finance leases. In this context, it has provided an insight into the new leases standard of IFRS

16 that is developed by the IASB to report the accounting transactions relating to both the

operating and finance leases. The report ahs specifically examined the difference between the

accounting treatment of leases for manufactures or dealer lessors. This has facilitated in gaining

an adequate understanding of the finance leases and the specific requirements that need to be met

by the manufacturer during their accounting. Also, it has provided knowledge in context of the

method of preparation of journal entries for reporting the impairment losses during financial

reporting.

3

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

IFRS 16: Leases...............................................................................................................................4

Accounting for finance leases in the books of accounts of manufacturers or dealer lessor............5

Conclusion.....................................................................................................................................11

References......................................................................................................................................13

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

IFRS 16: Leases...............................................................................................................................4

Accounting for finance leases in the books of accounts of manufacturers or dealer lessor............5

Conclusion.....................................................................................................................................11

References......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

The present report is developed for providing an understanding of the process used for

accounting for finance leases by business entities. A lease can be defined as a contract in which

an asset such as property is transferred to another for using that asset for achieving specific

returns such as money or assets. There are two major types of leases used in accounting these are

operating and financial leases. In this context, a finance lease can be described as a lease for

transferring the overall risks and rewards associated with a leased asset to the lessee. IASB

(International Accounting Standard Board) has advocated the use of IFRS 16 for reporting of the

accounting transaction related to lease. The standard has eliminated the need for classifying the

leases separately under operating or finance leases for a lessee. The leases are recorded by

recognition of the present value of lease payments and depicting them either as lease assets or in

combination with properly, plant or equipment. The recognition of lease payments in the

financial reports of a company ensures that it meets its financial liability as they become due. In

this context, the present assessment is undertaken for present a discussion in relation to the

accounting for finance leases by manufactures or dealer lessors. In addition to this, it has

prepared journal entries for Gali Ltd in relation to the impairment loses that it has incurred by

using the information provided in context of carrying amount of the assets.

IFRS 16: Leases

The standards of IFRS 16 are developed mainly to provide guidance for both the lessees

and the lessor in relation to the application of accounting policies for reporting leases. The

finance leases are different from that of an operating lease as it involves pre-determination of the

amount to be realized after completion of the lease term. The lease term can be sated as the time-

period between the dates from which lessee possess the authority to use the lease asset without

any further payment (IFRS 16 Leases, 2018). The accounting for finance leases during the

financial reporting consists of the process of initial recognition, measurement and disclosure as

stated as follows:

Recognition

Introduction

The present report is developed for providing an understanding of the process used for

accounting for finance leases by business entities. A lease can be defined as a contract in which

an asset such as property is transferred to another for using that asset for achieving specific

returns such as money or assets. There are two major types of leases used in accounting these are

operating and financial leases. In this context, a finance lease can be described as a lease for

transferring the overall risks and rewards associated with a leased asset to the lessee. IASB

(International Accounting Standard Board) has advocated the use of IFRS 16 for reporting of the

accounting transaction related to lease. The standard has eliminated the need for classifying the

leases separately under operating or finance leases for a lessee. The leases are recorded by

recognition of the present value of lease payments and depicting them either as lease assets or in

combination with properly, plant or equipment. The recognition of lease payments in the

financial reports of a company ensures that it meets its financial liability as they become due. In

this context, the present assessment is undertaken for present a discussion in relation to the

accounting for finance leases by manufactures or dealer lessors. In addition to this, it has

prepared journal entries for Gali Ltd in relation to the impairment loses that it has incurred by

using the information provided in context of carrying amount of the assets.

IFRS 16: Leases

The standards of IFRS 16 are developed mainly to provide guidance for both the lessees

and the lessor in relation to the application of accounting policies for reporting leases. The

finance leases are different from that of an operating lease as it involves pre-determination of the

amount to be realized after completion of the lease term. The lease term can be sated as the time-

period between the dates from which lessee possess the authority to use the lease asset without

any further payment (IFRS 16 Leases, 2018). The accounting for finance leases during the

financial reporting consists of the process of initial recognition, measurement and disclosure as

stated as follows:

Recognition

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

The lessees are entities to recognize the finance leases as an asset or liability in its

balance sheet at the fair value of the leased property

The non-recognition of the lease transaction in the balance sheet can lead to understating

the economic resource of an entity by understating its financial position

Measurement

The minimum lease payments should be determined between the finance charge and the

reduction of the outstanding liability.

The amount of depreciation incurred on a leased asset need is attributed to the accounting

period during which an asset is used

Disclosure

The net carrying amount of the finance leases need to be disclosed at the end of a

reporting period for each asset class

Contingent rents should be recognized as expense in the accounting period (IFRS 16,

Leases, 2017)

Accounting for finance leases in the books of accounts of manufacturers or dealer lessor

Initial recognition of leases

The accounting of finance leases has been provided in accounting standard IFRS 16:

Leases. To initial recognize the finance leases in the books of accounts, lessor should take the

value of lease in their balance sheet under the heading receivables. The value of leases should be

equal to the net investment in leases. In general, all the risks and rewards related to the legal

ownership, under the finance lease have been transferred by the lessor to the lessee. The payment

received under lease tenure is treated as repayment of principle amount, finance income that has

to be reimbursed and rewards that lessor received for providing the lessee the lease assets and

providing services (Effects Analysis International Financial Reporting Standard, 2016).

To calculate the value of lease, the lessor has to determine the initial direct cost that has

been levied under the lease arrangement. The initial direct cost includes the amount such as

commissions, legal fees, and other internal cost that is incremental in nature and that is directly

The lessees are entities to recognize the finance leases as an asset or liability in its

balance sheet at the fair value of the leased property

The non-recognition of the lease transaction in the balance sheet can lead to understating

the economic resource of an entity by understating its financial position

Measurement

The minimum lease payments should be determined between the finance charge and the

reduction of the outstanding liability.

The amount of depreciation incurred on a leased asset need is attributed to the accounting

period during which an asset is used

Disclosure

The net carrying amount of the finance leases need to be disclosed at the end of a

reporting period for each asset class

Contingent rents should be recognized as expense in the accounting period (IFRS 16,

Leases, 2017)

Accounting for finance leases in the books of accounts of manufacturers or dealer lessor

Initial recognition of leases

The accounting of finance leases has been provided in accounting standard IFRS 16:

Leases. To initial recognize the finance leases in the books of accounts, lessor should take the

value of lease in their balance sheet under the heading receivables. The value of leases should be

equal to the net investment in leases. In general, all the risks and rewards related to the legal

ownership, under the finance lease have been transferred by the lessor to the lessee. The payment

received under lease tenure is treated as repayment of principle amount, finance income that has

to be reimbursed and rewards that lessor received for providing the lessee the lease assets and

providing services (Effects Analysis International Financial Reporting Standard, 2016).

To calculate the value of lease, the lessor has to determine the initial direct cost that has

been levied under the lease arrangement. The initial direct cost includes the amount such as

commissions, legal fees, and other internal cost that is incremental in nature and that is directly

6

attributable to negotiating and arranging the lease agreement. The direct cost of lease does not

cover the expenses that are occurred in relation to arrangement of lease by the sales and

marketing team. After calculating the value of lease that has to be initial recognised in the

balance sheet the treatment in books or manufacture or dealers have been specially provided in

IFRS 16. As per IFRS 16, the cost incurred by the manufacturers and dealers lessor in relation to

negotiating and also arranging the lease has to be excluded from the value of initial direct cost. It

means the net investment in lease does not include direct cost occurred in relation to the leases.

All the direct cost incurred in relation to the arrangement and negotiating lease is taken to the

income statement as expenses in the period when the revenue against that has been recognised

(IFRS 16 – The new leases standard, 2016). The value of lease has to be initial recognised at net

investment value in lease. In case of manufacturers or dealer lessor the value of net investment

here means total values less any cost incurred in arranging or negotiating the lease. As provided

earlier in this para that any direct expenses that have incurred by manufacturer or dealer lessor

has to be taken to income statement as expenses (IFRS 16, Leases, 2017).

Subsequent measurement and recognition

Manufacturing or dealer lessors receive the finance income from the finance leases which

they made agreement with. As per IFRS 16, the recognition of income from the finance income

is typically based on the pattern that reflects a constant rate of return on the net investment in

leases by lessor. As per the accounting method, lessor has to prepare a chart that allocates the

finance income, received from the lessee, over the terms of lease in systematic and prorate basis

(rational basis). The lease payments from the lessee (excluding the cost of services) have to

apply to the gross investment value shown in balance sheet in order to reduce the value of

principle and unearned finance income. It will offset the value of lease assets and liabilities

together. As per IFRS 16, lessor has to be periodically review the value of unguaranteed residual

values (used in calculating the value of lease) in order to recognize the any reduction in value to

the value of income allocated over the useful lease term. In case of manufacturers or dealers

lessor the value of selling profit or loss as per the policies that has been used by the entity as

outright sales. In case lessor intentionally quotes the low interest rates the value of selling profit

has to be restricted to the market interest rate. There is option with the manufacturer or dealer

lessor to make offer to the lessee to either buy or lessee the asset at the end of lease term. These

attributable to negotiating and arranging the lease agreement. The direct cost of lease does not

cover the expenses that are occurred in relation to arrangement of lease by the sales and

marketing team. After calculating the value of lease that has to be initial recognised in the

balance sheet the treatment in books or manufacture or dealers have been specially provided in

IFRS 16. As per IFRS 16, the cost incurred by the manufacturers and dealers lessor in relation to

negotiating and also arranging the lease has to be excluded from the value of initial direct cost. It

means the net investment in lease does not include direct cost occurred in relation to the leases.

All the direct cost incurred in relation to the arrangement and negotiating lease is taken to the

income statement as expenses in the period when the revenue against that has been recognised

(IFRS 16 – The new leases standard, 2016). The value of lease has to be initial recognised at net

investment value in lease. In case of manufacturers or dealer lessor the value of net investment

here means total values less any cost incurred in arranging or negotiating the lease. As provided

earlier in this para that any direct expenses that have incurred by manufacturer or dealer lessor

has to be taken to income statement as expenses (IFRS 16, Leases, 2017).

Subsequent measurement and recognition

Manufacturing or dealer lessors receive the finance income from the finance leases which

they made agreement with. As per IFRS 16, the recognition of income from the finance income

is typically based on the pattern that reflects a constant rate of return on the net investment in

leases by lessor. As per the accounting method, lessor has to prepare a chart that allocates the

finance income, received from the lessee, over the terms of lease in systematic and prorate basis

(rational basis). The lease payments from the lessee (excluding the cost of services) have to

apply to the gross investment value shown in balance sheet in order to reduce the value of

principle and unearned finance income. It will offset the value of lease assets and liabilities

together. As per IFRS 16, lessor has to be periodically review the value of unguaranteed residual

values (used in calculating the value of lease) in order to recognize the any reduction in value to

the value of income allocated over the useful lease term. In case of manufacturers or dealers

lessor the value of selling profit or loss as per the policies that has been used by the entity as

outright sales. In case lessor intentionally quotes the low interest rates the value of selling profit

has to be restricted to the market interest rate. There is option with the manufacturer or dealer

lessor to make offer to the lessee to either buy or lessee the asset at the end of lease term. These

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

transactions will give rise to accounting of two types of income. Firstly, the profit or loss from

the sale of lease asset at normal selling price less any trade discounts and secondly finance

income over the lease terms.

Sales revenue recognised by manufacturer or dealer lessor in book of accounts lower of

fair value of assets or the present value of minimum lease payments that is computed at the

market rate of interest. The cost of sale related to the lease assets is calculated as cost (carrying

amount) less the present of unguaranteed residual value. The difference that arises due to sale

revenue and cost of sales is known as selling profit and it should be recognised as company

policy of outright sales (IFRS 16 Leases, 2018).

Disclosures of finance leases by the lessor

Lessor has to made disclosers regarding the value of finance lease in relation of all the

finance lease held by them and bifurcate them as the lease payments that has to be received in

three board categories i.e. not later than one year, later than one year but not later than one year

and later than five years.

transactions will give rise to accounting of two types of income. Firstly, the profit or loss from

the sale of lease asset at normal selling price less any trade discounts and secondly finance

income over the lease terms.

Sales revenue recognised by manufacturer or dealer lessor in book of accounts lower of

fair value of assets or the present value of minimum lease payments that is computed at the

market rate of interest. The cost of sale related to the lease assets is calculated as cost (carrying

amount) less the present of unguaranteed residual value. The difference that arises due to sale

revenue and cost of sales is known as selling profit and it should be recognised as company

policy of outright sales (IFRS 16 Leases, 2018).

Disclosures of finance leases by the lessor

Lessor has to made disclosers regarding the value of finance lease in relation of all the

finance lease held by them and bifurcate them as the lease payments that has to be received in

three board categories i.e. not later than one year, later than one year but not later than one year

and later than five years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Part B: Journal Entries for Accounting of Impairment Loss

Part B: Journal Entries for Accounting of Impairment Loss

9

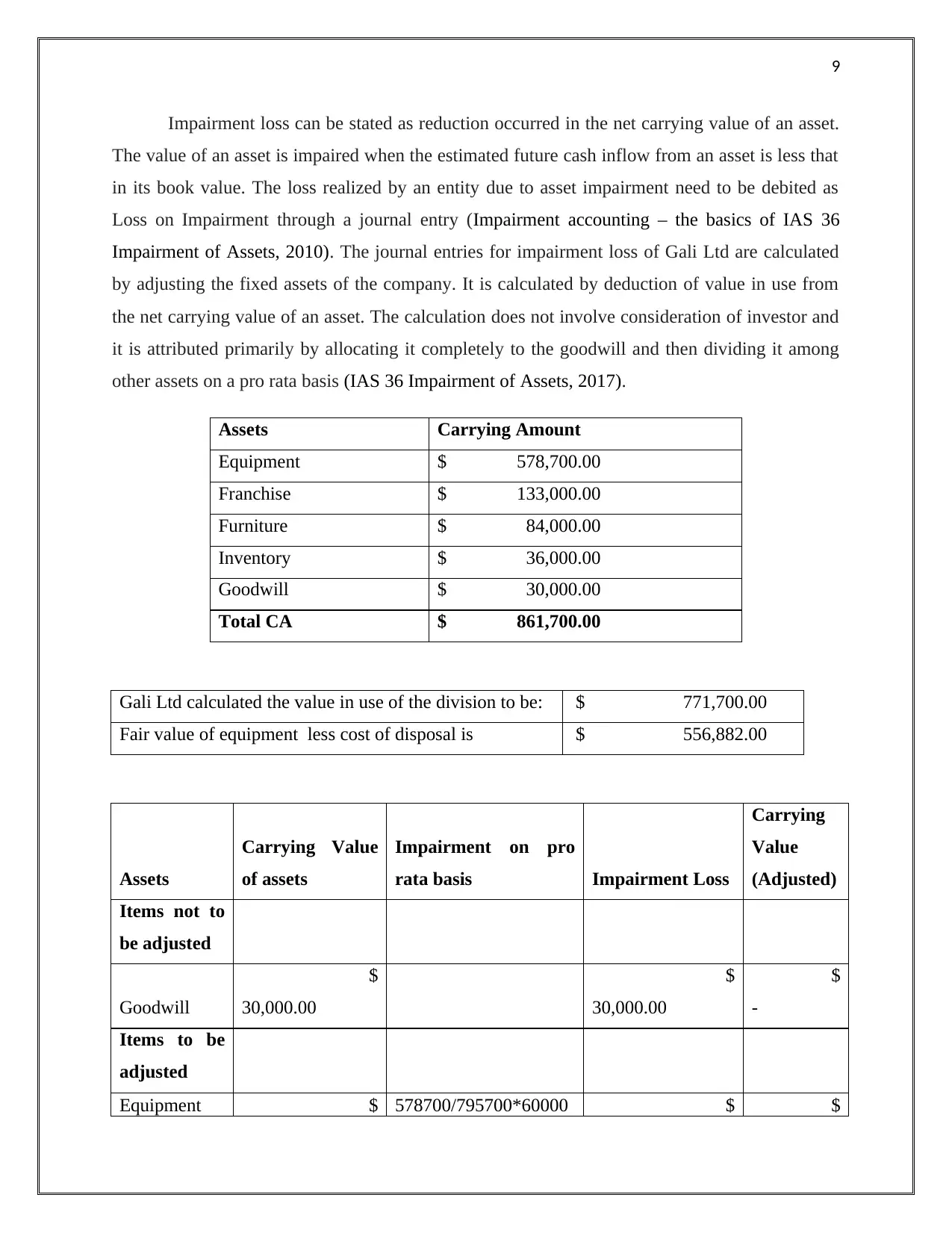

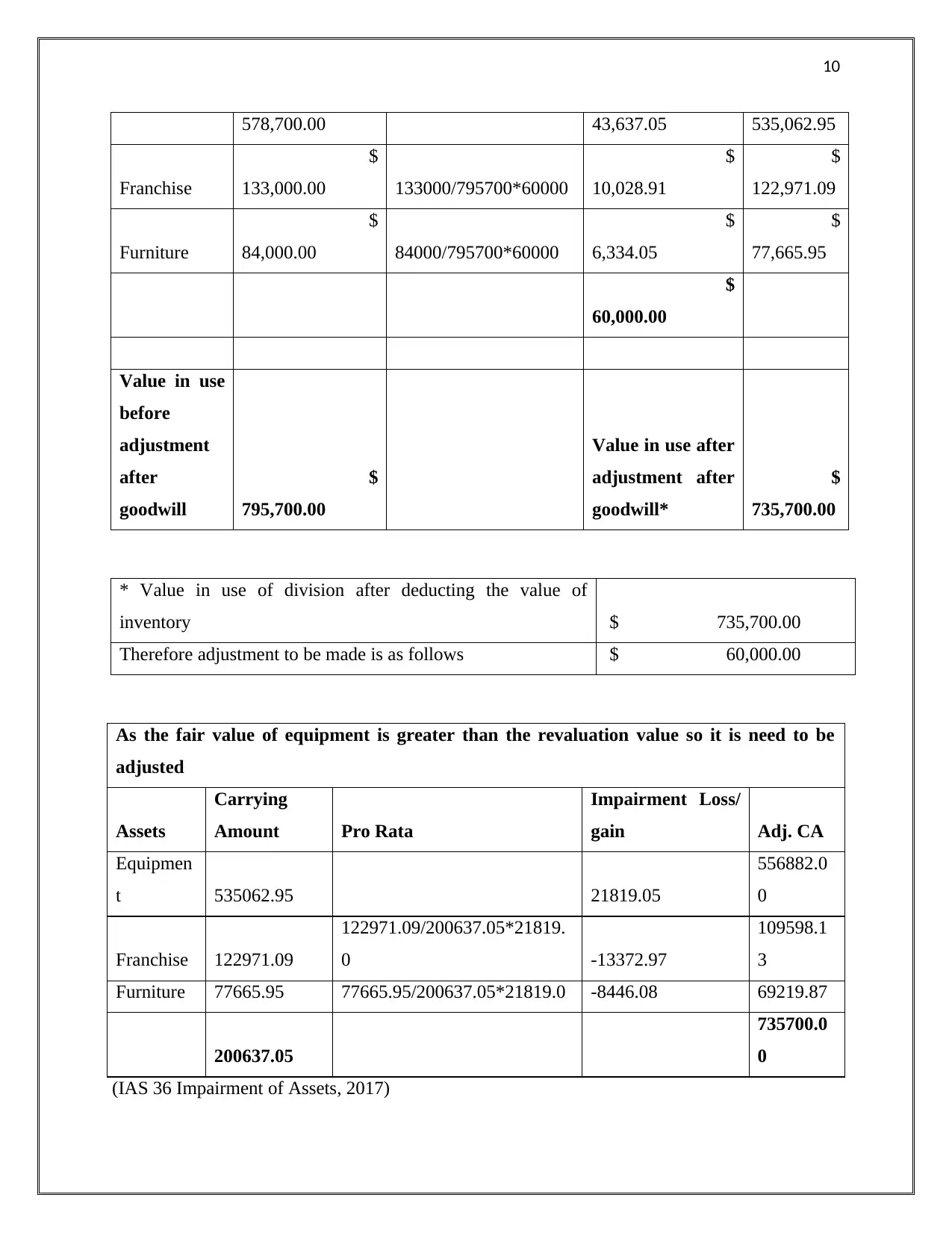

Impairment loss can be stated as reduction occurred in the net carrying value of an asset.

The value of an asset is impaired when the estimated future cash inflow from an asset is less that

in its book value. The loss realized by an entity due to asset impairment need to be debited as

Loss on Impairment through a journal entry (Impairment accounting – the basics of IAS 36

Impairment of Assets, 2010). The journal entries for impairment loss of Gali Ltd are calculated

by adjusting the fixed assets of the company. It is calculated by deduction of value in use from

the net carrying value of an asset. The calculation does not involve consideration of investor and

it is attributed primarily by allocating it completely to the goodwill and then dividing it among

other assets on a pro rata basis (IAS 36 Impairment of Assets, 2017).

Assets Carrying Amount

Equipment $ 578,700.00

Franchise $ 133,000.00

Furniture $ 84,000.00

Inventory $ 36,000.00

Goodwill $ 30,000.00

Total CA $ 861,700.00

Gali Ltd calculated the value in use of the division to be: $ 771,700.00

Fair value of equipment less cost of disposal is $ 556,882.00

Assets

Carrying Value

of assets

Impairment on pro

rata basis Impairment Loss

Carrying

Value

(Adjusted)

Items not to

be adjusted

Goodwill

$

30,000.00

$

30,000.00

$

-

Items to be

adjusted

Equipment $ 578700/795700*60000 $ $

Impairment loss can be stated as reduction occurred in the net carrying value of an asset.

The value of an asset is impaired when the estimated future cash inflow from an asset is less that

in its book value. The loss realized by an entity due to asset impairment need to be debited as

Loss on Impairment through a journal entry (Impairment accounting – the basics of IAS 36

Impairment of Assets, 2010). The journal entries for impairment loss of Gali Ltd are calculated

by adjusting the fixed assets of the company. It is calculated by deduction of value in use from

the net carrying value of an asset. The calculation does not involve consideration of investor and

it is attributed primarily by allocating it completely to the goodwill and then dividing it among

other assets on a pro rata basis (IAS 36 Impairment of Assets, 2017).

Assets Carrying Amount

Equipment $ 578,700.00

Franchise $ 133,000.00

Furniture $ 84,000.00

Inventory $ 36,000.00

Goodwill $ 30,000.00

Total CA $ 861,700.00

Gali Ltd calculated the value in use of the division to be: $ 771,700.00

Fair value of equipment less cost of disposal is $ 556,882.00

Assets

Carrying Value

of assets

Impairment on pro

rata basis Impairment Loss

Carrying

Value

(Adjusted)

Items not to

be adjusted

Goodwill

$

30,000.00

$

30,000.00

$

-

Items to be

adjusted

Equipment $ 578700/795700*60000 $ $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

578,700.00 43,637.05 535,062.95

Franchise

$

133,000.00 133000/795700*60000

$

10,028.91

$

122,971.09

Furniture

$

84,000.00 84000/795700*60000

$

6,334.05

$

77,665.95

$

60,000.00

Value in use

before

adjustment

after

goodwill

$

795,700.00

Value in use after

adjustment after

goodwill*

$

735,700.00

* Value in use of division after deducting the value of

inventory $ 735,700.00

Therefore adjustment to be made is as follows $ 60,000.00

As the fair value of equipment is greater than the revaluation value so it is need to be

adjusted

Assets

Carrying

Amount Pro Rata

Impairment Loss/

gain Adj. CA

Equipmen

t 535062.95 21819.05

556882.0

0

Franchise 122971.09

122971.09/200637.05*21819.

0 -13372.97

109598.1

3

Furniture 77665.95 77665.95/200637.05*21819.0 -8446.08 69219.87

200637.05

735700.0

0

(IAS 36 Impairment of Assets, 2017)

578,700.00 43,637.05 535,062.95

Franchise

$

133,000.00 133000/795700*60000

$

10,028.91

$

122,971.09

Furniture

$

84,000.00 84000/795700*60000

$

6,334.05

$

77,665.95

$

60,000.00

Value in use

before

adjustment

after

goodwill

$

795,700.00

Value in use after

adjustment after

goodwill*

$

735,700.00

* Value in use of division after deducting the value of

inventory $ 735,700.00

Therefore adjustment to be made is as follows $ 60,000.00

As the fair value of equipment is greater than the revaluation value so it is need to be

adjusted

Assets

Carrying

Amount Pro Rata

Impairment Loss/

gain Adj. CA

Equipmen

t 535062.95 21819.05

556882.0

0

Franchise 122971.09

122971.09/200637.05*21819.

0 -13372.97

109598.1

3

Furniture 77665.95 77665.95/200637.05*21819.0 -8446.08 69219.87

200637.05

735700.0

0

(IAS 36 Impairment of Assets, 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

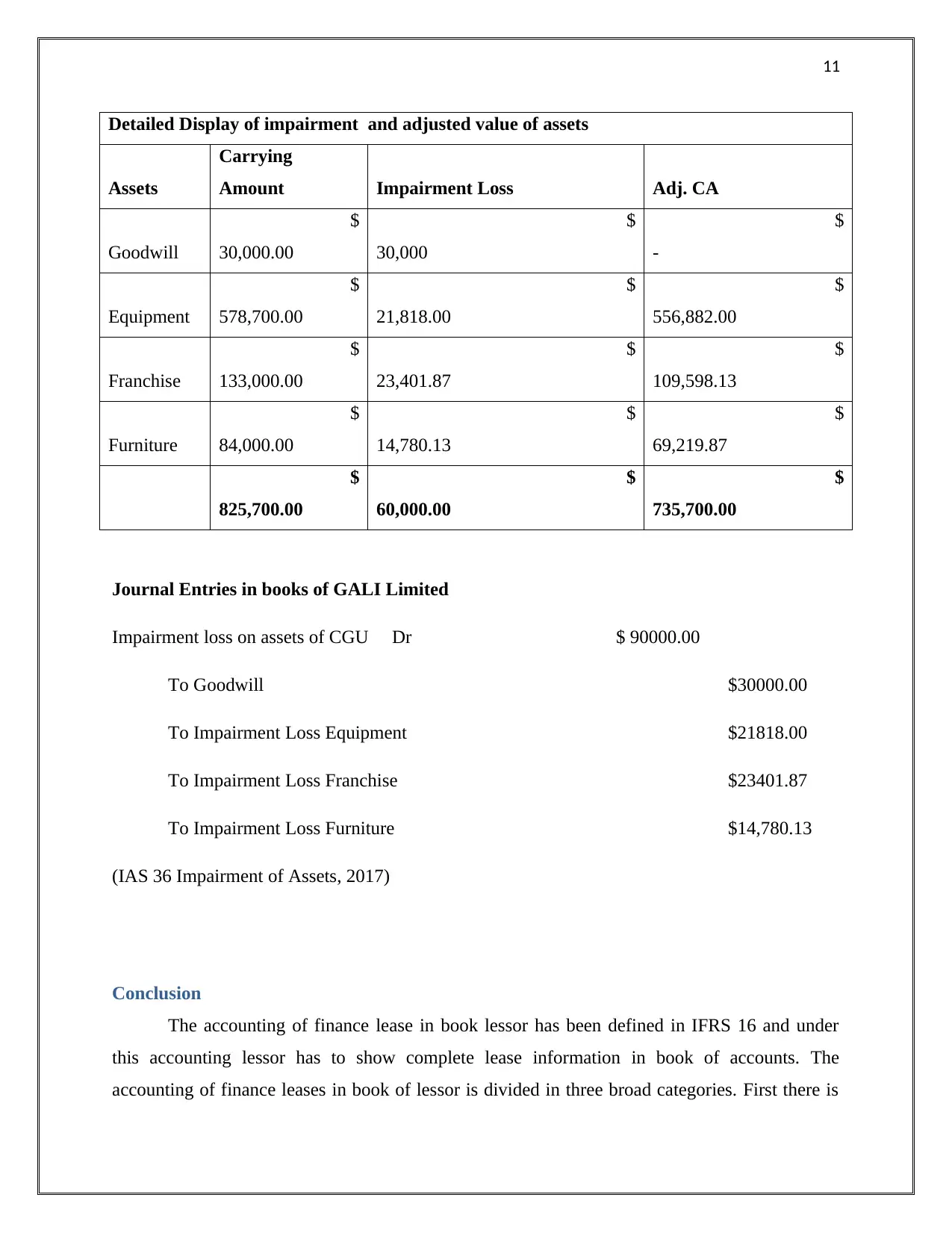

Detailed Display of impairment and adjusted value of assets

Assets

Carrying

Amount Impairment Loss Adj. CA

Goodwill

$

30,000.00

$

30,000

$

-

Equipment

$

578,700.00

$

21,818.00

$

556,882.00

Franchise

$

133,000.00

$

23,401.87

$

109,598.13

Furniture

$

84,000.00

$

14,780.13

$

69,219.87

$

825,700.00

$

60,000.00

$

735,700.00

Journal Entries in books of GALI Limited

Impairment loss on assets of CGU Dr $ 90000.00

To Goodwill $30000.00

To Impairment Loss Equipment $21818.00

To Impairment Loss Franchise $23401.87

To Impairment Loss Furniture $14,780.13

(IAS 36 Impairment of Assets, 2017)

Conclusion

The accounting of finance lease in book lessor has been defined in IFRS 16 and under

this accounting lessor has to show complete lease information in book of accounts. The

accounting of finance leases in book of lessor is divided in three broad categories. First there is

Detailed Display of impairment and adjusted value of assets

Assets

Carrying

Amount Impairment Loss Adj. CA

Goodwill

$

30,000.00

$

30,000

$

-

Equipment

$

578,700.00

$

21,818.00

$

556,882.00

Franchise

$

133,000.00

$

23,401.87

$

109,598.13

Furniture

$

84,000.00

$

14,780.13

$

69,219.87

$

825,700.00

$

60,000.00

$

735,700.00

Journal Entries in books of GALI Limited

Impairment loss on assets of CGU Dr $ 90000.00

To Goodwill $30000.00

To Impairment Loss Equipment $21818.00

To Impairment Loss Franchise $23401.87

To Impairment Loss Furniture $14,780.13

(IAS 36 Impairment of Assets, 2017)

Conclusion

The accounting of finance lease in book lessor has been defined in IFRS 16 and under

this accounting lessor has to show complete lease information in book of accounts. The

accounting of finance leases in book of lessor is divided in three broad categories. First there is

12

need to initial recognize the value of lease, after that there is need to make changes in value of

leases due to change in value of different items in lease accounting and lastly there is need to

make the disclosures in book of accounts.

need to initial recognize the value of lease, after that there is need to make changes in value of

leases due to change in value of different items in lease accounting and lastly there is need to

make the disclosures in book of accounts.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.