Critically Discussing IFRS 2 & Positive Accounting Theory

VerifiedAdded on 2023/06/15

|9

|2203

|427

Report

AI Summary

This report provides a critical discussion of IFRS 2's guidance on share-based payments and evaluates the key constructs behind Positive Accounting Theory (PAT). It examines how managers might manipulate financial information for self-interest, supported by academic references. The report covers the theoretical basis and content of financial accounting systems, including the grant date model, scope of IFRS 2, recognition principles, and valuation techniques. It also addresses current issues in financial reporting, such as the use of grant date fair value measurements and challenges related to equity-settled schemes. The analysis incorporates perspectives from prior research and concludes with insights into optimizing firm prospects through strategic accounting policy choices.

Running head: ADVANCED FINANCIAL REPORTING AND THEORY

Advanced Financial Reporting and Theory

University Name

Student Name

Authors’ Note

Advanced Financial Reporting and Theory

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2ADVANCED FINANCIAL REPORTING AND THEORY

Introduction

The current study analytically examines theoretical foundation and content of financial

accounting systems that can provide financial information for the communication to different

users. In addition to this, the current segment also presents a research on current issues in

financial reporting and explains the effect of the issues on the overall regulatory structure

within the purview of UK. The section also presents specific guidance of IFRS 2 that is

related to the manner share based payments have the need to be accounted and reported in the

financial assertions. Moving further, the study also states about Positive Accounting Theory

that indicates towards altering accounting policies, handling discretionary accruals, timing of

implementation of novel accounting standards, altering real variables and many others. The

study also helps in relating important application of the notion in the current case.

Critical assessment of the theoretical basis and content of financial accounting systems

The current section intends to analyse the theoretical basis as well as content of financial

accounting system with special reference to article “Get Grips with IFRS 2” accounting

standard. The utilization of the grant dated alternative to enumerate the fair value of

particularly the equity settled remuneration can be considered as an important component of

IFRS 2. However, critics are of the opinion that it can necessarily lead to inaccuracy in the

process of reporting (Brigham and Ehrhardt 2013). Analysis of prior reports reveal the fact

that share based payment in IFRS 2 presently sits on the list of diverse research projects

designed by the International Accounting Standards Board and is also one of more intricate

of IFRS directives.

Theoretical Basis and content of financial accounting system

Introduction

The current study analytically examines theoretical foundation and content of financial

accounting systems that can provide financial information for the communication to different

users. In addition to this, the current segment also presents a research on current issues in

financial reporting and explains the effect of the issues on the overall regulatory structure

within the purview of UK. The section also presents specific guidance of IFRS 2 that is

related to the manner share based payments have the need to be accounted and reported in the

financial assertions. Moving further, the study also states about Positive Accounting Theory

that indicates towards altering accounting policies, handling discretionary accruals, timing of

implementation of novel accounting standards, altering real variables and many others. The

study also helps in relating important application of the notion in the current case.

Critical assessment of the theoretical basis and content of financial accounting systems

The current section intends to analyse the theoretical basis as well as content of financial

accounting system with special reference to article “Get Grips with IFRS 2” accounting

standard. The utilization of the grant dated alternative to enumerate the fair value of

particularly the equity settled remuneration can be considered as an important component of

IFRS 2. However, critics are of the opinion that it can necessarily lead to inaccuracy in the

process of reporting (Brigham and Ehrhardt 2013). Analysis of prior reports reveal the fact

that share based payment in IFRS 2 presently sits on the list of diverse research projects

designed by the International Accounting Standards Board and is also one of more intricate

of IFRS directives.

Theoretical Basis and content of financial accounting system

3ADVANCED FINANCIAL REPORTING AND THEORY

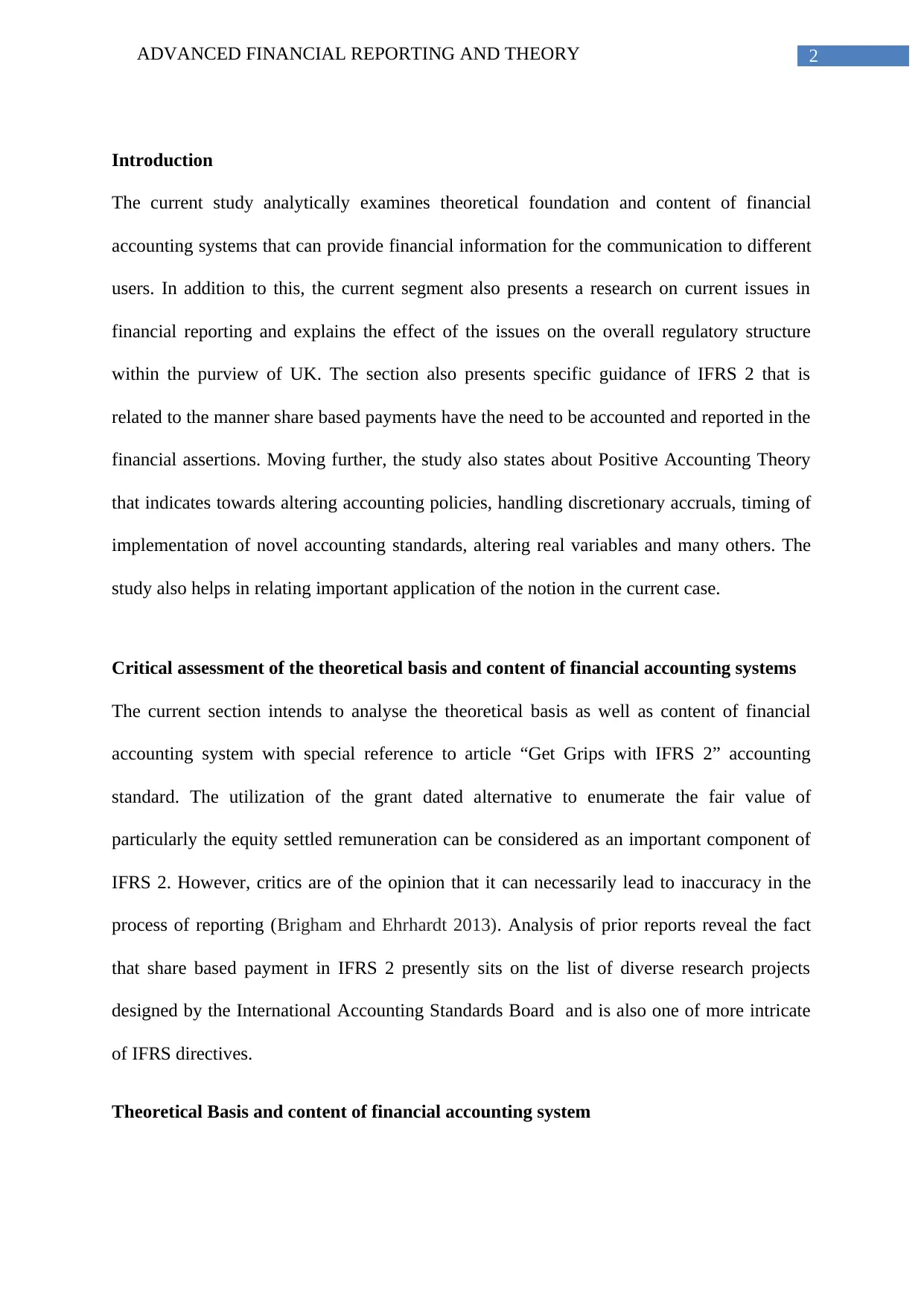

The standard IFRS 2 mainly calls for entities to detect diverse awards of share based payment

in different financial assertions founded on fair value (Leuz and Wysocki 2016). This

happens at the time when both goods as well as services are accepted and that is presently

determined at specific grant date for particular share based payments that are issued to

different members of the staff. IASB also settled on grant date model. Under this specific

model, a specific entity enumerates fair value of particular share based payment award issued

to a specific worker on the grant date (Zeff et al. 2016).

Scope of IFRS

The scope of IFRS 2 mainly includes equity based share based payment deal; cash settled

share based payment deal and share based payment deal with cash alternatives (Lusardi and

Mitchell 2014). However, the IFRS 2 also does not include the transactions counting transfers

of particularly equity instruments that are evidently not disbursement for products as well as

services. In addition to this, IFRS 2 also does not include transactions/deals with shareholders

that are essentially at the time when shareholders act solely in the capability as shareholders

(Zeff 2013). Again, transactions that are within the scope of the regulation IAS 32 as well as

IAS 39 are also not included within the purview of IFRS 2.

Recognition Principle:

the requirements of the directives of IFRS 2 essentially requires business entities to recognize

the expends or else an asset in case if the goods as well services accepted satisfy the criteria

for detecting a specific asset (Sunder 2016). In addition to this, an enhancement in equity

(that mainly refers to transactions that are settled in various equity instruments) or else in

liabilities (that primarily refers to cash settled deals). Nevertheless, IFRS mentions that for

specifically awards to diverse employees, a particular entity have the need to utilize fair value

of instruments of equity enumerated particularly at the grant date. Furthermore, according to

The standard IFRS 2 mainly calls for entities to detect diverse awards of share based payment

in different financial assertions founded on fair value (Leuz and Wysocki 2016). This

happens at the time when both goods as well as services are accepted and that is presently

determined at specific grant date for particular share based payments that are issued to

different members of the staff. IASB also settled on grant date model. Under this specific

model, a specific entity enumerates fair value of particular share based payment award issued

to a specific worker on the grant date (Zeff et al. 2016).

Scope of IFRS

The scope of IFRS 2 mainly includes equity based share based payment deal; cash settled

share based payment deal and share based payment deal with cash alternatives (Lusardi and

Mitchell 2014). However, the IFRS 2 also does not include the transactions counting transfers

of particularly equity instruments that are evidently not disbursement for products as well as

services. In addition to this, IFRS 2 also does not include transactions/deals with shareholders

that are essentially at the time when shareholders act solely in the capability as shareholders

(Zeff 2013). Again, transactions that are within the scope of the regulation IAS 32 as well as

IAS 39 are also not included within the purview of IFRS 2.

Recognition Principle:

the requirements of the directives of IFRS 2 essentially requires business entities to recognize

the expends or else an asset in case if the goods as well services accepted satisfy the criteria

for detecting a specific asset (Sunder 2016). In addition to this, an enhancement in equity

(that mainly refers to transactions that are settled in various equity instruments) or else in

liabilities (that primarily refers to cash settled deals). Nevertheless, IFRS mentions that for

specifically awards to diverse employees, a particular entity have the need to utilize fair value

of instruments of equity enumerated particularly at the grant date. Furthermore, according to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4ADVANCED FINANCIAL REPORTING AND THEORY

the regulation, for awards to different non-employees, there remains a rebuttable supposition

that the fair value of goods as well as services can be considered to be more consistently

determinable, enumerated at the time when these goods and services are accepted.

Valuation Techniques refers to the fact unless a specific option with the same or else

comparable terms is listed, a business entities cannot acquire fair values externally. Thus, it is

important to approximate the fair value of mainly share based payment utilizing an option

pricing model (Lee 2014).

Thus, it can be mentioned that structural plans are somewhat identical to the regulations of

IFRS 2 and the associated expend ramifications. Vesting conditions exert immense influence

on the expense charged to the earning assertion in a different manner. In case if an option has

market vesting situation or else a non-vesting circumstances, a specific unit might help in

recognizing expends though a condition is not attained and the option does not necessarily

vest. In contrast, an award subject to specific non-marketing vesting situation does not lead to

IFRS 2 expense only if the condition is not satisfied (Vernimmen et al. 2014). Finally, it can

be said that decision makers also need to take into consideration diverse hidden awards of

share based payments that again might be within the purview of IFRS 2 in specific situations.

For instance the cases include non-corporate shareholder of a specific business entity

providing shares to members of the staff of the business entity. Again, employees also accept

the regulation, for awards to different non-employees, there remains a rebuttable supposition

that the fair value of goods as well as services can be considered to be more consistently

determinable, enumerated at the time when these goods and services are accepted.

Valuation Techniques refers to the fact unless a specific option with the same or else

comparable terms is listed, a business entities cannot acquire fair values externally. Thus, it is

important to approximate the fair value of mainly share based payment utilizing an option

pricing model (Lee 2014).

Thus, it can be mentioned that structural plans are somewhat identical to the regulations of

IFRS 2 and the associated expend ramifications. Vesting conditions exert immense influence

on the expense charged to the earning assertion in a different manner. In case if an option has

market vesting situation or else a non-vesting circumstances, a specific unit might help in

recognizing expends though a condition is not attained and the option does not necessarily

vest. In contrast, an award subject to specific non-marketing vesting situation does not lead to

IFRS 2 expense only if the condition is not satisfied (Vernimmen et al. 2014). Finally, it can

be said that decision makers also need to take into consideration diverse hidden awards of

share based payments that again might be within the purview of IFRS 2 in specific situations.

For instance the cases include non-corporate shareholder of a specific business entity

providing shares to members of the staff of the business entity. Again, employees also accept

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5ADVANCED FINANCIAL REPORTING AND THEORY

a cash payout that is equal to the enhancement in the share index. Furthermore, a business

entity also provides a specific employee a restricted recourse loan for the purpose of

acquiring shares.

Critical assessment of the ability to research current issues in financial reporting

Based on the current article, it can be mentioned that part of the intricacy stems from the

utilization of the grant date fair value measurement model. Essentially, this can be utilized in

the process of arrangements that can be settled in specific shares else wise in share options.

However, in order to comprehend potential issues behind the causes. As per Merz (2015),

potential issues mainly stems up from two diverse transaction types that can be utilized for

remunerating employees. As rightly indicated by Cascino and Gassen (2015), the equity

settled schemes refers to the ones where employee receives the advantage specifically in the

form of equity, namely shares or else share options. Again, the cash settled schemes refer to

the fact that employees accept cash associated to the price of share of a business entity at a

specific period. As per IFRS 2, diverse share based payments need to be identified in

financial assertions utilizing fair value over a specific period of time.

In addition to this, there are also certain issues associated to the grant date fair value. In

essence, it generates less relevant information as the same is not properly updated to

represent the alterations in the value of the option. Again, issues also stem at the time of

dealing with particular share options that is underwater (Christensen et al. 2013). Also, the

grant date is also very inconsistent with the treatment of cash that refers to cash settled plan

and other employee based system of accounting.

IASB addresses diverse issues at the time of deciding the model that is to be implemented at

the time of introduction of particularly IFRS 2. This necessarily represents value of service,

instead of option. Essentially, the fair value of particularly services accepted is not affected

a cash payout that is equal to the enhancement in the share index. Furthermore, a business

entity also provides a specific employee a restricted recourse loan for the purpose of

acquiring shares.

Critical assessment of the ability to research current issues in financial reporting

Based on the current article, it can be mentioned that part of the intricacy stems from the

utilization of the grant date fair value measurement model. Essentially, this can be utilized in

the process of arrangements that can be settled in specific shares else wise in share options.

However, in order to comprehend potential issues behind the causes. As per Merz (2015),

potential issues mainly stems up from two diverse transaction types that can be utilized for

remunerating employees. As rightly indicated by Cascino and Gassen (2015), the equity

settled schemes refers to the ones where employee receives the advantage specifically in the

form of equity, namely shares or else share options. Again, the cash settled schemes refer to

the fact that employees accept cash associated to the price of share of a business entity at a

specific period. As per IFRS 2, diverse share based payments need to be identified in

financial assertions utilizing fair value over a specific period of time.

In addition to this, there are also certain issues associated to the grant date fair value. In

essence, it generates less relevant information as the same is not properly updated to

represent the alterations in the value of the option. Again, issues also stem at the time of

dealing with particular share options that is underwater (Christensen et al. 2013). Also, the

grant date is also very inconsistent with the treatment of cash that refers to cash settled plan

and other employee based system of accounting.

IASB addresses diverse issues at the time of deciding the model that is to be implemented at

the time of introduction of particularly IFRS 2. This necessarily represents value of service,

instead of option. Essentially, the fair value of particularly services accepted is not affected

6ADVANCED FINANCIAL REPORTING AND THEORY

by alterations in the fair value of specific equity instruments accepted in exchange. Alteration

in option value in second year is unrelated to the service value delivered by members of staff

in first year (DeFond et al. 2014).

This necessarily represents the service value instead of option. In this case, the fair value of

particularly services accepted is not influenced by consequent alterations in the equity

represented in fair value. The equity that is being relocated is theoretically different from

cash payment. IASB thereafter started the use of specific principles that implement to equity

transactions under Conceptual Framework for purpose of Financial Reporting. Again,

utilization of the grant date fair value system thereafter initiates less volatility particularly in

the financial assertions than utilizing reporting date system in a fair value framework., since

the fair value remains fixed and thus generates a more predictable annual expenditure

(Brigham and Ehrhardt 2013). In addition to this, challenges of the grant date fair value

model also lead to displacement of the same. Present accounting exercises implemented in

IFRS 2 as well as IAS 19 also deliver two alternatives that are already present. A specific

alternative that can be implemented include introducing reporting date fair value system as is

utilized in cash settled plans. Another alternative that can be implemented include

introduction of service date measurement system in a particular manner identical to IAS 19.

The corporations might take into consideration the necessity of good predictions of real world

incidents and translate the same into accounting deals as per Positive Accounting Theory. As

per PAT, management of firms can think about optimizing their prospects for the survival

and thereby organize them effectively. For this, the challenges due to the current issues in

regulations need to be identified and rectified at the same time (Brigham and Ehrhardt 2013).

In addition to this, as per this theory altering situations also calls for the need of the managers

to have adequate flexibility in selecting accounting policies. However, this reflects the

by alterations in the fair value of specific equity instruments accepted in exchange. Alteration

in option value in second year is unrelated to the service value delivered by members of staff

in first year (DeFond et al. 2014).

This necessarily represents the service value instead of option. In this case, the fair value of

particularly services accepted is not influenced by consequent alterations in the equity

represented in fair value. The equity that is being relocated is theoretically different from

cash payment. IASB thereafter started the use of specific principles that implement to equity

transactions under Conceptual Framework for purpose of Financial Reporting. Again,

utilization of the grant date fair value system thereafter initiates less volatility particularly in

the financial assertions than utilizing reporting date system in a fair value framework., since

the fair value remains fixed and thus generates a more predictable annual expenditure

(Brigham and Ehrhardt 2013). In addition to this, challenges of the grant date fair value

model also lead to displacement of the same. Present accounting exercises implemented in

IFRS 2 as well as IAS 19 also deliver two alternatives that are already present. A specific

alternative that can be implemented include introducing reporting date fair value system as is

utilized in cash settled plans. Another alternative that can be implemented include

introduction of service date measurement system in a particular manner identical to IAS 19.

The corporations might take into consideration the necessity of good predictions of real world

incidents and translate the same into accounting deals as per Positive Accounting Theory. As

per PAT, management of firms can think about optimizing their prospects for the survival

and thereby organize them effectively. For this, the challenges due to the current issues in

regulations need to be identified and rectified at the same time (Brigham and Ehrhardt 2013).

In addition to this, as per this theory altering situations also calls for the need of the managers

to have adequate flexibility in selecting accounting policies. However, this reflects the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7ADVANCED FINANCIAL REPORTING AND THEORY

opportunistic behaviour that takes place at time when the actions are for the better of personal

interests.

Conclusion

In conclusion, it can be said that the above mentioned study helps in understanding key

concepts of advanced financial reporting and associated theoretical foundation. The above

study thereby assists in understanding the fact that the utilization of the grant date option for

the purpose of measuring the fair value of particularly equity settled remuneration is an

important component of IFRS 2. Nonetheless critics are of the view that this can lead to

inaccurate ways of reporting.

opportunistic behaviour that takes place at time when the actions are for the better of personal

interests.

Conclusion

In conclusion, it can be said that the above mentioned study helps in understanding key

concepts of advanced financial reporting and associated theoretical foundation. The above

study thereby assists in understanding the fact that the utilization of the grant date option for

the purpose of measuring the fair value of particularly equity settled remuneration is an

important component of IFRS 2. Nonetheless critics are of the view that this can lead to

inaccurate ways of reporting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8ADVANCED FINANCIAL REPORTING AND THEORY

References

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Cascino, S. and Gassen, J., 2015. What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies, 20(1), pp.242-282.

Christensen, H.B., Hail, L. and Leuz, C., 2013. Mandatory IFRS reporting and changes in

enforcement. Journal of Accounting and Economics, 56(2), pp.147-177.

DeFond, M.L., Hung, M., Li, S. and Li, Y., 2014. Does mandatory IFRS adoption affect

crash risk?. The Accounting Review, 90(1), pp.265-299.

Lee, T.A., 2014. Evolution of Corporate Financial Reporting (RLE Accounting). Routledge.

Leuz, C. and Wysocki, P.D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting

Research, 54(2), pp.525-622.

Lusardi, A. and Mitchell, O.S., 2014. The economic importance of financial literacy: Theory

and evidence. Journal of Economic Literature, 52(1), pp.5-44.

Merz, A., 2015. Expensing Performance-Vested Executive Stock Options: Is There

Underreporting Under IFRS 2?. Browser Download This Paper.

Sunder, S., 2016. Rethinking financial reporting: standards, norms and

institutions. Foundations and Trends® in Accounting, 11(1–2), pp.1-118.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate finance:

theory and practice. John Wiley & Sons.

References

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Cascino, S. and Gassen, J., 2015. What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies, 20(1), pp.242-282.

Christensen, H.B., Hail, L. and Leuz, C., 2013. Mandatory IFRS reporting and changes in

enforcement. Journal of Accounting and Economics, 56(2), pp.147-177.

DeFond, M.L., Hung, M., Li, S. and Li, Y., 2014. Does mandatory IFRS adoption affect

crash risk?. The Accounting Review, 90(1), pp.265-299.

Lee, T.A., 2014. Evolution of Corporate Financial Reporting (RLE Accounting). Routledge.

Leuz, C. and Wysocki, P.D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting

Research, 54(2), pp.525-622.

Lusardi, A. and Mitchell, O.S., 2014. The economic importance of financial literacy: Theory

and evidence. Journal of Economic Literature, 52(1), pp.5-44.

Merz, A., 2015. Expensing Performance-Vested Executive Stock Options: Is There

Underreporting Under IFRS 2?. Browser Download This Paper.

Sunder, S., 2016. Rethinking financial reporting: standards, norms and

institutions. Foundations and Trends® in Accounting, 11(1–2), pp.1-118.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate finance:

theory and practice. John Wiley & Sons.

9ADVANCED FINANCIAL REPORTING AND THEORY

Zeff, S.A., 2013. The objectives of financial reporting: a historical survey and

analysis. Accounting and Business Research, 43(4), pp.262-327.

Zeff, S.A., van der Wel, F. and Camfferman, C., 2016. Company financial reporting: A

historical and comparative study of the Dutch regulatory process. Routledge.

Zeff, S.A., 2013. The objectives of financial reporting: a historical survey and

analysis. Accounting and Business Research, 43(4), pp.262-327.

Zeff, S.A., van der Wel, F. and Camfferman, C., 2016. Company financial reporting: A

historical and comparative study of the Dutch regulatory process. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.