IKEA: Management Accounting Systems, Budgeting and Financial Analysis

VerifiedAdded on 2023/06/18

|21

|5553

|87

Report

AI Summary

This report provides an in-depth analysis of IKEA's management accounting methodologies, highlighting the company's use of various systems such as inventory management, cost reporting, and price optimization. It explores the application of different costing techniques, including managerial and absorption costing, to manage costs effectively. The report also examines IKEA's planning procedures, focusing on operating, master, and capital budgets. Furthermore, it discusses how IKEA utilizes management accounting systems to address financial challenges. The analysis demonstrates how these practices contribute to informed decision-making, budgetary control, and overall financial health, ensuring optimal business performance and sustainable growth for IKEA.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Companies utilise a variety of management accounting methodologies in the finance area. It

is an accountancy procedure in which accounting experts examine economic or non economic

information for internal managerial accounting purposes. This accountancy has a defined set

of roles and obligations for giant corporations. This report based on the IKEA Company

which is using management accounting to manage their financial information in effective

manner. In this report using various types of reports and systems like inventory management,

cost report and pricing optimising systems. Along with, company uses various costing

techniques to manage cost like managerial and absorption costing techniques. For planning

procedure company use different budget like operating, master and capital. To dealing with

financial problem company use different management accounting systems.

Companies utilise a variety of management accounting methodologies in the finance area. It

is an accountancy procedure in which accounting experts examine economic or non economic

information for internal managerial accounting purposes. This accountancy has a defined set

of roles and obligations for giant corporations. This report based on the IKEA Company

which is using management accounting to manage their financial information in effective

manner. In this report using various types of reports and systems like inventory management,

cost report and pricing optimising systems. Along with, company uses various costing

techniques to manage cost like managerial and absorption costing techniques. For planning

procedure company use different budget like operating, master and capital. To dealing with

financial problem company use different management accounting systems.

Table of Contents

INTRODUCTION.....................................................................................................................................3

P1: Management accounting explanation as well as key management accounting system needs .......3

P2: Various techniques of accounting applications...............................................................................5

P3: Calculate the price per unit using absorption as well as marginal costing. .....................................7

P4: An overview of both the benefits and drawbacks of various budget planning tools. ...................10

P5: Methods through which enterprises might utilise management accounting and address financial

issues ..................................................................................................................................................11

Conclusion ..........................................................................................................................................13

INTRODUCTION.....................................................................................................................................3

P1: Management accounting explanation as well as key management accounting system needs .......3

P2: Various techniques of accounting applications...............................................................................5

P3: Calculate the price per unit using absorption as well as marginal costing. .....................................7

P4: An overview of both the benefits and drawbacks of various budget planning tools. ...................10

P5: Methods through which enterprises might utilise management accounting and address financial

issues ..................................................................................................................................................11

Conclusion ..........................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting, often referred as managerial accounting, seems to be a

methodology that gives financial tools and help to administrators for making decisions

(Benjaafar and Hu, 2020). Management accounting is exclusively utilised by company's inner

staff, and that's the only difference between it and financial accounting. During this

procedure, finance management shares accounting records as well as statistics with business

unit head, such as invoices as well as corporate balance statements. The goal of managerial

accounting would be to use statistical data to make better and more accurate decisions about

the firm, business operations, as well as progress. Managerial accounting makes use of

numerous accounting and financial information to make important choices that affect the

growth of the organisation. It goes through numerous accounting processes with the goal of

delivering useful as well as correct information to the management authority in order for

them to better understand and analyse business operating metrics. Managerial accountants

analyse data linked to the cost of products sold and the company's sales revenue for goods

and services. Cost accounting is a subset of managerial accounting that focuses on finding as

well as capturing overall production costs by analysing the fixed costs and variable costs of

each manufacturing stage. This is beneficial to organs. The report has extensively have

included firm IKEA's managerial accounting procedure, which has secured an optimal

business performance in the fiscal years to assure good business growth. This report has

emphasised the debate about several financial accounting which have been assessed for

obtaining the specific judgement regarding the firm's good functioning. Various purposes of

management accounting reporting have been emphasised, and the correct features of using

their significance have been explored in the study.

P1: Management accounting explanation as well as key management accounting system

needs

Management accounting denotes to the accounting procedures that comprise the

integration of financial as well as non accounts with goal of providing the company more

effective decision-making possibilities (Hatchuel, and Segrestin, 2019). Accounting

information may be used by money planners to make informed decisions. Management

accounting is essential for managerial decision making, budgeting and monitoring

management systems, as well as unified financial statements. Management accounting is the

Management accounting, often referred as managerial accounting, seems to be a

methodology that gives financial tools and help to administrators for making decisions

(Benjaafar and Hu, 2020). Management accounting is exclusively utilised by company's inner

staff, and that's the only difference between it and financial accounting. During this

procedure, finance management shares accounting records as well as statistics with business

unit head, such as invoices as well as corporate balance statements. The goal of managerial

accounting would be to use statistical data to make better and more accurate decisions about

the firm, business operations, as well as progress. Managerial accounting makes use of

numerous accounting and financial information to make important choices that affect the

growth of the organisation. It goes through numerous accounting processes with the goal of

delivering useful as well as correct information to the management authority in order for

them to better understand and analyse business operating metrics. Managerial accountants

analyse data linked to the cost of products sold and the company's sales revenue for goods

and services. Cost accounting is a subset of managerial accounting that focuses on finding as

well as capturing overall production costs by analysing the fixed costs and variable costs of

each manufacturing stage. This is beneficial to organs. The report has extensively have

included firm IKEA's managerial accounting procedure, which has secured an optimal

business performance in the fiscal years to assure good business growth. This report has

emphasised the debate about several financial accounting which have been assessed for

obtaining the specific judgement regarding the firm's good functioning. Various purposes of

management accounting reporting have been emphasised, and the correct features of using

their significance have been explored in the study.

P1: Management accounting explanation as well as key management accounting system

needs

Management accounting denotes to the accounting procedures that comprise the

integration of financial as well as non accounts with goal of providing the company more

effective decision-making possibilities (Hatchuel, and Segrestin, 2019). Accounting

information may be used by money planners to make informed decisions. Management

accounting is essential for managerial decision making, budgeting and monitoring

management systems, as well as unified financial statements. Management accounting is the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

standard for providing a thorough description of revenue percentages, product offerings, and

client bases.

IKEA is now aiming to employ sophisticated management accounting for better

decision-making. Management accounting offers a thorough view of profit statistics, client

bases, goods and services; financial accounting aids in reporting and managing the business's

ultimate outcome (Shojaei. and Haeri, 2019). Financial accounting provides a clear view of

the company's financial situation, whereas managerial accounting identifies the root reasons

of managerial difficulties. Financial accounting aids in the preparation of financial

statements, whereas management accounting allows IKEA to concentrate solely on

operational reporting assigned inside the business. IKEA formerly had to conform with

numerous accounting standards; however, with the advancement of managerial accounting,

management no longer has to comply with any accounting rules if the data is utilised for

internal management as well as accounting reasons. As small and medium-sized businesses

face a plethora of accounting difficulties on a regular basis, managerial accounting is an

effective instrument that leverages accounting data and activities to provide an idea of the

business's profitability (Halkias and Neubert, 2020).

IKEA will be able to simply calculate the number of goods sold out using management

accounting. The accountant may simply calculate the associated expenses among the

advertising while ignoring the common expenditures. IKEA would indeed be able to identify

the actions for generating those product offerings across the world by implementing

managerial accounting approaches . Management accounting provides knowledge about

production and aids in the budgeting process for the ongoing development of management

processes.

Cost accounting, inventory management accounting, and task costing methods are the most

often utilised management accounting approaches (Al‐Dabbagh, 2020). IKEA will be able to

control overall management and operational expenses by documenting, analysing,

summarising, assigning, and classifying all activities through the use of cost accounting

techniques. Inventory management procedures are crucial for technology multinational

businesses such as IKEA since they allow the managerial accountant to understand when to

refill the inventory, the precise manufacturing volume, and so on. Inventory management

thus entails the act of storing and replenishing a firm's stock in order to enhance its

profitability. Another frequently utilised approach is job costing, which is a sort of

client bases.

IKEA is now aiming to employ sophisticated management accounting for better

decision-making. Management accounting offers a thorough view of profit statistics, client

bases, goods and services; financial accounting aids in reporting and managing the business's

ultimate outcome (Shojaei. and Haeri, 2019). Financial accounting provides a clear view of

the company's financial situation, whereas managerial accounting identifies the root reasons

of managerial difficulties. Financial accounting aids in the preparation of financial

statements, whereas management accounting allows IKEA to concentrate solely on

operational reporting assigned inside the business. IKEA formerly had to conform with

numerous accounting standards; however, with the advancement of managerial accounting,

management no longer has to comply with any accounting rules if the data is utilised for

internal management as well as accounting reasons. As small and medium-sized businesses

face a plethora of accounting difficulties on a regular basis, managerial accounting is an

effective instrument that leverages accounting data and activities to provide an idea of the

business's profitability (Halkias and Neubert, 2020).

IKEA will be able to simply calculate the number of goods sold out using management

accounting. The accountant may simply calculate the associated expenses among the

advertising while ignoring the common expenditures. IKEA would indeed be able to identify

the actions for generating those product offerings across the world by implementing

managerial accounting approaches . Management accounting provides knowledge about

production and aids in the budgeting process for the ongoing development of management

processes.

Cost accounting, inventory management accounting, and task costing methods are the most

often utilised management accounting approaches (Al‐Dabbagh, 2020). IKEA will be able to

control overall management and operational expenses by documenting, analysing,

summarising, assigning, and classifying all activities through the use of cost accounting

techniques. Inventory management procedures are crucial for technology multinational

businesses such as IKEA since they allow the managerial accountant to understand when to

refill the inventory, the precise manufacturing volume, and so on. Inventory management

thus entails the act of storing and replenishing a firm's stock in order to enhance its

profitability. Another frequently utilised approach is job costing, which is a sort of

accounting management technique that is primarily employed in machine production units

since the accountant can readily see the precise cost for each and every work. Because IKEA

manufacture goods, the accountant will be able to analyse the expenses for all distinct batches

by assigning overhead charges individually.

Inventory management system: This system is primarily used to maintain an organization's

inventory and stock levels, as well as to retain archives of all information and goods. It is

critical for businesses to recognize their clients' demands in terms of market growth and to

keep accurate records in order to deliver accurate information about stock availability and

unavailable. This is necessary for IKEA administration to keep track of stock levels and

process customer.

Cost accounting system: This is a structure that organisations are using to calculate and

evaluate the cost of its products in order to preserve competitiveness. It explains how and

where to deal with product costs that may occur and how to handle them correctly. IKEA

employs a cost accounting system to measure expenses and monitor progress through cost

identification. This is necessary for making the company more cost-effective and to increase

revenues by controlling expenditures.

Price optimization system: The price optimization method is a logical tool that is primarily

used to establish the cost of things and services offered by businesses. IKEA determines the

pricing of its items and services, which can assist in profit analysis. The primary goal of a

price optimization plan is to identify pricing and meet consumer needs by providing products.

Job costing system: This might be understood as a management accounting system that is

properly linked to the cost measuring procedure in each unit produced. The goal of MAS is to

assist in the reduction of total direct cost. This is not suitable for small businesses due to the

limited product choice. It's perfect for businesses with a diverse product line. This accounting

method is expanded in the case of IKEA to include the cost of the products manufactured by

the manufacturer.

P2: Various techniques of accounting applications

Budgetary control refers to a method in which budgets are utilised to forecast as well

as drive down costs. Budgeting specifies what must be accomplished and how it must be

accomplished, whereas control guarantees that goals are accomplished and that actual

outcomes do not stray from planned course more than required. A corporate firm's budget

since the accountant can readily see the precise cost for each and every work. Because IKEA

manufacture goods, the accountant will be able to analyse the expenses for all distinct batches

by assigning overhead charges individually.

Inventory management system: This system is primarily used to maintain an organization's

inventory and stock levels, as well as to retain archives of all information and goods. It is

critical for businesses to recognize their clients' demands in terms of market growth and to

keep accurate records in order to deliver accurate information about stock availability and

unavailable. This is necessary for IKEA administration to keep track of stock levels and

process customer.

Cost accounting system: This is a structure that organisations are using to calculate and

evaluate the cost of its products in order to preserve competitiveness. It explains how and

where to deal with product costs that may occur and how to handle them correctly. IKEA

employs a cost accounting system to measure expenses and monitor progress through cost

identification. This is necessary for making the company more cost-effective and to increase

revenues by controlling expenditures.

Price optimization system: The price optimization method is a logical tool that is primarily

used to establish the cost of things and services offered by businesses. IKEA determines the

pricing of its items and services, which can assist in profit analysis. The primary goal of a

price optimization plan is to identify pricing and meet consumer needs by providing products.

Job costing system: This might be understood as a management accounting system that is

properly linked to the cost measuring procedure in each unit produced. The goal of MAS is to

assist in the reduction of total direct cost. This is not suitable for small businesses due to the

limited product choice. It's perfect for businesses with a diverse product line. This accounting

method is expanded in the case of IKEA to include the cost of the products manufactured by

the manufacturer.

P2: Various techniques of accounting applications

Budgetary control refers to a method in which budgets are utilised to forecast as well

as drive down costs. Budgeting specifies what must be accomplished and how it must be

accomplished, whereas control guarantees that goals are accomplished and that actual

outcomes do not stray from planned course more than required. A corporate firm's budget

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

serves more or less the same objective like an individuals personal budget. Business budgets,

on the other hand, are more detailed and need more work than personal budgets. A company's

success doesn't really happen by chance. That is why budgeting is essential for all trade and

business organisations. The application of management accounting systems at IKEA will

enable accountants to portray administrative accounting data in an operational manner,

allowing the company to make strategic choices for the company's seamless transition. IKEA

lucrative operations are clearly apparent to stakeholders thanks to the implementation of

management accounting methods (Edwards Jr, 2019). Managerial accounting reports are

classified into four categories: accounting information, receivables reports, work cost reports,

plus inventory as well as manufacturing reports.

The following are some of the advantages of using management accounting at IKEA:-

1. A managerial accounting increases the computing technology firm's overall efficiency in

completing its essential activities.

2. Because managerial accounting incorporates budgeting process, it aids in budgetary

control procedures. Through this procedure, the firm will be able to separate total expenses

into operating and investment operations.

3. Accounting management aids in administrative choices by providing easy reporting of

income statement and a clear & distinctive opportunity for investors to analyse the company's

financial status.

4. By utilising managerial accounting at IKEA., management may readily collaborate with

IT department while also ensuring budgetary activities. This guarantees that the company's

costs are transparent (Keegan, Brandl and Aust, 2019).

Inventory management report: This report is recommended for organisations that

manufacture physical things and inventory, or are involved in the flow of goods and services

with a variety of challenges. It is developed to analyse difficulties, expenses associated with

each manufacturing output, worker expenditures, and overheads associated with these

operations. In the case of IKEA, this aids in the analysis of data on stock levels, personnel,

and other overhead expenses associated with the manufacturing process. Input data or

information are utilised to optimise the manufacturing and mechanical processes in this

study. It gives a detailed overview of different commodities' inventory or availability.

on the other hand, are more detailed and need more work than personal budgets. A company's

success doesn't really happen by chance. That is why budgeting is essential for all trade and

business organisations. The application of management accounting systems at IKEA will

enable accountants to portray administrative accounting data in an operational manner,

allowing the company to make strategic choices for the company's seamless transition. IKEA

lucrative operations are clearly apparent to stakeholders thanks to the implementation of

management accounting methods (Edwards Jr, 2019). Managerial accounting reports are

classified into four categories: accounting information, receivables reports, work cost reports,

plus inventory as well as manufacturing reports.

The following are some of the advantages of using management accounting at IKEA:-

1. A managerial accounting increases the computing technology firm's overall efficiency in

completing its essential activities.

2. Because managerial accounting incorporates budgeting process, it aids in budgetary

control procedures. Through this procedure, the firm will be able to separate total expenses

into operating and investment operations.

3. Accounting management aids in administrative choices by providing easy reporting of

income statement and a clear & distinctive opportunity for investors to analyse the company's

financial status.

4. By utilising managerial accounting at IKEA., management may readily collaborate with

IT department while also ensuring budgetary activities. This guarantees that the company's

costs are transparent (Keegan, Brandl and Aust, 2019).

Inventory management report: This report is recommended for organisations that

manufacture physical things and inventory, or are involved in the flow of goods and services

with a variety of challenges. It is developed to analyse difficulties, expenses associated with

each manufacturing output, worker expenditures, and overheads associated with these

operations. In the case of IKEA, this aids in the analysis of data on stock levels, personnel,

and other overhead expenses associated with the manufacturing process. Input data or

information are utilised to optimise the manufacturing and mechanical processes in this

study. It gives a detailed overview of different commodities' inventory or availability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance report: It is critical for management to framework to analyse progress and

offer satisfaction level through incentives. This report is used to assess effectiveness and

improve inspiration so that employees stay on for the long run. Administration at IKEA

prepares a performance evaluation that may be used to assess how workers work and how

quickly they finish their tasks. Workers are also motivated by administration to accept needs

and develop organizational effectiveness.

Cost managerial accounting report: Accounting cost management is a type of management

accounting that aims to assist entrepreneurs in forecasting their expenditures. The goal of this

accounting report is to keep organisations from exceeding the budget. Accounting

information at IKEA is concerned with the measurement and evaluation of fees and expenses

associated with the procurement or production of a product. Its main goal is to help

management make better decisions by calculating per unit price using various costing

approaches.

Job costing report: Job costing is a type of accounting that records expenses and revenues

by "task," allowing for uniform reporting of profit per job. An accountancy system should

allow employment figures to also be allocated to specific items of costs and revenues in order

to support job costing. Job Cost reports will provide IKEA managers with a systematic

evaluation of overall costs for various projects. In comparison to revenue reports, the extra

expenses incurred for production procedures for products.

M1 Benefits of management accounting

System Benefits and application

Cost accounting This has the advantage of allowing you to estimate the cost of

items and activities, making it easier to compute earnings. IKEA

is using this to learn more about making investments and making

profits in this industry.

Inventory management This can aid in inventory tracking and offer accurate easy

accessibility and just out items. This is used by IKEA's

management to receive data on the company's inventories and

operations.

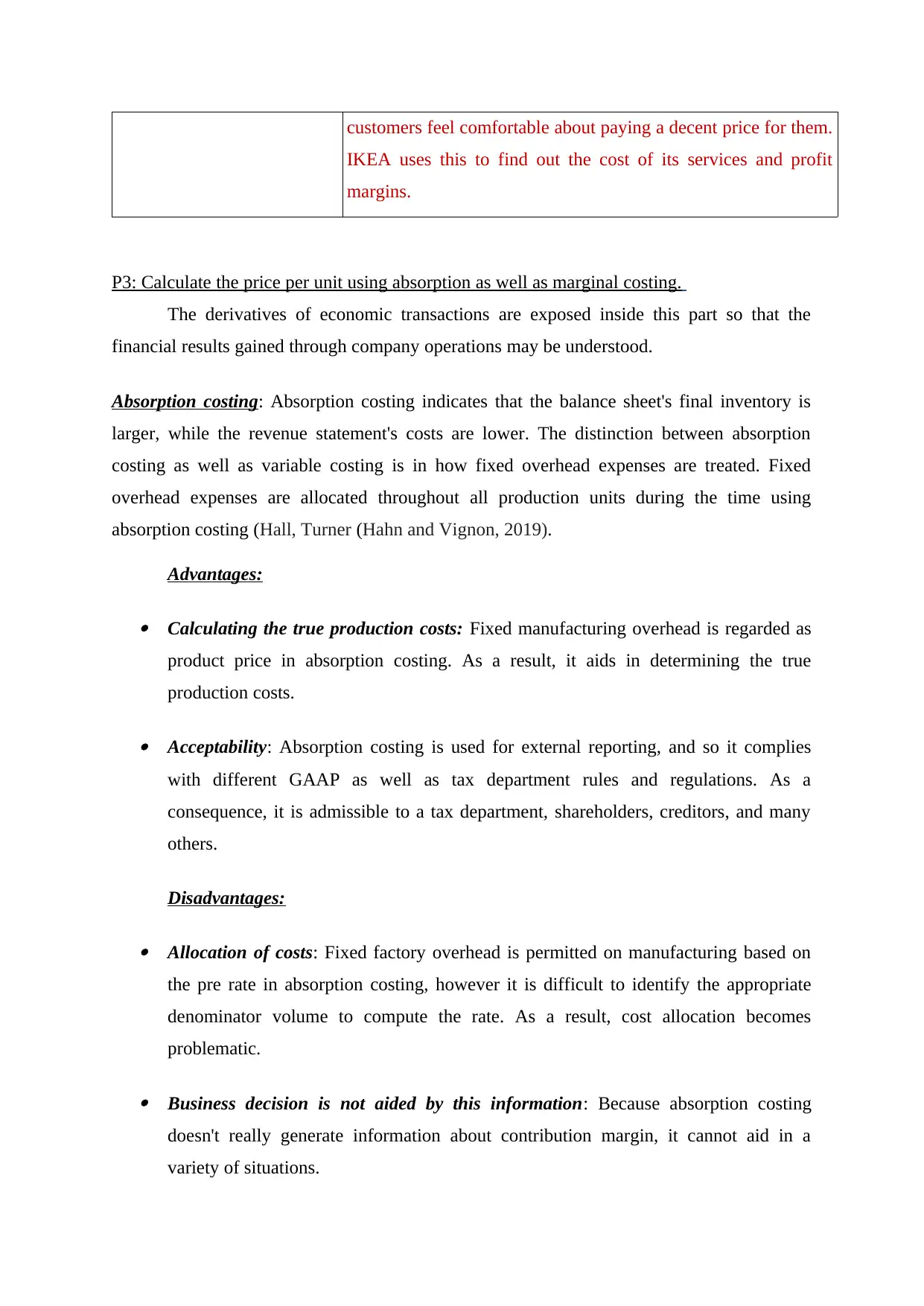

Price optimisation This can assist determine the proper price for items so that

offer satisfaction level through incentives. This report is used to assess effectiveness and

improve inspiration so that employees stay on for the long run. Administration at IKEA

prepares a performance evaluation that may be used to assess how workers work and how

quickly they finish their tasks. Workers are also motivated by administration to accept needs

and develop organizational effectiveness.

Cost managerial accounting report: Accounting cost management is a type of management

accounting that aims to assist entrepreneurs in forecasting their expenditures. The goal of this

accounting report is to keep organisations from exceeding the budget. Accounting

information at IKEA is concerned with the measurement and evaluation of fees and expenses

associated with the procurement or production of a product. Its main goal is to help

management make better decisions by calculating per unit price using various costing

approaches.

Job costing report: Job costing is a type of accounting that records expenses and revenues

by "task," allowing for uniform reporting of profit per job. An accountancy system should

allow employment figures to also be allocated to specific items of costs and revenues in order

to support job costing. Job Cost reports will provide IKEA managers with a systematic

evaluation of overall costs for various projects. In comparison to revenue reports, the extra

expenses incurred for production procedures for products.

M1 Benefits of management accounting

System Benefits and application

Cost accounting This has the advantage of allowing you to estimate the cost of

items and activities, making it easier to compute earnings. IKEA

is using this to learn more about making investments and making

profits in this industry.

Inventory management This can aid in inventory tracking and offer accurate easy

accessibility and just out items. This is used by IKEA's

management to receive data on the company's inventories and

operations.

Price optimisation This can assist determine the proper price for items so that

customers feel comfortable about paying a decent price for them.

IKEA uses this to find out the cost of its services and profit

margins.

P3: Calculate the price per unit using absorption as well as marginal costing.

The derivatives of economic transactions are exposed inside this part so that the

financial results gained through company operations may be understood.

Absorption costing: Absorption costing indicates that the balance sheet's final inventory is

larger, while the revenue statement's costs are lower. The distinction between absorption

costing as well as variable costing is in how fixed overhead expenses are treated. Fixed

overhead expenses are allocated throughout all production units during the time using

absorption costing (Hall, Turner (Hahn and Vignon, 2019).

Advantages:

Calculating the true production costs: Fixed manufacturing overhead is regarded as

product price in absorption costing. As a result, it aids in determining the true

production costs.

Acceptability: Absorption costing is used for external reporting, and so it complies

with different GAAP as well as tax department rules and regulations. As a

consequence, it is admissible to a tax department, shareholders, creditors, and many

others.

Disadvantages:

Allocation of costs: Fixed factory overhead is permitted on manufacturing based on

the pre rate in absorption costing, however it is difficult to identify the appropriate

denominator volume to compute the rate. As a result, cost allocation becomes

problematic.

Business decision is not aided by this information: Because absorption costing

doesn't really generate information about contribution margin, it cannot aid in a

variety of situations.

IKEA uses this to find out the cost of its services and profit

margins.

P3: Calculate the price per unit using absorption as well as marginal costing.

The derivatives of economic transactions are exposed inside this part so that the

financial results gained through company operations may be understood.

Absorption costing: Absorption costing indicates that the balance sheet's final inventory is

larger, while the revenue statement's costs are lower. The distinction between absorption

costing as well as variable costing is in how fixed overhead expenses are treated. Fixed

overhead expenses are allocated throughout all production units during the time using

absorption costing (Hall, Turner (Hahn and Vignon, 2019).

Advantages:

Calculating the true production costs: Fixed manufacturing overhead is regarded as

product price in absorption costing. As a result, it aids in determining the true

production costs.

Acceptability: Absorption costing is used for external reporting, and so it complies

with different GAAP as well as tax department rules and regulations. As a

consequence, it is admissible to a tax department, shareholders, creditors, and many

others.

Disadvantages:

Allocation of costs: Fixed factory overhead is permitted on manufacturing based on

the pre rate in absorption costing, however it is difficult to identify the appropriate

denominator volume to compute the rate. As a result, cost allocation becomes

problematic.

Business decision is not aided by this information: Because absorption costing

doesn't really generate information about contribution margin, it cannot aid in a

variety of situations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

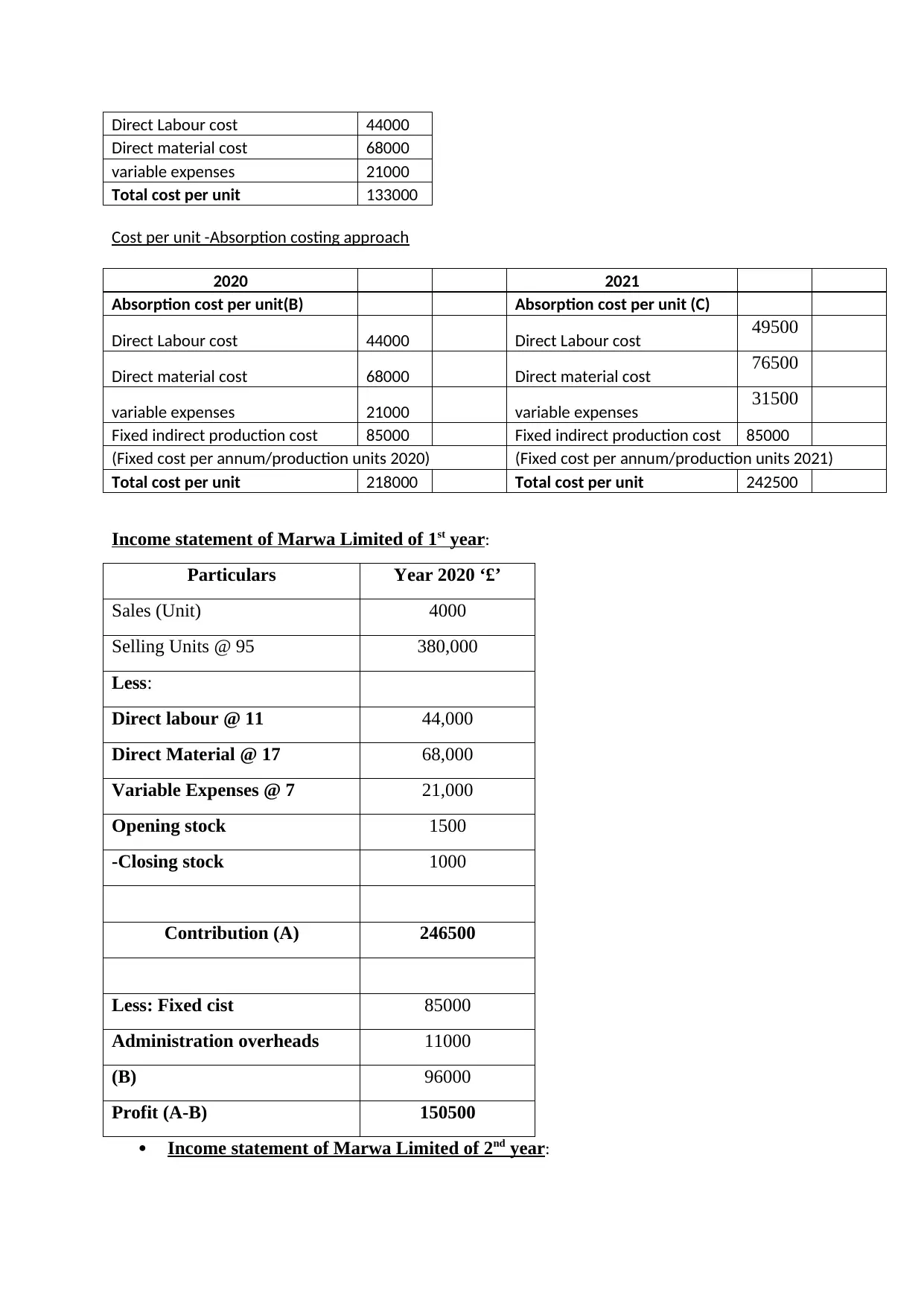

Marginal costing: The idea of marginal costing states all variable expenses are

charged to cost units and fixed costs related to the period covered are wiped off in whole

against with the contributions for said period. The determination of marginal cost as well as

the impact on profitability of volume changes or kind of production by distinguishing among

variable and fixed is known as marginal costing. Costs can be divided into variable and fixed

costs in marginal costing.

Advantages:

Easy: This is easy to grasp as well as quick to calculate, so everyone can grasp it.

Decision making: It aids in decision making, such as calculating profitability,

estimating the selling price of a product, deciding whether it should buy or produce a

product, and deciding whether to use the firm's spare capacity (Weitzner and Deutsch,

2019).

Disadvantages:

Ignorance: In marginal costing, all expenses are categorised either as fixed or

variable, whereas semi-variable costs are ignored.

Fixed cost is not consider: It is not appropriate for businesses with significant fixed

costs per unit since it solely considers variable costs per unit.

Calculate opening and closing inventory units

2020 2021

Opening

stock 1,500.00 1000

production 3,500.00 4,200.00

sales 4,000.00 4,500.00

closing stock 1000 700

2. Calculate cost per unit using marginal costing and absorption costing approach

Cost per unit -Marginal costing approach

2020/2021

Marginal cost per unit (A)

charged to cost units and fixed costs related to the period covered are wiped off in whole

against with the contributions for said period. The determination of marginal cost as well as

the impact on profitability of volume changes or kind of production by distinguishing among

variable and fixed is known as marginal costing. Costs can be divided into variable and fixed

costs in marginal costing.

Advantages:

Easy: This is easy to grasp as well as quick to calculate, so everyone can grasp it.

Decision making: It aids in decision making, such as calculating profitability,

estimating the selling price of a product, deciding whether it should buy or produce a

product, and deciding whether to use the firm's spare capacity (Weitzner and Deutsch,

2019).

Disadvantages:

Ignorance: In marginal costing, all expenses are categorised either as fixed or

variable, whereas semi-variable costs are ignored.

Fixed cost is not consider: It is not appropriate for businesses with significant fixed

costs per unit since it solely considers variable costs per unit.

Calculate opening and closing inventory units

2020 2021

Opening

stock 1,500.00 1000

production 3,500.00 4,200.00

sales 4,000.00 4,500.00

closing stock 1000 700

2. Calculate cost per unit using marginal costing and absorption costing approach

Cost per unit -Marginal costing approach

2020/2021

Marginal cost per unit (A)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct Labour cost 44000

Direct material cost 68000

variable expenses 21000

Total cost per unit 133000

Cost per unit -Absorption costing approach

2020 2021

Absorption cost per unit(B) Absorption cost per unit (C)

Direct Labour cost 44000 Direct Labour cost 49500

Direct material cost 68000 Direct material cost 76500

variable expenses 21000 variable expenses 31500

Fixed indirect production cost 85000 Fixed indirect production cost 85000

(Fixed cost per annum/production units 2020) (Fixed cost per annum/production units 2021)

Total cost per unit 218000 Total cost per unit 242500

Income statement of Marwa Limited of 1st year:

Particulars Year 2020 ‘£’

Sales (Unit) 4000

Selling Units @ 95 380,000

Less:

Direct labour @ 11 44,000

Direct Material @ 17 68,000

Variable Expenses @ 7 21,000

Opening stock 1500

-Closing stock 1000

Contribution (A) 246500

Less: Fixed cist 85000

Administration overheads 11000

(B) 96000

Profit (A-B) 150500

Income statement of Marwa Limited of 2nd year:

Direct material cost 68000

variable expenses 21000

Total cost per unit 133000

Cost per unit -Absorption costing approach

2020 2021

Absorption cost per unit(B) Absorption cost per unit (C)

Direct Labour cost 44000 Direct Labour cost 49500

Direct material cost 68000 Direct material cost 76500

variable expenses 21000 variable expenses 31500

Fixed indirect production cost 85000 Fixed indirect production cost 85000

(Fixed cost per annum/production units 2020) (Fixed cost per annum/production units 2021)

Total cost per unit 218000 Total cost per unit 242500

Income statement of Marwa Limited of 1st year:

Particulars Year 2020 ‘£’

Sales (Unit) 4000

Selling Units @ 95 380,000

Less:

Direct labour @ 11 44,000

Direct Material @ 17 68,000

Variable Expenses @ 7 21,000

Opening stock 1500

-Closing stock 1000

Contribution (A) 246500

Less: Fixed cist 85000

Administration overheads 11000

(B) 96000

Profit (A-B) 150500

Income statement of Marwa Limited of 2nd year:

Particulars Year 2021 ‘£’

Sales (Unit) 4500

Selling Units @ 95 427500

Less:

Direct labour @ 11 49500

Direct Material @ 17 76500

Variable Expenses @ 7 31500

Opening stock 1000

-Closing stock 700

Contribution (A) 269700

Less: Fixed cist 85000

Administration overheads 11000

(B) 96000

Profit (A-B) 258700

Absorption costing:

Income statement of Aarwa Limited of 1st year:

Particulars Year 2020 ‘£’

Production Units 3600

Direct material @ 11 39,600

Direct material @ 17 61,200

Variable expense @ 7 25,200

Fixed indirect production cost 84,000

Total Production cost 210,000

Sales (Unit) 4500

Selling Units @ 95 427500

Less:

Direct labour @ 11 49500

Direct Material @ 17 76500

Variable Expenses @ 7 31500

Opening stock 1000

-Closing stock 700

Contribution (A) 269700

Less: Fixed cist 85000

Administration overheads 11000

(B) 96000

Profit (A-B) 258700

Absorption costing:

Income statement of Aarwa Limited of 1st year:

Particulars Year 2020 ‘£’

Production Units 3600

Direct material @ 11 39,600

Direct material @ 17 61,200

Variable expense @ 7 25,200

Fixed indirect production cost 84,000

Total Production cost 210,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.