IKEA Management Accounting Report: Costing, Planning, and Control

VerifiedAdded on 2022/12/26

|17

|3975

|64

Report

AI Summary

This report provides a comprehensive analysis of IKEA's management accounting practices. It begins with an introduction to management accounting and its significance in business decision-making, focusing on cost accounting, job costing, inventory management, and price optimization systems. The report then explores various managerial accounting reports, including cost reports, budget reports, and inventory reports, highlighting their roles in planning, controlling, and measuring financial performance. A significant portion of the report is dedicated to assessing costs using absorption and marginal costing systems, providing detailed calculations and interpretations. Finally, it examines the advantages and disadvantages of different planning tools used for budgetary control, such as cash budgets and operating budgets, and compares how different types of management accounting systems can be used for responding to monetary problems. The report aims to provide insights into IKEA's financial strategies and the application of management accounting principles in a real-world business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

P1 Explaining management accounting and essential requirements pertaining to different types

of systems....................................................................................................................................3

P2 Explaining different methods that can be used for managerial accounting reports...............5

P3 Assessing cost using absorption and marginal costing systems.............................................6

P4 Explaining advantages and disadvantages of different planning tools used for budgetary

control..........................................................................................................................................9

P5 comparing how different types of management accounting systems can be used for

responding monetary problems..................................................................................................11

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

P1 Explaining management accounting and essential requirements pertaining to different types

of systems....................................................................................................................................3

P2 Explaining different methods that can be used for managerial accounting reports...............5

P3 Assessing cost using absorption and marginal costing systems.............................................6

P4 Explaining advantages and disadvantages of different planning tools used for budgetary

control..........................................................................................................................................9

P5 comparing how different types of management accounting systems can be used for

responding monetary problems..................................................................................................11

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting refers to the process of assessing, evaluating, interpreting and

communicating monetary information to the managers for ensuring effectual decision making. In

the context of business organization, management accounting is highly significant which helps

management team in getting deeper insight about business operations. By taking into account

managerial report firm can develop competent framework and thereby facilitates achievement of

goals. The present report is based on the case scenario of Ikea which provides customers with

unique furniture at suitable prices. This report will develop understanding about the concepts of

managerial accounting and reports used for decision making purpose. Further, report will shed

light on how absorption and marginal costing method helps in identifying cost and profitability

associated with particular operations. In addition to this, it highlights several tools which can be

used by Ikea for planning and resolving financial problem that occurs within business.

P1 Explaining management accounting and essential requirements pertaining to different types

of systems

Cost accounting

This system implies for the framework which is undertaken by the company for

analyzing cost and profit margin of per unit (What is a Cost Accounting System?, 2020). Hence,

by recording and summing up all the cost of production total expenditure can be find out. Thus,

referring below mentioned formulas Ikea can set prices for its offerings.

Cost per unit (CPU) = Total cost / number of units produced

Profit = CPU + (CPU * profit%)

Ikea can use results derived through cost accounting as a benchmark for comparing

current performance. This in turn enables firm to take corrective measures on time as per the

deviations assessed.

Advantages Disadvantages

Helps in reducing cost and enhances

profitability

This system is more complex as it’s

based on estimation level.

Management accounting refers to the process of assessing, evaluating, interpreting and

communicating monetary information to the managers for ensuring effectual decision making. In

the context of business organization, management accounting is highly significant which helps

management team in getting deeper insight about business operations. By taking into account

managerial report firm can develop competent framework and thereby facilitates achievement of

goals. The present report is based on the case scenario of Ikea which provides customers with

unique furniture at suitable prices. This report will develop understanding about the concepts of

managerial accounting and reports used for decision making purpose. Further, report will shed

light on how absorption and marginal costing method helps in identifying cost and profitability

associated with particular operations. In addition to this, it highlights several tools which can be

used by Ikea for planning and resolving financial problem that occurs within business.

P1 Explaining management accounting and essential requirements pertaining to different types

of systems

Cost accounting

This system implies for the framework which is undertaken by the company for

analyzing cost and profit margin of per unit (What is a Cost Accounting System?, 2020). Hence,

by recording and summing up all the cost of production total expenditure can be find out. Thus,

referring below mentioned formulas Ikea can set prices for its offerings.

Cost per unit (CPU) = Total cost / number of units produced

Profit = CPU + (CPU * profit%)

Ikea can use results derived through cost accounting as a benchmark for comparing

current performance. This in turn enables firm to take corrective measures on time as per the

deviations assessed.

Advantages Disadvantages

Helps in reducing cost and enhances

profitability

This system is more complex as it’s

based on estimation level.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Helps manager in ascertaining reasons

behind profit or loss

Assists in setting appropriate price by

exerting control on cost

Usually cost is absorbed on pre-decided

rate which in turn leads problem of

under or over absorption.

Expensive in nature as it requires high

maintenance of cost accounting

records.

Job costing system: It provides information about the cost related to specific job either

production or service. Ikea can use job accounting system when there is a need in relation to

submitting cost information to the customer for cost reimbursement (Job costing, 2021).

Advantages Disadvantages

It facilitates comparison of cost and

profit pertaining to specific job.

Referring job costing framework

manager can draft suitable budget for

the upcoming time period.

Due to the inclusion of more clerical

work it is considered as time intensive

exercise.

Avoids cost control as in this after

manufacturing cost is recorded.

Inventory management system: It may be served as an approach to source, store and

sell both raw material and finished stock. By using FIFO, LIFO and WACM firm can do

better valuation of inventory takes place within an organization. In addition to this, EOQ, JIT

etc are the most effectual methods which help company in identifying the level of stock that

need to maintained for ensuring smooth functioning of business activities (Fleischman and

McLean, 2020).

Advantages Disadvantages

Increases operational efficiency by

saving both cost and time.

Ensures uninterrupted production by

It eliminates business risk to the limited

extent.

behind profit or loss

Assists in setting appropriate price by

exerting control on cost

Usually cost is absorbed on pre-decided

rate which in turn leads problem of

under or over absorption.

Expensive in nature as it requires high

maintenance of cost accounting

records.

Job costing system: It provides information about the cost related to specific job either

production or service. Ikea can use job accounting system when there is a need in relation to

submitting cost information to the customer for cost reimbursement (Job costing, 2021).

Advantages Disadvantages

It facilitates comparison of cost and

profit pertaining to specific job.

Referring job costing framework

manager can draft suitable budget for

the upcoming time period.

Due to the inclusion of more clerical

work it is considered as time intensive

exercise.

Avoids cost control as in this after

manufacturing cost is recorded.

Inventory management system: It may be served as an approach to source, store and

sell both raw material and finished stock. By using FIFO, LIFO and WACM firm can do

better valuation of inventory takes place within an organization. In addition to this, EOQ, JIT

etc are the most effectual methods which help company in identifying the level of stock that

need to maintained for ensuring smooth functioning of business activities (Fleischman and

McLean, 2020).

Advantages Disadvantages

Increases operational efficiency by

saving both cost and time.

Ensures uninterrupted production by

It eliminates business risk to the limited

extent.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

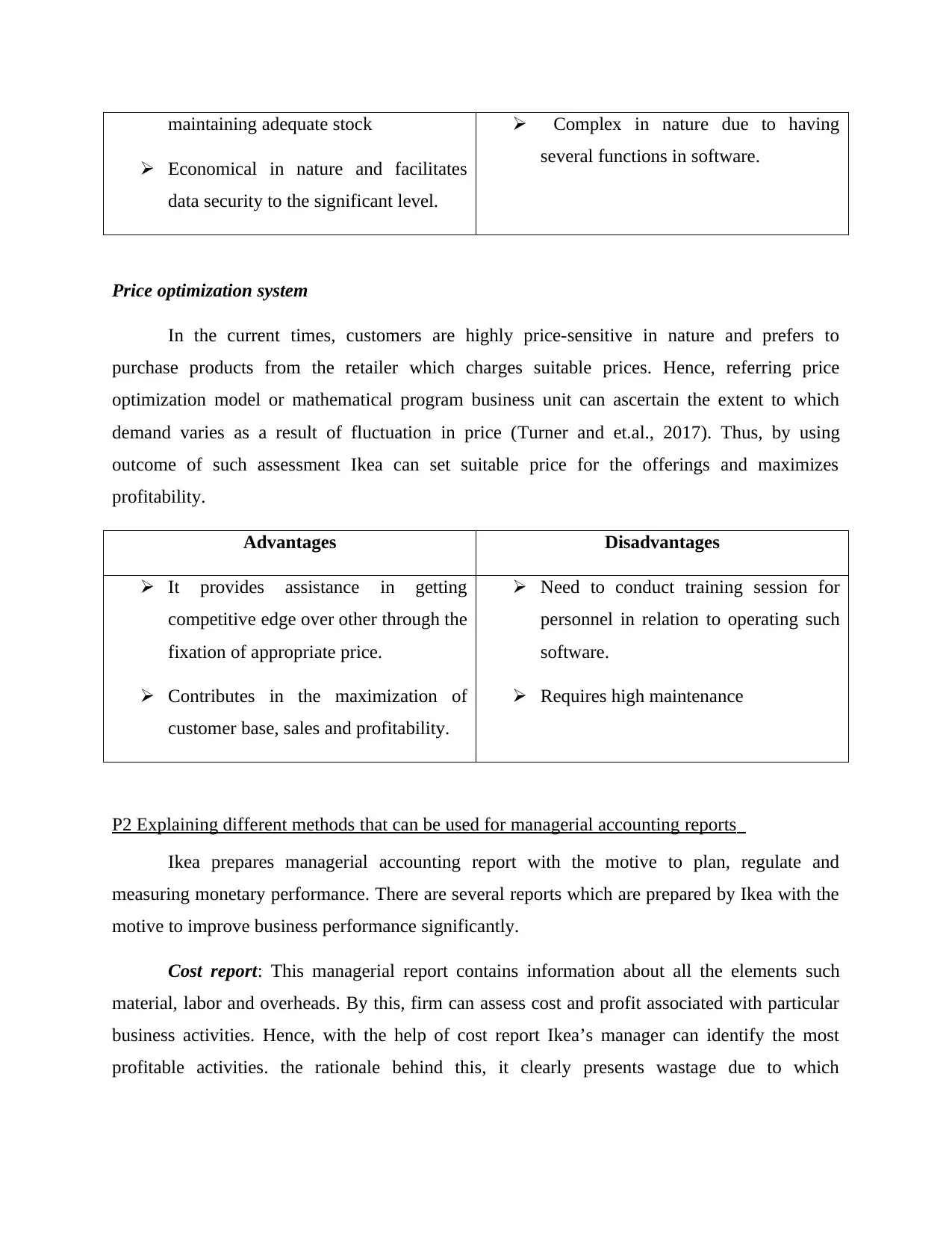

maintaining adequate stock

Economical in nature and facilitates

data security to the significant level.

Complex in nature due to having

several functions in software.

Price optimization system

In the current times, customers are highly price-sensitive in nature and prefers to

purchase products from the retailer which charges suitable prices. Hence, referring price

optimization model or mathematical program business unit can ascertain the extent to which

demand varies as a result of fluctuation in price (Turner and et.al., 2017). Thus, by using

outcome of such assessment Ikea can set suitable price for the offerings and maximizes

profitability.

Advantages Disadvantages

It provides assistance in getting

competitive edge over other through the

fixation of appropriate price.

Contributes in the maximization of

customer base, sales and profitability.

Need to conduct training session for

personnel in relation to operating such

software.

Requires high maintenance

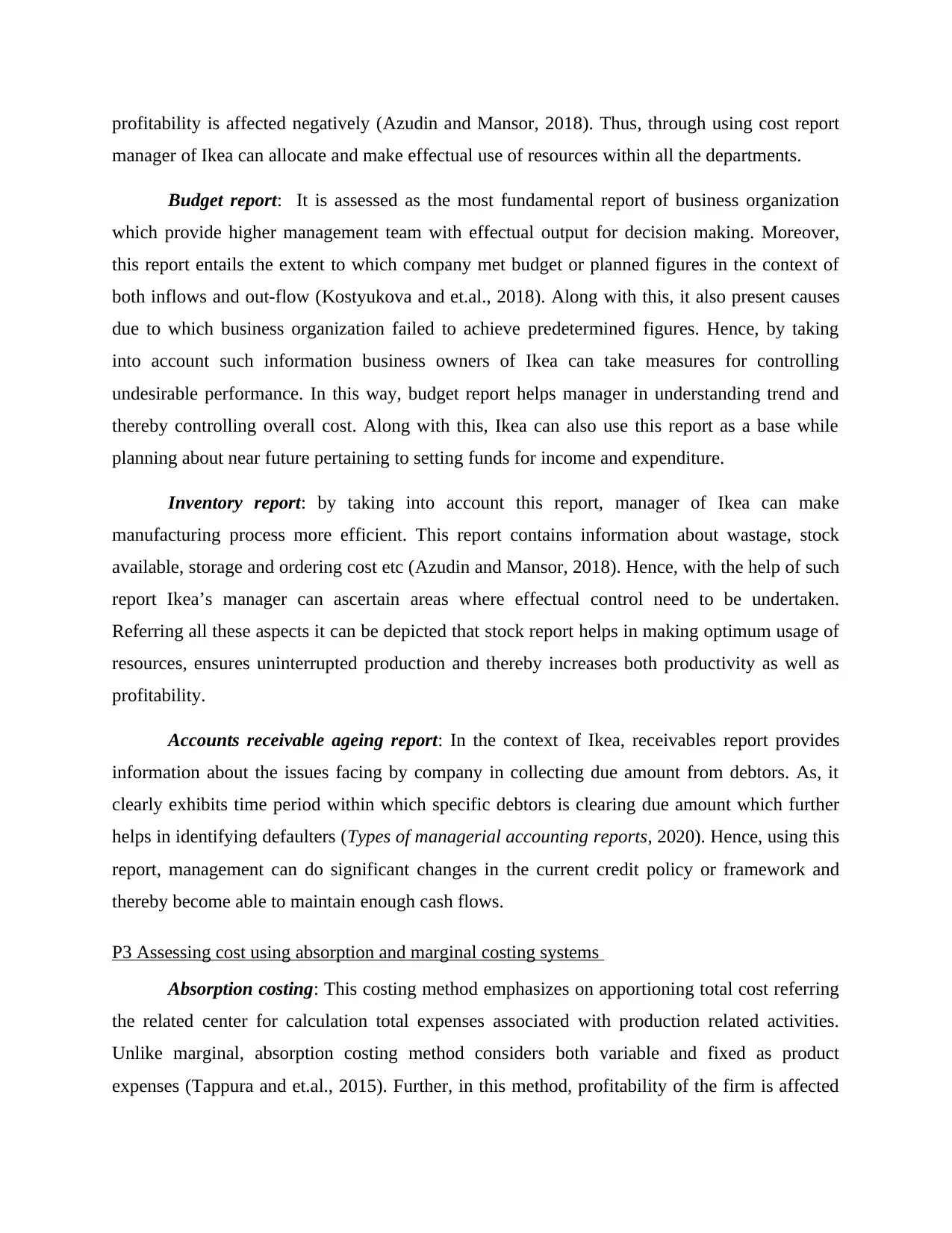

P2 Explaining different methods that can be used for managerial accounting reports

Ikea prepares managerial accounting report with the motive to plan, regulate and

measuring monetary performance. There are several reports which are prepared by Ikea with the

motive to improve business performance significantly.

Cost report: This managerial report contains information about all the elements such

material, labor and overheads. By this, firm can assess cost and profit associated with particular

business activities. Hence, with the help of cost report Ikea’s manager can identify the most

profitable activities. the rationale behind this, it clearly presents wastage due to which

Economical in nature and facilitates

data security to the significant level.

Complex in nature due to having

several functions in software.

Price optimization system

In the current times, customers are highly price-sensitive in nature and prefers to

purchase products from the retailer which charges suitable prices. Hence, referring price

optimization model or mathematical program business unit can ascertain the extent to which

demand varies as a result of fluctuation in price (Turner and et.al., 2017). Thus, by using

outcome of such assessment Ikea can set suitable price for the offerings and maximizes

profitability.

Advantages Disadvantages

It provides assistance in getting

competitive edge over other through the

fixation of appropriate price.

Contributes in the maximization of

customer base, sales and profitability.

Need to conduct training session for

personnel in relation to operating such

software.

Requires high maintenance

P2 Explaining different methods that can be used for managerial accounting reports

Ikea prepares managerial accounting report with the motive to plan, regulate and

measuring monetary performance. There are several reports which are prepared by Ikea with the

motive to improve business performance significantly.

Cost report: This managerial report contains information about all the elements such

material, labor and overheads. By this, firm can assess cost and profit associated with particular

business activities. Hence, with the help of cost report Ikea’s manager can identify the most

profitable activities. the rationale behind this, it clearly presents wastage due to which

profitability is affected negatively (Azudin and Mansor, 2018). Thus, through using cost report

manager of Ikea can allocate and make effectual use of resources within all the departments.

Budget report: It is assessed as the most fundamental report of business organization

which provide higher management team with effectual output for decision making. Moreover,

this report entails the extent to which company met budget or planned figures in the context of

both inflows and out-flow (Kostyukova and et.al., 2018). Along with this, it also present causes

due to which business organization failed to achieve predetermined figures. Hence, by taking

into account such information business owners of Ikea can take measures for controlling

undesirable performance. In this way, budget report helps manager in understanding trend and

thereby controlling overall cost. Along with this, Ikea can also use this report as a base while

planning about near future pertaining to setting funds for income and expenditure.

Inventory report: by taking into account this report, manager of Ikea can make

manufacturing process more efficient. This report contains information about wastage, stock

available, storage and ordering cost etc (Azudin and Mansor, 2018). Hence, with the help of such

report Ikea’s manager can ascertain areas where effectual control need to be undertaken.

Referring all these aspects it can be depicted that stock report helps in making optimum usage of

resources, ensures uninterrupted production and thereby increases both productivity as well as

profitability.

Accounts receivable ageing report: In the context of Ikea, receivables report provides

information about the issues facing by company in collecting due amount from debtors. As, it

clearly exhibits time period within which specific debtors is clearing due amount which further

helps in identifying defaulters (Types of managerial accounting reports, 2020). Hence, using this

report, management can do significant changes in the current credit policy or framework and

thereby become able to maintain enough cash flows.

P3 Assessing cost using absorption and marginal costing systems

Absorption costing: This costing method emphasizes on apportioning total cost referring

the related center for calculation total expenses associated with production related activities.

Unlike marginal, absorption costing method considers both variable and fixed as product

expenses (Tappura and et.al., 2015). Further, in this method, profitability of the firm is affected

manager of Ikea can allocate and make effectual use of resources within all the departments.

Budget report: It is assessed as the most fundamental report of business organization

which provide higher management team with effectual output for decision making. Moreover,

this report entails the extent to which company met budget or planned figures in the context of

both inflows and out-flow (Kostyukova and et.al., 2018). Along with this, it also present causes

due to which business organization failed to achieve predetermined figures. Hence, by taking

into account such information business owners of Ikea can take measures for controlling

undesirable performance. In this way, budget report helps manager in understanding trend and

thereby controlling overall cost. Along with this, Ikea can also use this report as a base while

planning about near future pertaining to setting funds for income and expenditure.

Inventory report: by taking into account this report, manager of Ikea can make

manufacturing process more efficient. This report contains information about wastage, stock

available, storage and ordering cost etc (Azudin and Mansor, 2018). Hence, with the help of such

report Ikea’s manager can ascertain areas where effectual control need to be undertaken.

Referring all these aspects it can be depicted that stock report helps in making optimum usage of

resources, ensures uninterrupted production and thereby increases both productivity as well as

profitability.

Accounts receivable ageing report: In the context of Ikea, receivables report provides

information about the issues facing by company in collecting due amount from debtors. As, it

clearly exhibits time period within which specific debtors is clearing due amount which further

helps in identifying defaulters (Types of managerial accounting reports, 2020). Hence, using this

report, management can do significant changes in the current credit policy or framework and

thereby become able to maintain enough cash flows.

P3 Assessing cost using absorption and marginal costing systems

Absorption costing: This costing method emphasizes on apportioning total cost referring

the related center for calculation total expenses associated with production related activities.

Unlike marginal, absorption costing method considers both variable and fixed as product

expenses (Tappura and et.al., 2015). Further, in this method, profitability of the firm is affected

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

due to the inclusion of fixed expenses. In this, data pertaining to the cost is presented in

conventional manner and presents net profit associated with the related activities.

Marginal costing: It may be presented as a technique which helps in determining

production cost and thereby contributes in decision making. In this, variable cost is considered

related to product, whereas fixed expenses treated as periodical one (Rikhardsson and

Yigitbasioglu, 2018). Manager of business unit can ascertain profitability using PV ratio and lays

focus on highlighting contribution.

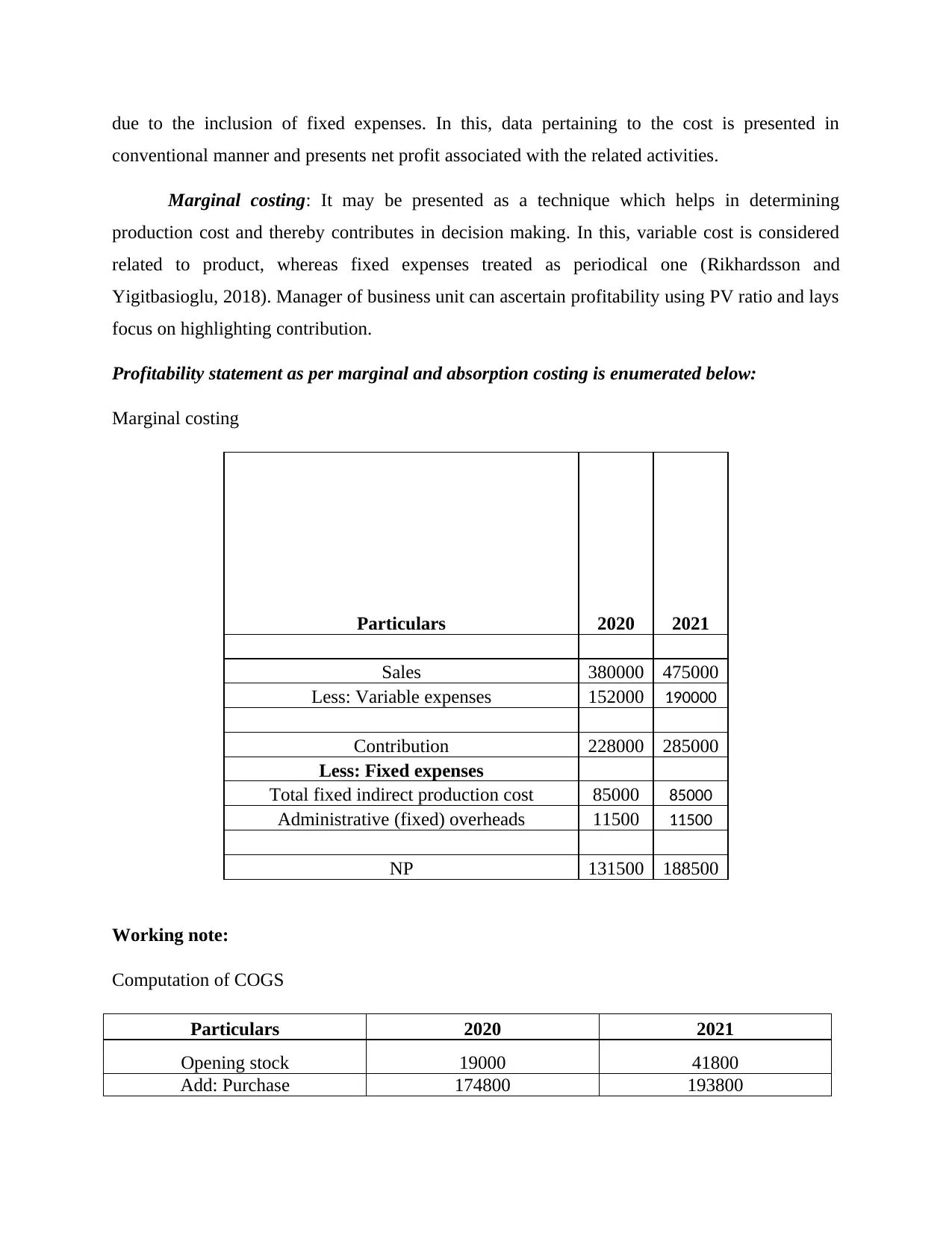

Profitability statement as per marginal and absorption costing is enumerated below:

Marginal costing

Particulars 2020 2021

Sales 380000 475000

Less: Variable expenses 152000 190000

Contribution 228000 285000

Less: Fixed expenses

Total fixed indirect production cost 85000 85000

Administrative (fixed) overheads 11500 11500

NP 131500 188500

Working note:

Computation of COGS

Particulars 2020 2021

Opening stock 19000 41800

Add: Purchase 174800 193800

conventional manner and presents net profit associated with the related activities.

Marginal costing: It may be presented as a technique which helps in determining

production cost and thereby contributes in decision making. In this, variable cost is considered

related to product, whereas fixed expenses treated as periodical one (Rikhardsson and

Yigitbasioglu, 2018). Manager of business unit can ascertain profitability using PV ratio and lays

focus on highlighting contribution.

Profitability statement as per marginal and absorption costing is enumerated below:

Marginal costing

Particulars 2020 2021

Sales 380000 475000

Less: Variable expenses 152000 190000

Contribution 228000 285000

Less: Fixed expenses

Total fixed indirect production cost 85000 85000

Administrative (fixed) overheads 11500 11500

NP 131500 188500

Working note:

Computation of COGS

Particulars 2020 2021

Opening stock 19000 41800

Add: Purchase 174800 193800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

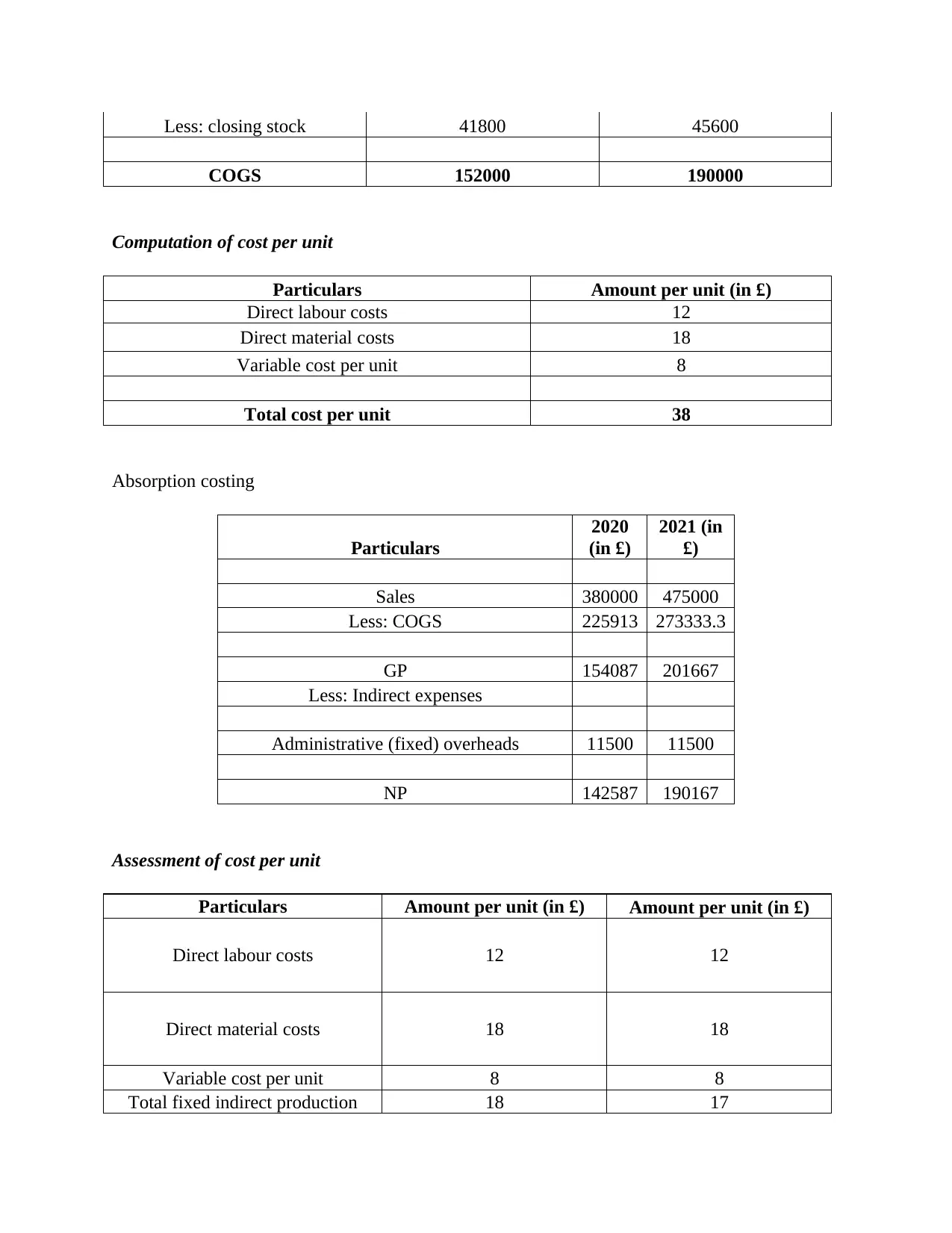

Less: closing stock 41800 45600

COGS 152000 190000

Computation of cost per unit

Particulars Amount per unit (in £)

Direct labour costs 12

Direct material costs 18

Variable cost per unit 8

Total cost per unit 38

Absorption costing

Particulars

2020

(in £)

2021 (in

£)

Sales 380000 475000

Less: COGS 225913 273333.3

GP 154087 201667

Less: Indirect expenses

Administrative (fixed) overheads 11500 11500

NP 142587 190167

Assessment of cost per unit

Particulars Amount per unit (in £) Amount per unit (in £)

Direct labour costs 12 12

Direct material costs 18 18

Variable cost per unit 8 8

Total fixed indirect production 18 17

COGS 152000 190000

Computation of cost per unit

Particulars Amount per unit (in £)

Direct labour costs 12

Direct material costs 18

Variable cost per unit 8

Total cost per unit 38

Absorption costing

Particulars

2020

(in £)

2021 (in

£)

Sales 380000 475000

Less: COGS 225913 273333.3

GP 154087 201667

Less: Indirect expenses

Administrative (fixed) overheads 11500 11500

NP 142587 190167

Assessment of cost per unit

Particulars Amount per unit (in £) Amount per unit (in £)

Direct labour costs 12 12

Direct material costs 18 18

Variable cost per unit 8 8

Total fixed indirect production 18 17

cost

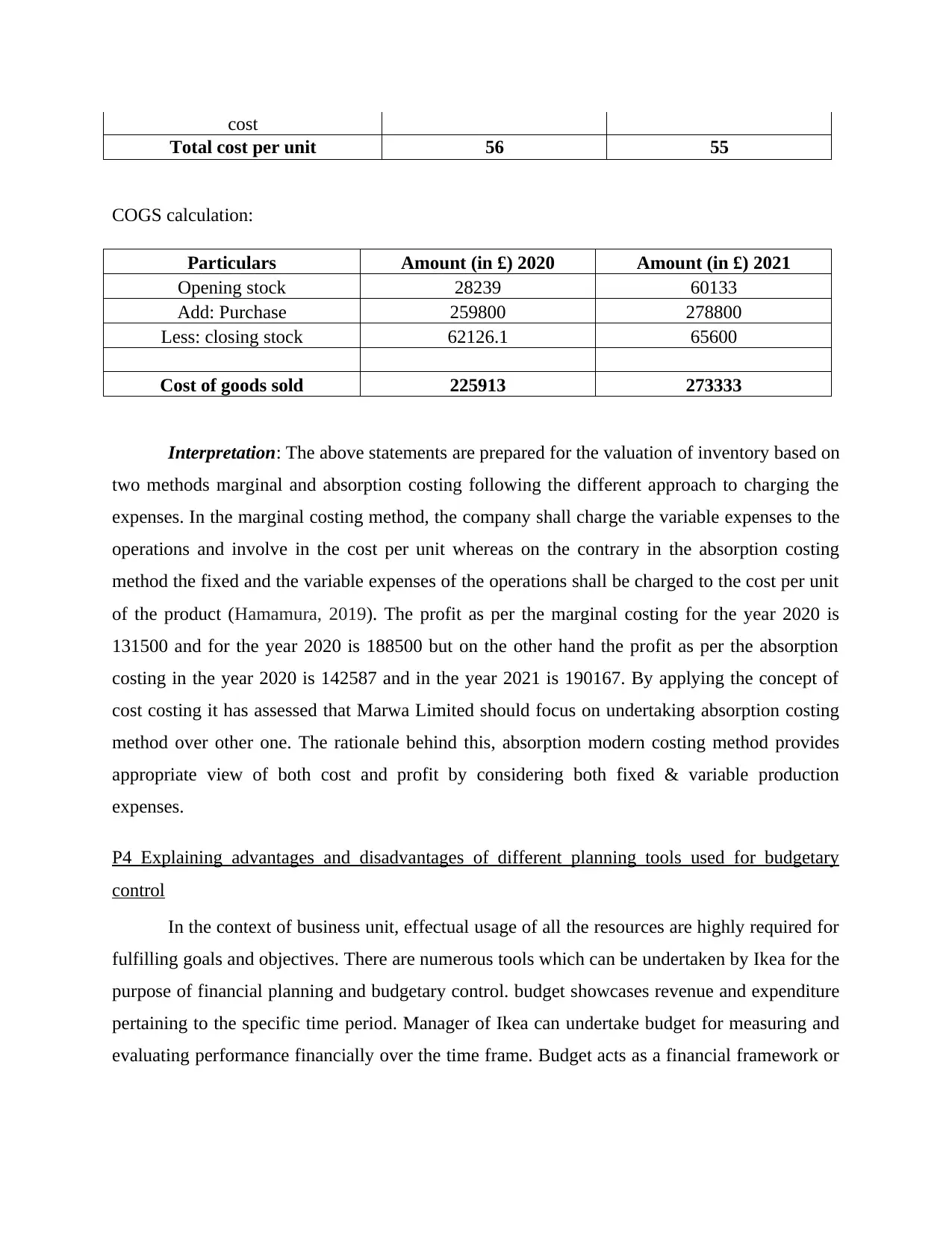

Total cost per unit 56 55

COGS calculation:

Particulars Amount (in £) 2020 Amount (in £) 2021

Opening stock 28239 60133

Add: Purchase 259800 278800

Less: closing stock 62126.1 65600

Cost of goods sold 225913 273333

Interpretation: The above statements are prepared for the valuation of inventory based on

two methods marginal and absorption costing following the different approach to charging the

expenses. In the marginal costing method, the company shall charge the variable expenses to the

operations and involve in the cost per unit whereas on the contrary in the absorption costing

method the fixed and the variable expenses of the operations shall be charged to the cost per unit

of the product (Hamamura, 2019). The profit as per the marginal costing for the year 2020 is

131500 and for the year 2020 is 188500 but on the other hand the profit as per the absorption

costing in the year 2020 is 142587 and in the year 2021 is 190167. By applying the concept of

cost costing it has assessed that Marwa Limited should focus on undertaking absorption costing

method over other one. The rationale behind this, absorption modern costing method provides

appropriate view of both cost and profit by considering both fixed & variable production

expenses.

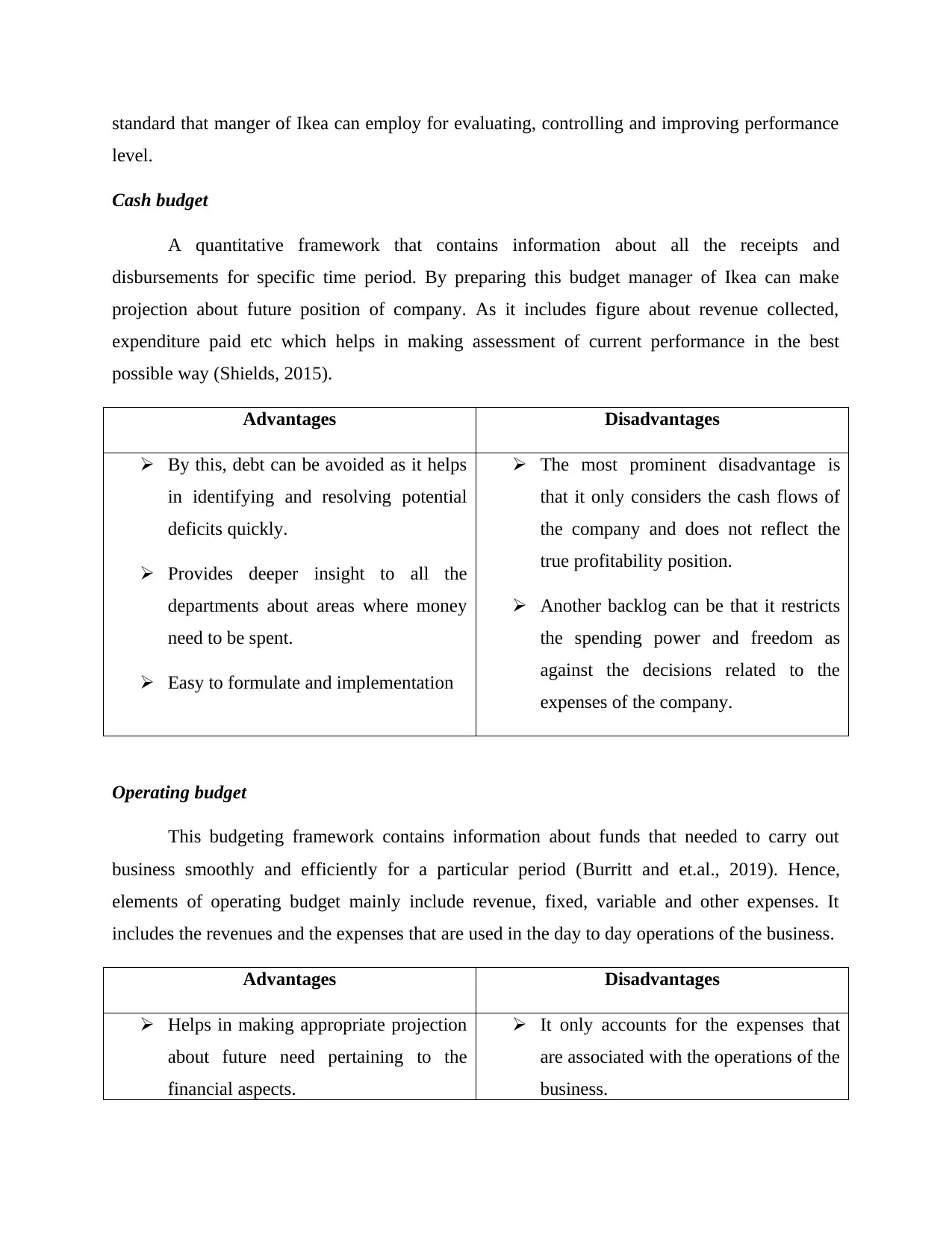

P4 Explaining advantages and disadvantages of different planning tools used for budgetary

control

In the context of business unit, effectual usage of all the resources are highly required for

fulfilling goals and objectives. There are numerous tools which can be undertaken by Ikea for the

purpose of financial planning and budgetary control. budget showcases revenue and expenditure

pertaining to the specific time period. Manager of Ikea can undertake budget for measuring and

evaluating performance financially over the time frame. Budget acts as a financial framework or

Total cost per unit 56 55

COGS calculation:

Particulars Amount (in £) 2020 Amount (in £) 2021

Opening stock 28239 60133

Add: Purchase 259800 278800

Less: closing stock 62126.1 65600

Cost of goods sold 225913 273333

Interpretation: The above statements are prepared for the valuation of inventory based on

two methods marginal and absorption costing following the different approach to charging the

expenses. In the marginal costing method, the company shall charge the variable expenses to the

operations and involve in the cost per unit whereas on the contrary in the absorption costing

method the fixed and the variable expenses of the operations shall be charged to the cost per unit

of the product (Hamamura, 2019). The profit as per the marginal costing for the year 2020 is

131500 and for the year 2020 is 188500 but on the other hand the profit as per the absorption

costing in the year 2020 is 142587 and in the year 2021 is 190167. By applying the concept of

cost costing it has assessed that Marwa Limited should focus on undertaking absorption costing

method over other one. The rationale behind this, absorption modern costing method provides

appropriate view of both cost and profit by considering both fixed & variable production

expenses.

P4 Explaining advantages and disadvantages of different planning tools used for budgetary

control

In the context of business unit, effectual usage of all the resources are highly required for

fulfilling goals and objectives. There are numerous tools which can be undertaken by Ikea for the

purpose of financial planning and budgetary control. budget showcases revenue and expenditure

pertaining to the specific time period. Manager of Ikea can undertake budget for measuring and

evaluating performance financially over the time frame. Budget acts as a financial framework or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

standard that manger of Ikea can employ for evaluating, controlling and improving performance

level.

Cash budget

A quantitative framework that contains information about all the receipts and

disbursements for specific time period. By preparing this budget manager of Ikea can make

projection about future position of company. As it includes figure about revenue collected,

expenditure paid etc which helps in making assessment of current performance in the best

possible way (Shields, 2015).

Advantages Disadvantages

By this, debt can be avoided as it helps

in identifying and resolving potential

deficits quickly.

Provides deeper insight to all the

departments about areas where money

need to be spent.

Easy to formulate and implementation

The most prominent disadvantage is

that it only considers the cash flows of

the company and does not reflect the

true profitability position.

Another backlog can be that it restricts

the spending power and freedom as

against the decisions related to the

expenses of the company.

Operating budget

This budgeting framework contains information about funds that needed to carry out

business smoothly and efficiently for a particular period (Burritt and et.al., 2019). Hence,

elements of operating budget mainly include revenue, fixed, variable and other expenses. It

includes the revenues and the expenses that are used in the day to day operations of the business.

Advantages Disadvantages

Helps in making appropriate projection

about future need pertaining to the

financial aspects.

It only accounts for the expenses that

are associated with the operations of the

business.

level.

Cash budget

A quantitative framework that contains information about all the receipts and

disbursements for specific time period. By preparing this budget manager of Ikea can make

projection about future position of company. As it includes figure about revenue collected,

expenditure paid etc which helps in making assessment of current performance in the best

possible way (Shields, 2015).

Advantages Disadvantages

By this, debt can be avoided as it helps

in identifying and resolving potential

deficits quickly.

Provides deeper insight to all the

departments about areas where money

need to be spent.

Easy to formulate and implementation

The most prominent disadvantage is

that it only considers the cash flows of

the company and does not reflect the

true profitability position.

Another backlog can be that it restricts

the spending power and freedom as

against the decisions related to the

expenses of the company.

Operating budget

This budgeting framework contains information about funds that needed to carry out

business smoothly and efficiently for a particular period (Burritt and et.al., 2019). Hence,

elements of operating budget mainly include revenue, fixed, variable and other expenses. It

includes the revenues and the expenses that are used in the day to day operations of the business.

Advantages Disadvantages

Helps in making appropriate projection

about future need pertaining to the

financial aspects.

It only accounts for the expenses that

are associated with the operations of the

business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

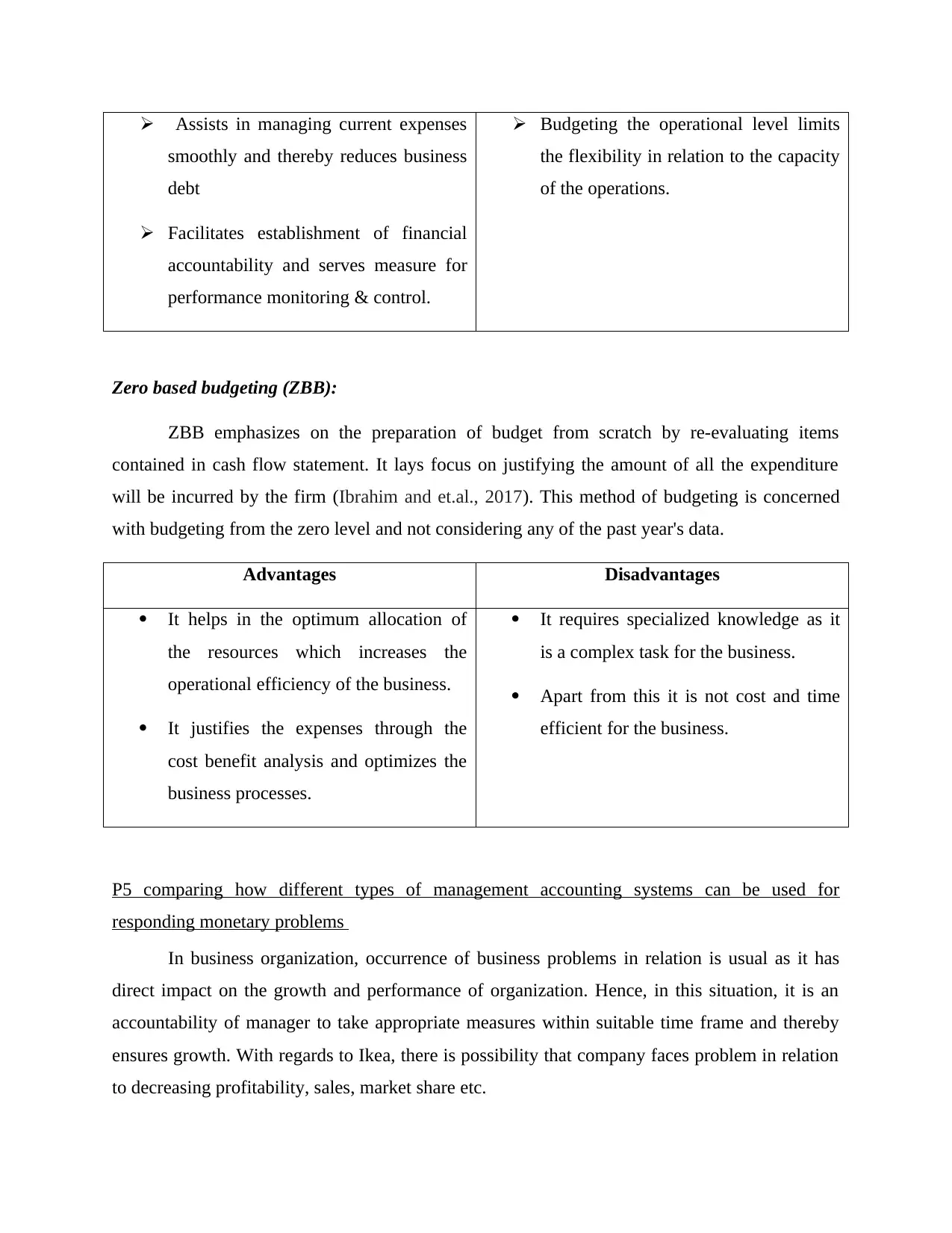

Assists in managing current expenses

smoothly and thereby reduces business

debt

Facilitates establishment of financial

accountability and serves measure for

performance monitoring & control.

Budgeting the operational level limits

the flexibility in relation to the capacity

of the operations.

Zero based budgeting (ZBB):

ZBB emphasizes on the preparation of budget from scratch by re-evaluating items

contained in cash flow statement. It lays focus on justifying the amount of all the expenditure

will be incurred by the firm (Ibrahim and et.al., 2017). This method of budgeting is concerned

with budgeting from the zero level and not considering any of the past year's data.

Advantages Disadvantages

It helps in the optimum allocation of

the resources which increases the

operational efficiency of the business.

It justifies the expenses through the

cost benefit analysis and optimizes the

business processes.

It requires specialized knowledge as it

is a complex task for the business.

Apart from this it is not cost and time

efficient for the business.

P5 comparing how different types of management accounting systems can be used for

responding monetary problems

In business organization, occurrence of business problems in relation is usual as it has

direct impact on the growth and performance of organization. Hence, in this situation, it is an

accountability of manager to take appropriate measures within suitable time frame and thereby

ensures growth. With regards to Ikea, there is possibility that company faces problem in relation

to decreasing profitability, sales, market share etc.

smoothly and thereby reduces business

debt

Facilitates establishment of financial

accountability and serves measure for

performance monitoring & control.

Budgeting the operational level limits

the flexibility in relation to the capacity

of the operations.

Zero based budgeting (ZBB):

ZBB emphasizes on the preparation of budget from scratch by re-evaluating items

contained in cash flow statement. It lays focus on justifying the amount of all the expenditure

will be incurred by the firm (Ibrahim and et.al., 2017). This method of budgeting is concerned

with budgeting from the zero level and not considering any of the past year's data.

Advantages Disadvantages

It helps in the optimum allocation of

the resources which increases the

operational efficiency of the business.

It justifies the expenses through the

cost benefit analysis and optimizes the

business processes.

It requires specialized knowledge as it

is a complex task for the business.

Apart from this it is not cost and time

efficient for the business.

P5 comparing how different types of management accounting systems can be used for

responding monetary problems

In business organization, occurrence of business problems in relation is usual as it has

direct impact on the growth and performance of organization. Hence, in this situation, it is an

accountability of manager to take appropriate measures within suitable time frame and thereby

ensures growth. With regards to Ikea, there is possibility that company faces problem in relation

to decreasing profitability, sales, market share etc.

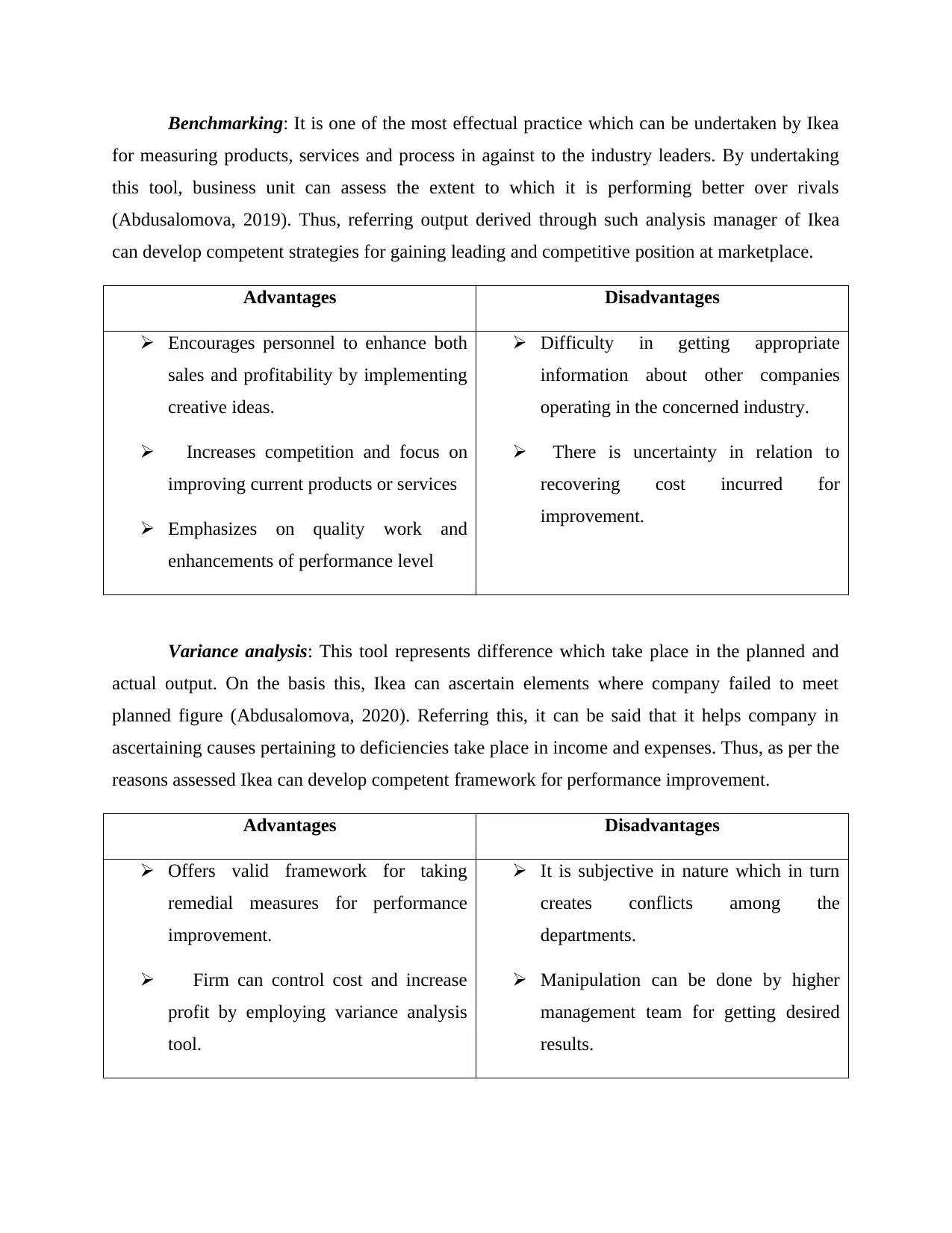

Benchmarking: It is one of the most effectual practice which can be undertaken by Ikea

for measuring products, services and process in against to the industry leaders. By undertaking

this tool, business unit can assess the extent to which it is performing better over rivals

(Abdusalomova, 2019). Thus, referring output derived through such analysis manager of Ikea

can develop competent strategies for gaining leading and competitive position at marketplace.

Advantages Disadvantages

Encourages personnel to enhance both

sales and profitability by implementing

creative ideas.

Increases competition and focus on

improving current products or services

Emphasizes on quality work and

enhancements of performance level

Difficulty in getting appropriate

information about other companies

operating in the concerned industry.

There is uncertainty in relation to

recovering cost incurred for

improvement.

Variance analysis: This tool represents difference which take place in the planned and

actual output. On the basis this, Ikea can ascertain elements where company failed to meet

planned figure (Abdusalomova, 2020). Referring this, it can be said that it helps company in

ascertaining causes pertaining to deficiencies take place in income and expenses. Thus, as per the

reasons assessed Ikea can develop competent framework for performance improvement.

Advantages Disadvantages

Offers valid framework for taking

remedial measures for performance

improvement.

Firm can control cost and increase

profit by employing variance analysis

tool.

It is subjective in nature which in turn

creates conflicts among the

departments.

Manipulation can be done by higher

management team for getting desired

results.

for measuring products, services and process in against to the industry leaders. By undertaking

this tool, business unit can assess the extent to which it is performing better over rivals

(Abdusalomova, 2019). Thus, referring output derived through such analysis manager of Ikea

can develop competent strategies for gaining leading and competitive position at marketplace.

Advantages Disadvantages

Encourages personnel to enhance both

sales and profitability by implementing

creative ideas.

Increases competition and focus on

improving current products or services

Emphasizes on quality work and

enhancements of performance level

Difficulty in getting appropriate

information about other companies

operating in the concerned industry.

There is uncertainty in relation to

recovering cost incurred for

improvement.

Variance analysis: This tool represents difference which take place in the planned and

actual output. On the basis this, Ikea can ascertain elements where company failed to meet

planned figure (Abdusalomova, 2020). Referring this, it can be said that it helps company in

ascertaining causes pertaining to deficiencies take place in income and expenses. Thus, as per the

reasons assessed Ikea can develop competent framework for performance improvement.

Advantages Disadvantages

Offers valid framework for taking

remedial measures for performance

improvement.

Firm can control cost and increase

profit by employing variance analysis

tool.

It is subjective in nature which in turn

creates conflicts among the

departments.

Manipulation can be done by higher

management team for getting desired

results.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.