Management Accounting Report: IKEA Systems, Techniques, Planning Tools

VerifiedAdded on 2023/01/11

|18

|4585

|36

Report

AI Summary

This report delves into the management accounting practices of IKEA, a global furniture retailer. It begins by defining management accounting and differentiating it from financial accounting. The report then explores various management accounting systems such as inventory management, cost accounting, price management, and job order costing, highlighting their essential requirements and applications within IKEA. It examines different reporting methods used in management accounting, including budget reports, inventory reports, and accounts receivable aging reports, and their benefits. The report further analyzes costing methods like marginal and absorption costing, illustrating their application in preparing income statements and determining net profit. It also discusses different planning tools, their advantages, disadvantages, and their use in preparing and forecasting budgets. Finally, the report compares how companies use management accounting systems to solve financial problems, emphasizing how these tools can lead organizations to sustainable success. The report uses IKEA as a case study throughout, providing practical examples of these concepts.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Various types of MA system and essential requirement..................................................3

P2. Different methods of reporting used in management accounting....................................5

M1. Benefits of management accounting systems and its applications.................................6

D1. Evaluation of MA systems and reporting linked with organizational process................6

TASK 2............................................................................................................................................6

P3. Costing methods to prepare income statement and detect net profit................................6

M2. Range of MA techniques and appropriate financial report...........................................11

D2. Produce a report that applies business operations correctly and interpretation.............12

TASK 3..........................................................................................................................................12

P4. Advantages and disadvantages of different types of planning tools..............................12

M3. Use of different planning tools and their application for preparing and forecasting

budgets..................................................................................................................................13

TASK 4..........................................................................................................................................14

P5. Comparison of companies in using of MAS to solve and responds to their financial

problems...............................................................................................................................14

M4. MA can lead organisations to sustainable success........................................................15

D3. Planning tools used appropriately to solving financial problems..................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Various types of MA system and essential requirement..................................................3

P2. Different methods of reporting used in management accounting....................................5

M1. Benefits of management accounting systems and its applications.................................6

D1. Evaluation of MA systems and reporting linked with organizational process................6

TASK 2............................................................................................................................................6

P3. Costing methods to prepare income statement and detect net profit................................6

M2. Range of MA techniques and appropriate financial report...........................................11

D2. Produce a report that applies business operations correctly and interpretation.............12

TASK 3..........................................................................................................................................12

P4. Advantages and disadvantages of different types of planning tools..............................12

M3. Use of different planning tools and their application for preparing and forecasting

budgets..................................................................................................................................13

TASK 4..........................................................................................................................................14

P5. Comparison of companies in using of MAS to solve and responds to their financial

problems...............................................................................................................................14

M4. MA can lead organisations to sustainable success........................................................15

D3. Planning tools used appropriately to solving financial problems..................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

MA is a discipline that involves involvement in policy taking, creation of success

assessment and management systems, including financial reporting and monitoring tools that

better monitor the organization's plan in the design and execution (Arnaboldi, Lapsley and

Steccolini 2015). The firm requires many other MA concepts to help manager decision-makers

achieve business objectives. In order to compile corporate accounting analyses, databases and

books, the company expense and activities are assessed. This study is focused on IKEA, a

Swedish-based, Netherlands-based, international company that produced and marketed entirely

ready-made furniture in 1943. It contains kitchen equipment, household products, goods &

services each time at household.

This report covers important requirements of different MA systems and reports. The report

provides an evaluation of the application of integrated budget preparation planning tools as well

as an evaluation of how the issue is quantified using such management techniques and financial

accounting. It also requires at least 2 examples to begin by contrasting the adaptation of

MA systems by organisations to deal with their financial challenges.

TASK 1

P1. Various types of MA system and essential requirement.

MA, during an organizational context, looks at operations somewhere like a corporation

while taking into consideration of customer needs. The MA method converts these assessments

and details into a vocabulary used eventually to make decision-making better. Management

accounting is a process where provisions of accounting information are used by managers for

deciding matters in their organisations and managing as well as controlling the crucial

operations. The major difference between accounting and finance is the internally or externally

priority (Cooper, 2017). In order to increase operational performance, managers of IKEA

implement MA system and maximize their outcome.

Essential requirement of management accounting systems:

Inventory management system: It’s a tool that enables companies to measure goods

throughout their supply chain. It maximizes the completeness of order placement with the

supplier to fulfil your customer and framework the whole path of even a manufacturing

company. This software offers responsibility and greatly influences an enterprise. Through

MA is a discipline that involves involvement in policy taking, creation of success

assessment and management systems, including financial reporting and monitoring tools that

better monitor the organization's plan in the design and execution (Arnaboldi, Lapsley and

Steccolini 2015). The firm requires many other MA concepts to help manager decision-makers

achieve business objectives. In order to compile corporate accounting analyses, databases and

books, the company expense and activities are assessed. This study is focused on IKEA, a

Swedish-based, Netherlands-based, international company that produced and marketed entirely

ready-made furniture in 1943. It contains kitchen equipment, household products, goods &

services each time at household.

This report covers important requirements of different MA systems and reports. The report

provides an evaluation of the application of integrated budget preparation planning tools as well

as an evaluation of how the issue is quantified using such management techniques and financial

accounting. It also requires at least 2 examples to begin by contrasting the adaptation of

MA systems by organisations to deal with their financial challenges.

TASK 1

P1. Various types of MA system and essential requirement.

MA, during an organizational context, looks at operations somewhere like a corporation

while taking into consideration of customer needs. The MA method converts these assessments

and details into a vocabulary used eventually to make decision-making better. Management

accounting is a process where provisions of accounting information are used by managers for

deciding matters in their organisations and managing as well as controlling the crucial

operations. The major difference between accounting and finance is the internally or externally

priority (Cooper, 2017). In order to increase operational performance, managers of IKEA

implement MA system and maximize their outcome.

Essential requirement of management accounting systems:

Inventory management system: It’s a tool that enables companies to measure goods

throughout their supply chain. It maximizes the completeness of order placement with the

supplier to fulfil your customer and framework the whole path of even a manufacturing

company. This software offers responsibility and greatly influences an enterprise. Through

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reliably tracking goods, companies may reduce data duplication, detect trends and focus on

better spending (Inventory Management Systems, 2020). Whenever company’s inventory is

being ordered, stored and used the whole process called inventory management. Management of

components and raw materials are included. Inventory management plays main role and it’s a

variable asset of the company. Inventory management helps to keep restock certain items and to

decide amounts of products of purchasing and selling and re ordering and tracking of stock and

determining the reorder points as well. IKEA’s Manager incorporates the way to measure the

accessibility of inventory in storage facilities on a frequent basis. It allows them to produce

furniture appropriately or to produce additional inventories as needed. In the sense of the

enterprise, additional managers may develop successful plans in order to operate their company

effectively.

Cost accounting system: This method is used by producers to monitor manufacturing processes

using an on-going inventory program. In these other words, it was an accounting method

developed for manufacturing firms that monitors the movement of goods across the various

phases of development and measures each company’s costs at various speeds (Fleischman and

Parker, 2017). The accurate cost of products is essential to productive products. An IKEA

manager must know which line of products is profited and which are not profitable, but can only

be reached if the appropriate product cost is predicted. Cost accounting is a thing which

determines cost in corporate or business the basic process of cost accounting is to establish

budgets and essential cost requirements of corporation and essential budget management. Cost

accounting helps in future data management of a business and details of efficiency of each data

process in case when a corporation increase and decrease any business prices or fix any price this

process also called cost accounting. Furthermore, IKEA management can develop strategies to

minimize or control costs over the entire operation period.

Price management program: The organization is using this tool as it is conscious that its

current clients are prone to demand variability. The degree to which businesses will achieve

established efficiency and productivity can also be addressed. Optimal level costing is essential

when IKEA try to communicate sales revenues and, more importantly, if it helped to improve

profits through the maintenance of the same customer satisfaction levels. Price optimization is

now becoming extremely important because of extremely competitive purchases in specific

business areas (Gray, 2015). So many firms in market emerging markets also seek to launch new

better spending (Inventory Management Systems, 2020). Whenever company’s inventory is

being ordered, stored and used the whole process called inventory management. Management of

components and raw materials are included. Inventory management plays main role and it’s a

variable asset of the company. Inventory management helps to keep restock certain items and to

decide amounts of products of purchasing and selling and re ordering and tracking of stock and

determining the reorder points as well. IKEA’s Manager incorporates the way to measure the

accessibility of inventory in storage facilities on a frequent basis. It allows them to produce

furniture appropriately or to produce additional inventories as needed. In the sense of the

enterprise, additional managers may develop successful plans in order to operate their company

effectively.

Cost accounting system: This method is used by producers to monitor manufacturing processes

using an on-going inventory program. In these other words, it was an accounting method

developed for manufacturing firms that monitors the movement of goods across the various

phases of development and measures each company’s costs at various speeds (Fleischman and

Parker, 2017). The accurate cost of products is essential to productive products. An IKEA

manager must know which line of products is profited and which are not profitable, but can only

be reached if the appropriate product cost is predicted. Cost accounting is a thing which

determines cost in corporate or business the basic process of cost accounting is to establish

budgets and essential cost requirements of corporation and essential budget management. Cost

accounting helps in future data management of a business and details of efficiency of each data

process in case when a corporation increase and decrease any business prices or fix any price this

process also called cost accounting. Furthermore, IKEA management can develop strategies to

minimize or control costs over the entire operation period.

Price management program: The organization is using this tool as it is conscious that its

current clients are prone to demand variability. The degree to which businesses will achieve

established efficiency and productivity can also be addressed. Optimal level costing is essential

when IKEA try to communicate sales revenues and, more importantly, if it helped to improve

profits through the maintenance of the same customer satisfaction levels. Price optimization is

now becoming extremely important because of extremely competitive purchases in specific

business areas (Gray, 2015). So many firms in market emerging markets also seek to launch new

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

products at lower price. Throughout this context, having the right market value would be even

more important or a company can waste its competitors with significant clients.

Job order costing system: This system is beneficial in defining the total cost involved by

company on different jobs that are part of operating and non-operating activity. It further help to

detect the total spending of company on non-profitable activity and enables manager to make

certain plans to remove these jobs or add new activities. Job costing system is a system when it

involves all costs which are associated with a specific production and accumulating information.

Job costing system determines each and individual profitability and provides cost of material and

cost of estimation of cost of similar jobs. It helps in requirement of labour and overheads of each

and individual job as manager calculate job cost then it includes direct materials, direct labour

and applied overhead. In respective firm this system is effective enough to find the total cost

spend on various jobs working to increase the profit earning capacity.

The management of IKEA Furniture required each MA system mentioned above within their

operation to make proper decision that help to increase profitability. Through the successful

execution, the enterprise may work in a proper manner or accomplish corporate objectives and

targets.

P2. Different methods of reporting used in management accounting

MA reports are really a key element in building that participants get such a clear sight of

how well the company works. These reports advertise income reports that could include

information like cash transfers, operational costs, item profitability and provincial revenues

(Management Accounting Reports, 2020). These reports are aimed at making informed choices

for IKEA managers. When businesses depend on planned bookkeeping assistance, information

can be collected more professionally that assistances management guide the organization to

achieve its goals. The following are specific observing approaches:

Budget report: The report is important and helps companies to identify and cut prices

during accounting years that increase profit margin (Brustbauer, 2016). IKEA’s administrator

compiles the summary for efficient business planned organization to approximate the total price

and additional return that can be produced by selling forecasted volumes.

Inventory report: Companies making physical goods are quite beneficial with this report,

especially to those with a reduced fault tolerance in production (Gullberg 2016). The honest

circumstances provide original information for maximizing installation or machining on the

more important or a company can waste its competitors with significant clients.

Job order costing system: This system is beneficial in defining the total cost involved by

company on different jobs that are part of operating and non-operating activity. It further help to

detect the total spending of company on non-profitable activity and enables manager to make

certain plans to remove these jobs or add new activities. Job costing system is a system when it

involves all costs which are associated with a specific production and accumulating information.

Job costing system determines each and individual profitability and provides cost of material and

cost of estimation of cost of similar jobs. It helps in requirement of labour and overheads of each

and individual job as manager calculate job cost then it includes direct materials, direct labour

and applied overhead. In respective firm this system is effective enough to find the total cost

spend on various jobs working to increase the profit earning capacity.

The management of IKEA Furniture required each MA system mentioned above within their

operation to make proper decision that help to increase profitability. Through the successful

execution, the enterprise may work in a proper manner or accomplish corporate objectives and

targets.

P2. Different methods of reporting used in management accounting

MA reports are really a key element in building that participants get such a clear sight of

how well the company works. These reports advertise income reports that could include

information like cash transfers, operational costs, item profitability and provincial revenues

(Management Accounting Reports, 2020). These reports are aimed at making informed choices

for IKEA managers. When businesses depend on planned bookkeeping assistance, information

can be collected more professionally that assistances management guide the organization to

achieve its goals. The following are specific observing approaches:

Budget report: The report is important and helps companies to identify and cut prices

during accounting years that increase profit margin (Brustbauer, 2016). IKEA’s administrator

compiles the summary for efficient business planned organization to approximate the total price

and additional return that can be produced by selling forecasted volumes.

Inventory report: Companies making physical goods are quite beneficial with this report,

especially to those with a reduced fault tolerance in production (Gullberg 2016). The honest

circumstances provide original information for maximizing installation or machining on the

expense of inventories, labour, and other operating expenditure operational activities involved in

the manufacturing cycle. It contains data on stock, such as labour costs, transport costs, ordering

costs and other charges, followed by the company IKEA. This report is used by IKEA

management teams to document information that will be useful for management to develop

strategies and control stock level in order to increase overall profitability.

Accounts Receivable Aging Report: All companies that provide risky loans maintain this

report which shows an insight of the average credit account, typically for items 30, 60 and 90

days late. It could help to change the repayment terms to include both customers' payment

capacity. IKEA administrators use this tool to classify defaulters over a particular span of time.

A management should create stringent credit strategies to limit the amount of defaulters lists and

popular their liability.

M1. Benefits of management accounting systems and its applications.

MA systems are extremely important in the organisational culture and offer several

advantages also at time they are implemented in IKEA Company. IKEA managers may control

the whole stock volume by implementing a stock tracking program, which minimizes the

possibility of over sales, eliminates maintenance costs and improves operations. Cost

system helps IKEA managers to assess each item cost which really helps reduce manufacturing

overall costs and ensures that cost authority over the time frame is maintained (Harrison and

Lock, 2017). At the other side, the demand control program allows managers to fix rates for their

goods according to their market priorities and even to insure that they fulfil the needs of

consumers. This accounting system allows the management to operate and to ensure that

efficiency and effectiveness are maximised. It also maximizes efficiency and the success of the

organization.

D1. Evaluation of MA systems and reporting linked with organizational process.

Accounting schemes of administration and budgets are very critical for the company to carry

out its activities. Critically assessed, the costing system assists the management team in

estimating the value of the goods, which is included in the costing report. Moreover, the stock

management system is being implemented to governor the stock level as well as provides further

assessment of these details in the stock management report. There is an examination of the

relation between accounting records and programs. It further allows the executive of IKEA in

the manufacturing cycle. It contains data on stock, such as labour costs, transport costs, ordering

costs and other charges, followed by the company IKEA. This report is used by IKEA

management teams to document information that will be useful for management to develop

strategies and control stock level in order to increase overall profitability.

Accounts Receivable Aging Report: All companies that provide risky loans maintain this

report which shows an insight of the average credit account, typically for items 30, 60 and 90

days late. It could help to change the repayment terms to include both customers' payment

capacity. IKEA administrators use this tool to classify defaulters over a particular span of time.

A management should create stringent credit strategies to limit the amount of defaulters lists and

popular their liability.

M1. Benefits of management accounting systems and its applications.

MA systems are extremely important in the organisational culture and offer several

advantages also at time they are implemented in IKEA Company. IKEA managers may control

the whole stock volume by implementing a stock tracking program, which minimizes the

possibility of over sales, eliminates maintenance costs and improves operations. Cost

system helps IKEA managers to assess each item cost which really helps reduce manufacturing

overall costs and ensures that cost authority over the time frame is maintained (Harrison and

Lock, 2017). At the other side, the demand control program allows managers to fix rates for their

goods according to their market priorities and even to insure that they fulfil the needs of

consumers. This accounting system allows the management to operate and to ensure that

efficiency and effectiveness are maximised. It also maximizes efficiency and the success of the

organization.

D1. Evaluation of MA systems and reporting linked with organizational process.

Accounting schemes of administration and budgets are very critical for the company to carry

out its activities. Critically assessed, the costing system assists the management team in

estimating the value of the goods, which is included in the costing report. Moreover, the stock

management system is being implemented to governor the stock level as well as provides further

assessment of these details in the stock management report. There is an examination of the

relation between accounting records and programs. It further allows the executive of IKEA in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decision taking phase to operate operating cycle in effective group to attain market goals &

objectives.

TASK 2

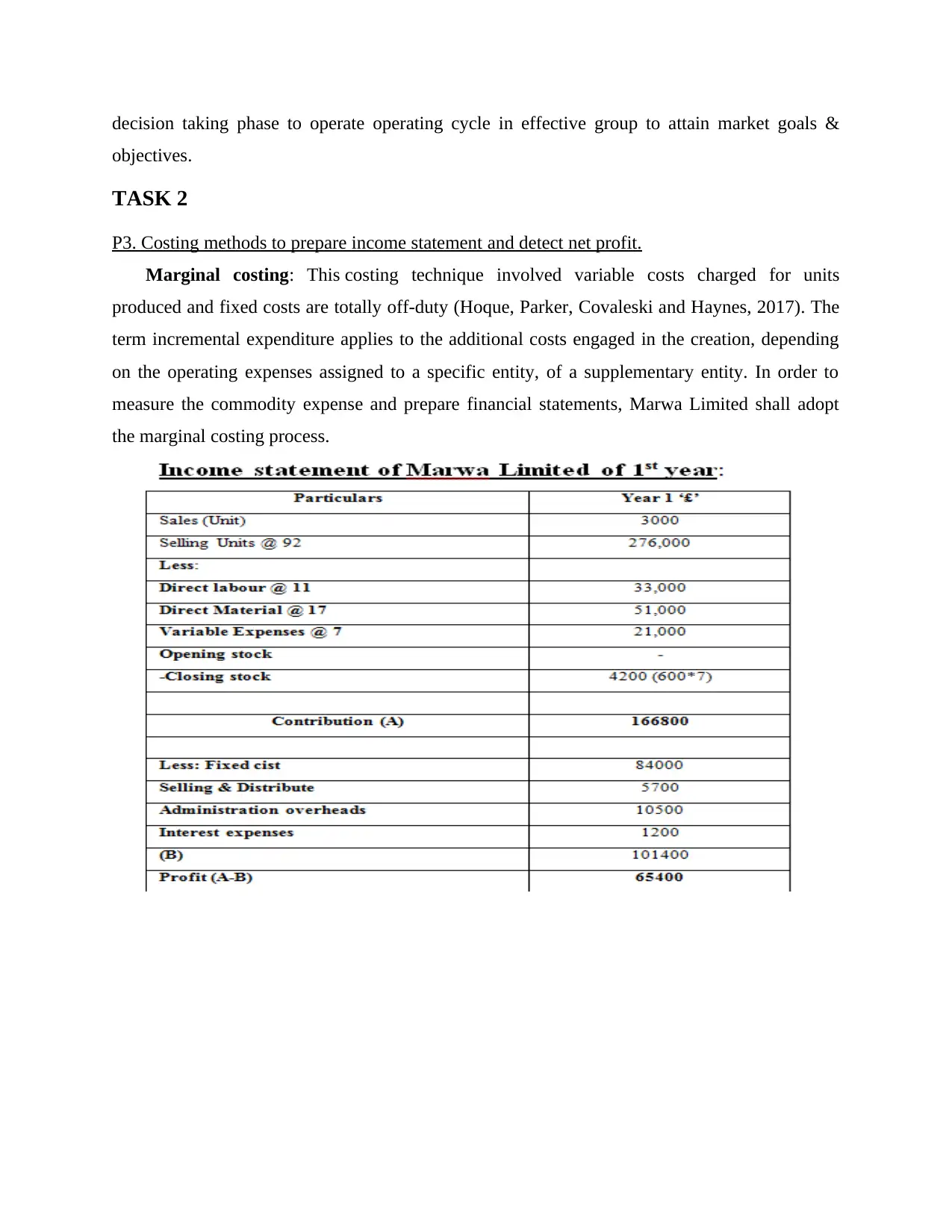

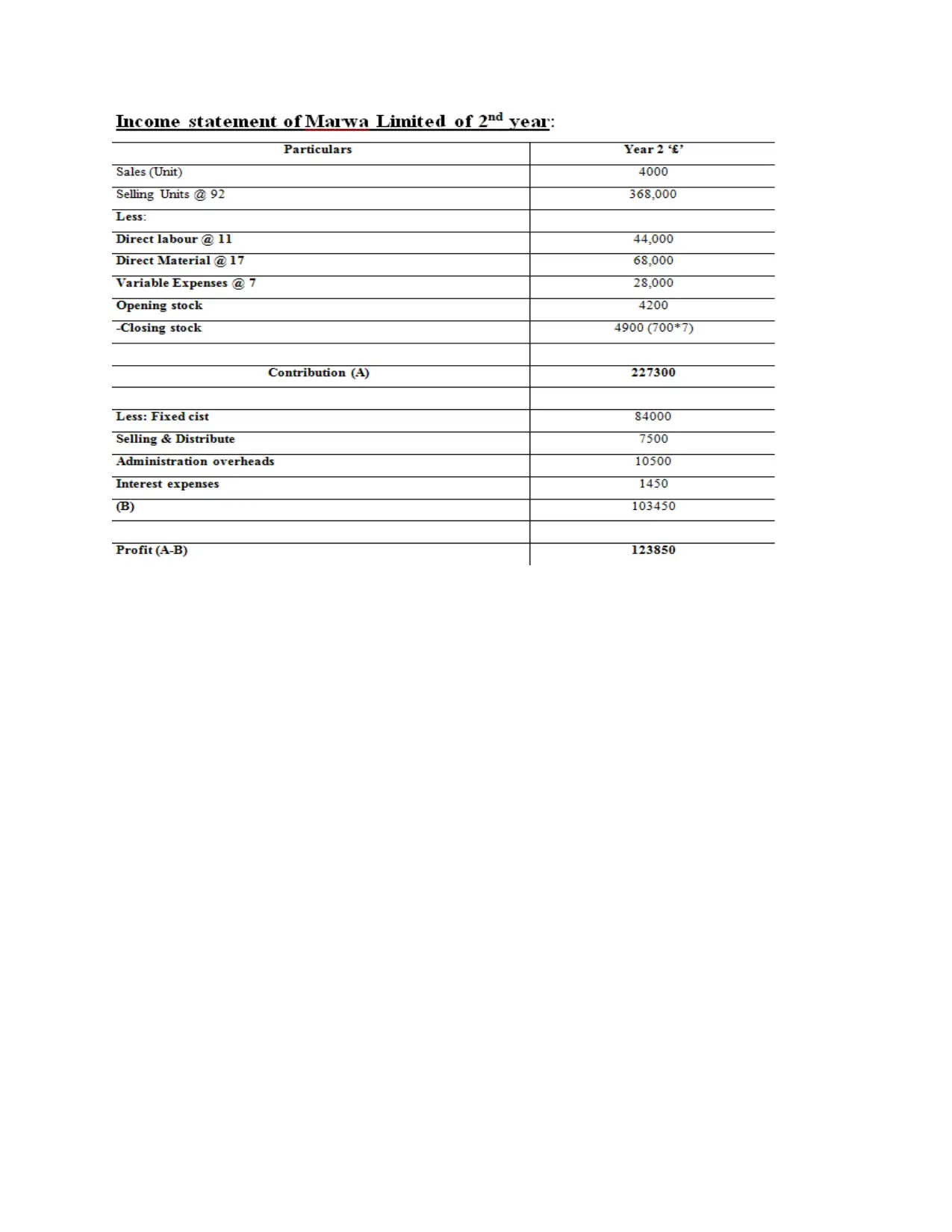

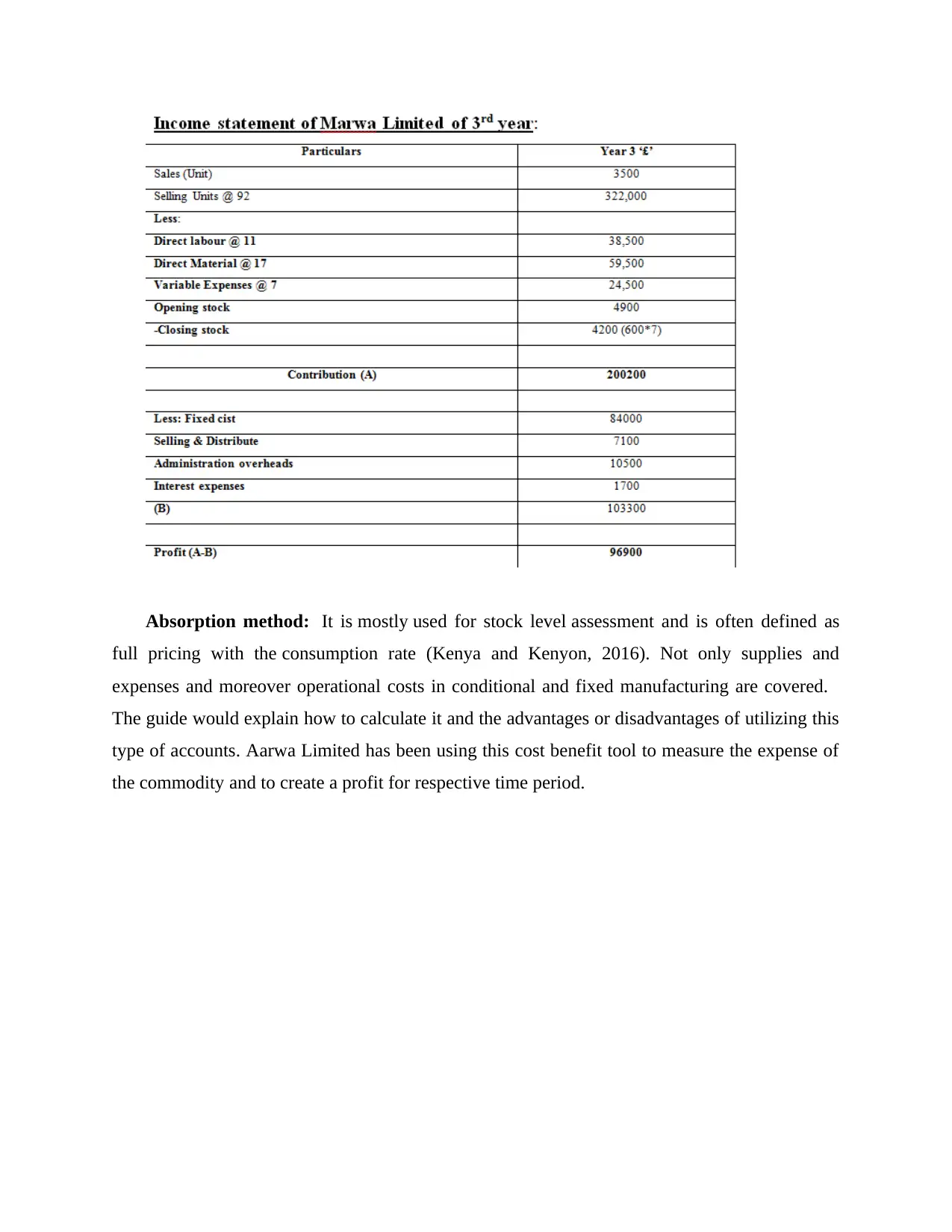

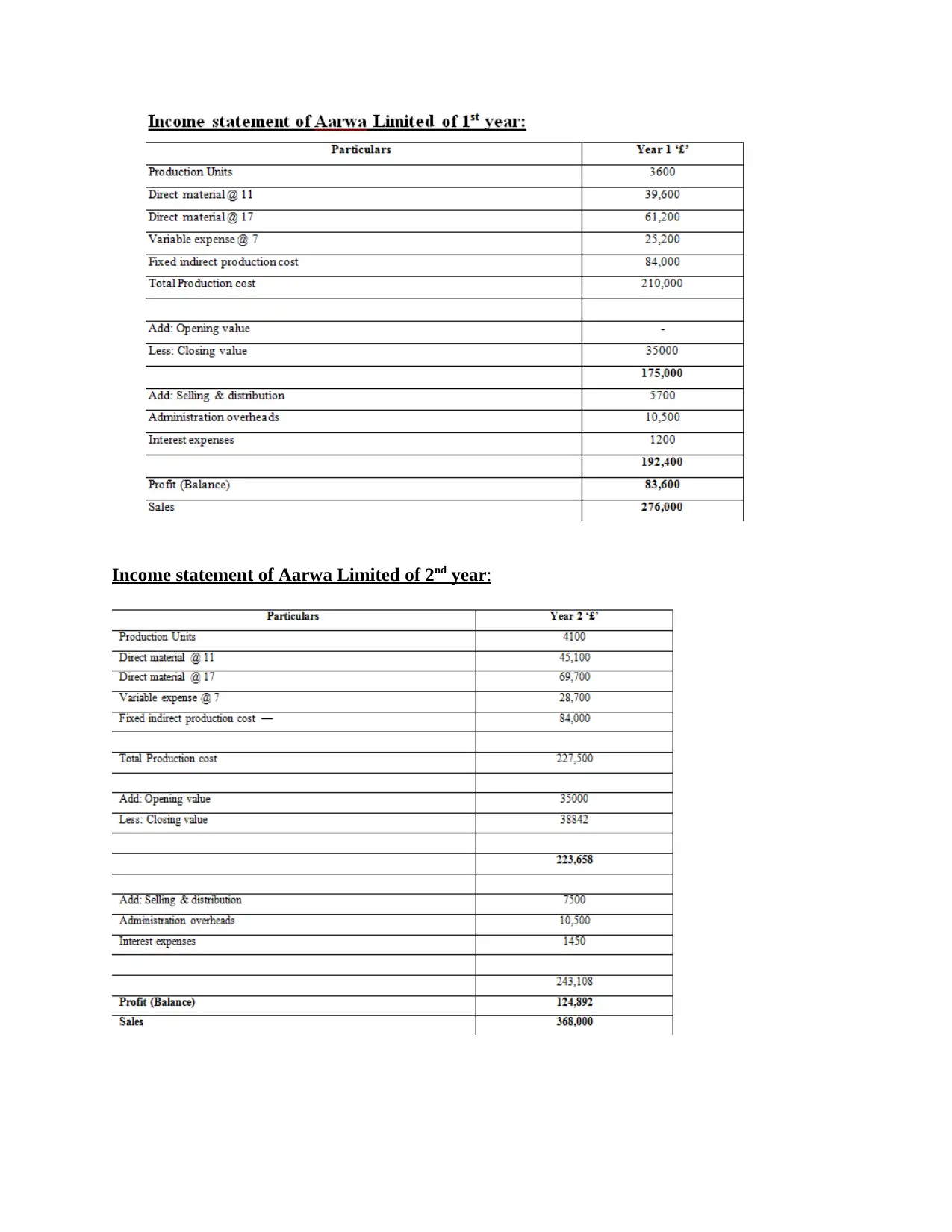

P3. Costing methods to prepare income statement and detect net profit.

Marginal costing: This costing technique involved variable costs charged for units

produced and fixed costs are totally off-duty (Hoque, Parker, Covaleski and Haynes, 2017). The

term incremental expenditure applies to the additional costs engaged in the creation, depending

on the operating expenses assigned to a specific entity, of a supplementary entity. In order to

measure the commodity expense and prepare financial statements, Marwa Limited shall adopt

the marginal costing process.

objectives.

TASK 2

P3. Costing methods to prepare income statement and detect net profit.

Marginal costing: This costing technique involved variable costs charged for units

produced and fixed costs are totally off-duty (Hoque, Parker, Covaleski and Haynes, 2017). The

term incremental expenditure applies to the additional costs engaged in the creation, depending

on the operating expenses assigned to a specific entity, of a supplementary entity. In order to

measure the commodity expense and prepare financial statements, Marwa Limited shall adopt

the marginal costing process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

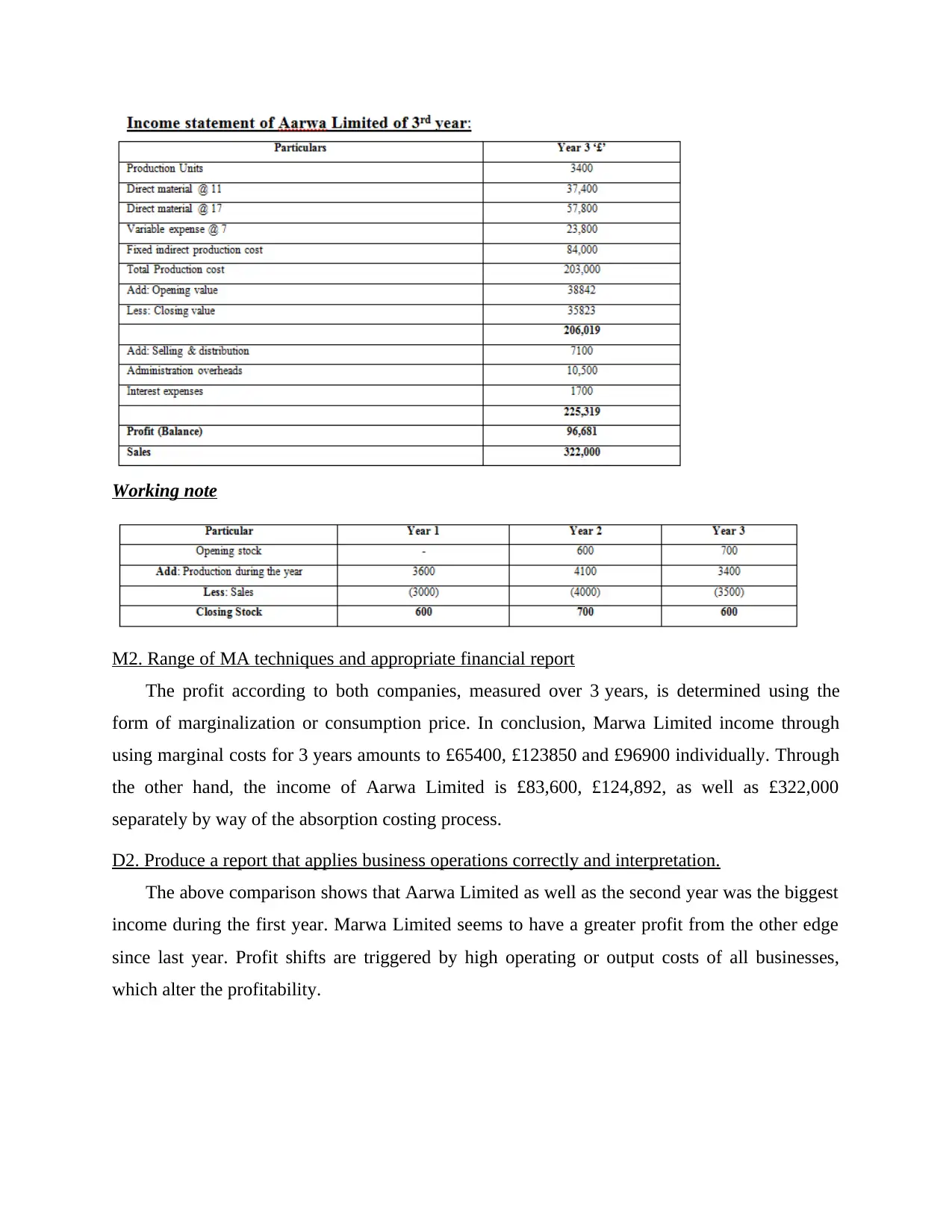

Absorption method: It is mostly used for stock level assessment and is often defined as

full pricing with the consumption rate (Kenya and Kenyon, 2016). Not only supplies and

expenses and moreover operational costs in conditional and fixed manufacturing are covered.

The guide would explain how to calculate it and the advantages or disadvantages of utilizing this

type of accounts. Aarwa Limited has been using this cost benefit tool to measure the expense of

the commodity and to create a profit for respective time period.

full pricing with the consumption rate (Kenya and Kenyon, 2016). Not only supplies and

expenses and moreover operational costs in conditional and fixed manufacturing are covered.

The guide would explain how to calculate it and the advantages or disadvantages of utilizing this

type of accounts. Aarwa Limited has been using this cost benefit tool to measure the expense of

the commodity and to create a profit for respective time period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Income statement of Aarwa Limited of 2nd year:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working note

M2. Range of MA techniques and appropriate financial report

The profit according to both companies, measured over 3 years, is determined using the

form of marginalization or consumption price. In conclusion, Marwa Limited income through

using marginal costs for 3 years amounts to £65400, £123850 and £96900 individually. Through

the other hand, the income of Aarwa Limited is £83,600, £124,892, as well as £322,000

separately by way of the absorption costing process.

D2. Produce a report that applies business operations correctly and interpretation.

The above comparison shows that Aarwa Limited as well as the second year was the biggest

income during the first year. Marwa Limited seems to have a greater profit from the other edge

since last year. Profit shifts are triggered by high operating or output costs of all businesses,

which alter the profitability.

M2. Range of MA techniques and appropriate financial report

The profit according to both companies, measured over 3 years, is determined using the

form of marginalization or consumption price. In conclusion, Marwa Limited income through

using marginal costs for 3 years amounts to £65400, £123850 and £96900 individually. Through

the other hand, the income of Aarwa Limited is £83,600, £124,892, as well as £322,000

separately by way of the absorption costing process.

D2. Produce a report that applies business operations correctly and interpretation.

The above comparison shows that Aarwa Limited as well as the second year was the biggest

income during the first year. Marwa Limited seems to have a greater profit from the other edge

since last year. Profit shifts are triggered by high operating or output costs of all businesses,

which alter the profitability.

TASK 3

P4. Advantages and disadvantages of different types of planning tools

Budgetary control: This is a company process, in which management teams and

department heads established budget goals and stages of expenditure for each operating unit.

Unit managers attempt only at end of each month or half to equate real results with target sums

and respond dramatically. Plan preparation is a mechanism that allows senior executives to retain

project headings properly. This reform is necessary so because large amounts expenditure will

have an adverse influence on the firm revenues.

The IKEA firm have many planning tools to monitor its budget. Using such forecasting

methods, administrators may carry out their task properly and establish plans for executing these

budgets to achieve operational efficiency. The following are among the planning activities that

IKEA can use and its pros and cons:

Capital budgeting: It can be defined as an expenditure plan form linked to the

determination of long-term investment productive output in firms like machine tools, plants, etc.

This budget allows for long-term investment throughout the department of economics (Kerr,

Rouse and de Villiers, 2015). The IKEA reduced capital group generally means to this strategic

plan in order to see results in the appropriate control of financial cash required. In addition, this

budget contains some advantages and disadvantages:

• Benefit: The investment calculation can be conducted using many investment

measurement methods including the payback time, NPV, IRR, etc. in this form of

capital financial planning. Lesser payback time was chosen, higher was denied and

lower NPV or IRR was chosen on the other hand so because company is benefiting

from the investment.

• Drawback: The exact amount of capital is not taken into account in the payback

date estimate as well as the net current value measurement is solely dependent on a

discounting method, which may be adjusted according to the plan. The end results

can be different because the undervaluing rate is changing as well as the total success

of the property can be changed further.

Flexible budgeting: It is a schedule that adjusts or deforms in spite of modification of

quantity or behaviour. The financial plan is also much simpler than static budget and more

practical which gives higher results. It is the amounts that remain the same as those fixed

P4. Advantages and disadvantages of different types of planning tools

Budgetary control: This is a company process, in which management teams and

department heads established budget goals and stages of expenditure for each operating unit.

Unit managers attempt only at end of each month or half to equate real results with target sums

and respond dramatically. Plan preparation is a mechanism that allows senior executives to retain

project headings properly. This reform is necessary so because large amounts expenditure will

have an adverse influence on the firm revenues.

The IKEA firm have many planning tools to monitor its budget. Using such forecasting

methods, administrators may carry out their task properly and establish plans for executing these

budgets to achieve operational efficiency. The following are among the planning activities that

IKEA can use and its pros and cons:

Capital budgeting: It can be defined as an expenditure plan form linked to the

determination of long-term investment productive output in firms like machine tools, plants, etc.

This budget allows for long-term investment throughout the department of economics (Kerr,

Rouse and de Villiers, 2015). The IKEA reduced capital group generally means to this strategic

plan in order to see results in the appropriate control of financial cash required. In addition, this

budget contains some advantages and disadvantages:

• Benefit: The investment calculation can be conducted using many investment

measurement methods including the payback time, NPV, IRR, etc. in this form of

capital financial planning. Lesser payback time was chosen, higher was denied and

lower NPV or IRR was chosen on the other hand so because company is benefiting

from the investment.

• Drawback: The exact amount of capital is not taken into account in the payback

date estimate as well as the net current value measurement is solely dependent on a

discounting method, which may be adjusted according to the plan. The end results

can be different because the undervaluing rate is changing as well as the total success

of the property can be changed further.

Flexible budgeting: It is a schedule that adjusts or deforms in spite of modification of

quantity or behaviour. The financial plan is also much simpler than static budget and more

practical which gives higher results. It is the amounts that remain the same as those fixed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.