Management Accounting Report: Analysis of IKEA's Accounting Practices

VerifiedAdded on 2023/01/06

|21

|5486

|92

Report

AI Summary

This report delves into the realm of management accounting (MA), focusing on its application within IKEA, a prominent furniture manufacturer in the UK. The introduction establishes MA as a crucial process for generating both financial and non-financial data to facilitate sound business judgments. The report examines various MA systems, including financial management, auditing, planning, cost accounting, controlling, and decision-making. It differentiates between management and financial accounting, emphasizing the former's role in internal decision-making. The core of the report explores diverse costing methods and their impact on income statements, alongside an assessment of various planning tools used for budgetary control. Furthermore, the report highlights the benefits and integration of MA systems within organizational processes, using IKEA as a case study. The report also includes an analysis of different MA reporting methods, such as inventory management and performance reports. The report concludes with an analysis of how the MA system is used to recognize and solve many business-related financial challenges. This report provides insights into how IKEA utilizes MA principles for effective financial management and strategic decision-making.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 MA and essential requirement of 4 MA system.....................................................................3

P2. Various method of management accounting reporting.........................................................6

TASK 2............................................................................................................................................8

P3. Preparation of income statements with different costing scheme.........................................8

TASK 3..........................................................................................................................................13

P4 Advantages and disadvantages of different planning tools used for budgetary control.......13

TASK 4..........................................................................................................................................16

P5. Comparison between organisations regarding using of MA system to solve problems......16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 MA and essential requirement of 4 MA system.....................................................................3

P2. Various method of management accounting reporting.........................................................6

TASK 2............................................................................................................................................8

P3. Preparation of income statements with different costing scheme.........................................8

TASK 3..........................................................................................................................................13

P4 Advantages and disadvantages of different planning tools used for budgetary control.......13

TASK 4..........................................................................................................................................16

P5. Comparison between organisations regarding using of MA system to solve problems......16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

The approach relating to the accurate documentation of relevant and usable financial and

non-financial information needed to make useful judgments is known as management accounting

(MA). It is a comprehensive procedure in which the organisation manager uses various forms of

MA method to produce critical reports that assist in analysing the key data in different market

circumstances (Cescon, Costantini and Grassetti, 2019). The research is based on IKEA, which is

used in the UK to manufacture designer furniture.

Different types of MA systems and their successful advantages are identified in this report that is

used to produce some relevant studies that are also addressed in this document. The report

frequently discusses multiple costing methods used to produce revenue estimates and, most

notably, different forecasting tools are used to execute budgets within the enterprise. In addition,

the MA system is used to recognise and solve many business-related financial challenges.

TASK 1

P1 MA and essential requirement of 4 MA system.

"MA assures key stakeholders of the dynamic and frequent financial health and position of the

organisation."

"MA is a method for drawing up managerial accounts and records to provide managers with

loyal and responsible non-financial and factual evidence to make short and long-term

judgments."

It has been specifically established from the aforementioned two concepts that MA is a process

connected to the development of a critical study that includes comprehensive details about the

financial and non - financial facets of business in order to make effective choices. There are 6

major MA functions that are listed below:

Financial management- The financial department must arrange and change the required

components of the P&L report, the declaration of revenue (Johnstone, 2020). The documentation

is given to the finance officer, for example, in the most standardised manner, which streamlines

the handling of financial reports during the year.

The approach relating to the accurate documentation of relevant and usable financial and

non-financial information needed to make useful judgments is known as management accounting

(MA). It is a comprehensive procedure in which the organisation manager uses various forms of

MA method to produce critical reports that assist in analysing the key data in different market

circumstances (Cescon, Costantini and Grassetti, 2019). The research is based on IKEA, which is

used in the UK to manufacture designer furniture.

Different types of MA systems and their successful advantages are identified in this report that is

used to produce some relevant studies that are also addressed in this document. The report

frequently discusses multiple costing methods used to produce revenue estimates and, most

notably, different forecasting tools are used to execute budgets within the enterprise. In addition,

the MA system is used to recognise and solve many business-related financial challenges.

TASK 1

P1 MA and essential requirement of 4 MA system.

"MA assures key stakeholders of the dynamic and frequent financial health and position of the

organisation."

"MA is a method for drawing up managerial accounts and records to provide managers with

loyal and responsible non-financial and factual evidence to make short and long-term

judgments."

It has been specifically established from the aforementioned two concepts that MA is a process

connected to the development of a critical study that includes comprehensive details about the

financial and non - financial facets of business in order to make effective choices. There are 6

major MA functions that are listed below:

Financial management- The financial department must arrange and change the required

components of the P&L report, the declaration of revenue (Johnstone, 2020). The documentation

is given to the finance officer, for example, in the most standardised manner, which streamlines

the handling of financial reports during the year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing- It is important for the manager to adjust the data submitted according to the

expectations that assist in auditing. To fulfil the audit process director, the information is updated

in compliance with the accounting concept and requirements to help make practical decisions.

Planning- Appropriate knowledge is presented by the business manager to help decide the

direction of the firm. Includes managers for business reasons with all organisation forecast data.

Cost accounting- Comparative statements are designed to generate efficient effects of reflection

and may scale statements. Organizational planners, for example, use the ratio to forecast cost

trends and develop such strategies to minimise and eliminate costs and maximise profitability.

Controlling- This is the primary responsibility of MA to monitor the finances of the organisation

and the success of staff and workers. Like the use of managers to monitor and handle the scarce

resources that allow operations to work better.

Decision making- Eventually, to optimise the findings and make valuable decisions to improve

total productivity and affectivity, important evidence and related knowledge is shared and

transmitted to workers. In order to maximise the overall benefit and make decisions to boost the

customer base, changed data is given to each employee at different levels in the same

organisation.

Difference between Management accounting and financial accounting.

Financial accounting Management accounting

Reports are produced in this method and are

used by third parties such as clients ,

customers, etc.

It is linked to the production of reports that are

used for better and rational decision making by

top management (Taschner and Charifzadeh,

2020).

For the business as a whole, financial

management is mainly concerned with

accounting.

Managerial accounting imposes even harder on

a corporation's sections, or divisions.

For effective decision-making purposes, MA comprises of several structures that can achieve

both management and accounting requirements. These are addressed in depth under there:

expectations that assist in auditing. To fulfil the audit process director, the information is updated

in compliance with the accounting concept and requirements to help make practical decisions.

Planning- Appropriate knowledge is presented by the business manager to help decide the

direction of the firm. Includes managers for business reasons with all organisation forecast data.

Cost accounting- Comparative statements are designed to generate efficient effects of reflection

and may scale statements. Organizational planners, for example, use the ratio to forecast cost

trends and develop such strategies to minimise and eliminate costs and maximise profitability.

Controlling- This is the primary responsibility of MA to monitor the finances of the organisation

and the success of staff and workers. Like the use of managers to monitor and handle the scarce

resources that allow operations to work better.

Decision making- Eventually, to optimise the findings and make valuable decisions to improve

total productivity and affectivity, important evidence and related knowledge is shared and

transmitted to workers. In order to maximise the overall benefit and make decisions to boost the

customer base, changed data is given to each employee at different levels in the same

organisation.

Difference between Management accounting and financial accounting.

Financial accounting Management accounting

Reports are produced in this method and are

used by third parties such as clients ,

customers, etc.

It is linked to the production of reports that are

used for better and rational decision making by

top management (Taschner and Charifzadeh,

2020).

For the business as a whole, financial

management is mainly concerned with

accounting.

Managerial accounting imposes even harder on

a corporation's sections, or divisions.

For effective decision-making purposes, MA comprises of several structures that can achieve

both management and accounting requirements. These are addressed in depth under there:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost Accounting system- It is often known as a form of inventory pricing that the organisation

uses to quantify the cost of its goods to aid in market control, quality estimation and product

evaluation. This scheme can be used in IKEA to measure the overall expense engaged in

multiple operations and procedures. It may also be beneficial for companies to reduce extra

expenses and increase the allocation of funds in a successful activity. By utilising this

framework, the business can remove activities that require higher costs which are not beneficial

for performance. The FIFO approach suggests that the product that is first bought must first be

sold at a feasible price in order to offset the company's expenses. On the other hand, AVCO is a

tool of a standardised approach to market inventory at all weighted average costs of sales. Any

time inventory is published, an average cost is calculated to further increase the firm's revenue

profit. It is also recognised that ensuring that no new expenses are expended on any wasteful

operation is an integral condition in cost accounting. Some of the basic necessity is as follow:

The cost accounting system must be personalised, functional, simple and reliable of

fulfilling a user's needs.

The costing method by adding detailed and redundant details does not lose usefulness.

By using network research for the development of the framework, a properly phased plan

could be planned.

Inventory Management System- Company inventory is handled successfully throughout this

MA framework. During the year, the most useful use of this method for industry would be to

manage demand and supply (Doktoralina and Apollo, 2019). In order to accommodate the

overall demand of the consumer, the respective organisation should use this approach as it can

keep accurate details on total finished products, raw materials and items in transit. The basic

necessity of this method is to facilitate the preservation of sufficient calculation of manufactured

products stored in warehouses in order to satisfy consumer requirements. Any methods such as

ROP are used in this method, which basically means the reorder stage from which the business

must order again such that the development and procurement phase stays going. Likewise in

IKEA, where the quantity of raw resources short is used by the manager to rearrange the

quantities needed to produce designer furniture. The other JIT method is helpful to the respective

business as it allows to directly ordering the distributor whenever possible.

Essential requirement: Stock management system is essential for companies in order to manage

various kinds of inventories like raw material, work in progress and finished goods. In IKEA

uses to quantify the cost of its goods to aid in market control, quality estimation and product

evaluation. This scheme can be used in IKEA to measure the overall expense engaged in

multiple operations and procedures. It may also be beneficial for companies to reduce extra

expenses and increase the allocation of funds in a successful activity. By utilising this

framework, the business can remove activities that require higher costs which are not beneficial

for performance. The FIFO approach suggests that the product that is first bought must first be

sold at a feasible price in order to offset the company's expenses. On the other hand, AVCO is a

tool of a standardised approach to market inventory at all weighted average costs of sales. Any

time inventory is published, an average cost is calculated to further increase the firm's revenue

profit. It is also recognised that ensuring that no new expenses are expended on any wasteful

operation is an integral condition in cost accounting. Some of the basic necessity is as follow:

The cost accounting system must be personalised, functional, simple and reliable of

fulfilling a user's needs.

The costing method by adding detailed and redundant details does not lose usefulness.

By using network research for the development of the framework, a properly phased plan

could be planned.

Inventory Management System- Company inventory is handled successfully throughout this

MA framework. During the year, the most useful use of this method for industry would be to

manage demand and supply (Doktoralina and Apollo, 2019). In order to accommodate the

overall demand of the consumer, the respective organisation should use this approach as it can

keep accurate details on total finished products, raw materials and items in transit. The basic

necessity of this method is to facilitate the preservation of sufficient calculation of manufactured

products stored in warehouses in order to satisfy consumer requirements. Any methods such as

ROP are used in this method, which basically means the reorder stage from which the business

must order again such that the development and procurement phase stays going. Likewise in

IKEA, where the quantity of raw resources short is used by the manager to rearrange the

quantities needed to produce designer furniture. The other JIT method is helpful to the respective

business as it allows to directly ordering the distributor whenever possible.

Essential requirement: Stock management system is essential for companies in order to manage

various kinds of inventories like raw material, work in progress and finished goods. In IKEA

company, they track usage of material on daily basis and accordingly they order for new material

as well as produce other products.

Job Costing Systems- for those industries where the variety of goods is wider and more and

more work is needed in various divisions, this accounting method is essential. By using IKEA's

device planner, the exact costs involved with different activities can be calculated and some

arrangements can be made to minimise these costs if the outcomes are not satisfactory.

Price accounting system- In addition to input obtained from consumers on various price points,

this MA method is interested in deciding the true rates of service and product. Through using this

IKEA system manager, the correct and acceptable price of furniture will be set, which will

effectively expand the client base and raise sales overall.

Essential requirement: This accounting system is crucial and essential for companies in order to

set prices at a level so that customers can get satisfied as well as seller also get affordable

revenues. In relation to IKEA Company, they set prices of their products in accordance of market

research and customer’s feedback which contribute in better result.

P2. Various method of management accounting reporting.

MA reports are described as a framework for presenting information about particular types of

operations taking place within an organisation. In the current time, it is important for each report

to be updated as per the latest activity and business mission that helps to define the actual

operating. In order to assess the main conclusions of the organisation, all presentations must be

appropriate and do not mislead managers when reviewing meetings. Some notable studies are

discussed below:

Inventory management report: Specific detail on the volume of storage content is provided in

this report to allow potential requirements to be predicted. Similarly, this report can be prepared

on a regular basis at IKEA to document the overall raw resources used only to manufacture

various designer furniture. In addition, the total inventory in the manufacturing cycle and the

total merchandise ready for sale should be registered. ABC research study, for instance, which

allows management to realise when the most and least valuable asset is required to perform

decently within the product of the business.

Account receivable ageing report- This report provides comprehensive details about those

creditors who, since the extension, have not repaid the unpaid balance (Zandi, Khalid and Islam,

2019). With the assistance of these firms, it is important to decide whether or not card facilities

as well as produce other products.

Job Costing Systems- for those industries where the variety of goods is wider and more and

more work is needed in various divisions, this accounting method is essential. By using IKEA's

device planner, the exact costs involved with different activities can be calculated and some

arrangements can be made to minimise these costs if the outcomes are not satisfactory.

Price accounting system- In addition to input obtained from consumers on various price points,

this MA method is interested in deciding the true rates of service and product. Through using this

IKEA system manager, the correct and acceptable price of furniture will be set, which will

effectively expand the client base and raise sales overall.

Essential requirement: This accounting system is crucial and essential for companies in order to

set prices at a level so that customers can get satisfied as well as seller also get affordable

revenues. In relation to IKEA Company, they set prices of their products in accordance of market

research and customer’s feedback which contribute in better result.

P2. Various method of management accounting reporting.

MA reports are described as a framework for presenting information about particular types of

operations taking place within an organisation. In the current time, it is important for each report

to be updated as per the latest activity and business mission that helps to define the actual

operating. In order to assess the main conclusions of the organisation, all presentations must be

appropriate and do not mislead managers when reviewing meetings. Some notable studies are

discussed below:

Inventory management report: Specific detail on the volume of storage content is provided in

this report to allow potential requirements to be predicted. Similarly, this report can be prepared

on a regular basis at IKEA to document the overall raw resources used only to manufacture

various designer furniture. In addition, the total inventory in the manufacturing cycle and the

total merchandise ready for sale should be registered. ABC research study, for instance, which

allows management to realise when the most and least valuable asset is required to perform

decently within the product of the business.

Account receivable ageing report- This report provides comprehensive details about those

creditors who, since the extension, have not repaid the unpaid balance (Zandi, Khalid and Islam,

2019). With the assistance of these firms, it is important to decide whether or not card facilities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

should be authorised for customers. This report will be used by the corresponding business

management to document the cumulative amount remaining with the client to figure out which

consumers have no payments since the last date. This will also serve to improve the company's

credit policies such that the benefit can only be gained from the individual whose financial

record is higher.

Performance report- It is known as a report that contains projected revenue & expenses that are

related to actual revenue & expenses. It also aims to determine the efficiency of multiple people

participating in diverse job positions in order to eliminate any dispensaries. Manager will prepare

this report, such as in the above Mention Business, to monitor the results of each employee and

actual revenue and expenditures on distinct activities. In addition, success can be evaluated and

the lack of variables and coordinated methods can be calculated to minimise income and cost

inequalities for an era.

Benefits of MA system

Name of management

accounting system

Benefits

Inventory management

system

It helps to manage demand and supply within the organisation.

It also helps to retain adequate amounts of finished products

stored in warehouses to satisfy consumer requirements.

Price optimisation system This method is applied to produce the most acceptable cost of

products that can be used to bring in new customers and retain

more profit for the business.

Cost accounting system By utilising this framework, the business can eliminate activities

that require higher costs that are not conducive to profitability.

Job costing system This is associated with the estimation of the rate, benefit and loss

outcomes of each task. Each work and expense associated with

various activities can be evaluated in the above listed entity's

sector.

Management accounting system and reporting integrated with organisational process.

management to document the cumulative amount remaining with the client to figure out which

consumers have no payments since the last date. This will also serve to improve the company's

credit policies such that the benefit can only be gained from the individual whose financial

record is higher.

Performance report- It is known as a report that contains projected revenue & expenses that are

related to actual revenue & expenses. It also aims to determine the efficiency of multiple people

participating in diverse job positions in order to eliminate any dispensaries. Manager will prepare

this report, such as in the above Mention Business, to monitor the results of each employee and

actual revenue and expenditures on distinct activities. In addition, success can be evaluated and

the lack of variables and coordinated methods can be calculated to minimise income and cost

inequalities for an era.

Benefits of MA system

Name of management

accounting system

Benefits

Inventory management

system

It helps to manage demand and supply within the organisation.

It also helps to retain adequate amounts of finished products

stored in warehouses to satisfy consumer requirements.

Price optimisation system This method is applied to produce the most acceptable cost of

products that can be used to bring in new customers and retain

more profit for the business.

Cost accounting system By utilising this framework, the business can eliminate activities

that require higher costs that are not conducive to profitability.

Job costing system This is associated with the estimation of the rate, benefit and loss

outcomes of each task. Each work and expense associated with

various activities can be evaluated in the above listed entity's

sector.

Management accounting system and reporting integrated with organisational process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Important types of MA systems, such as expense, task, stock and price control systems, are

connected to the firm's operating structure and are implemented to produce useful reports (Łada,

Kozarkiewicz and Haslam, 2020). As in IKEA, the cost accounting system is used to calculate

the overall cost involved in different business activities and this detail is reported in cost

accounting records. This allows administrators to analyse expense data and make choices either

to reduce costs or to avoid unprofitable operations.

TASK 2

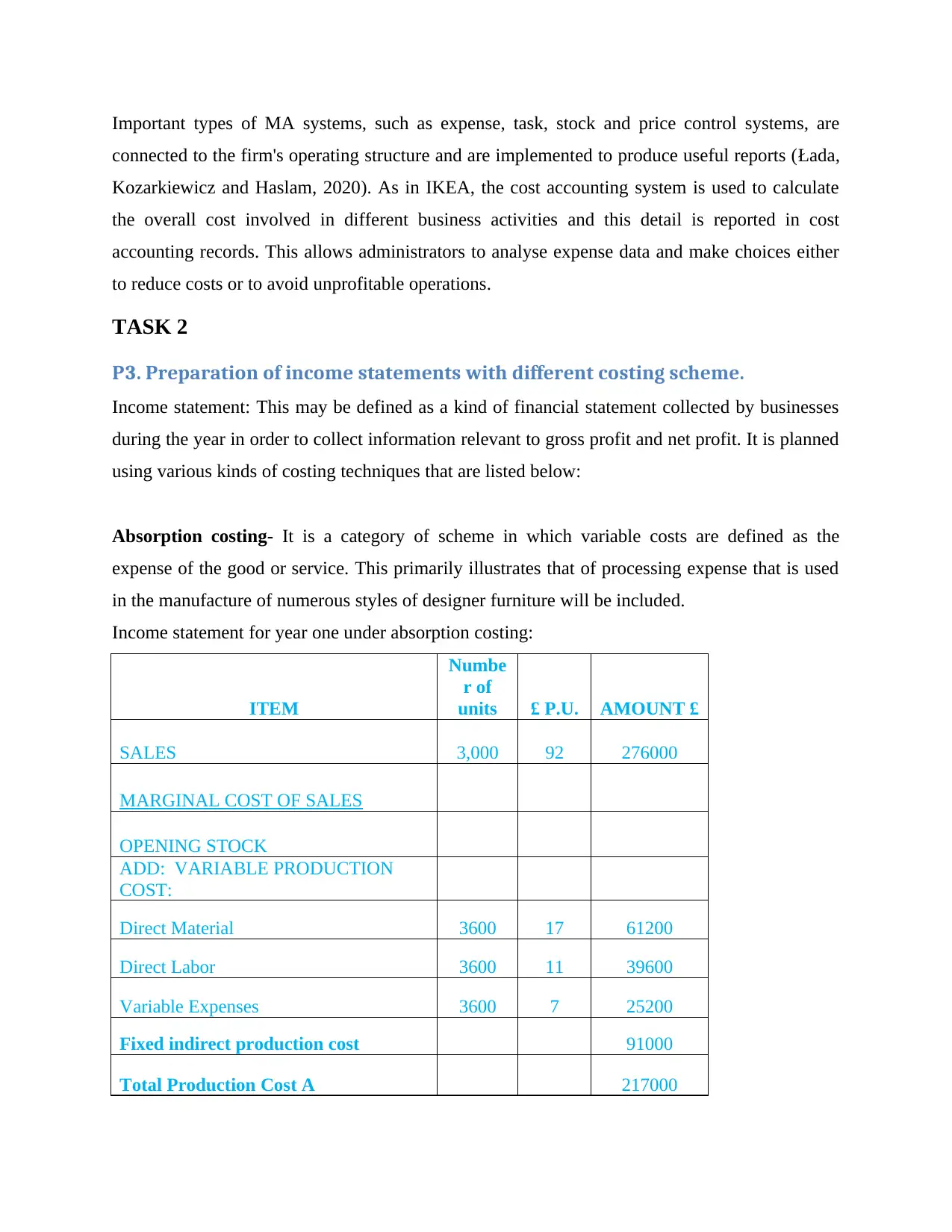

P3. Preparation of income statements with different costing scheme.

Income statement: This may be defined as a kind of financial statement collected by businesses

during the year in order to collect information relevant to gross profit and net profit. It is planned

using various kinds of costing techniques that are listed below:

Absorption costing- It is a category of scheme in which variable costs are defined as the

expense of the good or service. This primarily illustrates that of processing expense that is used

in the manufacture of numerous styles of designer furniture will be included.

Income statement for year one under absorption costing:

ITEM

Numbe

r of

units £ P.U. AMOUNT £

SALES 3,000 92 276000

MARGINAL COST OF SALES

OPENING STOCK

ADD: VARIABLE PRODUCTION

COST:

Direct Material 3600 17 61200

Direct Labor 3600 11 39600

Variable Expenses 3600 7 25200

Fixed indirect production cost 91000

Total Production Cost A 217000

connected to the firm's operating structure and are implemented to produce useful reports (Łada,

Kozarkiewicz and Haslam, 2020). As in IKEA, the cost accounting system is used to calculate

the overall cost involved in different business activities and this detail is reported in cost

accounting records. This allows administrators to analyse expense data and make choices either

to reduce costs or to avoid unprofitable operations.

TASK 2

P3. Preparation of income statements with different costing scheme.

Income statement: This may be defined as a kind of financial statement collected by businesses

during the year in order to collect information relevant to gross profit and net profit. It is planned

using various kinds of costing techniques that are listed below:

Absorption costing- It is a category of scheme in which variable costs are defined as the

expense of the good or service. This primarily illustrates that of processing expense that is used

in the manufacture of numerous styles of designer furniture will be included.

Income statement for year one under absorption costing:

ITEM

Numbe

r of

units £ P.U. AMOUNT £

SALES 3,000 92 276000

MARGINAL COST OF SALES

OPENING STOCK

ADD: VARIABLE PRODUCTION

COST:

Direct Material 3600 17 61200

Direct Labor 3600 11 39600

Variable Expenses 3600 7 25200

Fixed indirect production cost 91000

Total Production Cost A 217000

Less: Closing stock at end of year 1.

[Opening stock units + units produced -

units sold] use formula to calculate

amount. B 36166

Cost of SALES : A-B: 180834

Gross Profit: Sales - Cost of Sales : 95166

Selling and Distribution Overheads 5700

Admin Overheads 10500

Profit from operations Before Interest

& Tax (PBIT) 78966

Interest Expenses 1200

Profit Before Tax [PBIT-interest] 77766

Corporation Tax @ 19% 14775.54

Net Profit 62990.46

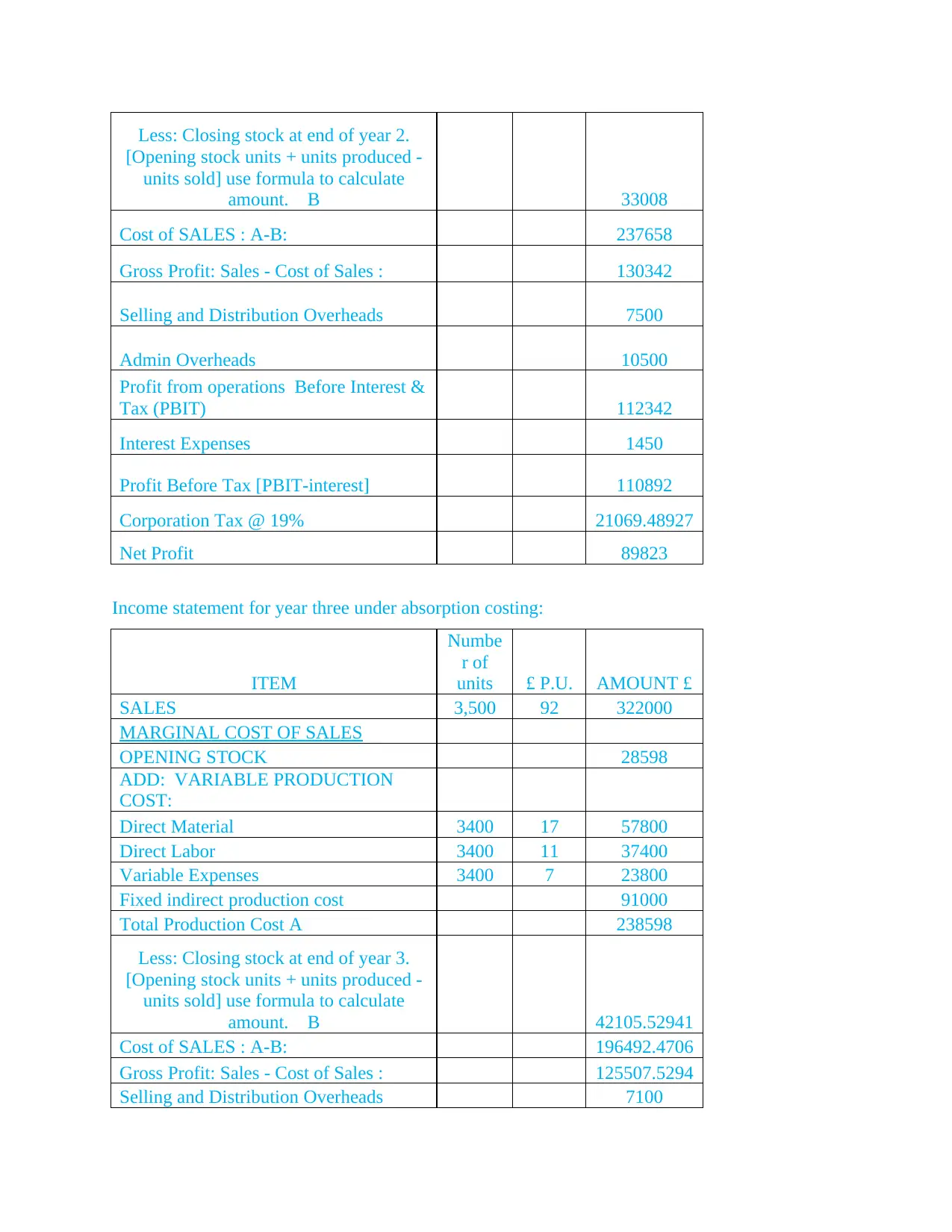

Income statement for year two under absorption costing:

ITEM

Numbe

r of

units £ P.U. AMOUNT £

SALES 4,000 92 368000

MARGINAL COST OF SALES

OPENING STOCK 36166

ADD: VARIABLE PRODUCTION

COST:

Direct Material 4100 17 69700

Direct Labor 4100 11 45100

Variable Expenses 4100 7 28700

Fixed indirect production cost 91000

Total Production Cost A 270666

[Opening stock units + units produced -

units sold] use formula to calculate

amount. B 36166

Cost of SALES : A-B: 180834

Gross Profit: Sales - Cost of Sales : 95166

Selling and Distribution Overheads 5700

Admin Overheads 10500

Profit from operations Before Interest

& Tax (PBIT) 78966

Interest Expenses 1200

Profit Before Tax [PBIT-interest] 77766

Corporation Tax @ 19% 14775.54

Net Profit 62990.46

Income statement for year two under absorption costing:

ITEM

Numbe

r of

units £ P.U. AMOUNT £

SALES 4,000 92 368000

MARGINAL COST OF SALES

OPENING STOCK 36166

ADD: VARIABLE PRODUCTION

COST:

Direct Material 4100 17 69700

Direct Labor 4100 11 45100

Variable Expenses 4100 7 28700

Fixed indirect production cost 91000

Total Production Cost A 270666

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Closing stock at end of year 2.

[Opening stock units + units produced -

units sold] use formula to calculate

amount. B 33008

Cost of SALES : A-B: 237658

Gross Profit: Sales - Cost of Sales : 130342

Selling and Distribution Overheads 7500

Admin Overheads 10500

Profit from operations Before Interest &

Tax (PBIT) 112342

Interest Expenses 1450

Profit Before Tax [PBIT-interest] 110892

Corporation Tax @ 19% 21069.48927

Net Profit 89823

Income statement for year three under absorption costing:

ITEM

Numbe

r of

units £ P.U. AMOUNT £

SALES 3,500 92 322000

MARGINAL COST OF SALES

OPENING STOCK 28598

ADD: VARIABLE PRODUCTION

COST:

Direct Material 3400 17 57800

Direct Labor 3400 11 37400

Variable Expenses 3400 7 23800

Fixed indirect production cost 91000

Total Production Cost A 238598

Less: Closing stock at end of year 3.

[Opening stock units + units produced -

units sold] use formula to calculate

amount. B 42105.52941

Cost of SALES : A-B: 196492.4706

Gross Profit: Sales - Cost of Sales : 125507.5294

Selling and Distribution Overheads 7100

[Opening stock units + units produced -

units sold] use formula to calculate

amount. B 33008

Cost of SALES : A-B: 237658

Gross Profit: Sales - Cost of Sales : 130342

Selling and Distribution Overheads 7500

Admin Overheads 10500

Profit from operations Before Interest &

Tax (PBIT) 112342

Interest Expenses 1450

Profit Before Tax [PBIT-interest] 110892

Corporation Tax @ 19% 21069.48927

Net Profit 89823

Income statement for year three under absorption costing:

ITEM

Numbe

r of

units £ P.U. AMOUNT £

SALES 3,500 92 322000

MARGINAL COST OF SALES

OPENING STOCK 28598

ADD: VARIABLE PRODUCTION

COST:

Direct Material 3400 17 57800

Direct Labor 3400 11 37400

Variable Expenses 3400 7 23800

Fixed indirect production cost 91000

Total Production Cost A 238598

Less: Closing stock at end of year 3.

[Opening stock units + units produced -

units sold] use formula to calculate

amount. B 42105.52941

Cost of SALES : A-B: 196492.4706

Gross Profit: Sales - Cost of Sales : 125507.5294

Selling and Distribution Overheads 7100

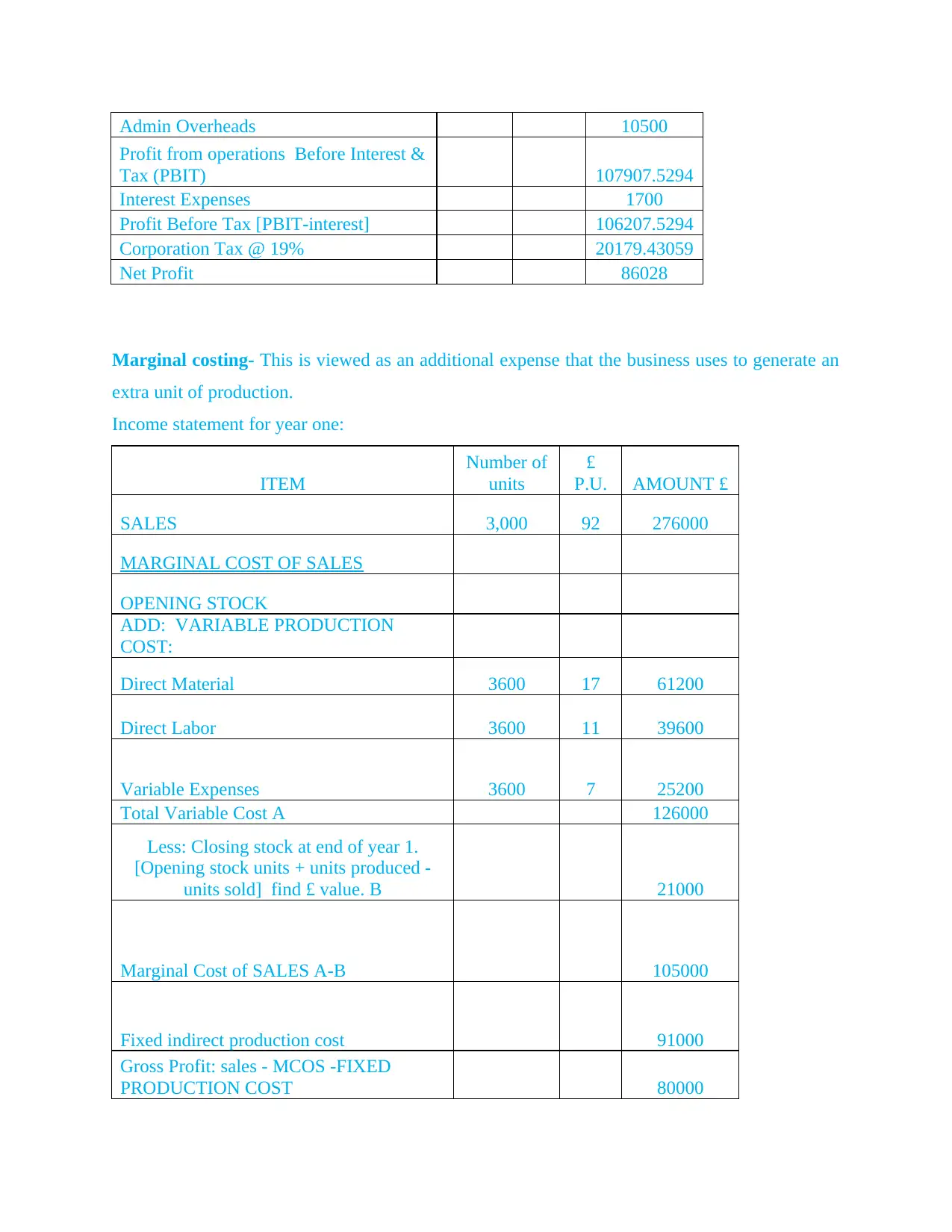

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Admin Overheads 10500

Profit from operations Before Interest &

Tax (PBIT) 107907.5294

Interest Expenses 1700

Profit Before Tax [PBIT-interest] 106207.5294

Corporation Tax @ 19% 20179.43059

Net Profit 86028

Marginal costing- This is viewed as an additional expense that the business uses to generate an

extra unit of production.

Income statement for year one:

ITEM

Number of

units

£

P.U. AMOUNT £

SALES 3,000 92 276000

MARGINAL COST OF SALES

OPENING STOCK

ADD: VARIABLE PRODUCTION

COST:

Direct Material 3600 17 61200

Direct Labor 3600 11 39600

Variable Expenses 3600 7 25200

Total Variable Cost A 126000

Less: Closing stock at end of year 1.

[Opening stock units + units produced -

units sold] find £ value. B 21000

Marginal Cost of SALES A-B 105000

Fixed indirect production cost 91000

Gross Profit: sales - MCOS -FIXED

PRODUCTION COST 80000

Profit from operations Before Interest &

Tax (PBIT) 107907.5294

Interest Expenses 1700

Profit Before Tax [PBIT-interest] 106207.5294

Corporation Tax @ 19% 20179.43059

Net Profit 86028

Marginal costing- This is viewed as an additional expense that the business uses to generate an

extra unit of production.

Income statement for year one:

ITEM

Number of

units

£

P.U. AMOUNT £

SALES 3,000 92 276000

MARGINAL COST OF SALES

OPENING STOCK

ADD: VARIABLE PRODUCTION

COST:

Direct Material 3600 17 61200

Direct Labor 3600 11 39600

Variable Expenses 3600 7 25200

Total Variable Cost A 126000

Less: Closing stock at end of year 1.

[Opening stock units + units produced -

units sold] find £ value. B 21000

Marginal Cost of SALES A-B 105000

Fixed indirect production cost 91000

Gross Profit: sales - MCOS -FIXED

PRODUCTION COST 80000

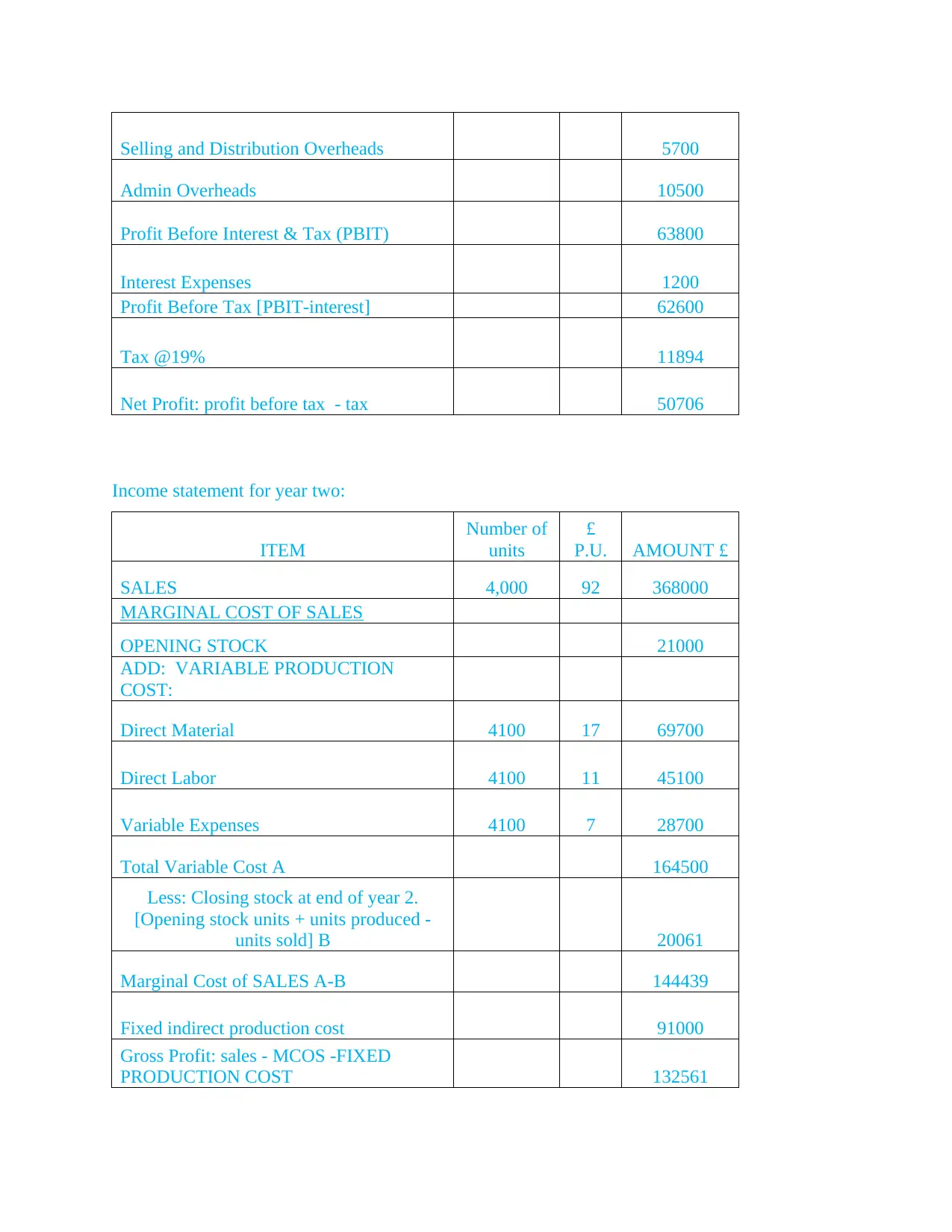

Selling and Distribution Overheads 5700

Admin Overheads 10500

Profit Before Interest & Tax (PBIT) 63800

Interest Expenses 1200

Profit Before Tax [PBIT-interest] 62600

Tax @19% 11894

Net Profit: profit before tax - tax 50706

Income statement for year two:

ITEM

Number of

units

£

P.U. AMOUNT £

SALES 4,000 92 368000

MARGINAL COST OF SALES

OPENING STOCK 21000

ADD: VARIABLE PRODUCTION

COST:

Direct Material 4100 17 69700

Direct Labor 4100 11 45100

Variable Expenses 4100 7 28700

Total Variable Cost A 164500

Less: Closing stock at end of year 2.

[Opening stock units + units produced -

units sold] B 20061

Marginal Cost of SALES A-B 144439

Fixed indirect production cost 91000

Gross Profit: sales - MCOS -FIXED

PRODUCTION COST 132561

Admin Overheads 10500

Profit Before Interest & Tax (PBIT) 63800

Interest Expenses 1200

Profit Before Tax [PBIT-interest] 62600

Tax @19% 11894

Net Profit: profit before tax - tax 50706

Income statement for year two:

ITEM

Number of

units

£

P.U. AMOUNT £

SALES 4,000 92 368000

MARGINAL COST OF SALES

OPENING STOCK 21000

ADD: VARIABLE PRODUCTION

COST:

Direct Material 4100 17 69700

Direct Labor 4100 11 45100

Variable Expenses 4100 7 28700

Total Variable Cost A 164500

Less: Closing stock at end of year 2.

[Opening stock units + units produced -

units sold] B 20061

Marginal Cost of SALES A-B 144439

Fixed indirect production cost 91000

Gross Profit: sales - MCOS -FIXED

PRODUCTION COST 132561

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.