IKEA: Management Accounting Report on Systems, Techniques, and Tools

VerifiedAdded on 2023/01/11

|16

|4112

|21

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, systems, and techniques, using IKEA as a case study. It begins with an introduction to management accounting, contrasting it with financial accounting, and explores essential requirements of management accounting systems, including inventory management, cost accounting, and price optimization. The report then delves into various management accounting reporting methods such as margin analysis, accounts receivable aging, and trend analysis. Furthermore, it examines marginal and absorption costing methods, providing detailed income statements for Marwa Limited and Aarwa Limited to illustrate their application. The report also includes planning tools like budgeting and assesses how these tools are used to quantify business problems. The report concludes with a discussion on how modern organizations implement management accounting systems to address financial issues and a comprehensive reference list.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...............................................................................................................................3

TASK 1.................................................................................................................................................3

P1......................................................................................................................................................3

P2......................................................................................................................................................5

TASK 2.................................................................................................................................................7

P3......................................................................................................................................................7

P4....................................................................................................................................................12

TASK 4...............................................................................................................................................13

P5....................................................................................................................................................13

CONCLUSION..................................................................................................................................14

REFERENCES..................................................................................................................................16

TASK 1.................................................................................................................................................3

P1......................................................................................................................................................3

P2......................................................................................................................................................5

TASK 2.................................................................................................................................................7

P3......................................................................................................................................................7

P4....................................................................................................................................................12

TASK 4...............................................................................................................................................13

P5....................................................................................................................................................13

CONCLUSION..................................................................................................................................14

REFERENCES..................................................................................................................................16

INTRODUCTION

Management accounting is also known as managerial accounting as well as it can be

explained as procedure of providing financial information and resources to the manager

within decision making (Gullberg, 2016). In addition to this, management accounting is used

by internal team of company and this is thing which create differences from financial

accounting. This report is based on IKEA which is Swedish origin multinational group and

respected company was established in 1943. They are well known for their designing and

selling fully prepared-to-assemble furniture. It includes home accessories, kitchen appliances

which include goods and products often home services.

This report will going to cover several topic such as management accounting and

essential requirement of management accounting system as well as reporting documents. In

addition to this, assessment involves analysis of different planning tool for preparing budgets

and assessment how these planning tools as well as accounting system have been utilizing for

quantifying problem. Furthermore, it involves minimum 2 examples for comparing how

modern world organizations are implementing management accounting system for

responding financial issues.

TASK 1

P1

Management accounting is also known as managerial accounting as well as it can be

explained as procedure of providing financial information and resources to the manager

within decision making. In addition to this, management accounting is used by internal team

of company and this is thing which create differences from financial accounting.

Furthermore, financial management for taxpayers and creditors, relies on producing as well

as reviewing annual statement which company publish publicly (Harrison and Lock, 2017).

Through comparison management analysis techniques as well as findings are use by owner of

company to guide decision making for running operation of company in effective manner.

Management accounting handle uncountable facts related to accounting such as margins,

restrictions, prediction, budgeting of money, cost of goods and many more. Thus, IKEA’s

manager will follow management accounting functions for enhancing their operations in

effective manner and maximizing outputs. There are several essential requirement of

management accounting system explanation of these are as follows :-

Management accounting is also known as managerial accounting as well as it can be

explained as procedure of providing financial information and resources to the manager

within decision making (Gullberg, 2016). In addition to this, management accounting is used

by internal team of company and this is thing which create differences from financial

accounting. This report is based on IKEA which is Swedish origin multinational group and

respected company was established in 1943. They are well known for their designing and

selling fully prepared-to-assemble furniture. It includes home accessories, kitchen appliances

which include goods and products often home services.

This report will going to cover several topic such as management accounting and

essential requirement of management accounting system as well as reporting documents. In

addition to this, assessment involves analysis of different planning tool for preparing budgets

and assessment how these planning tools as well as accounting system have been utilizing for

quantifying problem. Furthermore, it involves minimum 2 examples for comparing how

modern world organizations are implementing management accounting system for

responding financial issues.

TASK 1

P1

Management accounting is also known as managerial accounting as well as it can be

explained as procedure of providing financial information and resources to the manager

within decision making. In addition to this, management accounting is used by internal team

of company and this is thing which create differences from financial accounting.

Furthermore, financial management for taxpayers and creditors, relies on producing as well

as reviewing annual statement which company publish publicly (Harrison and Lock, 2017).

Through comparison management analysis techniques as well as findings are use by owner of

company to guide decision making for running operation of company in effective manner.

Management accounting handle uncountable facts related to accounting such as margins,

restrictions, prediction, budgeting of money, cost of goods and many more. Thus, IKEA’s

manager will follow management accounting functions for enhancing their operations in

effective manner and maximizing outputs. There are several essential requirement of

management accounting system explanation of these are as follows :-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system – It is an instrument which help business firm in

tracking goods across the supply chain for their business. It advances the full

continuum from putting in of requests with the wholesaler to arrange satisfaction to

their customer, demonstrating a producer's whole way. Responsibility gave by this

product and bigly affects an organization's main concern. Organizations can lessen

duplication by exact checking of items, distinguish examples and settle on more

brilliant venture choices (Inventory Management System, 2020). Supervisor of IKEA

actualize this framework in their association to follow their everyday schedule

accessibility of stock in distribution centers. It causes them to fabricate furniture in

like manner or further request stock according to the creation prerequisite. Because of

this explanation, stock administration framework is basically required in this

association and it additionally helps in following stock level or gives

straightforwardness. Further chief can fabricate powerful system in setting of the

association to maintain their business activities in well way.

Cost accounting system – Manufacturer of use cost accounting system for

maintaining records of activities through utilisation of constant system of inventories.

In simple term it can be said that, it is accounting system which mainly designed for

manufacturing organisations because with the assistance of this they will be able to

tracks flow of inventory by different production stages as well as evaluate cost of

every units at several stages (Hoque and et. al., 2017). For profitable activities it is

important to determine proper cost of products. Thus, it is important for manager of

IKEA to identify that which product line is profitable and which is not. But taking this

decision is only appropriate only company forecast the appropriate product cost.

Likewise, cost bookkeeping framework is essential for estimating conclusion

estimation of stock of items, work in progress and load of completed things for

arranging of budget summaries. Moreover, Manager of separate organization ready to

fabricate procedures for limiting or controlling expense inside creation process.

Price optimization system – This system business firm use after getting aware of

how responsive their existing customers are in fluctuation of product price. Price

optimization system come into how much business firm can accomplish within

defined profitability as well as performance. For IKEA optimum pricing is important

if they want to connect their sakes revenue to profit crucially and if aim of business

firm is to expand profit through maintaining client relation at same levels. Moreover,

price optimization is become more important because sales of particular corporation

tracking goods across the supply chain for their business. It advances the full

continuum from putting in of requests with the wholesaler to arrange satisfaction to

their customer, demonstrating a producer's whole way. Responsibility gave by this

product and bigly affects an organization's main concern. Organizations can lessen

duplication by exact checking of items, distinguish examples and settle on more

brilliant venture choices (Inventory Management System, 2020). Supervisor of IKEA

actualize this framework in their association to follow their everyday schedule

accessibility of stock in distribution centers. It causes them to fabricate furniture in

like manner or further request stock according to the creation prerequisite. Because of

this explanation, stock administration framework is basically required in this

association and it additionally helps in following stock level or gives

straightforwardness. Further chief can fabricate powerful system in setting of the

association to maintain their business activities in well way.

Cost accounting system – Manufacturer of use cost accounting system for

maintaining records of activities through utilisation of constant system of inventories.

In simple term it can be said that, it is accounting system which mainly designed for

manufacturing organisations because with the assistance of this they will be able to

tracks flow of inventory by different production stages as well as evaluate cost of

every units at several stages (Hoque and et. al., 2017). For profitable activities it is

important to determine proper cost of products. Thus, it is important for manager of

IKEA to identify that which product line is profitable and which is not. But taking this

decision is only appropriate only company forecast the appropriate product cost.

Likewise, cost bookkeeping framework is essential for estimating conclusion

estimation of stock of items, work in progress and load of completed things for

arranging of budget summaries. Moreover, Manager of separate organization ready to

fabricate procedures for limiting or controlling expense inside creation process.

Price optimization system – This system business firm use after getting aware of

how responsive their existing customers are in fluctuation of product price. Price

optimization system come into how much business firm can accomplish within

defined profitability as well as performance. For IKEA optimum pricing is important

if they want to connect their sakes revenue to profit crucially and if aim of business

firm is to expand profit through maintaining client relation at same levels. Moreover,

price optimization is become more important because sales of particular corporation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are becoming highly competitive. There are several other organisations also who are

looking to bring new products in some niche market segmentation also. It is important

to have appropriate price because inappropriate cost of product may result in reducing

customer base in competitive environment.

These accounting systems are needed by manager of IKEA Company as with the

implementation of these organisation will able to conduct their operational activities in better

manner and accomplish objectives.

P2

Management Accounting can be defined as the process of analysing the different

business operations as well as costs in order to prepare internal financial report to help

managers in making effective decisions so that organizational goals and objectives are

achieved effectively (Azudin and Mansor, 2018). Managerial Accounting Reports are

important documents that are used for planning and measuring performance within the

company. There are different methods that IKEA can use for management accounting

reporting which are explained below -

Margin Analysis – This is one of the methods that is used for management

accounting reporting that is primarily concerned with the benefits that are associated with

increased production. Margin analysis is one of the most essential techniques that are used in

management accounting and includes calculating breakeven point. In simple words, it can be

defined as the additional benefits that are associated with a particular activity as compared to

the costs that are incurred by it. IKEA can use this method to balance the costs as well as

benefits of additional actions. This can include analysing if there is a need to produce more or

not, consume more etc.

Accounts Receivable Aging Report – This is another method which is important for

organizations that offers mortgage lending. In simple words, it is a record that demonstrates

the unpaid invoices. It is important because it helps the management of the organization to

identify the money that is outstanding by the customers. The management of IKEA can

effectively use this method for management accounting reporting (Kumarasiri, 2017). Also, it

will be able to identify the customers who are lagging behind on their respective payments.

There are many companies that still do not use this technique and have to face the

consequences.

looking to bring new products in some niche market segmentation also. It is important

to have appropriate price because inappropriate cost of product may result in reducing

customer base in competitive environment.

These accounting systems are needed by manager of IKEA Company as with the

implementation of these organisation will able to conduct their operational activities in better

manner and accomplish objectives.

P2

Management Accounting can be defined as the process of analysing the different

business operations as well as costs in order to prepare internal financial report to help

managers in making effective decisions so that organizational goals and objectives are

achieved effectively (Azudin and Mansor, 2018). Managerial Accounting Reports are

important documents that are used for planning and measuring performance within the

company. There are different methods that IKEA can use for management accounting

reporting which are explained below -

Margin Analysis – This is one of the methods that is used for management

accounting reporting that is primarily concerned with the benefits that are associated with

increased production. Margin analysis is one of the most essential techniques that are used in

management accounting and includes calculating breakeven point. In simple words, it can be

defined as the additional benefits that are associated with a particular activity as compared to

the costs that are incurred by it. IKEA can use this method to balance the costs as well as

benefits of additional actions. This can include analysing if there is a need to produce more or

not, consume more etc.

Accounts Receivable Aging Report – This is another method which is important for

organizations that offers mortgage lending. In simple words, it is a record that demonstrates

the unpaid invoices. It is important because it helps the management of the organization to

identify the money that is outstanding by the customers. The management of IKEA can

effectively use this method for management accounting reporting (Kumarasiri, 2017). Also, it

will be able to identify the customers who are lagging behind on their respective payments.

There are many companies that still do not use this technique and have to face the

consequences.

Inventory Management Report - Realizing how much stock you have at some

random time is basic for an effective business. Stock control reports will show how much

stock you have available. Effectively controlling stock ensures your important capital is being

utilized in the most ideal manner conceivable. Stock book is mostly utilized for a private

venture with barely any things. Stock books track stock physically by entering when stock

comes in and when it goes out. It ought not be a drawn-out answer for stock administration as

it is inclined to blunders and not adaptable as the organization develops.

Trend Analysis and Forecasting – Both these methods basically focus on the

identification of patterns as well as trends of the costs of products. Trend analysis is an

effective and measurable method that businesses should use in order to determine future

outputs. It is also used for forecasting market trends, growth in overall sales as well as

interest rates. Forecasting on the other hand, is a method which makes use of historical data

in the form of input so that effective decisions can be made (Maziriri and Mapuranga, 2017).

Organizations can make use of forecasting method in order to determine the future trends as

well as to determine how can budgets be allocated in the most efficient manner.

Inventory Valuation and Product Costing – Inventory Valuation is another

technique which can be defined the monetary amount that is associated with the products

within the inventory at the end of a particular accounting. The overall valuation of the

inventory is based on the costs that are incurred in order to acquire the inventory. Product

Costing on the other hand, include direct labour, direct materials etc. this can be defined as

the process of assigning costs to inventory as well as the expenses that go into buying

inventory. This can be an important process for IKEA as it manufactures products. The

advantages of product costing include accuracy, product tracking as well as effective

decision-making.

Constraint Analysis – This is another important method that is used for management

accounting reporting. It focuses on the obstructions within organization wherein the manager

within the company should focus on maximising the overall profitability. One of the

advantages of constraint analysis is that obstructions within the company can be found

anywhere. This method also focuses on any kind of efficiencies that are caused by these

obstructions as well as their impact the company’s overall ability to generate profits

(Nkundabayanga, Tauringana and Muhwezi, 2018). This particular method can be used to

random time is basic for an effective business. Stock control reports will show how much

stock you have available. Effectively controlling stock ensures your important capital is being

utilized in the most ideal manner conceivable. Stock book is mostly utilized for a private

venture with barely any things. Stock books track stock physically by entering when stock

comes in and when it goes out. It ought not be a drawn-out answer for stock administration as

it is inclined to blunders and not adaptable as the organization develops.

Trend Analysis and Forecasting – Both these methods basically focus on the

identification of patterns as well as trends of the costs of products. Trend analysis is an

effective and measurable method that businesses should use in order to determine future

outputs. It is also used for forecasting market trends, growth in overall sales as well as

interest rates. Forecasting on the other hand, is a method which makes use of historical data

in the form of input so that effective decisions can be made (Maziriri and Mapuranga, 2017).

Organizations can make use of forecasting method in order to determine the future trends as

well as to determine how can budgets be allocated in the most efficient manner.

Inventory Valuation and Product Costing – Inventory Valuation is another

technique which can be defined the monetary amount that is associated with the products

within the inventory at the end of a particular accounting. The overall valuation of the

inventory is based on the costs that are incurred in order to acquire the inventory. Product

Costing on the other hand, include direct labour, direct materials etc. this can be defined as

the process of assigning costs to inventory as well as the expenses that go into buying

inventory. This can be an important process for IKEA as it manufactures products. The

advantages of product costing include accuracy, product tracking as well as effective

decision-making.

Constraint Analysis – This is another important method that is used for management

accounting reporting. It focuses on the obstructions within organization wherein the manager

within the company should focus on maximising the overall profitability. One of the

advantages of constraint analysis is that obstructions within the company can be found

anywhere. This method also focuses on any kind of efficiencies that are caused by these

obstructions as well as their impact the company’s overall ability to generate profits

(Nkundabayanga, Tauringana and Muhwezi, 2018). This particular method can be used to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

generate effective reports through which obstructions can be identified and addressed in an

effective manner.

TASK 2

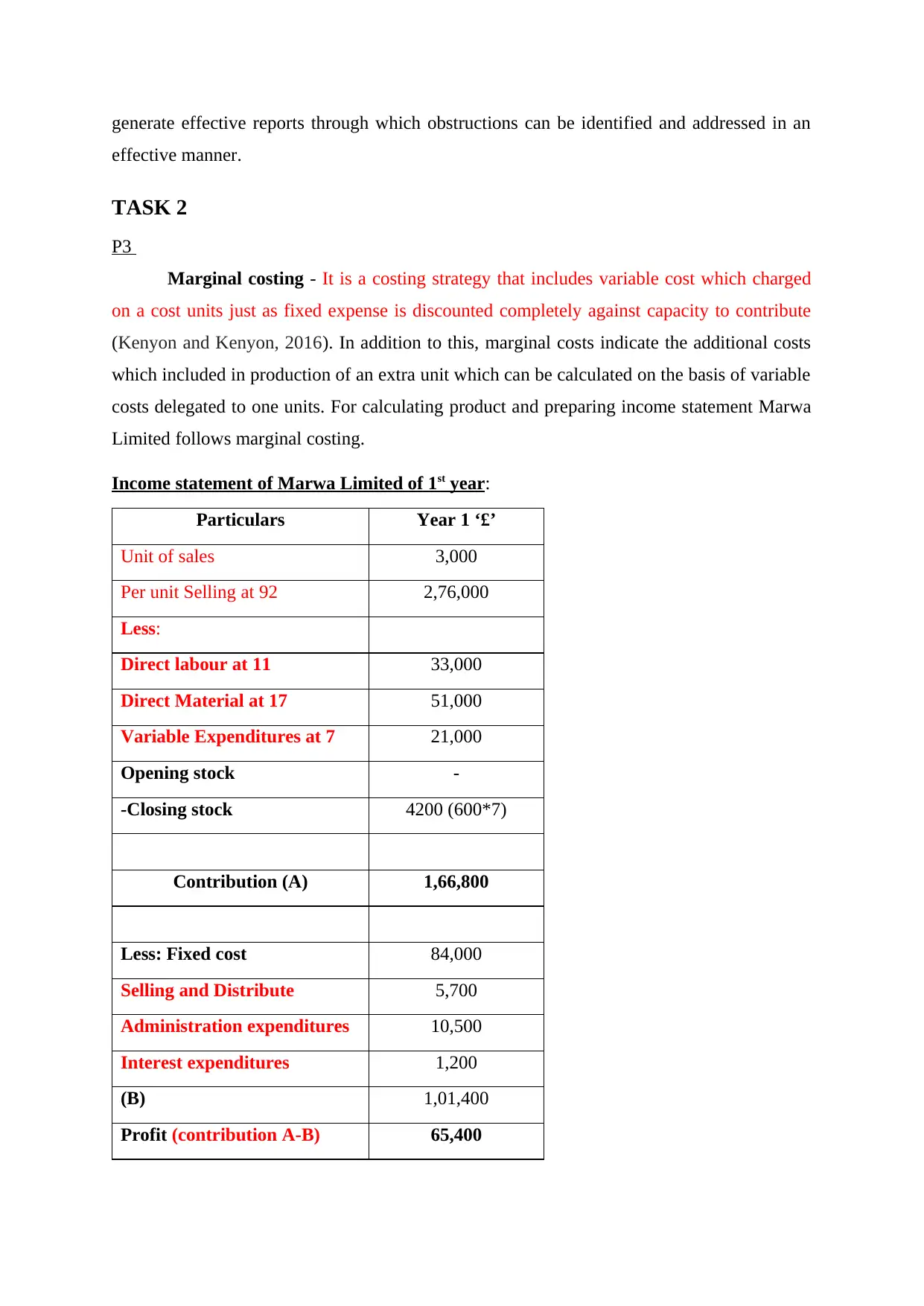

P3

Marginal costing - It is a costing strategy that includes variable cost which charged

on a cost units just as fixed expense is discounted completely against capacity to contribute

(Kenyon and Kenyon, 2016). In addition to this, marginal costs indicate the additional costs

which included in production of an extra unit which can be calculated on the basis of variable

costs delegated to one units. For calculating product and preparing income statement Marwa

Limited follows marginal costing.

Income statement of Marwa Limited of 1st year:

Particulars Year 1 ‘£’

Unit of sales 3,000

Per unit Selling at 92 2,76,000

Less:

Direct labour at 11 33,000

Direct Material at 17 51,000

Variable Expenditures at 7 21,000

Opening stock -

-Closing stock 4200 (600*7)

Contribution (A) 1,66,800

Less: Fixed cost 84,000

Selling and Distribute 5,700

Administration expenditures 10,500

Interest expenditures 1,200

(B) 1,01,400

Profit (contribution A-B) 65,400

effective manner.

TASK 2

P3

Marginal costing - It is a costing strategy that includes variable cost which charged

on a cost units just as fixed expense is discounted completely against capacity to contribute

(Kenyon and Kenyon, 2016). In addition to this, marginal costs indicate the additional costs

which included in production of an extra unit which can be calculated on the basis of variable

costs delegated to one units. For calculating product and preparing income statement Marwa

Limited follows marginal costing.

Income statement of Marwa Limited of 1st year:

Particulars Year 1 ‘£’

Unit of sales 3,000

Per unit Selling at 92 2,76,000

Less:

Direct labour at 11 33,000

Direct Material at 17 51,000

Variable Expenditures at 7 21,000

Opening stock -

-Closing stock 4200 (600*7)

Contribution (A) 1,66,800

Less: Fixed cost 84,000

Selling and Distribute 5,700

Administration expenditures 10,500

Interest expenditures 1,200

(B) 1,01,400

Profit (contribution A-B) 65,400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

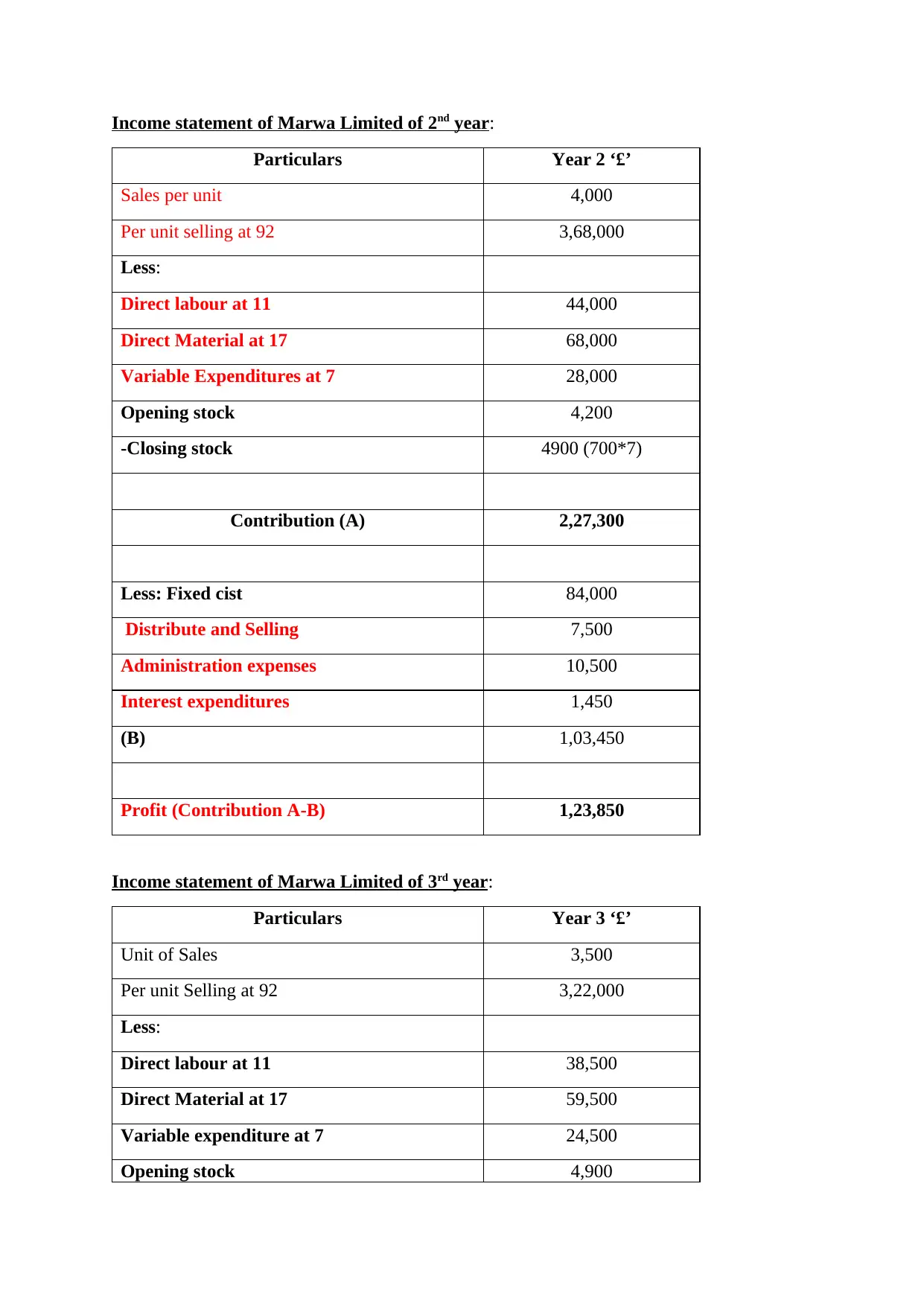

Income statement of Marwa Limited of 2nd year:

Particulars Year 2 ‘£’

Sales per unit 4,000

Per unit selling at 92 3,68,000

Less:

Direct labour at 11 44,000

Direct Material at 17 68,000

Variable Expenditures at 7 28,000

Opening stock 4,200

-Closing stock 4900 (700*7)

Contribution (A) 2,27,300

Less: Fixed cist 84,000

Distribute and Selling 7,500

Administration expenses 10,500

Interest expenditures 1,450

(B) 1,03,450

Profit (Contribution A-B) 1,23,850

Income statement of Marwa Limited of 3rd year:

Particulars Year 3 ‘£’

Unit of Sales 3,500

Per unit Selling at 92 3,22,000

Less:

Direct labour at 11 38,500

Direct Material at 17 59,500

Variable expenditure at 7 24,500

Opening stock 4,900

Particulars Year 2 ‘£’

Sales per unit 4,000

Per unit selling at 92 3,68,000

Less:

Direct labour at 11 44,000

Direct Material at 17 68,000

Variable Expenditures at 7 28,000

Opening stock 4,200

-Closing stock 4900 (700*7)

Contribution (A) 2,27,300

Less: Fixed cist 84,000

Distribute and Selling 7,500

Administration expenses 10,500

Interest expenditures 1,450

(B) 1,03,450

Profit (Contribution A-B) 1,23,850

Income statement of Marwa Limited of 3rd year:

Particulars Year 3 ‘£’

Unit of Sales 3,500

Per unit Selling at 92 3,22,000

Less:

Direct labour at 11 38,500

Direct Material at 17 59,500

Variable expenditure at 7 24,500

Opening stock 4,900

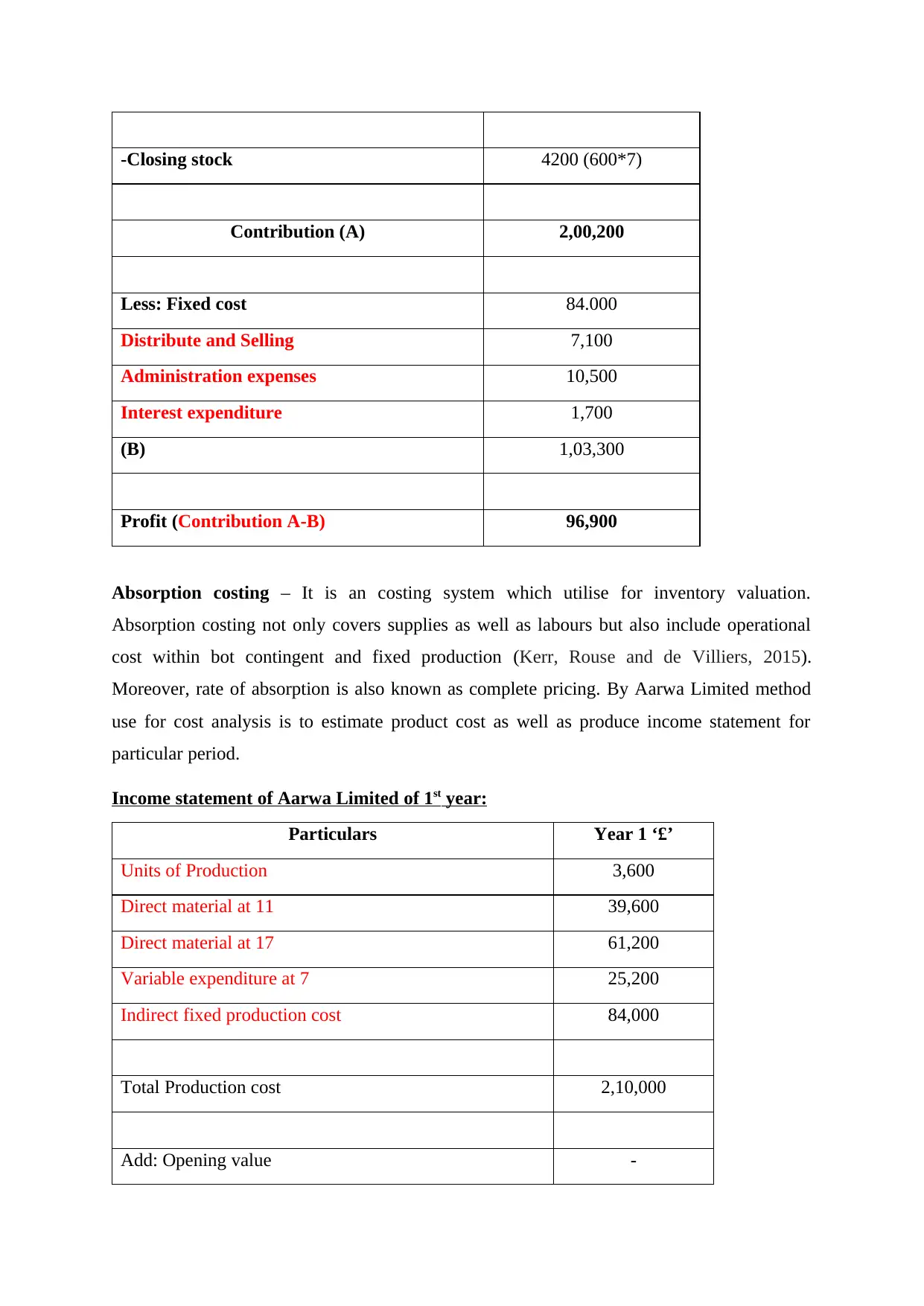

-Closing stock 4200 (600*7)

Contribution (A) 2,00,200

Less: Fixed cost 84.000

Distribute and Selling 7,100

Administration expenses 10,500

Interest expenditure 1,700

(B) 1,03,300

Profit (Contribution A-B) 96,900

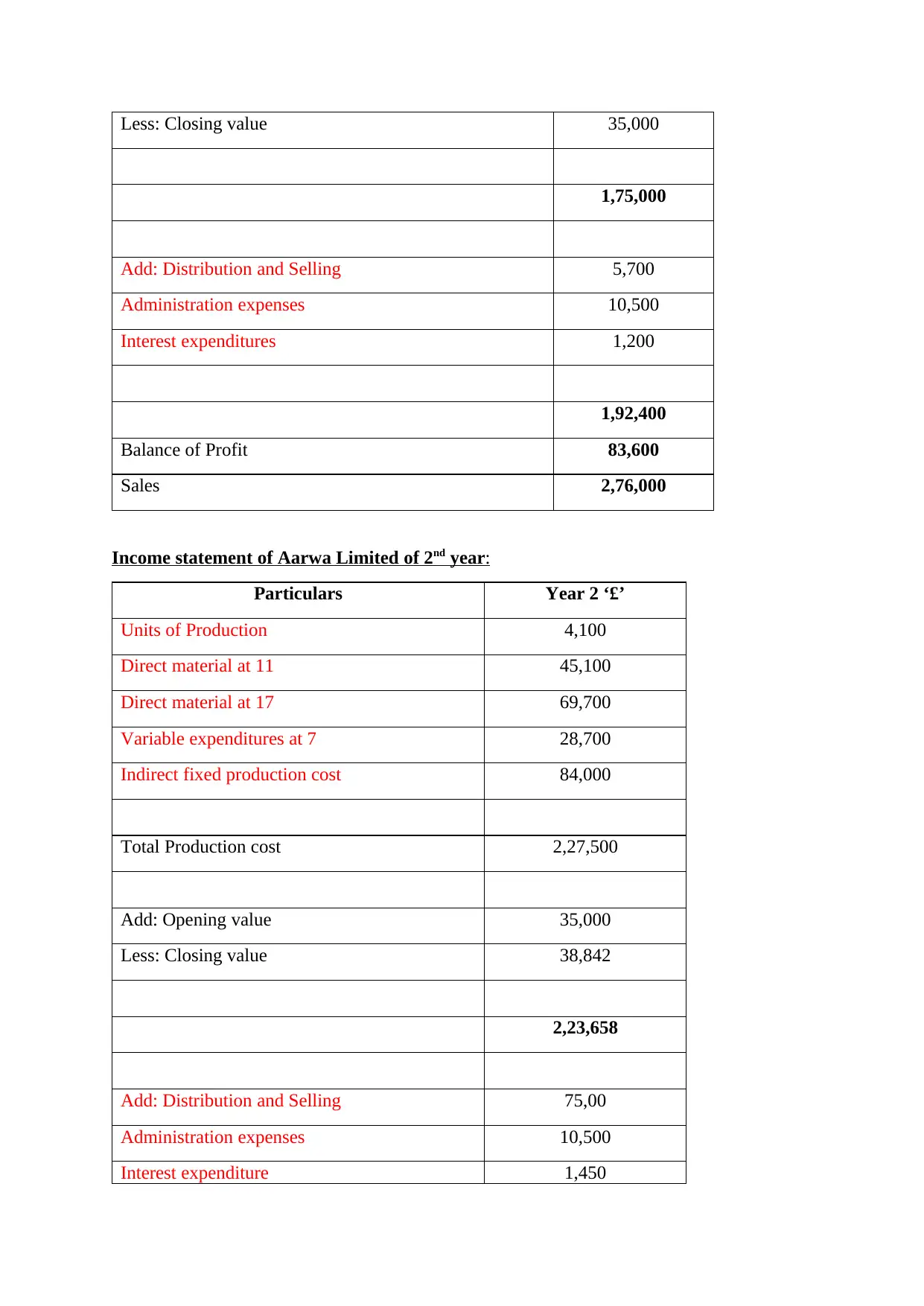

Absorption costing – It is an costing system which utilise for inventory valuation.

Absorption costing not only covers supplies as well as labours but also include operational

cost within bot contingent and fixed production (Kerr, Rouse and de Villiers, 2015).

Moreover, rate of absorption is also known as complete pricing. By Aarwa Limited method

use for cost analysis is to estimate product cost as well as produce income statement for

particular period.

Income statement of Aarwa Limited of 1st year:

Particulars Year 1 ‘£’

Units of Production 3,600

Direct material at 11 39,600

Direct material at 17 61,200

Variable expenditure at 7 25,200

Indirect fixed production cost 84,000

Total Production cost 2,10,000

Add: Opening value -

Contribution (A) 2,00,200

Less: Fixed cost 84.000

Distribute and Selling 7,100

Administration expenses 10,500

Interest expenditure 1,700

(B) 1,03,300

Profit (Contribution A-B) 96,900

Absorption costing – It is an costing system which utilise for inventory valuation.

Absorption costing not only covers supplies as well as labours but also include operational

cost within bot contingent and fixed production (Kerr, Rouse and de Villiers, 2015).

Moreover, rate of absorption is also known as complete pricing. By Aarwa Limited method

use for cost analysis is to estimate product cost as well as produce income statement for

particular period.

Income statement of Aarwa Limited of 1st year:

Particulars Year 1 ‘£’

Units of Production 3,600

Direct material at 11 39,600

Direct material at 17 61,200

Variable expenditure at 7 25,200

Indirect fixed production cost 84,000

Total Production cost 2,10,000

Add: Opening value -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Closing value 35,000

1,75,000

Add: Distribution and Selling 5,700

Administration expenses 10,500

Interest expenditures 1,200

1,92,400

Balance of Profit 83,600

Sales 2,76,000

Income statement of Aarwa Limited of 2nd year:

Particulars Year 2 ‘£’

Units of Production 4,100

Direct material at 11 45,100

Direct material at 17 69,700

Variable expenditures at 7 28,700

Indirect fixed production cost 84,000

Total Production cost 2,27,500

Add: Opening value 35,000

Less: Closing value 38,842

2,23,658

Add: Distribution and Selling 75,00

Administration expenses 10,500

Interest expenditure 1,450

1,75,000

Add: Distribution and Selling 5,700

Administration expenses 10,500

Interest expenditures 1,200

1,92,400

Balance of Profit 83,600

Sales 2,76,000

Income statement of Aarwa Limited of 2nd year:

Particulars Year 2 ‘£’

Units of Production 4,100

Direct material at 11 45,100

Direct material at 17 69,700

Variable expenditures at 7 28,700

Indirect fixed production cost 84,000

Total Production cost 2,27,500

Add: Opening value 35,000

Less: Closing value 38,842

2,23,658

Add: Distribution and Selling 75,00

Administration expenses 10,500

Interest expenditure 1,450

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

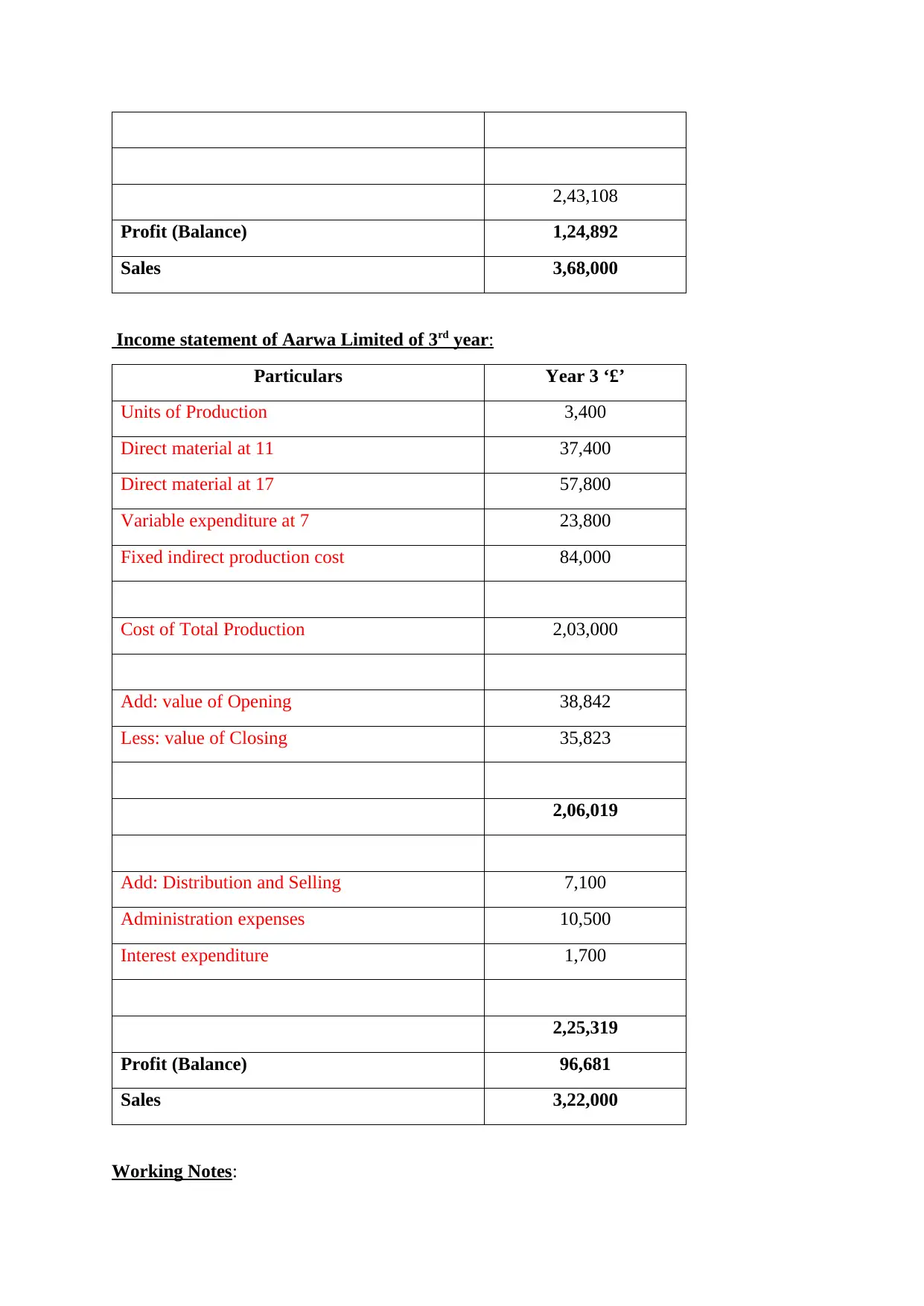

2,43,108

Profit (Balance) 1,24,892

Sales 3,68,000

Income statement of Aarwa Limited of 3rd year:

Particulars Year 3 ‘£’

Units of Production 3,400

Direct material at 11 37,400

Direct material at 17 57,800

Variable expenditure at 7 23,800

Fixed indirect production cost 84,000

Cost of Total Production 2,03,000

Add: value of Opening 38,842

Less: value of Closing 35,823

2,06,019

Add: Distribution and Selling 7,100

Administration expenses 10,500

Interest expenditure 1,700

2,25,319

Profit (Balance) 96,681

Sales 3,22,000

Working Notes:

Profit (Balance) 1,24,892

Sales 3,68,000

Income statement of Aarwa Limited of 3rd year:

Particulars Year 3 ‘£’

Units of Production 3,400

Direct material at 11 37,400

Direct material at 17 57,800

Variable expenditure at 7 23,800

Fixed indirect production cost 84,000

Cost of Total Production 2,03,000

Add: value of Opening 38,842

Less: value of Closing 35,823

2,06,019

Add: Distribution and Selling 7,100

Administration expenses 10,500

Interest expenditure 1,700

2,25,319

Profit (Balance) 96,681

Sales 3,22,000

Working Notes:

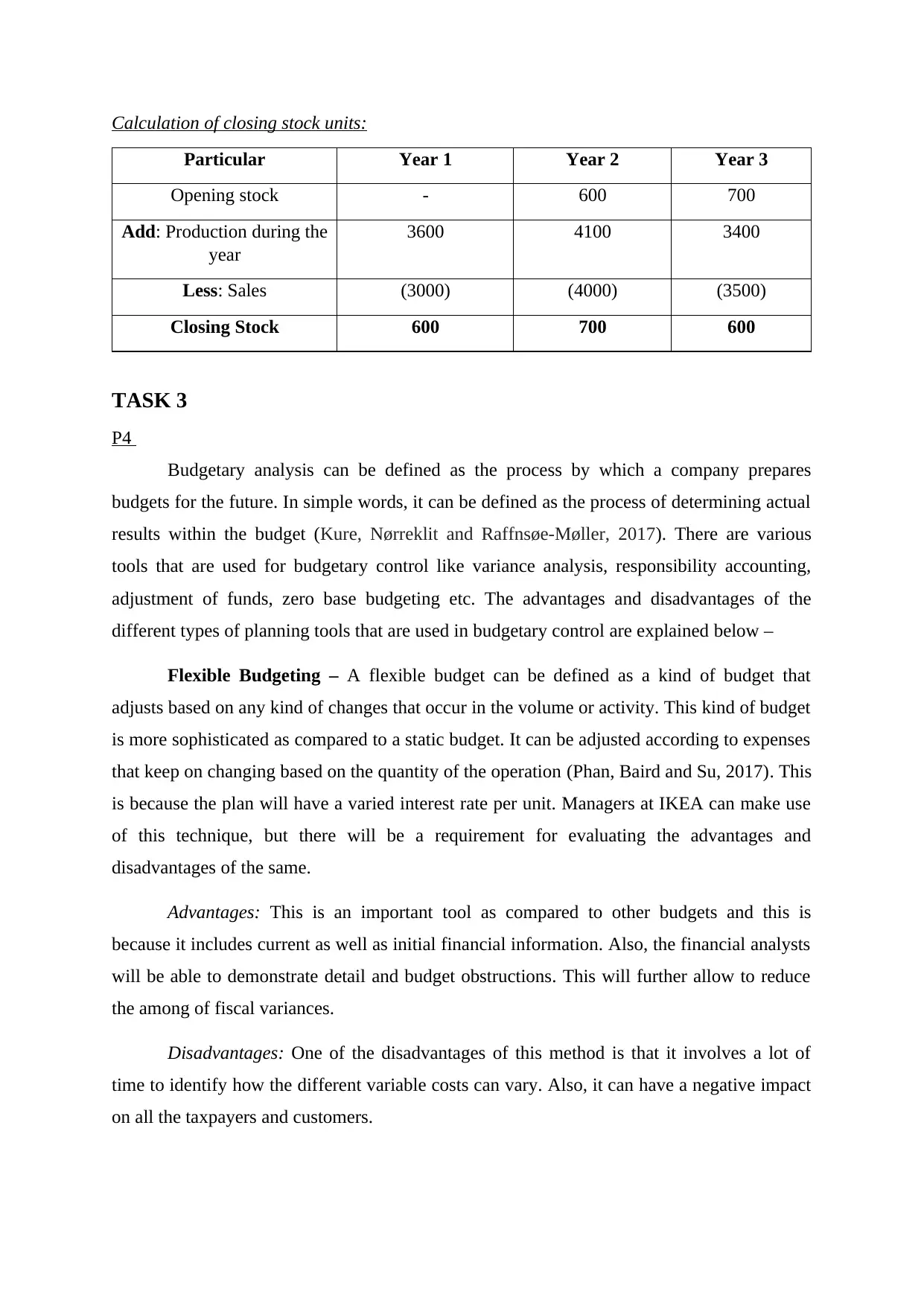

Calculation of closing stock units:

Particular Year 1 Year 2 Year 3

Opening stock - 600 700

Add: Production during the

year

3600 4100 3400

Less: Sales (3000) (4000) (3500)

Closing Stock 600 700 600

TASK 3

P4

Budgetary analysis can be defined as the process by which a company prepares

budgets for the future. In simple words, it can be defined as the process of determining actual

results within the budget (Kure, Nørreklit and Raffnsøe-Møller, 2017). There are various

tools that are used for budgetary control like variance analysis, responsibility accounting,

adjustment of funds, zero base budgeting etc. The advantages and disadvantages of the

different types of planning tools that are used in budgetary control are explained below –

Flexible Budgeting – A flexible budget can be defined as a kind of budget that

adjusts based on any kind of changes that occur in the volume or activity. This kind of budget

is more sophisticated as compared to a static budget. It can be adjusted according to expenses

that keep on changing based on the quantity of the operation (Phan, Baird and Su, 2017). This

is because the plan will have a varied interest rate per unit. Managers at IKEA can make use

of this technique, but there will be a requirement for evaluating the advantages and

disadvantages of the same.

Advantages: This is an important tool as compared to other budgets and this is

because it includes current as well as initial financial information. Also, the financial analysts

will be able to demonstrate detail and budget obstructions. This will further allow to reduce

the among of fiscal variances.

Disadvantages: One of the disadvantages of this method is that it involves a lot of

time to identify how the different variable costs can vary. Also, it can have a negative impact

on all the taxpayers and customers.

Particular Year 1 Year 2 Year 3

Opening stock - 600 700

Add: Production during the

year

3600 4100 3400

Less: Sales (3000) (4000) (3500)

Closing Stock 600 700 600

TASK 3

P4

Budgetary analysis can be defined as the process by which a company prepares

budgets for the future. In simple words, it can be defined as the process of determining actual

results within the budget (Kure, Nørreklit and Raffnsøe-Møller, 2017). There are various

tools that are used for budgetary control like variance analysis, responsibility accounting,

adjustment of funds, zero base budgeting etc. The advantages and disadvantages of the

different types of planning tools that are used in budgetary control are explained below –

Flexible Budgeting – A flexible budget can be defined as a kind of budget that

adjusts based on any kind of changes that occur in the volume or activity. This kind of budget

is more sophisticated as compared to a static budget. It can be adjusted according to expenses

that keep on changing based on the quantity of the operation (Phan, Baird and Su, 2017). This

is because the plan will have a varied interest rate per unit. Managers at IKEA can make use

of this technique, but there will be a requirement for evaluating the advantages and

disadvantages of the same.

Advantages: This is an important tool as compared to other budgets and this is

because it includes current as well as initial financial information. Also, the financial analysts

will be able to demonstrate detail and budget obstructions. This will further allow to reduce

the among of fiscal variances.

Disadvantages: One of the disadvantages of this method is that it involves a lot of

time to identify how the different variable costs can vary. Also, it can have a negative impact

on all the taxpayers and customers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.