Management Accounting Systems: Analysis of IKEA's Financial Reports

VerifiedAdded on 2023/01/11

|21

|4970

|60

Report

AI Summary

This report provides an analysis of management accounting practices within IKEA, a multinational furniture company. It explains management accounting principles and evaluates essential requirements of different management accounting systems such as inventory management, cost accounting, and price optimization. The report also explores various reporting methods used in management accounting, including budget reports, inventory management reports, and accounts receivable aging reports. Furthermore, it evaluates the benefits and applications of these systems in enhancing IKEA's operational efficiency and strategic decision-making. The report also touches on how modern organizations adapt management accounting systems to address their financial issues.

Accounting (Unit 5)

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

INTRODUCTION

Management accounting is a profession requiring engaging with decision-making processes,

developing performance measurement and management programs, and offering financial

analysis and tracking services to assist management in formulating and implementing the

strategy of the organisation (Arnaboldi, Lapsley and Steccolini, 2015). To assist managers'

decision making process in achieving business goals, company follow several management

accounting concepts. It is the process of evaluating business costs and operations to prepare

internal financial report, records, and account. This report is based on IKEA which is a Swedish

origin multinational group, headquartered in the Netherlands, established in 1943, designing and

selling fully prepared-to-assemble furniture. It includes kitchen appliances, home accessories,

including goods and products and every so often home services.

This assessment covers topics such as management accounting, essential requirement of

management accounting systems and reporting documents. The report include the analysis of the

implementation of different planning tools to prepare budgets; as well as an assessment about

how these planning tools and accounting systems have been used to quantify the problem. In

addition, it includes at least 2 examples to start comparing how modern world organisations are

adapting management accounting systems to response their financial issues.

MAIN BODY

P1. Explain management accounting and evaluate the essential requirement if different types of

management accounting systems

Management accounting looking at the activities that arise in or around a company while

keeping the client needs into consideration. From that it emerges details and forecasts.

Management accounting is the process by which these estimates and data are translated into

understanding which will inevitably have been used to facilitate decision - making. Internal or

external focus is the key difference among financial and managerial accounting (Cooper, 2017).

Financial management, for creditors and taxpayers, relies on producing and reviewing annual

statements that must be published publicly.

By comparison, management accounting analysis techniques and findings are held by-

house for use by corporate owners to guide decision-making and more efficiently run the

organization. Management accountants handle countless facets of accounting. Those include

3

Management accounting is a profession requiring engaging with decision-making processes,

developing performance measurement and management programs, and offering financial

analysis and tracking services to assist management in formulating and implementing the

strategy of the organisation (Arnaboldi, Lapsley and Steccolini, 2015). To assist managers'

decision making process in achieving business goals, company follow several management

accounting concepts. It is the process of evaluating business costs and operations to prepare

internal financial report, records, and account. This report is based on IKEA which is a Swedish

origin multinational group, headquartered in the Netherlands, established in 1943, designing and

selling fully prepared-to-assemble furniture. It includes kitchen appliances, home accessories,

including goods and products and every so often home services.

This assessment covers topics such as management accounting, essential requirement of

management accounting systems and reporting documents. The report include the analysis of the

implementation of different planning tools to prepare budgets; as well as an assessment about

how these planning tools and accounting systems have been used to quantify the problem. In

addition, it includes at least 2 examples to start comparing how modern world organisations are

adapting management accounting systems to response their financial issues.

MAIN BODY

P1. Explain management accounting and evaluate the essential requirement if different types of

management accounting systems

Management accounting looking at the activities that arise in or around a company while

keeping the client needs into consideration. From that it emerges details and forecasts.

Management accounting is the process by which these estimates and data are translated into

understanding which will inevitably have been used to facilitate decision - making. Internal or

external focus is the key difference among financial and managerial accounting (Cooper, 2017).

Financial management, for creditors and taxpayers, relies on producing and reviewing annual

statements that must be published publicly.

By comparison, management accounting analysis techniques and findings are held by-

house for use by corporate owners to guide decision-making and more efficiently run the

organization. Management accountants handle countless facets of accounting. Those include

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

margins, restrictions, budgeting of money, patterns and predictions, pricing and costing of the

goods. Manager of IKEA Company follows the management accounting functions to improve

their operational efficiency as well as maximise its Output.

Roles of management accounting:

The role of the accountant is to carry out a set of activities to maintain financial stability

for the client, overseeing effectively all business affairs and thereby helping to push the daily

operations and strategy of the firm. Management Accountants are crucial players in assessing a

company's reputation and performance. Many have to become a Certified Management

Accountant (CMA), a certification comparable to CPA, but with a greater emphasis on the issues

of cost accounting, financial development and scheduling. Another role of management

accountant is to gather information regarding ongoing cost and revenue of the company. All the

transduction needs to be recorded in a double entry book keeping system. Calculate cost of each

product for the valuation purpose of stock, cost contrail and make strategic decisions.

Difference between MA and FA:

Management accounting Financial accounting

It helps the managers to make essential

decisions, policies or strategies to improve

their operational performance.

In this accounting, main focus of accountant is

to prepare financial statements which required

analysing by the interested parties.

In this management accounting, monetary or

non-monetary information required to build

strategies.

It contains only monetary information in order

to prepare financial statement.

It is prepared as per the company’s

requirement or need.

It is prepared yearly or quarterly as per the

accounting period.

Essential requirement of management accounting systems:

Inventory management system: It is an instrument enabling organizations to track

goods across the supply chain of their business. It optimizes the full continuum from placing of

orders with the distributor to order fulfilment to their client, modeling a manufacturer's entire

path. Accountability provided by this software and has a big effect on a company's bottom line.

Businesses can reduce duplication by precise monitoring of products, identify patterns and make

smarter investment decisions (Inventory Management System, 2020). Manager of IKEA

4

goods. Manager of IKEA Company follows the management accounting functions to improve

their operational efficiency as well as maximise its Output.

Roles of management accounting:

The role of the accountant is to carry out a set of activities to maintain financial stability

for the client, overseeing effectively all business affairs and thereby helping to push the daily

operations and strategy of the firm. Management Accountants are crucial players in assessing a

company's reputation and performance. Many have to become a Certified Management

Accountant (CMA), a certification comparable to CPA, but with a greater emphasis on the issues

of cost accounting, financial development and scheduling. Another role of management

accountant is to gather information regarding ongoing cost and revenue of the company. All the

transduction needs to be recorded in a double entry book keeping system. Calculate cost of each

product for the valuation purpose of stock, cost contrail and make strategic decisions.

Difference between MA and FA:

Management accounting Financial accounting

It helps the managers to make essential

decisions, policies or strategies to improve

their operational performance.

In this accounting, main focus of accountant is

to prepare financial statements which required

analysing by the interested parties.

In this management accounting, monetary or

non-monetary information required to build

strategies.

It contains only monetary information in order

to prepare financial statement.

It is prepared as per the company’s

requirement or need.

It is prepared yearly or quarterly as per the

accounting period.

Essential requirement of management accounting systems:

Inventory management system: It is an instrument enabling organizations to track

goods across the supply chain of their business. It optimizes the full continuum from placing of

orders with the distributor to order fulfilment to their client, modeling a manufacturer's entire

path. Accountability provided by this software and has a big effect on a company's bottom line.

Businesses can reduce duplication by precise monitoring of products, identify patterns and make

smarter investment decisions (Inventory Management System, 2020). Manager of IKEA

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

implement this system in their organization to track their daily basis availability of stock in

warehouses. It is essentially required to manufacture furniture accordingly or further order

inventory as per the production requirement. Due to this reason, inventory management system is

essentially required in this organization and it also helps in tracking inventory level or provides

transparency. Further manager is able to build effective strategy in context of the organization to

run their business operations in well manner.

Economic Order Quantity: This is the number of items which a business can add from

each order to the inventory to reduce net production costs such as storage costs, shipment

costs, and scarcity costs.

Just In Time: This is a technique to improve productivity and reduce inventory just by

receiving products when they are required in the manufacturing cycle, thereby reducing

the expense of inventories.

LIFO: LIFO is a method of inventory control in which the last purchased commodity or

item is used first and thus the in-house stock consists of the latest supply.

FIFO: FIFO is yet another inventory control method where the first received item is

consumed initially, i.e. the problem of goods is made from either the earliest lot and the

purchase in hand comprises the newest lot.

Cost accounting system: Manufacturers are using this system to maintain record

of production activities using a constant system of inventories. In many other words, it's an

accounting system which is designed for manufacturing companies that constantly tracks the

inventory flow through the different production stages and evaluates the cost of each unit at

different stages (Fleischman and Parker, 2017). It is critical for profitable activities to determine

the exact cost of goods. A manager of IKEA needs to know which product lines are profitable

and which ones are not, but that can only be concluded when it has forecasted the appropriate

product cost. Cost accounting system is essential to measure the closure value of the inventory of

products, work-in - progress and stock of finished items for planning of financial statements. In

addition, managers of IKEA are able to build strategies to minimise or control the cost

throughout the production period. It includes some elements which are as follow:

In order to measure the value of inputs, managers can use several methods such as

historical vs standard costing, direct & indirect costing, variable, overheads etc.

5

warehouses. It is essentially required to manufacture furniture accordingly or further order

inventory as per the production requirement. Due to this reason, inventory management system is

essentially required in this organization and it also helps in tracking inventory level or provides

transparency. Further manager is able to build effective strategy in context of the organization to

run their business operations in well manner.

Economic Order Quantity: This is the number of items which a business can add from

each order to the inventory to reduce net production costs such as storage costs, shipment

costs, and scarcity costs.

Just In Time: This is a technique to improve productivity and reduce inventory just by

receiving products when they are required in the manufacturing cycle, thereby reducing

the expense of inventories.

LIFO: LIFO is a method of inventory control in which the last purchased commodity or

item is used first and thus the in-house stock consists of the latest supply.

FIFO: FIFO is yet another inventory control method where the first received item is

consumed initially, i.e. the problem of goods is made from either the earliest lot and the

purchase in hand comprises the newest lot.

Cost accounting system: Manufacturers are using this system to maintain record

of production activities using a constant system of inventories. In many other words, it's an

accounting system which is designed for manufacturing companies that constantly tracks the

inventory flow through the different production stages and evaluates the cost of each unit at

different stages (Fleischman and Parker, 2017). It is critical for profitable activities to determine

the exact cost of goods. A manager of IKEA needs to know which product lines are profitable

and which ones are not, but that can only be concluded when it has forecasted the appropriate

product cost. Cost accounting system is essential to measure the closure value of the inventory of

products, work-in - progress and stock of finished items for planning of financial statements. In

addition, managers of IKEA are able to build strategies to minimise or control the cost

throughout the production period. It includes some elements which are as follow:

In order to measure the value of inputs, managers can use several methods such as

historical vs standard costing, direct & indirect costing, variable, overheads etc.

5

For the valuation of inventory, managers need to adopt marginal or absorption costing

methods.

This system also required to follow cost accumulation methods in order to identify

specific cost and further evaluate the particulate consumer, jobs, department, process,

batches order etc.

For the assumption of cost, managers can use the several inventory management methods

such as FIFO, LIFO or AVCO.

Inventory cost flow should be measured on two intervals such as perpetual or periodic

basis.

Price optimization system: It is used by the company after becoming aware of how

responsive its existing customers are to product price fluctuations. It might well come into how

much companies can achieve within defined performance and profitability. Optimum pricing is

essential if a IKEA wants to connect its sales revenue to profits and more crucially, if it aims to

expand profits by maintaining the same levels of client retention. Price optimization is becoming

more and more essential because sales of individual business lines are becoming highly

competitive (Gray, 2015). There are also several companies looking to introduce new products,

including some in niche market segments. In this sense, it is even more essential to have the right

price or a business may waste significant customer base to its rivals. This accounting system

helps the managers to colleting historical data which further support in decision making process.

It includes the quantity of product along with price and its promotional strategy also considered

while taking decisions regarding product price. Managers of IKEA also compare the

competitor’s product price, their marketing strategy etc. In addition, they need to consider

economic conditions, availability of predicts in the market, fixed and variable cost details etc.

Above discussed accounting systems are essentially required by the managers of IKEA

Furniture Company. With the help of effective implementation, organization is able to run their

operational activities in well manner or achieve business goals & objectives.

P2. Explain different methods which are used for reporting purpose in management accounting

Management Accounting reports are a critical part of ensuring users to get a full view of

how the business is doing. Each quarter should give a short accounting report to offer a holistic

view of the finances of their business. Such reports publish financial information from financial

statements which can include data such as money transfers, operating costs, profit margins of the

6

methods.

This system also required to follow cost accumulation methods in order to identify

specific cost and further evaluate the particulate consumer, jobs, department, process,

batches order etc.

For the assumption of cost, managers can use the several inventory management methods

such as FIFO, LIFO or AVCO.

Inventory cost flow should be measured on two intervals such as perpetual or periodic

basis.

Price optimization system: It is used by the company after becoming aware of how

responsive its existing customers are to product price fluctuations. It might well come into how

much companies can achieve within defined performance and profitability. Optimum pricing is

essential if a IKEA wants to connect its sales revenue to profits and more crucially, if it aims to

expand profits by maintaining the same levels of client retention. Price optimization is becoming

more and more essential because sales of individual business lines are becoming highly

competitive (Gray, 2015). There are also several companies looking to introduce new products,

including some in niche market segments. In this sense, it is even more essential to have the right

price or a business may waste significant customer base to its rivals. This accounting system

helps the managers to colleting historical data which further support in decision making process.

It includes the quantity of product along with price and its promotional strategy also considered

while taking decisions regarding product price. Managers of IKEA also compare the

competitor’s product price, their marketing strategy etc. In addition, they need to consider

economic conditions, availability of predicts in the market, fixed and variable cost details etc.

Above discussed accounting systems are essentially required by the managers of IKEA

Furniture Company. With the help of effective implementation, organization is able to run their

operational activities in well manner or achieve business goals & objectives.

P2. Explain different methods which are used for reporting purpose in management accounting

Management Accounting reports are a critical part of ensuring users to get a full view of

how the business is doing. Each quarter should give a short accounting report to offer a holistic

view of the finances of their business. Such reports publish financial information from financial

statements which can include data such as money transfers, operating costs, profit margins of the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

item and regional sales (Management Accounting Reports, 2020). Such reports are intended to

enable managers of IKEA to make better decisions. As companies rely on support from strategic

accounting, they can more effectively obtain information that lets management direct the

company towards achieving its targets. Different methods of reporting are as follow:

Budget report: The most basic report in financial reporting is the budget report. It helps

businesses to understand and reduce costs throughout the company, whether it's a cohesive

organization or has many departments in it (Brustbauer, 2016). It becomes possible to determine

budgets for the preceding year by evaluating expenditures in previous years, and to find things to

cut costs. Manager of IKEA build this report for effective implementation of business strategy

where they estimate the overall product cost and further profit which can be generated through

selling predicted volume. In addition, overall expenses rather than manufacturing goods also

included for the estimation and it help the managers to formulate strategic decisions to achieve

business goals & objectives.

Inventory management report: Companies producing physical products, particularly

those of us with a low fault tolerance in manufacturing, find such reports are very valuable

(Gullberg, 2016). Those who authentic situations data on the cost of inventories, labour and other

structures of administrative costs involved in the production process, supplying raw data for

optimizing installation or machining. This report followed by the IKEA Company and it includes

the information related to inventory such as labour cost, carrying cost, ordering cost and other

expenses. Managers of IKEA use this report to record the information which is valuable for

management to build strategies.

Accounts Receivable Aging Report: This section of the report is important to any

organization that offers mortgage lending. It gives an overview of the age-specific credit

balances, usually which include distinct classes for items 30, 60 and 90 day late. It might help to

modify payment terms to integrate them with both the payment capacities of consumers.

Manager of IKEA use this report to identify their defaulters on the basis of different time period.

In order to minimise the number of defaulters list, manager should build such strict credit

policies to reduce their debt.

M1. Evaluate the benefits of management accounting systems and its applications

In an organizational context, management accounting systems are very essential and it

provides several benefits at the time of implementing such accounting systems in IKEA

7

enable managers of IKEA to make better decisions. As companies rely on support from strategic

accounting, they can more effectively obtain information that lets management direct the

company towards achieving its targets. Different methods of reporting are as follow:

Budget report: The most basic report in financial reporting is the budget report. It helps

businesses to understand and reduce costs throughout the company, whether it's a cohesive

organization or has many departments in it (Brustbauer, 2016). It becomes possible to determine

budgets for the preceding year by evaluating expenditures in previous years, and to find things to

cut costs. Manager of IKEA build this report for effective implementation of business strategy

where they estimate the overall product cost and further profit which can be generated through

selling predicted volume. In addition, overall expenses rather than manufacturing goods also

included for the estimation and it help the managers to formulate strategic decisions to achieve

business goals & objectives.

Inventory management report: Companies producing physical products, particularly

those of us with a low fault tolerance in manufacturing, find such reports are very valuable

(Gullberg, 2016). Those who authentic situations data on the cost of inventories, labour and other

structures of administrative costs involved in the production process, supplying raw data for

optimizing installation or machining. This report followed by the IKEA Company and it includes

the information related to inventory such as labour cost, carrying cost, ordering cost and other

expenses. Managers of IKEA use this report to record the information which is valuable for

management to build strategies.

Accounts Receivable Aging Report: This section of the report is important to any

organization that offers mortgage lending. It gives an overview of the age-specific credit

balances, usually which include distinct classes for items 30, 60 and 90 day late. It might help to

modify payment terms to integrate them with both the payment capacities of consumers.

Manager of IKEA use this report to identify their defaulters on the basis of different time period.

In order to minimise the number of defaulters list, manager should build such strict credit

policies to reduce their debt.

M1. Evaluate the benefits of management accounting systems and its applications

In an organizational context, management accounting systems are very essential and it

provides several benefits at the time of implementing such accounting systems in IKEA

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Company. By using inventory management system, manager of IKEA can manage the entire

stock level which minimise the risk of overselling, beneficial to save cost or simplify the process.

Cost management accounting helps the managers of IKEA to evaluate each product cost which

further beneficial in reducing overall cost of production and make sure to control the cost over

the period (Harrison and Lock, 2017). On the other hand, price optimization system helps the

management to set price of their products as per the business objectives and make sure that it

will meet the customer’s expectation as well. These accounting systems help the organization to

run their operational activities as well as make sure that it will maximise the overall efficiency as

well as effectiveness. It further maximise productivity as well as performance which provide

organizational success.

D1. Critically evaluated that how accounting systems or reporting linked with organizational

process

Management accounting systems and accounting reports are very essential for the

organization to implement for the completion of their task. It has been critically evaluated that,

cost accounting system help the manager to estimate product cost which further recorded in the

costing report and from that document, manager use this information at the time of developing

strategies which helps in successful implementation of organizational process. In addition,

inventory management system used to track the inventory level and further this information

recorded in the inventory management report for the further analysis. It is evaluated that,

accounting reports and systems are linked with each other. It further helps the manager of IKEA

in decision making process to run operational process in well manner to achieve business goals

& objectives.

P3. Calculate cost by using suitable techniques of cost analysis to prepare income statement

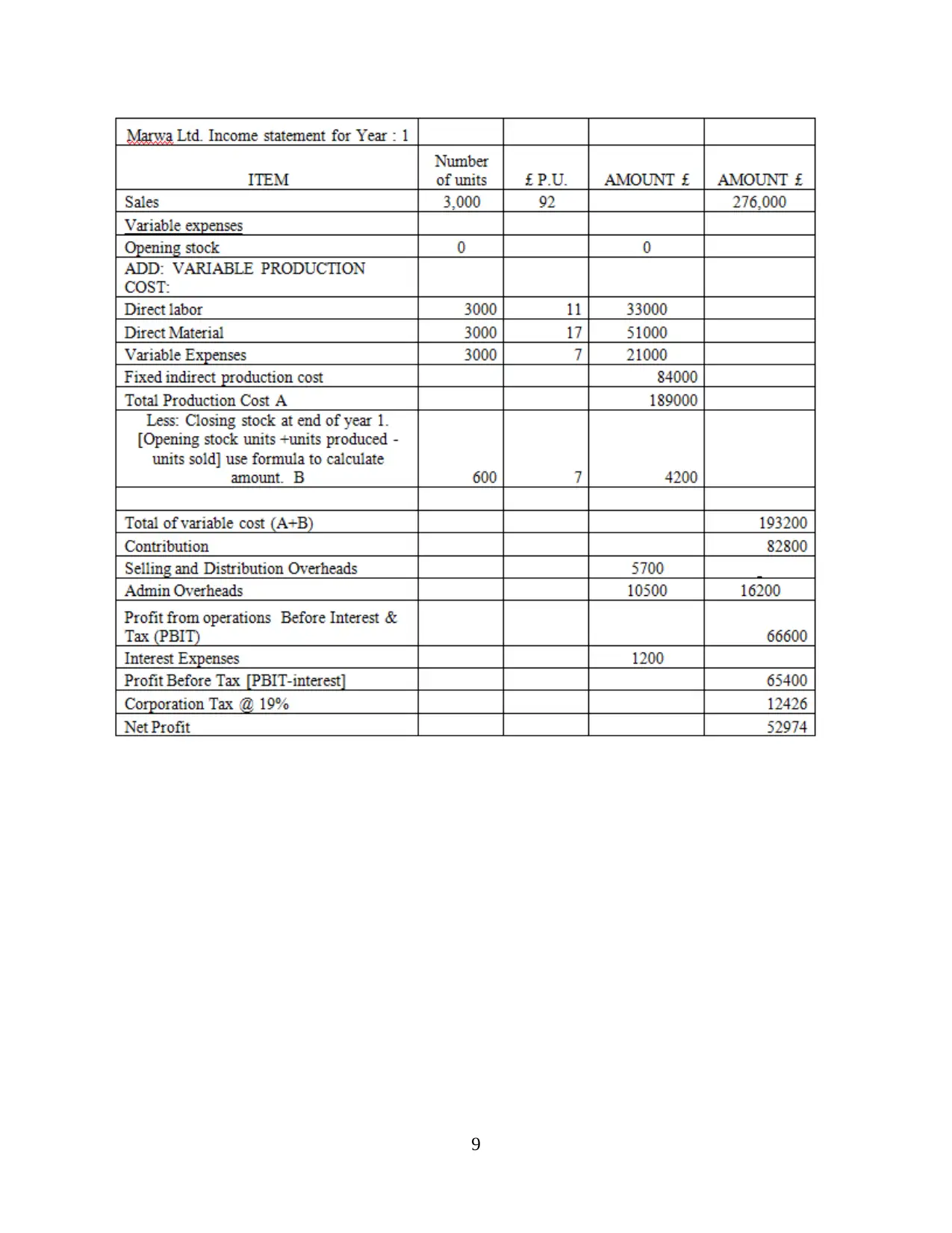

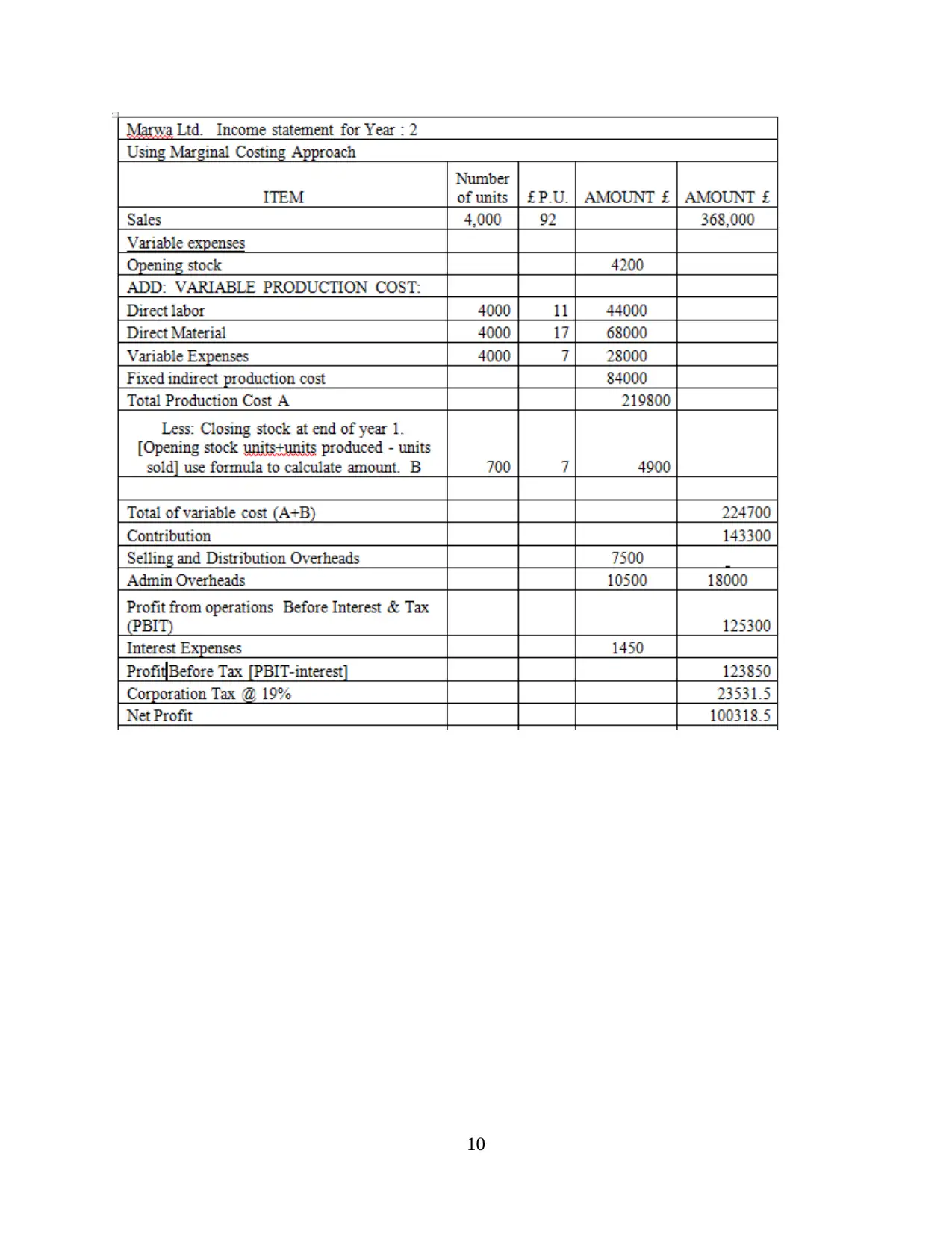

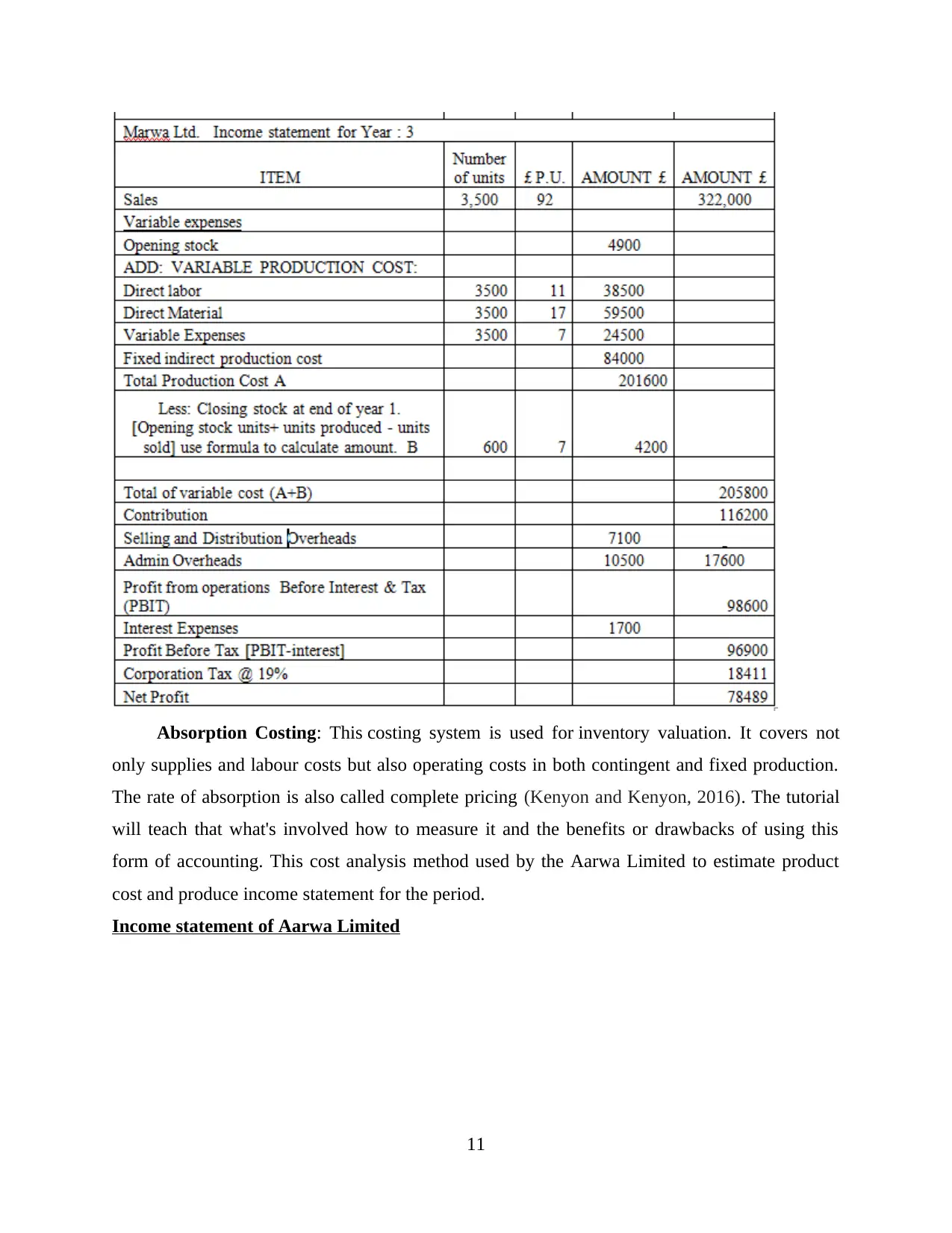

Marginal Costing: It is a costing method in which the marginal cost includes variable cost

that charged to cost units, whereas the fixed cost is written off entirely against ability to

contribute (Hoque, Parker, Covaleski and Haynes, 2017). The word marginal cost indicates the

additional costs involved in making an extra output unit that can be calculated on the basis of the

variable costs delegated to one unit. Marwa Limited follows the marginal costing method to

calculate the product cost or prepare income statement.

Income statement of Marwa Limited

8

stock level which minimise the risk of overselling, beneficial to save cost or simplify the process.

Cost management accounting helps the managers of IKEA to evaluate each product cost which

further beneficial in reducing overall cost of production and make sure to control the cost over

the period (Harrison and Lock, 2017). On the other hand, price optimization system helps the

management to set price of their products as per the business objectives and make sure that it

will meet the customer’s expectation as well. These accounting systems help the organization to

run their operational activities as well as make sure that it will maximise the overall efficiency as

well as effectiveness. It further maximise productivity as well as performance which provide

organizational success.

D1. Critically evaluated that how accounting systems or reporting linked with organizational

process

Management accounting systems and accounting reports are very essential for the

organization to implement for the completion of their task. It has been critically evaluated that,

cost accounting system help the manager to estimate product cost which further recorded in the

costing report and from that document, manager use this information at the time of developing

strategies which helps in successful implementation of organizational process. In addition,

inventory management system used to track the inventory level and further this information

recorded in the inventory management report for the further analysis. It is evaluated that,

accounting reports and systems are linked with each other. It further helps the manager of IKEA

in decision making process to run operational process in well manner to achieve business goals

& objectives.

P3. Calculate cost by using suitable techniques of cost analysis to prepare income statement

Marginal Costing: It is a costing method in which the marginal cost includes variable cost

that charged to cost units, whereas the fixed cost is written off entirely against ability to

contribute (Hoque, Parker, Covaleski and Haynes, 2017). The word marginal cost indicates the

additional costs involved in making an extra output unit that can be calculated on the basis of the

variable costs delegated to one unit. Marwa Limited follows the marginal costing method to

calculate the product cost or prepare income statement.

Income statement of Marwa Limited

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

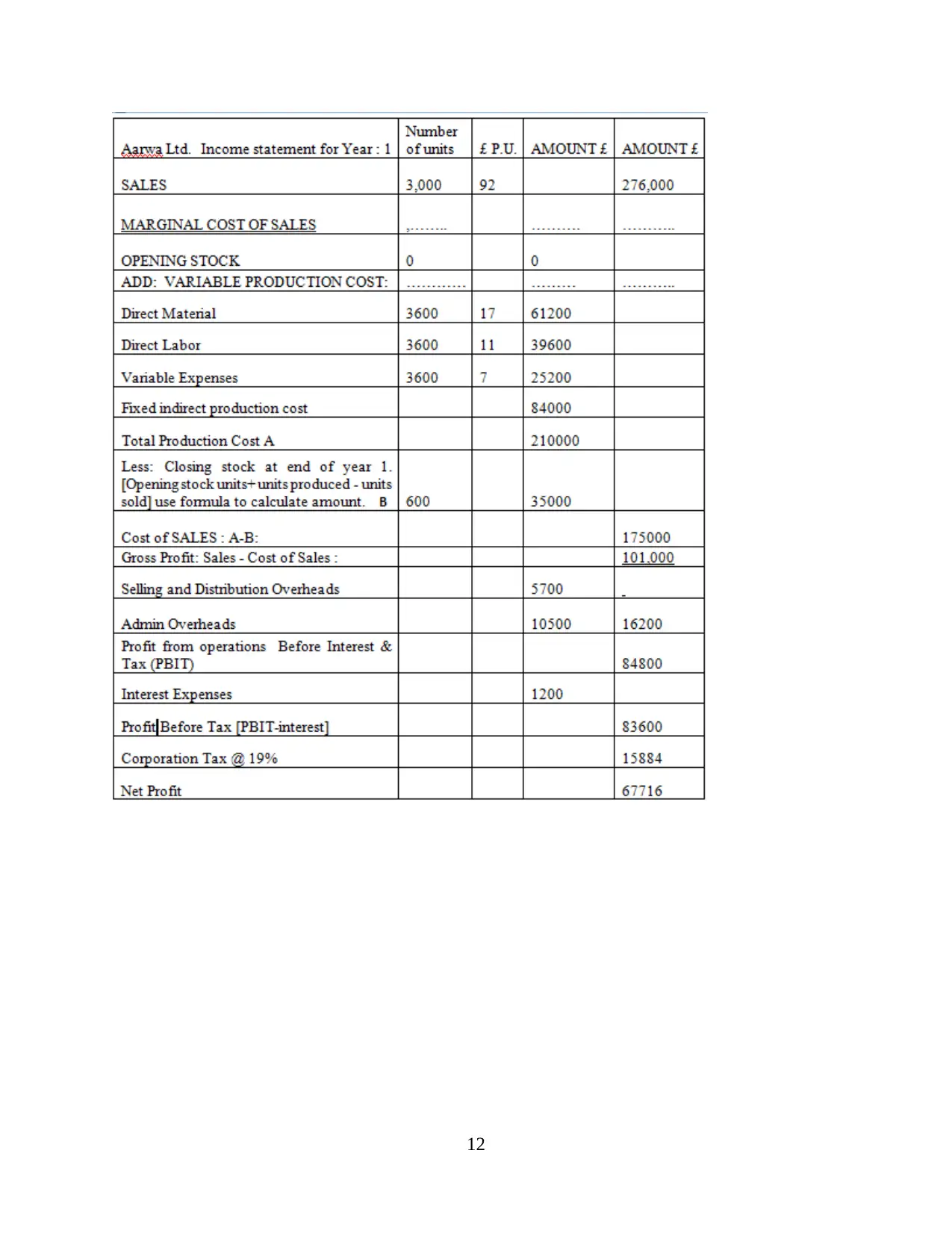

Absorption Costing: This costing system is used for inventory valuation. It covers not

only supplies and labour costs but also operating costs in both contingent and fixed production.

The rate of absorption is also called complete pricing (Kenyon and Kenyon, 2016). The tutorial

will teach that what's involved how to measure it and the benefits or drawbacks of using this

form of accounting. This cost analysis method used by the Aarwa Limited to estimate product

cost and produce income statement for the period.

Income statement of Aarwa Limited

11

only supplies and labour costs but also operating costs in both contingent and fixed production.

The rate of absorption is also called complete pricing (Kenyon and Kenyon, 2016). The tutorial

will teach that what's involved how to measure it and the benefits or drawbacks of using this

form of accounting. This cost analysis method used by the Aarwa Limited to estimate product

cost and produce income statement for the period.

Income statement of Aarwa Limited

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.